Key Audit Matter in Telecommunication

VerifiedAdded on 2022/11/23

|13

|3657

|201

AI Summary

This paper evaluates and analyzes the key audit matters (KAM) and their inclusion in the independent audit reports while focusing on the telecommunication industry. It highlights major auditing firms and their role in big organizations, including those that collapsed, causing a meltdown in financial markets. Key audit matters are identified and their benefits to organizations listed.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Key Audit Matter in Telecommunication

Abstract

The main purpose of this paper is to evaluate and analyze the key audit matters (KAM) and their

inclusion in the independent audit reports as required by the International Auditing Assurance

standards board (IAASB) ,the Public company accounting oversight board (PCAOB) and other

international audit regulatory bodies while focusing on the telecommunication industry. The

paper examines the changes that have been made over the years by regulatory bodies that govern

auditing in entities to improve the work done by independent auditors and to boost the

confidence of investors. Different regulations like the Sarbanes Oxley act are mentioned, but the

significant discussion is based on the new international auditing standard ISA 701. What it is and

its benefits in entities. It highlights major auditing firms and their role in big organizations,

including those that collapsed, causing a meltdown in financial markets. This paper also gives an

insight into what happened to Lehman's brothers that led to its liquidation. Key audit matters are

identified and their benefits to organizations listed.

Contents

Abstract

The main purpose of this paper is to evaluate and analyze the key audit matters (KAM) and their

inclusion in the independent audit reports as required by the International Auditing Assurance

standards board (IAASB) ,the Public company accounting oversight board (PCAOB) and other

international audit regulatory bodies while focusing on the telecommunication industry. The

paper examines the changes that have been made over the years by regulatory bodies that govern

auditing in entities to improve the work done by independent auditors and to boost the

confidence of investors. Different regulations like the Sarbanes Oxley act are mentioned, but the

significant discussion is based on the new international auditing standard ISA 701. What it is and

its benefits in entities. It highlights major auditing firms and their role in big organizations,

including those that collapsed, causing a meltdown in financial markets. This paper also gives an

insight into what happened to Lehman's brothers that led to its liquidation. Key audit matters are

identified and their benefits to organizations listed.

Contents

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Abstract............................................................................................................................................1

Introduction......................................................................................................................................1

The Big four.................................................................................................................................2

ISA 701........................................................................................................................................3

Failure of the Lehman brothers....................................................................................................4

Key Audit Matters in the telecommunication industry................................................................5

Determining KAM...................................................................................................................6

KAM in Testra and TPG Telecom companies.............................................................................6

Revenue Recognition...................................................................................................................7

Addressing revenue recognition as a key audit matter.............................................................7

Goodwill...................................................................................................................................8

The Classification Lease arrangement with China tower.........................................................9

Depreciable useful lives of the plant......................................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Introduction

Introduction......................................................................................................................................1

The Big four.................................................................................................................................2

ISA 701........................................................................................................................................3

Failure of the Lehman brothers....................................................................................................4

Key Audit Matters in the telecommunication industry................................................................5

Determining KAM...................................................................................................................6

KAM in Testra and TPG Telecom companies.............................................................................6

Revenue Recognition...................................................................................................................7

Addressing revenue recognition as a key audit matter.............................................................7

Goodwill...................................................................................................................................8

The Classification Lease arrangement with China tower.........................................................9

Depreciable useful lives of the plant......................................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Introduction

In the past fifty years, there have been fundamental changes in the responsibilities of auditors

about what they should and should not include in their audit reports. These changes have been

influenced by the global economic crisis and collapsing of big organizations around the world.

As a result, the responsibilities of auditors have been reviewed to enable users to understand the

financial statements of organizations. Before, audit reports majored on fraud detection and

errors, but in recent years, it has evolved to the provision of valuable information. Auditors now

provide services that have more value to their clients by including risks in the business, offering

guidance to the risks identified and reporting internal failures.

It is mandatory for auditors to be clear in different matters by touching on technology issues,

legal aspects, and the financial part of the business. The recent corporate failures that have been

linked to previous audit reports have made users, investors, and clients to put so much pressure

on auditors resulting in an introduction of new auditing standards.

In the year 2002, the Public Company Accounting Oversight Board was created, and the

Sarbanes Oxley Act (SOX) was introduced to guide auditors, but the SOX act did not do much to

prevent corporate failures that have been occurring in recent economic crisis. ISA 701 act was

enacted following many accounting irregularities in business to restore the confidence of

investors and also enhance reliability in financial reports by improving governance in corporate

systems. Therefore, governments and regulators are once again focusing their attention on this

profession and are more closely examining the systemic risk associated with the role of the

auditor.

The Big Four

With the rise of many organizations in the world, every company competes to hire the best audit

firm to do their audit report, and among the many audit firms in the world, those have positioned

about what they should and should not include in their audit reports. These changes have been

influenced by the global economic crisis and collapsing of big organizations around the world.

As a result, the responsibilities of auditors have been reviewed to enable users to understand the

financial statements of organizations. Before, audit reports majored on fraud detection and

errors, but in recent years, it has evolved to the provision of valuable information. Auditors now

provide services that have more value to their clients by including risks in the business, offering

guidance to the risks identified and reporting internal failures.

