CREDIT AND LENDING MANAGEMENT: Stockland Company Report Analysis

VerifiedAdded on 2020/05/11

|9

|1288

|131

Report

AI Summary

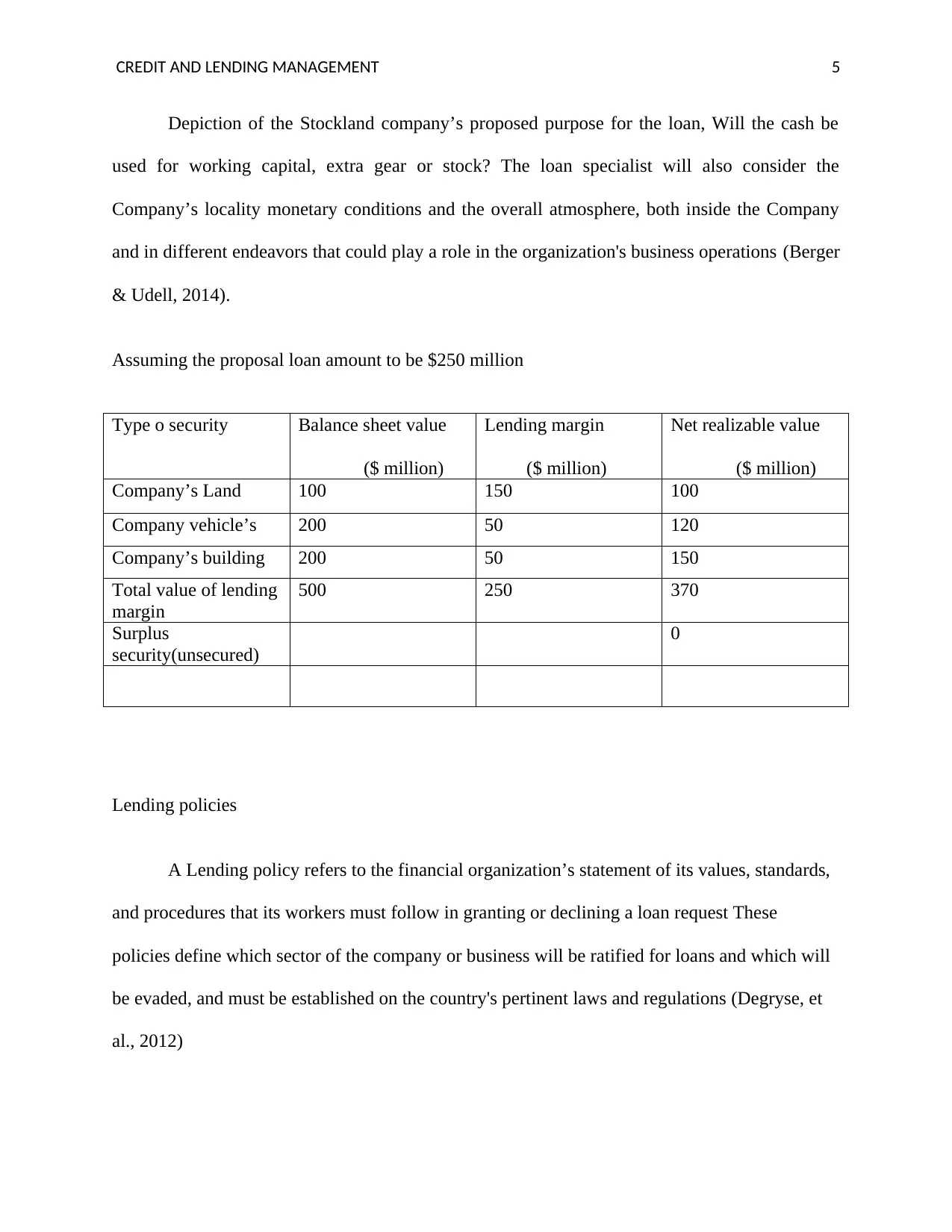

This report delves into the critical aspects of credit and lending management, focusing on loan evaluation techniques, security in business, and the role of securities in raising capital. It examines the key credit issues considered in loan proposals, utilizing the "5 C's" framework (Capacity, Capital, Collateral, Conditions, and Character) to assess the creditworthiness of borrowers. The report analyzes the Stockland Company's decision-making process regarding retirement borrowing, evaluating its capacity to repay loans, the capital invested in the business, and the collateral offered. It also assesses the proposed loan conditions, including the purpose of the loan and the prevailing economic environment. Furthermore, the report provides a detailed analysis of lending policies and their impact on the Stockland Company's financial decisions, concluding with recommendations for financial institutions and companies. The report includes a table outlining the value of security and lending margins, along with a discussion of how the lending policies apply to the Stockland Company's situation. The report concludes with the importance of aligning borrowing decisions with the financial institution's lending policies.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.