AASB Standards Application in Financial Reporting: Practical Task

VerifiedAdded on 2023/06/14

|8

|1718

|436

Practical Assignment

AI Summary

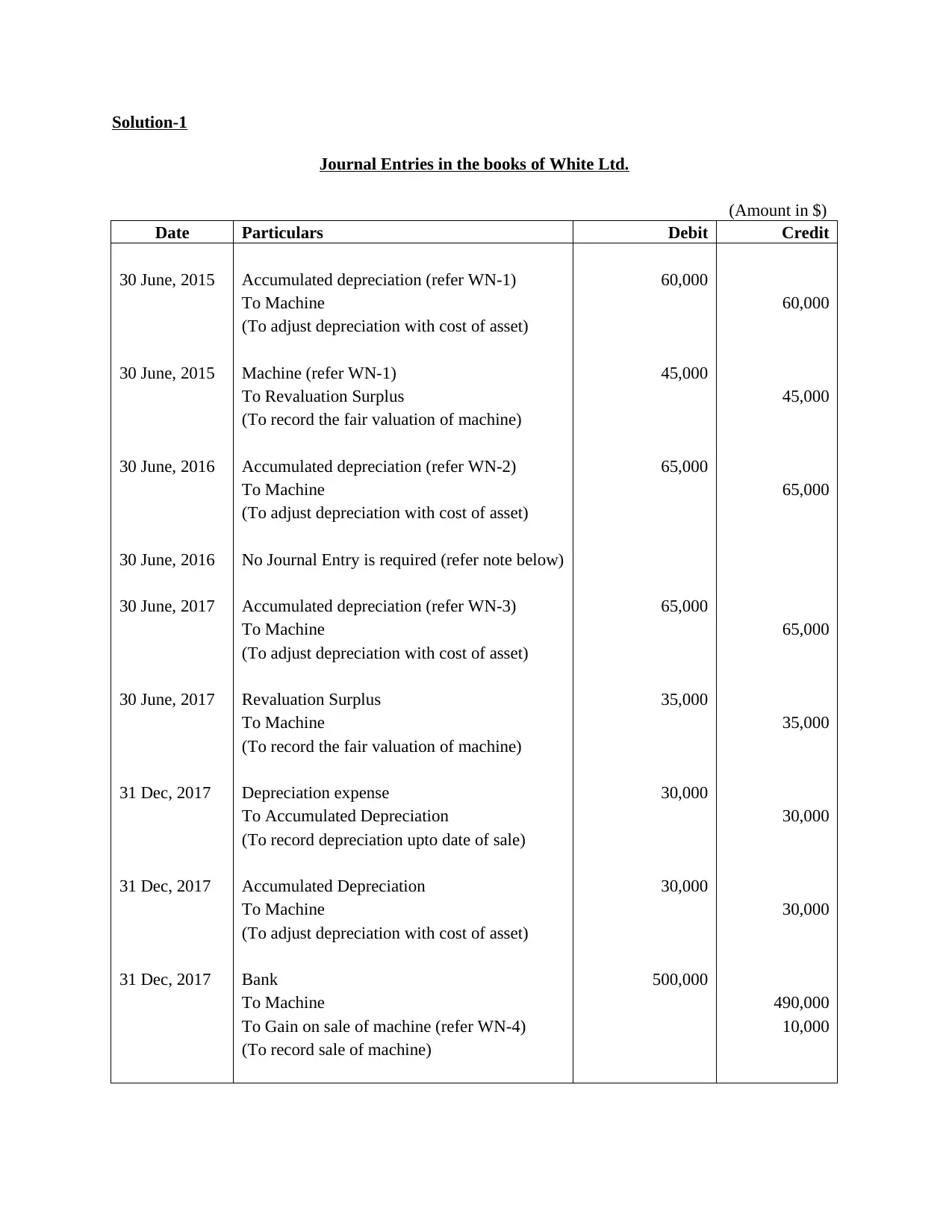

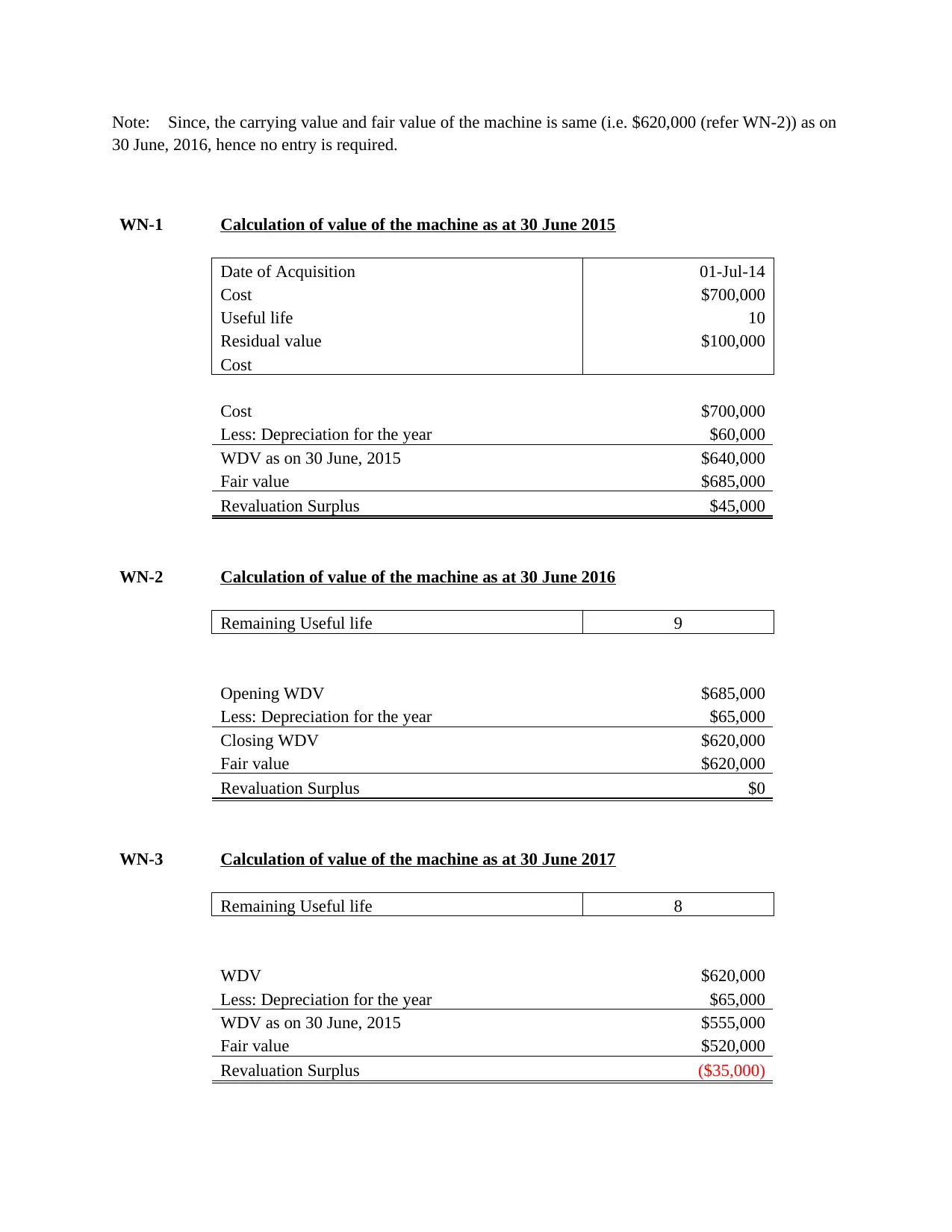

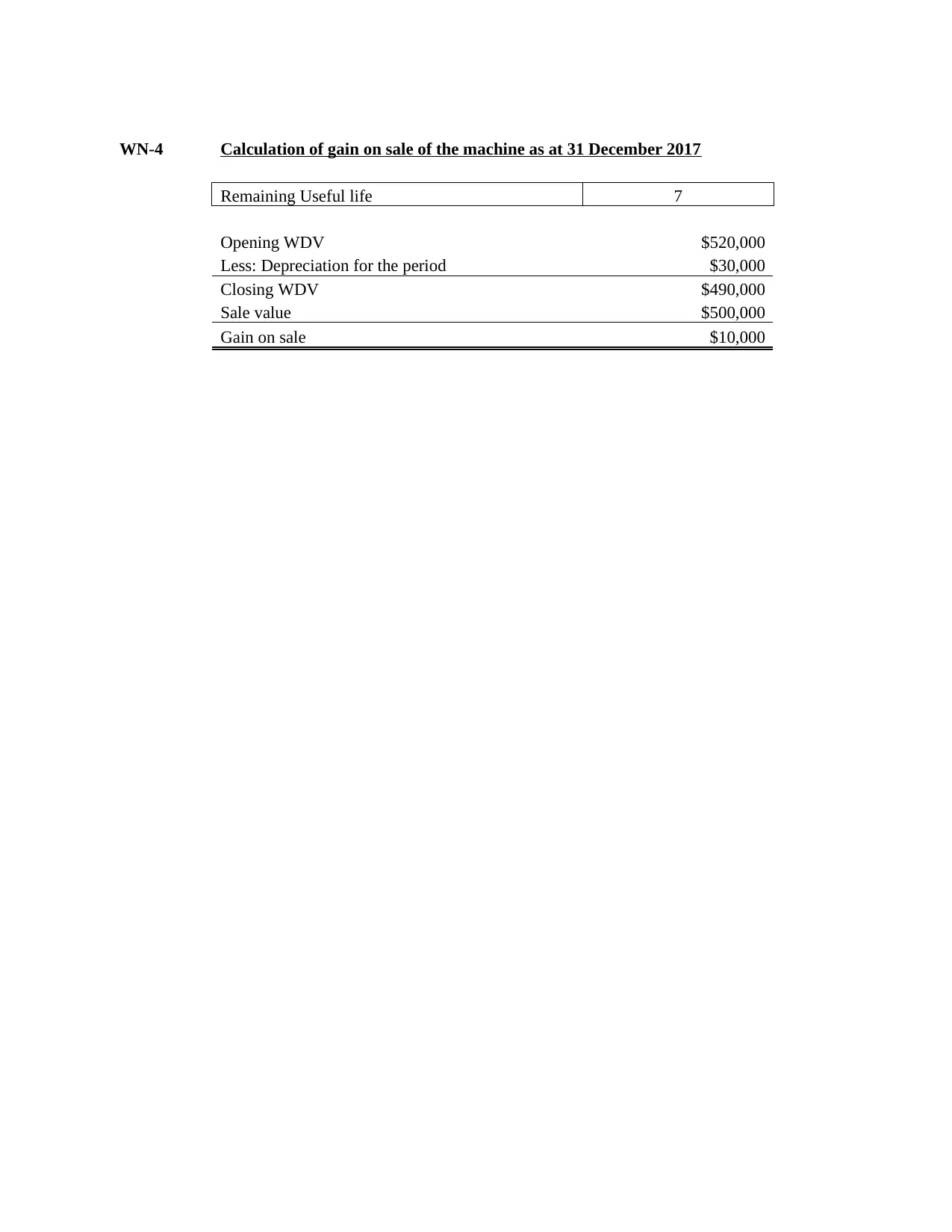

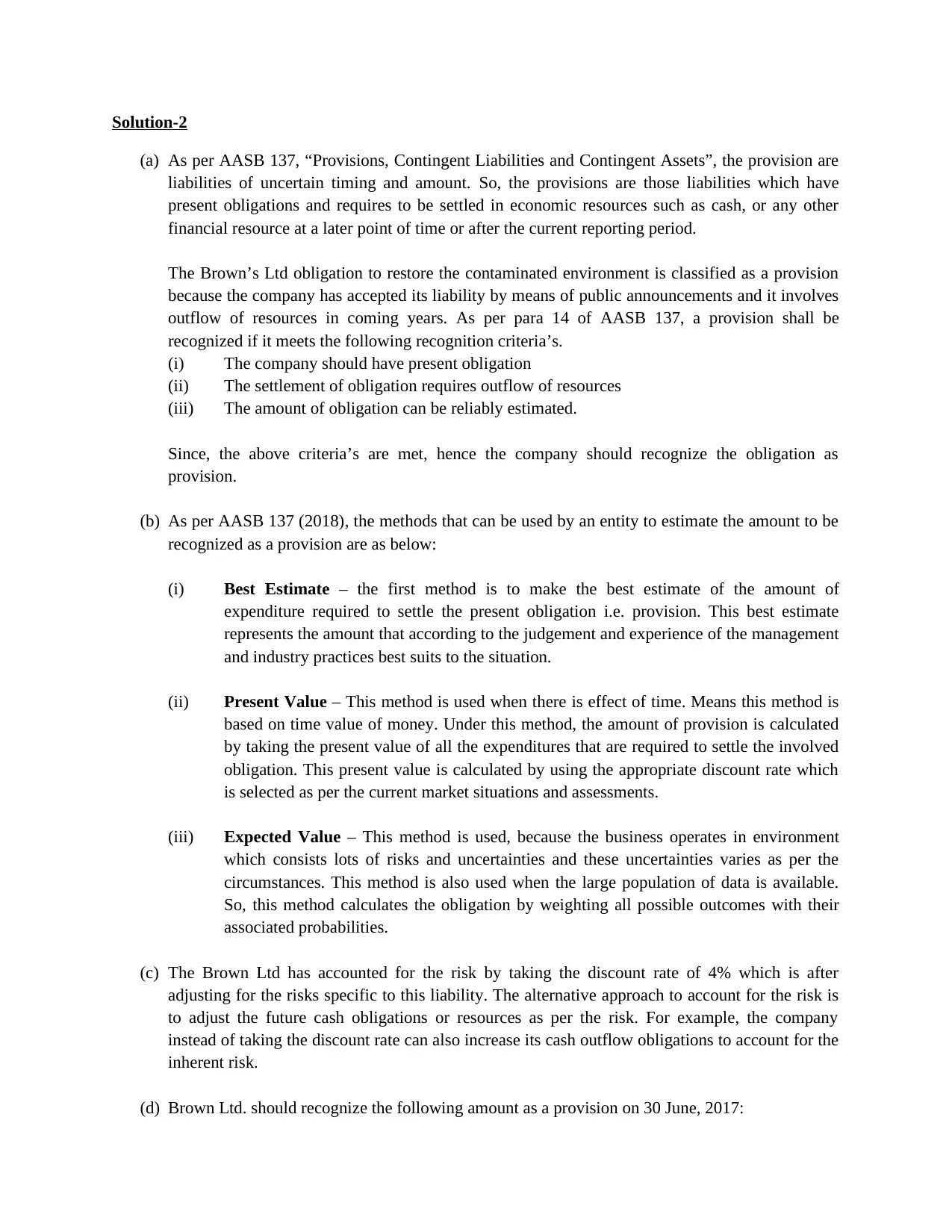

This practical assignment delves into the application of Australian Accounting Standards Board (AASB) standards in financial reporting. It includes journal entries for White Ltd., demonstrating the revaluation model for property, plant, and equipment (AASB 116), and calculations for depreciation and gains on sales. Furthermore, it addresses provisions, contingent liabilities, and contingent assets according to AASB 137, including the recognition criteria, estimation methods, and risk assessment. The assignment also covers intangible assets as per AASB 138, discussing identifiability, measurement models (cost and revaluation), and useful life determination for master licenses. The solutions provided offer a comprehensive understanding of how to apply these standards in various financial scenarios. Desklib provides more solved assignments and resources for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.