Management Economics: Market Analysis of Barclays Plc

VerifiedAdded on 2023/01/09

|19

|3613

|70

AI Summary

This report provides an overview of Barclays Plc, its products/services, and history. It also analyzes the market factors that influence the demand for Barclays Plc's products. The report explores factors like price of substitutes, complements, consumer preferences, and demographics. The analysis helps understand how these factors impact the products and services of Barclays plc.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Economics

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

1. Overview of Barclays Plc its products/services and history.................................................................3

2. Market Analysis of Barclays Plc to evaluate factors which influence its demand...............................4

3. How factors influence the products and services of Barclays plc......................................................11

CONCLUSION.........................................................................................................................................15

REFERENCES..........................................................................................................................................17

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

1. Overview of Barclays Plc its products/services and history.................................................................3

2. Market Analysis of Barclays Plc to evaluate factors which influence its demand...............................4

3. How factors influence the products and services of Barclays plc......................................................11

CONCLUSION.........................................................................................................................................15

REFERENCES..........................................................................................................................................17

INTRODUCTION

Managerial economics describes as a business administration term which integrates in a

productive way the original contributors including such revenue and expenditure, asset etc.

Usually, a company's management uses this definition to solve any business-related problems,

particularly financial ones, which offers a variety of key approaches and concepts for making

decisions (Adam, Quansah and Kawor, 2017). The current study would expand about how

organization has used the principle of management economics to understand their past actions

and predict potential business success. This report based on the Barclays Plc which is British

multinational investment bank and financial service company. It is a financial sector organization

that provides different types of products in different banking. The company operates their

business into various nations where supply of raw materials and variation in economic structure

impacts its demand of product in large manner. In the current study, various variables are

analyzed in order to examine this dimension, which also helps determine how competition for

Barclays Plc products is relatively elastic.

MAIN BODY

1. Overview of Barclays Plc its products/services and history

The financial sector is a segment of the economy composed of companies and

organizations which provide business and commercial easy access to financial products. This

field covers a wide variety of sectors, namely banks, brokerage companies, insurance providers,

and property developers. A substantial percentage of this business produces mortgage refinance

income, which increases value as interest rates decrease. The nation's economic wellbeing is

largely dependent upon the power of its finance industry. The better the market is the safer it is.

A poor banking industry typically indicates a shrinking population. In an economy to stay

unchanged, a sustainable economic provider is likely. This sector is advancing loans for

enterprises so they can grow, offer mortgages insurance, and provide protection coverage to

protect individuals, firms, and their properties. This also helps to strengthen retirement money,

which supports hundreds of thousands of individuals. For example, Barclays PLC is a

multinational financial services provider with services for retail banking , credit cards, corporate

banking , corporate banking, asset management , and investment strategic planning. Barclays

Managerial economics describes as a business administration term which integrates in a

productive way the original contributors including such revenue and expenditure, asset etc.

Usually, a company's management uses this definition to solve any business-related problems,

particularly financial ones, which offers a variety of key approaches and concepts for making

decisions (Adam, Quansah and Kawor, 2017). The current study would expand about how

organization has used the principle of management economics to understand their past actions

and predict potential business success. This report based on the Barclays Plc which is British

multinational investment bank and financial service company. It is a financial sector organization

that provides different types of products in different banking. The company operates their

business into various nations where supply of raw materials and variation in economic structure

impacts its demand of product in large manner. In the current study, various variables are

analyzed in order to examine this dimension, which also helps determine how competition for

Barclays Plc products is relatively elastic.

MAIN BODY

1. Overview of Barclays Plc its products/services and history

The financial sector is a segment of the economy composed of companies and

organizations which provide business and commercial easy access to financial products. This

field covers a wide variety of sectors, namely banks, brokerage companies, insurance providers,

and property developers. A substantial percentage of this business produces mortgage refinance

income, which increases value as interest rates decrease. The nation's economic wellbeing is

largely dependent upon the power of its finance industry. The better the market is the safer it is.

A poor banking industry typically indicates a shrinking population. In an economy to stay

unchanged, a sustainable economic provider is likely. This sector is advancing loans for

enterprises so they can grow, offer mortgages insurance, and provide protection coverage to

protect individuals, firms, and their properties. This also helps to strengthen retirement money,

which supports hundreds of thousands of individuals. For example, Barclays PLC is a

multinational financial services provider with services for retail banking , credit cards, corporate

banking , corporate banking, asset management , and investment strategic planning. Barclays

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Bank, the Nation's biggest consumer banking company, maintains around 5,000 offices in

England and Wales and abroad, and has many branches in britain and other european. Barclay

Bank International Ltd., that has some 2,000 offices in over 70 countries, manages the

organization's international sales. The company's office is in London. The company provides

different product and services such as, retail banking, commercial, investment, private, wholesale

banking and wealth management (Adisetiawan and Surono, 2016). For the research selected this

company because it is leading finance Service Company that provides banking services in

different manner as per the customer’s requirements. The company continues to grow and

evolve, offering a broad variety of goods and services that support our consumers today fulfill

their objectives. They deliver an array of goods and services, ranging from award-winning

subprime mortgages to asset and financial advisory, and from revolutionary payment solutions to

internet banking online initially. The Group is divided into two sections: division Barclays UK

(Barclays UK) and division Barclays Global (Barclays International). Barclays UK provides

regular goods and services to UK-based commercial clients and small and medium to medium-

sized businesses (Bartkowski and et.al, 2018).

2. Market Analysis of Barclays Plc to evaluate factors which influence its demand

According to the modern economics i.e. supply and demand law, supply and demand of a

specific product or service are interrelated. Here, it is understood that the relationship between

these two main concepts is includes the central, that significantly influences the cost of goods

and services. When introducing in a given market the various goods and services, manufacturers

used it to come up with a way to offer the same as in the right value. It would attract more

potential a strong demand to meet potential buyers, through contemplated mechanism to prevent

damages at the same time. All these information can be explored by implementing the revenue

and cost principle, which states that the manufacturer must quality in order to fulfil the needs of

customers by providing the highest products of goods at a fair price. In the sense of Barclays'

marketing research, this consumer's demand is growing rapidly well after release, that also

overlaps its supply. There are a range of factors current in the background of the finance industry

which affects the supply for related goods such as personal and quality loans. It includes

alternative or complementary manufacturing costs, customer preferences & taste, customer

preferences, demographic and much more (Elena, 2016). The effect of these variables can be

evaluated in the following manner on the demand of Barclays Plc:

England and Wales and abroad, and has many branches in britain and other european. Barclay

Bank International Ltd., that has some 2,000 offices in over 70 countries, manages the

organization's international sales. The company's office is in London. The company provides

different product and services such as, retail banking, commercial, investment, private, wholesale

banking and wealth management (Adisetiawan and Surono, 2016). For the research selected this

company because it is leading finance Service Company that provides banking services in

different manner as per the customer’s requirements. The company continues to grow and

evolve, offering a broad variety of goods and services that support our consumers today fulfill

their objectives. They deliver an array of goods and services, ranging from award-winning

subprime mortgages to asset and financial advisory, and from revolutionary payment solutions to

internet banking online initially. The Group is divided into two sections: division Barclays UK

(Barclays UK) and division Barclays Global (Barclays International). Barclays UK provides

regular goods and services to UK-based commercial clients and small and medium to medium-

sized businesses (Bartkowski and et.al, 2018).

