Job Order Costing System in Manufacturing Industries

VerifiedAdded on 2024/04/26

|12

|1529

|440

AI Summary

This document discusses the application of job order costing system in manufacturing industries, focusing on work in process inventory, finished goods inventory, and treatment of overapplied overhead. It also explores the benefits of implementing Activity-Based Costing.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACC200

1.

1

1.

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

1.......................................................................................................................................................3

a. Circumstances when the job order costing system can be used........................................3

b. Balance as on 30 June 2017 for work in process account..................................................4

c. Computation of Chairs in Finished Goods Inventory at 30 June 2017.............................5

d. Calculate over or under applied overhead for the year.....................................................7

e. Treatment for over applied of Overhead.............................................................................9

f. Approach to be used if the over applied overhead is material.........................................10

g. Activity-Based Costing should be used by the company to expand the range of the

product......................................................................................................................................11

References.....................................................................................................................................12

2

1.......................................................................................................................................................3

a. Circumstances when the job order costing system can be used........................................3

b. Balance as on 30 June 2017 for work in process account..................................................4

c. Computation of Chairs in Finished Goods Inventory at 30 June 2017.............................5

d. Calculate over or under applied overhead for the year.....................................................7

e. Treatment for over applied of Overhead.............................................................................9

f. Approach to be used if the over applied overhead is material.........................................10

g. Activity-Based Costing should be used by the company to expand the range of the

product......................................................................................................................................11

References.....................................................................................................................................12

2

1.

a. Circumstances when the job order costing system can be used

The job order costing system can be followed by the service and manufacturing industries. The

companies following this system will of the nature of manufacturing different products. The

system can be used by the company who requires the orders to be placed in a customized

manner. When the products of the company are manufactured on the basis of the customers then

the job order costing system should be used. When the products are similar then the system used

will be the process costing system. The job order costing system will create cost record of the job

for every product. The cost record will state the cost of the direct material, direct labour and

overheads relating to the manufacturing. The cost records also help the company in the

preparation of the ledger and the documents required for the finished stock inventory, work in

process inventory and the goods sold cost (Bragg, 2017).

3

a. Circumstances when the job order costing system can be used

The job order costing system can be followed by the service and manufacturing industries. The

companies following this system will of the nature of manufacturing different products. The

system can be used by the company who requires the orders to be placed in a customized

manner. When the products of the company are manufactured on the basis of the customers then

the job order costing system should be used. When the products are similar then the system used

will be the process costing system. The job order costing system will create cost record of the job

for every product. The cost record will state the cost of the direct material, direct labour and

overheads relating to the manufacturing. The cost records also help the company in the

preparation of the ledger and the documents required for the finished stock inventory, work in

process inventory and the goods sold cost (Bragg, 2017).