It is mandatory for auditors to be clear in different matters by touching on technology issues,

legal aspects, and the financial part of the business. The recent corporate failures that have been

linked to previous audit reports have made users, investors, and clients to put so much pressure

on auditors resulting in an introduction of new auditing standards.

In the year 2002, the Public Company Accounting Oversight Board was created, and the

Sarbanes Oxley Act (SOX) was introduced to guide auditors, but the SOX act did not do much to

prevent corporate failures that have been occurring in recent economic crisis. ISA 701 act was

enacted following many accounting irregularities in business to restore the confidence of

investors and also enhance reliability in financial reports by improving governance in corporate

systems. Therefore, governments and regulators are once again focusing their attention on this

profession and are more closely examining the systemic risk associated with the role of the

auditor.

The Big Four

With the rise of many organizations in the world, every company competes to hire the best audit

firm to do their audit report, and among the many audit firms in the world, those have positioned

themselves as market challenges by becoming the biggest accounting firms in the world. These

firms are known as the Big Four; Deloitte, Ernst & Young (E&Y), PriceWaterhouse Coopers

(PwC) and Klynyeld Peat Marwick Goerdeler (KPMG). They offer accounting and auditing

services, including consultancy and external audit. After Arthur Andersen being accused of

playing a role in the fall of Enron, regulators saw the need to revise the old regulations that

govern auditors and come up with a way to regulate their audit reports to improve impartiality

and transparency, and that is how ISA 701 was introduced (DeZoort and Harrison, 2018)

ISA 701

A new auditing standard ISA 701 known as key Audit Matters has been introduced to regulate

independent audit reports and ensure future audit failures are prevented. The standard will

restrict independent auditors, especially those who provide service to organizations that are

registered in foreign jurisdictions and listed in foreign security exchange. The European, U.S and

Japanese regulators have come up with reforms that will require foreign audit firms or foreign

auditors to register and comply with regulations in each jurisdiction if they want to audit in any

of the regulated firms. Each country has different regulations that must be adhered to (Masdor

and Shamsuddin, 2018)

According to Altawalbeh and Alhajaya (2019), there has been a retaliation response

internationally by other regulators that could easily lead to a disaster in the corporate world and

the audit profession around the world if not looked into and addressed properly. The new

regulations that might be seen by others as over-regulation could also contribute to corporate

failures since the transaction of firms have become voluminous, thus increasing the filing

requirement. This has led to the quality of the work done by auditors being affected because they

firms are known as the Big Four; Deloitte, Ernst & Young (E&Y), PriceWaterhouse Coopers

(PwC) and Klynyeld Peat Marwick Goerdeler (KPMG). They offer accounting and auditing

services, including consultancy and external audit. After Arthur Andersen being accused of

playing a role in the fall of Enron, regulators saw the need to revise the old regulations that

govern auditors and come up with a way to regulate their audit reports to improve impartiality

and transparency, and that is how ISA 701 was introduced (DeZoort and Harrison, 2018)

ISA 701

A new auditing standard ISA 701 known as key Audit Matters has been introduced to regulate

independent audit reports and ensure future audit failures are prevented. The standard will

restrict independent auditors, especially those who provide service to organizations that are

registered in foreign jurisdictions and listed in foreign security exchange. The European, U.S and

Japanese regulators have come up with reforms that will require foreign audit firms or foreign

auditors to register and comply with regulations in each jurisdiction if they want to audit in any

of the regulated firms. Each country has different regulations that must be adhered to (Masdor

and Shamsuddin, 2018)

According to Altawalbeh and Alhajaya (2019), there has been a retaliation response

internationally by other regulators that could easily lead to a disaster in the corporate world and

the audit profession around the world if not looked into and addressed properly. The new

regulations that might be seen by others as over-regulation could also contribute to corporate

failures since the transaction of firms have become voluminous, thus increasing the filing

requirement. This has led to the quality of the work done by auditors being affected because they

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

don’t have enough time to evaluate and understand the financial information they receive from

the organization. The regulations are mandatory (Jermakowicz, Epstein, and Ramamoorti, 2018)

Failure of the Lehman Brothers

The liquidation of Lehman brothers was ordered by the Swiss Financial market supervisory

authority as Pricewatercoopers (PwC) was appointed to be the liquidators of the bankruptcy.

PwC undertook proceedings to implement a way of returning the assets, safeguarding the

company's interests, handling failed trades, and communicating with the bank creditors, among

other issues. Even though the Liquidation of Lehman Holdings has not been completed yet,

James W Giddens, the lawyer in charge says it might end this year. It is 11 years since the

company filed for bankruptcy leading to a financial crisis globally. Lehman Holdings Inc. was

among Wall Street's top five investment bank before its demise in 2008. Secured creditors and

clients have been paid in full while unsecured creditors have been paid about $ 9 billion. Had key

audit matters existed then, maybe Lehman’s failure could have been avoided (Schiereck, Kiesel,

and Kolaric, 2016)

Ernst & young was alleged to have played a role in the fall of Lehman for failing to report any

misstatements in their audit report. E & Y helped Lehman to hide its financial situation by aiding

them to remove billions of dollars of fixed income securities from their balance sheet to come

clean by deceiving the public about the bank's condition. E & Y was the official auditors of

Lehman from the year 2001 to 2008. In defense to the allegations made, E & Y claimed that the

transactions were recorded according to the Generally Accepted Accounting Principles that were

in place then thus justifying their actions, but their claim was faulted by the bankruptcy

examiners report that claimed the auditor, did not audit the transactions in question. Lehman

manipulated the transactions internally to manage the balance of the sheet. All these audit

the organization. The regulations are mandatory (Jermakowicz, Epstein, and Ramamoorti, 2018)

Failure of the Lehman Brothers

The liquidation of Lehman brothers was ordered by the Swiss Financial market supervisory

authority as Pricewatercoopers (PwC) was appointed to be the liquidators of the bankruptcy.