2. Market Analysis of Barclays Plc to evaluate factors which influence its demand

According to the modern economics i.e. supply and demand law, supply and demand of a

specific product or service are interrelated. Here, it is understood that the relationship between

these two main concepts is includes the central, that significantly influences the cost of goods

and services. When introducing in a given market the various goods and services, manufacturers

used it to come up with a way to offer the same as in the right value. It would attract more

potential a strong demand to meet potential buyers, through contemplated mechanism to prevent

damages at the same time. All these information can be explored by implementing the revenue

and cost principle, which states that the manufacturer must quality in order to fulfil the needs of

customers by providing the highest products of goods at a fair price. In the sense of Barclays'

marketing research, this consumer's demand is growing rapidly well after release, that also

overlaps its supply. There are a range of factors current in the background of the finance industry

which affects the supply for related goods such as personal and quality loans. It includes

alternative or complementary manufacturing costs, customer preferences & taste, customer

preferences, demographic and much more (Elena, 2016). The effect of these variables can be

evaluated in the following manner on the demand of Barclays Plc:

Price of substitutes: Influence on the price of replacement goods on just that marketplace would

also directly impact the actual demand. As far as the finance sector is concerned, the existence of

financial institutions' replacements generates a reasonable mortgage force. In this respect,

Barclays Plc's replacements include HSBC bank which is a major UK bank that provides

consumers with innovative financial services and goods. The strength of danger from these

replacements perceived as week because of expensive insurance assurance and low interest on

Barclays plc mortgages.

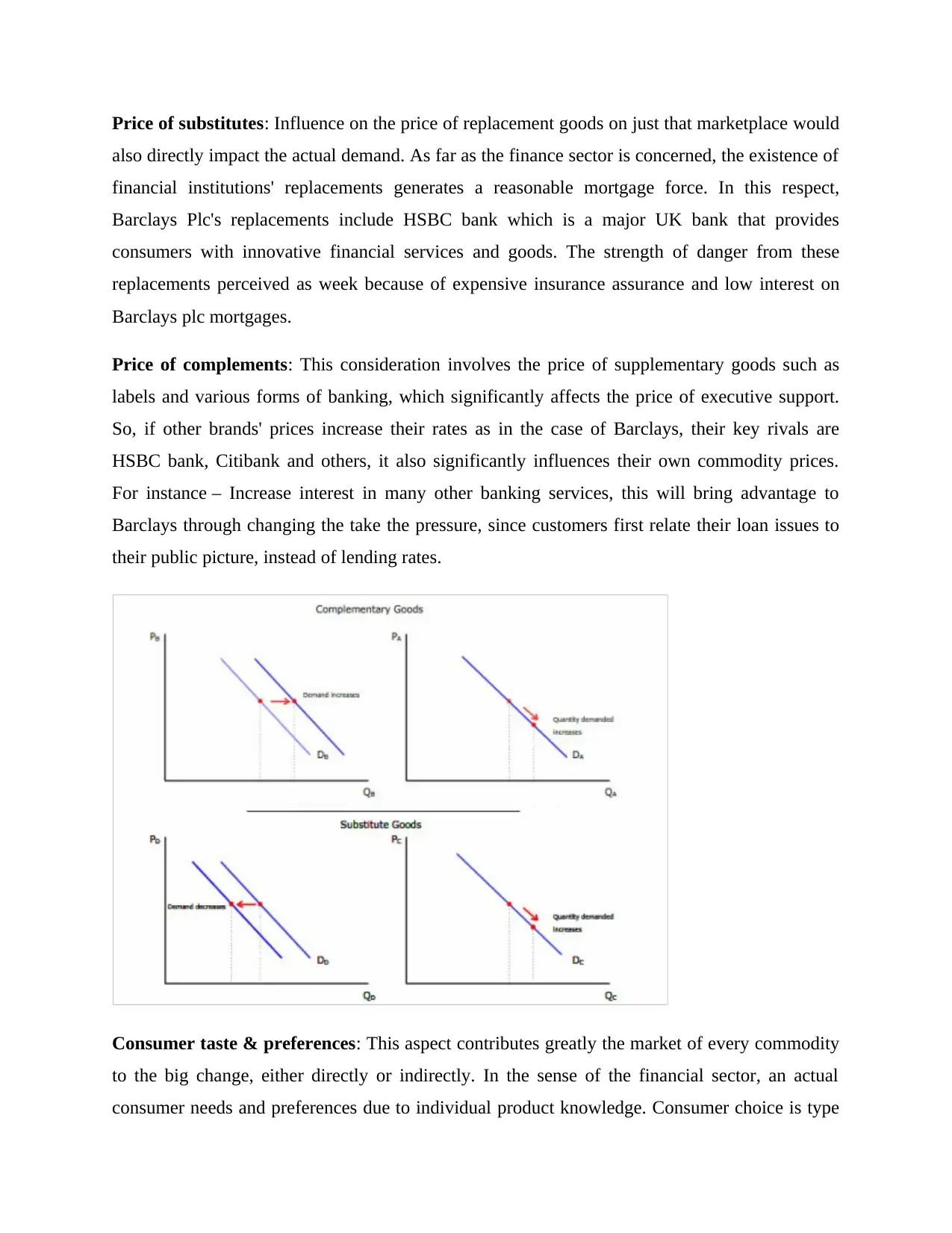

Price of complements: This consideration involves the price of supplementary goods such as

labels and various forms of banking, which significantly affects the price of executive support.

So, if other brands' prices increase their rates as in the case of Barclays, their key rivals are

HSBC bank, Citibank and others, it also significantly influences their own commodity prices.

For instance – Increase interest in many other banking services, this will bring advantage to

Barclays through changing the take the pressure, since customers first relate their loan issues to

their public picture, instead of lending rates.

Consumer taste & preferences: This aspect contributes greatly the market of every commodity

to the big change, either directly or indirectly. In the sense of the financial sector, an actual

consumer needs and preferences due to individual product knowledge. Consumer choice is type

also directly impact the actual demand. As far as the finance sector is concerned, the existence of

financial institutions' replacements generates a reasonable mortgage force. In this respect,

Barclays Plc's replacements include HSBC bank which is a major UK bank that provides

consumers with innovative financial services and goods. The strength of danger from these

replacements perceived as week because of expensive insurance assurance and low interest on

Barclays plc mortgages.

Price of complements: This consideration involves the price of supplementary goods such as

labels and various forms of banking, which significantly affects the price of executive support.

So, if other brands' prices increase their rates as in the case of Barclays, their key rivals are

HSBC bank, Citibank and others, it also significantly influences their own commodity prices.

For instance – Increase interest in many other banking services, this will bring advantage to

Barclays through changing the take the pressure, since customers first relate their loan issues to

their public picture, instead of lending rates.

