ACC30005 Taxation Case Study: Letter of Advice for Ms. McKendrick

VerifiedAdded on 2022/11/19

|10

|2411

|333

Case Study

AI Summary

This document presents a comprehensive letter of advice prepared for Ms. McKendrick, addressing her tax liabilities based on provided documentation and consultations. The letter analyzes various issues, including employment income, business transactions (such as widget importation, distribution, and related expenses), investment decisions (property sales, dividends), and relevant ATO guidelines. It covers topics like capital gains tax (CGT) on property sales and contract terminations, franked dividends, allowable deductions (office rent, employee payments, and work-related expenses), and the implications of bad debts and depreciation. The advice applies the relevant laws to Ms. McKendrick's situation, offering specific recommendations regarding CGT deductions, taxation of franked dividends, and the treatment of various expenses, with a conclusion that highlights the need for additional information to make precise calculations and the satisfactory nature of the maintained records. The document follows the IRAC method to analyze the case.

Running head: LETTER OF ADVICE

Letter of Advice to Ms McKendrick

Name of the Student

Name of the University

Author Note

Letter of Advice to Ms McKendrick

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1LETTER OF ADVICE

Tax Advisors Pty Ltd

ANZ Tower 175 Ferguson Street

Sydney NSW 2000

Australia

Our Ref: 305

24th September 2019.

100 Marina Crescent,

Manly,

New South Wales 2095,

Australia.

Dear Ms Mckendrick,

After going through the various documents that you had provided to us and taking a note of the

requirements suggested by you in our previous meetings, advices have been prepared about your

tax liability for the given year. Kindly find the same below.

Issue

The documents provided by you contain some important matters and suggestions that are

relevant with regards to your situation. This section contains the details of those issues that can

be considered to be relevant to determine your tax situation. They are as follows:

- You have been employed in Compass Airways Ltd. as a long haul flight attendant since

2001. Due to the nature of your job, you tend to fly to international airports for 183 days

in a year and hence the majority of your time is spent in foreign countries;

- During the remaining days, you tend to organise the importation of widgets into Australia

from Widgets Inc. This company has been registered in the USA. Until recently, you had

also been working as a distributor of these widgets to retailers in Australia;

- Your bank statement suggests that you had entered into transactions of varying nature in

the given year. These include employment, investment and business related issues. They

Tax Advisors Pty Ltd

ANZ Tower 175 Ferguson Street

Sydney NSW 2000

Australia

Our Ref: 305

24th September 2019.

100 Marina Crescent,

Manly,

New South Wales 2095,

Australia.

Dear Ms Mckendrick,

After going through the various documents that you had provided to us and taking a note of the

requirements suggested by you in our previous meetings, advices have been prepared about your

tax liability for the given year. Kindly find the same below.

Issue

The documents provided by you contain some important matters and suggestions that are

relevant with regards to your situation. This section contains the details of those issues that can

be considered to be relevant to determine your tax situation. They are as follows:

- You have been employed in Compass Airways Ltd. as a long haul flight attendant since

2001. Due to the nature of your job, you tend to fly to international airports for 183 days

in a year and hence the majority of your time is spent in foreign countries;

- During the remaining days, you tend to organise the importation of widgets into Australia

from Widgets Inc. This company has been registered in the USA. Until recently, you had

also been working as a distributor of these widgets to retailers in Australia;

- Your bank statement suggests that you had entered into transactions of varying nature in

the given year. These include employment, investment and business related issues. They

2LETTER OF ADVICE

have been grouped into different categories for your better understanding of your tax

situation;

- The business related transactions of yours include the purchase of furniture and

partitions, debts written off from outstanding debtors and the stock purchase of widgets

for the business. Others include the salary and redundancy payment for your employee.

The sum received on the distribution agreement is also a part of the business transactions.

