Holmes Institute: Accounting for Lease - AASB 16 Critical Review

VerifiedAdded on 2023/03/23

|14

|4421

|90

Report

AI Summary

This report provides a critical evaluation of AASB 16, the new accounting standard for leases, replacing the previous AASB 117. It explores the drawbacks of AASB 117, the rationale behind the change, and the key provisions of AASB 16, focusing on its impact on financial statements, particularly for companies heavily involved in lease financing. The report examines the shift from operating to finance leases, the improved comparability between companies that lease assets and those that borrow, and the potential impact on asset purchasing behavior. It also includes a case study of Woolworths Group, highlighting their disclosures related to the transition to AASB 16. The report analyzes the tendency of companies to classify leases as operating leases under AASB 117 and relates this behavior to positive accounting theory. The report concludes by discussing the potential implications of the new standard and the importance of understanding the accounting changes for stakeholders.

Leasing

Module Number-

[DATE]

Hewlett-Packard

[Company address]

Module Number-

[DATE]

Hewlett-Packard

[Company address]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abstract

The current report has been presented to critically evaluate the new accounting

standard for lease financing being AASB 16, Leases. The reason for replacing of earlier

AASB 117 due to its drawbacks has been discussed. The provisions set by the newly

formulated standard AASB 16 are discussed in the report, with main discussion about the

effect casted on the financial statements of companies dealing significantly in lease financing.

The possible effect on the leasing habits because of change brought by the standard are also

discussed. The effect of the pronouncement of the accounting standard on the comparability

between the financial statements of companies using the lease assets and owned assets is also

conversed. In the final section the key disclosures highlighted by Woolworths Group in its

annual report in relation to the transitional provisions adopted by the company are shown.

The disclosures made by the company represent the effect of the application of the new

AASB 16 on the consolidated statement of financial position as at 24th June 2018.

The current report has been presented to critically evaluate the new accounting

standard for lease financing being AASB 16, Leases. The reason for replacing of earlier

AASB 117 due to its drawbacks has been discussed. The provisions set by the newly

formulated standard AASB 16 are discussed in the report, with main discussion about the

effect casted on the financial statements of companies dealing significantly in lease financing.

The possible effect on the leasing habits because of change brought by the standard are also

discussed. The effect of the pronouncement of the accounting standard on the comparability

between the financial statements of companies using the lease assets and owned assets is also

conversed. In the final section the key disclosures highlighted by Woolworths Group in its

annual report in relation to the transitional provisions adopted by the company are shown.

The disclosures made by the company represent the effect of the application of the new

AASB 16 on the consolidated statement of financial position as at 24th June 2018.

Table of Contents

Abstract..........................................................................................................................1

Introduction....................................................................................................................2

Drawbacks of old accounting standard for lease, AASB 117...............................................2

Why was the change necessary.........................................................................................3

Changes incorporated by new accounting standard.............................................................3

Effect of change on companies having significant level of lease financing...........................4

In the former accounting standard for lease (AASB 117) both operating lease and finance

lease were allowed, why did companies have a tendency to classify most of the lease contract

as operating lease? How does positive accounting theory relate to this behaviour of

managers?.......................................................................................................................5

Improved comparability between the companies that lease assets and companies that borrow

to buy assets because of implementation of IFRS 16..........................................................5

Possible explanation as to why after the implementation of AASB 16, reporting entities might

be more likely to buy more assets and lease fewer assets....................................................6

The key disclosures made by Woolworths Group on its accounting for leases including on the

transitional provision and effect of the transition to AASB 16 from AASB 117....................7

Conclusion......................................................................................................................8

References......................................................................................................................9

Abstract..........................................................................................................................1

Introduction....................................................................................................................2

Drawbacks of old accounting standard for lease, AASB 117...............................................2

Why was the change necessary.........................................................................................3

Changes incorporated by new accounting standard.............................................................3

Effect of change on companies having significant level of lease financing...........................4

In the former accounting standard for lease (AASB 117) both operating lease and finance

lease were allowed, why did companies have a tendency to classify most of the lease contract

as operating lease? How does positive accounting theory relate to this behaviour of

managers?.......................................................................................................................5

Improved comparability between the companies that lease assets and companies that borrow

to buy assets because of implementation of IFRS 16..........................................................5

Possible explanation as to why after the implementation of AASB 16, reporting entities might

be more likely to buy more assets and lease fewer assets....................................................6

The key disclosures made by Woolworths Group on its accounting for leases including on the

transitional provision and effect of the transition to AASB 16 from AASB 117....................7

Conclusion......................................................................................................................8

References......................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

AASB 16, Leases has been formulated to replace the former accounting standard dealing with

leases, i.e. AASB 117. The provisions set by AASB 16 are equivalent to the provisions

marked by the IAS 17, Leases. The purpose of setting of AASB 16 is setting up of a broad

model dealing with the identification and financial statement treatment for the lease

arrangements entered by both the lessor and lessee. The provisions of the newly formed

AASB 16 are different from earlier AASB 17 and the listed entities are mandated to switch to

the new standard. Switching to the new standard requires implementation of transitional

provisions. These transitional provisions are discussed in the current report with the example

of information disclosed in the annual report of Woolworths Group.

