Auditing Theory and Practice: Evaluating Audit Procedures and Controls

VerifiedAdded on 2020/04/07

|15

|3632

|48

Report

AI Summary

This report provides a detailed analysis of auditing theory and practice, addressing key aspects such as ethical considerations, risk assessment, and internal controls. The report begins by examining ethical issues, including conflicts of interest and the auditor's responsibility to protect public interest. It then delves into the concept of business risk and how it can lead to material misstatements in financial statements, providing specific examples and relevant ISA 315 guidelines. The report also explores various audit procedures, including the evaluation of control deficiencies and the testing of controls using computer-assisted audit techniques (CAATs). Furthermore, it discusses specific threats to auditor independence, such as self-review, advocacy, familiarity, and self-interest threats, along with appropriate safeguards. The report also covers deficiencies in internal controls, such as the lack of integration between a website and inventory systems, and provides recommendations for improvements. Overall, the report offers a comprehensive overview of auditing principles and practices, making it a valuable resource for students studying auditing.

AUDITING THEORY AND PRACTICE

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Part A...............................................................................................................................................3

Part A-1........................................................................................................................................3

Part A-2........................................................................................................................................3

Part A-3........................................................................................................................................3

Part A-4........................................................................................................................................4

Part B...............................................................................................................................................6

(a): Business Risk........................................................................................................................6

(b): How it may lead to risk of material misstatement................................................................6

Part C...............................................................................................................................................8

(a): Deficiency and explanation...................................................................................................8

(b): Control..................................................................................................................................8

(c) Test of Control.......................................................................................................................8

Part D.............................................................................................................................................10

2

Part A...............................................................................................................................................3

Part A-1........................................................................................................................................3

Part A-2........................................................................................................................................3

Part A-3........................................................................................................................................3

Part A-4........................................................................................................................................4

Part B...............................................................................................................................................6

(a): Business Risk........................................................................................................................6

(b): How it may lead to risk of material misstatement................................................................6

Part C...............................................................................................................................................8

(a): Deficiency and explanation...................................................................................................8

(b): Control..................................................................................................................................8

(c) Test of Control.......................................................................................................................8

Part D.............................................................................................................................................10

2

Part A

Part A-1

Ethics in business management and business organisation is the prime factor that shall be

consider by auditor before accepting the audit or audit engagement. Auditor has overall

responsibility of verifying financial position and other unethical practices involved in the

business. In this case, management and Pharmaceuticals Ltd are involved in the practice of spill

of toxic chemicals into a nearby river. Therefore, protecting the public interest is the key ethical

matter that shall be considered by auditor before accepting the engagement (Duska, et. al, 2011).

Since management and Pharmaceuticals Ltd involve in unethical practice, therefore, before

accepting audit public interest ethical practice shall be should be considered.

Part A-2

In this case, no further course of action has been taken regarding Pharmaceuticals Ltd

adjustments that are identified during the audit and reported to the management. Errors in

accounting for hedging are small and not materially misstated. In this case, further course of

action is to make adjustments in the financial statement and same shall be reported in audit report

(Merle, et. al., 2014). For identified control weakness, the auditor shall recommend new treasurer

or new internal control system to be placed in the Pharmaceuticals Ltd.

Part A-3

An audit can be defined as the process of identifying material misstatement in the financial

statements and objective of the audit is to issue an opinion on true and fairness on client’s

financial statements. On the other hand, review engagement is very much different from auditing

i.e. in review engagement objective is to provide opinion on whether financial statements can be

trusted or not. It depends on audit engagement, whether the auditor is appointed for auditor for

review engagement. In this case, Billings & Associates has been appointed for an audit of

Reaction Pty Ltd as Billings & Associates has issued audit engagement prior to the

commencement of the audit. Since Reaction Pty Ltd is not available with complete documents

related to accounts receivable. In this case, auditor (Billings & Associates) has planned to issue

3

Part A-1

Ethics in business management and business organisation is the prime factor that shall be

consider by auditor before accepting the audit or audit engagement. Auditor has overall

responsibility of verifying financial position and other unethical practices involved in the

business. In this case, management and Pharmaceuticals Ltd are involved in the practice of spill

of toxic chemicals into a nearby river. Therefore, protecting the public interest is the key ethical

matter that shall be considered by auditor before accepting the engagement (Duska, et. al, 2011).

Since management and Pharmaceuticals Ltd involve in unethical practice, therefore, before

accepting audit public interest ethical practice shall be should be considered.

Part A-2

In this case, no further course of action has been taken regarding Pharmaceuticals Ltd

adjustments that are identified during the audit and reported to the management. Errors in

accounting for hedging are small and not materially misstated. In this case, further course of

action is to make adjustments in the financial statement and same shall be reported in audit report

(Merle, et. al., 2014). For identified control weakness, the auditor shall recommend new treasurer

or new internal control system to be placed in the Pharmaceuticals Ltd.

