TAXATION LAW Assignment - Taxation Law - Semester 2, 2024

VerifiedAdded on 2020/02/24

|14

|3106

|30

Homework Assignment

AI Summary

This document provides a comprehensive solution to a Taxation Law assignment, addressing various aspects of Australian taxation. It begins with an overview of the constitutional basis for taxation in Australia, including relevant sections of the Constitution and key legislation such as the Income Tax Assessment Act. The solution explores the sources of Australian tax law, including legislation, case law, and taxation rulings. It covers topics such as residential status, Medicare Levy, and the application of the Competition and Consumer Act. The assignment delves into specific provisions of the Income Tax Assessment Act, including deductions for losses arising from theft and the deductibility of repair expenses. The solution also examines methods for valuing stock items and provides calculations for tax liabilities based on income levels. Furthermore, the assignment analyzes the deductibility of various expenses, including tax agent fees and solicitor fees, and defines the concept of residency for tax purposes. It also explores the treatment of different types of income, including ordinary income, statutory income, and gifts. The solution also includes a section on the PAYG (Pay As You Go) income tax instalment system.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to Part A:.......................................................................................................................2

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to Question 3:................................................................................................................2

Answer to question 4:.................................................................................................................3

Answer to Question 5.................................................................................................................3

Answer to Question 6.................................................................................................................3

Answer to Question 7.................................................................................................................4

Answer to Question 8.................................................................................................................4

Answer to Question 9.................................................................................................................5

Answer to question 10:...............................................................................................................5

Part B:.........................................................................................................................................5

Answer to Part C:.......................................................................................................................7

Answer to Part D:.......................................................................................................................8

Answer to Part E:.......................................................................................................................9

Reference List:.........................................................................................................................11

Table of Contents

Answer to Part A:.......................................................................................................................2

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to Question 3:................................................................................................................2

Answer to question 4:.................................................................................................................3

Answer to Question 5.................................................................................................................3

Answer to Question 6.................................................................................................................3

Answer to Question 7.................................................................................................................4

Answer to Question 8.................................................................................................................4

Answer to Question 9.................................................................................................................5

Answer to question 10:...............................................................................................................5

Part B:.........................................................................................................................................5

Answer to Part C:.......................................................................................................................7

Answer to Part D:.......................................................................................................................8

Answer to Part E:.......................................................................................................................9

Reference List:.........................................................................................................................11

2TAXATION LAW

Answer to Part A:

Answer to question 1:

In compliance with the Constitution of Australia, the main source of Commonwealth

Parliament’s power of taxation generally comes from the sections 51(ii), 53, 55, 90 and 96.

As defined under Section 51(ii) of Australian Constitution, the power of creating laws in

relation to tax is assigned with the Commonwealth Parliament (Pinto, 2011). It can be stated

that there are some conditions that those laws does not create any form of differentiation

between the states or parts of the states.

Answer to question 2:

Acts are mainly designed to establish the laws relating to tax. Hence, this forms the

primary source of Australian Taxation Laws that originates from the legislation with

numerous Parliamentary Acts and Regulations that are delegated in the legislation

(Braithwaite, 2017). The second source of Tax in Australia are the case laws that helps in

interpreting the legislation such as the judgment of court, tribunals etc. The third source of

taxation in Australia is the taxation rulings stated by the Commissioner of Taxation.

Answer to Question 3:

As per the Taxation Ruling TR 98/17 it is concerned with the residential status of an

individual entering in Australia (Cao et al., 2015). The Taxation Ruling TR 98/17 of is

applicable to most of the individuals that are entering Australia and comprises of the

following;

a. Any Migrants

Answer to Part A:

Answer to question 1:

In compliance with the Constitution of Australia, the main source of Commonwealth

Parliament’s power of taxation generally comes from the sections 51(ii), 53, 55, 90 and 96.

As defined under Section 51(ii) of Australian Constitution, the power of creating laws in

relation to tax is assigned with the Commonwealth Parliament (Pinto, 2011). It can be stated

that there are some conditions that those laws does not create any form of differentiation

between the states or parts of the states.

Answer to question 2:

Acts are mainly designed to establish the laws relating to tax. Hence, this forms the

primary source of Australian Taxation Laws that originates from the legislation with

numerous Parliamentary Acts and Regulations that are delegated in the legislation

(Braithwaite, 2017). The second source of Tax in Australia are the case laws that helps in

interpreting the legislation such as the judgment of court, tribunals etc. The third source of

taxation in Australia is the taxation rulings stated by the Commissioner of Taxation.

