Risk Management Plan for a Small Business

VerifiedAdded on 2021/04/29

|8

|1817

|95

AI Summary

This assignment involves creating a risk management plan for a small business, which includes identifying and assessing potential risks, developing mitigation strategies, and establishing a contingency plan. The plan is designed to protect the business from various threats such as fire, food poisoning, supplier disputes, key staff resignation, and others. It provides a detailed analysis of each risk, including its likelihood and impact, and suggests practical solutions to minimize their impact.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

0

La

Per

la

La

Per

la

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Introduction:

The method of recognising, evaluating, and managing risks to an organization's

resources and profits is known as risk management. These challenges or hazards may

arise from a range of causes, such as financial volatility, legal obligations, strategic

management mistakes, incidents, and natural disasters. IT security vulnerabilities and

data-related risks, as well as risk control techniques to reduce them, have risen to the

top of the priority list for digitized enterprises. As a result, businesses' mechanisms for

detecting and monitoring risks to their digital properties, such as confidential business

records, a customer's personally identifiable information (PII), and intellectual property,

are gradually being used in risk management programs. Any corporation and

organisation faces the possibility of unanticipated, damaging incidents that might cost

them revenue or force them to close permanently. Risk assessment enables businesses

to brace for the unexpected by reducing risks and additional expenses before they

occur.

An company can save money and secure the prospects by adopting a risk management

strategy and considering the multiple possible threats or incidents before they arise.

This is because a solid risk control strategy would assist an organisation in establishing

policies to prevent future risks, mitigate their effect if they do exist, and deal with the

consequences. Organizations will be more secure in their strategic choices if they can

consider and manage risk. Furthermore, sound corporate governance practices that

emphasise on risk control will assist an organisation in achieving its objectives.

Literature review:

The probability theory and decision-making under uncertainty are the foundations of risk

assessment. The predicted utility principle, the theory of bounded rationality, and

prospect theory, in particular, had a big impact. The concept of expected utility theory

states that people make decisions dependent on the expected utility of various options.

The theory of bounded rationality notes that in the physical world, multiple outcomes

and their probabilities are difficult to comprehend. Prospect theory aids in simulating the

impact of human experience on decision-making. (Misra, & Kumar, 2006).

1

The method of recognising, evaluating, and managing risks to an organization's

resources and profits is known as risk management. These challenges or hazards may

arise from a range of causes, such as financial volatility, legal obligations, strategic

management mistakes, incidents, and natural disasters. IT security vulnerabilities and

data-related risks, as well as risk control techniques to reduce them, have risen to the

top of the priority list for digitized enterprises. As a result, businesses' mechanisms for

detecting and monitoring risks to their digital properties, such as confidential business

records, a customer's personally identifiable information (PII), and intellectual property,

are gradually being used in risk management programs. Any corporation and

organisation faces the possibility of unanticipated, damaging incidents that might cost

them revenue or force them to close permanently. Risk assessment enables businesses

to brace for the unexpected by reducing risks and additional expenses before they

occur.

An company can save money and secure the prospects by adopting a risk management

strategy and considering the multiple possible threats or incidents before they arise.

This is because a solid risk control strategy would assist an organisation in establishing

policies to prevent future risks, mitigate their effect if they do exist, and deal with the

consequences. Organizations will be more secure in their strategic choices if they can

consider and manage risk. Furthermore, sound corporate governance practices that

emphasise on risk control will assist an organisation in achieving its objectives.

Literature review:

The probability theory and decision-making under uncertainty are the foundations of risk

assessment. The predicted utility principle, the theory of bounded rationality, and

prospect theory, in particular, had a big impact. The concept of expected utility theory

states that people make decisions dependent on the expected utility of various options.

The theory of bounded rationality notes that in the physical world, multiple outcomes

and their probabilities are difficult to comprehend. Prospect theory aids in simulating the

impact of human experience on decision-making. (Misra, & Kumar, 2006).

1

The art and science of recognising, assessing, and reacting to risk over the life of a

project in the best interests of achieving project goals is known as project risk

management (Schwalbe,2006).

