Comprehensive Analysis of Taxation Laws: Income, CGT, and Concessions

VerifiedAdded on 2022/08/19

|12

|2719

|16

Report

AI Summary

This report analyzes several aspects of taxation law, beginning with a case study examining the tax liabilities of an individual, Emmi, and her various sources of income, including tips, salary, and gifts. The analysis delves into the concepts of assessable income, ordinary income, and fringe benefits, referencing relevant sections of the ITAA 1997 and case law. The second part of the report focuses on capital gains tax (CGT), defining CGT assets, and the treatment of pre-CGT assets and personal use assets. It examines the CGT concessions available to small businesses, including the 15-year exemption, 50% reduction, retirement concession, and roll-over relief, with an application to a small business studio. Finally, the report addresses the taxation of personal use assets and collectibles, outlining the relevant rules and regulations. The report concludes with a summary of key findings and implications for taxpayers.

Running head: LAWS OF TAXATION

LAWS OF TAXATION

Name of Student

Name of University

Author note

Course ID

LAWS OF TAXATION

Name of Student

Name of University

Author note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

LAWS OF TAXATION

Table of Contents

Answer to question 1..................................................................................................................2

Issues:.........................................................................................................................................2

Rule:...........................................................................................................................................2

Application.................................................................................................................................3

Conclusion:................................................................................................................................5

Answer to question 2..................................................................................................................5

Answer a:...................................................................................................................................5

Answer b:...................................................................................................................................6

Answer c:...................................................................................................................................6

Answer d:...................................................................................................................................8

Answer e:...................................................................................................................................8

References................................................................................................................................10

LAWS OF TAXATION

Table of Contents

Answer to question 1..................................................................................................................2

Issues:.........................................................................................................................................2

Rule:...........................................................................................................................................2

Application.................................................................................................................................3

Conclusion:................................................................................................................................5

Answer to question 2..................................................................................................................5

Answer a:...................................................................................................................................5

Answer b:...................................................................................................................................6

Answer c:...................................................................................................................................6

Answer d:...................................................................................................................................8

Answer e:...................................................................................................................................8

References................................................................................................................................10

2

LAWS OF TAXATION

Answer to question 1

Issues:

Tax liabilities of different receipts that are received by the taxpayer resulting from the

employment will be discussed in the case study.

Rule:

Some deductions are followed by the assessable income that are involved in the

income of the taxpayer will be discussed under “sec 6-5 (1)” which states that the

characteristics of income described that it must be income and it should be convertible into

money (Ford and Dibden, 2019). The section also describes that the assessable income are

included in the income in agreement and it is mentioned in the “ordinary concept”. An

ordinary income is a voluntary or unanticipated payment that is obvious and it is received by

the taxpayer in the employment. Under “sec 6-5 (1) ITA Act 1997” describes that a tip

received by the taxi driver is taxable and it should be treated as ordinary income. “Calvert

and Wainwright (1947)” noted about this in the section (Burton, 2017).

Fringe benefit can be provided by the employer to the employee for any personal

service and it should be taxable from the employer. It can act as a motivated factor for the

employee (Pasztor and Valent, 2016). The receipts that are originated from the personal

service of taxpayer’s and is relating to the receipt is amounted and treated as ordinary

income. Relation with the receipts are established through personal services like salary and

wages. “Moorhouse and Dooland (1995)” stated through their tax commissioner that the

amount received by the taxpayer direct or indirectly from the personal service of taxpayer is

defined as ordinary earning.

LAWS OF TAXATION

Answer to question 1

Issues:

Tax liabilities of different receipts that are received by the taxpayer resulting from the

employment will be discussed in the case study.

Rule:

Some deductions are followed by the assessable income that are involved in the

income of the taxpayer will be discussed under “sec 6-5 (1)” which states that the

characteristics of income described that it must be income and it should be convertible into

money (Ford and Dibden, 2019). The section also describes that the assessable income are

included in the income in agreement and it is mentioned in the “ordinary concept”. An

ordinary income is a voluntary or unanticipated payment that is obvious and it is received by

the taxpayer in the employment. Under “sec 6-5 (1) ITA Act 1997” describes that a tip

received by the taxi driver is taxable and it should be treated as ordinary income. “Calvert

and Wainwright (1947)” noted about this in the section (Burton, 2017).

