MPA702 Financial Interpretation: Kathmandu Holding Ratio Analysis

VerifiedAdded on 2023/06/08

|19

|3994

|239

Report

AI Summary

This report provides a comprehensive financial analysis of Kathmandu Holding Limited over the past five years using ratio analysis. It assesses the company's liquidity, profitability, operating efficiency, and solvency positions. The liquidity analysis reveals a strong position until 2015, followed by a decline. Profitability, measured by ROE, ROA, and net profit margin, decreased from 2013 to 2015 but showed improvement in subsequent years. Operating efficiency, evaluated through inventory, receivables, and payables turnover, indicates efficient inventory management but challenges in collecting receivables and managing payables. Solvency analysis suggests a healthy capital structure with low financial risk. The report concludes that while Kathmandu faces some challenges, its overall financial health is stable, with recent improvements in key areas. Desklib offers similar solved assignments for students.

Running ead athmandu olding imitedH : K H L

RATIO ANALYSIS

RATIO ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

athmandu olding imitedK H L 1

Introduction:

Kathmandu holding Limited is a company that is listed on New Zealand Stock Exchange

however it operates its business from three major segments: New Zealand, Australia and

United Kingdoms. The company was established in the year 1987 and is located in

Christchurch, New Zealand. The business in which Kathmandu group is engaged is of

designing, marketing as well as retailing the wide range of clothing and equipment that are

required for the tour and travel purpose. The product range of the company covers variety of

apparels such as waterproof jackets, fleece jackets, thermals, merino thermals and jackets. It

also manufactures shoes and shocks for the travelling purposes. The travelling and touring

equipment includes bag-backs, sleeping bags, tents and various other travelling accessories

that are used for camping and trekking. In all Kathmandu Group has around, 160 stores out of

which 110 stores are located in Australia, over 46 stores are located in New Zealand and

around 4 stores are operated in United Kingdom. The subsidiaries of the company are

Milford Group Holdings Limited, Kathmandu Limited, Kathmandu Pty Limited and

Kathmandu (U.K.) Limited.

The purpose of this report is to carry out the evaluation of financial performance of

Kathmandu Holding Limited in last 5 years. To evaluate the company’s performance, the use

of Ratio analysis technique is made which is the key technique of financial management. As a

part of ratio analysis, various ratios in regards to various important components of the

financial statements of the company has been taken into account and their impact on the

overall financial position and performance of the business of Kathmandu Ltd. has been

analysed.

Application of Ratio Analysis

Introduction:

Kathmandu holding Limited is a company that is listed on New Zealand Stock Exchange

however it operates its business from three major segments: New Zealand, Australia and

United Kingdoms. The company was established in the year 1987 and is located in

Christchurch, New Zealand. The business in which Kathmandu group is engaged is of

designing, marketing as well as retailing the wide range of clothing and equipment that are

required for the tour and travel purpose. The product range of the company covers variety of

apparels such as waterproof jackets, fleece jackets, thermals, merino thermals and jackets. It

also manufactures shoes and shocks for the travelling purposes. The travelling and touring

equipment includes bag-backs, sleeping bags, tents and various other travelling accessories

that are used for camping and trekking. In all Kathmandu Group has around, 160 stores out of

which 110 stores are located in Australia, over 46 stores are located in New Zealand and

around 4 stores are operated in United Kingdom. The subsidiaries of the company are

Milford Group Holdings Limited, Kathmandu Limited, Kathmandu Pty Limited and

Kathmandu (U.K.) Limited.

The purpose of this report is to carry out the evaluation of financial performance of

Kathmandu Holding Limited in last 5 years. To evaluate the company’s performance, the use

of Ratio analysis technique is made which is the key technique of financial management. As a

part of ratio analysis, various ratios in regards to various important components of the

financial statements of the company has been taken into account and their impact on the

overall financial position and performance of the business of Kathmandu Ltd. has been

analysed.

Application of Ratio Analysis

athmandu olding imitedK H L 2

In order to identify the overall financial health of the business, ratio analysis has been carried

in four major aspects of financial position i.e. the liquidity position, profitability position,

operating efficiency position and solvency position of the business. The use of different sorts

of ratio will allow the managers of the company to pay more attention to the areas where the

financial ratios are indicating irregularity or any sort of risk on the company (Gibson, 2011).

All the financial results of preceding 5 financial years have been represented through graphs

to allow the managers or users of this information, to understand each result in the convenient

and clear manner. Along with the analysis of results of each individual year, a comparative

study has been made to understand the changes in the financial performance of the business

so that any required changes or recommendations for the subsequent periods could be made

for the purpose of achieving better results (Godwin and Alderman, 2012).

Liquidity Position:

First of all, liquidity position of the business has been analysed using the two key liquidity

ratios i.e. the current ratio and the liquid ratio. Generally, in regards of current ratio, a ratio of

2:1 is considered as ideal. In the present case of Kathmandu Holdings, it has been identified

that the current ratio of the company in 2013, 2014 and 2015 was satisfactory as it has

already achieved the ideal standards in these standards (Kathmandu, 2014). Therefore, it can

be said that the company had sufficient amount of current assets to meet the short term

liabilities that were supposed to be due in next 12 months from the date on which such

liabilities were entered into. The results of current ratio of shows that the company had sound

liquidity position till the end of 2015. After, 2015, both the current and quick ratios of the

company started declining and the declining liquidity ratios of the company clearly indicates

that the liquidity position of the company has worsened in last two reporting years. The

declining liquidity position of the business is faced when the company is not able to

efficiently manage and utilise its current assets to pay off its current liabilities. Thus to meet

In order to identify the overall financial health of the business, ratio analysis has been carried

in four major aspects of financial position i.e. the liquidity position, profitability position,

operating efficiency position and solvency position of the business. The use of different sorts

of ratio will allow the managers of the company to pay more attention to the areas where the

financial ratios are indicating irregularity or any sort of risk on the company (Gibson, 2011).

All the financial results of preceding 5 financial years have been represented through graphs

to allow the managers or users of this information, to understand each result in the convenient

and clear manner. Along with the analysis of results of each individual year, a comparative

study has been made to understand the changes in the financial performance of the business

so that any required changes or recommendations for the subsequent periods could be made

for the purpose of achieving better results (Godwin and Alderman, 2012).