3

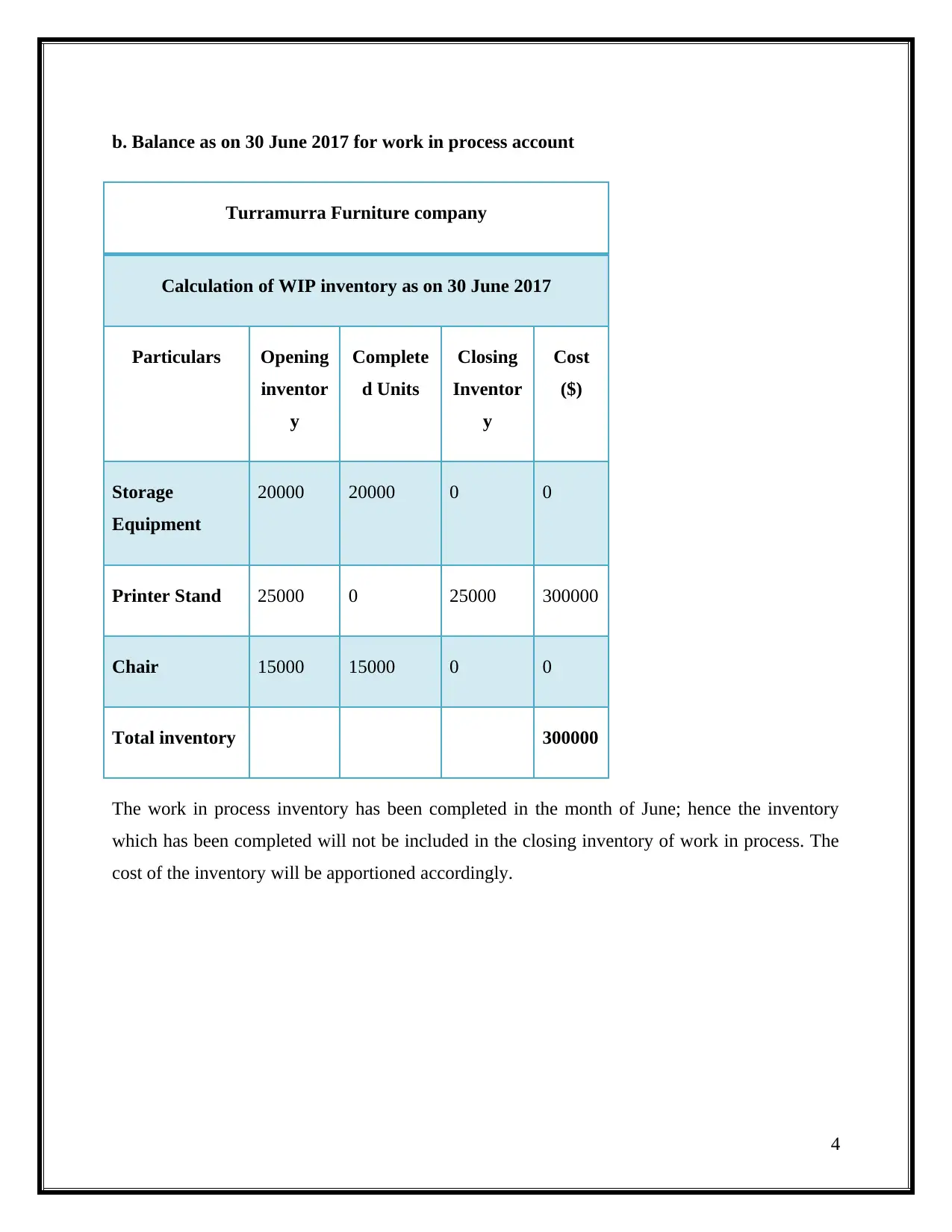

b. Balance as on 30 June 2017 for work in process account

Turramurra Furniture company

Calculation of WIP inventory as on 30 June 2017

Particulars Opening

inventor

y

Complete

d Units

Closing

Inventor

y

Cost

($)

Storage

Equipment

20000 20000 0 0

Printer Stand 25000 0 25000 300000

Chair 15000 15000 0 0

Total inventory 300000

The work in process inventory has been completed in the month of June; hence the inventory

which has been completed will not be included in the closing inventory of work in process. The

cost of the inventory will be apportioned accordingly.

4

Turramurra Furniture company

Calculation of WIP inventory as on 30 June 2017

Particulars Opening

inventor

y

Complete

d Units

Closing

Inventor

y

Cost

($)

Storage

Equipment

20000 20000 0 0

Printer Stand 25000 0 25000 300000

Chair 15000 15000 0 0

Total inventory 300000

The work in process inventory has been completed in the month of June; hence the inventory

which has been completed will not be included in the closing inventory of work in process. The

cost of the inventory will be apportioned accordingly.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