Part A-3

An audit can be defined as the process of identifying material misstatement in the financial

statements and objective of the audit is to issue an opinion on true and fairness on client’s

financial statements. On the other hand, review engagement is very much different from auditing

i.e. in review engagement objective is to provide opinion on whether financial statements can be

trusted or not. It depends on audit engagement, whether the auditor is appointed for auditor for

review engagement. In this case, Billings & Associates has been appointed for an audit of

Reaction Pty Ltd as Billings & Associates has issued audit engagement prior to the

commencement of the audit. Since Reaction Pty Ltd is not available with complete documents

related to accounts receivable. In this case, auditor (Billings & Associates) has planned to issue

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

modified auditor’s report because of scope limited. The contention of management (Reaction Pty

Ltd) that the engagement becomes review engagement as they are required to have an audit.

It can be conducted that, the contention of management is wrong and if review engagement is

required then audit engagement shall be according to review engagement (Arens, 2010). Since

initial audit engagement is for audit, therefore management cannot demand review engagement.

Part A-4

1:

Threat: Self-review threat

Justification: In this case, the auditor has finalized the financial statement of the Hail Pty Ltd

(client organisation) after client prepared the financial statement during the year. Another self-

review factor, in this case, is also proving because management of Hail Pty Ltd has admitted that

they had limited knowledge of identifying and calculates impairment. Now, while auditing, the

auditor is required to review or verify their own work i.e. all the adjustments provided to client’s

financial statement (Ianniello, 2015).

Safeguard: Client (Hail Pty Ltd) shall have the final decision on the outcome of the work done

by auditor or auditor’s firm. In this way, non-audit services to the client shall be mi minimised

and audit shall not conduct auditor should not provide opinion on impairment figure in the

financial statement.

2:

Threat: Advocacy Threat

Justification: In this given case, Travel Time Ltd (client organization) has required the auditor to

promote or recommend Travel Time Ltd to their other audit clients and help them to recover

from the bad time that they are facing. Auditor has also accepted the proposal from the Travel

Time Ltd and agrees to promote the business of client i.e. Travel Time Ltd. In this situation,

there is advocacy threat that auditor can face and is not allowed according to auditing principles

and standards (Li & Wu., 2017).

4

Ltd) that the engagement becomes review engagement as they are required to have an audit.

It can be conducted that, the contention of management is wrong and if review engagement is

required then audit engagement shall be according to review engagement (Arens, 2010). Since

initial audit engagement is for audit, therefore management cannot demand review engagement.

Part A-4

1:

Threat: Self-review threat

Justification: In this case, the auditor has finalized the financial statement of the Hail Pty Ltd

(client organisation) after client prepared the financial statement during the year. Another self-

review factor, in this case, is also proving because management of Hail Pty Ltd has admitted that

they had limited knowledge of identifying and calculates impairment. Now, while auditing, the

auditor is required to review or verify their own work i.e. all the adjustments provided to client’s

financial statement (Ianniello, 2015).

Safeguard: Client (Hail Pty Ltd) shall have the final decision on the outcome of the work done

by auditor or auditor’s firm. In this way, non-audit services to the client shall be mi minimised

and audit shall not conduct auditor should not provide opinion on impairment figure in the

financial statement.

2:

Threat: Advocacy Threat

Justification: In this given case, Travel Time Ltd (client organization) has required the auditor to

promote or recommend Travel Time Ltd to their other audit clients and help them to recover

from the bad time that they are facing. Auditor has also accepted the proposal from the Travel

Time Ltd and agrees to promote the business of client i.e. Travel Time Ltd. In this situation,

there is advocacy threat that auditor can face and is not allowed according to auditing principles

and standards (Li & Wu., 2017).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Safeguard: There shall be some policies or rules in the auditor’s firm that any partner or any

auditor cannot engage in promoting shares or business of client’s business. Another safeguard is

to use rotating policy at the audit firm.

3:

Threat: Familiarity Threat

Justification: New client i.e. Civil Constructions Ltd has been approached by auditor’s firm to

conduct audits. It can be analyzed that one of the audit firm’s partner’s wife has a substantial

shareholding in the Civil Constructions Ltd. Therefore there is familiarity threat in this case.

According to familiarity threat, an auditor (partners in audit firm) has a family member who is a

member who is a director or having a substantial shareholding in client’s business (Wines, 2012).

Safeguard: Safeguard in this case can be rotation policy that audit shall adopt while conducting

an audit of Civil Constructions Ltd. That partner of the audit firm shall be involved in auditing or

other audit or non-audit services of Civil Constructions Ltd.

4:

Threat: Self-Interest Threat

Justification: Pleasure Cruises Ltd is the business organization, having some cash flow problems

in their business operations. Therefore they are not able to pay audit fee to the auditor for

providing their audit services in prior years. However, management of Pleasure Cruises Ltd

expects that business will pick up in coming years and then audit fees will be paid to auditors

(Hellman, 2011). Therefore, in this case, audit firm or auditor

Safeguard: There shall be a regular review of client’s account and by client audit fees. Audit firm

shall on regular interval demand for bill payment and shall minimise non-audit service to the

client organisation (Wines, 2011).