Liquidity Position:

First of all, liquidity position of the business has been analysed using the two key liquidity

ratios i.e. the current ratio and the liquid ratio. Generally, in regards of current ratio, a ratio of

2:1 is considered as ideal. In the present case of Kathmandu Holdings, it has been identified

that the current ratio of the company in 2013, 2014 and 2015 was satisfactory as it has

already achieved the ideal standards in these standards (Kathmandu, 2014). Therefore, it can

be said that the company had sufficient amount of current assets to meet the short term

liabilities that were supposed to be due in next 12 months from the date on which such

liabilities were entered into. The results of current ratio of shows that the company had sound

liquidity position till the end of 2015. After, 2015, both the current and quick ratios of the

company started declining and the declining liquidity ratios of the company clearly indicates

that the liquidity position of the company has worsened in last two reporting years. The

declining liquidity position of the business is faced when the company is not able to

efficiently manage and utilise its current assets to pay off its current liabilities. Thus to meet

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

athmandu olding imitedK H L 3

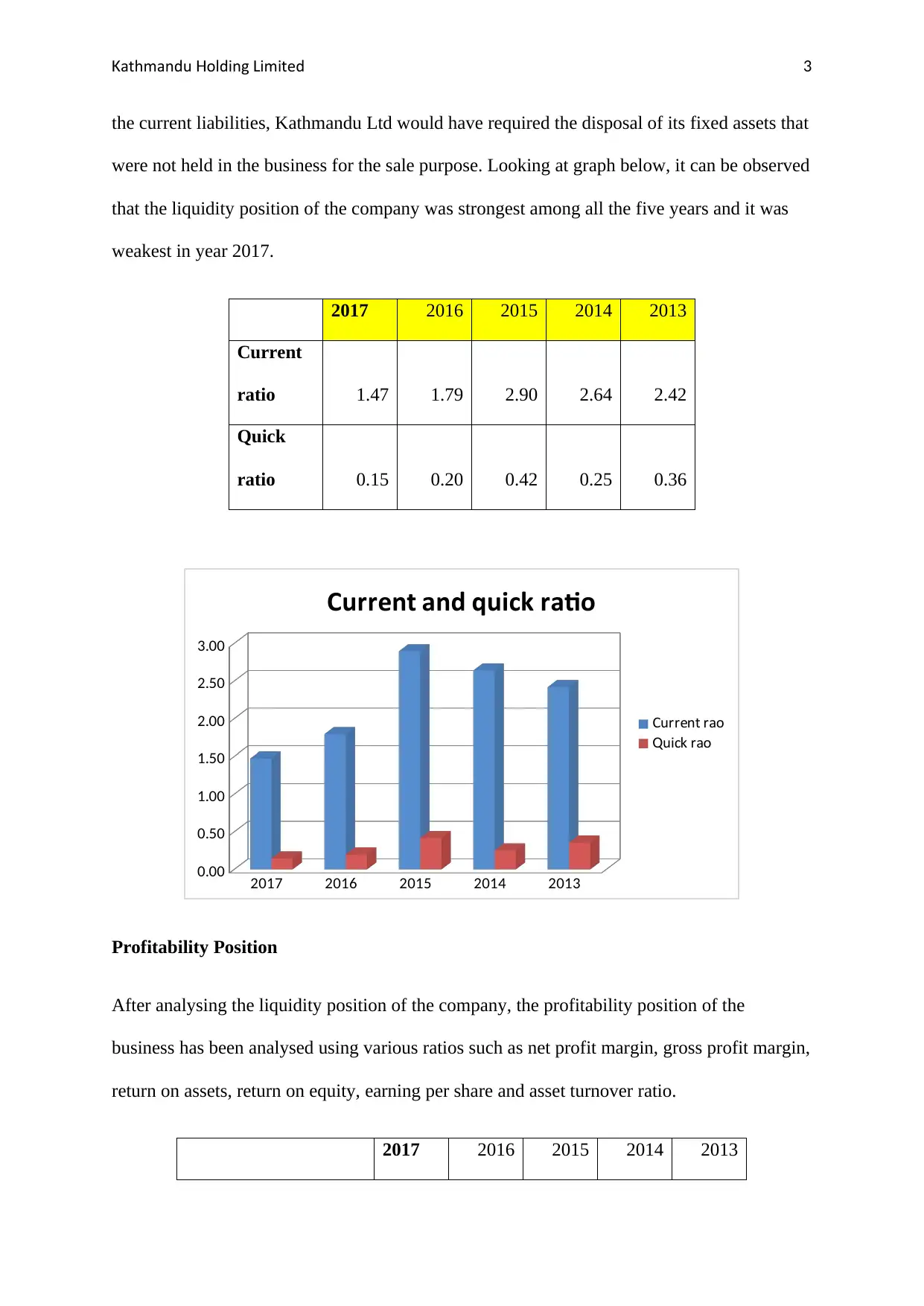

the current liabilities, Kathmandu Ltd would have required the disposal of its fixed assets that

were not held in the business for the sale purpose. Looking at graph below, it can be observed

that the liquidity position of the company was strongest among all the five years and it was

weakest in year 2017.

2017 2016 2015 2014 2013

Current

ratio 1.47 1.79 2.90 2.64 2.42

Quick

ratio 0.15 0.20 0.42 0.25 0.36

2017 2016 2015 2014 2013

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Current and quick ratio

Current ratio

uick ratioQ

Profitability Position

After analysing the liquidity position of the company, the profitability position of the

business has been analysed using various ratios such as net profit margin, gross profit margin,

return on assets, return on equity, earning per share and asset turnover ratio.

2017 2016 2015 2014 2013

the current liabilities, Kathmandu Ltd would have required the disposal of its fixed assets that

were not held in the business for the sale purpose. Looking at graph below, it can be observed

that the liquidity position of the company was strongest among all the five years and it was

weakest in year 2017.

2017 2016 2015 2014 2013

Current

ratio 1.47 1.79 2.90 2.64 2.42

Quick

ratio 0.15 0.20 0.42 0.25 0.36

2017 2016 2015 2014 2013

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Current and quick ratio

Current ratio

uick ratioQ

Profitability Position

After analysing the liquidity position of the company, the profitability position of the

business has been analysed using various ratios such as net profit margin, gross profit margin,

return on assets, return on equity, earning per share and asset turnover ratio.