c. Computation of Chairs in Finished Goods Inventory on 30 June 2017

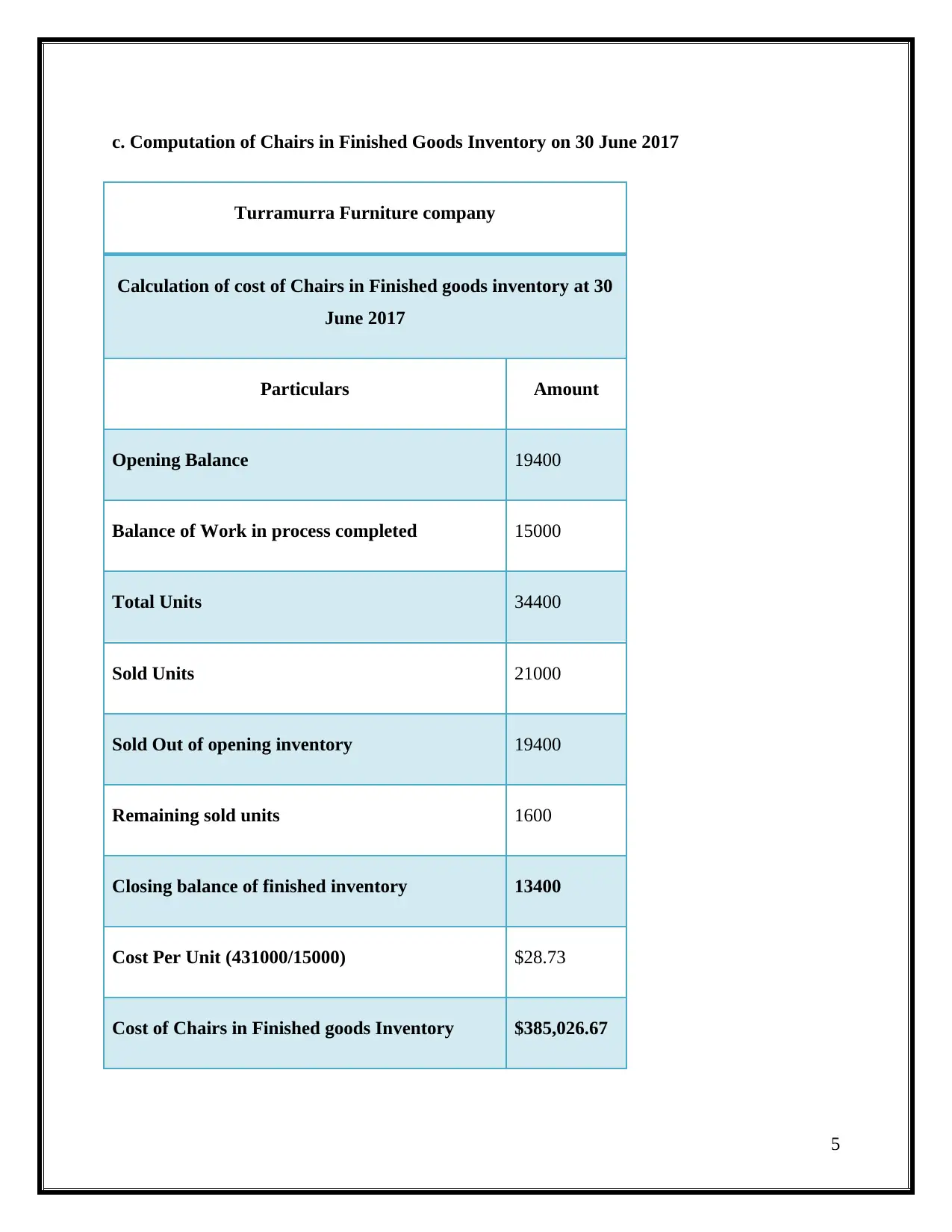

Turramurra Furniture company

Calculation of cost of Chairs in Finished goods inventory at 30

June 2017

Particulars Amount

Opening Balance 19400

Balance of Work in process completed 15000

Total Units 34400

Sold Units 21000

Sold Out of opening inventory 19400

Remaining sold units 1600

Closing balance of finished inventory 13400

Cost Per Unit (431000/15000) $28.73

Cost of Chairs in Finished goods Inventory $385,026.67

5

Turramurra Furniture company

Calculation of cost of Chairs in Finished goods inventory at 30

June 2017

Particulars Amount

Opening Balance 19400

Balance of Work in process completed 15000

Total Units 34400

Sold Units 21000

Sold Out of opening inventory 19400

Remaining sold units 1600

Closing balance of finished inventory 13400

Cost Per Unit (431000/15000) $28.73

Cost of Chairs in Finished goods Inventory $385,026.67

5

The balance of the chairs will be calculated as it is shown in the above table. The inventory

which was completed in the month of June will also be included in the finished goods inventory.