Answer to Question 3:

As per the Taxation Ruling TR 98/17 it is concerned with the residential status of an

individual entering in Australia (Cao et al., 2015). The Taxation Ruling TR 98/17 of is

applicable to most of the individuals that are entering Australia and comprises of the

following;

a. Any Migrants

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

b. Any overseas student visited Australia for the purpose of study

c. Any visiting coming to Australia

d. Any form of workers arriving in Australia for the purpose of planned contracts of

employment

Answer to question 4:

Medicare Levy in Australia is designed to provide residents with the health care

access. Medicare levy is required to be paid by the taxpayers at a rate of 2% to partly fund for

the health care access (Saad, 2014). If an individual’s assessable income is below the certain

limit then that person Medicare levy might be lowered or at times they might not be required

to pay any form of levy. Conversely, an individual is required to pay Medicare Levy

surcharge if an individuals have the health insurance of a private hospital.

Answer to Question 5

As defined under the Schedule 2 of the Competition and Consumer Act 2010, any

form of misconduct that is deceptive or false shall be barred under Section 18 of the

Australian Consumer Law (Woellner et al., 2016). Section 12DA of the Australian

Securities and Investment Commission Act 2001 defines the prohibition of deceptive and

false conduct of financial service. The main purpose of this principle is to offer security and

safety to the consumers from being misguided by deceptive business practices.

Answer to Question 6

Section 25-45 of the Income Tax Assessment Act 1997 is concerned with the lost arising out

of theft (Robin, 2017). The section clearly defines the loss in regard to the money that cannot

be deducted by one if;

b. Any overseas student visited Australia for the purpose of study

c. Any visiting coming to Australia

d. Any form of workers arriving in Australia for the purpose of planned contracts of

employment

Answer to question 4:

Medicare Levy in Australia is designed to provide residents with the health care

access. Medicare levy is required to be paid by the taxpayers at a rate of 2% to partly fund for

the health care access (Saad, 2014). If an individual’s assessable income is below the certain

limit then that person Medicare levy might be lowered or at times they might not be required

to pay any form of levy. Conversely, an individual is required to pay Medicare Levy

surcharge if an individuals have the health insurance of a private hospital.

Answer to Question 5

As defined under the Schedule 2 of the Competition and Consumer Act 2010, any

form of misconduct that is deceptive or false shall be barred under Section 18 of the

Australian Consumer Law (Woellner et al., 2016). Section 12DA of the Australian

Securities and Investment Commission Act 2001 defines the prohibition of deceptive and

false conduct of financial service. The main purpose of this principle is to offer security and

safety to the consumers from being misguided by deceptive business practices.

Answer to Question 6

Section 25-45 of the Income Tax Assessment Act 1997 is concerned with the lost arising out

of theft (Robin, 2017). The section clearly defines the loss in regard to the money that cannot

be deducted by one if;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

a. An individual determines the loss in the income year

b. The loss that is determined is resulting out of the activities in the form of theft,

stealing, defalcation etc.

c. The amount should be involved in the assessable income of the individual or might be

an earlier year of income.

Answer to Question 7

The Case of W Thomas & Co Pty Ltd v FC of T (1965), is concerned with the

deduction that a tax payer can claim for undertaking repair (Blakelock & King, 2017). As

evident from the case, the taxpayer is considered as flour miller and grain merchant who

purchased a building and some of the parts were in a broken state. An individual then took

the extensive amount of repairs of work that comprised of roof, guttering, walls and floor of

the building. Then the taxpayer in this case claimed deductions for the cost of repair.

However, it can be stated that the amount cannot be claimed as allowable deductions since

the expenditure was not for the purpose of the generating assessable income of the taxpayer.

Answer to Question 8

A taxpayer can undertake one of the following method of valuing stock item at the end of

income year which are as follows;

a. The taxpayer can adopt cost price method by bringing all the cost related stock at its

current location and situation

b. Market selling value that uses stock current value if it is sold in the normal course of

business

c. Method of replacement value where the cost to acquire is relatively same

a. An individual determines the loss in the income year

b. The loss that is determined is resulting out of the activities in the form of theft,

stealing, defalcation etc.

c. The amount should be involved in the assessable income of the individual or might be

an earlier year of income.