Office rent, dinner with the client and advertising contract all come under this head;

- Investment related decisions include the property sold and the early release of deposit

obtained on it. Dividends received on the shares is also a part;

- Your income statement suggests that the tax withheld by you for the year ended 30 June

2019 is $19812 and the gross payments made by you for the year were $82252;

- The laundry, uniform and skin care products purchased by you are a part of the job

related expenditure incurred by you. PAYG instalments paid by you are also a part of the

employment income received by you in the given year;

- Your contract of sale agreement suggests that the price of the land was $720000 and 10%

of the amount was paid at the time of signing. The payment is due on 5/7/2019 and the

contract of sale was completed on 30 April 2019;

- Your distribution agreement with Widgets Ltd. was terminated on 30th June 2019. This

agreement was entered into on 1 September 2017 and is not valid anymore. The payment

received for the termination of the same was $49950. This agreement is a part of what

constitutes a settlement for restraint of trade and ;

have been grouped into different categories for your better understanding of your tax

situation;

- The business related transactions of yours include the purchase of furniture and

partitions, debts written off from outstanding debtors and the stock purchase of widgets

for the business. Others include the salary and redundancy payment for your employee.

The sum received on the distribution agreement is also a part of the business transactions.

Office rent, dinner with the client and advertising contract all come under this head;

- Investment related decisions include the property sold and the early release of deposit

obtained on it. Dividends received on the shares is also a part;

- Your income statement suggests that the tax withheld by you for the year ended 30 June

2019 is $19812 and the gross payments made by you for the year were $82252;

- The laundry, uniform and skin care products purchased by you are a part of the job

related expenditure incurred by you. PAYG instalments paid by you are also a part of the

employment income received by you in the given year;

- Your contract of sale agreement suggests that the price of the land was $720000 and 10%

of the amount was paid at the time of signing. The payment is due on 5/7/2019 and the

contract of sale was completed on 30 April 2019;

- Your distribution agreement with Widgets Ltd. was terminated on 30th June 2019. This

agreement was entered into on 1 September 2017 and is not valid anymore. The payment

received for the termination of the same was $49950. This agreement is a part of what

constitutes a settlement for restraint of trade and ;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3LETTER OF ADVICE

- The fixed asset register suggests that you own a computer, printer and furniture. The

depreciation rates provided on them are at the rate of 33.30%, 33.30% and 10%

respectively;

- The investment property was purchased by you on 1 October 2016 for $440000. This

amount was inclusive of GST. Stamp duty was $21470, legal costs were $990 and

building inspection costs $550. Building repair and renovations that you undertook in

2018 were $6600;

- Despite the termination of the agreement, you had made the payments to the employees.

At present you have stock worth $12000 that the company refuses to take back and you

cannot sell;

Rule

This section of the letter consists of the important guidelines and regulations of the ATO which

have been identified to be relevant in your situation. They are stated in an orderly manner as per

your requirements:

- As per the ATO guidelines, the tax returns for a financial year cover the dates from 1 July

to 30 June of the next year. If any person has withheld tax from previous years, they are

required to file a tax return in the given year;

- According to section 82.135(j) of the Income Tax Assessment Act 1997 (ITAA), a capital

payment received on a contract of restraint of trade that can be considered to be

reasonable to the extent for which it is received does not form a part of the employment

termination payments made by an entity (Ato.gov.au 2019). Hence, it can be considered

to be a part of the capital restraint payments made to you by Widgets Inc. The amount

received as a part of this payment is eligible for the capital gains discount. However you

- The fixed asset register suggests that you own a computer, printer and furniture. The

depreciation rates provided on them are at the rate of 33.30%, 33.30% and 10%

respectively;

- The investment property was purchased by you on 1 October 2016 for $440000. This

amount was inclusive of GST. Stamp duty was $21470, legal costs were $990 and

building inspection costs $550. Building repair and renovations that you undertook in

2018 were $6600;

- Despite the termination of the agreement, you had made the payments to the employees.