Fringe benefit can be provided by the employer to the employee for any personal

service and it should be taxable from the employer. It can act as a motivated factor for the

employee (Pasztor and Valent, 2016). The receipts that are originated from the personal

service of taxpayer’s and is relating to the receipt is amounted and treated as ordinary

income. Relation with the receipts are established through personal services like salary and

wages. “Moorhouse and Dooland (1995)” stated through their tax commissioner that the

amount received by the taxpayer direct or indirectly from the personal service of taxpayer is

defined as ordinary earning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

LAWS OF TAXATION

Any taxable income should include any income excluding gifts that a person gets for

their personal services and this type of gifts should not be treated as taxable income of the

receiver. “Scott v FCT (1996)” noted that if any gift are given for certain services and matter

of appreciation, then it should not be treated as ordinary income and other factors regarding

this should be considered. Fringe benefit can be observed as a benefit given by the employer

to the employee during the tax year or relating to the tax payer. This definition is stated under

“sec 136 (1) FBTAA” and assumption regarding this are discussed in the section. This type

of benefit can be any interest in the real or personal property, facilities and privilege services

and also involves the benefit excluding salary which is given to the employee by the

employer in the relation of employment. The assessable value of benefit are the basis of FBT

and is should be paid by the employer with relation to the employment. Those benefit can be

direct or indirect and is related with the employment. As noted by the law court in “FCT v

J&G Knowles (2000)” that there should be a reason among the benefit and services and it

should be discernable and reasonable. Also is court described that there should be a rational

connection among the remunerations and services.

Any cash gift that is received by a person is not treated as ordinary income rather it is

amounted as capital receipts. “Hayes v FCT (1956)” described that, amongst the donor and

recipient, if there is any personal relationship then the pre-existing relationship will result in

the voluntary payment and should not be treated as voluntary earning. Any money which is

received from the family member due to any personal reason should not be treated as income

and these amounts are not assessable and treatable in the tax return hence it should not be

reported in the tax return.

LAWS OF TAXATION

Any taxable income should include any income excluding gifts that a person gets for

their personal services and this type of gifts should not be treated as taxable income of the

receiver. “Scott v FCT (1996)” noted that if any gift are given for certain services and matter

of appreciation, then it should not be treated as ordinary income and other factors regarding

this should be considered. Fringe benefit can be observed as a benefit given by the employer

to the employee during the tax year or relating to the tax payer. This definition is stated under

“sec 136 (1) FBTAA” and assumption regarding this are discussed in the section. This type

of benefit can be any interest in the real or personal property, facilities and privilege services

and also involves the benefit excluding salary which is given to the employee by the

employer in the relation of employment. The assessable value of benefit are the basis of FBT

and is should be paid by the employer with relation to the employment. Those benefit can be

direct or indirect and is related with the employment. As noted by the law court in “FCT v

J&G Knowles (2000)” that there should be a reason among the benefit and services and it

should be discernable and reasonable. Also is court described that there should be a rational

connection among the remunerations and services.

Any cash gift that is received by a person is not treated as ordinary income rather it is

amounted as capital receipts. “Hayes v FCT (1956)” described that, amongst the donor and

recipient, if there is any personal relationship then the pre-existing relationship will result in

the voluntary payment and should not be treated as voluntary earning. Any money which is

received from the family member due to any personal reason should not be treated as income

and these amounts are not assessable and treatable in the tax return hence it should not be

reported in the tax return.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

LAWS OF TAXATION

Application

From this case study, it can be observed that Emmi, the taxpayer is working part time

in Crown Melbourne Restaurant along with her studying. She received tips worth $335 from

her customer and the tips received by the taxpayer is amounted to voluntary payment that is

received in the form of “Incidence of employment”. Under “sec 6-5 (1) ITA Act 1997”,

“Calvert v Wainwright (1947)” noted that these type of tips are to be treated as ordinary

income as there is an essential relation with her activities that produces income.