Consumer taste & preferences: This aspect contributes greatly the market of every commodity

to the big change, either directly or indirectly. In the sense of the financial sector, an actual

consumer needs and preferences due to individual product knowledge. Consumer choice is type

of image a consumer likes and does not like. It is effective and it requires less taxation. The other

explanation for shifting consumer tastes and taste involves varying and successful interest rates,

whereby they seek to buy the loans that are priced and built according to their preferences and

living standards (Genovese and et.al, 2017).

Consumer expectations of price: Customers from the financial industry wanted to buy certain

cars that would provide them with better protection and pedestrian safety. The cars are strongly

expected to meet their requirements as inexpensive as per their distribution of wealth, energy

efficient, spend less in interest etc.

Demographics: Demographic shift also affects the outcome of the banking industry because, by

taking various loans, creative features and much more, customer behavior is heavily impacted.

Citizens also are easily moving to cities to enjoy the loan acquisition in order to satisfy the need.

It would also help increase the share of banking industry revenues by rising loan demand.

According to statistical evidence, there is a large market add significantly to development of the,

which also allows Barclays Plc to expand its business. Because of the change in demographics,

i.e. the migration of citizens in developing areas, the UK, Norway, the US and other advanced

nations find the largest differences between different mortgages (Hanley, Shogren and White,

2016).

This conduct is indicating a positive change in demand as per the rule of supply and

demand. As seen in the graph following, it has become obvious that consumers are able to buy

financial services at a certain value because of the highest products and great functionality. This

indicates good signs of increased sales and high profitability at the industry for Barclays

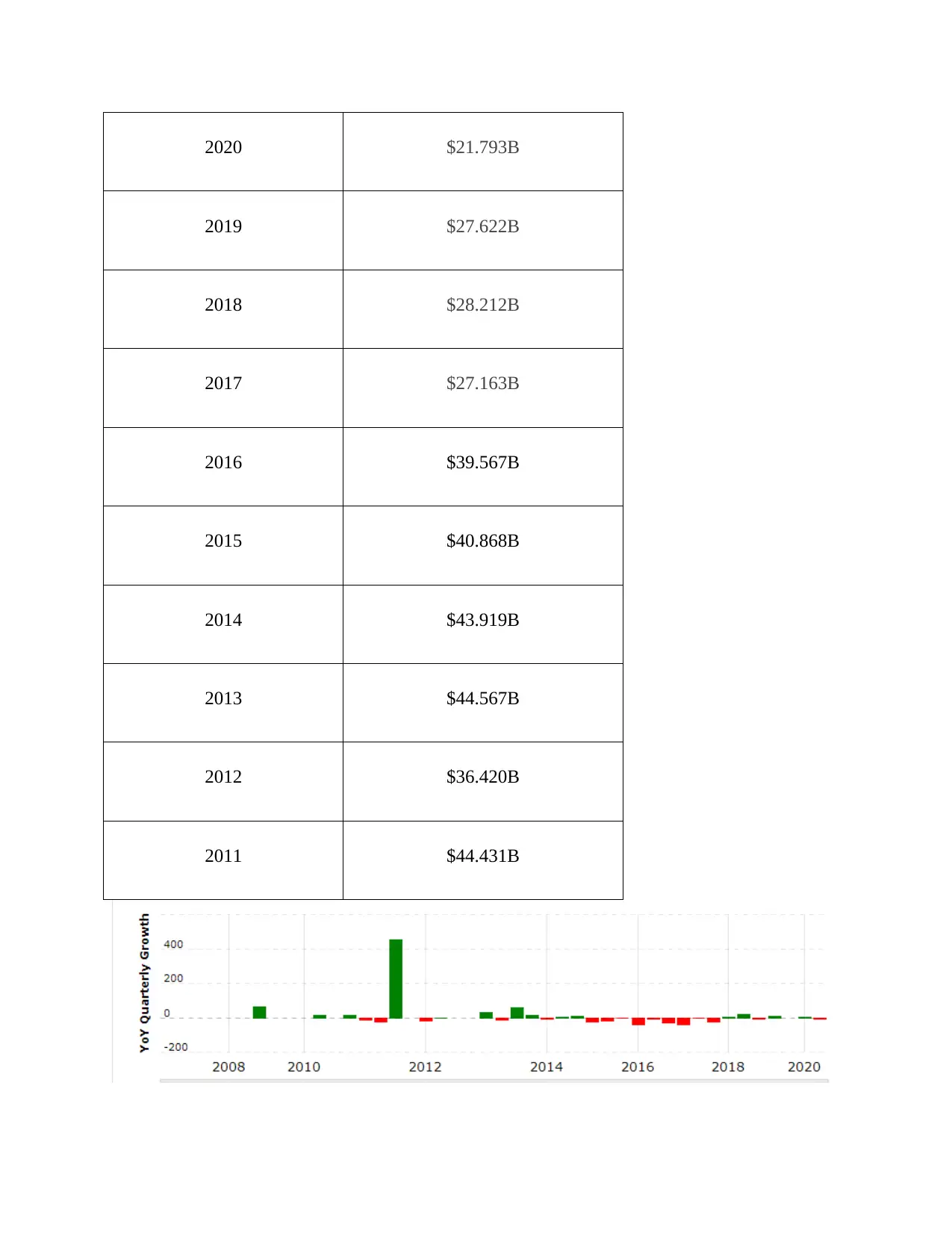

Sales Performance of Barclays Plc from last ten years –

Year Barclays Plc Annual Revenue

(Millions of US $)

2020 $6.624B

explanation for shifting consumer tastes and taste involves varying and successful interest rates,

whereby they seek to buy the loans that are priced and built according to their preferences and

living standards (Genovese and et.al, 2017).

Consumer expectations of price: Customers from the financial industry wanted to buy certain

cars that would provide them with better protection and pedestrian safety. The cars are strongly

expected to meet their requirements as inexpensive as per their distribution of wealth, energy

efficient, spend less in interest etc.

Demographics: Demographic shift also affects the outcome of the banking industry because, by

taking various loans, creative features and much more, customer behavior is heavily impacted.

Citizens also are easily moving to cities to enjoy the loan acquisition in order to satisfy the need.

It would also help increase the share of banking industry revenues by rising loan demand.

According to statistical evidence, there is a large market add significantly to development of the,

which also allows Barclays Plc to expand its business. Because of the change in demographics,

i.e. the migration of citizens in developing areas, the UK, Norway, the US and other advanced

nations find the largest differences between different mortgages (Hanley, Shogren and White,

2016).