2017 2016 2015 2014 2013

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

athmandu olding imitedK H L 4

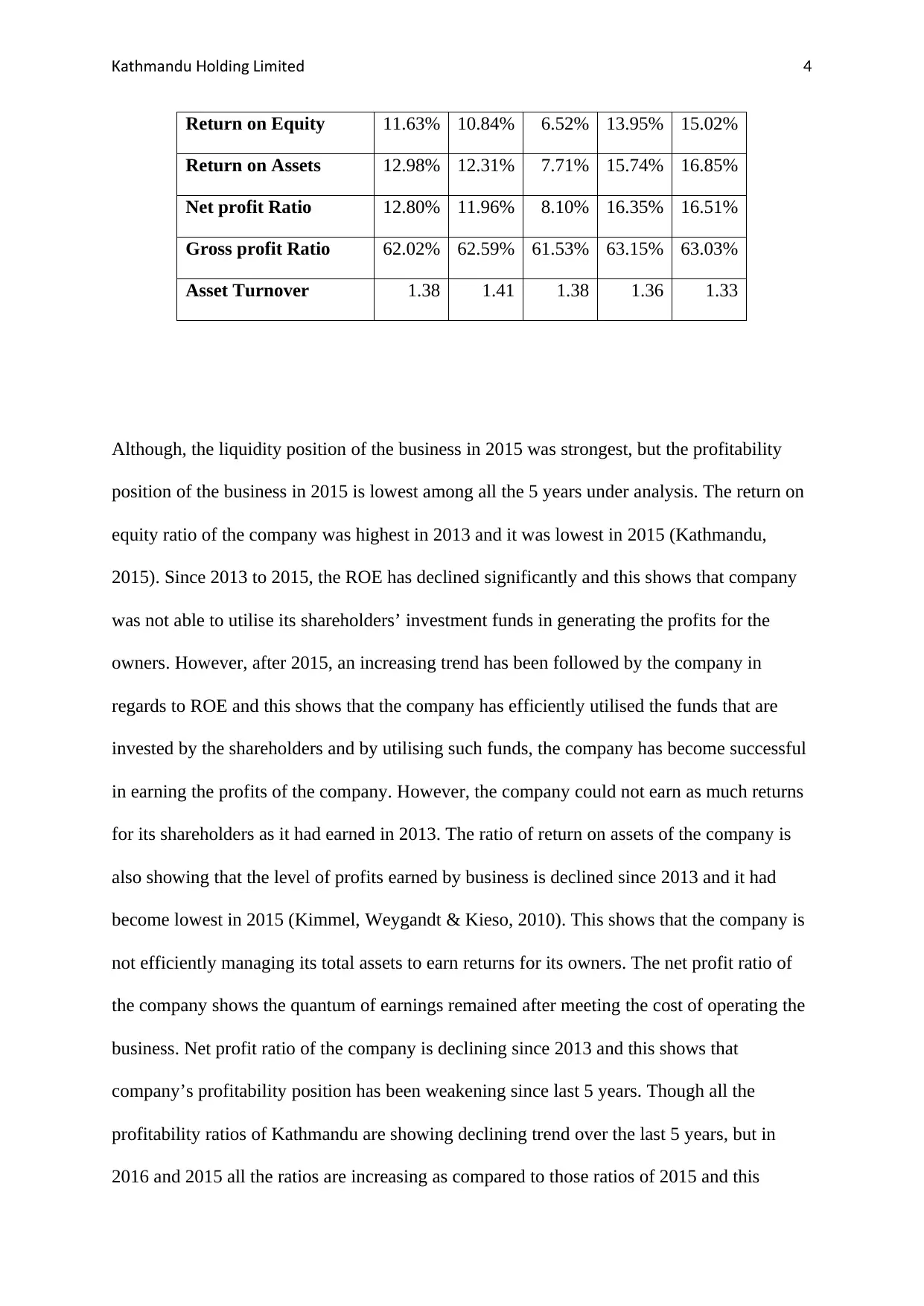

Return on Equity 11.63% 10.84% 6.52% 13.95% 15.02%

Return on Assets 12.98% 12.31% 7.71% 15.74% 16.85%

Net profit Ratio 12.80% 11.96% 8.10% 16.35% 16.51%

Gross profit Ratio 62.02% 62.59% 61.53% 63.15% 63.03%

Asset Turnover 1.38 1.41 1.38 1.36 1.33

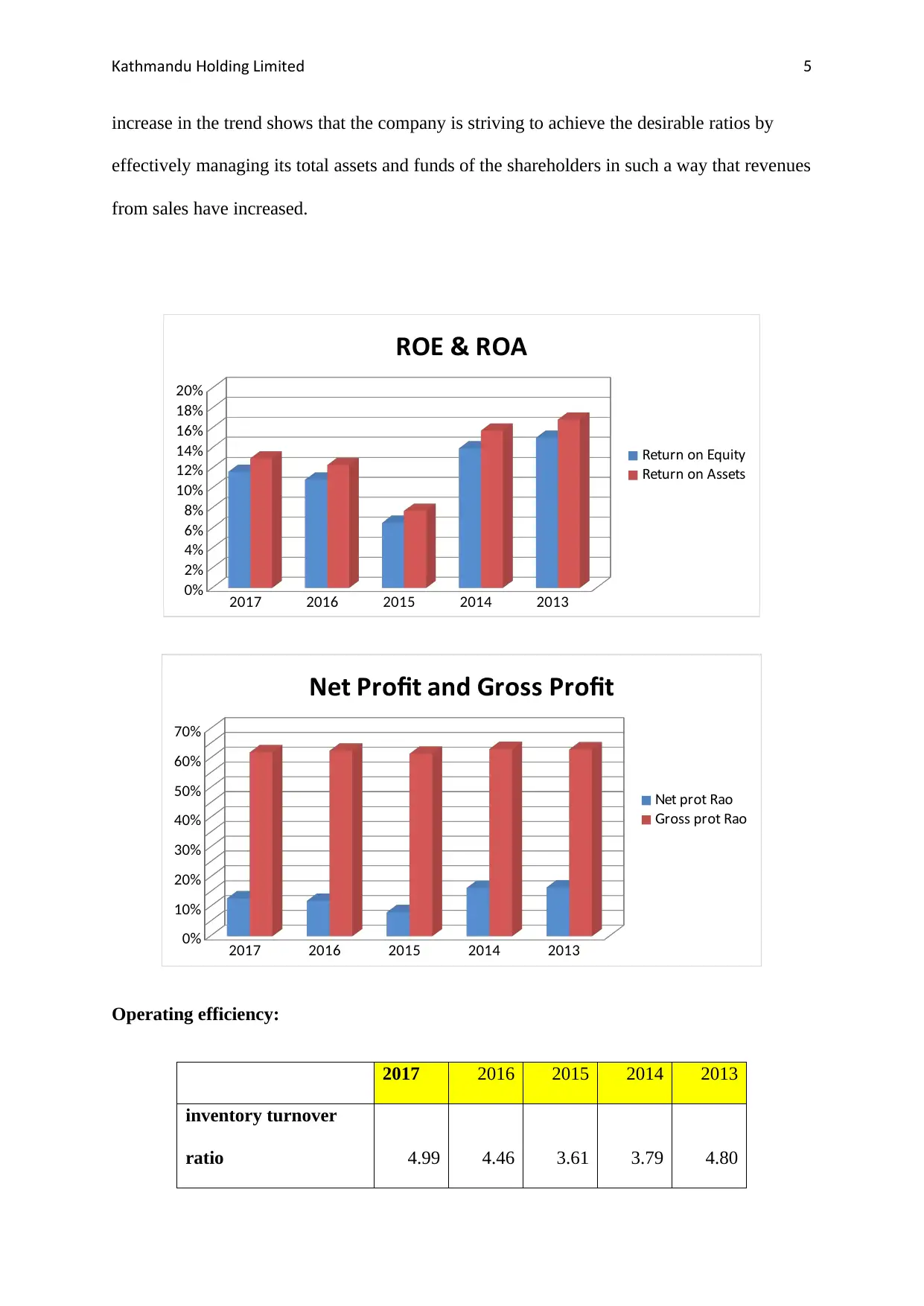

Although, the liquidity position of the business in 2015 was strongest, but the profitability

position of the business in 2015 is lowest among all the 5 years under analysis. The return on

equity ratio of the company was highest in 2013 and it was lowest in 2015 (Kathmandu,