Further, $25,000 payment are also received by Emmi from Crown Melbourne

restaurant in terms of employment. As noted by “Moorhouse v Dooland (1955), these

incomes received by taxpayer is provided for her personal service and it is related to her

employment. Under “sec 6-5 ITAA 1997”, these tips are chargeable as ordinary income as it

has been given with the relation with employment and provided for their personal service.

Emmi also received an expensive perfume valued as $250 by a customer. This type of

personal gift are treated as ordinary earnings and it is provided to Emmi by the customer for

her personal qualities as described under “sec 6-5 ITA Act 1997”. “Scott v FCT (1966)”

noted that this gift is a solicited gift and it cannot be observed as ordinary income because

this gift is given by appreciation for Emmi’s personal services.

Emmi was paid with entertainment event expenses by the employer. The employer

also provided Emmi with meals worth $380 and it was also consumed by her. This type of

non-salary fringe benefit is given with the relation to employment by taxpayer. “Sec 136(1)

describes about the fringe benefit given by the employer to the employee. “FCT v J&G

Knowles (2000)” noted that these benefits are connected with the necessary services and

directly given to her by the employer and the employer of Crown Melbourne restaurant

LAWS OF TAXATION

Application

From this case study, it can be observed that Emmi, the taxpayer is working part time

in Crown Melbourne Restaurant along with her studying. She received tips worth $335 from

her customer and the tips received by the taxpayer is amounted to voluntary payment that is

received in the form of “Incidence of employment”. Under “sec 6-5 (1) ITA Act 1997”,

“Calvert v Wainwright (1947)” noted that these type of tips are to be treated as ordinary

income as there is an essential relation with her activities that produces income.

Further, $25,000 payment are also received by Emmi from Crown Melbourne

restaurant in terms of employment. As noted by “Moorhouse v Dooland (1955), these

incomes received by taxpayer is provided for her personal service and it is related to her

employment. Under “sec 6-5 ITAA 1997”, these tips are chargeable as ordinary income as it

has been given with the relation with employment and provided for their personal service.

Emmi also received an expensive perfume valued as $250 by a customer. This type of

personal gift are treated as ordinary earnings and it is provided to Emmi by the customer for

her personal qualities as described under “sec 6-5 ITA Act 1997”. “Scott v FCT (1966)”

noted that this gift is a solicited gift and it cannot be observed as ordinary income because

this gift is given by appreciation for Emmi’s personal services.

Emmi was paid with entertainment event expenses by the employer. The employer

also provided Emmi with meals worth $380 and it was also consumed by her. This type of

non-salary fringe benefit is given with the relation to employment by taxpayer. “Sec 136(1)

describes about the fringe benefit given by the employer to the employee. “FCT v J&G

Knowles (2000)” noted that these benefits are connected with the necessary services and

directly given to her by the employer and the employer of Crown Melbourne restaurant

5

LAWS OF TAXATION

should pay the FBT based on the assessable value of benefit. This requirement are discussed

under “sec 66(1)”.

Emmi received $15,000 from her father as a Christmas gift during the year. “Hayes v

FCT (1956)” noted that this type of gift is a personal gift and given with to employee. There

is also a personal relation between Emmi and her father therefore this payments are not to be

treated as ordinary earnings. The given money was provided to Emmi just because of the

personal reason and it will not be treated with any activity that generated income. This

amount is not taxable for the same and will not be assessable in Emmi’s tax return report.