Woolworths Group works in the retail industry and is headquartered in Bella Vista, in New

South Wales Australia. The company is named as second largest Australian corporation in

terms of revenue. The group is known in Australia mainly for the super market chain it

operates therein.

Drawbacks of old accounting standard for lease, AASB 117

The main drawbacks of the earlier applicable AASB 117, Leases dealing with accounting of

leases are listed in the following sections. These drawbacks framed a major criterion for the

authorities to replace the AASB 117 with AASB 16.

The state of financial statements was misrepresented when AASB 117 was applicable. The

financial statements only represented the lease liabilities and right-to-use assets in case of

finance leases earlier. The reporting of operating leases was limited to note to accounts. The

liability in case of operating leases was only shown in notes and hence remained unread by

most readers. The financial statements hence lacked transparency then.

The lessee companies shall be now required to fully disclose all the lease liabilities in the

balance sheet, which earlier were only informed about in the notes to financial statements. It

may result to issues in complying with the domestic and international reporting frameworks.

Due to the application of AASB 117, most of the lessee companies having large lease

portfolios opted for classifying their most of the leases as operating leases to remain safe

from disclosing lease liabilities in balance sheet. The classification that was actually required

for the type of lease was erroneously modified to gain advantage. This gave them the

AASB 16, Leases has been formulated to replace the former accounting standard dealing with

leases, i.e. AASB 117. The provisions set by AASB 16 are equivalent to the provisions

marked by the IAS 17, Leases. The purpose of setting of AASB 16 is setting up of a broad

model dealing with the identification and financial statement treatment for the lease

arrangements entered by both the lessor and lessee. The provisions of the newly formed

AASB 16 are different from earlier AASB 17 and the listed entities are mandated to switch to

the new standard. Switching to the new standard requires implementation of transitional

provisions. These transitional provisions are discussed in the current report with the example

of information disclosed in the annual report of Woolworths Group.

Woolworths Group works in the retail industry and is headquartered in Bella Vista, in New

South Wales Australia. The company is named as second largest Australian corporation in

terms of revenue. The group is known in Australia mainly for the super market chain it

operates therein.

Drawbacks of old accounting standard for lease, AASB 117

The main drawbacks of the earlier applicable AASB 117, Leases dealing with accounting of

leases are listed in the following sections. These drawbacks framed a major criterion for the

authorities to replace the AASB 117 with AASB 16.

The state of financial statements was misrepresented when AASB 117 was applicable. The

financial statements only represented the lease liabilities and right-to-use assets in case of

finance leases earlier. The reporting of operating leases was limited to note to accounts. The

liability in case of operating leases was only shown in notes and hence remained unread by

most readers. The financial statements hence lacked transparency then.

The lessee companies shall be now required to fully disclose all the lease liabilities in the

balance sheet, which earlier were only informed about in the notes to financial statements. It

may result to issues in complying with the domestic and international reporting frameworks.

Due to the application of AASB 117, most of the lessee companies having large lease

portfolios opted for classifying their most of the leases as operating leases to remain safe

from disclosing lease liabilities in balance sheet. The classification that was actually required

for the type of lease was erroneously modified to gain advantage. This gave them the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

opportunity to play with financial statements and manipulate the real state of their financial

position. This policy could be taken as equal to earnings management, as the readers only

saw what was in financial statements and considered the liability of entities to be lesser than

it actually was. Their credit risk kept hidden under the name of operating leases (Xu,

Davidson, and Cheong, 2017).

Even when the disclosures about the off-balance sheet operating liabilities was made in the

notes to financial statements, many readers used to find the information insufficient to reflect

completely the obligations attached with those leases. The presentation style too did not

reflect the actual state of affairs.

There is need to align the domestic reporting framework of the organization with the

international reporting frameworks to avoid the possible issues in determining the capital and

revenue nature lease in the recorded framework.

Why was the change necessary

The earlier AASB 117 required classification for leases as finance lease or operating lease.

The identified operating leases were allowed to be transacted off balance sheet and no

reporting was required in the financial statements. The only effect on financial statements

was upon the profit & loss account because of charging of lease payment as expenses. There

was no charge of either asset or liability in the books relating to the operating leases. Because

of non-presentation of lease liability anywhere, the actual liability always kept hidden from

the stakeholders using the information presented in financial statements. Only place where

disclosures were made in financial statements were in notes to accounts, which again

remained unread by majority of readers. The financial information, due to non-representation

of liability relating to operating leases, was misled. There was no faithful representation in

relation to the lease related transactions (Brumm, Liu, 2019).