2015). Since 2013 to 2015, the ROE has declined significantly and this shows that company

was not able to utilise its shareholders’ investment funds in generating the profits for the

owners. However, after 2015, an increasing trend has been followed by the company in

regards to ROE and this shows that the company has efficiently utilised the funds that are

invested by the shareholders and by utilising such funds, the company has become successful

in earning the profits of the company. However, the company could not earn as much returns

for its shareholders as it had earned in 2013. The ratio of return on assets of the company is

also showing that the level of profits earned by business is declined since 2013 and it had

become lowest in 2015 (Kimmel, Weygandt & Kieso, 2010). This shows that the company is

not efficiently managing its total assets to earn returns for its owners. The net profit ratio of

the company shows the quantum of earnings remained after meeting the cost of operating the

business. Net profit ratio of the company is declining since 2013 and this shows that

company’s profitability position has been weakening since last 5 years. Though all the

profitability ratios of Kathmandu are showing declining trend over the last 5 years, but in

2016 and 2015 all the ratios are increasing as compared to those ratios of 2015 and this

Return on Equity 11.63% 10.84% 6.52% 13.95% 15.02%

Return on Assets 12.98% 12.31% 7.71% 15.74% 16.85%

Net profit Ratio 12.80% 11.96% 8.10% 16.35% 16.51%

Gross profit Ratio 62.02% 62.59% 61.53% 63.15% 63.03%

Asset Turnover 1.38 1.41 1.38 1.36 1.33

Although, the liquidity position of the business in 2015 was strongest, but the profitability

position of the business in 2015 is lowest among all the 5 years under analysis. The return on

equity ratio of the company was highest in 2013 and it was lowest in 2015 (Kathmandu,

2015). Since 2013 to 2015, the ROE has declined significantly and this shows that company

was not able to utilise its shareholders’ investment funds in generating the profits for the

owners. However, after 2015, an increasing trend has been followed by the company in

regards to ROE and this shows that the company has efficiently utilised the funds that are

invested by the shareholders and by utilising such funds, the company has become successful

in earning the profits of the company. However, the company could not earn as much returns

for its shareholders as it had earned in 2013. The ratio of return on assets of the company is

also showing that the level of profits earned by business is declined since 2013 and it had

become lowest in 2015 (Kimmel, Weygandt & Kieso, 2010). This shows that the company is

not efficiently managing its total assets to earn returns for its owners. The net profit ratio of

the company shows the quantum of earnings remained after meeting the cost of operating the

business. Net profit ratio of the company is declining since 2013 and this shows that

company’s profitability position has been weakening since last 5 years. Though all the

profitability ratios of Kathmandu are showing declining trend over the last 5 years, but in

2016 and 2015 all the ratios are increasing as compared to those ratios of 2015 and this

athmandu olding imitedK H L 5

increase in the trend shows that the company is striving to achieve the desirable ratios by

effectively managing its total assets and funds of the shareholders in such a way that revenues

from sales have increased.

2017 2016 2015 2014 2013

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

ROE & ROA

Return on quityE

Return on Assets

2017 2016 2015 2014 2013

0%

10%

20%

30%

40%

50%

60%

70%

Net Profit and Gross Profit

et profit RatioN

ross profit RatioG

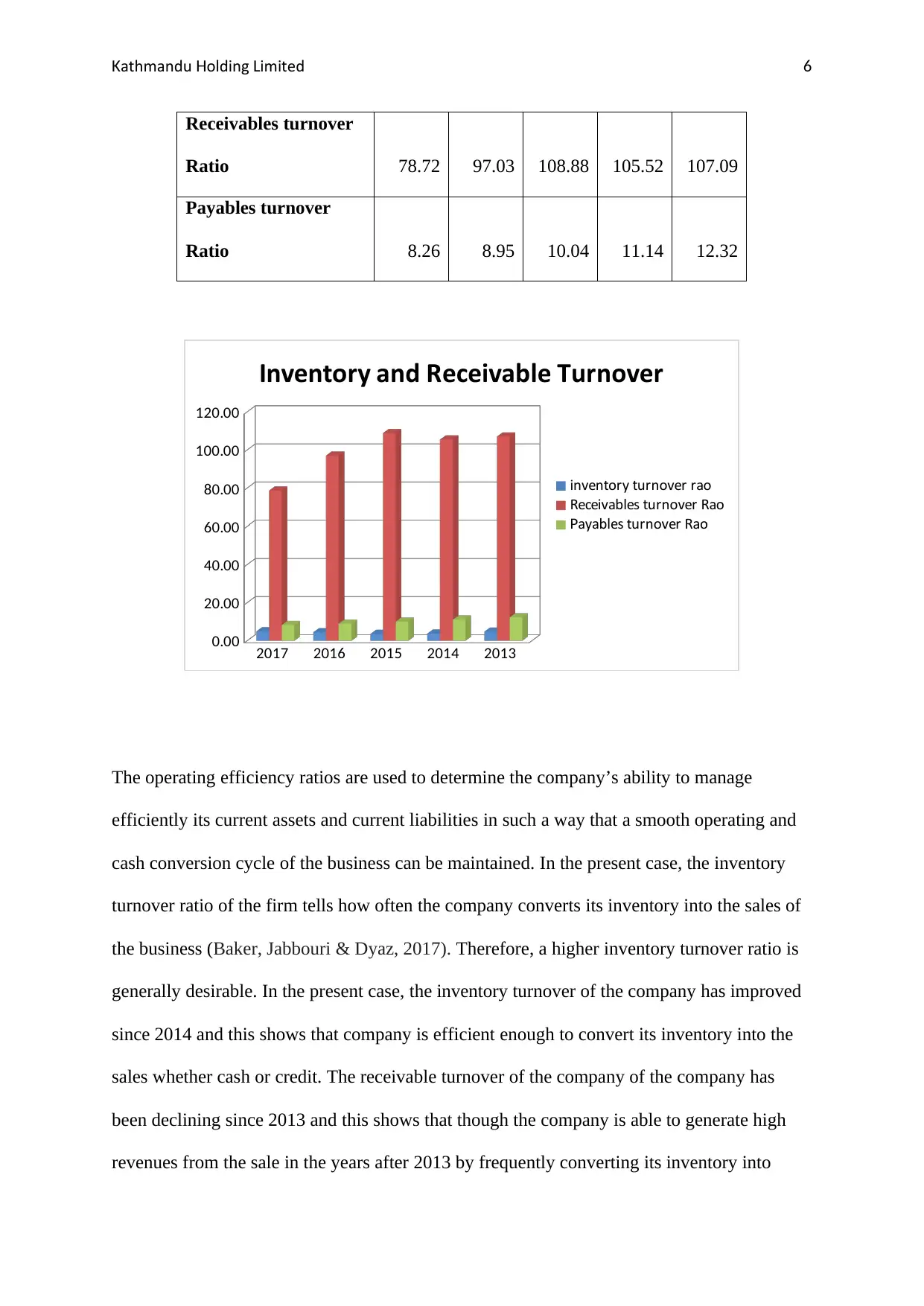

Operating efficiency:

2017 2016 2015 2014 2013

inventory turnover

ratio 4.99 4.46 3.61 3.79 4.80

increase in the trend shows that the company is striving to achieve the desirable ratios by

effectively managing its total assets and funds of the shareholders in such a way that revenues

from sales have increased.

2017 2016 2015 2014 2013

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

ROE & ROA

Return on quityE

Return on Assets

2017 2016 2015 2014 2013

0%

10%

20%

30%

40%

50%

60%

70%

Net Profit and Gross Profit

et profit RatioN

ross profit RatioG

Operating efficiency:

2017 2016 2015 2014 2013

inventory turnover

ratio 4.99 4.46 3.61 3.79 4.80

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

athmandu olding imitedK H L 6

Receivables turnover

Ratio 78.72 97.03 108.88 105.52 107.09

Payables turnover

Ratio 8.26 8.95 10.04 11.14 12.32

2017 2016 2015 2014 2013

0.00

20.00

40.00

60.00

80.00

100.00

120.00

Inventory and Receivable Turnover

inventory turnover ratio

Receivables turnover Ratio

ayables turnover RatioP

The operating efficiency ratios are used to determine the company’s ability to manage

efficiently its current assets and current liabilities in such a way that a smooth operating and

cash conversion cycle of the business can be maintained. In the present case, the inventory

turnover ratio of the firm tells how often the company converts its inventory into the sales of

the business (Baker, Jabbouri & Dyaz, 2017). Therefore, a higher inventory turnover ratio is

generally desirable. In the present case, the inventory turnover of the company has improved

since 2014 and this shows that company is efficient enough to convert its inventory into the

sales whether cash or credit. The receivable turnover of the company of the company has

been declining since 2013 and this shows that though the company is able to generate high

revenues from the sale in the years after 2013 by frequently converting its inventory into

Receivables turnover

Ratio 78.72 97.03 108.88 105.52 107.09

Payables turnover

Ratio 8.26 8.95 10.04 11.14 12.32

2017 2016 2015 2014 2013

0.00

20.00

40.00

60.00

80.00

100.00

120.00

Inventory and Receivable Turnover

inventory turnover ratio

Receivables turnover Ratio

ayables turnover RatioP

The operating efficiency ratios are used to determine the company’s ability to manage

efficiently its current assets and current liabilities in such a way that a smooth operating and

cash conversion cycle of the business can be maintained. In the present case, the inventory

turnover ratio of the firm tells how often the company converts its inventory into the sales of

the business (Baker, Jabbouri & Dyaz, 2017). Therefore, a higher inventory turnover ratio is

generally desirable. In the present case, the inventory turnover of the company has improved

since 2014 and this shows that company is efficient enough to convert its inventory into the

sales whether cash or credit. The receivable turnover of the company of the company has

been declining since 2013 and this shows that though the company is able to generate high

revenues from the sale in the years after 2013 by frequently converting its inventory into

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

athmandu olding imitedK H L 7

sales but is it not able to collect sufficient cash from the sales made in the particular year

because of its lose trade credit policies. The declining receivable turnover ratio of the

company is a clear indicator of company’s inefficiency towards collecting the amount

receivables for the credit sales made in the year because company is not making required

efforts to convert its credit sales into cash. Due to this, the operating cash cycle of the

company is not maintained effectively and efficiently and leading to weak working capital

management of the company (Kathmandu, 2016). The payable turnover ratio of the company

gauges the speed with which a firm pays offs the amount that is due to its accounts payables

i.e. the suppliers and creditors of the business. In the present case, the accounts payable ratio

is continuously declining since 2013 till 2017 and this shows that the company is not paying

off its trade creditors on timely basis, all the amount due to them for the credit purchases

made from them (Kathmandu, 2017). The declining accounts payable ratio is an indication of

weakening financial position of the business. One of the major reason due to which the

company is unable to meet its trade credit obligations is the unavailability of sufficient

amount of funds with the company as a result of excessive blockage of funds in the trade

credits allowed to the customers of the business.