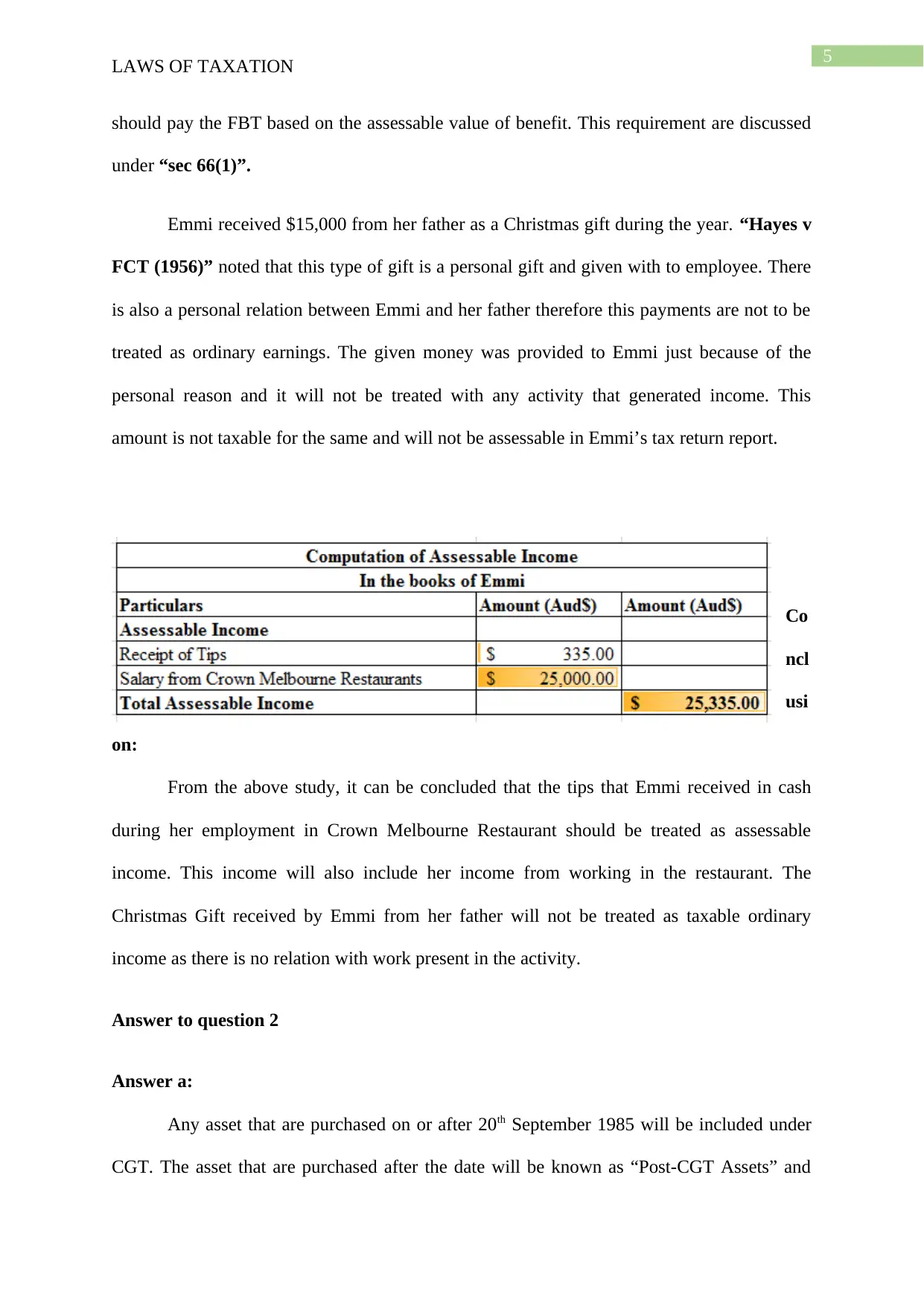

Co

ncl

usi

on:

From the above study, it can be concluded that the tips that Emmi received in cash

during her employment in Crown Melbourne Restaurant should be treated as assessable

income. This income will also include her income from working in the restaurant. The

Christmas Gift received by Emmi from her father will not be treated as taxable ordinary

income as there is no relation with work present in the activity.

Answer to question 2

Answer a:

Any asset that are purchased on or after 20th September 1985 will be included under

CGT. The asset that are purchased after the date will be known as “Post-CGT Assets” and

LAWS OF TAXATION

should pay the FBT based on the assessable value of benefit. This requirement are discussed

under “sec 66(1)”.

Emmi received $15,000 from her father as a Christmas gift during the year. “Hayes v

FCT (1956)” noted that this type of gift is a personal gift and given with to employee. There

is also a personal relation between Emmi and her father therefore this payments are not to be

treated as ordinary earnings. The given money was provided to Emmi just because of the

personal reason and it will not be treated with any activity that generated income. This

amount is not taxable for the same and will not be assessable in Emmi’s tax return report.

