ACC200: Job Order Costing, Turramurra Furniture Co. - WIP & Overhead

VerifiedAdded on 2024/04/26

|12

|1529

|440

Report

AI Summary

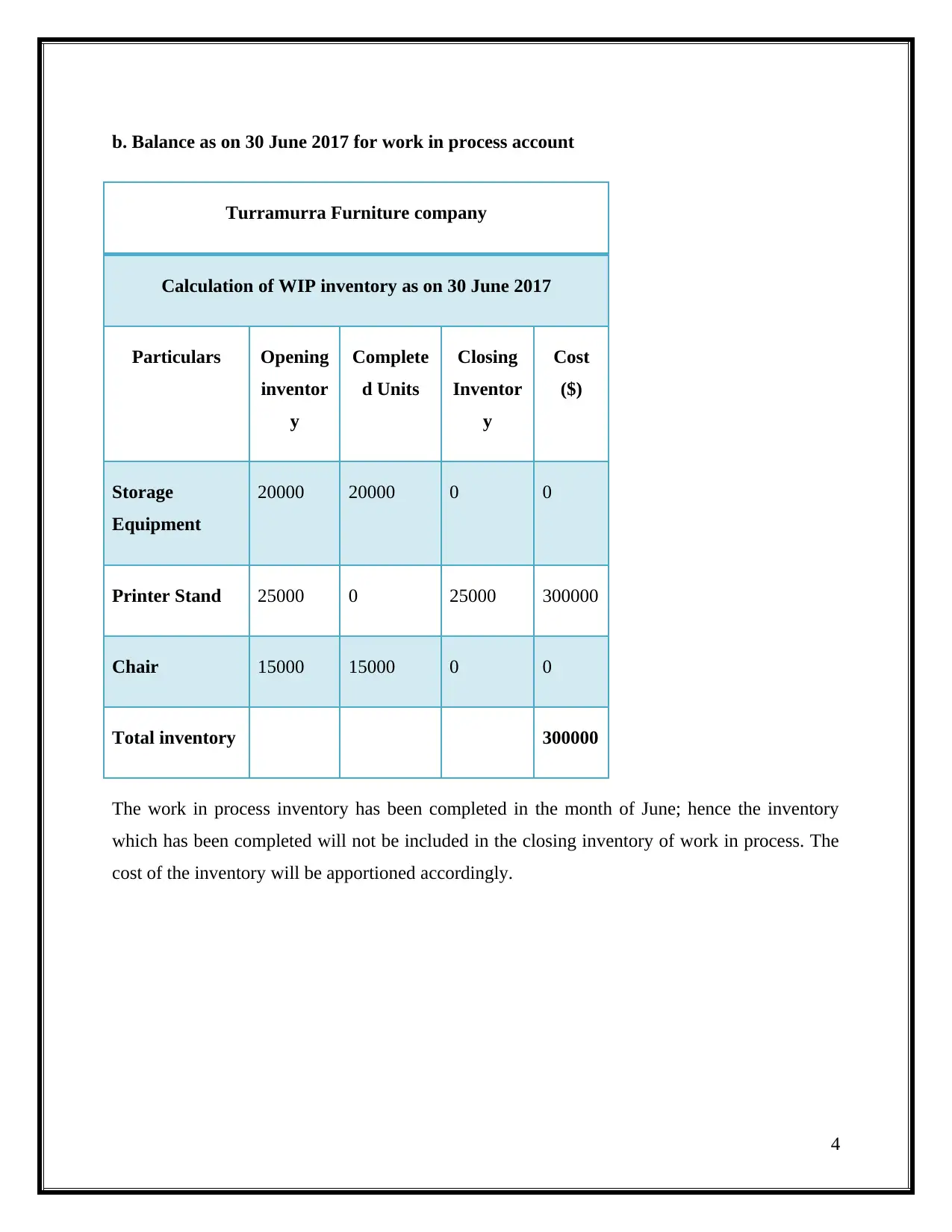

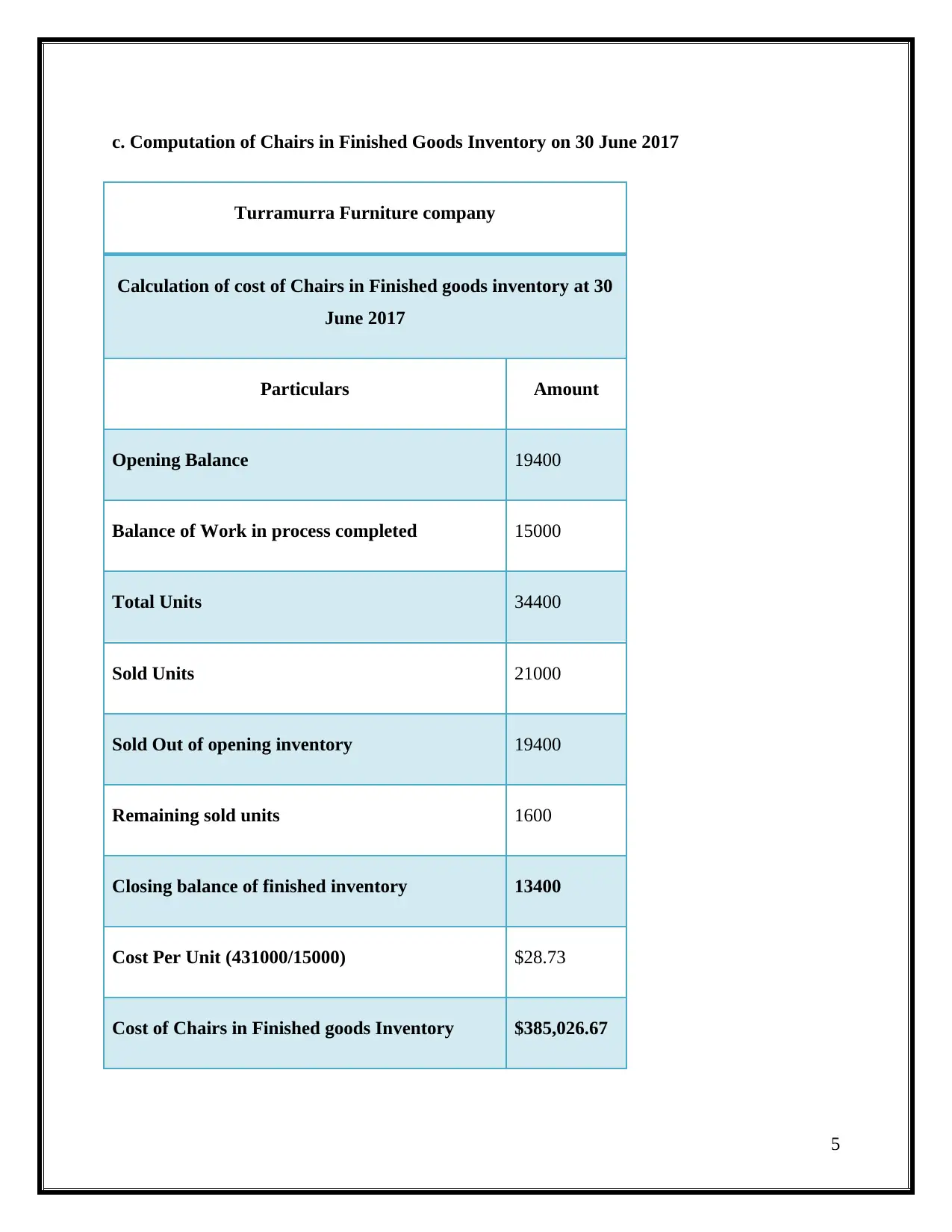

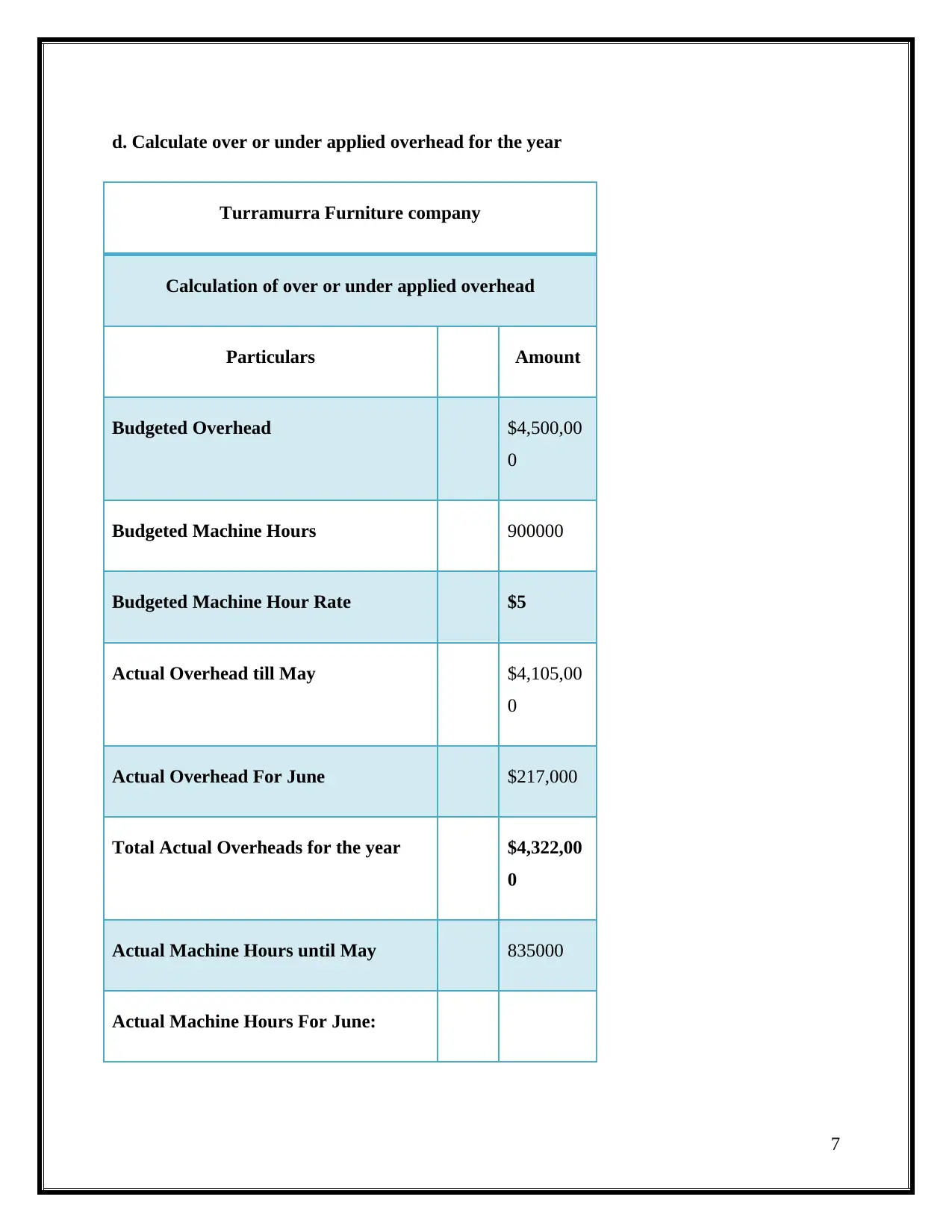

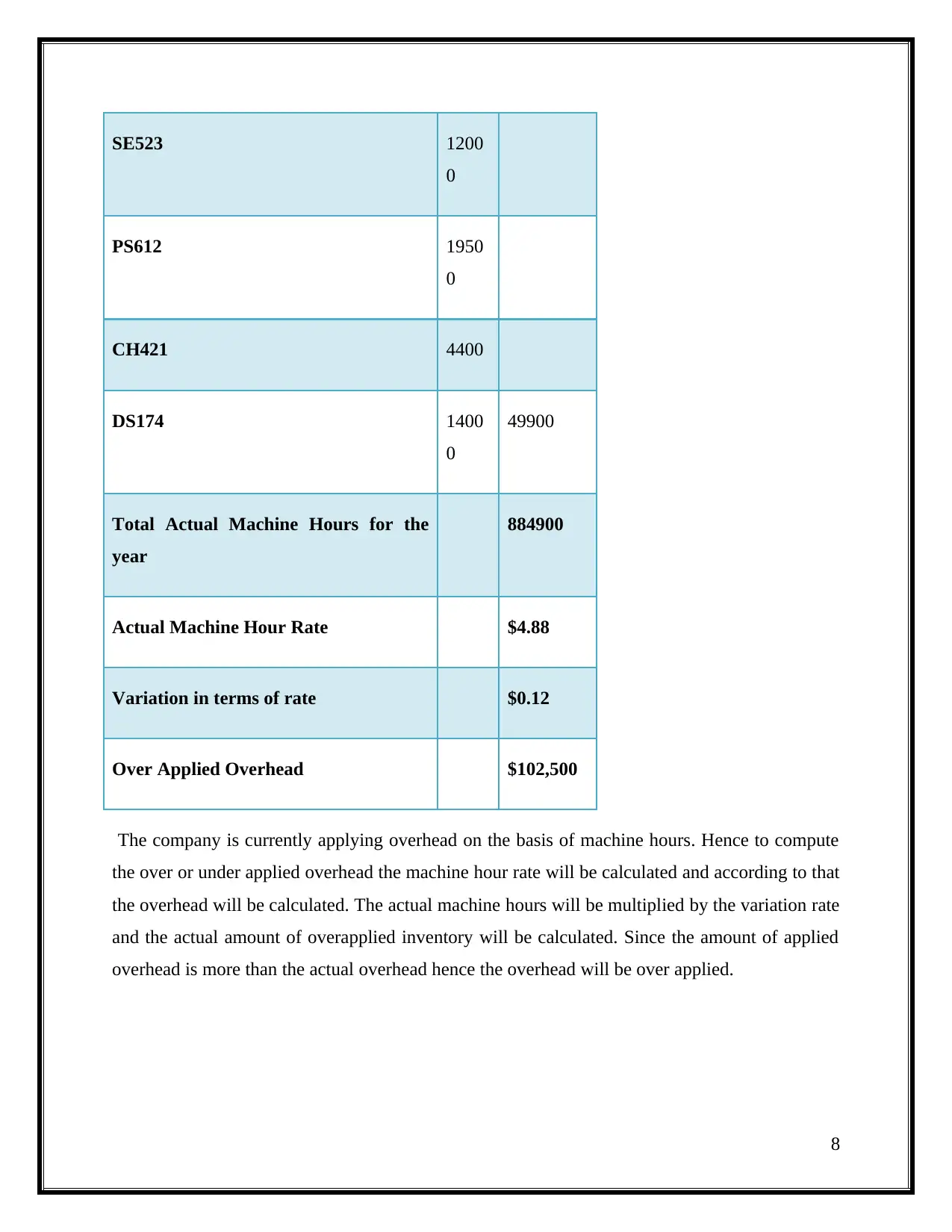

This report provides a detailed analysis of Turramurra Furniture Company's job order costing system. It includes calculations for work-in-process (WIP) inventory as of June 30, 2017, and the cost of chairs in finished goods inventory for the same period. The report also calculates the over or under applied overhead for the year, discusses the treatment of over applied overhead, and suggests an approach for handling material over applied overhead. Furthermore, it explores the potential benefits of using activity-based costing (ABC) for expanding the company's product range, arguing that ABC offers advantages over the traditional job order costing method by allocating costs based on cost drivers rather than machine hours. The report concludes that implementing ABC could improve activity planning, control processes, and capacity utilization within the company.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.