To eliminate the misrepresentation of financial statements due to differential treatment

followed for operating and finance leases, the old AASB 117 was decided to be eliminated by

the standard setting authorities. In place of AASB 117, AASB 16, Leases was introduced.

The introduction of this standard brought in effect a single system of accounting for both

operating and financing leases. Resultant, the earlier discrepancy got eliminated and now,

accounting is required for both kinds of leases. The issue in the lease recording framework

arise due to the procedural work used for the recording of the lease items.

position. This policy could be taken as equal to earnings management, as the readers only

saw what was in financial statements and considered the liability of entities to be lesser than

it actually was. Their credit risk kept hidden under the name of operating leases (Xu,

Davidson, and Cheong, 2017).

Even when the disclosures about the off-balance sheet operating liabilities was made in the

notes to financial statements, many readers used to find the information insufficient to reflect

completely the obligations attached with those leases. The presentation style too did not

reflect the actual state of affairs.

There is need to align the domestic reporting framework of the organization with the

international reporting frameworks to avoid the possible issues in determining the capital and

revenue nature lease in the recorded framework.

Why was the change necessary

The earlier AASB 117 required classification for leases as finance lease or operating lease.

The identified operating leases were allowed to be transacted off balance sheet and no

reporting was required in the financial statements. The only effect on financial statements

was upon the profit & loss account because of charging of lease payment as expenses. There

was no charge of either asset or liability in the books relating to the operating leases. Because

of non-presentation of lease liability anywhere, the actual liability always kept hidden from

the stakeholders using the information presented in financial statements. Only place where

disclosures were made in financial statements were in notes to accounts, which again

remained unread by majority of readers. The financial information, due to non-representation

of liability relating to operating leases, was misled. There was no faithful representation in

relation to the lease related transactions (Brumm, Liu, 2019).

To eliminate the misrepresentation of financial statements due to differential treatment

followed for operating and finance leases, the old AASB 117 was decided to be eliminated by

the standard setting authorities. In place of AASB 117, AASB 16, Leases was introduced.

The introduction of this standard brought in effect a single system of accounting for both

operating and financing leases. Resultant, the earlier discrepancy got eliminated and now,

accounting is required for both kinds of leases. The issue in the lease recording framework

arise due to the procedural work used for the recording of the lease items.

Changes incorporated by new accounting standard

The accounting model adopted by new AASB 16 is single. The model followed earlier just

for financing lease is now followed for both operating and finance leases and lessees are no

longer required to initially determine whether a lease is operating or financing. This is the

change which shall impact upon the accounting earlier followed by the lessees. Any off

balance sheet treatment has been done away with now. However, still exemption to treat off

balance sheet is yet available for low value asset lease and short term lease (i.e. less than 12

months) (Joubert, Garvie, and Parle, 2017).

As far as the accounting model for lessors is concerned, the AASB 16 does not bring

significant change into that except the enhancement of the disclosure process. The additional

disclosure required from the end of lessor relates to risk management related activities. Also,

the AASB 16 has disallowed the non-resources debt netting as the leveraged lease model is

now removed. Further, the change is observed in the treatment followed for residual value

guarantees (Kabir, and Rahman, 2018).

Effect of change on companies having significant level of lease financing

The main effect of the change is undoubtedly to be observed significantly upon the

companies that have significant level of lease financing. However, the major impact yet shall

be upon those relying on operating leases as compared to those with reliance upon finance

lease.

For the entities that have significant level of operating leases shall face a transformation in

the statement of financial position. The indicators signifying the finances shall drastically

change because the balance sheet shall now be required to add some assets as well liabilities

which were earlier treated off balance sheet. Earlier only the profit & loss statement was

affected by operating leases, but now the balance sheet shall also show the effects (Giner,

Merello, and Pardo, 2018).

The lessee companies shall be now required to fully disclose all the lease liabilities in the

balance sheet, which earlier were only informed about in the notes to financial statements.

The impact is major, as the accounting is changed and so is the presentation. The major

corporations are even expected to be required to create new departments for just accounting

the new lease requirements. The effort and money expenditure to deal with the impact is

supposed to be high in the initial adoption at least (Dakis, 2016).

The accounting model adopted by new AASB 16 is single. The model followed earlier just

for financing lease is now followed for both operating and finance leases and lessees are no

longer required to initially determine whether a lease is operating or financing. This is the

change which shall impact upon the accounting earlier followed by the lessees. Any off

balance sheet treatment has been done away with now. However, still exemption to treat off

balance sheet is yet available for low value asset lease and short term lease (i.e. less than 12

months) (Joubert, Garvie, and Parle, 2017).