Since the beginning of time, risk assessment has been done informally by all, whether

they are aware of it or not. Modern risk management, which came to prominence as a

commonly recognised management function between 1955 and 1964 (Snider, 1991),

has its origins in insurance, with which it has been closely connected for more than

three decades. Risk assessment hasn't always been a happy tale, and research shows

that it's currently unsuccessful at coping with unpredictable incidents. Project

management was heavily chastised in the 1960s for failing to deliver projects due to

technological complexity, contact strategy, citizen resistance, and project environmental

impacts (Morris, 1997). A project manager can also contend that the last two are

external project considerations that are outside their direct influence (Ibid), and it is

generally believed that these would be moved up the chain to higher management

levels (Chapman & Ward, 1997).

The main objectives of risk management include (Yee et al., 2001):

To allow for more organised and less discretionary decision-making.

By assessing threats and solution situations, a better view of the risks that a

project faces can be gained.

To assist in determining which threats demand immediate intervention and which

can wait.

To let managers aware that a project will have a variety of effects, and that

reasonable action can be taken to mitigate any negative repercussions.

Methodology:

This research follows the descriptive approach. We concern study risk management

through collecting data from previous studies and literature. We will give further

application risk management applied on a project in the discussion.

2

project in the best interests of achieving project goals is known as project risk

management (Schwalbe,2006).

Since the beginning of time, risk assessment has been done informally by all, whether

they are aware of it or not. Modern risk management, which came to prominence as a

commonly recognised management function between 1955 and 1964 (Snider, 1991),

has its origins in insurance, with which it has been closely connected for more than

three decades. Risk assessment hasn't always been a happy tale, and research shows

that it's currently unsuccessful at coping with unpredictable incidents. Project

management was heavily chastised in the 1960s for failing to deliver projects due to

technological complexity, contact strategy, citizen resistance, and project environmental

impacts (Morris, 1997). A project manager can also contend that the last two are

external project considerations that are outside their direct influence (Ibid), and it is

generally believed that these would be moved up the chain to higher management

levels (Chapman & Ward, 1997).

The main objectives of risk management include (Yee et al., 2001):

To allow for more organised and less discretionary decision-making.

By assessing threats and solution situations, a better view of the risks that a

project faces can be gained.

To assist in determining which threats demand immediate intervention and which

can wait.

To let managers aware that a project will have a variety of effects, and that

reasonable action can be taken to mitigate any negative repercussions.

Methodology:

This research follows the descriptive approach. We concern study risk management

through collecting data from previous studies and literature. We will give further

application risk management applied on a project in the discussion.

2

Result and Discussion:

Risk management strategy

The launch approach (LaPerla coffe shop) involved talking to stakeholders

(interviewing) based on brainstorming, and discussion among the various employees to

determine the maximum risks that should be taken into account when completing the

project plan. All risks were identified and identified, and a countermeasure was

identified for each risk. Staff will make every effort to ensure that steps are taken to

mitigate risks, should they arise.

Identifying risks:

Abbreviation: (L: low; M: medium; H: high)

Description Risk How to prevent and mitigate

the riskP S P*S

2. Fire damage to property

and life

3 5 15 Always ensure the proper

working and positions of smoke

alarms, fire extinguishers by

conducting regular check and

test. Staff training must be

provided for cases of fire,

including how to evacuate.

Adequately cover the negative

impact of fire to life and property

by purchasing insurances.

3. Suppliers amend their

terms and conditions of

supply

2 3 6 Establish and sustain the good

relationship with long-term

suppliers. Ensure proper plan B

in case the suppliers change the

terms and conditions.

4. Hygiene of food is not

ensure or food is

poisoning

2 4 8 Always utilize the most quality

ingredients and ensure the

hygiene of food preparation by

providing training to staff.

Manage the expiry date of the

inventory in a timely manner.

5. Suppliers do not fulfil their

obligations of supplying

2 4 8 Prepare a list of more than one

supplier for more choices. Also,

substitute products should also

be taken into account.

3

Risk management strategy

The launch approach (LaPerla coffe shop) involved talking to stakeholders

(interviewing) based on brainstorming, and discussion among the various employees to

determine the maximum risks that should be taken into account when completing the

project plan. All risks were identified and identified, and a countermeasure was

identified for each risk. Staff will make every effort to ensure that steps are taken to

mitigate risks, should they arise.