This conduct is indicating a positive change in demand as per the rule of supply and

demand. As seen in the graph following, it has become obvious that consumers are able to buy

financial services at a certain value because of the highest products and great functionality. This

indicates good signs of increased sales and high profitability at the industry for Barclays

Sales Performance of Barclays Plc from last ten years –

Year Barclays Plc Annual Revenue

(Millions of US $)

2020 $6.624B

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2020 $21.793B

2019 $27.622B

2018 $28.212B

2017 $27.163B

2016 $39.567B

2015 $40.868B

2014 $43.919B

2013 $44.567B

2012 $36.420B

2011 $44.431B

2019 $27.622B

2018 $28.212B

2017 $27.163B

2016 $39.567B

2015 $40.868B

2014 $43.919B

2013 $44.567B

2012 $36.420B

2011 $44.431B

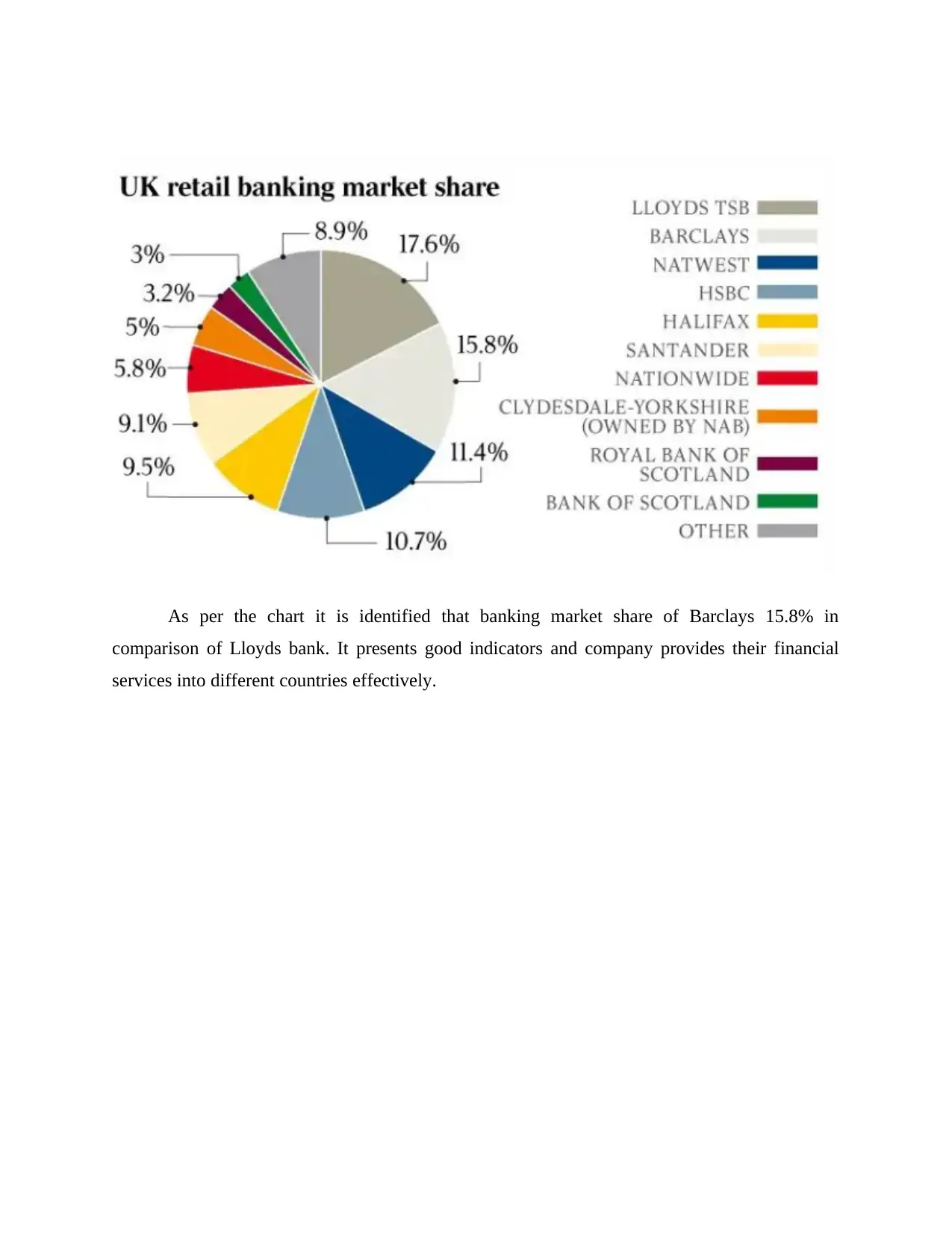

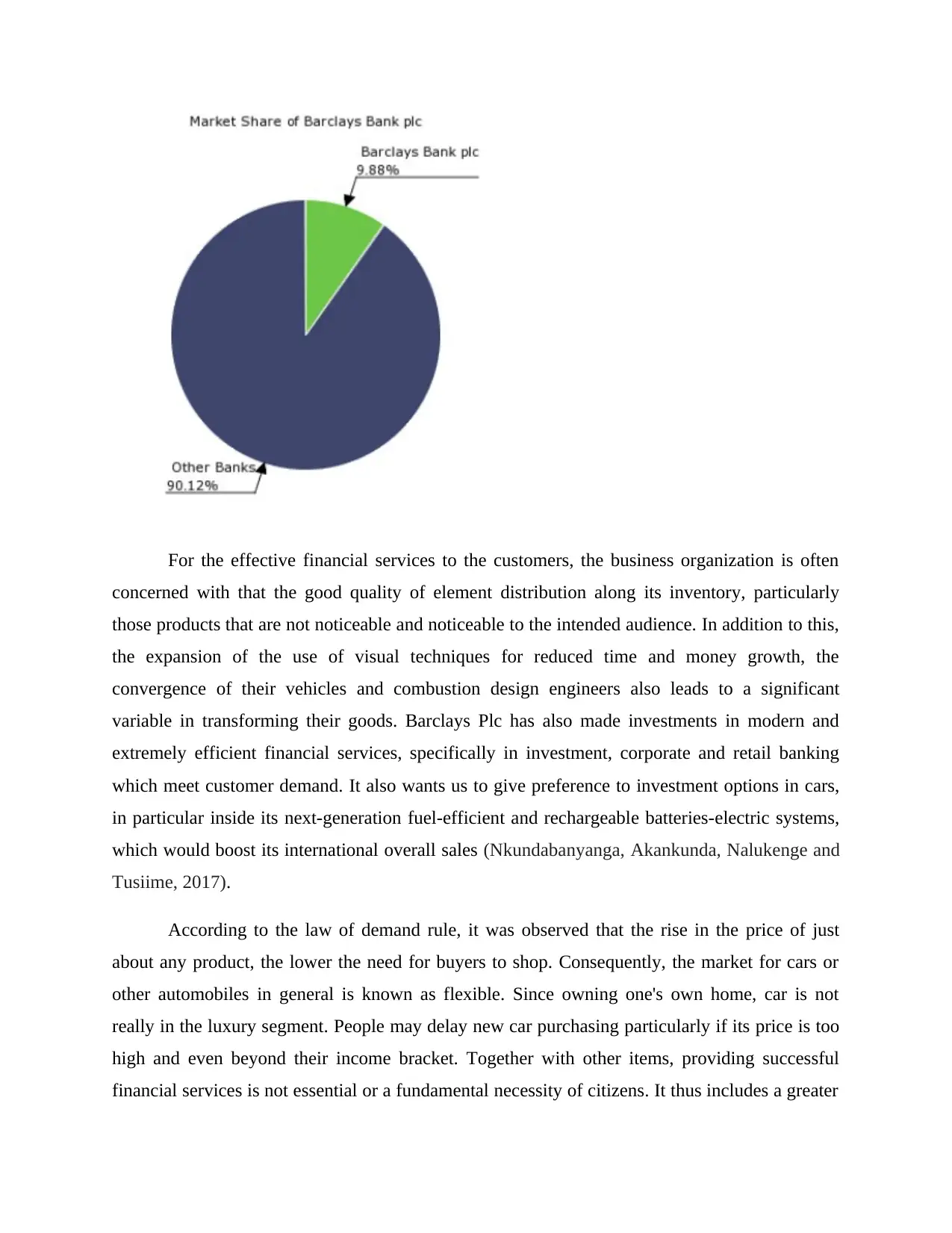

As per the chart it is identified that banking market share of Barclays 15.8% in

comparison of Lloyds bank. It presents good indicators and company provides their financial

services into different countries effectively.

comparison of Lloyds bank. It presents good indicators and company provides their financial

services into different countries effectively.

