Understanding Tax Law and Principles

VerifiedAdded on 2020/06/04

|10

|2930

|61

AI Summary

The assignment delves into the core concepts of tax law, outlining how it operates within various sectors. It discusses the imposition of taxes, payment schedules, and compliance requirements. Additionally, the document examines specific areas like gift taxes, agricultural exemptions, charitable contributions, and the deduction of advance taxes from final payments.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

LAW

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

QUESTION 1...................................................................................................................................1

QUESTION 2...................................................................................................................................1

QUESTION 3...................................................................................................................................2

QUESTION 4...................................................................................................................................2

QUESTION 5...................................................................................................................................2

QUESTION 6...................................................................................................................................2

QUESTION 7...................................................................................................................................3

QUESTION 8...................................................................................................................................3

QUESTION 9...................................................................................................................................3

QUESTION 10.................................................................................................................................3

TASK 2............................................................................................................................................4

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

QUESTION 1...................................................................................................................................1

QUESTION 2...................................................................................................................................1

QUESTION 3...................................................................................................................................2

QUESTION 4...................................................................................................................................2

QUESTION 5...................................................................................................................................2

QUESTION 6...................................................................................................................................2

QUESTION 7...................................................................................................................................3

QUESTION 8...................................................................................................................................3

QUESTION 9...................................................................................................................................3

QUESTION 10.................................................................................................................................3

TASK 2............................................................................................................................................4

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

INTRODUCTION

Law consists various types of rules and regulation which are imposed on companies as

well as individuals. Also government imposed tax law on each person and company on their

income and assets. They are responsible to pay tax equal to rate mentioned under provision of

law and imposed on them as well (Alexander and Alexander, 2011). Also there are certain things

available which are exempt from rule of tax. Expenses which are spent by them are deduct from

their income. Payment of tax is the compulsory payment for tax payer. There are various types of

taxes which should be paid as per dates mentioned under law (Taxation Law. 2017). Income tax

must be paid once in a year for assessment year 1st April to 31st March.

TASK 1

QUESTION 1

According to rule of law if person go outside the country for work purpose then

organization is responsible to pay amount of travelling. But in case points received by employees

on such travelling then on which tax needs to be paid by themselves. Because such benefits are

received by them so that tax needs to paid by them as well (Barnard, 2013). They have to comply

with rules and regulation which are imposed on them. Tax needs to be paid equal to the rate

mentioned under law. Some certain rules mentioned under law which are related to points

received by employees when they go outside for work purpose.

QUESTION 2

Crane hire company has been received amount from its customers for the purpose of

damaged crane. Thus, for this amount organization is responsible to pay amount of tax which are

imposed on them. As per the rule of taxation law received has been considered as taxable amount

for which tax have to be paid equal to the amount mentioned under provision. There is no

exemption provided to entities (Becker, Reimer and Rust, 2015). No rule can protect them from

payment of tax. It should be considered as compulsory payment for them. There are different

rules and regulation mentioned under provisions of laws in the case of damaged goods and

services.

Law consists various types of rules and regulation which are imposed on companies as

well as individuals. Also government imposed tax law on each person and company on their

income and assets. They are responsible to pay tax equal to rate mentioned under provision of

law and imposed on them as well (Alexander and Alexander, 2011). Also there are certain things

available which are exempt from rule of tax. Expenses which are spent by them are deduct from

their income. Payment of tax is the compulsory payment for tax payer. There are various types of

taxes which should be paid as per dates mentioned under law (Taxation Law. 2017). Income tax

must be paid once in a year for assessment year 1st April to 31st March.

TASK 1

QUESTION 1

According to rule of law if person go outside the country for work purpose then

organization is responsible to pay amount of travelling. But in case points received by employees

on such travelling then on which tax needs to be paid by themselves. Because such benefits are

received by them so that tax needs to paid by them as well (Barnard, 2013). They have to comply

with rules and regulation which are imposed on them. Tax needs to be paid equal to the rate

mentioned under law. Some certain rules mentioned under law which are related to points

received by employees when they go outside for work purpose.