PwC undertook proceedings to implement a way of returning the assets, safeguarding the

company's interests, handling failed trades, and communicating with the bank creditors, among

other issues. Even though the Liquidation of Lehman Holdings has not been completed yet,

James W Giddens, the lawyer in charge says it might end this year. It is 11 years since the

company filed for bankruptcy leading to a financial crisis globally. Lehman Holdings Inc. was

among Wall Street's top five investment bank before its demise in 2008. Secured creditors and

clients have been paid in full while unsecured creditors have been paid about $ 9 billion. Had key

audit matters existed then, maybe Lehman’s failure could have been avoided (Schiereck, Kiesel,

and Kolaric, 2016)

Ernst & young was alleged to have played a role in the fall of Lehman for failing to report any

misstatements in their audit report. E & Y helped Lehman to hide its financial situation by aiding

them to remove billions of dollars of fixed income securities from their balance sheet to come

clean by deceiving the public about the bank's condition. E & Y was the official auditors of

Lehman from the year 2001 to 2008. In defense to the allegations made, E & Y claimed that the

transactions were recorded according to the Generally Accepted Accounting Principles that were

in place then thus justifying their actions, but their claim was faulted by the bankruptcy

examiners report that claimed the auditor, did not audit the transactions in question. Lehman

manipulated the transactions internally to manage the balance of the sheet. All these audit

mishaps led to the introduction of better auditing standards to govern auditors. With these new

regulations in place, auditors are forced to be competent by giving sufficient information in their

reports something that was lacking than in the Lehman’s brothers issue (Beccar et al., 2017)

Key Audit Matters in the telecommunication industry

According to Segal (2017), key audit matters (KAM) are the most important matters according to

the auditor’s professional judgment included in the audit report of the current year. The auditor is

supposed to communicate them to those charged with governance as needed in all listed

companies by the international auditing standard (ISA). Auditors are required to give specific

and relevant information on the entity in their reports to help investors, internal auditors,

customers and those charged with governance to understand key aspects in the financial

statements (Kachelmeier, Schmidt, and Valentine, 2017)

The key audit matters (KAM) in audit reports are meant to highlight crucial matters that are

termed as significant to increase the users and public confidence in entities. Apart from including

key audit matters, the auditors still have a responsibility to do a thorough assessment of possible

risks and come up with an appropriate way to address those risks. Regulators, investors, and

accounting firms have received this concept positively with many auditors across the world

implementing it by including it in their reports Mactavish, McCracken, and Schmidt (2018)

Including the key audit matters in audit reports increases transparency, help users to engage with

those charged with governance on matters that relate to the entity, upgrades the quality of work

done by editors and give investors a chance to focus on issues in the financial statements which

are subject to management judgment (Gaynor et al., 2016)

regulations in place, auditors are forced to be competent by giving sufficient information in their

reports something that was lacking than in the Lehman’s brothers issue (Beccar et al., 2017)

Key Audit Matters in the telecommunication industry

According to Segal (2017), key audit matters (KAM) are the most important matters according to

the auditor’s professional judgment included in the audit report of the current year. The auditor is

supposed to communicate them to those charged with governance as needed in all listed

companies by the international auditing standard (ISA). Auditors are required to give specific

and relevant information on the entity in their reports to help investors, internal auditors,

customers and those charged with governance to understand key aspects in the financial

statements (Kachelmeier, Schmidt, and Valentine, 2017)

The key audit matters (KAM) in audit reports are meant to highlight crucial matters that are

termed as significant to increase the users and public confidence in entities. Apart from including

key audit matters, the auditors still have a responsibility to do a thorough assessment of possible

risks and come up with an appropriate way to address those risks. Regulators, investors, and

accounting firms have received this concept positively with many auditors across the world

implementing it by including it in their reports Mactavish, McCracken, and Schmidt (2018)

Including the key audit matters in audit reports increases transparency, help users to engage with

those charged with governance on matters that relate to the entity, upgrades the quality of work

done by editors and give investors a chance to focus on issues in the financial statements which

are subject to management judgment (Gaynor et al., 2016)

Determining key audit matters (KAM)

To give relevant information, auditors should ensure the key audit matter listed are specific to the

entity. For a matter to qualify as KAM, the auditor must consider areas where significant risks

have been identified according to the ISA 315(revised), the auditors judgment to places in the

financial statement that involve accounting estimates identified to have high estimation

uncertainty and how significant transactions that occurred during the year will affect the audit

(Velte, 2018)

Auditors should also consider the communication they have with those charged with governance

concerning matters. Which are likely to qualify as key especially on complex matters; how

important the matter is to the users, policies that relate to the matter compared to policies in other

entities in the same industry, nature of uncorrected and corrected misstatements due to fraud and

the effort needed to address the matter (Ahmed, Haji and Anifowose, 2016)

KAM in Telstra and TPG telecom

The report gives a fair view of the financial statements of the Telestra and TPG

telecommunication companies according to the companies’ policies and the international

auditing standards. One key audit matter is identified and addressed in each company separately.