Identifying risks:

Abbreviation: (L: low; M: medium; H: high)

Description Risk How to prevent and mitigate

the riskP S P*S

2. Fire damage to property

and life

3 5 15 Always ensure the proper

working and positions of smoke

alarms, fire extinguishers by

conducting regular check and

test. Staff training must be

provided for cases of fire,

including how to evacuate.

Adequately cover the negative

impact of fire to life and property

by purchasing insurances.

3. Suppliers amend their

terms and conditions of

supply

2 3 6 Establish and sustain the good

relationship with long-term

suppliers. Ensure proper plan B

in case the suppliers change the

terms and conditions.

4. Hygiene of food is not

ensure or food is

poisoning

2 4 8 Always utilize the most quality

ingredients and ensure the

hygiene of food preparation by

providing training to staff.

Manage the expiry date of the

inventory in a timely manner.

5. Suppliers do not fulfil their

obligations of supplying

2 4 8 Prepare a list of more than one

supplier for more choices. Also,

substitute products should also

be taken into account.

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

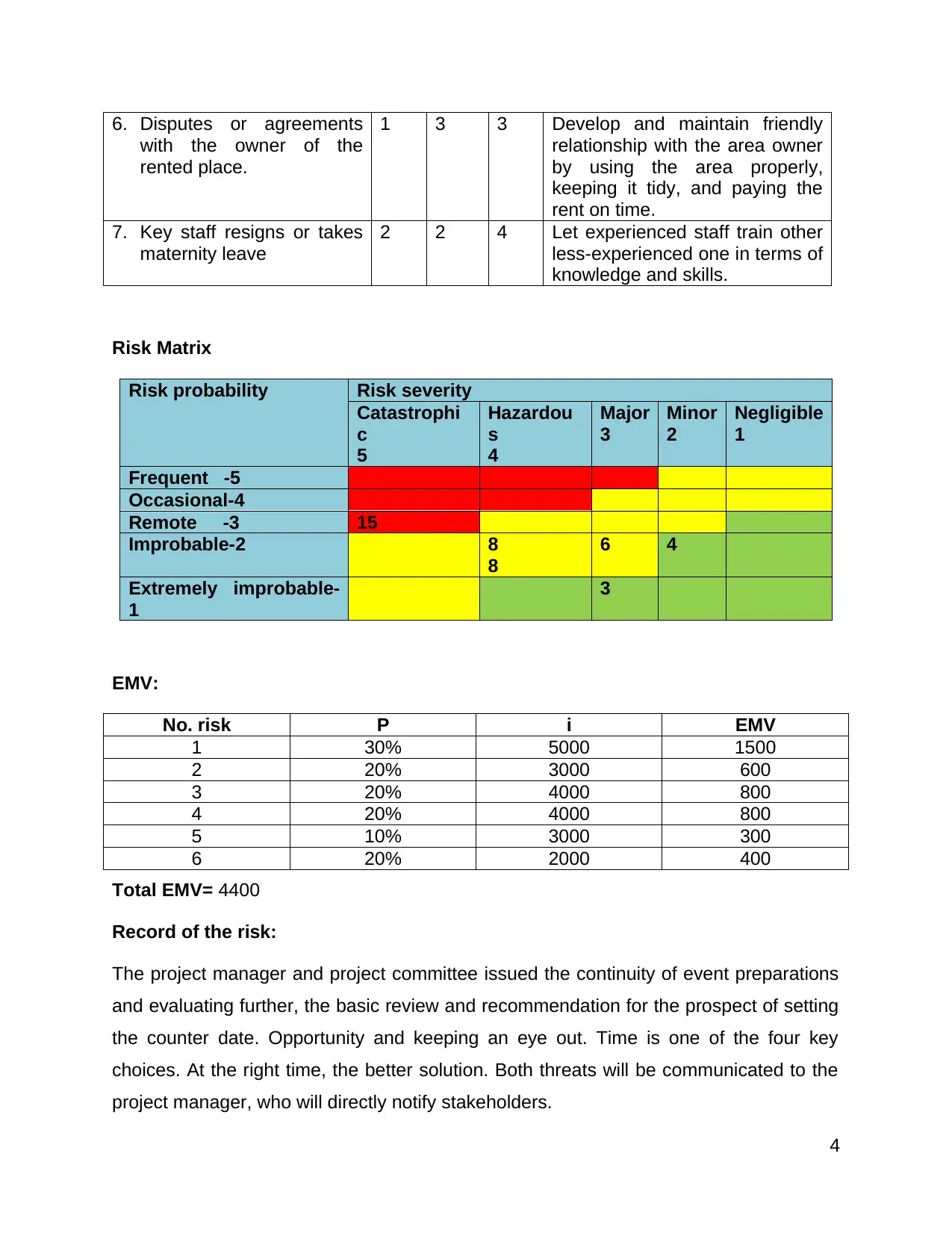

6. Disputes or agreements

with the owner of the

rented place.

1 3 3 Develop and maintain friendly

relationship with the area owner

by using the area properly,

keeping it tidy, and paying the

rent on time.

7. Key staff resigns or takes

maternity leave

2 2 4 Let experienced staff train other

less-experienced one in terms of

knowledge and skills.

Risk Matrix

Risk probability Risk severity

Catastrophi

c

5

Hazardou

s

4

Major

3

Minor

2

Negligible

1

Frequent -5

Occasional-4

Remote -3 15

Improbable-2 8

8

6 4

Extremely improbable-

1

3

EMV:

No. risk P i EMV

1 30% 5000 1500

2 20% 3000 600

3 20% 4000 800

4 20% 4000 800

5 10% 3000 300

6 20% 2000 400

Total EMV= 4400

Record of the risk:

The project manager and project committee issued the continuity of event preparations

and evaluating further, the basic review and recommendation for the prospect of setting

the counter date. Opportunity and keeping an eye out. Time is one of the four key

choices. At the right time, the better solution. Both threats will be communicated to the

project manager, who will directly notify stakeholders.

4

with the owner of the

rented place.

1 3 3 Develop and maintain friendly

relationship with the area owner

by using the area properly,

keeping it tidy, and paying the

rent on time.

7. Key staff resigns or takes

maternity leave

2 2 4 Let experienced staff train other

less-experienced one in terms of

knowledge and skills.

Risk Matrix

Risk probability Risk severity

Catastrophi

c

5

Hazardou

s

4

Major

3

Minor

2

Negligible

1

Frequent -5

Occasional-4

Remote -3 15

Improbable-2 8

8

6 4

Extremely improbable-

1

3

EMV:

No. risk P i EMV

1 30% 5000 1500

2 20% 3000 600

3 20% 4000 800

4 20% 4000 800

5 10% 3000 300

6 20% 2000 400

Total EMV= 4400

Record of the risk:

The project manager and project committee issued the continuity of event preparations

and evaluating further, the basic review and recommendation for the prospect of setting

the counter date. Opportunity and keeping an eye out. Time is one of the four key

choices. At the right time, the better solution. Both threats will be communicated to the

project manager, who will directly notify stakeholders.