5

auditor cannot engage in promoting shares or business of client’s business. Another safeguard is

to use rotating policy at the audit firm.

3:

Threat: Familiarity Threat

Justification: New client i.e. Civil Constructions Ltd has been approached by auditor’s firm to

conduct audits. It can be analyzed that one of the audit firm’s partner’s wife has a substantial

shareholding in the Civil Constructions Ltd. Therefore there is familiarity threat in this case.

According to familiarity threat, an auditor (partners in audit firm) has a family member who is a

member who is a director or having a substantial shareholding in client’s business (Wines, 2012).

Safeguard: Safeguard in this case can be rotation policy that audit shall adopt while conducting

an audit of Civil Constructions Ltd. That partner of the audit firm shall be involved in auditing or

other audit or non-audit services of Civil Constructions Ltd.

4:

Threat: Self-Interest Threat

Justification: Pleasure Cruises Ltd is the business organization, having some cash flow problems

in their business operations. Therefore they are not able to pay audit fee to the auditor for

providing their audit services in prior years. However, management of Pleasure Cruises Ltd

expects that business will pick up in coming years and then audit fees will be paid to auditors

(Hellman, 2011). Therefore, in this case, audit firm or auditor

Safeguard: There shall be a regular review of client’s account and by client audit fees. Audit firm

shall on regular interval demand for bill payment and shall minimise non-audit service to the

client organisation (Wines, 2011).

5

Part B

ISA 315, states the business risks that might lead the company to material misstatement risk at

the financial statement level. The misstatements in an organization can occur due to a number of

factors, such as- judgemental transactions, fraudulent activities, mistakes, breach of requirement

etc.

(a): Business Risk

(b): How it may lead to risk of material misstatement

BUSINESS RISK How it may lead to risk of material

misstatement

1. Offering new service In order to maintain a large customer base,

CPPI has initiated an idea which is linked

with the loyalty scheme. In order to provide

value-added services to the customers,

CPPL provides coffees to the loyal

customers as complementary (Handsworth,

2012). This strategy has helped to expand

the customer base. However, as per ISA

315, the offering of a new service can lead

to material misstatement risk for the

company; for a reason that in order to

maintain the cost which incurs in providing

value-added services, the company may

adjust the cost with other transactions.

2. Business operation risk The premises of CPPL are leased. The

lessor demands rent after increasing it by 50

%. As the lease for two premises is going to

6

ISA 315, states the business risks that might lead the company to material misstatement risk at

the financial statement level. The misstatements in an organization can occur due to a number of

factors, such as- judgemental transactions, fraudulent activities, mistakes, breach of requirement

etc.

(a): Business Risk

(b): How it may lead to risk of material misstatement

BUSINESS RISK How it may lead to risk of material

misstatement

1. Offering new service In order to maintain a large customer base,

CPPI has initiated an idea which is linked

with the loyalty scheme. In order to provide

value-added services to the customers,

CPPL provides coffees to the loyal

customers as complementary (Handsworth,

2012). This strategy has helped to expand

the customer base. However, as per ISA

315, the offering of a new service can lead

to material misstatement risk for the

company; for a reason that in order to

maintain the cost which incurs in providing

value-added services, the company may

adjust the cost with other transactions.

2. Business operation risk The premises of CPPL are leased. The

lessor demands rent after increasing it by 50

%. As the lease for two premises is going to

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

expire, earlier to the end of financial year.

This may lead to the material misstatement

risk for the CPPL, as due to the complexity

of the regulations misstatement may occur

that can cause business risk for the company

(Gordon, 2014).

3. Legal risk Legal action against a competitor company

has been initiated by the CPPL. This action

has been taken, because of the competitor`s

anti-competitive behavior (Hoelzer, 2011).

This may lead to business risk for the

company, as in the case, the company loses

the legal proceedings against the competitor,

and then CPPL will have to pay a huge

compensation to the competitor.

4. Fall in demand CPPL has emphasized on the expansion of

the products. This strategy is made by the

company in order to increase the sales and

to provide more options regarding products

to the customers. In contrast to this, the

stock obsolescence of the company is high

(Young & Coleman, 2010). In this case, the

type of risk related to the risk of material

misstatement is a valuation of inventory and

at assertion level. As the fall in demand of

the product can also make an impact on the

going concern status of the company for a

long time period. This may lead to a

7

This may lead to the material misstatement

risk for the CPPL, as due to the complexity

of the regulations misstatement may occur

that can cause business risk for the company

(Gordon, 2014).

3. Legal risk Legal action against a competitor company

has been initiated by the CPPL. This action

has been taken, because of the competitor`s

anti-competitive behavior (Hoelzer, 2011).

This may lead to business risk for the

company, as in the case, the company loses

the legal proceedings against the competitor,

and then CPPL will have to pay a huge

compensation to the competitor.