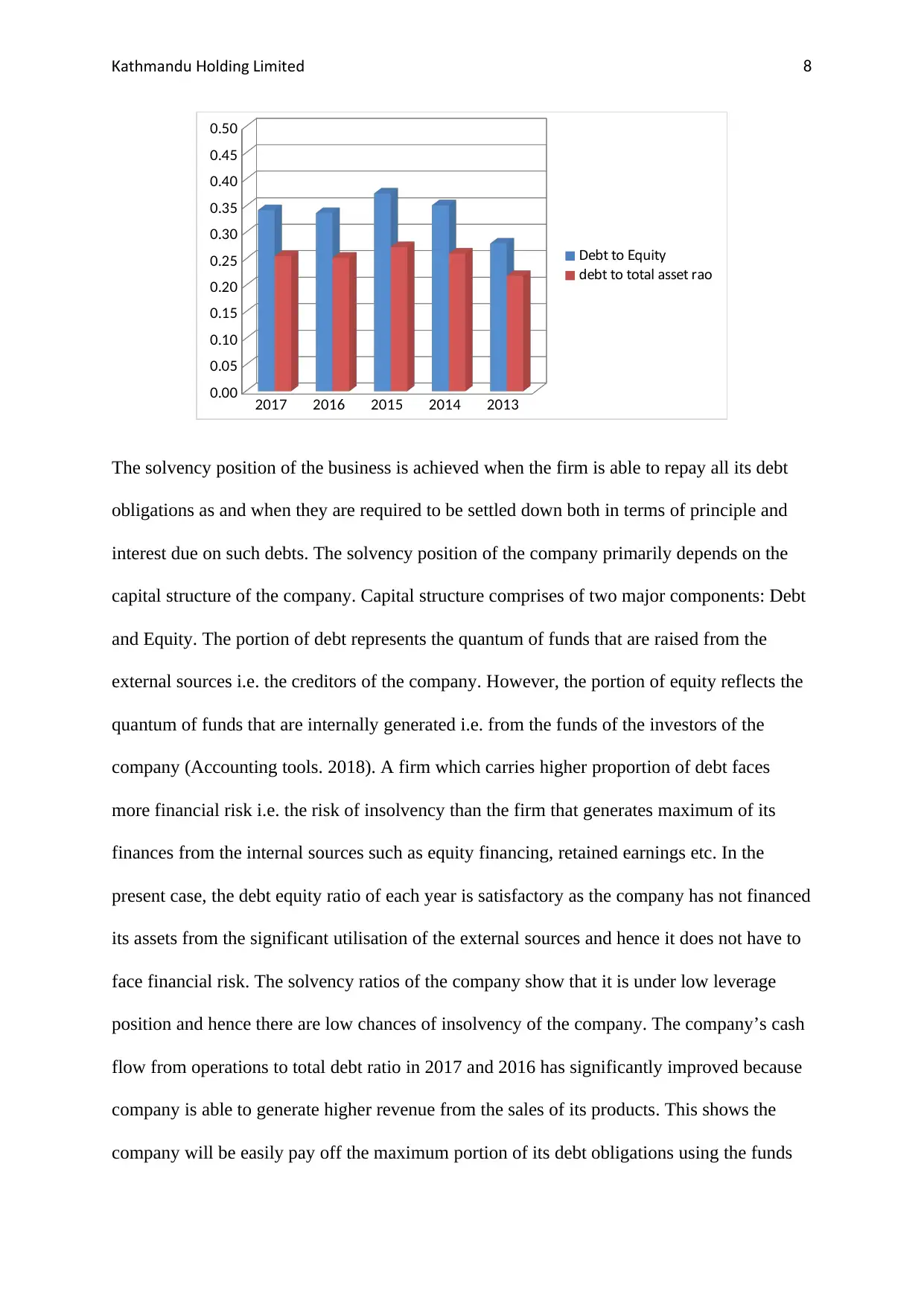

Solvency position (Gearing Ratios)

2017 2016 2015 2014 2013

Leverage Ratio 25.50% 25.20% 27.21% 26.00% 21.80%

Debt To Equity 34.23% 33.68% 37.39% 35.13% 27.88%

Debt To Total Asset Ratio 25.50% 25.20% 27.21% 26.00% 21.80%

Interest Coverage Ratio 28.08 14.31 12.09 13.99 14.38

Cash Flow From Operations To

Total Liabilities 60% 66% 25% 29% 56%

sales but is it not able to collect sufficient cash from the sales made in the particular year

because of its lose trade credit policies. The declining receivable turnover ratio of the

company is a clear indicator of company’s inefficiency towards collecting the amount

receivables for the credit sales made in the year because company is not making required

efforts to convert its credit sales into cash. Due to this, the operating cash cycle of the

company is not maintained effectively and efficiently and leading to weak working capital

management of the company (Kathmandu, 2016). The payable turnover ratio of the company

gauges the speed with which a firm pays offs the amount that is due to its accounts payables

i.e. the suppliers and creditors of the business. In the present case, the accounts payable ratio

is continuously declining since 2013 till 2017 and this shows that the company is not paying

off its trade creditors on timely basis, all the amount due to them for the credit purchases

made from them (Kathmandu, 2017). The declining accounts payable ratio is an indication of

weakening financial position of the business. One of the major reason due to which the

company is unable to meet its trade credit obligations is the unavailability of sufficient

amount of funds with the company as a result of excessive blockage of funds in the trade

credits allowed to the customers of the business.

Solvency position (Gearing Ratios)

2017 2016 2015 2014 2013

Leverage Ratio 25.50% 25.20% 27.21% 26.00% 21.80%

Debt To Equity 34.23% 33.68% 37.39% 35.13% 27.88%

Debt To Total Asset Ratio 25.50% 25.20% 27.21% 26.00% 21.80%

Interest Coverage Ratio 28.08 14.31 12.09 13.99 14.38

Cash Flow From Operations To

Total Liabilities 60% 66% 25% 29% 56%

athmandu olding imitedK H L 8

2017 2016 2015 2014 2013

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

Debt to quityE

debt to total asset ratio

The solvency position of the business is achieved when the firm is able to repay all its debt

obligations as and when they are required to be settled down both in terms of principle and

interest due on such debts. The solvency position of the company primarily depends on the

capital structure of the company. Capital structure comprises of two major components: Debt

and Equity. The portion of debt represents the quantum of funds that are raised from the

external sources i.e. the creditors of the company. However, the portion of equity reflects the

quantum of funds that are internally generated i.e. from the funds of the investors of the

company (Accounting tools. 2018). A firm which carries higher proportion of debt faces

more financial risk i.e. the risk of insolvency than the firm that generates maximum of its

finances from the internal sources such as equity financing, retained earnings etc. In the

present case, the debt equity ratio of each year is satisfactory as the company has not financed

its assets from the significant utilisation of the external sources and hence it does not have to

face financial risk. The solvency ratios of the company show that it is under low leverage

position and hence there are low chances of insolvency of the company. The company’s cash

flow from operations to total debt ratio in 2017 and 2016 has significantly improved because

company is able to generate higher revenue from the sales of its products. This shows the

company will be easily pay off the maximum portion of its debt obligations using the funds

2017 2016 2015 2014 2013

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

Debt to quityE

debt to total asset ratio

The solvency position of the business is achieved when the firm is able to repay all its debt

obligations as and when they are required to be settled down both in terms of principle and

interest due on such debts. The solvency position of the company primarily depends on the

capital structure of the company. Capital structure comprises of two major components: Debt

and Equity. The portion of debt represents the quantum of funds that are raised from the

external sources i.e. the creditors of the company. However, the portion of equity reflects the

quantum of funds that are internally generated i.e. from the funds of the investors of the

company (Accounting tools. 2018). A firm which carries higher proportion of debt faces

more financial risk i.e. the risk of insolvency than the firm that generates maximum of its

finances from the internal sources such as equity financing, retained earnings etc. In the

present case, the debt equity ratio of each year is satisfactory as the company has not financed

its assets from the significant utilisation of the external sources and hence it does not have to

face financial risk. The solvency ratios of the company show that it is under low leverage

position and hence there are low chances of insolvency of the company. The company’s cash

flow from operations to total debt ratio in 2017 and 2016 has significantly improved because

company is able to generate higher revenue from the sales of its products. This shows the

company will be easily pay off the maximum portion of its debt obligations using the funds