4

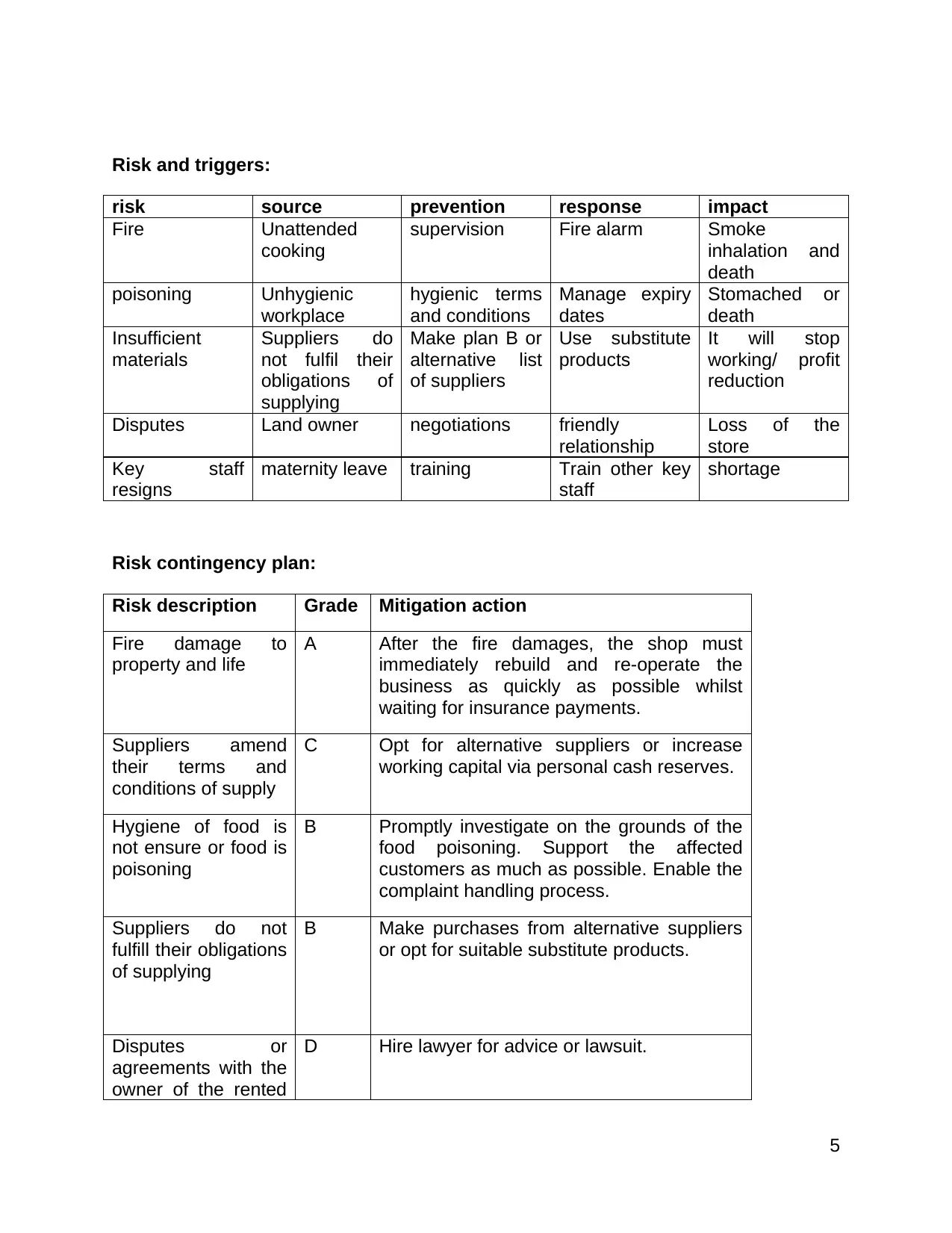

Risk and triggers:

risk source prevention response impact

Fire Unattended

cooking

supervision Fire alarm Smoke

inhalation and

death

poisoning Unhygienic

workplace

hygienic terms

and conditions

Manage expiry

dates

Stomached or

death

Insufficient

materials

Suppliers do

not fulfil their

obligations of

supplying

Make plan B or

alternative list

of suppliers

Use substitute

products

It will stop

working/ profit

reduction

Disputes Land owner negotiations friendly

relationship

Loss of the

store

Key staff

resigns

maternity leave training Train other key

staff

shortage

Risk contingency plan:

Risk description Grade Mitigation action

Fire damage to

property and life

A After the fire damages, the shop must

immediately rebuild and re-operate the

business as quickly as possible whilst

waiting for insurance payments.

Suppliers amend

their terms and

conditions of supply

C Opt for alternative suppliers or increase

working capital via personal cash reserves.

Hygiene of food is

not ensure or food is

poisoning

B Promptly investigate on the grounds of the

food poisoning. Support the affected

customers as much as possible. Enable the

complaint handling process.

Suppliers do not

fulfill their obligations

of supplying

B Make purchases from alternative suppliers

or opt for suitable substitute products.

Disputes or

agreements with the

owner of the rented

D Hire lawyer for advice or lawsuit.