4. Fall in demand CPPL has emphasized on the expansion of

the products. This strategy is made by the

company in order to increase the sales and

to provide more options regarding products

to the customers. In contrast to this, the

stock obsolescence of the company is high

(Young & Coleman, 2010). In this case, the

type of risk related to the risk of material

misstatement is a valuation of inventory and

at assertion level. As the fall in demand of

the product can also make an impact on the

going concern status of the company for a

long time period. This may lead to a

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

prospect for material misstatement risk in

the company`s financial statement.

5. Alterations in the supply chain One of the other risk factors that may cause

material misstatement for the company is an

alteration in the supply chain. As through

evaluating the CPPL`s case, it can be

depicted that suppliers have reduced the

term of payment from fourteen to thirty

days (Popov, et. al., 2016). Due to the

withdrawal of the volume for the rebate, the

company may practice some activities that

may lead to the misstatement risk.

Part C

(a): Deficiency and explanation

(b): Control

(c) Test of Control

(a) Deficiency Explanation (b) Control (c) Test of Control

8

the company`s financial statement.

5. Alterations in the supply chain One of the other risk factors that may cause

material misstatement for the company is an

alteration in the supply chain. As through

evaluating the CPPL`s case, it can be

depicted that suppliers have reduced the

term of payment from fourteen to thirty

days (Popov, et. al., 2016). Due to the

withdrawal of the volume for the rebate, the

company may practice some activities that

may lead to the misstatement risk.

Part C

(a): Deficiency and explanation

(b): Control

(c) Test of Control

(a) Deficiency Explanation (b) Control (c) Test of Control

8

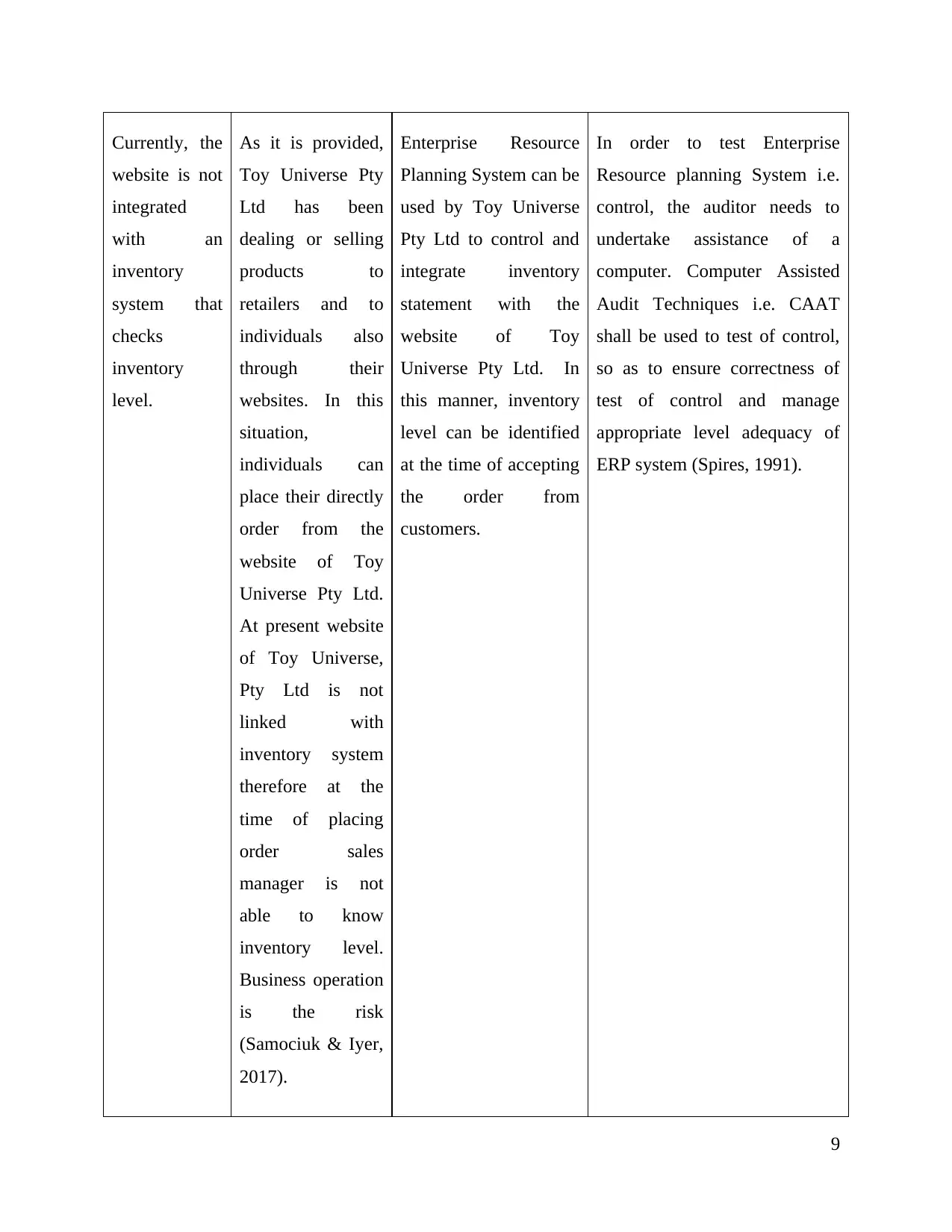

Currently, the

website is not

integrated

with an

inventory

system that

checks

inventory

level.