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

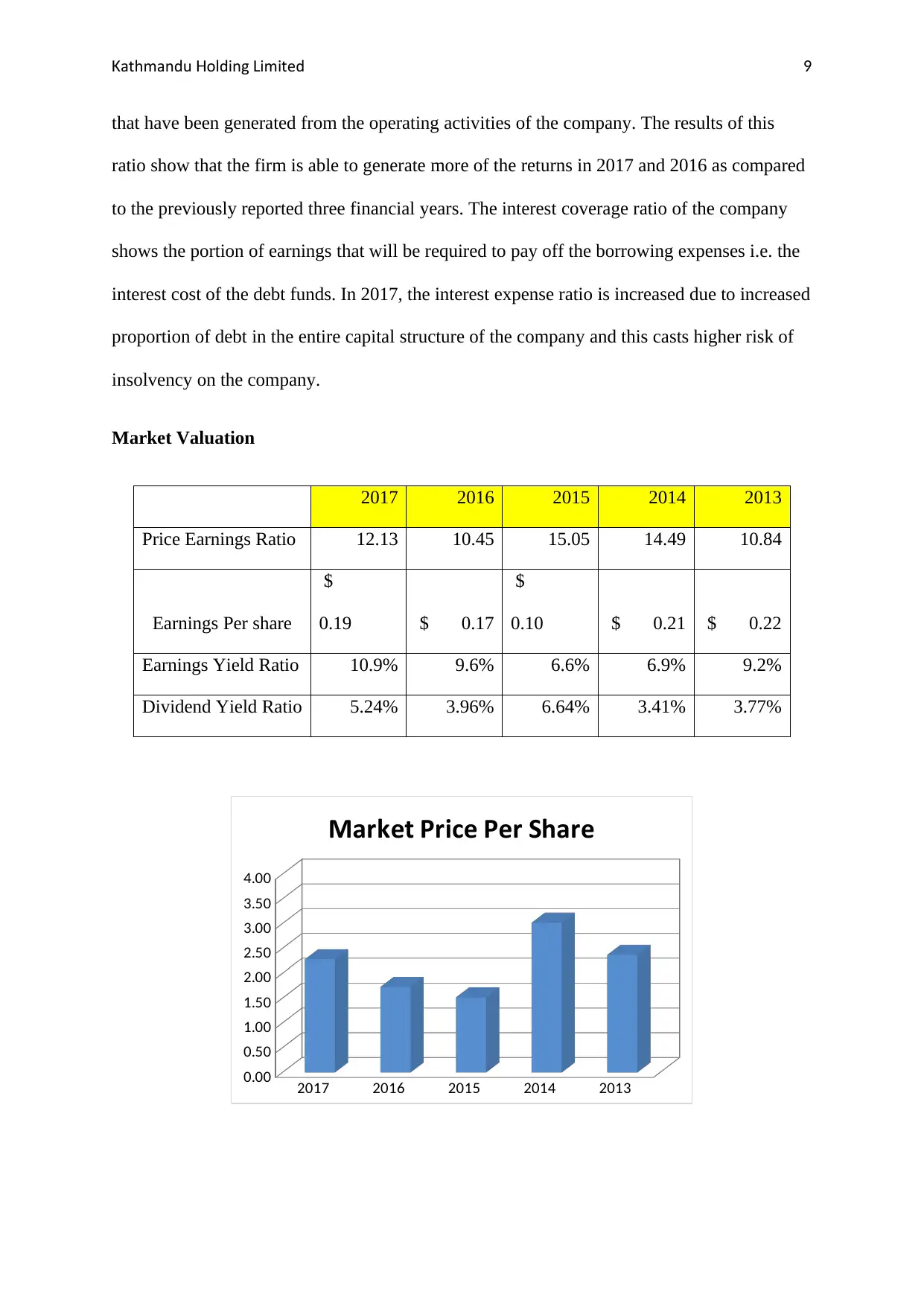

athmandu olding imitedK H L 9

that have been generated from the operating activities of the company. The results of this

ratio show that the firm is able to generate more of the returns in 2017 and 2016 as compared

to the previously reported three financial years. The interest coverage ratio of the company

shows the portion of earnings that will be required to pay off the borrowing expenses i.e. the

interest cost of the debt funds. In 2017, the interest expense ratio is increased due to increased

proportion of debt in the entire capital structure of the company and this casts higher risk of

insolvency on the company.

Market Valuation

2017 2016 2015 2014 2013

Price Earnings Ratio 12.13 10.45 15.05 14.49 10.84

Earnings Per share

$

0.19 $ 0.17

$

0.10 $ 0.21 $ 0.22

Earnings Yield Ratio 10.9% 9.6% 6.6% 6.9% 9.2%

Dividend Yield Ratio 5.24% 3.96% 6.64% 3.41% 3.77%

2017 2016 2015 2014 2013

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Market Price Per Share

that have been generated from the operating activities of the company. The results of this

ratio show that the firm is able to generate more of the returns in 2017 and 2016 as compared

to the previously reported three financial years. The interest coverage ratio of the company

shows the portion of earnings that will be required to pay off the borrowing expenses i.e. the

interest cost of the debt funds. In 2017, the interest expense ratio is increased due to increased

proportion of debt in the entire capital structure of the company and this casts higher risk of

insolvency on the company.