QUESTION 2

Crane hire company has been received amount from its customers for the purpose of

damaged crane. Thus, for this amount organization is responsible to pay amount of tax which are

imposed on them. As per the rule of taxation law received has been considered as taxable amount

for which tax have to be paid equal to the amount mentioned under provision. There is no

exemption provided to entities (Becker, Reimer and Rust, 2015). No rule can protect them from

payment of tax. It should be considered as compulsory payment for them. There are different

rules and regulation mentioned under provisions of laws in the case of damaged goods and

services.

QUESTION 3

Alcohol suppliers provide free overseas holidays to night club manager is not taxable

according to the rule of tax of Australia. So that, on the basis of this rule club manager is not

responsible to pay tax for the same because holidays are provided in kind which is not taxable

for individuals as well companies (Chirelstein and Zelenak, 2011). This is kind an award which

is provided to club so that ion case it was offered in monetary form then it was taxable equal to

the tax rate mentioned under provision of law. This is specific rule which is mentioned under

law. There is separate rate of tax mentioned under law related to alcoholic products and services.

Assesses needs to pay such tax which is higher than other products and no redemption provided

to them.

QUESTION 4

Canoe club purchase additional canoes on which it receives some additional excess

funds. Such amount needs to be returned to its members. Parties have to pay amount as a tax on

such additional amount. It should be paid by members as they receive such payment. According

to rule of law tax imposed or liabilities on members and they are responsible to pay such amount

within stipulated time period (Gale, Hines and Slemrod, 2011). They have to comply with rule of

law and try to maintain their performance as well.

QUESTION 5

According to the rule of taxation law of Australia in case television station provide some

payment to Australian footballer for the reason of best and fairest in the AFL. So that, tax needs

to paid by footballer equal to the amount mentioned under provision of law. Payment of tax has

been considered as compulsory payment (Helminen, 2011). Various types of rules, regulation

and policies are imposed on them. So that, individual needs to comply with such rule. Footballer

is responsible to pay amount equal to maintain under law. He is bound to do the same. Certain

laws are applicable on him which are imposed on them.

Alcohol suppliers provide free overseas holidays to night club manager is not taxable

according to the rule of tax of Australia. So that, on the basis of this rule club manager is not

responsible to pay tax for the same because holidays are provided in kind which is not taxable

for individuals as well companies (Chirelstein and Zelenak, 2011). This is kind an award which

is provided to club so that ion case it was offered in monetary form then it was taxable equal to

the tax rate mentioned under provision of law. This is specific rule which is mentioned under

law. There is separate rate of tax mentioned under law related to alcoholic products and services.

Assesses needs to pay such tax which is higher than other products and no redemption provided

to them.

QUESTION 4

Canoe club purchase additional canoes on which it receives some additional excess

funds. Such amount needs to be returned to its members. Parties have to pay amount as a tax on

such additional amount. It should be paid by members as they receive such payment. According

to rule of law tax imposed or liabilities on members and they are responsible to pay such amount

within stipulated time period (Gale, Hines and Slemrod, 2011). They have to comply with rule of

law and try to maintain their performance as well.

QUESTION 5

According to the rule of taxation law of Australia in case television station provide some

payment to Australian footballer for the reason of best and fairest in the AFL. So that, tax needs

to paid by footballer equal to the amount mentioned under provision of law. Payment of tax has

been considered as compulsory payment (Helminen, 2011). Various types of rules, regulation

and policies are imposed on them. So that, individual needs to comply with such rule. Footballer

is responsible to pay amount equal to maintain under law. He is bound to do the same. Certain

laws are applicable on him which are imposed on them.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

QUESTION 6

Expenses which are related to building qualification for a building apprentice. For the

same purpose they receive amount of deduction (Hill and Mancino, 2014). They have to

com0ply with rules of law. Legal authorities provide deduction to them in their taxable income.

QUESTION 7

Different types of forms of tax available in Australia country. Person as well as

companies are responsible to pay amount of taxes equal to rate mentioned under law. Thus, it has

been charged by government and considered as compulsory payment. In case art management

spend some amount of money for the purpose of become an art director. Such amount has been

deduct from payment of tax (Kitagawa, 2016). These types of deductions are available in rules of

law. Assesses needs to manage their duty and

QUESTION 8

Large number of companies restrict their employees to wear dress code it doesn't mean

that workers having right to claim deduction for the same as such dress not able to use for their

personal life. Further, requirement is able to use for the purpose of claim deduction. There is rule

mentioned under law related to cloths at work place. The amount of such cloths which are used

at workplace no deduction applied for the same (Lang, Pistone, Schuch and Staringer, 2015).