Answer to Question 7

The Case of W Thomas & Co Pty Ltd v FC of T (1965), is concerned with the

deduction that a tax payer can claim for undertaking repair (Blakelock & King, 2017). As

evident from the case, the taxpayer is considered as flour miller and grain merchant who

purchased a building and some of the parts were in a broken state. An individual then took

the extensive amount of repairs of work that comprised of roof, guttering, walls and floor of

the building. Then the taxpayer in this case claimed deductions for the cost of repair.

However, it can be stated that the amount cannot be claimed as allowable deductions since

the expenditure was not for the purpose of the generating assessable income of the taxpayer.

Answer to Question 8

A taxpayer can undertake one of the following method of valuing stock item at the end of

income year which are as follows;

a. The taxpayer can adopt cost price method by bringing all the cost related stock at its

current location and situation

b. Market selling value that uses stock current value if it is sold in the normal course of

business

c. Method of replacement value where the cost to acquire is relatively same

5TAXATION LAW

Answer to Question 9

An individual with a taxable income of $45,000 in the year 2016/17 shall be liable to

pay tax of $3752 and additionally the taxpayer would be required to pay 32.5c for every $1

over $37,000.

Answer to question 10:

The PAYG can be defined as Pay As You Go income tax instalment system which

comprises of the payments that are made constantly by the employers and other taxpayers

(Fry, 2017). An instalment method of collecting income tax is used to make regular payments

towards the anticipated income tax liability of a person for the year. Individual paying PAYG

instalments will be required to file a tax return for the year.

Part B:

As defined under Division 8 of the Income Tax Assessment Act 1997 it provides the

rules that is concerned with the deductibility of outgoing and losses (Tran-Nam & Walpole,

2016). The division helps in making distinction between the general deductions with

reference to discussion made under section 8-1 of the Income Tax Assessment Act 1997

along with the specific deductions that is provided under section 8-5 of the Income tax

Assessment Act 1997. As defined under section 8-1 of the Income Tax Assessment Act 1997

a taxpayer can be allowed for claiming allowable deductions for the loss or outgoing that has

been occurred for;

a. Generating and producing the taxable income

b. The expenditure that is occurred is related with the business activities of the taxpayers

As defined under section 8-5 of the Income tax Assessment Act 1997 an individual is

allowed to claim specific deductions from the taxable income (James, 2016). As evident from

Answer to Question 9

An individual with a taxable income of $45,000 in the year 2016/17 shall be liable to

pay tax of $3752 and additionally the taxpayer would be required to pay 32.5c for every $1

over $37,000.

Answer to question 10:

The PAYG can be defined as Pay As You Go income tax instalment system which

comprises of the payments that are made constantly by the employers and other taxpayers

(Fry, 2017). An instalment method of collecting income tax is used to make regular payments

towards the anticipated income tax liability of a person for the year. Individual paying PAYG

instalments will be required to file a tax return for the year.

Part B:

As defined under Division 8 of the Income Tax Assessment Act 1997 it provides the

rules that is concerned with the deductibility of outgoing and losses (Tran-Nam & Walpole,

2016). The division helps in making distinction between the general deductions with

reference to discussion made under section 8-1 of the Income Tax Assessment Act 1997

along with the specific deductions that is provided under section 8-5 of the Income tax

Assessment Act 1997. As defined under section 8-1 of the Income Tax Assessment Act 1997

a taxpayer can be allowed for claiming allowable deductions for the loss or outgoing that has

been occurred for;

a. Generating and producing the taxable income

b. The expenditure that is occurred is related with the business activities of the taxpayers

As defined under section 8-5 of the Income tax Assessment Act 1997 an individual is

allowed to claim specific deductions from the taxable income (James, 2016). As evident from

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

the present case Ram has incurred three forms of expenditure and the deductibility of the

nature is defined under the stated section. Section 25-5 of the Income Tax Assessment Act

1997 defines that the expenditure have been occurred for administrating the tax affairs that

can be allowed as deductions. Hence, the taxpayer can claim deductions for the cost of

accounting and the fees incurred for tax agent. As evident Ram incurred the solicitor expense

so that it can draft an objection against the assessment.

As defined under Para 11 of the Taxation Ruling 2011/5 it defines that a person on not

being satisfied with the assessment the taxpayer can bring forward the objection in regard to

the provision defined under section 175A(1) of the Income Tax Assessment Act 1936. The

Interpretive Decision 2002/814 is concerned with the issue relating to the deductibility of the

legal or accounting expenditure for dispute with the authorities of tax (Russell, 2016).

Therefore, with reference to section 8-1 of the Income Tax Assessment Act 1997 the

expenses incurred by Ram can be claimed as allowable deductions.