Co

ncl

usi

on:

From the above study, it can be concluded that the tips that Emmi received in cash

during her employment in Crown Melbourne Restaurant should be treated as assessable

income. This income will also include her income from working in the restaurant. The

Christmas Gift received by Emmi from her father will not be treated as taxable ordinary

income as there is no relation with work present in the activity.

Answer to question 2

Answer a:

Any asset that are purchased on or after 20th September 1985 will be included under

CGT. The asset that are purchased after the date will be known as “Post-CGT Assets” and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

LAWS OF TAXATION

these assets are sold and disposed afterward. Any assets bought before 20th September 1985

should be treated as “Pre-CGT Asset” and from the sale of these assets, if there is any capital

loss or gain, it should be ignored by the taxpayer (Jones, 2016).

Liu purchased a house which has acquisition cost of $55,000 in the year 1981. This

house was mainly used by Liu for the purpose of her main residence for the whole time of her

ownership and she sold the house in the market for $630,000. This house are treated as pre-

CGT asset as the taxpayer purchased this in 1981 for $55,000 and the capital gain from the

sale of the house should be levied from any tax liability (Wilson and Ashworth, 2019).

Answer b:

“Sec 108-5 ITAA 1997” defined CGT asset which include any property or lawful

rights which is not a property. “When a personal asset is used by the taxpayer for own

purpose, then it should be treated as CGT asset. “Sec 108-20 ITAA 1997” describes CGT

asset as mentioned above. “Sec 118-20(1) described that capital loss from this asset should be

ignored by the tax payer (Chung, 2017).

Liu, the taxpayer sold her car worth $8,000. She purchased the car for $37,000. This

type of asset must be categorized as personal use asset under “sec 108-20(1)”, and the capital

loss from the sale of car should be ignored by Liu.

Answer c:

The “Division 152” describes that capital gains from small business should be given

concession and to obtain this concession some conditions should be followed and satisfied by

the taxpayer of the small business (How, 2019). The conscessions are discussed below

The net worth of assets in the business should be less than $6 million and the size of

the business should be small.

LAWS OF TAXATION

these assets are sold and disposed afterward. Any assets bought before 20th September 1985

should be treated as “Pre-CGT Asset” and from the sale of these assets, if there is any capital

loss or gain, it should be ignored by the taxpayer (Jones, 2016).

Liu purchased a house which has acquisition cost of $55,000 in the year 1981. This

house was mainly used by Liu for the purpose of her main residence for the whole time of her

ownership and she sold the house in the market for $630,000. This house are treated as pre-

CGT asset as the taxpayer purchased this in 1981 for $55,000 and the capital gain from the

sale of the house should be levied from any tax liability (Wilson and Ashworth, 2019).

Answer b:

“Sec 108-5 ITAA 1997” defined CGT asset which include any property or lawful

rights which is not a property. “When a personal asset is used by the taxpayer for own

purpose, then it should be treated as CGT asset. “Sec 108-20 ITAA 1997” describes CGT

asset as mentioned above. “Sec 118-20(1) described that capital loss from this asset should be

ignored by the tax payer (Chung, 2017).

Liu, the taxpayer sold her car worth $8,000. She purchased the car for $37,000. This

type of asset must be categorized as personal use asset under “sec 108-20(1)”, and the capital

loss from the sale of car should be ignored by Liu.

Answer c:

The “Division 152” describes that capital gains from small business should be given

concession and to obtain this concession some conditions should be followed and satisfied by

the taxpayer of the small business (How, 2019). The conscessions are discussed below

The net worth of assets in the business should be less than $6 million and the size of

the business should be small.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

LAWS OF TAXATION

The criteria under CGT assets should be met by the small business. The business

should observe and follow the use of CGT assets (Weisback, 2017).

After meeting the criteria, the business is given with four concession given below

15-year exemption:

If the taxpayer held the asset for more than 15 year and the age of the taxpayer is

more than 55 years then the capital gain from selling of CGT asset should be exempted

following this exemption (Burns, 2019).

50% reduction:

Any taxpayer can qualify this concession to reduce their capital gains by 50%

followed by the general 50% discount percentage (Chung, 2017).