As it is provided,

Toy Universe Pty

Ltd has been

dealing or selling

products to

retailers and to

individuals also

through their

websites. In this

situation,

individuals can

place their directly

order from the

website of Toy

Universe Pty Ltd.

At present website

of Toy Universe,

Pty Ltd is not

linked with

inventory system

therefore at the

time of placing

order sales

manager is not

able to know

inventory level.

Business operation

is the risk

(Samociuk & Iyer,

2017).

Enterprise Resource

Planning System can be

used by Toy Universe

Pty Ltd to control and

integrate inventory

statement with the

website of Toy

Universe Pty Ltd. In

this manner, inventory

level can be identified

at the time of accepting

the order from

customers.

In order to test Enterprise

Resource planning System i.e.

control, the auditor needs to

undertake assistance of a

computer. Computer Assisted

Audit Techniques i.e. CAAT

shall be used to test of control,

so as to ensure correctness of

test of control and manage

appropriate level adequacy of

ERP system (Spires, 1991).

9

website is not

integrated

with an

inventory

system that

checks

inventory

level.

As it is provided,

Toy Universe Pty

Ltd has been

dealing or selling

products to

retailers and to

individuals also

through their

websites. In this

situation,

individuals can

place their directly

order from the

website of Toy

Universe Pty Ltd.

At present website

of Toy Universe,

Pty Ltd is not

linked with

inventory system

therefore at the

time of placing

order sales

manager is not

able to know

inventory level.

Business operation

is the risk

(Samociuk & Iyer,

2017).

Enterprise Resource

Planning System can be

used by Toy Universe

Pty Ltd to control and

integrate inventory

statement with the

website of Toy

Universe Pty Ltd. In

this manner, inventory

level can be identified

at the time of accepting

the order from

customers.

In order to test Enterprise

Resource planning System i.e.