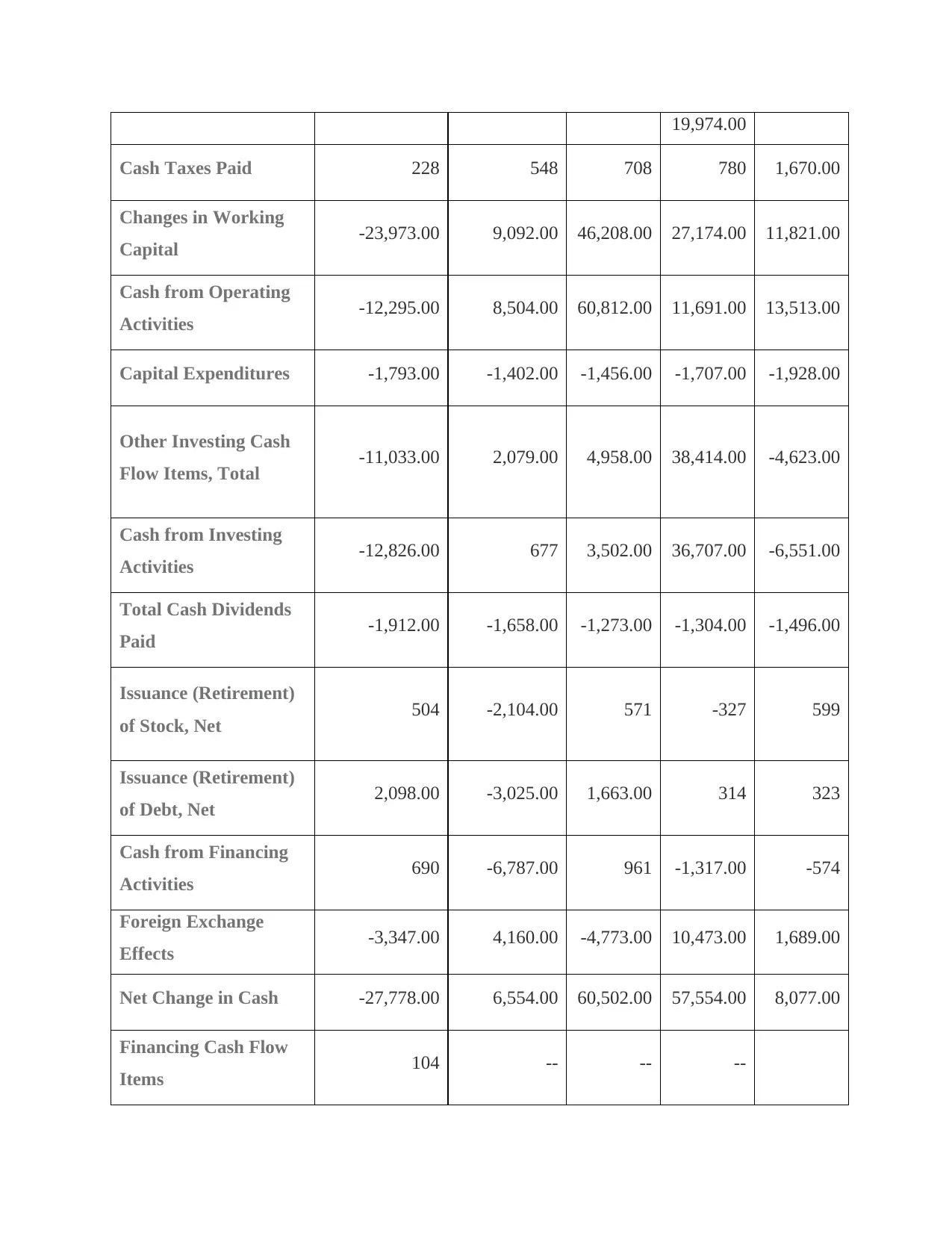

31-Dec-19 31-Dec-18

31-Dec-

17

31-Dec-

16

31-Dec-

15

Net Income/Starting

Line 4,357.00 3,494.00 3,541.00 3,230.00 1,146.00

Depreciation/Depletion 1,520.00 1,261.00 1,241.00 1,261.00 1,215.00

Non-Cash Items 5,801.00 -5,343.00 9,822.00 - -669

31-Dec-

17

31-Dec-

16

31-Dec-

15

Net Income/Starting

Line 4,357.00 3,494.00 3,541.00 3,230.00 1,146.00

Depreciation/Depletion 1,520.00 1,261.00 1,241.00 1,261.00 1,215.00

Non-Cash Items 5,801.00 -5,343.00 9,822.00 - -669

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

19,974.00

Cash Taxes Paid 228 548 708 780 1,670.00

Changes in Working

Capital -23,973.00 9,092.00 46,208.00 27,174.00 11,821.00

Cash from Operating

Activities -12,295.00 8,504.00 60,812.00 11,691.00 13,513.00

Capital Expenditures -1,793.00 -1,402.00 -1,456.00 -1,707.00 -1,928.00

Other Investing Cash

Flow Items, Total -11,033.00 2,079.00 4,958.00 38,414.00 -4,623.00

Cash from Investing

Activities -12,826.00 677 3,502.00 36,707.00 -6,551.00

Total Cash Dividends

Paid -1,912.00 -1,658.00 -1,273.00 -1,304.00 -1,496.00

Issuance (Retirement)

of Stock, Net 504 -2,104.00 571 -327 599

Issuance (Retirement)

of Debt, Net 2,098.00 -3,025.00 1,663.00 314 323

Cash from Financing

Activities 690 -6,787.00 961 -1,317.00 -574

Foreign Exchange

Effects -3,347.00 4,160.00 -4,773.00 10,473.00 1,689.00

Net Change in Cash -27,778.00 6,554.00 60,502.00 57,554.00 8,077.00

Financing Cash Flow

Items 104 -- -- --

Cash Taxes Paid 228 548 708 780 1,670.00

Changes in Working

Capital -23,973.00 9,092.00 46,208.00 27,174.00 11,821.00

Cash from Operating

Activities -12,295.00 8,504.00 60,812.00 11,691.00 13,513.00

Capital Expenditures -1,793.00 -1,402.00 -1,456.00 -1,707.00 -1,928.00

Other Investing Cash

Flow Items, Total -11,033.00 2,079.00 4,958.00 38,414.00 -4,623.00

Cash from Investing

Activities -12,826.00 677 3,502.00 36,707.00 -6,551.00

Total Cash Dividends

Paid -1,912.00 -1,658.00 -1,273.00 -1,304.00 -1,496.00

Issuance (Retirement)