Retirement concession:

If the selling price of CGT asset is not more than $500,000 then this concession are

given to the small business which allows the taxpayer to simply disregard the capital gain

from the sale of asset as it is proceeded for retirement purpose only (Tapiolas, 2017).

Roll-over relief:

This concession is provided when the taxpayer purchases a replacement asset.

In this situation, Liu had a small business studio that she sold to the buyer for

$125,000. This included photography asset worth $53,000 and goodwill worth $50,000. The

net value of asset is less that $6 million therefore Liu is eligible for claiming the CGT

concession under small business. Further, Liu is 55 years old and the asset she owned is aged

more than 15 years therefore, as described in “Subdivision 152-B” she is eligible for

LAWS OF TAXATION

The criteria under CGT assets should be met by the small business. The business

should observe and follow the use of CGT assets (Weisback, 2017).

After meeting the criteria, the business is given with four concession given below

15-year exemption:

If the taxpayer held the asset for more than 15 year and the age of the taxpayer is

more than 55 years then the capital gain from selling of CGT asset should be exempted

following this exemption (Burns, 2019).

50% reduction:

Any taxpayer can qualify this concession to reduce their capital gains by 50%

followed by the general 50% discount percentage (Chung, 2017).

Retirement concession:

If the selling price of CGT asset is not more than $500,000 then this concession are

given to the small business which allows the taxpayer to simply disregard the capital gain

from the sale of asset as it is proceeded for retirement purpose only (Tapiolas, 2017).

Roll-over relief:

This concession is provided when the taxpayer purchases a replacement asset.

In this situation, Liu had a small business studio that she sold to the buyer for

$125,000. This included photography asset worth $53,000 and goodwill worth $50,000. The

net value of asset is less that $6 million therefore Liu is eligible for claiming the CGT

concession under small business. Further, Liu is 55 years old and the asset she owned is aged

more than 15 years therefore, as described in “Subdivision 152-B” she is eligible for

8

LAWS OF TAXATION

claiming 15 year exemption. She will be grated with full exemption from CGT asset as

described in the section (Geljic, Koustas and Burke, 2016).

Answer d:

Certain rules are there applied on the personal use of asset. “Section 108-20 (1)”

noted that any loss from the sale of personal use asset should be disregarded by the taxpayer.

In the scenario, Liu purchased a furniture for $4,800 which she sold for $2,000. This furniture

is defined as personal use asset under “section 108-20 ITAA 1997”. Under this “sec118-

20(1)” the capital loss from the sale of this furniture should be disregarded by the taxpayer.

Answer e:

Under “sec 108-10 ITAA 1997” collectibles are a type of asset which is primarily

used by the taxpayer of kept for personal purpose and enjoyment. “Section 108-10 (2)”

described some type of assets which can be stamps, paintings, coins and sculptures. Any sum

of capital gain from this type of assets should be ignored when the cost of asset is less than

$500 as noted under “sec 118-10 (1)”. This rules are needed to be understood before

evaluating collectibles and judging their taxability (O’Connell, 2017).

In this scenario, Liu bought many used paintings from second hand shop. The costs of

these paintings are less than $500 and all the paintings were sold for $28,000. Those

paintings should be treated as collectibles under “sec 108-10 (2) ITAA 1997” as the capital

gains from the paintings will be ignored under “sec 118-10 (1)” because the costs of the

