Detailed Report on Risk, Return, and Portfolio Management Analysis

VerifiedAdded on 2021/09/08

|7

|1500

|376

Report

AI Summary

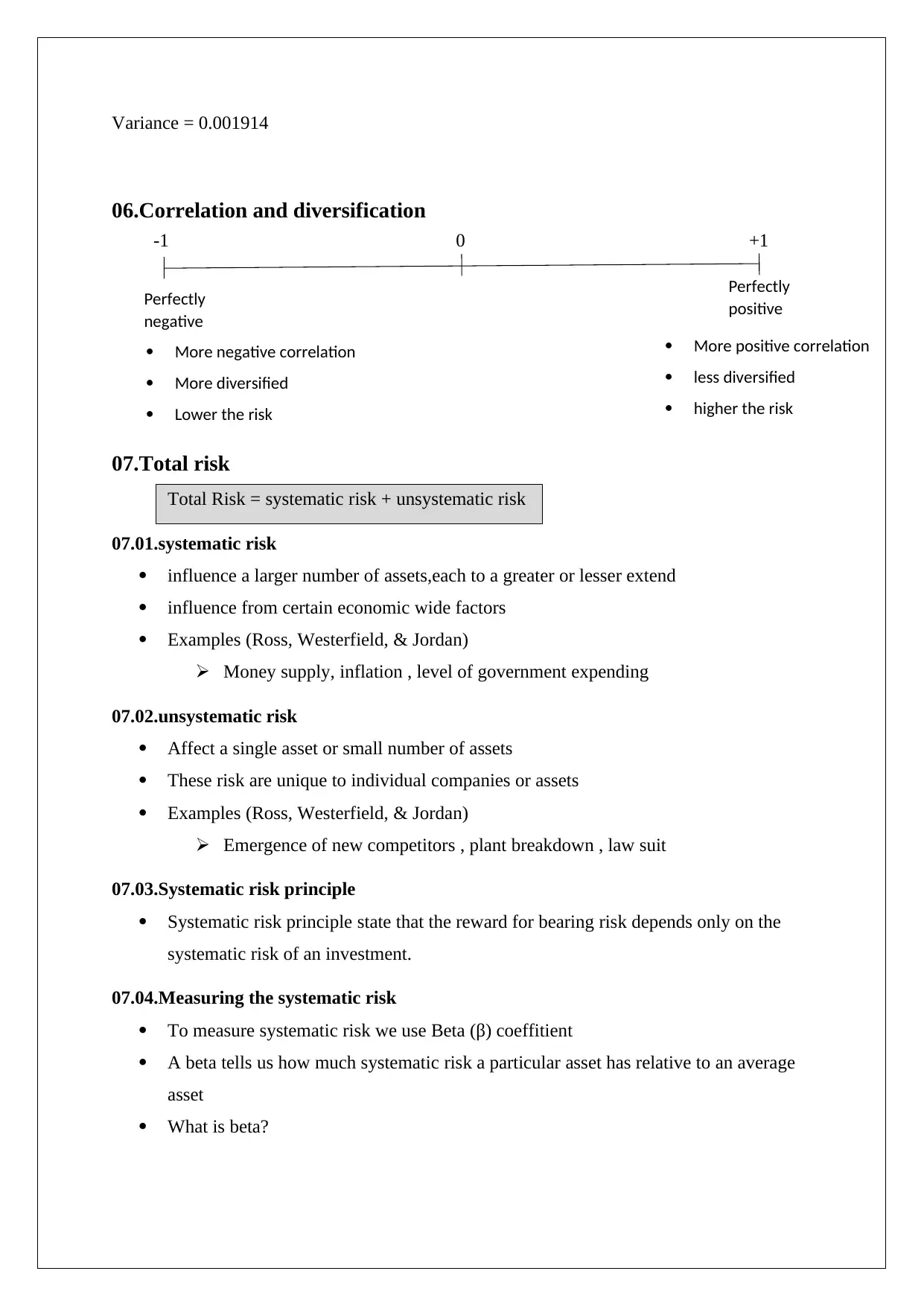

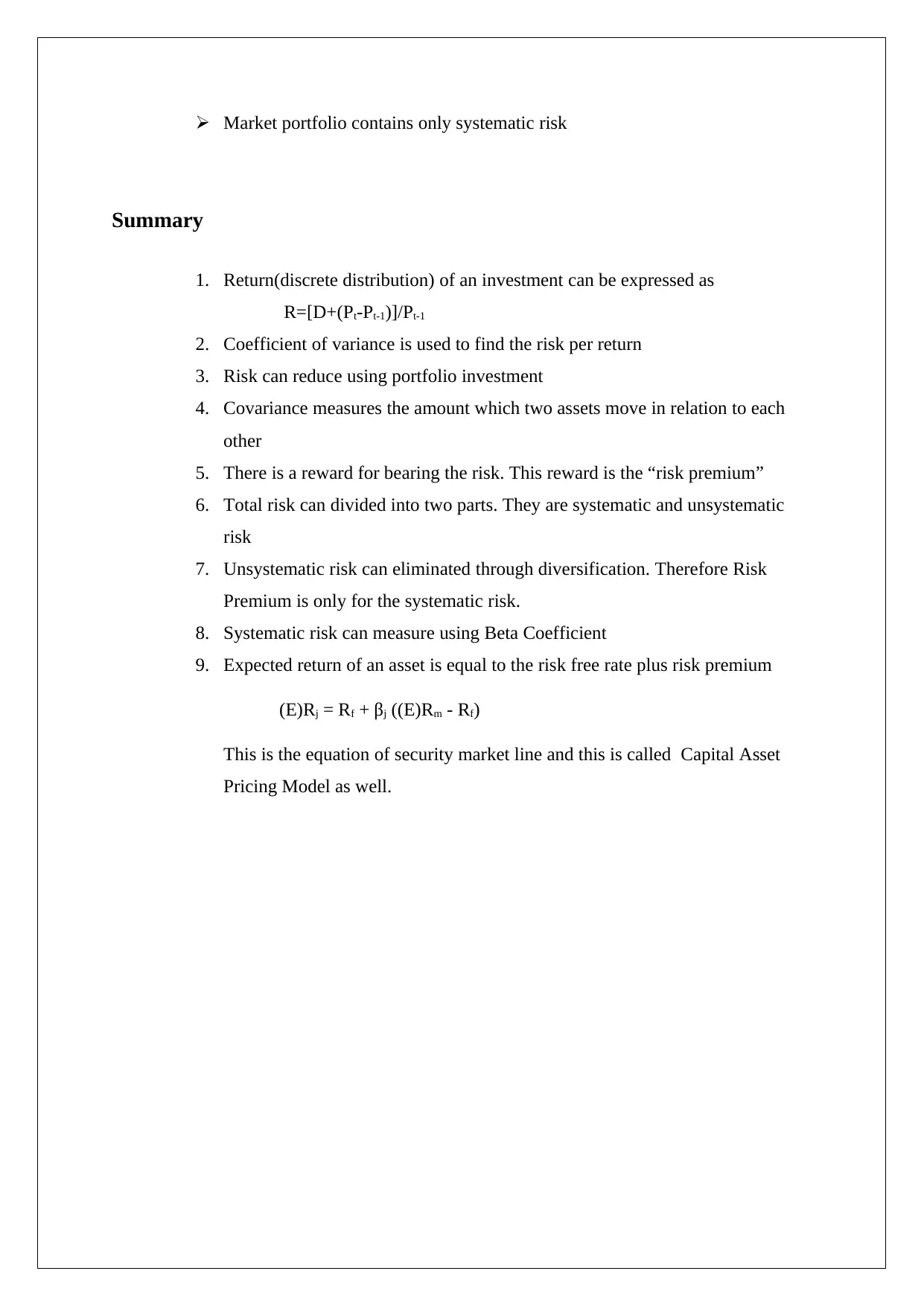

This assignment solution provides a comprehensive overview of risk and return calculations in investment, focusing on both discrete and continuous distributions. It covers key concepts such as the calculation of return using the formula R=[D+(Pt-Pt-1)]/Pt-1, risk assessment using standard deviation and coefficient of variance, and the application of covariance in portfolio evaluation. The report further explains portfolio management strategies, including expected return and variance calculations, diversification benefits, and the distinction between systematic and unsystematic risks. It also delves into the systematic risk principle, its measurement using Beta (β) coefficient, and the security market line (SML) with the Capital Asset Pricing Model (CAPM). The document concludes by summarizing the importance of risk premium and diversification in investment decisions, highlighting the relationship between risk-free rate, risk premium, and expected return as defined by the SML equation.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.