The company is following FIFO method, hence the opening balance of finished inventory will be

sold out first and then the balance of the work in process inventory will be sold out. The cost of

the work in process inventory will be used to calculate the cost due to the FIFO method.

6

which was completed in the month of June will also be included in the finished goods inventory.

The company is following FIFO method, hence the opening balance of finished inventory will be

sold out first and then the balance of the work in process inventory will be sold out. The cost of

the work in process inventory will be used to calculate the cost due to the FIFO method.

6

d. Calculate over or under applied overhead for the year

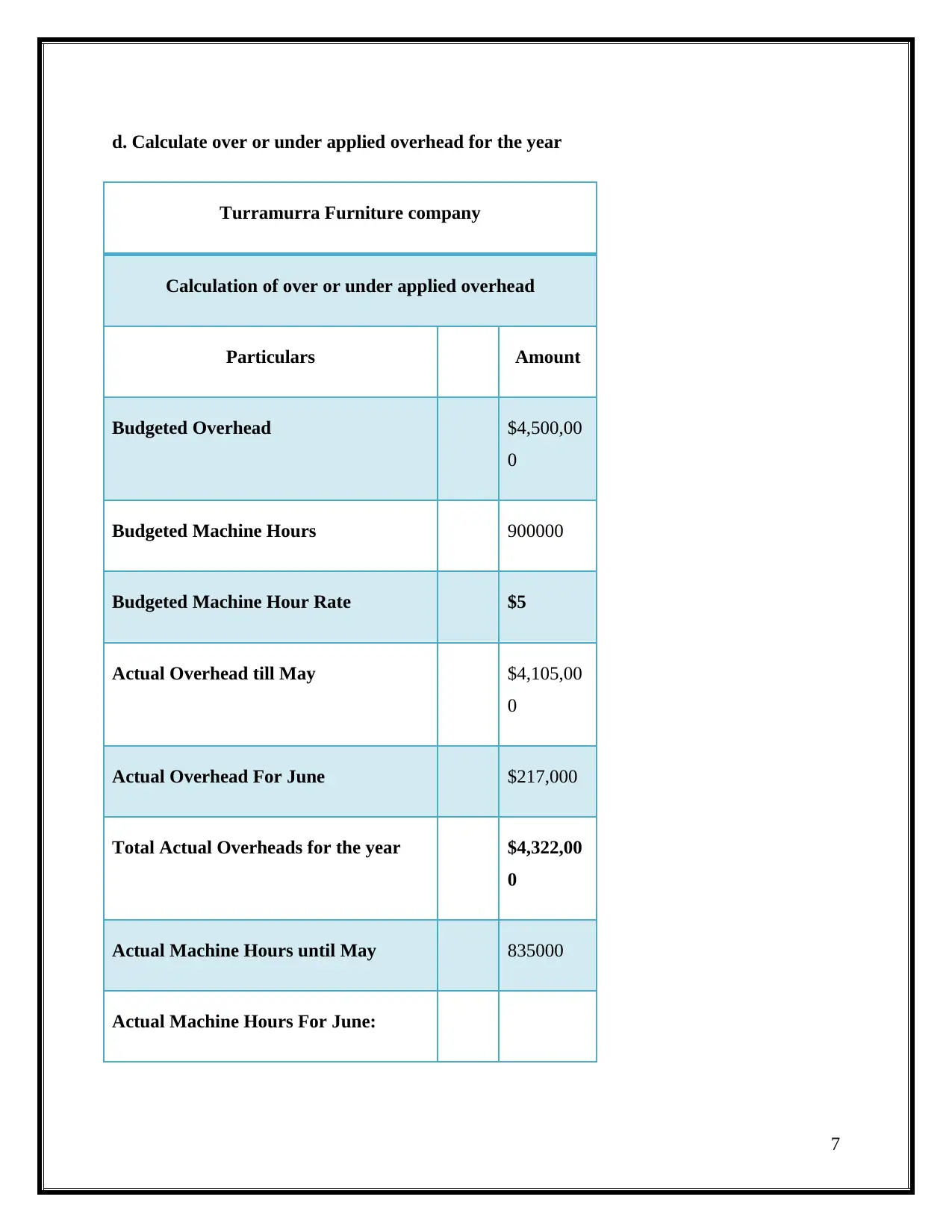

Turramurra Furniture company

Calculation of over or under applied overhead

Particulars Amount

Budgeted Overhead $4,500,00

0

Budgeted Machine Hours 900000

Budgeted Machine Hour Rate $5

Actual Overhead till May $4,105,00

0

Actual Overhead For June $217,000

Total Actual Overheads for the year $4,322,00

0

Actual Machine Hours until May 835000

Actual Machine Hours For June:

7

Turramurra Furniture company

Calculation of over or under applied overhead

Particulars Amount

Budgeted Overhead $4,500,00

0

Budgeted Machine Hours 900000

Budgeted Machine Hour Rate $5

Actual Overhead till May $4,105,00

0

Actual Overhead For June $217,000

Total Actual Overheads for the year $4,322,00

0

Actual Machine Hours until May 835000

Actual Machine Hours For June:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SE523 1200