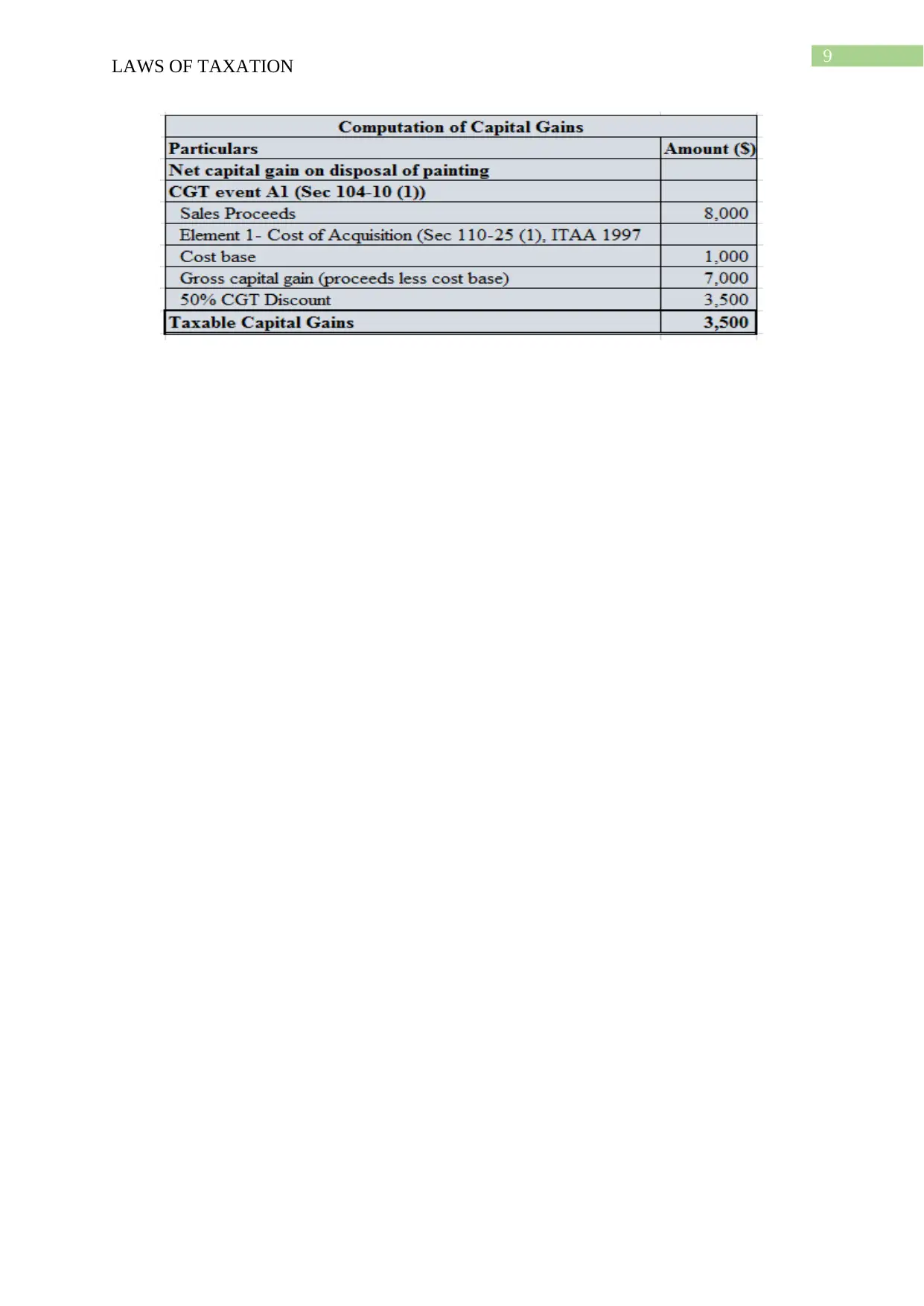

paintings are less than $500. Additionally, Liu, the taxpayer had also sold one of his paintings

for $1000 that was purchased from an artist which costs him $8000.As this sale of painting

has led to capital gain, the income from the sale of paintings will be treated under “sec 102-

5” and this painting will be treated as statutory income.

LAWS OF TAXATION

claiming 15 year exemption. She will be grated with full exemption from CGT asset as

described in the section (Geljic, Koustas and Burke, 2016).

Answer d:

Certain rules are there applied on the personal use of asset. “Section 108-20 (1)”

noted that any loss from the sale of personal use asset should be disregarded by the taxpayer.

In the scenario, Liu purchased a furniture for $4,800 which she sold for $2,000. This furniture

is defined as personal use asset under “section 108-20 ITAA 1997”. Under this “sec118-

20(1)” the capital loss from the sale of this furniture should be disregarded by the taxpayer.

