Auditing Report for CBA: Analysis of 2017 Financial Statements

VerifiedAdded on 2020/12/09

|16

|3667

|313

Report

AI Summary

This report provides an in-depth analysis of the auditing process for the Commonwealth Bank of Australia (CBA), focusing on its 2017 annual report. It examines the auditor's compliance with independence requirements, non-audit services provided by PwC, and a detailed comparison of auditor's remuneration with the prior year. The report highlights key audit matters, including provisions for impaired lending assets, fair value of financial instruments, and risk-related provisions. It also discusses the role of the audit committee, the auditor's opinion on the financial statements, and the responsibilities of directors and management compared to the auditor. Furthermore, it outlines material subsequent events, the effectiveness of material information, and potential follow-up questions for the auditor at the annual general meeting. The analysis references relevant regulations and accounting standards, offering a comprehensive overview of CBA's financial auditing practices.

AUDITING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

Auditing is a systematic and independent examination of books of accounts, statutory

records and statements related with an organisation to ascertain accuracy and dependability of

financial statements revealed by that business. Auditing is vital task representing fair view of

financials of company. In this process authenticity of remuneration to directors and auditors is

checked. The outcomes are generated for audit report for CBA which is effectively prepared for

financial statements with references taken from professional bodies regulations.

Auditing is a systematic and independent examination of books of accounts, statutory

records and statements related with an organisation to ascertain accuracy and dependability of

financial statements revealed by that business. Auditing is vital task representing fair view of

financials of company. In this process authenticity of remuneration to directors and auditors is

checked. The outcomes are generated for audit report for CBA which is effectively prepared for

financial statements with references taken from professional bodies regulations.

TABLE OF CONTENTS

INTRODUCTION..............................................................................................................................1

1. Auditor compliance with Independence requirements....................................................1

2. Non-audit services............................................................................................................1

3. Auditor's Remuneration and comparison with prior year................................................1

4. Discussing Key Audit Matters............................................................................................4

5. Audit Committee of company...........................................................................................7

6. Outlining Audit Opinion....................................................................................................7

7. Directors and Management responsibilities differ from Auditor’s responsibilities..........8

8. Outlining material subsequent events..............................................................................9

9. Discussing effectiveness of material information- Group materiality...............................9

10. Undisclosed material information from annual report.................................................10

11. Asking follow-up questions to Auditor at AGM............................................................10

CONCLUSION................................................................................................................................10

REFERENCES................................................................................................................................. 12

INTRODUCTION..............................................................................................................................1

1. Auditor compliance with Independence requirements....................................................1

2. Non-audit services............................................................................................................1

3. Auditor's Remuneration and comparison with prior year................................................1

4. Discussing Key Audit Matters............................................................................................4

5. Audit Committee of company...........................................................................................7

6. Outlining Audit Opinion....................................................................................................7

7. Directors and Management responsibilities differ from Auditor’s responsibilities..........8

8. Outlining material subsequent events..............................................................................9

9. Discussing effectiveness of material information- Group materiality...............................9

10. Undisclosed material information from annual report.................................................10

11. Asking follow-up questions to Auditor at AGM............................................................10

CONCLUSION................................................................................................................................10

REFERENCES................................................................................................................................. 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Auditing is vital task representing fair view of financials of company. Present report

deals with CBA (Commonwealth of Australia), which is a banking company, providing wide

variety of services to customers. In this report, CBA's annual report ended as at 30 June, 2017

has been effectively reviewed particularly with that of Auditor's section. PwC is the auditor of

CBA and compliance of independence requirements are discussed along with non-audit

services. Moreover, remuneration of auditor with previous year is explained with percentage

change. Key audit matters and audit opinion are reviewed. Material subsequent events and

effectiveness of material informatics and follow-up questions to be asked to auditor are

discussed. In all, it can be said that auditor of CBA has assessed financials by taking into account

relevant information and thus, carried out whether financial statements reflects fair view of

affairs of company or not.

1. Auditor compliance with Independence requirements

In annual report of 2017, Auditor has complied with provisions of Corporations Act 2001

of Australia and no contraventions are being made to it. Furthermore, no contraventions are

made with regards to professional code of conduct with respect to audit.

2. Non-audit services

The non-audit services have been provided by Price water house Coopers to CBA are

satisfactory as they are compatible with independence declaration made by auditor. Such

services were being adopted by Audit Committee as per the laid down provisions and policies

(Craig, Smieliauskas and Amernic, 2017). On the other hand, nature of non-audit services were

being complied and independence of auditor was not compromised as communicated by

directors.

3. Auditor's Remuneration and comparison with prior year

1

Auditing is vital task representing fair view of financials of company. Present report

deals with CBA (Commonwealth of Australia), which is a banking company, providing wide

variety of services to customers. In this report, CBA's annual report ended as at 30 June, 2017

has been effectively reviewed particularly with that of Auditor's section. PwC is the auditor of

CBA and compliance of independence requirements are discussed along with non-audit

services. Moreover, remuneration of auditor with previous year is explained with percentage

change. Key audit matters and audit opinion are reviewed. Material subsequent events and

effectiveness of material informatics and follow-up questions to be asked to auditor are

discussed. In all, it can be said that auditor of CBA has assessed financials by taking into account

relevant information and thus, carried out whether financial statements reflects fair view of

affairs of company or not.