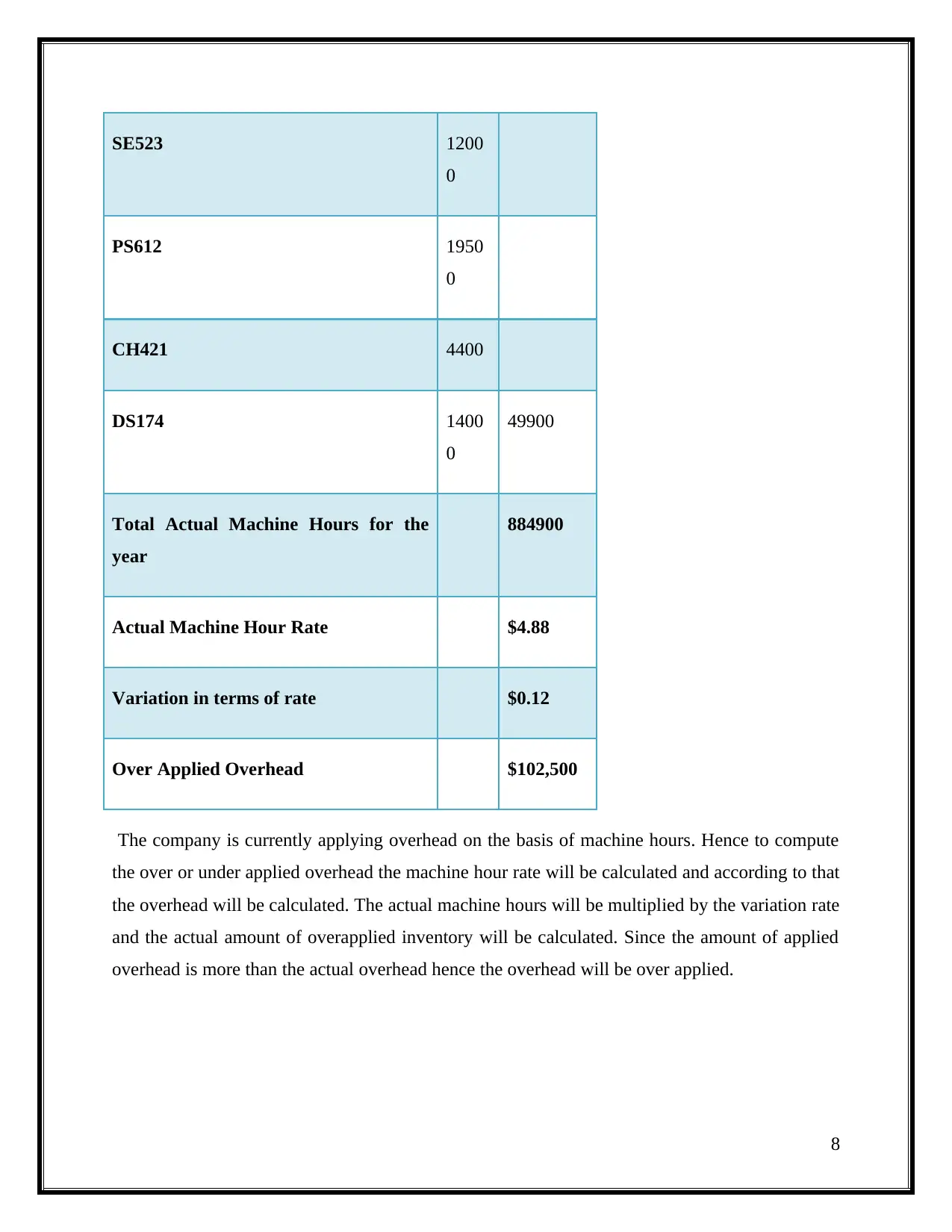

0

PS612 1950

0

CH421 4400

DS174 1400

0

49900

Total Actual Machine Hours for the

year

884900

Actual Machine Hour Rate $4.88

Variation in terms of rate $0.12

Over Applied Overhead $102,500

The company is currently applying overhead on the basis of machine hours. Hence to compute

the over or under applied overhead the machine hour rate will be calculated and according to that

the overhead will be calculated. The actual machine hours will be multiplied by the variation rate

and the actual amount of overapplied inventory will be calculated. Since the amount of applied

overhead is more than the actual overhead hence the overhead will be over applied.

8

0

PS612 1950

0

CH421 4400

DS174 1400

0

49900

Total Actual Machine Hours for the

year

884900

Actual Machine Hour Rate $4.88

Variation in terms of rate $0.12

Over Applied Overhead $102,500

The company is currently applying overhead on the basis of machine hours. Hence to compute

the over or under applied overhead the machine hour rate will be calculated and according to that

the overhead will be calculated. The actual machine hours will be multiplied by the variation rate

and the actual amount of overapplied inventory will be calculated. Since the amount of applied

overhead is more than the actual overhead hence the overhead will be over applied.

8

e. Treatment for over applied of Overhead

The overhead which is applied is more than the actual overhead hence the overhead is over

applied. The over applied of inventory can be treated in two ways:

The over applied of inventory can be allocated among the cost of goods sold account

and inventory account i.e. finished goods, work in process and dispose it off.

The over applied of inventory can also be treated by allocating to the cost of goods

sold account and then dispose it off.

The above are the two treatments which can be used by the company if it has been following the

job order costing system. The company will then pass the accounting entries regarding the above