of Stock, Net 504 -2,104.00 571 -327 599

Issuance (Retirement)

of Debt, Net 2,098.00 -3,025.00 1,663.00 314 323

Cash from Financing

Activities 690 -6,787.00 961 -1,317.00 -574

Foreign Exchange

Effects -3,347.00 4,160.00 -4,773.00 10,473.00 1,689.00

Net Change in Cash -27,778.00 6,554.00 60,502.00 57,554.00 8,077.00

Financing Cash Flow

Items 104 -- -- --

Using this statistical knowledge Barclays Plc's productivity and income has been

analyzed. Increasingly improved year by year, which also makes a major benefit to the growth.

Generally, it has employed much more than the financial and banking services staff members.

This demonstrates another major significant contribution to economic growth by creating jobs

for both qualified and low-qualified individuals on the job site (Hyers and Kovacova, 2018).

3. How factors influence the products and services of Barclays plc

As there are different aspects current, such as customer tastes, replacement and

alternative pricing etc. impact the market for loans in Barclays Plc, both positively and

negatively. Thus this organization is actively making improvements in goods and services to

address these demands and preserve its corporate image.

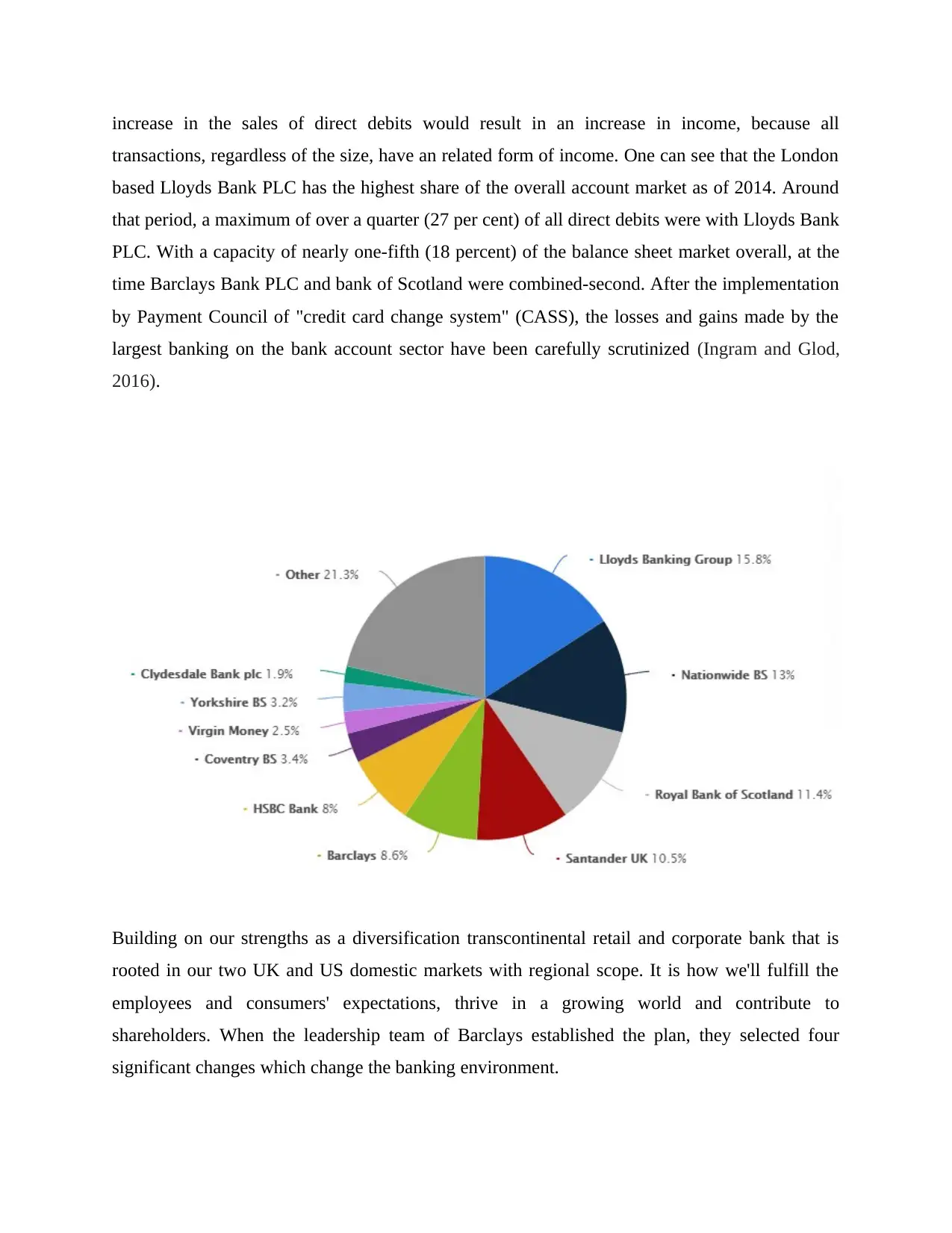

This figure reflects the market share of largest British (UK) banks' existing funds as of 2014.

Sales volume of direct debits is an significant metric for banks to compare, since a bigger

proportion of the credit card marketplace that more users are constantly holding their cash with a

specific bank. In fact, credit card share of the market is significant for the banks directly as an

analyzed. Increasingly improved year by year, which also makes a major benefit to the growth.

Generally, it has employed much more than the financial and banking services staff members.

This demonstrates another major significant contribution to economic growth by creating jobs

for both qualified and low-qualified individuals on the job site (Hyers and Kovacova, 2018).

3. How factors influence the products and services of Barclays plc

As there are different aspects current, such as customer tastes, replacement and

alternative pricing etc. impact the market for loans in Barclays Plc, both positively and

negatively. Thus this organization is actively making improvements in goods and services to

address these demands and preserve its corporate image.

This figure reflects the market share of largest British (UK) banks' existing funds as of 2014.

Sales volume of direct debits is an significant metric for banks to compare, since a bigger

proportion of the credit card marketplace that more users are constantly holding their cash with a

specific bank. In fact, credit card share of the market is significant for the banks directly as an

increase in the sales of direct debits would result in an increase in income, because all

transactions, regardless of the size, have an related form of income. One can see that the London

based Lloyds Bank PLC has the highest share of the overall account market as of 2014. Around

that period, a maximum of over a quarter (27 per cent) of all direct debits were with Lloyds Bank

PLC. With a capacity of nearly one-fifth (18 percent) of the balance sheet market overall, at the

time Barclays Bank PLC and bank of Scotland were combined-second. After the implementation

by Payment Council of "credit card change system" (CASS), the losses and gains made by the

largest banking on the bank account sector have been carefully scrutinized (Ingram and Glod,

2016).