1. Auditor compliance with Independence requirements

In annual report of 2017, Auditor has complied with provisions of Corporations Act 2001

of Australia and no contraventions are being made to it. Furthermore, no contraventions are

made with regards to professional code of conduct with respect to audit.

2. Non-audit services

The non-audit services have been provided by Price water house Coopers to CBA are

satisfactory as they are compatible with independence declaration made by auditor. Such

services were being adopted by Audit Committee as per the laid down provisions and policies

(Craig, Smieliauskas and Amernic, 2017). On the other hand, nature of non-audit services were

being complied and independence of auditor was not compromised as communicated by

directors.

3. Auditor's Remuneration and comparison with prior year

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

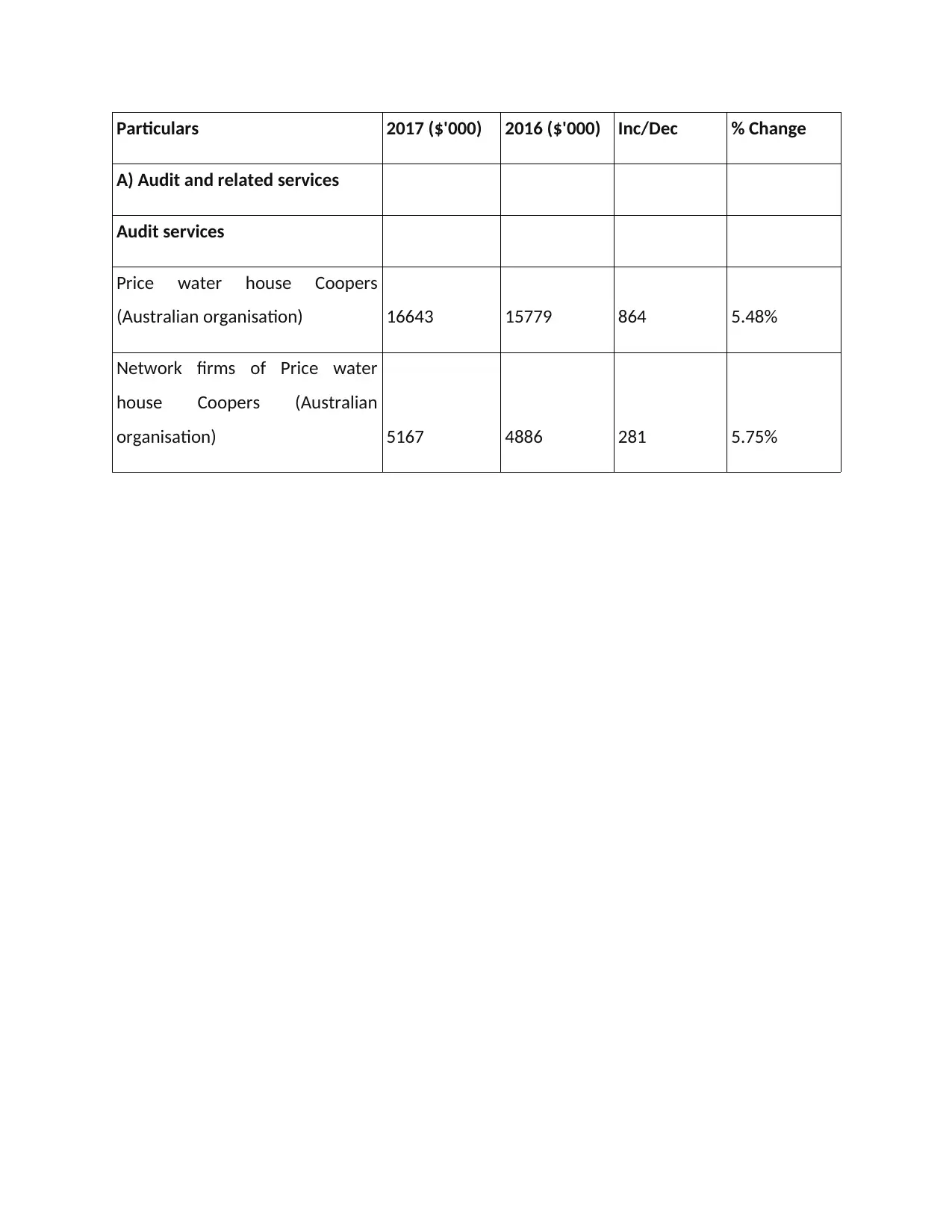

Particulars 2017 ($'000) 2016 ($'000) Inc/Dec % Change

A) Audit and related services

Audit services

Price water house Coopers

(Australian organisation) 16643 15779 864 5.48%

Network firms of Price water

house Coopers (Australian

organisation) 5167 4886 281 5.75%

A) Audit and related services

Audit services

Price water house Coopers

(Australian organisation) 16643 15779 864 5.48%

Network firms of Price water

house Coopers (Australian

organisation) 5167 4886 281 5.75%

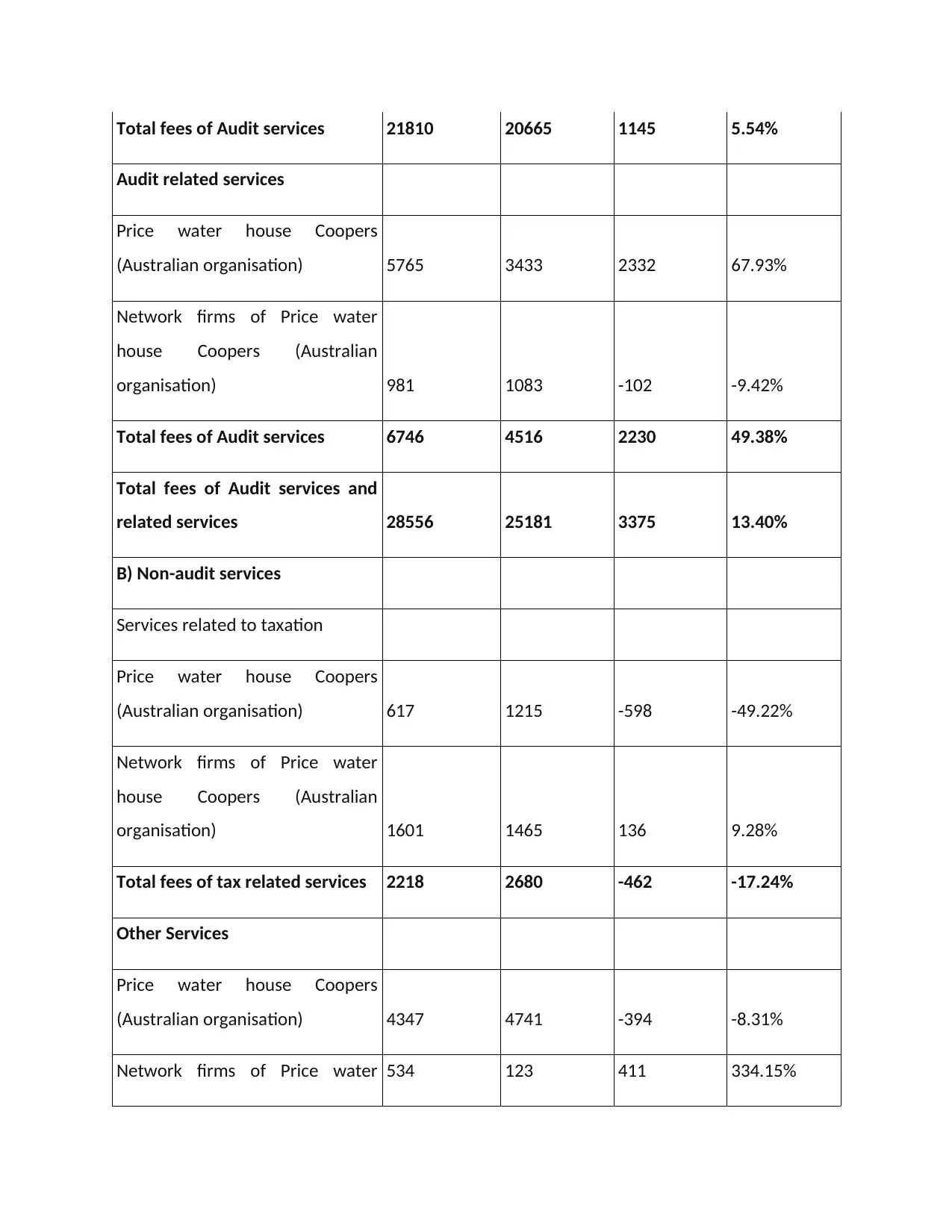

Total fees of Audit services 21810 20665 1145 5.54%

Audit related services

Price water house Coopers

(Australian organisation) 5765 3433 2332 67.93%

Network firms of Price water

house Coopers (Australian

organisation) 981 1083 -102 -9.42%

Total fees of Audit services 6746 4516 2230 49.38%

Total fees of Audit services and

related services 28556 25181 3375 13.40%

B) Non-audit services

Services related to taxation

Price water house Coopers