treatments and dispose off the manufacturing overhead that is over applied. The company will

allocate the amount of overapplied inventory in the proportionate amount (Chiang, 2013).

9

The overhead which is applied is more than the actual overhead hence the overhead is over

applied. The over applied of inventory can be treated in two ways:

The over applied of inventory can be allocated among the cost of goods sold account

and inventory account i.e. finished goods, work in process and dispose it off.

The over applied of inventory can also be treated by allocating to the cost of goods

sold account and then dispose it off.

The above are the two treatments which can be used by the company if it has been following the

job order costing system. The company will then pass the accounting entries regarding the above

treatments and dispose off the manufacturing overhead that is over applied. The company will

allocate the amount of overapplied inventory in the proportionate amount (Chiang, 2013).

9

f. Approach to be used if the overapplied overhead is material

Among the total amount of overapplied overhead of $ 102,500, the amount of $ 40,000 is

material. To adjust the amount of material overapplied overhead, the company is required to

apply the method which is applied in absorption costing. In the absorption costing method, the

product cost is calculated by adding the direct cost and the proportion of overheads. The

absorption costing method is the method where the cost of the product is calculated and the

adjustment of the overapplied overhead will be necessary. The over or under applied overhead

will be treated in the income statement of the company (Aurora, 2013).

In the given scenario, the company will use the approach of the absorption costing where the

treatment of the overapplied overhead will be made in the income statement of the company. The

other approach is the marginal costing where there will be no treatment of the overapplied

overhead and in the given case the overapplied overhead is material which is important. Hence,

the absorption costing approach should be used by the company (Chiang, 2013).