Key audit matter Telestra telecom How it was addressed

Revenue recognition

To give relevant information, auditors should ensure the key audit matter listed are specific to the

entity. For a matter to qualify as KAM, the auditor must consider areas where significant risks

have been identified according to the ISA 315(revised), the auditors judgment to places in the

financial statement that involve accounting estimates identified to have high estimation

uncertainty and how significant transactions that occurred during the year will affect the audit

(Velte, 2018)

Auditors should also consider the communication they have with those charged with governance

concerning matters. Which are likely to qualify as key especially on complex matters; how

important the matter is to the users, policies that relate to the matter compared to policies in other

entities in the same industry, nature of uncorrected and corrected misstatements due to fraud and

the effort needed to address the matter (Ahmed, Haji and Anifowose, 2016)

KAM in Telstra and TPG telecom

The report gives a fair view of the financial statements of the Telestra and TPG

telecommunication companies according to the companies’ policies and the international

auditing standards. One key audit matter is identified and addressed in each company separately.

Key audit matter Telestra telecom How it was addressed

Revenue recognition

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

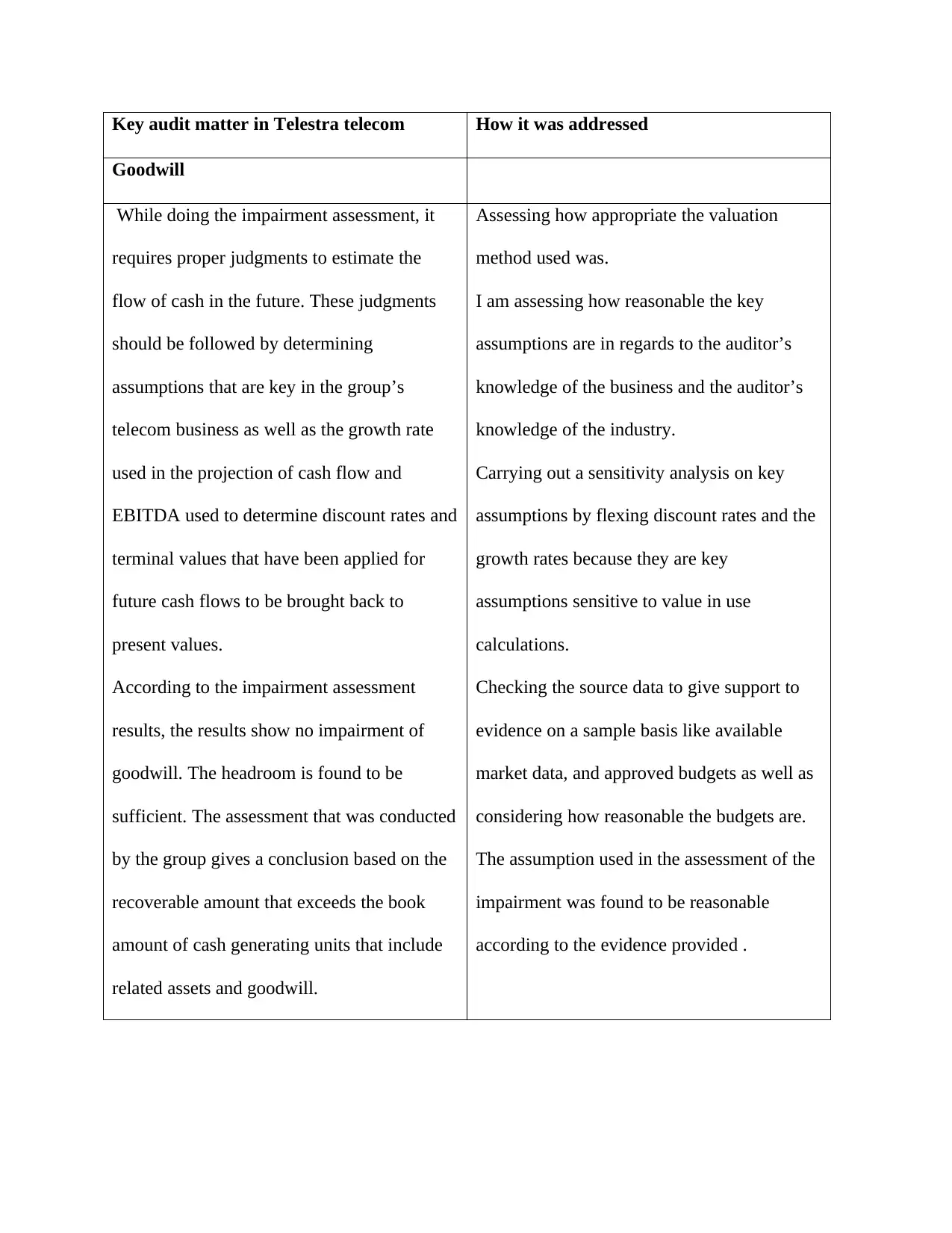

Key audit matter in Telestra telecom How it was addressed

Goodwill

While doing the impairment assessment, it

requires proper judgments to estimate the

flow of cash in the future. These judgments

should be followed by determining

assumptions that are key in the group’s

telecom business as well as the growth rate

used in the projection of cash flow and

EBITDA used to determine discount rates and

terminal values that have been applied for

future cash flows to be brought back to

present values.