Market Valuation

2017 2016 2015 2014 2013

Price Earnings Ratio 12.13 10.45 15.05 14.49 10.84

Earnings Per share

$

0.19 $ 0.17

$

0.10 $ 0.21 $ 0.22

Earnings Yield Ratio 10.9% 9.6% 6.6% 6.9% 9.2%

Dividend Yield Ratio 5.24% 3.96% 6.64% 3.41% 3.77%

2017 2016 2015 2014 2013

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Market Price Per Share

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

athmandu olding imitedK H L 10

2017 2016 2015 2014 2013

0.00

0.05

0.10

0.15

0.20

0.25

Earnings Per Share

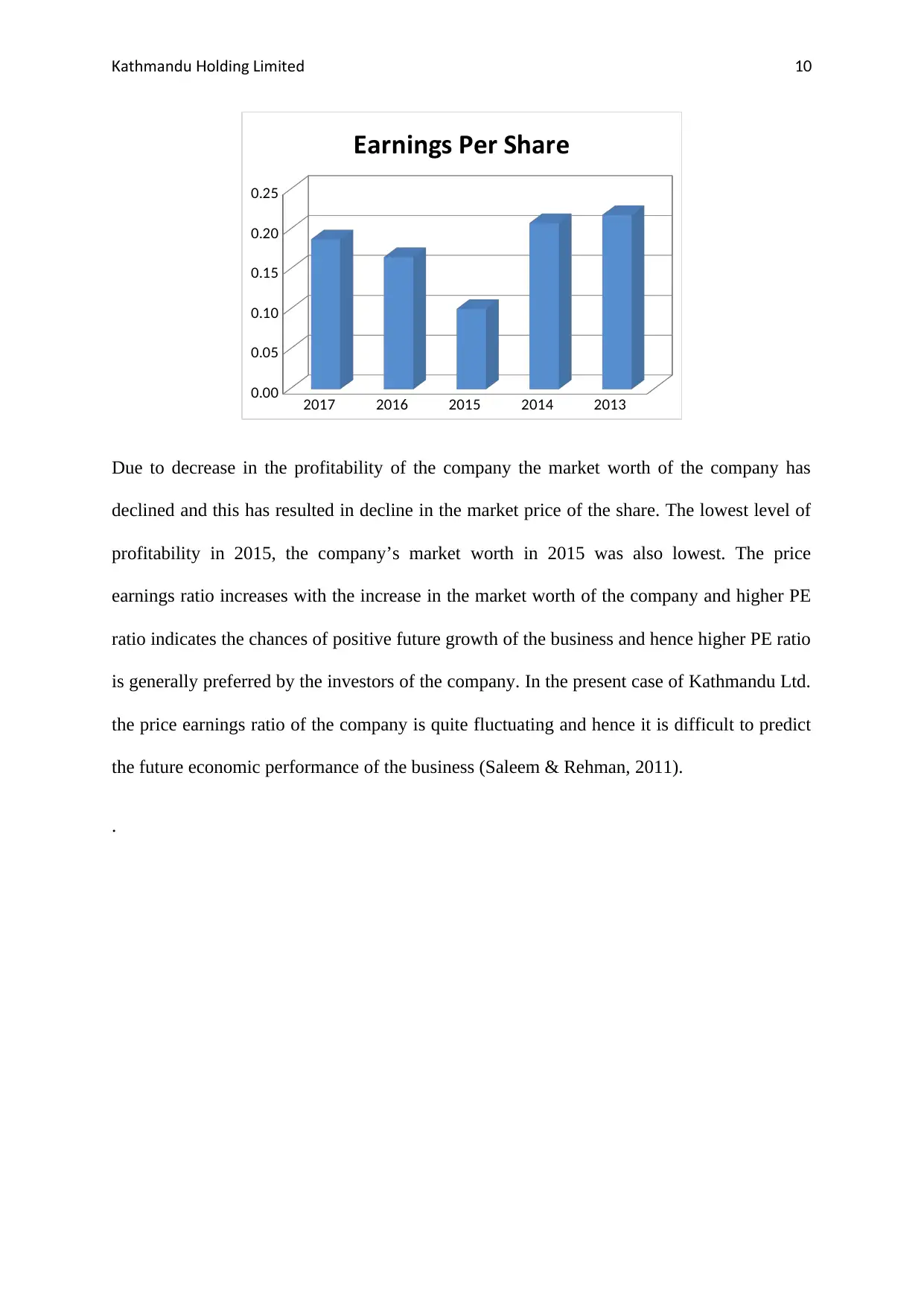

Due to decrease in the profitability of the company the market worth of the company has

declined and this has resulted in decline in the market price of the share. The lowest level of

profitability in 2015, the company’s market worth in 2015 was also lowest. The price

earnings ratio increases with the increase in the market worth of the company and higher PE

ratio indicates the chances of positive future growth of the business and hence higher PE ratio

is generally preferred by the investors of the company. In the present case of Kathmandu Ltd.

the price earnings ratio of the company is quite fluctuating and hence it is difficult to predict

the future economic performance of the business (Saleem & Rehman, 2011).

.

2017 2016 2015 2014 2013

0.00

0.05

0.10

0.15

0.20

0.25

Earnings Per Share

Due to decrease in the profitability of the company the market worth of the company has

declined and this has resulted in decline in the market price of the share. The lowest level of

profitability in 2015, the company’s market worth in 2015 was also lowest. The price

earnings ratio increases with the increase in the market worth of the company and higher PE

ratio indicates the chances of positive future growth of the business and hence higher PE ratio

is generally preferred by the investors of the company. In the present case of Kathmandu Ltd.

the price earnings ratio of the company is quite fluctuating and hence it is difficult to predict

the future economic performance of the business (Saleem & Rehman, 2011).

.

athmandu olding imitedK H L 11

Conclusion and Recommendations:

From the above analysis, it can be said that ratio analysis helps significantly in measuring the

overall financial performance of the business from different possible parameters. Ratio

analysis covers almost every important aspect of the business on which the financial

performance of business depends and helps the company to identify the areas where

significant deficiencies are found. In the present case of Kathmandu Ltd, the company’s

liquidity position has worsened with each passing years subsequent to 2015. The company

must make efforts to manage its current assets in such a way that they are sufficiently

available to meet the short term debt obligations of the business as and when they become

due so as to promote its working capital management. If adequate amount of current account

balance is not available with the business, the company will have to face severe cash crises in

the subsequent years. So, in order to improve the liquidity position of the business,

Kathmandu Ltd. will have to ensure that its trade credit policy is stringent enough to collect

cash from all the trade debtors of the company so that timely payment of trade creditors i.e.

the supplier of the business can be made and also to avoid incurrence of high interest costs on

the credit purchases which amounts to considerable outflow of cash from the business.

Further, the profitability position of the company can be improved further to reach the desired

profitability level (Lee, Lee & Lee, 2009). In order to improve the overall profitability of the

business, the company must focus on the ways that could increase its revenue from sales and

also to those ways that could lead to ultimate cost cutting of the business. The company must

make use of its funds of the shareholders in the most efficient way that allows it to generate

more sales from the business. Further, the company must reduce further the level of its debt

obligations so as to cut down the interest cost which negatively affects the earnings capacity

of the business. The major reason of decline in the market worth of the company is its

declining earnings per share which is resulted from the low profitability position of the

Conclusion and Recommendations:

From the above analysis, it can be said that ratio analysis helps significantly in measuring the

overall financial performance of the business from different possible parameters. Ratio

analysis covers almost every important aspect of the business on which the financial

performance of business depends and helps the company to identify the areas where

significant deficiencies are found. In the present case of Kathmandu Ltd, the company’s

liquidity position has worsened with each passing years subsequent to 2015. The company

must make efforts to manage its current assets in such a way that they are sufficiently

available to meet the short term debt obligations of the business as and when they become

due so as to promote its working capital management. If adequate amount of current account

balance is not available with the business, the company will have to face severe cash crises in

the subsequent years. So, in order to improve the liquidity position of the business,

Kathmandu Ltd. will have to ensure that its trade credit policy is stringent enough to collect

cash from all the trade debtors of the company so that timely payment of trade creditors i.e.

the supplier of the business can be made and also to avoid incurrence of high interest costs on

the credit purchases which amounts to considerable outflow of cash from the business.

Further, the profitability position of the company can be improved further to reach the desired

profitability level (Lee, Lee & Lee, 2009). In order to improve the overall profitability of the

business, the company must focus on the ways that could increase its revenue from sales and

also to those ways that could lead to ultimate cost cutting of the business. The company must

make use of its funds of the shareholders in the most efficient way that allows it to generate

more sales from the business. Further, the company must reduce further the level of its debt

obligations so as to cut down the interest cost which negatively affects the earnings capacity

of the business. The major reason of decline in the market worth of the company is its

declining earnings per share which is resulted from the low profitability position of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.