(Australian organisation) 617 1215 -598 -49.22%

Network firms of Price water

house Coopers (Australian

organisation) 1601 1465 136 9.28%

Total fees of tax related services 2218 2680 -462 -17.24%

Other Services

Price water house Coopers

(Australian organisation) 4347 4741 -394 -8.31%

Network firms of Price water 534 123 411 334.15%

Audit related services

Price water house Coopers

(Australian organisation) 5765 3433 2332 67.93%

Network firms of Price water

house Coopers (Australian

organisation) 981 1083 -102 -9.42%

Total fees of Audit services 6746 4516 2230 49.38%

Total fees of Audit services and

related services 28556 25181 3375 13.40%

B) Non-audit services

Services related to taxation

Price water house Coopers

(Australian organisation) 617 1215 -598 -49.22%

Network firms of Price water

house Coopers (Australian

organisation) 1601 1465 136 9.28%

Total fees of tax related services 2218 2680 -462 -17.24%

Other Services

Price water house Coopers

(Australian organisation) 4347 4741 -394 -8.31%

Network firms of Price water 534 123 411 334.15%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

house Coopers (Australian

organisation)

Total remuneration of other

services 4881 4864 17 0.35%

Total fees for non-audit services 7099 7544 -445 -5.90%

Total fees for audit and non-audit

services 35655 32725 2930 8.95%

It can be interpreted from the above table that, Auditor's remuneration paid in 2016 has

undergone change in next year. It is reflected in total fees paid for audit related services which

was 4516 ($'000) in 2016 and increased to 6746 in 2017 by having 49.28 % change. On the

other hand, total fees for audit and related services has also changed by 13.40 % from previous

year. Non-audit services are also changed. Non-audit services were 7544 in 2016 and decreased

to 7099 in 2017 having -5.90 % change. Collectively, audit and non-audit services remuneration

are increased by 8.95% in 2017.