The sum that is occurred for the payment of income tax will not be considered in teh form

of allowable deductions under the section 8-1 of the Income Tax Assessment Act 1997.

Hence it can be stated that the calculations of the allowable deductions are provided below;

Calculations of Allowable Deductions of Ram:

Computation of Allowable Deduction

Particulars Amount Reason

Tax Agent fees $ 1,000.00 Section 25-5 of ITAA 97

Solicitor Fees $ 2,000.00 ATO ID 2002/814

Allowable Deduction $ 3,000.00

Table 1: Allowable Deduction

(Source: Created by Author)

the present case Ram has incurred three forms of expenditure and the deductibility of the

nature is defined under the stated section. Section 25-5 of the Income Tax Assessment Act

1997 defines that the expenditure have been occurred for administrating the tax affairs that

can be allowed as deductions. Hence, the taxpayer can claim deductions for the cost of

accounting and the fees incurred for tax agent. As evident Ram incurred the solicitor expense

so that it can draft an objection against the assessment.

As defined under Para 11 of the Taxation Ruling 2011/5 it defines that a person on not

being satisfied with the assessment the taxpayer can bring forward the objection in regard to

the provision defined under section 175A(1) of the Income Tax Assessment Act 1936. The

Interpretive Decision 2002/814 is concerned with the issue relating to the deductibility of the

legal or accounting expenditure for dispute with the authorities of tax (Russell, 2016).

Therefore, with reference to section 8-1 of the Income Tax Assessment Act 1997 the

expenses incurred by Ram can be claimed as allowable deductions.

The sum that is occurred for the payment of income tax will not be considered in teh form

of allowable deductions under the section 8-1 of the Income Tax Assessment Act 1997.

Hence it can be stated that the calculations of the allowable deductions are provided below;

Calculations of Allowable Deductions of Ram:

Computation of Allowable Deduction

Particulars Amount Reason

Tax Agent fees $ 1,000.00 Section 25-5 of ITAA 97

Solicitor Fees $ 2,000.00 ATO ID 2002/814

Allowable Deduction $ 3,000.00

Table 1: Allowable Deduction

(Source: Created by Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to Part C:

The term “Resident” is stated under section 995-1 of the Income Tax Assessment Act

1997 which explains that an individual will be considered as Australian resident for the

purpose of taxation (Dunne et al., 2016). Section 6-1 of the Income Tax Assessment Act

1936 lays down definition of resident and reflects the primary test for deciding the residential

status of the individual. As defined under the Para 32 of the Taxation Ruling 98/17 it is

defined that a person can be considered as resident in compliance with the section 6-1 of the

Income tax Assessment Act 1936.

Section 6-1 of the Income tax Assessment Act 1936 defines four test of residency stated

below

a. Residential status in terms of the ordinary concept

b. Domicile test or the permanent place of abode

c. 183 days test; and

d. Superannuation fund test;

The taxpayer was born and residing in Australia will be considered as an Australian

resident for taxation purpose with ordinary concept. If an individual is not considered as

resident in terms of the ordinary concept then the statutory test is implemented in determining

the residential status and on satisfying the primary test the person shall be considered as

resident. As per the domicile test an individual with permanent place of abode in Australia

will be considered as the resident of Australia for the taxation purpose. The rule of 183 days

defines an individual to be an Australian resident if the person has been present in Australia

for a period of not less than six months either constantly or in breaks. The superannuation test

is applied for the Australian government employees working on overseas employment. The

law further defines that an individual shall be regarded as Australian resident if an individual

Answer to Part C:

The term “Resident” is stated under section 995-1 of the Income Tax Assessment Act

1997 which explains that an individual will be considered as Australian resident for the

purpose of taxation (Dunne et al., 2016). Section 6-1 of the Income Tax Assessment Act

1936 lays down definition of resident and reflects the primary test for deciding the residential

status of the individual. As defined under the Para 32 of the Taxation Ruling 98/17 it is

defined that a person can be considered as resident in compliance with the section 6-1 of the

Income tax Assessment Act 1936.