Employee are not able to claim for the deduction on this amount.

But in case logo of the company attached with their uniform then organization is

responsible to pay tax for the same and such amount needs to be deducted from payment of tax.

No further rule mentioned under law which rate of tax on clothing at work place (Langton and

Longbottom, 2012).

QUESTION 9

Expenses which is occurred between home and office needs to be paid by employers to

employees. For the same purpose they have to pay amount of tax which are mentioned under

provision of law. In case employees travel from his home to office then company is responsible

to pay amount of tax equal to mentioned under rules of law (Mason and Stephenson, 2015).

Employers have to pay travel cost of employees. Such cost includes providing, accommodation,

Expenses which are related to building qualification for a building apprentice. For the

same purpose they receive amount of deduction (Hill and Mancino, 2014). They have to

com0ply with rules of law. Legal authorities provide deduction to them in their taxable income.

QUESTION 7

Different types of forms of tax available in Australia country. Person as well as

companies are responsible to pay amount of taxes equal to rate mentioned under law. Thus, it has

been charged by government and considered as compulsory payment. In case art management

spend some amount of money for the purpose of become an art director. Such amount has been

deduct from payment of tax (Kitagawa, 2016). These types of deductions are available in rules of

law. Assesses needs to manage their duty and

QUESTION 8

Large number of companies restrict their employees to wear dress code it doesn't mean

that workers having right to claim deduction for the same as such dress not able to use for their

personal life. Further, requirement is able to use for the purpose of claim deduction. There is rule

mentioned under law related to cloths at work place. The amount of such cloths which are used

at workplace no deduction applied for the same (Lang, Pistone, Schuch and Staringer, 2015).

Employee are not able to claim for the deduction on this amount.

But in case logo of the company attached with their uniform then organization is

responsible to pay tax for the same and such amount needs to be deducted from payment of tax.

No further rule mentioned under law which rate of tax on clothing at work place (Langton and

Longbottom, 2012).

QUESTION 9

Expenses which is occurred between home and office needs to be paid by employers to

employees. For the same purpose they have to pay amount of tax which are mentioned under

provision of law. In case employees travel from his home to office then company is responsible

to pay amount of tax equal to mentioned under rules of law (Mason and Stephenson, 2015).

Employers have to pay travel cost of employees. Such cost includes providing, accommodation,

meals and much more. So that, on the basis of this rule amount of tax needs to paid by employers

on behalf of their employees. It should be imposed on them. Petrol charges involve in this such

situation which needs to be paid companies to their employees form home to office.

QUESTION 10

Companies are responsible to spend money on their travelling for the work purpose. If

case employees gone outside from their home country for the official purpose then expenses

must be paid by employers in order to comply with rules of law (Livingston and Gamage, 2010).

Expenses which are paid by company are needs to deduct from their amount of tax. Entities are

able to receive deduction for the same. Certain responsibilities imposed on parties which are

mentioned under rule of law.

TASK 2

Manpreet is a foreign resident who act as student in foreign country, Sydney. Her taxable

income will be calculated for the purpose of tax payment for assessment year 2016 to 2017. In

such year she starts part time working as office assistant in the office of accountant in order to

receive work experience in her selected career (McDaniel, Repetti and Ring, 2014). She receives

45,000 dollars from her job and 20,000 from her parents in order to assist her living expenses.

But such amount will not be considered as taxable income as per the rule of law. Because if

parents provide some money to their children then amount will not be considered as taxable

because they already paid tax for such amount. That should be taxable in the hands of parents.

There is no further rule mentioned under law related to tax payment. Also she received 10,000

dollars from trust which is established by her grandmother. On such amount she already paid tax

in foreign 1000 dollar. So that, according to rule she received 9000 dollars as income. That will

be add in the taxable income of Manpreet. Tax payer spent some amount on her studies equal to

18,500 dollars. Also she spent 2000 dollar on her computer as well as printer which has been

used for herb educational purpose. Along with this she has to pay 500 dollars on new mobile

which has been used for work purpose (Prebble and Prebble, 2010). Tax payer received

deduction for such type of expenses.

Net taxable income needs to calculated through add all incomes of person and deduct all

their expenses after remaining amount has been considered as net taxable income. Tax payer is

on behalf of their employees. It should be imposed on them. Petrol charges involve in this such

situation which needs to be paid companies to their employees form home to office.