5

risk source prevention response impact

Fire Unattended

cooking

supervision Fire alarm Smoke

inhalation and

death

poisoning Unhygienic

workplace

hygienic terms

and conditions

Manage expiry

dates

Stomached or

death

Insufficient

materials

Suppliers do

not fulfil their

obligations of

supplying

Make plan B or

alternative list

of suppliers

Use substitute

products

It will stop

working/ profit

reduction

Disputes Land owner negotiations friendly

relationship

Loss of the

store

Key staff

resigns

maternity leave training Train other key

staff

shortage

Risk contingency plan:

Risk description Grade Mitigation action

Fire damage to

property and life

A After the fire damages, the shop must

immediately rebuild and re-operate the

business as quickly as possible whilst

waiting for insurance payments.

Suppliers amend

their terms and

conditions of supply

C Opt for alternative suppliers or increase

working capital via personal cash reserves.

Hygiene of food is

not ensure or food is

poisoning

B Promptly investigate on the grounds of the

food poisoning. Support the affected

customers as much as possible. Enable the

complaint handling process.

Suppliers do not

fulfill their obligations

of supplying

B Make purchases from alternative suppliers

or opt for suitable substitute products.

Disputes or

agreements with the

owner of the rented

D Hire lawyer for advice or lawsuit.