4. Discussing Key Audit Matters

Audit matter

Provision for impairment of Lending assets: Provisions for impaired lending assets are

considered by management of CWB as auditing matter with regards to time frame and size of

provision to be recognised. An understanding has been developed for control, which is relevant

for the audit purpose. Key designs were framed for conducting auditing throughout the year:

Determination of impaired loans.

Integrity and reliability of credit information provided by Group's system.

Assessment by management about integrity of this model.

Audit Procedure:

organisation)

Total remuneration of other

services 4881 4864 17 0.35%

Total fees for non-audit services 7099 7544 -445 -5.90%

Total fees for audit and non-audit

services 35655 32725 2930 8.95%

It can be interpreted from the above table that, Auditor's remuneration paid in 2016 has

undergone change in next year. It is reflected in total fees paid for audit related services which

was 4516 ($'000) in 2016 and increased to 6746 in 2017 by having 49.28 % change. On the

other hand, total fees for audit and related services has also changed by 13.40 % from previous

year. Non-audit services are also changed. Non-audit services were 7544 in 2016 and decreased

to 7099 in 2017 having -5.90 % change. Collectively, audit and non-audit services remuneration

are increased by 8.95% in 2017.

4. Discussing Key Audit Matters

Audit matter

Provision for impairment of Lending assets: Provisions for impaired lending assets are

considered by management of CWB as auditing matter with regards to time frame and size of

provision to be recognised. An understanding has been developed for control, which is relevant

for the audit purpose. Key designs were framed for conducting auditing throughout the year:

Determination of impaired loans.

Integrity and reliability of credit information provided by Group's system.

Assessment by management about integrity of this model.

Audit Procedure:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For individually assessed provisions, auditors of CWB follow audit procedure of

examination of cash flow forecasted by management of company which support calculation of

impairment along with assessment of key judgements.

For testing collective assessed provisions, key data which is transferred between system

of group is tested for their accuracy and correctness (Pollard and et.al., 2018). Comparisons

was between support key evidences and market practices key assumption along with

comparability of modelled calculations with auditor's own calculations. In audit of provision for

impairment of lending assets, analytical procedure is been followed through comparison of

data and information.

Audit matter:

Fair value for financial instruments: CWB holds limited financial instruments and their

valuation requires judgement from management as per Australian Accounting Standards. This is

considered as key audit matter Audit because valuation of these instruments highly based on

judgement.

Audit Procedure:

The audit procedure is designed for carrying out assessment through development of

valuation model governance control framework. Checking completeness and accuracy of data

inputs including market data (Anginer, Demirgüç-Kunt and Mare, 2018). Methodologies were

developed for determination of fair value of adjustments and assessments of management is

done for measurement of fair value of their model. In this, test of control procedure is applied

by the auditor as it involves reliance on client's data.

Audit matter:

Provisions for Risk related with conduct, regulator action and related disclosures:

This is considered as key audit matter as Commonwealth Bank is more exposed to risk related

with legal and regulatory procedures of cases including jurisdictional proceedings that can raise

liabilities of bank significantly.

Audit Procedure:

examination of cash flow forecasted by management of company which support calculation of

impairment along with assessment of key judgements.

For testing collective assessed provisions, key data which is transferred between system

of group is tested for their accuracy and correctness (Pollard and et.al., 2018). Comparisons

was between support key evidences and market practices key assumption along with

comparability of modelled calculations with auditor's own calculations. In audit of provision for

impairment of lending assets, analytical procedure is been followed through comparison of

data and information.

Audit matter:

Fair value for financial instruments: CWB holds limited financial instruments and their

valuation requires judgement from management as per Australian Accounting Standards. This is

considered as key audit matter Audit because valuation of these instruments highly based on

judgement.

Audit Procedure:

The audit procedure is designed for carrying out assessment through development of

valuation model governance control framework. Checking completeness and accuracy of data

inputs including market data (Anginer, Demirgüç-Kunt and Mare, 2018). Methodologies were

developed for determination of fair value of adjustments and assessments of management is

done for measurement of fair value of their model. In this, test of control procedure is applied

by the auditor as it involves reliance on client's data.

Audit matter:

Provisions for Risk related with conduct, regulator action and related disclosures:

This is considered as key audit matter as Commonwealth Bank is more exposed to risk related

with legal and regulatory procedures of cases including jurisdictional proceedings that can raise

liabilities of bank significantly.