QUESTION 10

Companies are responsible to spend money on their travelling for the work purpose. If

case employees gone outside from their home country for the official purpose then expenses

must be paid by employers in order to comply with rules of law (Livingston and Gamage, 2010).

Expenses which are paid by company are needs to deduct from their amount of tax. Entities are

able to receive deduction for the same. Certain responsibilities imposed on parties which are

mentioned under rule of law.

TASK 2

Manpreet is a foreign resident who act as student in foreign country, Sydney. Her taxable

income will be calculated for the purpose of tax payment for assessment year 2016 to 2017. In

such year she starts part time working as office assistant in the office of accountant in order to

receive work experience in her selected career (McDaniel, Repetti and Ring, 2014). She receives

45,000 dollars from her job and 20,000 from her parents in order to assist her living expenses.

But such amount will not be considered as taxable income as per the rule of law. Because if

parents provide some money to their children then amount will not be considered as taxable

because they already paid tax for such amount. That should be taxable in the hands of parents.

There is no further rule mentioned under law related to tax payment. Also she received 10,000

dollars from trust which is established by her grandmother. On such amount she already paid tax

in foreign 1000 dollar. So that, according to rule she received 9000 dollars as income. That will

be add in the taxable income of Manpreet. Tax payer spent some amount on her studies equal to

18,500 dollars. Also she spent 2000 dollar on her computer as well as printer which has been

used for herb educational purpose. Along with this she has to pay 500 dollars on new mobile

which has been used for work purpose (Prebble and Prebble, 2010). Tax payer received

deduction for such type of expenses.

Net taxable income needs to calculated through add all incomes of person and deduct all

their expenses after remaining amount has been considered as net taxable income. Tax payer is

not able to pay tax on exempt income but responsible to pay tax on non-exempt income equal to

rates mentioned under law (Wigmore, 2016).

Exempt income involves Australian government pensions which include amount

disability. Scholarship, grants as well as further awards are also exempted from tax purpose.

Allowances and different types of payments which are provided by Australian government are

also considered as exempted income for purpose of tax payment (McDaniel, Repetti and Ring,

2014).

Tax payer have to pay payment on non-exempt income which are considered as taxable.

Such amount should be paid by person on which it was imposed (Lang, Pistone, Schuch and

Staringer, 2015). This is compulsory payment which is have to be paid by people in order to

comply with rules and regulation.

Also there are various other amounts are mentioned under rule which is not taxable under

law are as aligned below-

Prizes which are won through ordinary lotteries it should not be considered as taxable

income.

Person won prizes from further games.

Parents provide amount to their children for the purpose of maintenance (Hill and

Mancino, 2014).

Net taxable income should be calculated on the basis of set of formate which is

mentioned under rule of tax. According to the given scenario, the taxable income must be

considered as 33,000 dollars after calculation. So that, according to this 32.5c for each 1 dollar

have been imposed on him.

As per rule taxable income 0 to 87,000-dollar tax imposed on that amount 32.5c

for each 1 dollar.

87,001 to 1,80,000 dollar on which tax imposed 37c for 1 dollar each.

1,80,000 and above and imposed tax on 45c for 1 dollar each.

Above mentioned rules is the basic rule of tax which are imposed on person who is

responsible to pay tax (Hill and Mancino, 2014). People have to follow rules, regulation and

policies which are imposed on them. Certain rules mentioned for foreign residents which is not

imposed on normal resident person. They have to comply with such rules.

rates mentioned under law (Wigmore, 2016).

Exempt income involves Australian government pensions which include amount

disability. Scholarship, grants as well as further awards are also exempted from tax purpose.

Allowances and different types of payments which are provided by Australian government are

also considered as exempted income for purpose of tax payment (McDaniel, Repetti and Ring,

2014).

Tax payer have to pay payment on non-exempt income which are considered as taxable.

Such amount should be paid by person on which it was imposed (Lang, Pistone, Schuch and

Staringer, 2015). This is compulsory payment which is have to be paid by people in order to

comply with rules and regulation.

Also there are various other amounts are mentioned under rule which is not taxable under

law are as aligned below-

Prizes which are won through ordinary lotteries it should not be considered as taxable

income.

Person won prizes from further games.