Building on our strengths as a diversification transcontinental retail and corporate bank that is

rooted in our two UK and US domestic markets with regional scope. It is how we'll fulfill the

employees and consumers' expectations, thrive in a growing world and contribute to

shareholders. When the leadership team of Barclays established the plan, they selected four

significant changes which change the banking environment.

transactions, regardless of the size, have an related form of income. One can see that the London

based Lloyds Bank PLC has the highest share of the overall account market as of 2014. Around

that period, a maximum of over a quarter (27 per cent) of all direct debits were with Lloyds Bank

PLC. With a capacity of nearly one-fifth (18 percent) of the balance sheet market overall, at the

time Barclays Bank PLC and bank of Scotland were combined-second. After the implementation

by Payment Council of "credit card change system" (CASS), the losses and gains made by the

largest banking on the bank account sector have been carefully scrutinized (Ingram and Glod,

2016).

Building on our strengths as a diversification transcontinental retail and corporate bank that is

rooted in our two UK and US domestic markets with regional scope. It is how we'll fulfill the

employees and consumers' expectations, thrive in a growing world and contribute to

shareholders. When the leadership team of Barclays established the plan, they selected four

significant changes which change the banking environment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Regulatory landscape: After the financial crisis of 2008, the financial budget deal raised the age

equity rates that banks are expected to maintain toward balance sheet assets and rising the usage

of challenging requirements banking. Recent UK law also allows wealth management (small to

mid - size businesses finance) to be "ring-fenced" from corporate banking which has led to

Barclays UK and Barclays Global being established as two separate companies (Martin and et.al,

2017).

Capital markets: As a result of the change in policy, the added price of bank cash flow financing

has resulted in a shift in commercial debt to financial markets. As either a result, the position and

scale of capital markets has increased dramatically over the past decade in promoting economic

growth, and trend is expected to continue. Thus, efficiently serving our business customers needs

us to sustain the size, scope and revenue potential required for efficient exposure to the financial

system in New York and London.

Digital: The increasing digitization of banking changes radically what we represent each

customer and company, from people's individual commercial banks to the up this job. To thrive

in this modern virtual environment needs substantial investment, strategic alliances with software

providers, and proprietary rights to retain and achieve a competitive advantage.

Payment and transaction: The advancement of payment technologies has helped companies and

individuals to transfer money more easily, with less pressure, and at lower costs. When more

types of transactions are digitized, the technology that makes these payments becomes an

extremely important component of banks money capability (Nica, 2016).

equity rates that banks are expected to maintain toward balance sheet assets and rising the usage

of challenging requirements banking. Recent UK law also allows wealth management (small to

mid - size businesses finance) to be "ring-fenced" from corporate banking which has led to

Barclays UK and Barclays Global being established as two separate companies (Martin and et.al,

2017).

Capital markets: As a result of the change in policy, the added price of bank cash flow financing

has resulted in a shift in commercial debt to financial markets. As either a result, the position and

scale of capital markets has increased dramatically over the past decade in promoting economic

growth, and trend is expected to continue. Thus, efficiently serving our business customers needs

us to sustain the size, scope and revenue potential required for efficient exposure to the financial

system in New York and London.

Digital: The increasing digitization of banking changes radically what we represent each

customer and company, from people's individual commercial banks to the up this job. To thrive

in this modern virtual environment needs substantial investment, strategic alliances with software

providers, and proprietary rights to retain and achieve a competitive advantage.

Payment and transaction: The advancement of payment technologies has helped companies and

individuals to transfer money more easily, with less pressure, and at lower costs. When more

types of transactions are digitized, the technology that makes these payments becomes an

extremely important component of banks money capability (Nica, 2016).

For the effective financial services to the customers, the business organization is often

concerned with that the good quality of element distribution along its inventory, particularly

those products that are not noticeable and noticeable to the intended audience. In addition to this,

the expansion of the use of visual techniques for reduced time and money growth, the

convergence of their vehicles and combustion design engineers also leads to a significant

variable in transforming their goods. Barclays Plc has also made investments in modern and

extremely efficient financial services, specifically in investment, corporate and retail banking

which meet customer demand. It also wants us to give preference to investment options in cars,

in particular inside its next-generation fuel-efficient and rechargeable batteries-electric systems,

which would boost its international overall sales (Nkundabanyanga, Akankunda, Nalukenge and

Tusiime, 2017).

According to the law of demand rule, it was observed that the rise in the price of just

about any product, the lower the need for buyers to shop. Consequently, the market for cars or

other automobiles in general is known as flexible. Since owning one's own home, car is not

really in the luxury segment. People may delay new car purchasing particularly if its price is too

high and even beyond their income bracket. Together with other items, providing successful

financial services is not essential or a fundamental necessity of citizens. It thus includes a greater

concerned with that the good quality of element distribution along its inventory, particularly

those products that are not noticeable and noticeable to the intended audience. In addition to this,

the expansion of the use of visual techniques for reduced time and money growth, the

convergence of their vehicles and combustion design engineers also leads to a significant

variable in transforming their goods. Barclays Plc has also made investments in modern and

extremely efficient financial services, specifically in investment, corporate and retail banking

which meet customer demand. It also wants us to give preference to investment options in cars,

in particular inside its next-generation fuel-efficient and rechargeable batteries-electric systems,

which would boost its international overall sales (Nkundabanyanga, Akankunda, Nalukenge and

Tusiime, 2017).

According to the law of demand rule, it was observed that the rise in the price of just

about any product, the lower the need for buyers to shop. Consequently, the market for cars or

other automobiles in general is known as flexible. Since owning one's own home, car is not

really in the luxury segment. People may delay new car purchasing particularly if its price is too

high and even beyond their income bracket. Together with other items, providing successful

financial services is not essential or a fundamental necessity of citizens. It thus includes a greater

effect on global market credit supply, in which people who are living in high-standing areas are

demanding to buy luxurious lifestyle and extremely successful areas. There are setting the

financial services that must acquire by the middle class people in effective manner (Popescu,

2016).

In this context, Barclays Plc needs to follow successful interest rate initiatives to increase

international availability of economic operation. It involves overseeing right sale prices on

products which provide income backgrounds for customers. For the manufacturing of new

goods, the market for specific loans is needed to satisfy the expectation and the message

reductions to interest rates will have to be hammered on a regular basis. Easy and straightforward

pricing main message fails to attract consumer attention. In this end, it requires to adjust its

communication like 'Absolute Exposure Pledge' would attract financial service taker's attention.

The pricing strategy is efficient and has culminated in a consumer's unrestricted withdrawal

transfers from direct debits at safe, attractive interest rates payable annually (Siebenhüner,

Rodela and Ecker, 2016). Barclays also traded in fixed-income securities, which led to a high

increasing trend in its net earnings. Based on the success as a British universal bank, the aim is to

generate high returns: a financial institution with a rich tradition and close ties in the UK, but

also by the scope and versatility to serve its clients and consumers throughout the widest

spectrum of financial requirements from around globe. The companies include worldwide

consumer finance and payment activities (Wacker, Yang and Sheu, 2016).