As far as the accounting model for lessors is concerned, the AASB 16 does not bring

significant change into that except the enhancement of the disclosure process. The additional

disclosure required from the end of lessor relates to risk management related activities. Also,

the AASB 16 has disallowed the non-resources debt netting as the leveraged lease model is

now removed. Further, the change is observed in the treatment followed for residual value

guarantees (Kabir, and Rahman, 2018).

Effect of change on companies having significant level of lease financing

The main effect of the change is undoubtedly to be observed significantly upon the

companies that have significant level of lease financing. However, the major impact yet shall

be upon those relying on operating leases as compared to those with reliance upon finance

lease.

For the entities that have significant level of operating leases shall face a transformation in

the statement of financial position. The indicators signifying the finances shall drastically

change because the balance sheet shall now be required to add some assets as well liabilities

which were earlier treated off balance sheet. Earlier only the profit & loss statement was

affected by operating leases, but now the balance sheet shall also show the effects (Giner,

Merello, and Pardo, 2018).

The lessee companies shall be now required to fully disclose all the lease liabilities in the

balance sheet, which earlier were only informed about in the notes to financial statements.

The impact is major, as the accounting is changed and so is the presentation. The major

corporations are even expected to be required to create new departments for just accounting

the new lease requirements. The effort and money expenditure to deal with the impact is

supposed to be high in the initial adoption at least (Dakis, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In the former accounting standard for lease (AASB 117) both operating lease and

finance lease were allowed, why did companies have a tendency to classify most of the

lease contract as operating lease? How does positive accounting theory relate to this

behaviour of managers?

As seen above, the earlier accounting standard followed a dual model for accounting of

operating and finance leases. While the finance leases were compulsorily required to be

reported in financial statements and ease was seen in case of operating leases. The liability

and asset against operating leases were exempted to be reported in the balance sheet and were

allowed to be carried off balance sheet. A mere disclosure regarding the asset and liabilities

in relation to operating leases was required in the notes to financial statements. The entity

was able to misrepresent the financial statements and true picture of liability was not shown

to the readers of financial statements. The ease in method and opportunity to present

financials in a better state was a main motive behind the tendencies of organisations earlier to

classify most of the lease contracts as operating leases (Brumm, & Liu, 2019).

Positive accounting theory presents an organisation as an accumulation of all the contracts

entered by it. The motive of this theory is to minimize the contracts’ cost to make them look

more valuable. The use of this theory in operation usually leads to the organisations hiding

their material aspects to depict contracts attached with lower costs and organisation looking

more valuable (Kothari, 2019).

There is a relation between the practice of managers classifying most of the leases as

operating lease and positive accounting theory because classification of leases as operating

lease allowed the managers to hide the material liability attached to leases. This led to

showing the financials in a better state with lower obligations than actually headed on entity,

i.e. the costs were tried to be minimised as approached by positive accounting theory (Raj, &

Roy, 2016).

Improved comparability between the companies that lease assets and companies that

borrow to buy assets because of implementation of IFRS 16

The companies who borrow money to buy asset follows an accounting model in which the

assets they own are shown in the balance sheet on the asset side, and the liabilities they have

to pay, i.e. the borrowings are shown on the liabilities side. A dual effect is seen on the

balance sheet and the entire financial statements (Ogilvy, et al. 2018).

finance lease were allowed, why did companies have a tendency to classify most of the

lease contract as operating lease? How does positive accounting theory relate to this

behaviour of managers?

As seen above, the earlier accounting standard followed a dual model for accounting of

operating and finance leases. While the finance leases were compulsorily required to be

reported in financial statements and ease was seen in case of operating leases. The liability

and asset against operating leases were exempted to be reported in the balance sheet and were

allowed to be carried off balance sheet. A mere disclosure regarding the asset and liabilities

in relation to operating leases was required in the notes to financial statements. The entity

was able to misrepresent the financial statements and true picture of liability was not shown

to the readers of financial statements. The ease in method and opportunity to present

financials in a better state was a main motive behind the tendencies of organisations earlier to

classify most of the lease contracts as operating leases (Brumm, & Liu, 2019).

Positive accounting theory presents an organisation as an accumulation of all the contracts

entered by it. The motive of this theory is to minimize the contracts’ cost to make them look

more valuable. The use of this theory in operation usually leads to the organisations hiding

their material aspects to depict contracts attached with lower costs and organisation looking

more valuable (Kothari, 2019).

There is a relation between the practice of managers classifying most of the leases as

operating lease and positive accounting theory because classification of leases as operating

lease allowed the managers to hide the material liability attached to leases. This led to

showing the financials in a better state with lower obligations than actually headed on entity,

i.e. the costs were tried to be minimised as approached by positive accounting theory (Raj, &

Roy, 2016).