Parents provide amount to their children for the purpose of maintenance (Hill and

Mancino, 2014).

Net taxable income should be calculated on the basis of set of formate which is

mentioned under rule of tax. According to the given scenario, the taxable income must be

considered as 33,000 dollars after calculation. So that, according to this 32.5c for each 1 dollar

have been imposed on him.

As per rule taxable income 0 to 87,000-dollar tax imposed on that amount 32.5c

for each 1 dollar.

87,001 to 1,80,000 dollar on which tax imposed 37c for 1 dollar each.

1,80,000 and above and imposed tax on 45c for 1 dollar each.

Above mentioned rules is the basic rule of tax which are imposed on person who is

responsible to pay tax (Hill and Mancino, 2014). People have to follow rules, regulation and

policies which are imposed on them. Certain rules mentioned for foreign residents which is not

imposed on normal resident person. They have to comply with such rules.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

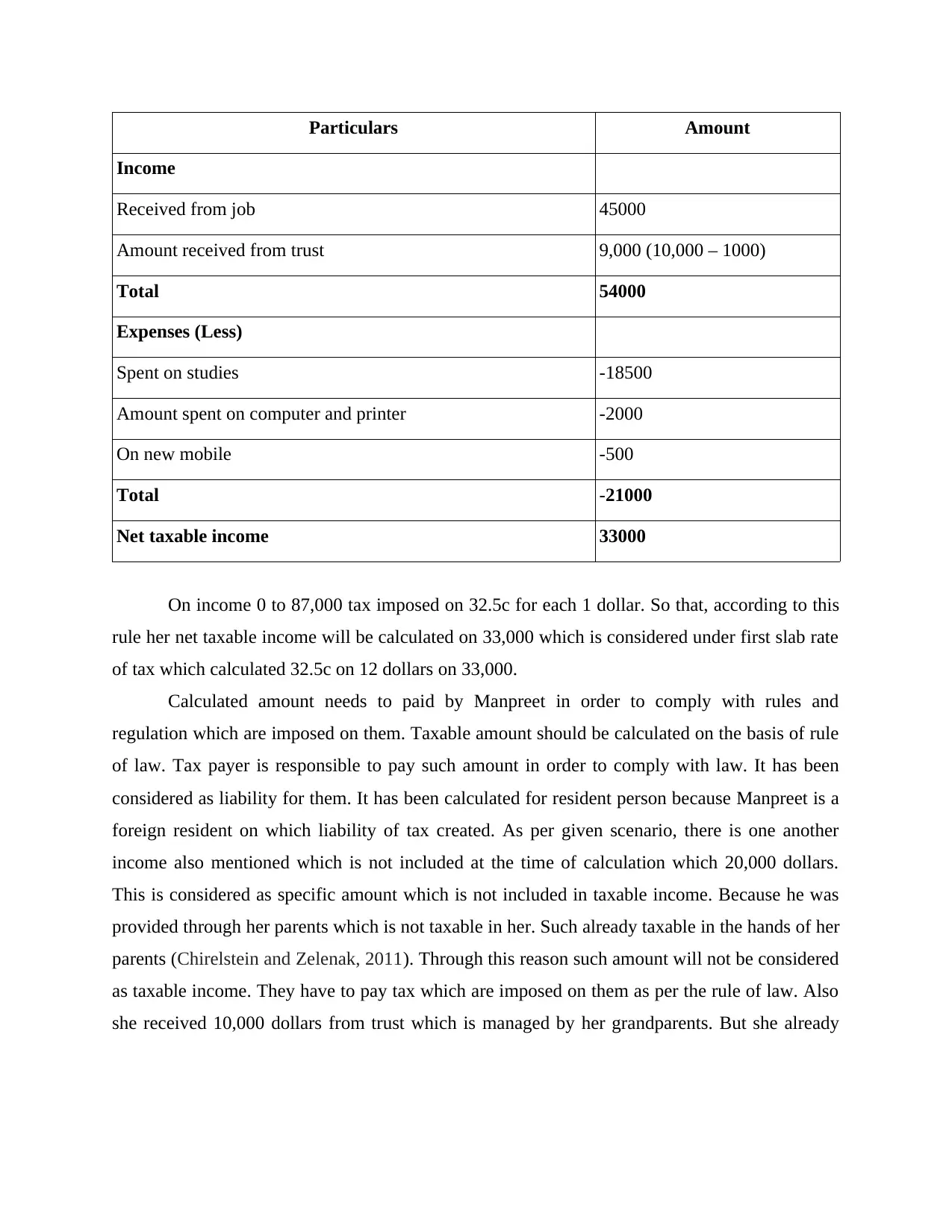

Particulars Amount

Income

Received from job 45000

Amount received from trust 9,000 (10,000 – 1000)