CONCLUSION

It was inferred from the general economic strategic management that perhaps a

organization would make effective business improvements by using the main principles and their

assumptions. Through adapting supply and demand law to goods and services, a business may

evaluate the effect of various influences on its revenues and selling rate and take appropriate

steps. In the background of the automotive industry, managerial economics indicates how by

making thousands of financial services each year, this industry contributed the main role in the

growth environment. In addition to this, large-scale running enterprise also tends to minimize the

unemployment figure, which eventually also contributes to the growth of community.

demanding to buy luxurious lifestyle and extremely successful areas. There are setting the

financial services that must acquire by the middle class people in effective manner (Popescu,

2016).

In this context, Barclays Plc needs to follow successful interest rate initiatives to increase

international availability of economic operation. It involves overseeing right sale prices on

products which provide income backgrounds for customers. For the manufacturing of new

goods, the market for specific loans is needed to satisfy the expectation and the message

reductions to interest rates will have to be hammered on a regular basis. Easy and straightforward

pricing main message fails to attract consumer attention. In this end, it requires to adjust its

communication like 'Absolute Exposure Pledge' would attract financial service taker's attention.

The pricing strategy is efficient and has culminated in a consumer's unrestricted withdrawal

transfers from direct debits at safe, attractive interest rates payable annually (Siebenhüner,

Rodela and Ecker, 2016). Barclays also traded in fixed-income securities, which led to a high

increasing trend in its net earnings. Based on the success as a British universal bank, the aim is to

generate high returns: a financial institution with a rich tradition and close ties in the UK, but

also by the scope and versatility to serve its clients and consumers throughout the widest

spectrum of financial requirements from around globe. The companies include worldwide

consumer finance and payment activities (Wacker, Yang and Sheu, 2016).

CONCLUSION

It was inferred from the general economic strategic management that perhaps a

organization would make effective business improvements by using the main principles and their

assumptions. Through adapting supply and demand law to goods and services, a business may

evaluate the effect of various influences on its revenues and selling rate and take appropriate

steps. In the background of the automotive industry, managerial economics indicates how by

making thousands of financial services each year, this industry contributed the main role in the

growth environment. In addition to this, large-scale running enterprise also tends to minimize the

unemployment figure, which eventually also contributes to the growth of community.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journal

Adam, A. M., Quansah, E. and Kawor, S., 2017. Working capital management policies and

returns of listed manufacturing firms in Ghana. Scientific annals of economics and

business. 64(2). pp.255-269.

Adisetiawan, R. and Surono, Y., 2016. Earnings Management and Accounting Information

Value: Impact and Relevance. Business, Management and Economics Research. 2(10).

pp.170-179.

Bartkowski, B. and et.al, 2018. Institutional economics of agricultural soil ecosystem

services. Sustainability. 10(7). p.2447.

Elena, C. A., 2016. Social Media–A strategy in developing customer relationship

management. Procedia Economics and Finance. 39. pp.785-790.

Genovese, A. and et.al, 2017. Sustainable supply chain management and the transition towards a

circular economy: Evidence and some applications. Omega. 66. pp.344-357.

Hanley, N., Shogren, J. F. and White, B., 2016. Environmental economics: in theory and

practice. Macmillan International Higher Education.

Hyers, D. and Kovacova, M., 2018. The economics of the online gig economy: Algorithmic

hiring practices, digital labor-market intermediation, and rights for platform

workers. Psychosociological Issues in Human Resource Management. 6(1). pp.160-165.

Ingram, T. and Glod, W., 2016. Talent management in healthcare organizations-qualitative

research results. Procedia Economics and Finance. 39. pp.339-346.

Martin, A. R. and et.al, 2017. Intraspecific trait variation across multiple scales: the leaf

economics spectrum in coffee. Functional Ecology. 31(3). pp.604-612.

Nica, E., 2016. The effect of perceived organizational support on organizational commitment and

employee performance. Journal of Self-Governance and Management Economics. 4(4).

pp.34-40.

Nkundabanyanga, S. K., Akankunda, B., Nalukenge, I. and Tusiime, I., 2017. The impact of

financial management practices and competitive advantage on the loan performance of

MFIs. International Journal of Social Economics.

Popescu, G. H., 2016. Does economic growth bring about increased happiness?. Journal of Self-

Governance and Management Economics. 4(4). pp.27-33.

Siebenhüner, B., Rodela, R. and Ecker, F., 2016. Social learning research in ecological

economics: A survey. Environmental Science & Policy, 55, pp.116-126.

Books and Journal

Adam, A. M., Quansah, E. and Kawor, S., 2017. Working capital management policies and

returns of listed manufacturing firms in Ghana. Scientific annals of economics and

business. 64(2). pp.255-269.

Adisetiawan, R. and Surono, Y., 2016. Earnings Management and Accounting Information

Value: Impact and Relevance. Business, Management and Economics Research. 2(10).

pp.170-179.

Bartkowski, B. and et.al, 2018. Institutional economics of agricultural soil ecosystem

services. Sustainability. 10(7). p.2447.

Elena, C. A., 2016. Social Media–A strategy in developing customer relationship

management. Procedia Economics and Finance. 39. pp.785-790.

Genovese, A. and et.al, 2017. Sustainable supply chain management and the transition towards a

circular economy: Evidence and some applications. Omega. 66. pp.344-357.

Hanley, N., Shogren, J. F. and White, B., 2016. Environmental economics: in theory and

practice. Macmillan International Higher Education.

Hyers, D. and Kovacova, M., 2018. The economics of the online gig economy: Algorithmic

hiring practices, digital labor-market intermediation, and rights for platform

workers. Psychosociological Issues in Human Resource Management. 6(1). pp.160-165.

Ingram, T. and Glod, W., 2016. Talent management in healthcare organizations-qualitative

research results. Procedia Economics and Finance. 39. pp.339-346.

Martin, A. R. and et.al, 2017. Intraspecific trait variation across multiple scales: the leaf

economics spectrum in coffee. Functional Ecology. 31(3). pp.604-612.

Nica, E., 2016. The effect of perceived organizational support on organizational commitment and

employee performance. Journal of Self-Governance and Management Economics. 4(4).

pp.34-40.

Nkundabanyanga, S. K., Akankunda, B., Nalukenge, I. and Tusiime, I., 2017. The impact of

financial management practices and competitive advantage on the loan performance of

MFIs. International Journal of Social Economics.

Popescu, G. H., 2016. Does economic growth bring about increased happiness?. Journal of Self-

Governance and Management Economics. 4(4). pp.27-33.

Siebenhüner, B., Rodela, R. and Ecker, F., 2016. Social learning research in ecological

economics: A survey. Environmental Science & Policy, 55, pp.116-126.

Wacker, J. G., Yang, C. and Sheu, C., 2016. A transaction cost economics model for estimating

performance effectiveness of relational and contractual governance. International

Journal of Operations & Production Management.

performance effectiveness of relational and contractual governance. International

Journal of Operations & Production Management.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.