According to the impairment assessment

results, the results show no impairment of

goodwill. The headroom is found to be

sufficient. The assessment that was conducted

by the group gives a conclusion based on the

recoverable amount that exceeds the book

amount of cash generating units that include

related assets and goodwill.

Assessing how appropriate the valuation

method used was.

I am assessing how reasonable the key

assumptions are in regards to the auditor’s

knowledge of the business and the auditor’s

knowledge of the industry.

Carrying out a sensitivity analysis on key

assumptions by flexing discount rates and the

growth rates because they are key

assumptions sensitive to value in use

calculations.

Checking the source data to give support to

evidence on a sample basis like available

market data, and approved budgets as well as

considering how reasonable the budgets are.

The assumption used in the assessment of the

impairment was found to be reasonable

according to the evidence provided .

Goodwill

While doing the impairment assessment, it

requires proper judgments to estimate the

flow of cash in the future. These judgments

should be followed by determining

assumptions that are key in the group’s

telecom business as well as the growth rate

used in the projection of cash flow and

EBITDA used to determine discount rates and

terminal values that have been applied for

future cash flows to be brought back to

present values.

According to the impairment assessment

results, the results show no impairment of

goodwill. The headroom is found to be

sufficient. The assessment that was conducted

by the group gives a conclusion based on the

recoverable amount that exceeds the book

amount of cash generating units that include

related assets and goodwill.

Assessing how appropriate the valuation

method used was.

I am assessing how reasonable the key

assumptions are in regards to the auditor’s

knowledge of the business and the auditor’s

knowledge of the industry.

Carrying out a sensitivity analysis on key

assumptions by flexing discount rates and the

growth rates because they are key

assumptions sensitive to value in use

calculations.

Checking the source data to give support to

evidence on a sample basis like available

market data, and approved budgets as well as

considering how reasonable the budgets are.

The assumption used in the assessment of the

impairment was found to be reasonable

according to the evidence provided .