Section 6-1 of the Income tax Assessment Act 1936 defines four test of residency stated

below

a. Residential status in terms of the ordinary concept

b. Domicile test or the permanent place of abode

c. 183 days test; and

d. Superannuation fund test;

The taxpayer was born and residing in Australia will be considered as an Australian

resident for taxation purpose with ordinary concept. If an individual is not considered as

resident in terms of the ordinary concept then the statutory test is implemented in determining

the residential status and on satisfying the primary test the person shall be considered as

resident. As per the domicile test an individual with permanent place of abode in Australia

will be considered as the resident of Australia for the taxation purpose. The rule of 183 days

defines an individual to be an Australian resident if the person has been present in Australia

for a period of not less than six months either constantly or in breaks. The superannuation test

is applied for the Australian government employees working on overseas employment. The

law further defines that an individual shall be regarded as Australian resident if an individual

8TAXATION LAW

enrols in a course having a duration of more than six. As evident in the present scenario of

Tina, she arrived in Australia for the purpose of study and her stay lasted for more than 183

days. As a result of this she will be considered as the Australian resident for the purpose of

taxation.

Answer to Part D:

An individual is taxed for their income across derived from all parts of the world. As

defined under section 4-15 of the Income Tax Assessment Act 1997 it lays down that the

taxable income is computed by deducting the allowable deductions from the taxable income

(Ato.gov.au, 2017). Section 6-5 of the Income tax Assessment Act 1997 categorizes

assessable income in the form of ordinary income and the statutory income is defined under

section 6-10 of the Income tax Assessment Act 1997. On the other hand, income that does

not form the part of the ordinary income is considered as statutory income under section 6-10

of the ITAA 97. This represents that the income that is earned by Jimmy by working in

restaurant in the form of taxpayer is considered as ordinary income under and it will be

considered taxable under section 6-5 of the ITAA 97.

The tips that are received by the customers in the form of incentive which is directly

related to the employment shall be considered in the form of taxable income. The receipt of

sum by the individual will not be considered for taxation purpose. As evident from the

present scenario of Jimmy it has been found that the receipt of $250 as a gift is considered as

taxable (Ato.gov.au, 2017). There are some forms of incomes that are included in the

assessable income since they are exempted from being considered as income under section 6-

20 of the Income Tax Assessment Act 1997.

Gifts are usually not considered for taxation however if it received as in the form of

part of business activity or received in the form of income generating activity then it is

enrols in a course having a duration of more than six. As evident in the present scenario of

Tina, she arrived in Australia for the purpose of study and her stay lasted for more than 183

days. As a result of this she will be considered as the Australian resident for the purpose of

taxation.

Answer to Part D:

An individual is taxed for their income across derived from all parts of the world. As

defined under section 4-15 of the Income Tax Assessment Act 1997 it lays down that the

taxable income is computed by deducting the allowable deductions from the taxable income

(Ato.gov.au, 2017). Section 6-5 of the Income tax Assessment Act 1997 categorizes

assessable income in the form of ordinary income and the statutory income is defined under

section 6-10 of the Income tax Assessment Act 1997. On the other hand, income that does

not form the part of the ordinary income is considered as statutory income under section 6-10

of the ITAA 97. This represents that the income that is earned by Jimmy by working in

restaurant in the form of taxpayer is considered as ordinary income under and it will be

considered taxable under section 6-5 of the ITAA 97.

The tips that are received by the customers in the form of incentive which is directly

related to the employment shall be considered in the form of taxable income. The receipt of

sum by the individual will not be considered for taxation purpose. As evident from the

present scenario of Jimmy it has been found that the receipt of $250 as a gift is considered as

taxable (Ato.gov.au, 2017). There are some forms of incomes that are included in the

assessable income since they are exempted from being considered as income under section 6-

20 of the Income Tax Assessment Act 1997.

Gifts are usually not considered for taxation however if it received as in the form of

part of business activity or received in the form of income generating activity then it is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