Improved comparability between the companies that lease assets and companies that

borrow to buy assets because of implementation of IFRS 16

The companies who borrow money to buy asset follows an accounting model in which the

assets they own are shown in the balance sheet on the asset side, and the liabilities they have

to pay, i.e. the borrowings are shown on the liabilities side. A dual effect is seen on the

balance sheet and the entire financial statements (Ogilvy, et al. 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

After the implementation of IFRS 16, all the companies operating anywhere in the world, if

required to comply with the guidelines of international accounting standards are required to

follow a single and realistic accounting model for lease transactions. Any form of lease, be it

operating of finance lease, shall affect two sides of a balance sheet. An asset shall be created

in the books of lessee and at the same time a lease liability shall also be created. IFRS 16 is

an umbrella standard based upon which the lease accounting standards as followed by every

listed entity, irrespective of the location shall be based. No off-balance sheet treatment of

lease transaction is allowed after the implementation of IFRS 16, except lease of low value

asset (i.e. US$ 5000 or less) and short term leases (i.e. less than 12 months).

As seen from the treatment followed by companies borrowing to buy asset, and leasing asset,

the implementation of IFRS 16 has brought a common accounting treatment, i.e. creation of

an asset and at the same time creation of a liability (Morales-Díaz, and Zamora-Ramírez,

2018).

E.g.: ABC concern borrows $10,000 to buy a plant for water filtering. The effect shall be,

showing a plant of $10,000 on asset side, and borrowings of $10,000 on liability side. The

competitor of ABC concern, XYZ Company leases the same plant for $10,000 and pays no

down payment. A simple treatment would be recording plant on asset side at $10,000 and

recording lease liability of $10,000. The reader reading the financials of both companies can

easily compare the transactions entered by both the companies (Giner, Merello, & Pardo,

2018).

Hence, it can be said that the implementation of IFRS 16 has improved comparability.

Possible explanation as to why after the implementation of AASB 16, reporting entities

might be more likely to buy more assets and lease fewer assets.

Introduction of the new AASB 16 has leashed the opportunity from the hand of organisations

to misstate the financials by classifying most of their leases as operating leases. The liability

of lease is now must to be entered in the financials. There is no way present to hide it from

the stakeholders (Abbott, & Tan‐Kantor, 2018). Also the reporting requirements for lease

transactions are now extended. Implementation of IFRS 16 has raised the costs for companies

that had material leases off balance sheet and that would have such transactions lined for

future as well. For companies who shall lease now have to follow AASB 16 with some

ongoing costs in for obtaining information periodically for reporting lease assets and lease

required to comply with the guidelines of international accounting standards are required to

follow a single and realistic accounting model for lease transactions. Any form of lease, be it

operating of finance lease, shall affect two sides of a balance sheet. An asset shall be created

in the books of lessee and at the same time a lease liability shall also be created. IFRS 16 is

an umbrella standard based upon which the lease accounting standards as followed by every

listed entity, irrespective of the location shall be based. No off-balance sheet treatment of

lease transaction is allowed after the implementation of IFRS 16, except lease of low value

asset (i.e. US$ 5000 or less) and short term leases (i.e. less than 12 months).

As seen from the treatment followed by companies borrowing to buy asset, and leasing asset,

the implementation of IFRS 16 has brought a common accounting treatment, i.e. creation of

an asset and at the same time creation of a liability (Morales-Díaz, and Zamora-Ramírez,

2018).

E.g.: ABC concern borrows $10,000 to buy a plant for water filtering. The effect shall be,

showing a plant of $10,000 on asset side, and borrowings of $10,000 on liability side. The

competitor of ABC concern, XYZ Company leases the same plant for $10,000 and pays no

down payment. A simple treatment would be recording plant on asset side at $10,000 and

recording lease liability of $10,000. The reader reading the financials of both companies can

easily compare the transactions entered by both the companies (Giner, Merello, & Pardo,

2018).

Hence, it can be said that the implementation of IFRS 16 has improved comparability.

Possible explanation as to why after the implementation of AASB 16, reporting entities

might be more likely to buy more assets and lease fewer assets.

Introduction of the new AASB 16 has leashed the opportunity from the hand of organisations

to misstate the financials by classifying most of their leases as operating leases. The liability

of lease is now must to be entered in the financials. There is no way present to hide it from

the stakeholders (Abbott, & Tan‐Kantor, 2018). Also the reporting requirements for lease

transactions are now extended. Implementation of IFRS 16 has raised the costs for companies

that had material leases off balance sheet and that would have such transactions lined for

future as well. For companies who shall lease now have to follow AASB 16 with some

ongoing costs in for obtaining information periodically for reporting lease assets and lease

liabilities on every reporting date. These could also be termed as re-measurement costs. Costs

are also to be incurred by organisations to determine discount rates now. Also, for the

companies whose lease portfolio is huge, the extended disclosure requirement shall also incur

costs. The financial information, due to non-representation of liability relating to operating

leases, was misled. There was no faithful representation in relation to the lease related

transactions. Mainly in every case the burden is largely upon the lessee side (Hladika, and

Valenta, 2018).