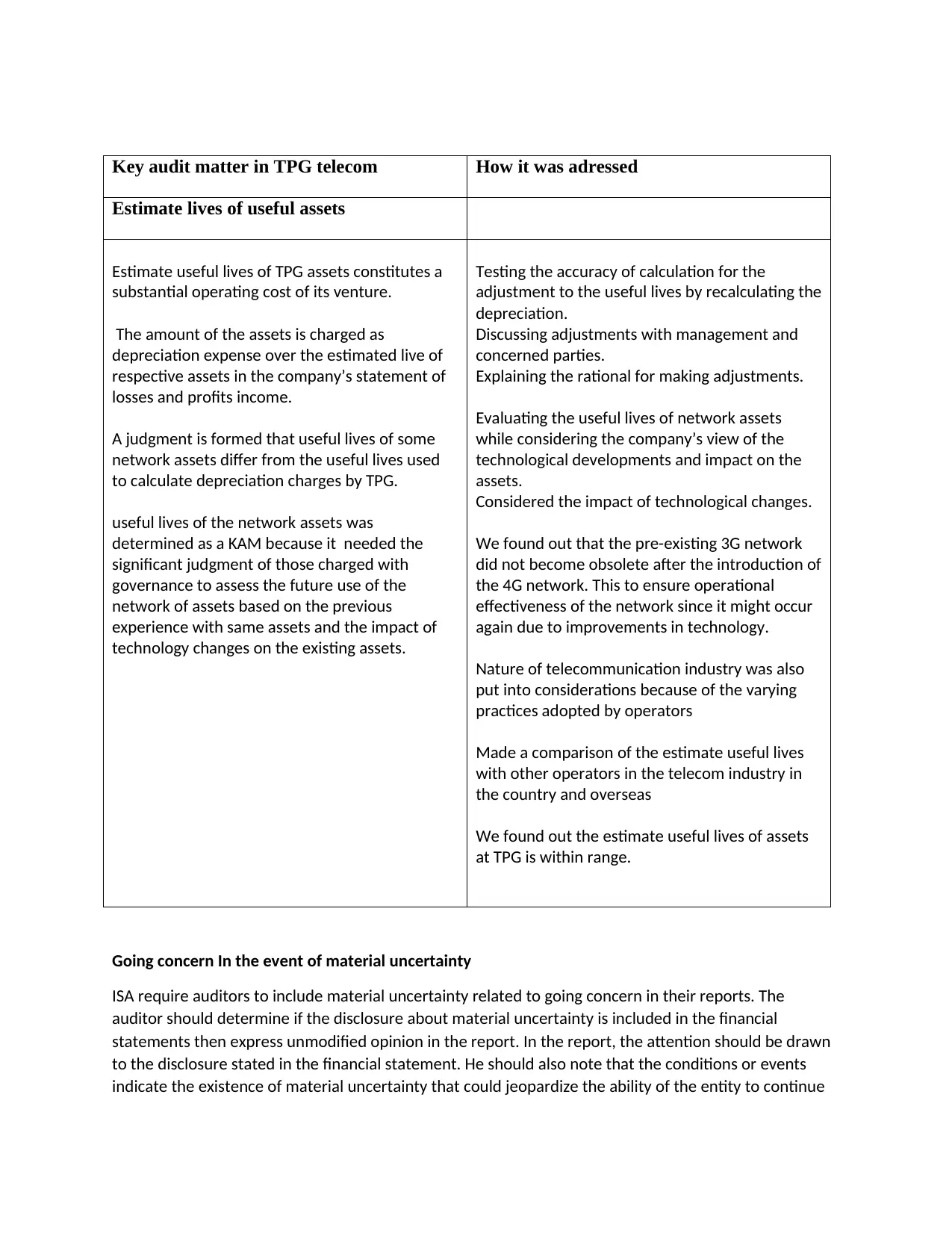

Key audit matter in TPG telecom How it was adressed

Estimate lives of useful assets

Estimate useful lives of TPG assets constitutes a

substantial operating cost of its venture.

The amount of the assets is charged as

depreciation expense over the estimated live of

respective assets in the company’s statement of

losses and profits income.

A judgment is formed that useful lives of some

network assets differ from the useful lives used

to calculate depreciation charges by TPG.

useful lives of the network assets was

determined as a KAM because it needed the

significant judgment of those charged with

governance to assess the future use of the

network of assets based on the previous

experience with same assets and the impact of

technology changes on the existing assets.

Testing the accuracy of calculation for the

adjustment to the useful lives by recalculating the

depreciation.

Discussing adjustments with management and

concerned parties.

Explaining the rational for making adjustments.

Evaluating the useful lives of network assets

while considering the company’s view of the

technological developments and impact on the

assets.

Considered the impact of technological changes.

We found out that the pre-existing 3G network

did not become obsolete after the introduction of

the 4G network. This to ensure operational

effectiveness of the network since it might occur

again due to improvements in technology.

Nature of telecommunication industry was also

put into considerations because of the varying

practices adopted by operators

Made a comparison of the estimate useful lives

with other operators in the telecom industry in

the country and overseas

We found out the estimate useful lives of assets

at TPG is within range.

Going concern In the event of material uncertainty

ISA require auditors to include material uncertainty related to going concern in their reports. The

auditor should determine if the disclosure about material uncertainty is included in the financial

statements then express unmodified opinion in the report. In the report, the attention should be drawn

to the disclosure stated in the financial statement. He should also note that the conditions or events

indicate the existence of material uncertainty that could jeopardize the ability of the entity to continue

Estimate lives of useful assets

Estimate useful lives of TPG assets constitutes a

substantial operating cost of its venture.

The amount of the assets is charged as

depreciation expense over the estimated live of

respective assets in the company’s statement of

losses and profits income.

A judgment is formed that useful lives of some

network assets differ from the useful lives used

to calculate depreciation charges by TPG.

useful lives of the network assets was

determined as a KAM because it needed the

significant judgment of those charged with

governance to assess the future use of the

network of assets based on the previous

experience with same assets and the impact of

technology changes on the existing assets.

Testing the accuracy of calculation for the

adjustment to the useful lives by recalculating the

depreciation.

Discussing adjustments with management and

concerned parties.

Explaining the rational for making adjustments.

Evaluating the useful lives of network assets

while considering the company’s view of the

technological developments and impact on the

assets.

Considered the impact of technological changes.

We found out that the pre-existing 3G network

did not become obsolete after the introduction of

the 4G network. This to ensure operational

effectiveness of the network since it might occur

again due to improvements in technology.

Nature of telecommunication industry was also

put into considerations because of the varying

practices adopted by operators

Made a comparison of the estimate useful lives

with other operators in the telecom industry in

the country and overseas

We found out the estimate useful lives of assets

at TPG is within range.

Going concern In the event of material uncertainty

ISA require auditors to include material uncertainty related to going concern in their reports. The

auditor should determine if the disclosure about material uncertainty is included in the financial

statements then express unmodified opinion in the report. In the report, the attention should be drawn

to the disclosure stated in the financial statement. He should also note that the conditions or events

indicate the existence of material uncertainty that could jeopardize the ability of the entity to continue

as a going concern. He should also state that his opinion regarding the matter is not modified (Bepari

and Mollik, 2015)

If there is no adequate disclosure about material uncertainty, the auditor should express a diverse

opinion in the basis for qualified opinion depending on the circumstance. In this case, he should state

the existence of material uncertainty related to going concern and its inadequate disclosure in financial

statements. An auditor can also express a disclaimer of opinion in the event where there is disclosure of

multiple uncertainties significant to the financial statements.