Audit Procedure:

The audit procedure of auditor includes development of an understanding about the

process adopted by bank for identification and assessment of impact of legal and regulatory

items and conduct risk.

Audit matter:

Valuation of liabilities of insurance policyholder: This is taken in account for auditing by

the auditor because valuation by management for matters related with settlement of future

insurance claims include intensive judgements and a small assumption can lead to materially

effecting valuation of liabilities.

Audit Procedure:

For this comparison of methodology and models used by management of the bank

is done with those which are generally applied in industry and regulatory standards.

Along with this, an understanding is developed by auditor for controlling measures used by

management of the Bank related with valuation matter. In this procedure the substantive test

of detail is applied as it is related with assessment risk involved in various matters.

Audit matter:

Valuation of retirement benefits: Common wealth Bank have defined two benefits

plans for employees, one in Australia and another in UK. Both this plans has financial

significance on financial reports of the group so it is taken as key audit matter by t auditor.

Audit Procedure:

Auditors have tested the data used by management for computation along with source

documents. Reasonableness of assumptions made for calculations is assessed with use of

external market data (Patterson and Smith, 2015). Auditors also developed their expectations

for possible alternative obligations and compared it with calculations done by management. In

this, analytical procedure is followed to carry out audit as there is comparison of calculation and

data.

Audit matter:

This is taken as key Audit matter because commonwealth bank's operations and

financial reporting matters heavily rely on its IT system. Also, automated accounting

procedures, manual control system of IT is also considered for auditing.

process adopted by bank for identification and assessment of impact of legal and regulatory

items and conduct risk.

Audit matter:

Valuation of liabilities of insurance policyholder: This is taken in account for auditing by

the auditor because valuation by management for matters related with settlement of future

insurance claims include intensive judgements and a small assumption can lead to materially

effecting valuation of liabilities.

Audit Procedure:

For this comparison of methodology and models used by management of the bank

is done with those which are generally applied in industry and regulatory standards.

Along with this, an understanding is developed by auditor for controlling measures used by

management of the Bank related with valuation matter. In this procedure the substantive test

of detail is applied as it is related with assessment risk involved in various matters.

Audit matter:

Valuation of retirement benefits: Common wealth Bank have defined two benefits

plans for employees, one in Australia and another in UK. Both this plans has financial

significance on financial reports of the group so it is taken as key audit matter by t auditor.

Audit Procedure:

Auditors have tested the data used by management for computation along with source

documents. Reasonableness of assumptions made for calculations is assessed with use of

external market data (Patterson and Smith, 2015). Auditors also developed their expectations

for possible alternative obligations and compared it with calculations done by management. In

this, analytical procedure is followed to carry out audit as there is comparison of calculation and

data.

Audit matter:

This is taken as key Audit matter because commonwealth bank's operations and

financial reporting matters heavily rely on its IT system. Also, automated accounting

procedures, manual control system of IT is also considered for auditing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Information system reporting and control:

Audit Procedure: Auditors focus on evaluation and tasting of effectiveness of designs and

operational measures implied for controlling the integrity of IT system of group. Direct test

applied by the auditor on a sample basis for audit testing and to check system functionality.

5. Audit Committee of company

Yes, there are various non-executive directors of CBA. These are Launa Inman, Shirish

Apte, Brian Long, Harrison Young (Annual Report of CBA. 2017). There is no Audit Committee

Charter for the company. However, it gives advices to Board of Directors and then after their

approval, further tasks are done in the best possible manner. On the other hand, auditor of

CBA, PwC has complied with general standard imposed by Corporations Act 2001. This means

that Audit Committee provides advices to Board and effectively attain activities in a better way.

6. Outlining Audit Opinion

Audit opinion has been made by PwC auditor of CBA, giving wide opinion about the

financial statements of company in effective manner. It has been identified that auditor has

audited Group and CBA's balance sheets, statements of - income, comprehensive income,

changes in equity and cash flow and notes to financial statements implying accounting policies

being adopted by company for the year ended on 30 June, 2017 and director's declaration. By

conducting proper analysis of these statements, it is found that, financials provide true and fair

view of Group and Company's affairs for the period. Moreover, statements are effectively

complying with Australia's regulations and standards such as AAS (Australian Accounting

Standards) and Corporations Regulations 2001.

Furthermore, it can be identified from the audit opinion that audit is designed in order

to provide assurance that financials are free from misstatements which may arise due to error

or fraud (Carson, Fargher and Zhang, 2017). Misstatements are considered to be influence

economic decision-making by users of financial information up to a high extent and it is

required that audit should be done in a proper manner by keeping in mind all such provisions

(Hay, Stewart and Botica Redmayne, 2017). Moreover, audit opinion has been made with

relation to geographic and management structure of CBA as a whole. Broader economies,

Audit Procedure: Auditors focus on evaluation and tasting of effectiveness of designs and

operational measures implied for controlling the integrity of IT system of group. Direct test

applied by the auditor on a sample basis for audit testing and to check system functionality.

5. Audit Committee of company

Yes, there are various non-executive directors of CBA. These are Launa Inman, Shirish

Apte, Brian Long, Harrison Young (Annual Report of CBA. 2017). There is no Audit Committee

Charter for the company. However, it gives advices to Board of Directors and then after their

approval, further tasks are done in the best possible manner. On the other hand, auditor of

CBA, PwC has complied with general standard imposed by Corporations Act 2001. This means

that Audit Committee provides advices to Board and effectively attain activities in a better way.