The impact of applying AASB 16 is huge as already seen. The lessee companies shall

certainly reconsider their lease strategies. It is likely from the part of the lessee companies

with large lease portfolio to now rather buy assets than to lease them because of the extended

regulations imparted upon them. Also the use of single accounting model has snatched the

opportunity to keep certain liabilities off balance sheet earlier. Hence, the implementation of

ASSB 16 is expected to have an impact upon the leasing market certainly (Baskerville,

George, & Makale, 2018).

The key disclosures made by Woolworths Group on its accounting for leases including

on the transitional provision and effect of the transition to AASB 16 from AASB 117.

KEY DISCLOSURES MADE IN ANNUAL REPORT

It is analysed that the lessee companies shall be now required to fully disclose all the lease

liabilities in the balance sheet, which earlier were only informed about in the notes to

financial statements. However, failure to meet these lease provisions of the company may

result to high penalties to company. Woolworths Group has clearly inserted a note in its

annual report in relation to the new AASB 16, Leases. The company mentions about

replacement of their earlier followed AASB 117 with the new AASB 16. The change in the

accounting of operating leases now by recognition of asset with name right-of-use (ROU)

asset and corresponding lease liability in the Consolidated Statement of Financial Position is

being correctly stated. The effect of the same upon the statement of financial performance is

also mentioned. The group shall now recognise depreciation upon the right-of-use (ROU)

asset and interest expense upon the lease liability. Disclosures have been made about the

impact upon the accounts of financial year 2018 to make them comparative with the

financials of upcoming year 2019, as the company has prepared to adopt the AASB 16 from 1

July 2019 (Han, Chand, & Mala, 2019).

are also to be incurred by organisations to determine discount rates now. Also, for the

companies whose lease portfolio is huge, the extended disclosure requirement shall also incur

costs. The financial information, due to non-representation of liability relating to operating

leases, was misled. There was no faithful representation in relation to the lease related

transactions. Mainly in every case the burden is largely upon the lessee side (Hladika, and

Valenta, 2018).

The impact of applying AASB 16 is huge as already seen. The lessee companies shall

certainly reconsider their lease strategies. It is likely from the part of the lessee companies

with large lease portfolio to now rather buy assets than to lease them because of the extended

regulations imparted upon them. Also the use of single accounting model has snatched the

opportunity to keep certain liabilities off balance sheet earlier. Hence, the implementation of

ASSB 16 is expected to have an impact upon the leasing market certainly (Baskerville,

George, & Makale, 2018).

The key disclosures made by Woolworths Group on its accounting for leases including

on the transitional provision and effect of the transition to AASB 16 from AASB 117.

KEY DISCLOSURES MADE IN ANNUAL REPORT

It is analysed that the lessee companies shall be now required to fully disclose all the lease

liabilities in the balance sheet, which earlier were only informed about in the notes to

financial statements. However, failure to meet these lease provisions of the company may

result to high penalties to company. Woolworths Group has clearly inserted a note in its

annual report in relation to the new AASB 16, Leases. The company mentions about

replacement of their earlier followed AASB 117 with the new AASB 16. The change in the

accounting of operating leases now by recognition of asset with name right-of-use (ROU)

asset and corresponding lease liability in the Consolidated Statement of Financial Position is

being correctly stated. The effect of the same upon the statement of financial performance is

also mentioned. The group shall now recognise depreciation upon the right-of-use (ROU)

asset and interest expense upon the lease liability. Disclosures have been made about the

impact upon the accounts of financial year 2018 to make them comparative with the

financials of upcoming year 2019, as the company has prepared to adopt the AASB 16 from 1

July 2019 (Han, Chand, & Mala, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The group expects the property leases for warehousing facilities, support offices, distribution

centres and retail premises to be mainly effected by the impact of the new AASB16 (Chen, et

al. 2018).However, disclosure related to the changes in the lease recording needs to be made

in the notes to accounts attached with the annual report of company. The main effect of the

change is undoubtedly to be observed significantly upon the companies that have significant

level of lease financing. However, the major impact yet shall be upon those relying on

operating leases as compared to those with reliance upon finance lease which would be