Total 54000

Expenses (Less)

Spent on studies -18500

Amount spent on computer and printer -2000

On new mobile -500

Total -21000

Net taxable income 33000

On income 0 to 87,000 tax imposed on 32.5c for each 1 dollar. So that, according to this

rule her net taxable income will be calculated on 33,000 which is considered under first slab rate

of tax which calculated 32.5c on 12 dollars on 33,000.

Calculated amount needs to paid by Manpreet in order to comply with rules and

regulation which are imposed on them. Taxable amount should be calculated on the basis of rule

of law. Tax payer is responsible to pay such amount in order to comply with law. It has been

considered as liability for them. It has been calculated for resident person because Manpreet is a

foreign resident on which liability of tax created. As per given scenario, there is one another

income also mentioned which is not included at the time of calculation which 20,000 dollars.

This is considered as specific amount which is not included in taxable income. Because he was

provided through her parents which is not taxable in her. Such already taxable in the hands of her

parents (Chirelstein and Zelenak, 2011). Through this reason such amount will not be considered

as taxable income. They have to pay tax which are imposed on them as per the rule of law. Also

she received 10,000 dollars from trust which is managed by her grandparents. But she already

Income

Received from job 45000

Amount received from trust 9,000 (10,000 – 1000)

Total 54000

Expenses (Less)

Spent on studies -18500

Amount spent on computer and printer -2000

On new mobile -500

Total -21000

Net taxable income 33000

On income 0 to 87,000 tax imposed on 32.5c for each 1 dollar. So that, according to this

rule her net taxable income will be calculated on 33,000 which is considered under first slab rate

of tax which calculated 32.5c on 12 dollars on 33,000.

Calculated amount needs to paid by Manpreet in order to comply with rules and

regulation which are imposed on them. Taxable amount should be calculated on the basis of rule

of law. Tax payer is responsible to pay such amount in order to comply with law. It has been

considered as liability for them. It has been calculated for resident person because Manpreet is a

foreign resident on which liability of tax created. As per given scenario, there is one another

income also mentioned which is not included at the time of calculation which 20,000 dollars.

This is considered as specific amount which is not included in taxable income. Because he was

provided through her parents which is not taxable in her. Such already taxable in the hands of her

parents (Chirelstein and Zelenak, 2011). Through this reason such amount will not be considered

as taxable income. They have to pay tax which are imposed on them as per the rule of law. Also

she received 10,000 dollars from trust which is managed by her grandparents. But she already

paid on same mount which is 1000 dollar in foreign. So that, there is no need to pay tax in home

country as well. Only 9000 dollars has been considered as taxable income.

Above mentioned income has been considered as net taxable income of Manpreet.

According to such calculation she has to pay tax equal to the amount imposed on her in order to

reduce her liabilities (Alexander and Alexander, 2011). It should be paid within stipulated time

period which is mentioned under rule of law. Certain amount of awards and gifts are not

included in taxable income.

CONCLUSION

On the basis of above report, it is concluded that tax is the compulsory payment which

needs to be paid by assesses equal to amount imposed on them. It must be paid according to

requirement of time. Furthermore, people have to follow rules and regulation which are imposed

on them. Amount which is receive as gift then no tax imposed on donee but only imposed on

doner. Tax is not imposed on agriculture and charitable sector. Advance tax deducted from final

payment.

country as well. Only 9000 dollars has been considered as taxable income.

Above mentioned income has been considered as net taxable income of Manpreet.

According to such calculation she has to pay tax equal to the amount imposed on her in order to

reduce her liabilities (Alexander and Alexander, 2011). It should be paid within stipulated time

period which is mentioned under rule of law. Certain amount of awards and gifts are not

included in taxable income.