6. Outlining Audit Opinion

Audit opinion has been made by PwC auditor of CBA, giving wide opinion about the

financial statements of company in effective manner. It has been identified that auditor has

audited Group and CBA's balance sheets, statements of - income, comprehensive income,

changes in equity and cash flow and notes to financial statements implying accounting policies

being adopted by company for the year ended on 30 June, 2017 and director's declaration. By

conducting proper analysis of these statements, it is found that, financials provide true and fair

view of Group and Company's affairs for the period. Moreover, statements are effectively

complying with Australia's regulations and standards such as AAS (Australian Accounting

Standards) and Corporations Regulations 2001.

Furthermore, it can be identified from the audit opinion that audit is designed in order

to provide assurance that financials are free from misstatements which may arise due to error

or fraud (Carson, Fargher and Zhang, 2017). Misstatements are considered to be influence

economic decision-making by users of financial information up to a high extent and it is

required that audit should be done in a proper manner by keeping in mind all such provisions

(Hay, Stewart and Botica Redmayne, 2017). Moreover, audit opinion has been made with

relation to geographic and management structure of CBA as a whole. Broader economies,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial and internal controls are being taken into consideration and auditing is done. Hence,

as per the Audit opinion of CBA, Group and Company's financials are reflecting true view

regarding overall operations of organisation.

7. Directors and Management responsibilities differ from Auditor’s responsibilities

Directors and Management responsibilities-

The higher personnel’s of CBA are to follow all the guidelines of accounting standards

and regulations so that financial statements may be effectively prepared with ease. Directors

has duty to produce financials as per the frameworks representing overall position of company.

Moreover, true view should be represented with the help of preparation of financials by abiding

regulations. Moreover, it is the duty to provide that internal control must be taken into account

which represents fairness of financials. Furthermore, CBA's directors and management are also

responsible in the context that misstatements must be extracted as it arises due to error or

frauds which must be taken into consideration by management. Another responsibility is to

assess and determine that whole CBA Group and Company would be able to continue for long-

run which is represented from going concern concept.

Auditor’s responsibilities-

Auditor has main responsibility and duty to analyse that he/she needs to be taken into

consideration regarding financials which should be free from misstatements arising out of fraud

or error (Kotsanopoulos and Arvanitoyannis, 2017). Moreover, another responsibility is issuing

auditor report including audit opinion. Reasonable assurance does not mean that full guarantee

is given with relation to company's financials. AAS needs to be taken into consideration and

rules must be followed in a better way. Misrepresentations, omissions with intention should in

reporting, also not to be made which is the due responsibility of Auditor in financial report.

Hence, responsibilities of auditor and directors and management differs a lot.

8. Outlining material subsequent events

There are various material subsequent events which are represented in annual report of

CBA. On 3 August, 2017, AUSTRAC (Australian Transaction Reports and Analysis Centre) went

on and commenced civil proceedings against organisation. AUSTRAC has alleged CBA with

as per the Audit opinion of CBA, Group and Company's financials are reflecting true view

regarding overall operations of organisation.

7. Directors and Management responsibilities differ from Auditor’s responsibilities

Directors and Management responsibilities-

The higher personnel’s of CBA are to follow all the guidelines of accounting standards

and regulations so that financial statements may be effectively prepared with ease. Directors

has duty to produce financials as per the frameworks representing overall position of company.

Moreover, true view should be represented with the help of preparation of financials by abiding

regulations. Moreover, it is the duty to provide that internal control must be taken into account

which represents fairness of financials. Furthermore, CBA's directors and management are also

responsible in the context that misstatements must be extracted as it arises due to error or

frauds which must be taken into consideration by management. Another responsibility is to

assess and determine that whole CBA Group and Company would be able to continue for long-

run which is represented from going concern concept.

Auditor’s responsibilities-

Auditor has main responsibility and duty to analyse that he/she needs to be taken into

consideration regarding financials which should be free from misstatements arising out of fraud

or error (Kotsanopoulos and Arvanitoyannis, 2017). Moreover, another responsibility is issuing

auditor report including audit opinion. Reasonable assurance does not mean that full guarantee

is given with relation to company's financials. AAS needs to be taken into consideration and

rules must be followed in a better way. Misrepresentations, omissions with intention should in

reporting, also not to be made which is the due responsibility of Auditor in financial report.

Hence, responsibilities of auditor and directors and management differs a lot.

8. Outlining material subsequent events

There are various material subsequent events which are represented in annual report of

CBA. On 3 August, 2017, AUSTRAC (Australian Transaction Reports and Analysis Centre) went

on and commenced civil proceedings against organisation. AUSTRAC has alleged CBA with

regards to contraventions of four provisions of Anti-Money Laundering and Counter-Terrorism

Financing Act, 2006. On this, CBA is dealing with this matter seriously and will file defence

against it in the future. It is representing that Court proceedings are taken into consideration

and as such, detailed information will be presented to the Court in further proceedings

(Simunic, Ye and Zhang, 2015). Another material subsequent event happened on 4 August

2017, it was in relation to Aussie Home Loan (AHL) Acquisition, John Symond has exercised it

and as such, CBA Group will acquire 20 % interest in AHL. Purchase consideration will be made

by issuing shares of company and remaining 20 % will be made according to terms and

conditions agreed in the financial year 2012. The acquisition was expected to be met at the end

of August 2017. On the other hand, CBA is planning to be committed towards customers by

providing insurance products as per its policies. Hence, strategic actions have been followed by

CBA.