Answer e:

Under “sec 108-10 ITAA 1997” collectibles are a type of asset which is primarily

used by the taxpayer of kept for personal purpose and enjoyment. “Section 108-10 (2)”

described some type of assets which can be stamps, paintings, coins and sculptures. Any sum

of capital gain from this type of assets should be ignored when the cost of asset is less than

$500 as noted under “sec 118-10 (1)”. This rules are needed to be understood before

evaluating collectibles and judging their taxability (O’Connell, 2017).

In this scenario, Liu bought many used paintings from second hand shop. The costs of

these paintings are less than $500 and all the paintings were sold for $28,000. Those

paintings should be treated as collectibles under “sec 108-10 (2) ITAA 1997” as the capital

gains from the paintings will be ignored under “sec 118-10 (1)” because the costs of the

paintings are less than $500. Additionally, Liu, the taxpayer had also sold one of his paintings

for $1000 that was purchased from an artist which costs him $8000.As this sale of painting

has led to capital gain, the income from the sale of paintings will be treated under “sec 102-

5” and this painting will be treated as statutory income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

LAWS OF TAXATION

LAWS OF TAXATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

LAWS OF TAXATION

References

Burns, A., 2019. Goodwill hunting. Taxation in Australia, 53(9), p.475.

Burton, M., 2017. A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax. J. Austl. Tax'n, 19, p.50.

Chung, E., 2017. The absolute beginner's guide to capital gains tax. REIQ Journal, (May

2017), p.35.

Ford, S. and Dibden, A., 2019. Gifted assets, valuation and ordinary income. Taxation in

Australia, 53(10), p.560.

Geljic, S., Koustas, H. and Burke, D., 2016. Small business restructure roll-over. Taxation in

Australia, 50(7), p.404.

How, S., 2019. Tax consolidation for SMEs. Tax Specialist, 23(1), p.2.

Jones, D., 2016. Capital gains tax: The rise of market value?. Taxation in Australia, 51(2),

p.67.

O’Connell, A., 2017. Australia. In Capital Gains Taxation. Edward Elgar Publishing.

Pasztor, J. and Valent, S., 2016. Fringe Benefit-still a Motivation?. In Proceedings of

FIKUSZ Symposium for Young Researchers (p. 127). Óbuda University Keleti Károly

Faculty of Economics.

Tapiolas, L., 2017. Restructuring: Rollovers, Small business restructure rollovers and small

business CGT concessions.

LAWS OF TAXATION

References

Burns, A., 2019. Goodwill hunting. Taxation in Australia, 53(9), p.475.

Burton, M., 2017. A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax. J. Austl. Tax'n, 19, p.50.

Chung, E., 2017. The absolute beginner's guide to capital gains tax. REIQ Journal, (May

2017), p.35.

Ford, S. and Dibden, A., 2019. Gifted assets, valuation and ordinary income. Taxation in

Australia, 53(10), p.560.

Geljic, S., Koustas, H. and Burke, D., 2016. Small business restructure roll-over. Taxation in

Australia, 50(7), p.404.

How, S., 2019. Tax consolidation for SMEs. Tax Specialist, 23(1), p.2.

Jones, D., 2016. Capital gains tax: The rise of market value?. Taxation in Australia, 51(2),

p.67.

O’Connell, A., 2017. Australia. In Capital Gains Taxation. Edward Elgar Publishing.

Pasztor, J. and Valent, S., 2016. Fringe Benefit-still a Motivation?. In Proceedings of

FIKUSZ Symposium for Young Researchers (p. 127). Óbuda University Keleti Károly

Faculty of Economics.

Tapiolas, L., 2017. Restructuring: Rollovers, Small business restructure rollovers and small

business CGT concessions.

11

LAWS OF TAXATION

Weisbach, D.A., 2017. Capital Gains Taxation and Corporate Investment. National Tax

Journal, 70(3), pp.621-642.

Wilson, B. and Ashworth, C., 2019. Deceased estates, real property and real issues. Taxation

in Australia, 54(6), p.307.

LAWS OF TAXATION

Weisbach, D.A., 2017. Capital Gains Taxation and Corporate Investment. National Tax

Journal, 70(3), pp.621-642.

Wilson, B. and Ashworth, C., 2019. Deceased estates, real property and real issues. Taxation

in Australia, 54(6), p.307.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.