CONCLUSION

On the basis of above report, it is concluded that tax is the compulsory payment which

needs to be paid by assesses equal to amount imposed on them. It must be paid according to

requirement of time. Furthermore, people have to follow rules and regulation which are imposed

on them. Amount which is receive as gift then no tax imposed on donee but only imposed on

doner. Tax is not imposed on agriculture and charitable sector. Advance tax deducted from final

payment.

REFERENCES

Books and Journals

Alexander, K. and Alexander, M.D., 2011. American public school law. Cengage Learning.

Barnard, C., 2013. The substantive law of the EU: the four freedoms. Oxford University Press.

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions. Kluwer

Law International.

Chirelstein, M. and Zelenak, L., 2011. Chirelstein and Zelenak's Federal Income Taxation, 12th

(Concepts and Insights Series). West Academic.

Gale, W.G., Hines, J.R. and Slemrod, J. eds., 2011. Rethinking estate and gift taxation.

Brookings Institution Press.

Helminen, M., 2011. EU tax law: direct taxation. IBFD.

Hill, F.R. and Mancino, D.M., 2014. Taxation of Exempt Organizations.

Kitagawa, Z., 2016. Administrative Regulations (Vol. 4). Doing Business in Japan.

Lang, M., Pistone, P., Schuch, J. and Staringer, C. eds., 2015. Introduction to European tax law

on direct taxation. Linde Verlag GmbH.

Langton, M. and Longbottom, J. eds., 2012. Community futures, legal architecture: foundations

for Indigenous peoples in the global mining boom. Routledge.

Livingston, M.A. and Gamage, D.S., 2010. Taxation: law, planning, and policy. LexisNexis.

Mason, A.T. and Stephenson, G., 2015. American constitutional law: introductory essays and

selected cases. Routledge.

McDaniel, P.R., Repetti, J.R. and Ring, D.M., 2014. Introduction to United States international

taxation. Wolters Kluwer Law & Business.

Prebble, R. and Prebble, J., 2010. Does the use of general anti-avoidance rules to combat tax

avoidance breach principles of the rule of law-a comparative study. . Louis ULJ. 55.

p.21.

Wigmore, J.H., 2016. Wigmore on evidence. Wolters Kluwer.

Online

Taxation Law. 2017. [Online]. Available

through:<https://www.sweetandmaxwell.co.uk/practicearea.aspx?

practicearea=75&family=6>. [Accessed on 5th September 2017].

Books and Journals

Alexander, K. and Alexander, M.D., 2011. American public school law. Cengage Learning.

Barnard, C., 2013. The substantive law of the EU: the four freedoms. Oxford University Press.

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions. Kluwer

Law International.

Chirelstein, M. and Zelenak, L., 2011. Chirelstein and Zelenak's Federal Income Taxation, 12th

(Concepts and Insights Series). West Academic.

Gale, W.G., Hines, J.R. and Slemrod, J. eds., 2011. Rethinking estate and gift taxation.

Brookings Institution Press.

Helminen, M., 2011. EU tax law: direct taxation. IBFD.

Hill, F.R. and Mancino, D.M., 2014. Taxation of Exempt Organizations.

Kitagawa, Z., 2016. Administrative Regulations (Vol. 4). Doing Business in Japan.

Lang, M., Pistone, P., Schuch, J. and Staringer, C. eds., 2015. Introduction to European tax law

on direct taxation. Linde Verlag GmbH.

Langton, M. and Longbottom, J. eds., 2012. Community futures, legal architecture: foundations

for Indigenous peoples in the global mining boom. Routledge.

Livingston, M.A. and Gamage, D.S., 2010. Taxation: law, planning, and policy. LexisNexis.

Mason, A.T. and Stephenson, G., 2015. American constitutional law: introductory essays and

selected cases. Routledge.

McDaniel, P.R., Repetti, J.R. and Ring, D.M., 2014. Introduction to United States international

taxation. Wolters Kluwer Law & Business.

Prebble, R. and Prebble, J., 2010. Does the use of general anti-avoidance rules to combat tax

avoidance breach principles of the rule of law-a comparative study. . Louis ULJ. 55.

p.21.

Wigmore, J.H., 2016. Wigmore on evidence. Wolters Kluwer.

Online

Taxation Law. 2017. [Online]. Available

through:<https://www.sweetandmaxwell.co.uk/practicearea.aspx?

practicearea=75&family=6>. [Accessed on 5th September 2017].

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.