According to Ramanna (2015) when there is a going concern on the entity, the auditor should provide

assurance about the going concern of the entity. This should be presented in the financial statements

based on assumption that the company will be a going concern. This could mean the entity being able to

realize its assets and settle its liabilities .for an auditor to express his opinion on an entity to continue as

a going concern, he must comply with ISA 570 that states the responsibilities of the auditor which

include communicating with those charged with governance and going through the entity’s budgets and

cash flows among other roles. Auditors should consider business and market conditions and other

relevant risks in order to give an opinion on the company’s going concern. According to ISA 700, the

auditor is required to be confident about the company’s going concern to give an unmodified opinion

(Al‐Shaer and Zaman, 2018)

Conclusion

The introduction of the new international auditing standard ISA 701, known as Key audit matters

is the solution to preventing fraudulent acts in organizations and improving the quality of work

done by independent auditors. Their inclusion in audit reports encourage transparency in entities

and help the investors to understand the financial statements better. A proper way is devised to

address any significant risk identified in the report, which if not handled well, could lead to

failure. These regulations are a way to go as they play a major role in preventing the collapse of

big firms that could lead to a financial crisis.

and Mollik, 2015)

If there is no adequate disclosure about material uncertainty, the auditor should express a diverse

opinion in the basis for qualified opinion depending on the circumstance. In this case, he should state

the existence of material uncertainty related to going concern and its inadequate disclosure in financial

statements. An auditor can also express a disclaimer of opinion in the event where there is disclosure of

multiple uncertainties significant to the financial statements.

According to Ramanna (2015) when there is a going concern on the entity, the auditor should provide

assurance about the going concern of the entity. This should be presented in the financial statements

based on assumption that the company will be a going concern. This could mean the entity being able to

realize its assets and settle its liabilities .for an auditor to express his opinion on an entity to continue as

a going concern, he must comply with ISA 570 that states the responsibilities of the auditor which

include communicating with those charged with governance and going through the entity’s budgets and

cash flows among other roles. Auditors should consider business and market conditions and other

relevant risks in order to give an opinion on the company’s going concern. According to ISA 700, the

auditor is required to be confident about the company’s going concern to give an unmodified opinion

(Al‐Shaer and Zaman, 2018)

Conclusion

The introduction of the new international auditing standard ISA 701, known as Key audit matters

is the solution to preventing fraudulent acts in organizations and improving the quality of work

done by independent auditors. Their inclusion in audit reports encourage transparency in entities

and help the investors to understand the financial statements better. A proper way is devised to

address any significant risk identified in the report, which if not handled well, could lead to

failure. These regulations are a way to go as they play a major role in preventing the collapse of

big firms that could lead to a financial crisis.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

References

Ahmed Haji, A. and Anifowose, M., 2016. Audit committee and integrated reporting practice:

does internal assurance matter?. Managerial Auditing Journal, 31(8/9), pp.915-948.

Al‐Shaer, H. and Zaman, M., 2018. Credibility of sustainability reports: The contribution of

audit committees. Business Strategy and the Environment, 27(7), pp.973-986.

Altawalbeh, M.A.F. and Alhajaya, M.E.S., 2019. The Investors Reaction to the Disclosure of

Key Audit Matters: Empirical Evidence from Jordan. International Business Research, 12(3),

pp.50-57.

Beccar-Varela, M.P., Mariani, M.C., Tweneboah, O.K. and Florescu, I., 2017. Analysis of the

Lehman Brothers collapse and the Flash Crash event by applying wavelets

methodologies. Physica A: Statistical Mechanics and its Applications, 474, pp.162-171.

Bepari, M.K. and Mollik, A.T., 2015. Effect of audit quality and accounting and finance

backgrounds of audit committee members on firms’ compliance with IFRS for goodwill

impairment testing. Journal of Applied Accounting Research, 16(2), pp.196-220.

Ahmed Haji, A. and Anifowose, M., 2016. Audit committee and integrated reporting practice:

does internal assurance matter?. Managerial Auditing Journal, 31(8/9), pp.915-948.

Al‐Shaer, H. and Zaman, M., 2018. Credibility of sustainability reports: The contribution of

audit committees. Business Strategy and the Environment, 27(7), pp.973-986.

Altawalbeh, M.A.F. and Alhajaya, M.E.S., 2019. The Investors Reaction to the Disclosure of

Key Audit Matters: Empirical Evidence from Jordan. International Business Research, 12(3),

pp.50-57.

Beccar-Varela, M.P., Mariani, M.C., Tweneboah, O.K. and Florescu, I., 2017. Analysis of the

Lehman Brothers collapse and the Flash Crash event by applying wavelets

methodologies. Physica A: Statistical Mechanics and its Applications, 474, pp.162-171.

Bepari, M.K. and Mollik, A.T., 2015. Effect of audit quality and accounting and finance

backgrounds of audit committee members on firms’ compliance with IFRS for goodwill

impairment testing. Journal of Applied Accounting Research, 16(2), pp.196-220.

DeZoort, F.T. and Harrison, P.D., 2018. Understanding auditors’ sense of responsibility for

detecting fraud within organizations. Journal of Business Ethics, 149(4), pp.857-874.

Drew, J., and Dollery, B., 2015. Inconsistent depreciation practice and public policymaking:

Local government reform in New South Wales. Australian Accounting Review, 25(1), pp.28-37.

Gaynor, L.M., Kelton, A.S., Mercer, M., and Yohn, T.L., 2016. Understanding the relation

between financial reportiInaam, Z. and Khamoussi, H., 2016. Audit committee effectiveness,

audit quality and earnings management: a meta-analysis. International Journal of Law and

Management, 58(2), pp.179-196.ng quality and audit quality. Auditing: A Journal of Practice &

Theory, 35(4), pp.1-22.