control, the auditor needs to

undertake assistance of a

computer. Computer Assisted

Audit Techniques i.e. CAAT

shall be used to test of control,

so as to ensure correctness of

test of control and manage

appropriate level adequacy of

ERP system (Spires, 1991).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

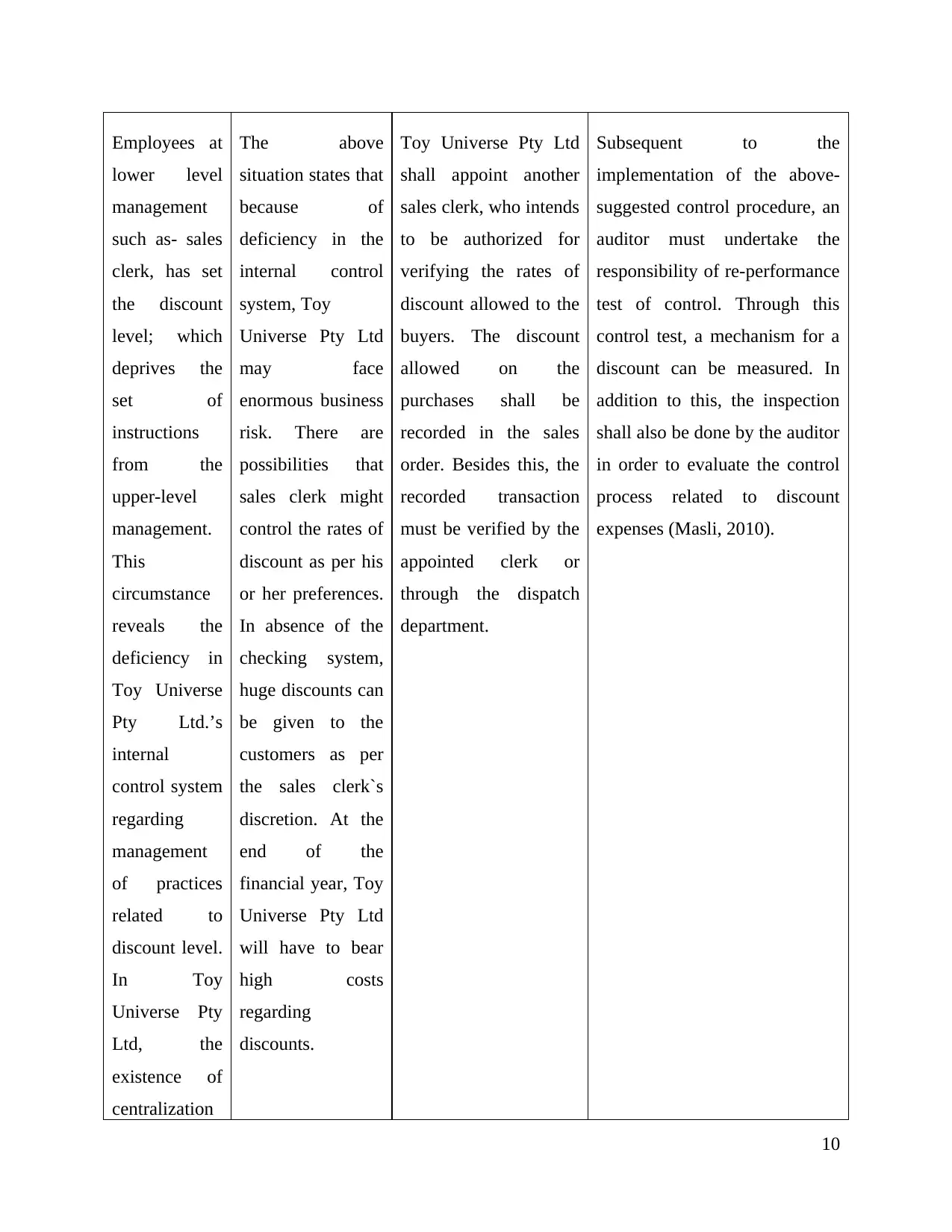

Employees at

lower level

management

such as- sales

clerk, has set

the discount

level; which

deprives the

set of

instructions

from the

upper-level

management.

This

circumstance

reveals the

deficiency in

Toy Universe

Pty Ltd.’s

internal

control system

regarding

management

of practices

related to

discount level.

In Toy

Universe Pty

Ltd, the

existence of

centralization

The above

situation states that

because of

deficiency in the

internal control

system, Toy

Universe Pty Ltd

may face

enormous business

risk. There are

possibilities that

sales clerk might

control the rates of

discount as per his

or her preferences.

In absence of the

checking system,

huge discounts can

be given to the

customers as per

the sales clerk`s

discretion. At the

end of the

financial year, Toy

Universe Pty Ltd

will have to bear

high costs

regarding

discounts.

Toy Universe Pty Ltd

shall appoint another

sales clerk, who intends

to be authorized for

verifying the rates of

discount allowed to the

buyers. The discount

allowed on the

purchases shall be

recorded in the sales

order. Besides this, the

recorded transaction

must be verified by the

appointed clerk or

through the dispatch

department.

Subsequent to the

implementation of the above-

suggested control procedure, an

auditor must undertake the

responsibility of re-performance

test of control. Through this

control test, a mechanism for a

discount can be measured. In

addition to this, the inspection

shall also be done by the auditor

in order to evaluate the control

process related to discount

expenses (Masli, 2010).

10

lower level

management

such as- sales

clerk, has set

the discount

level; which

deprives the

set of

instructions

from the

upper-level

management.

This

circumstance

reveals the

deficiency in

Toy Universe

Pty Ltd.’s

internal

control system

regarding

management

of practices

related to

discount level.

In Toy

Universe Pty

Ltd, the

existence of

centralization

The above

situation states that

because of

deficiency in the

internal control

system, Toy

Universe Pty Ltd

may face

enormous business

risk. There are

possibilities that

sales clerk might

control the rates of

discount as per his

or her preferences.

In absence of the

checking system,

huge discounts can

be given to the

customers as per

the sales clerk`s

discretion. At the

end of the

financial year, Toy

Universe Pty Ltd

will have to bear

high costs

regarding

discounts.

Toy Universe Pty Ltd

shall appoint another

sales clerk, who intends

to be authorized for

verifying the rates of

discount allowed to the

buyers. The discount

allowed on the

purchases shall be

recorded in the sales

order. Besides this, the

recorded transaction

must be verified by the

appointed clerk or

through the dispatch

department.

Subsequent to the

implementation of the above-

suggested control procedure, an

auditor must undertake the

responsibility of re-performance

test of control. Through this

control test, a mechanism for a

discount can be measured. In

addition to this, the inspection

shall also be done by the auditor

in order to evaluate the control

process related to discount

expenses (Masli, 2010).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in context to

making a huge

decision such

as setting the

discount rate

does not exist.