10

Among the total amount of overapplied overhead of $ 102,500, the amount of $ 40,000 is

material. To adjust the amount of material overapplied overhead, the company is required to

apply the method which is applied in absorption costing. In the absorption costing method, the

product cost is calculated by adding the direct cost and the proportion of overheads. The

absorption costing method is the method where the cost of the product is calculated and the

adjustment of the overapplied overhead will be necessary. The over or under applied overhead

will be treated in the income statement of the company (Aurora, 2013).

In the given scenario, the company will use the approach of the absorption costing where the

treatment of the overapplied overhead will be made in the income statement of the company. The

other approach is the marginal costing where there will be no treatment of the overapplied

overhead and in the given case the overapplied overhead is material which is important. Hence,

the absorption costing approach should be used by the company (Chiang, 2013).

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

g. Activity-Based Costing should be used by the company to expand the range of the

product

The job order costing is the system which is used by the company who produces the products as

per the demand of the customer. Under the job order costing system the product has to undergo

many stages till the product has reached its final stage. The cost is allocated on the basis of

machine hours in case of job costing system. The activity-based costing is the system which

allocates the cost on the basis of a particular cost driver and it is used to plan and control the

activities. The cost is not allocated on the basis of the machine hours while it allocates the cost

on the basis of the preferences of the product of the company on the basis of the cost driver

(Rojas, 2018).

The ABC system is implemented in the organization which is expensive at the time of

implementation but it is beneficial for the company in the long run. The system will improve the

activities of the business and improve the process of the company (Rojas, 2018). The system is

capable of identifying the spare capacity and allocates the capacity according to the use. The

system will be able to identify on the basis of the capacity any product or the process which is of

no use to the company. Hence the company will be of benefit if it implements the ABC system

for the new product range and new concerns as it is far better than the previous method i.e. job

order costing.

11

product

The job order costing is the system which is used by the company who produces the products as

per the demand of the customer. Under the job order costing system the product has to undergo

many stages till the product has reached its final stage. The cost is allocated on the basis of

machine hours in case of job costing system. The activity-based costing is the system which

allocates the cost on the basis of a particular cost driver and it is used to plan and control the

activities. The cost is not allocated on the basis of the machine hours while it allocates the cost

on the basis of the preferences of the product of the company on the basis of the cost driver

(Rojas, 2018).

The ABC system is implemented in the organization which is expensive at the time of

implementation but it is beneficial for the company in the long run. The system will improve the

activities of the business and improve the process of the company (Rojas, 2018). The system is

capable of identifying the spare capacity and allocates the capacity according to the use. The

system will be able to identify on the basis of the capacity any product or the process which is of

no use to the company. Hence the company will be of benefit if it implements the ABC system

for the new product range and new concerns as it is far better than the previous method i.e. job

order costing.

11

References

1. Aurora, B. B. C. (2013). The Cost of Production under Direct Costing and Absorption

Costing–A Comparative Approach. Annals-Economy Series, 2, 123-129.

2. Bragg, S., (2017). Job Costing. [Online]. Available at:

https://www.accountingtools.com/articles/2017/5/14/job-costing [Accessed: 22 January

2018].

3. Chiang, B. (2013). Indirect Labor Costs and Implications for Overhead Allocation.

4. Rojas, E., (2018). The Disadvantages and Advantages of Activity-Based Costing.

[Online]. Available at: http://smallbusiness.chron.com/disadvantages-advantages-

activity-based-costing-45096.html [Accessed: 22 January 2018].

12

1. Aurora, B. B. C. (2013). The Cost of Production under Direct Costing and Absorption

Costing–A Comparative Approach. Annals-Economy Series, 2, 123-129.

2. Bragg, S., (2017). Job Costing. [Online]. Available at:

https://www.accountingtools.com/articles/2017/5/14/job-costing [Accessed: 22 January

2018].

3. Chiang, B. (2013). Indirect Labor Costs and Implications for Overhead Allocation.

4. Rojas, E., (2018). The Disadvantages and Advantages of Activity-Based Costing.

[Online]. Available at: http://smallbusiness.chron.com/disadvantages-advantages-

activity-based-costing-45096.html [Accessed: 22 January 2018].

12

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.