Jermakowicz, E.K., Epstein, B.J. and Ramamoorti, S., 2018. CAM versus KAM-A Distinction

without a Difference?: Making Judgments in Reporting Critical Audit Matters. The CPA

Journal, 88(2), pp.34-40.

Kachelmeier, S.J., Schmidt, J.J. and Valentine, K., 2017. The disclaimer effect of disclosing

critical audit matters in the auditor’s report. Working paper.

Mactavish, C., McCracken, S. and Schmidt, R.N., 2018. External Auditors' Judgment and

Decision Making: An Audit Process Task Analysis. Accounting Perspectives, 17(3), pp.387-426.

Masdor, N. and Shamsuddin, A., 2018. The Implementation of ISA 701-Key Audit Matters: A

Review. Global Business & Management Research, 10.

Ramanna, K., 2015. Thin Political Markets: The Soft Underbelly of Capitalism. California

Management Review, 57(2), pp.5-19.

Redmond, J. and Walker, B., 2016. The value of energy audits for SMEs: an Australian

example. Energy Efficiency, 9(5), pp.1053-1063.

detecting fraud within organizations. Journal of Business Ethics, 149(4), pp.857-874.

Drew, J., and Dollery, B., 2015. Inconsistent depreciation practice and public policymaking:

Local government reform in New South Wales. Australian Accounting Review, 25(1), pp.28-37.

Gaynor, L.M., Kelton, A.S., Mercer, M., and Yohn, T.L., 2016. Understanding the relation

between financial reportiInaam, Z. and Khamoussi, H., 2016. Audit committee effectiveness,

audit quality and earnings management: a meta-analysis. International Journal of Law and

Management, 58(2), pp.179-196.ng quality and audit quality. Auditing: A Journal of Practice &

Theory, 35(4), pp.1-22.

Jermakowicz, E.K., Epstein, B.J. and Ramamoorti, S., 2018. CAM versus KAM-A Distinction

without a Difference?: Making Judgments in Reporting Critical Audit Matters. The CPA

Journal, 88(2), pp.34-40.

Kachelmeier, S.J., Schmidt, J.J. and Valentine, K., 2017. The disclaimer effect of disclosing

critical audit matters in the auditor’s report. Working paper.

Mactavish, C., McCracken, S. and Schmidt, R.N., 2018. External Auditors' Judgment and

Decision Making: An Audit Process Task Analysis. Accounting Perspectives, 17(3), pp.387-426.

Masdor, N. and Shamsuddin, A., 2018. The Implementation of ISA 701-Key Audit Matters: A

Review. Global Business & Management Research, 10.

Ramanna, K., 2015. Thin Political Markets: The Soft Underbelly of Capitalism. California

Management Review, 57(2), pp.5-19.

Redmond, J. and Walker, B., 2016. The value of energy audits for SMEs: an Australian

example. Energy Efficiency, 9(5), pp.1053-1063.

Schatt, A., Doukakis, L., Bessieux-Ollier, C. and Walliser, E., 2016. Do goodwill impairments

by European firms provide useful information to investors?. Accounting in Europe, 13(3),

pp.307-327.

Schiereck, D., Kiesel, F. and Kolaric, S., 2016. Brexit:(Not) another Lehman moment for

banks?. Finance Research Letters, 19, pp.291-297.

Segal, M., 2017. ISA 701: Key Audit Matters-An exploration of the rationale and possible

unintended consequences in a South African. Journal of Economic and Financial

Sciences, 10(2), pp.376-391.

Shrivastava, K. and Bedia, D.D., 2017. The Impact of Transition to Ind AS on Key Accounting

Areas: An Assessment. IUP Journal of Accounting Research & Audit Practices, 16(4), pp.35-43.

Velte, P., 2018. Does gender diversity in the audit committee influence key audit matters'

readability in the audit report? UK evidence. Corporate social responsibility and environmental

management, 25(5), pp.748-755.

Wilson, S. and Smith, K., 2017. Access Control: Key Control Policy 1.0 Purpose. Policy, 1, p.3.

by European firms provide useful information to investors?. Accounting in Europe, 13(3),

pp.307-327.

Schiereck, D., Kiesel, F. and Kolaric, S., 2016. Brexit:(Not) another Lehman moment for

banks?. Finance Research Letters, 19, pp.291-297.

Segal, M., 2017. ISA 701: Key Audit Matters-An exploration of the rationale and possible

unintended consequences in a South African. Journal of Economic and Financial

Sciences, 10(2), pp.376-391.

Shrivastava, K. and Bedia, D.D., 2017. The Impact of Transition to Ind AS on Key Accounting

Areas: An Assessment. IUP Journal of Accounting Research & Audit Practices, 16(4), pp.35-43.

Velte, P., 2018. Does gender diversity in the audit committee influence key audit matters'

readability in the audit report? UK evidence. Corporate social responsibility and environmental

management, 25(5), pp.748-755.

Wilson, S. and Smith, K., 2017. Access Control: Key Control Policy 1.0 Purpose. Policy, 1, p.3.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.