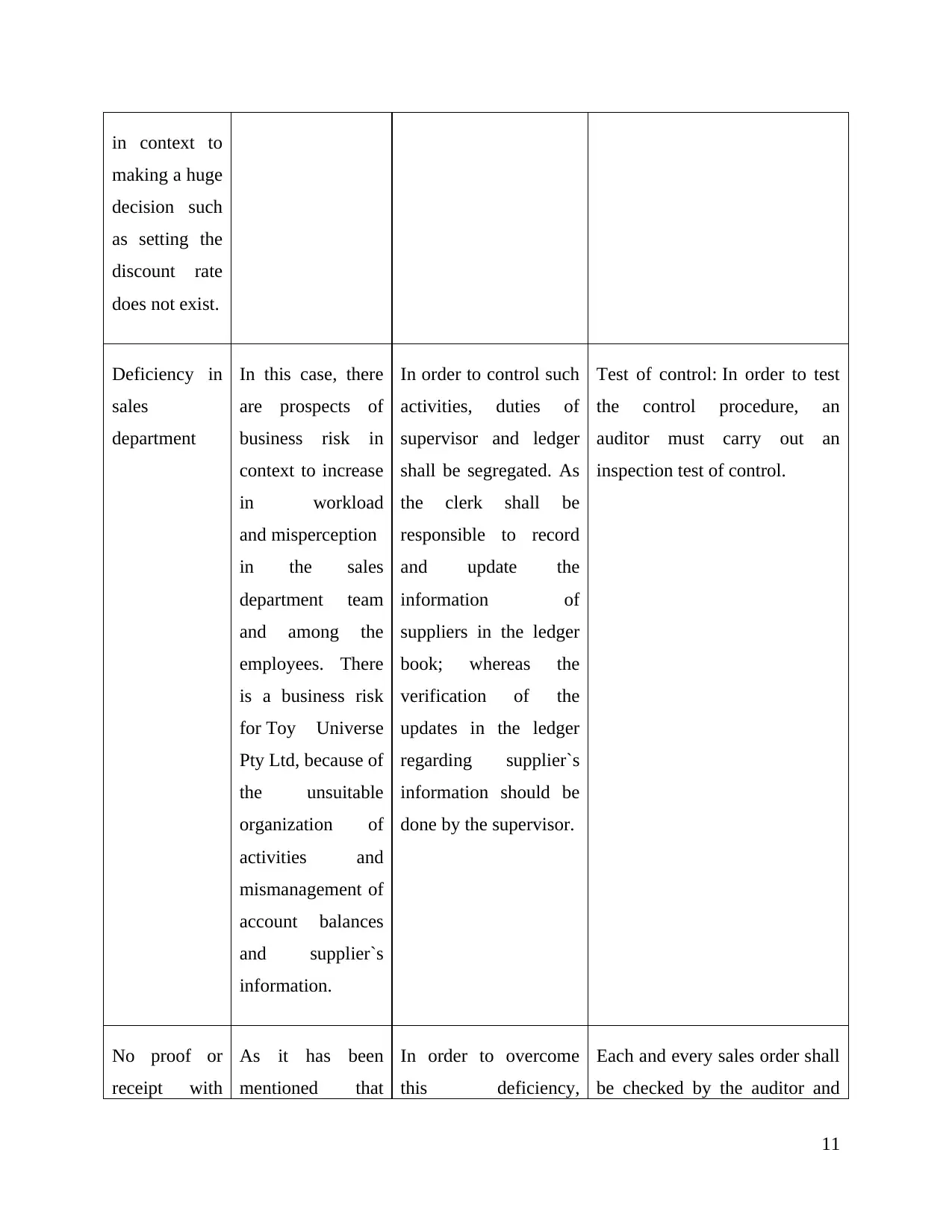

Deficiency in

sales

department

In this case, there

are prospects of

business risk in

context to increase

in workload

and misperception

in the sales

department team

and among the

employees. There

is a business risk

for Toy Universe

Pty Ltd, because of

the unsuitable

organization of

activities and

mismanagement of

account balances

and supplier`s

information.

In order to control such

activities, duties of

supervisor and ledger

shall be segregated. As

the clerk shall be

responsible to record

and update the

information of

suppliers in the ledger

book; whereas the

verification of the

updates in the ledger

regarding supplier`s

information should be

done by the supervisor.

Test of control: In order to test

the control procedure, an

auditor must carry out an

inspection test of control.