disclosed in the recorded items off the

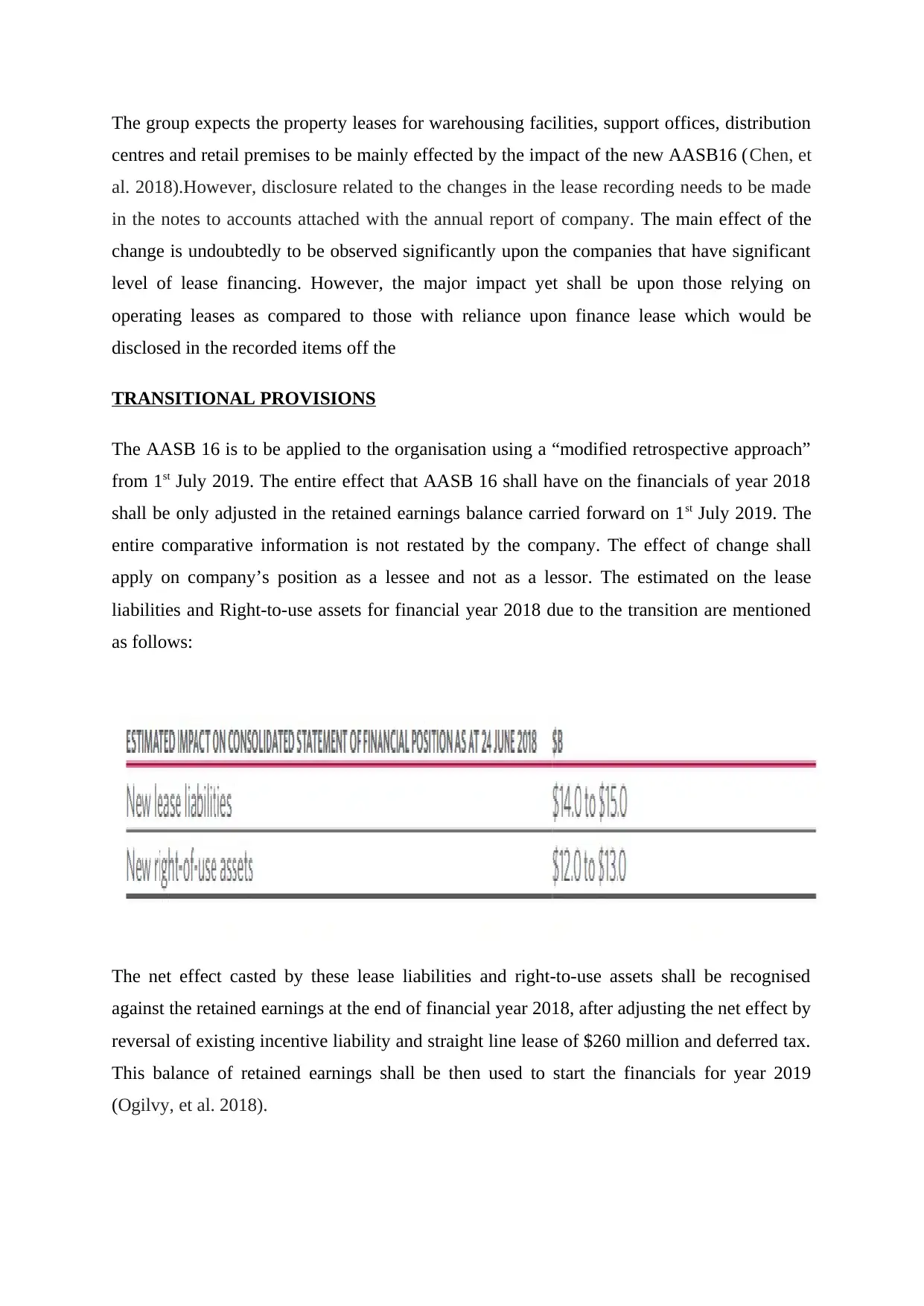

TRANSITIONAL PROVISIONS

The AASB 16 is to be applied to the organisation using a “modified retrospective approach”

from 1st July 2019. The entire effect that AASB 16 shall have on the financials of year 2018

shall be only adjusted in the retained earnings balance carried forward on 1st July 2019. The

entire comparative information is not restated by the company. The effect of change shall

apply on company’s position as a lessee and not as a lessor. The estimated on the lease

liabilities and Right-to-use assets for financial year 2018 due to the transition are mentioned

as follows:

The net effect casted by these lease liabilities and right-to-use assets shall be recognised

against the retained earnings at the end of financial year 2018, after adjusting the net effect by

reversal of existing incentive liability and straight line lease of $260 million and deferred tax.

This balance of retained earnings shall be then used to start the financials for year 2019

(Ogilvy, et al. 2018).

centres and retail premises to be mainly effected by the impact of the new AASB16 (Chen, et

al. 2018).However, disclosure related to the changes in the lease recording needs to be made

in the notes to accounts attached with the annual report of company. The main effect of the

change is undoubtedly to be observed significantly upon the companies that have significant

level of lease financing. However, the major impact yet shall be upon those relying on

operating leases as compared to those with reliance upon finance lease which would be

disclosed in the recorded items off the

TRANSITIONAL PROVISIONS

The AASB 16 is to be applied to the organisation using a “modified retrospective approach”

from 1st July 2019. The entire effect that AASB 16 shall have on the financials of year 2018

shall be only adjusted in the retained earnings balance carried forward on 1st July 2019. The

entire comparative information is not restated by the company. The effect of change shall

apply on company’s position as a lessee and not as a lessor. The estimated on the lease

liabilities and Right-to-use assets for financial year 2018 due to the transition are mentioned

as follows:

The net effect casted by these lease liabilities and right-to-use assets shall be recognised

against the retained earnings at the end of financial year 2018, after adjusting the net effect by

reversal of existing incentive liability and straight line lease of $260 million and deferred tax.