5

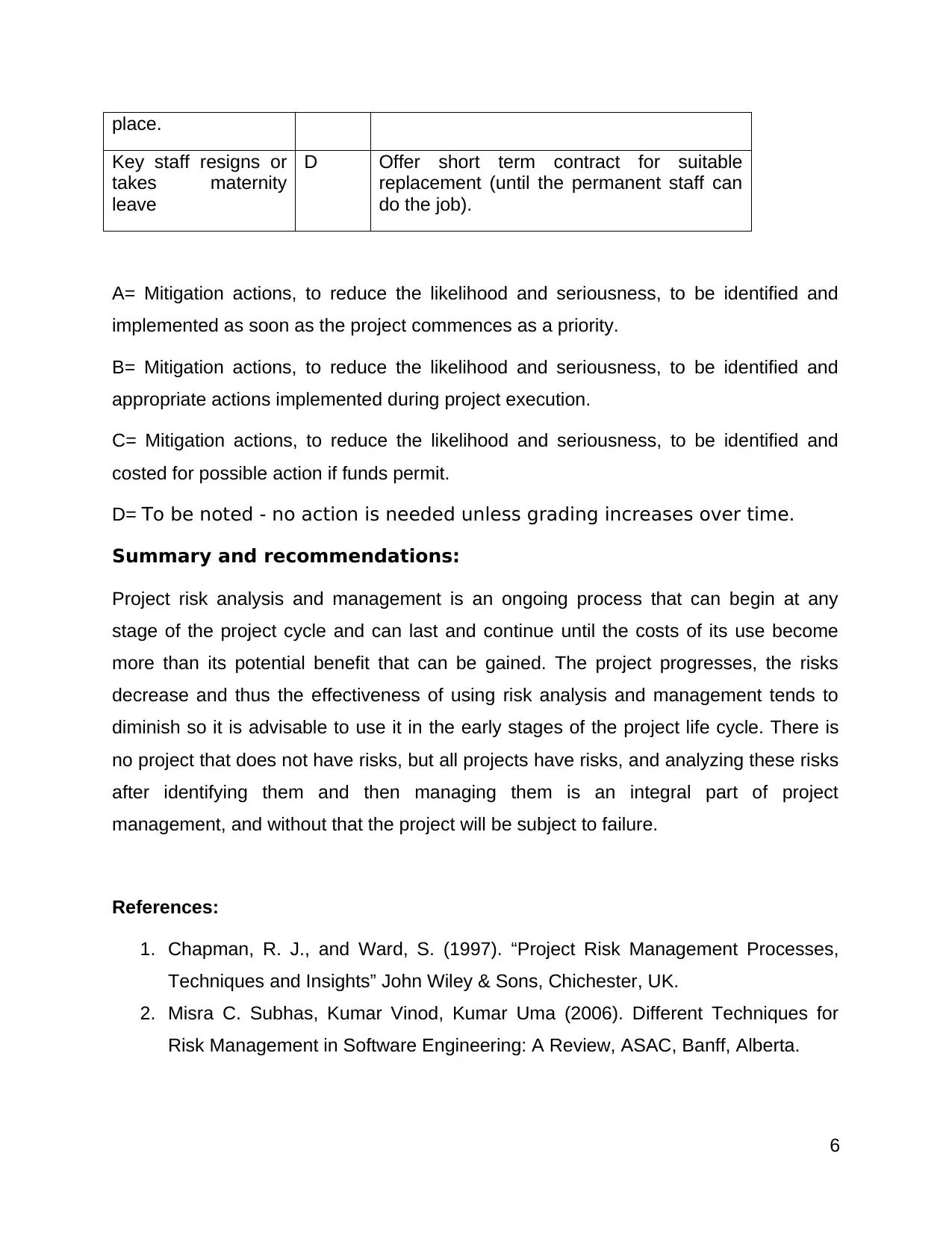

place.

Key staff resigns or

takes maternity

leave

D Offer short term contract for suitable

replacement (until the permanent staff can

do the job).

A= Mitigation actions, to reduce the likelihood and seriousness, to be identified and

implemented as soon as the project commences as a priority.

B= Mitigation actions, to reduce the likelihood and seriousness, to be identified and

appropriate actions implemented during project execution.

C= Mitigation actions, to reduce the likelihood and seriousness, to be identified and

costed for possible action if funds permit.

D= To be noted - no action is needed unless grading increases over time.

Summary and recommendations:

Project risk analysis and management is an ongoing process that can begin at any

stage of the project cycle and can last and continue until the costs of its use become

more than its potential benefit that can be gained. The project progresses, the risks

decrease and thus the effectiveness of using risk analysis and management tends to

diminish so it is advisable to use it in the early stages of the project life cycle. There is

no project that does not have risks, but all projects have risks, and analyzing these risks

after identifying them and then managing them is an integral part of project

management, and without that the project will be subject to failure.

References:

1. Chapman, R. J., and Ward, S. (1997). “Project Risk Management Processes,

Techniques and Insights” John Wiley & Sons, Chichester, UK.

2. Misra C. Subhas, Kumar Vinod, Kumar Uma (2006). Different Techniques for

Risk Management in Software Engineering: A Review, ASAC, Banff, Alberta.

6

Key staff resigns or

takes maternity

leave

D Offer short term contract for suitable

replacement (until the permanent staff can

do the job).

A= Mitigation actions, to reduce the likelihood and seriousness, to be identified and

implemented as soon as the project commences as a priority.

B= Mitigation actions, to reduce the likelihood and seriousness, to be identified and