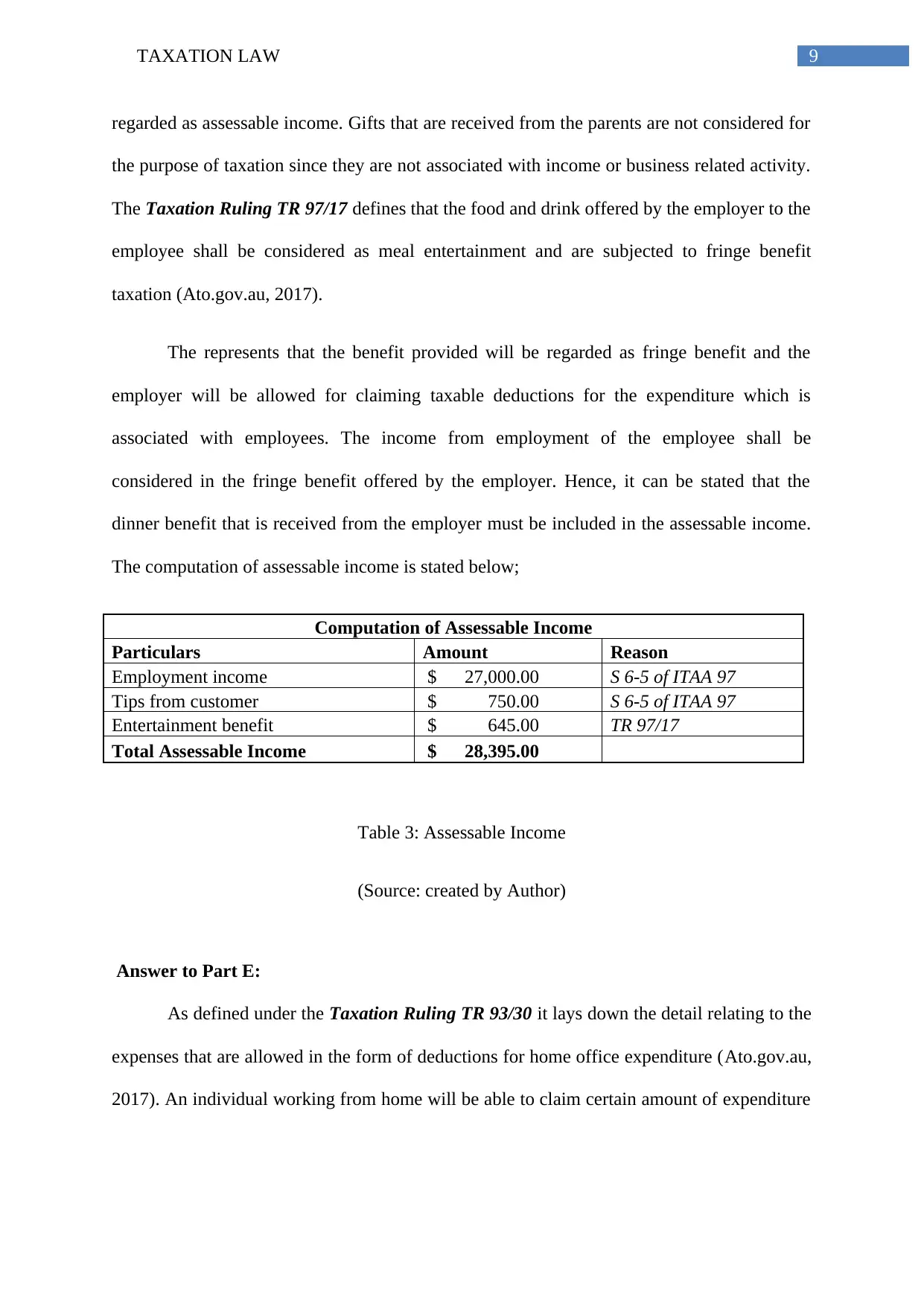

regarded as assessable income. Gifts that are received from the parents are not considered for

the purpose of taxation since they are not associated with income or business related activity.

The Taxation Ruling TR 97/17 defines that the food and drink offered by the employer to the

employee shall be considered as meal entertainment and are subjected to fringe benefit

taxation (Ato.gov.au, 2017).

The represents that the benefit provided will be regarded as fringe benefit and the

employer will be allowed for claiming taxable deductions for the expenditure which is

associated with employees. The income from employment of the employee shall be

considered in the fringe benefit offered by the employer. Hence, it can be stated that the

dinner benefit that is received from the employer must be included in the assessable income.

The computation of assessable income is stated below;

Computation of Assessable Income

Particulars Amount Reason

Employment income $ 27,000.00 S 6-5 of ITAA 97

Tips from customer $ 750.00 S 6-5 of ITAA 97

Entertainment benefit $ 645.00 TR 97/17

Total Assessable Income $ 28,395.00

Table 3: Assessable Income

(Source: created by Author)

Answer to Part E:

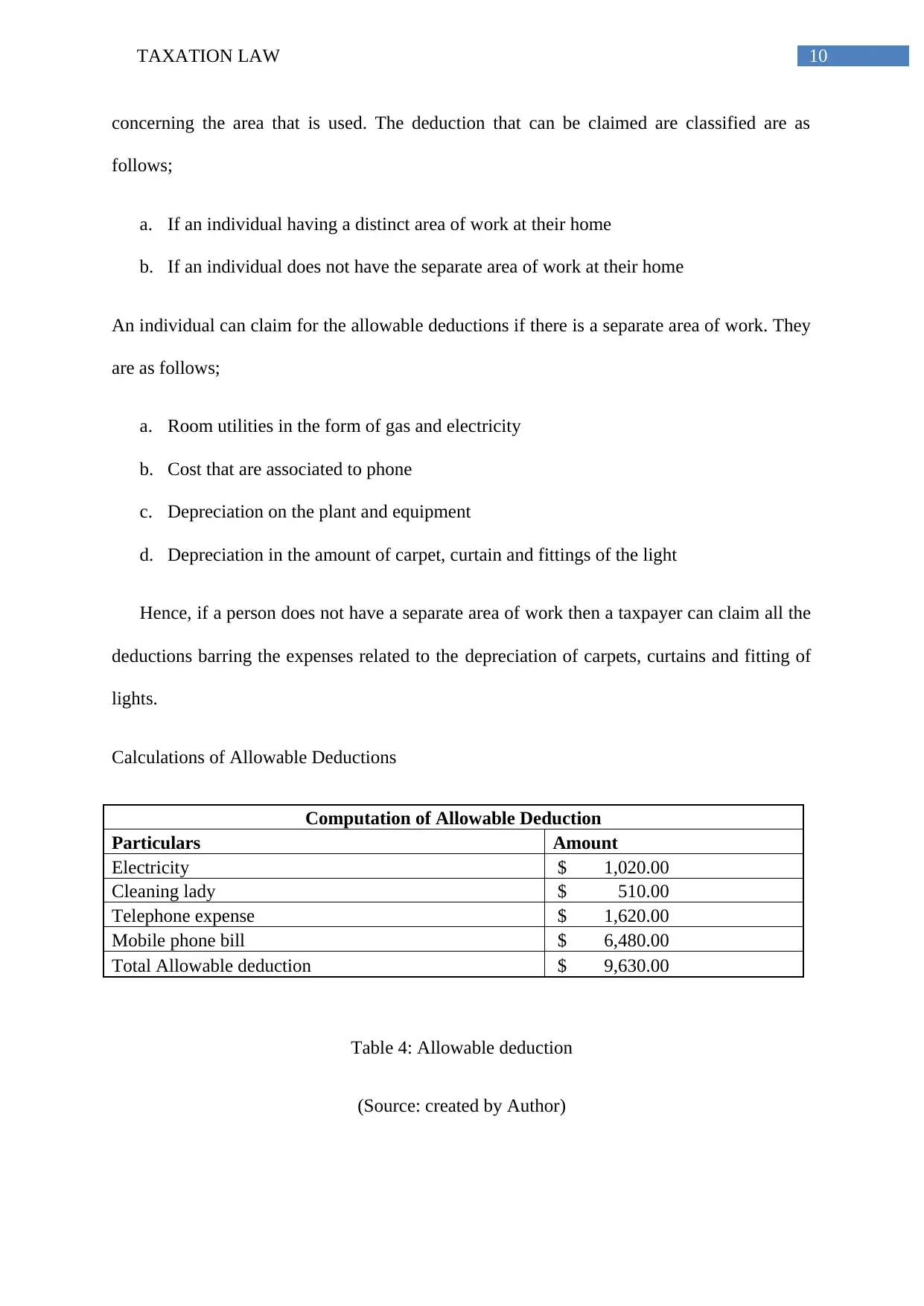

As defined under the Taxation Ruling TR 93/30 it lays down the detail relating to the

expenses that are allowed in the form of deductions for home office expenditure (Ato.gov.au,

2017). An individual working from home will be able to claim certain amount of expenditure

regarded as assessable income. Gifts that are received from the parents are not considered for

the purpose of taxation since they are not associated with income or business related activity.

The Taxation Ruling TR 97/17 defines that the food and drink offered by the employer to the

employee shall be considered as meal entertainment and are subjected to fringe benefit

taxation (Ato.gov.au, 2017).

The represents that the benefit provided will be regarded as fringe benefit and the

employer will be allowed for claiming taxable deductions for the expenditure which is

associated with employees. The income from employment of the employee shall be

considered in the fringe benefit offered by the employer. Hence, it can be stated that the

dinner benefit that is received from the employer must be included in the assessable income.