9. Discussing effectiveness of material information- Group materiality

Material information used for conducting audit of financials of CWB are:

Determined overall Group materiality of $606m, that reflects 5% earning of the bank

before taxation. For Determination of scope, nature, time frame of completion, extent

of procedures related with audit, above threshold limit is applied, along with qualitative

consideration. Moreover, measures are developed for effective evaluation of

misstatements in financial reports of the bank (Groomer and Murthy, 2018).

Profit before tax have been considered in presentation of audit reports because this is

the metric against which performance of bank is measured and is a generally accepted

benchmark in making industry.

5% is selected as per professional judgement of auditor and also this is the range which

is accepted a threshold limit in this industry.

10. Undisclosed material information from annual report

The material information disclosed by Auditor is limited to profit before tax only and

they have considered 5% as threshold limit as it is generally accepted in banking industry.

The profit after tax can be used and disclosed in auditor's report as this is a key point which is

considered by stakeholders for evaluation of performance of bank (Glover, Prawitt and Drake,

2014).

Financing Act, 2006. On this, CBA is dealing with this matter seriously and will file defence

against it in the future. It is representing that Court proceedings are taken into consideration

and as such, detailed information will be presented to the Court in further proceedings

(Simunic, Ye and Zhang, 2015). Another material subsequent event happened on 4 August

2017, it was in relation to Aussie Home Loan (AHL) Acquisition, John Symond has exercised it

and as such, CBA Group will acquire 20 % interest in AHL. Purchase consideration will be made

by issuing shares of company and remaining 20 % will be made according to terms and

conditions agreed in the financial year 2012. The acquisition was expected to be met at the end

of August 2017. On the other hand, CBA is planning to be committed towards customers by

providing insurance products as per its policies. Hence, strategic actions have been followed by

CBA.

9. Discussing effectiveness of material information- Group materiality

Material information used for conducting audit of financials of CWB are:

Determined overall Group materiality of $606m, that reflects 5% earning of the bank

before taxation. For Determination of scope, nature, time frame of completion, extent

of procedures related with audit, above threshold limit is applied, along with qualitative

consideration. Moreover, measures are developed for effective evaluation of

misstatements in financial reports of the bank (Groomer and Murthy, 2018).

Profit before tax have been considered in presentation of audit reports because this is

the metric against which performance of bank is measured and is a generally accepted

benchmark in making industry.

5% is selected as per professional judgement of auditor and also this is the range which

is accepted a threshold limit in this industry.

10. Undisclosed material information from annual report

The material information disclosed by Auditor is limited to profit before tax only and

they have considered 5% as threshold limit as it is generally accepted in banking industry.

The profit after tax can be used and disclosed in auditor's report as this is a key point which is

considered by stakeholders for evaluation of performance of bank (Glover, Prawitt and Drake,

2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Another material information which can be disclosed is related with income statement.

Auditors can determine the level of expenses and bad debts (non-performing assets) occurred

in a financial year which is a main performance checker of the bank.

11. Asking follow-up questions to Auditor at AGM

The question that can be asked to auditors in Annual generals meetings are as follows:

1. Did the audit committee took all the relevant permission which are required for

accessing confidential internal and financial information?

2. Did this report reveals any internal control deficiencies which was discovered by audit

committee during conducting auditing procedures? If yes, describe the same and

suggest some effective measures to overcome those material weaknesses.

3. Are there any items and matters on auditors schedule for unadjusted error and there

was disagreement with management about the same?? If yes, disclose the same and

state how you wish to resolve it.

CONCLUSION

Hereby, it can be concluded that audit process is significant for analysing company's

financials in the best possible manner. The outcome being generated from report signifies that

CBA is effectively preparing financial statements with professional bodies regulations such as

Corporations Act 2001 and AASB so as to reflect true view. Overall, independence auditor

report is issued by auditor and responsibilities are met of Directors and Management and also

Auditor have carried out them. Moreover, it is also being reflected that misstatements are

effectively rectified and subsequent events were occurred as reflected in annual report for

2017.

Auditors can determine the level of expenses and bad debts (non-performing assets) occurred

in a financial year which is a main performance checker of the bank.

11. Asking follow-up questions to Auditor at AGM

The question that can be asked to auditors in Annual generals meetings are as follows:

1. Did the audit committee took all the relevant permission which are required for

accessing confidential internal and financial information?

2. Did this report reveals any internal control deficiencies which was discovered by audit

committee during conducting auditing procedures? If yes, describe the same and

suggest some effective measures to overcome those material weaknesses.

3. Are there any items and matters on auditors schedule for unadjusted error and there

was disagreement with management about the same?? If yes, disclose the same and

state how you wish to resolve it.