appropriate actions implemented during project execution.

C= Mitigation actions, to reduce the likelihood and seriousness, to be identified and

costed for possible action if funds permit.

D= To be noted - no action is needed unless grading increases over time.

Summary and recommendations:

Project risk analysis and management is an ongoing process that can begin at any

stage of the project cycle and can last and continue until the costs of its use become

more than its potential benefit that can be gained. The project progresses, the risks

decrease and thus the effectiveness of using risk analysis and management tends to

diminish so it is advisable to use it in the early stages of the project life cycle. There is

no project that does not have risks, but all projects have risks, and analyzing these risks

after identifying them and then managing them is an integral part of project

management, and without that the project will be subject to failure.

References:

1. Chapman, R. J., and Ward, S. (1997). “Project Risk Management Processes,

Techniques and Insights” John Wiley & Sons, Chichester, UK.

2. Misra C. Subhas, Kumar Vinod, Kumar Uma (2006). Different Techniques for

Risk Management in Software Engineering: A Review, ASAC, Banff, Alberta.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Schwalbe, K. (2006). “Information Technology Project Management.” Thomson

Course Technology, 425

4. Snider, H. W. (1991). “Risk Management: A Retrospective View.” Risk

Management April, 47-54

5. Yee, C. W., Chan, P., and Hu, G. (2001). Construction Insurance and Risk

Management- A Practical Guide for Construction Professionals, The Singapore

Contractors Association Ltd., Singapore.

7

Course Technology, 425

4. Snider, H. W. (1991). “Risk Management: A Retrospective View.” Risk

Management April, 47-54

5. Yee, C. W., Chan, P., and Hu, G. (2001). Construction Insurance and Risk

Management- A Practical Guide for Construction Professionals, The Singapore

Contractors Association Ltd., Singapore.

7

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.