This balance of retained earnings shall be then used to start the financials for year 2019

(Ogilvy, et al. 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Another important transitional disclosure made by the group relate to the non-lease

component of the property lease. AASB 6 exempts payment for non-lease component from

the lease liability except when the lessee company specifically chooses to combine the non-

lease and lease component. The group on account of having material non-lease component in

the leased portfolio elects to not combine both of them. Resultant, the price of the non-lease

component taken on a stand-alone basis shall be excluded from the lease liability of the

property leases. Hence, the entity has estimated the price of non-lease component

individually from the accumulated undiscounted operating lease commitment of worth $22.9

billion for financial year 2018. The estimation of standalone non-lease component is worth

$3,807 million for year 2018. The standalone non-lease component for financial year 2017 is

measured at $4,014 million (Giner, Merello, & Pardo, 2018).

component of the property lease. AASB 6 exempts payment for non-lease component from

the lease liability except when the lessee company specifically chooses to combine the non-

lease and lease component. The group on account of having material non-lease component in

the leased portfolio elects to not combine both of them. Resultant, the price of the non-lease

component taken on a stand-alone basis shall be excluded from the lease liability of the

property leases. Hence, the entity has estimated the price of non-lease component

individually from the accumulated undiscounted operating lease commitment of worth $22.9

billion for financial year 2018. The estimation of standalone non-lease component is worth

$3,807 million for year 2018. The standalone non-lease component for financial year 2017 is

measured at $4,014 million (Giner, Merello, & Pardo, 2018).

Conclusion

It is analysed that financial information, due to non-representation of liability relating

to operating leases, was misled in the report. There was no faithful representation in relation

to the lease related transactions. However, various provisions of the lease and undertaken

work have been given in this report. The lease determination for the capital nature and

revenue nature is determined on the basis of the lease provisions. The New AASB 16 is

implemented to remove the erroneous and fraudulent practices for which AASB 117 was

started to be used by many corporations. The initial phase when AASB 16 has been

introduced however is facing much resentment from public. The main resentments are from

lessee corporations. Their efforts as well as cost are certain to raise atleast in the preliminary

phase because of the transition to the new standard. Also a drastic change shall be felt in their

financial statements as the transition is certain to impact upon the capital structure as well as

the profitability. However, the AASB 16 is very certain to leash out the unethical practices

followed in the shade of operating leases in AASB 117. The major benefit is for the

stakeholders of financial statements. Earlier the major liability by lessee corporations was just

reported in notes to accounts and never shown in the balance sheet. This kept the stakeholders

in a state of unawareness. Now the readers shall get a complete glance about the corporate

condition of an organisation by just simply looking at the financial statements. Also the

disclosure in notes shall be improved to impart to the understanding and comparability. The

users shall be more equipped to compare the financials of companies leasing assets and the

companies who borrow to buy assets. At the same time, the difference in the approach of two

companies shall also be known to the users.

It is analysed that financial information, due to non-representation of liability relating

to operating leases, was misled in the report. There was no faithful representation in relation

to the lease related transactions. However, various provisions of the lease and undertaken

work have been given in this report. The lease determination for the capital nature and

revenue nature is determined on the basis of the lease provisions. The New AASB 16 is

implemented to remove the erroneous and fraudulent practices for which AASB 117 was

started to be used by many corporations. The initial phase when AASB 16 has been

introduced however is facing much resentment from public. The main resentments are from

lessee corporations. Their efforts as well as cost are certain to raise atleast in the preliminary

phase because of the transition to the new standard. Also a drastic change shall be felt in their

financial statements as the transition is certain to impact upon the capital structure as well as

the profitability. However, the AASB 16 is very certain to leash out the unethical practices

followed in the shade of operating leases in AASB 117. The major benefit is for the

stakeholders of financial statements. Earlier the major liability by lessee corporations was just

reported in notes to accounts and never shown in the balance sheet. This kept the stakeholders

in a state of unawareness. Now the readers shall get a complete glance about the corporate

condition of an organisation by just simply looking at the financial statements. Also the

disclosure in notes shall be improved to impart to the understanding and comparability. The

users shall be more equipped to compare the financials of companies leasing assets and the

companies who borrow to buy assets. At the same time, the difference in the approach of two

companies shall also be known to the users.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.