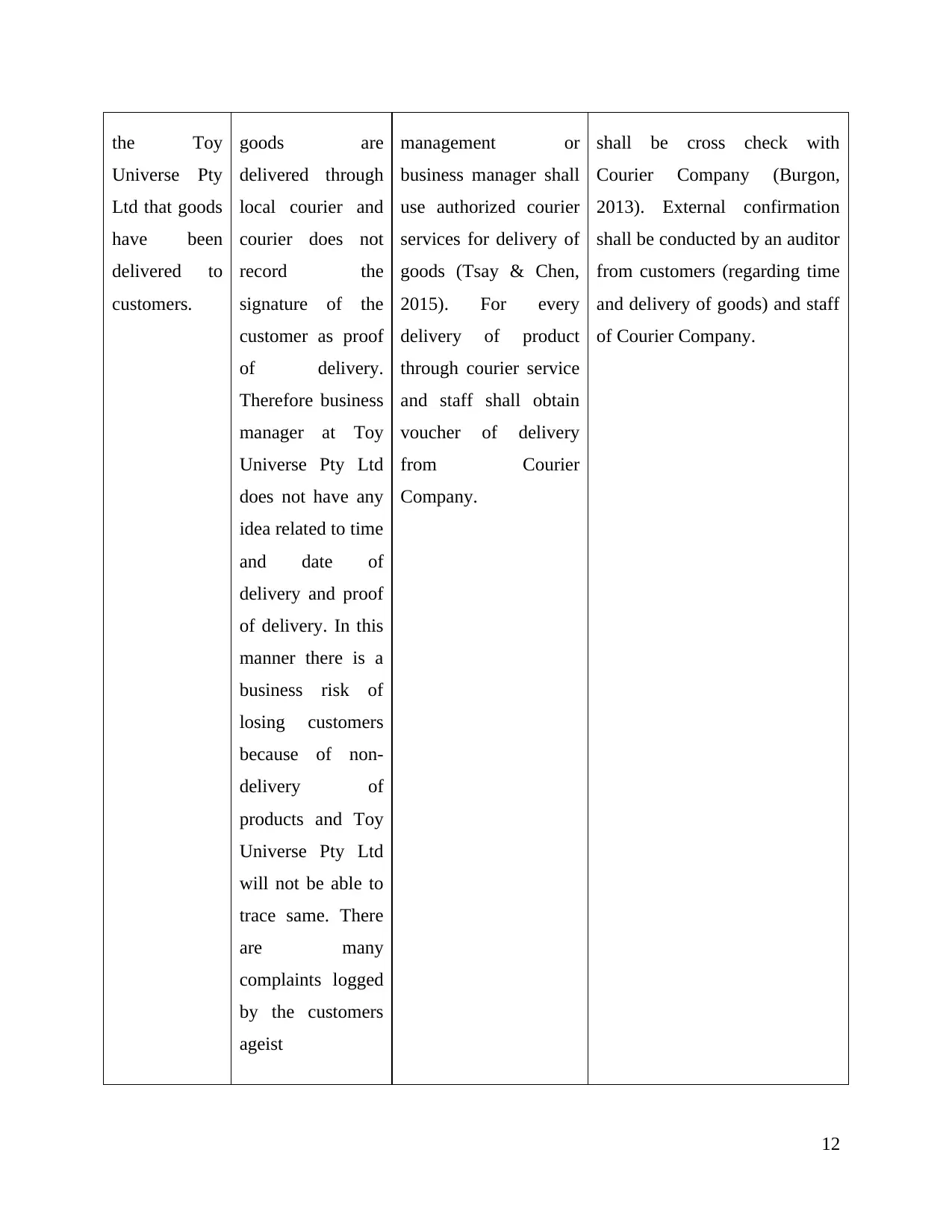

No proof or

receipt with

As it has been

mentioned that

In order to overcome

this deficiency,

Each and every sales order shall

be checked by the auditor and

11

making a huge

decision such

as setting the

discount rate

does not exist.

Deficiency in

sales

department

In this case, there

are prospects of

business risk in

context to increase

in workload

and misperception

in the sales

department team

and among the

employees. There

is a business risk

for Toy Universe

Pty Ltd, because of

the unsuitable

organization of

activities and

mismanagement of

account balances

and supplier`s

information.

In order to control such

activities, duties of

supervisor and ledger

shall be segregated. As

the clerk shall be

responsible to record

and update the

information of

suppliers in the ledger

book; whereas the

verification of the

updates in the ledger

regarding supplier`s

information should be

done by the supervisor.

Test of control: In order to test

the control procedure, an

auditor must carry out an

inspection test of control.

No proof or

receipt with

As it has been

mentioned that

In order to overcome

this deficiency,

Each and every sales order shall

be checked by the auditor and

11

the Toy

Universe Pty

Ltd that goods

have been

delivered to

customers.

goods are

delivered through

local courier and

courier does not

record the

signature of the

customer as proof

of delivery.

Therefore business

manager at Toy

Universe Pty Ltd

does not have any

idea related to time

and date of

delivery and proof

of delivery. In this

manner there is a

business risk of

losing customers

because of non-

delivery of

products and Toy

Universe Pty Ltd

will not be able to

trace same. There

are many

complaints logged

by the customers

ageist

management or

business manager shall

use authorized courier

services for delivery of

goods (Tsay & Chen,

2015). For every

delivery of product

through courier service

and staff shall obtain

voucher of delivery

from Courier

Company.

shall be cross check with

Courier Company (Burgon,

2013). External confirmation

shall be conducted by an auditor

from customers (regarding time

and delivery of goods) and staff

of Courier Company.

12

Universe Pty

Ltd that goods

have been

delivered to

customers.

goods are

delivered through

local courier and

courier does not

record the

signature of the

customer as proof

of delivery.

Therefore business

manager at Toy

Universe Pty Ltd

does not have any

idea related to time

and date of

delivery and proof

of delivery. In this

manner there is a

business risk of

losing customers

because of non-

delivery of

products and Toy

Universe Pty Ltd

will not be able to

trace same. There

are many

complaints logged

by the customers

ageist

management or

business manager shall

use authorized courier

services for delivery of

goods (Tsay & Chen,

2015). For every

delivery of product

through courier service

and staff shall obtain

voucher of delivery

from Courier

Company.

shall be cross check with

Courier Company (Burgon,

2013). External confirmation

shall be conducted by an auditor

from customers (regarding time

and delivery of goods) and staff

of Courier Company.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.