The computation of assessable income is stated below;

Computation of Assessable Income

Particulars Amount Reason

Employment income $ 27,000.00 S 6-5 of ITAA 97

Tips from customer $ 750.00 S 6-5 of ITAA 97

Entertainment benefit $ 645.00 TR 97/17

Total Assessable Income $ 28,395.00

Table 3: Assessable Income

(Source: created by Author)

Answer to Part E:

As defined under the Taxation Ruling TR 93/30 it lays down the detail relating to the

expenses that are allowed in the form of deductions for home office expenditure (Ato.gov.au,

2017). An individual working from home will be able to claim certain amount of expenditure

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

concerning the area that is used. The deduction that can be claimed are classified are as

follows;

a. If an individual having a distinct area of work at their home

b. If an individual does not have the separate area of work at their home

An individual can claim for the allowable deductions if there is a separate area of work. They

are as follows;

a. Room utilities in the form of gas and electricity

b. Cost that are associated to phone

c. Depreciation on the plant and equipment

d. Depreciation in the amount of carpet, curtain and fittings of the light

Hence, if a person does not have a separate area of work then a taxpayer can claim all the

deductions barring the expenses related to the depreciation of carpets, curtains and fitting of

lights.

Calculations of Allowable Deductions

Computation of Allowable Deduction

Particulars Amount

Electricity $ 1,020.00

Cleaning lady $ 510.00

Telephone expense $ 1,620.00

Mobile phone bill $ 6,480.00

Total Allowable deduction $ 9,630.00

Table 4: Allowable deduction

(Source: created by Author)

concerning the area that is used. The deduction that can be claimed are classified are as

follows;

a. If an individual having a distinct area of work at their home

b. If an individual does not have the separate area of work at their home

An individual can claim for the allowable deductions if there is a separate area of work. They

are as follows;

a. Room utilities in the form of gas and electricity

b. Cost that are associated to phone

c. Depreciation on the plant and equipment

d. Depreciation in the amount of carpet, curtain and fittings of the light

Hence, if a person does not have a separate area of work then a taxpayer can claim all the

deductions barring the expenses related to the depreciation of carpets, curtains and fitting of

lights.

Calculations of Allowable Deductions

Computation of Allowable Deduction

Particulars Amount

Electricity $ 1,020.00

Cleaning lady $ 510.00

Telephone expense $ 1,620.00

Mobile phone bill $ 6,480.00

Total Allowable deduction $ 9,630.00

Table 4: Allowable deduction

(Source: created by Author)

11TAXATION LAW

Reference List:

Blakelock, S., & King, P. (2017). Taxation law: The advance of ATO data matching. Proctor,

The, 37(6), 18.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

Dunne, J., Taylor, H., Batten, N., & Krapivensky, N. (2016). 2015 case review: High ATO

success rate continues. Taxation in Australia, 50(10), 609.

Fry, M. (2017). Australian taxation of offshore hubs: an examination of the law on the ability

of Australia to tax economic activity in offshore hubs and the position of the

Australian Taxation Office. The APPEA Journal, 57(1), 49-63.

James, K. (2016). The Australian Taxation Office perspective on work-related travel expense

deductions for academics. International Journal of Critical Accounting, 8(5-6), 345-

362.

Legal Database. (2017). Ato.gov.au. Retrieved 6 September 2017, from

https://www.ato.gov.au/law/view/document?Docid=TXR/TR9330/NAT/ATO/00001

Legal Database. (2017). Ato.gov.au. Retrieved 6 September 2017, from

https://www.ato.gov.au/law/view/document?docid=TXR/TR9717/NAT/ATO/00001

Reference List:

Blakelock, S., & King, P. (2017). Taxation law: The advance of ATO data matching. Proctor,

The, 37(6), 18.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

Dunne, J., Taylor, H., Batten, N., & Krapivensky, N. (2016). 2015 case review: High ATO

success rate continues. Taxation in Australia, 50(10), 609.

Fry, M. (2017). Australian taxation of offshore hubs: an examination of the law on the ability

of Australia to tax economic activity in offshore hubs and the position of the

Australian Taxation Office. The APPEA Journal, 57(1), 49-63.

James, K. (2016). The Australian Taxation Office perspective on work-related travel expense

deductions for academics. International Journal of Critical Accounting, 8(5-6), 345-

362.

Legal Database. (2017). Ato.gov.au. Retrieved 6 September 2017, from

https://www.ato.gov.au/law/view/document?Docid=TXR/TR9330/NAT/ATO/00001

Legal Database. (2017). Ato.gov.au. Retrieved 6 September 2017, from

https://www.ato.gov.au/law/view/document?docid=TXR/TR9717/NAT/ATO/00001

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.