CONCLUSION

Hereby, it can be concluded that audit process is significant for analysing company's

financials in the best possible manner. The outcome being generated from report signifies that

CBA is effectively preparing financial statements with professional bodies regulations such as

Corporations Act 2001 and AASB so as to reflect true view. Overall, independence auditor

report is issued by auditor and responsibilities are met of Directors and Management and also

Auditor have carried out them. Moreover, it is also being reflected that misstatements are

effectively rectified and subsequent events were occurred as reflected in annual report for

2017.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Anginer, D., Demirgüç-Kunt, A. and Mare, D.S., 2018. Bank capital, institutional environment

and systemic stability. Journal of Financial Stability. 37. pp.97-106.

Carson, E., Fargher, N. and Zhang, Y., 2017. Explaining auditors’ propensity to issue going‐

concern opinions in Australia after the global financial crisis. Accounting & Finance.

Craig, R., Smieliauskas, W. and Amernic, J., 2017. Estimation uncertainty and the IASB's

proposed conceptual framework.Australian Accounting Review. 27(1). pp.112-114.

Glover, S .M., Prawitt, D. F. and Drake, M.S., 2014. Between a rock and a hard place: A path

forward for using substantive analytical procedures in auditing large P&L accounts:

Commentary and analysis. Auditing: A Journal of Practice & Theory. 34(3). pp.161-179.

Groomer, S .M. and Murthy, U. S., 2018. Continuous auditing of database applications: An

embedded audit module approach. In Continuous Auditing: Theory and Application. (pp.

105-124). Emerald Publishing Limited.

Hay, D., Stewart, J. and Botica Redmayne, N., 2017. The Role of Auditing in Corporate

Governance in Australia and New Zealand: A Research Synthesis. Australian Accounting

Review. 27(4). pp.457-479.

Kotsanopoulos, K. V. and Arvanitoyannis, I. S., 2017. The Role of Auditing, Food Safety, and

Food Quality Standards in the Food Industry: A Review. Comprehensive Reviews in Food

Science and Food Safety. 16(5). pp.760-775.

Patterson, E. R. and Smith, J. R., 2015. The strategic effects of Auditing Standard No. 5 in a

multi-location setting. AUDITING: A Journal of Practice & Theory. 35(1). pp.119-138.

Pollard, C.M and et.al., 2018. Charitable Food Systems' Capacity to Address Food Insecurity: An

Australian Capital City Audit. International journal of environmental research and public

health. 15(6).

Simunic, D. A., Ye, M. and Zhang, P., 2015. Audit Quality, Auditing Standards, and Legal

Regimes: Implications for International Auditing Standards. Journal of International

Accounting Research. 14(2). pp.221-234.

Online

Annual Report of CBA. 2017 [PDF] Available Through:

<https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/

pdfs/annual-reports/annual_report_2017_14_aug_2017.pdf>

Books and Journals

Anginer, D., Demirgüç-Kunt, A. and Mare, D.S., 2018. Bank capital, institutional environment

and systemic stability. Journal of Financial Stability. 37. pp.97-106.

Carson, E., Fargher, N. and Zhang, Y., 2017. Explaining auditors’ propensity to issue going‐

concern opinions in Australia after the global financial crisis. Accounting & Finance.

Craig, R., Smieliauskas, W. and Amernic, J., 2017. Estimation uncertainty and the IASB's

proposed conceptual framework.Australian Accounting Review. 27(1). pp.112-114.

Glover, S .M., Prawitt, D. F. and Drake, M.S., 2014. Between a rock and a hard place: A path

forward for using substantive analytical procedures in auditing large P&L accounts:

Commentary and analysis. Auditing: A Journal of Practice & Theory. 34(3). pp.161-179.

Groomer, S .M. and Murthy, U. S., 2018. Continuous auditing of database applications: An

embedded audit module approach. In Continuous Auditing: Theory and Application. (pp.

105-124). Emerald Publishing Limited.

Hay, D., Stewart, J. and Botica Redmayne, N., 2017. The Role of Auditing in Corporate

Governance in Australia and New Zealand: A Research Synthesis. Australian Accounting

Review. 27(4). pp.457-479.

Kotsanopoulos, K. V. and Arvanitoyannis, I. S., 2017. The Role of Auditing, Food Safety, and

Food Quality Standards in the Food Industry: A Review. Comprehensive Reviews in Food

Science and Food Safety. 16(5). pp.760-775.

Patterson, E. R. and Smith, J. R., 2015. The strategic effects of Auditing Standard No. 5 in a

multi-location setting. AUDITING: A Journal of Practice & Theory. 35(1). pp.119-138.

Pollard, C.M and et.al., 2018. Charitable Food Systems' Capacity to Address Food Insecurity: An

Australian Capital City Audit. International journal of environmental research and public

health. 15(6).

Simunic, D. A., Ye, M. and Zhang, P., 2015. Audit Quality, Auditing Standards, and Legal

Regimes: Implications for International Auditing Standards. Journal of International

Accounting Research. 14(2). pp.221-234.

Online

Annual Report of CBA. 2017 [PDF] Available Through:

<https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/

pdfs/annual-reports/annual_report_2017_14_aug_2017.pdf>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.