At present you have stock worth $12000 that the company refuses to take back and you

cannot sell;

Rule

This section of the letter consists of the important guidelines and regulations of the ATO which

have been identified to be relevant in your situation. They are stated in an orderly manner as per

your requirements:

- As per the ATO guidelines, the tax returns for a financial year cover the dates from 1 July

to 30 June of the next year. If any person has withheld tax from previous years, they are

required to file a tax return in the given year;

- According to section 82.135(j) of the Income Tax Assessment Act 1997 (ITAA), a capital

payment received on a contract of restraint of trade that can be considered to be

reasonable to the extent for which it is received does not form a part of the employment

termination payments made by an entity (Ato.gov.au 2019). Hence, it can be considered

to be a part of the capital restraint payments made to you by Widgets Inc. The amount

received as a part of this payment is eligible for the capital gains discount. However you

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4LETTER OF ADVICE

should be able to prove that your business is eligible for capital gains discount under the

small businesses scheme which suggests that the overall turnover of a business in a given

financial year should not exceed $2 million. The legal fees incurred in this regard are also

deductible from tax;

- According to section 220.405 of ITAA 1997, Franked dividends arise in a situation where

a company pays dividends with franked credits attached to them. Tax is not payable on

such dividends as the tax on them has already been paid by the entity (Ato.gov.au 2019).

However, the franking credits should be separately mentioned in the dividend statement

by the company;

- Any property that is held for investment purposes is charged under the capital gains tax.

If it is used for any business purposes, then the amount received on its sale is a part of the

ordinary income earned by a business. Otherwise, it constitutes a part of the capital gains

earned by an individual. Costs incurred on purchasing it like stamp duty, legal fees and

repairs are added to the cost of the asset to determine the amount of capital gains;

- As per the ATO guidelines, termination payments are unproductive payments made to an

employee for a job that no longer exists. These payments are not to be taxed in the hands

of the employee. They are deducted as annual expenditure incurred in a business by the

employer. There should also be an agreement in place to deal with the stock remaining

with you. Otherwise, an analysis of the value of the remaining stock can be conducted to

obtain some tax benefits;

- Clothing, laundry and skin care expenses can be claimed as a deduction if they satisfy a

few conditions (Ato.gov. au 2019). If the amount claimed is greater than $150 and the

should be able to prove that your business is eligible for capital gains discount under the

small businesses scheme which suggests that the overall turnover of a business in a given

financial year should not exceed $2 million. The legal fees incurred in this regard are also

deductible from tax;

- According to section 220.405 of ITAA 1997, Franked dividends arise in a situation where

a company pays dividends with franked credits attached to them. Tax is not payable on

such dividends as the tax on them has already been paid by the entity (Ato.gov.au 2019).

However, the franking credits should be separately mentioned in the dividend statement

by the company;

- Any property that is held for investment purposes is charged under the capital gains tax.

If it is used for any business purposes, then the amount received on its sale is a part of the

ordinary income earned by a business. Otherwise, it constitutes a part of the capital gains

earned by an individual. Costs incurred on purchasing it like stamp duty, legal fees and

repairs are added to the cost of the asset to determine the amount of capital gains;

- As per the ATO guidelines, termination payments are unproductive payments made to an

employee for a job that no longer exists. These payments are not to be taxed in the hands

of the employee. They are deducted as annual expenditure incurred in a business by the

employer. There should also be an agreement in place to deal with the stock remaining

with you. Otherwise, an analysis of the value of the remaining stock can be conducted to

obtain some tax benefits;

- Clothing, laundry and skin care expenses can be claimed as a deduction if they satisfy a

few conditions (Ato.gov. au 2019). If the amount claimed is greater than $150 and the

5LETTER OF ADVICE

work-related expenses exceed $300, then written records must be maintained to claim

deductions on those expenses;

- Office rent and client’s dinner expense are allowed as a deduction due to the fact that

they are incurred as a part of conducting the business;

- As per section 63 of ITAA 1936 and paragraph 25-35(1)(a) of ITAA 1997, to be able to

write off a bad debt, the bad debt should have existed in the first place. This means that

the service was provided to a customer and the customer had become bankrupt before the

payment of the same.

- Amount spent on the education and the repayment of the HECS/HELP debt are allowed

as a deduction from the amount on which tax is to be paid in a given year;

- Speeding fine incurred during the course of the employment are not deductible by a

person under section 26-5 of ITAA 1997;

- Section 40.25 of the ITAA 1997 suggests that the depreciation charged on the value of an

asset can be deducted from the value of the asset (Legislation.gov.au. 2019). Hence,

depreciation charged on the fixed assets is allowed as a deduction. However, the

percentage of the asset that is put for private usage is not allowed as a deduction on the

value of the asset; and

- The agent’s fees paid on the sale of the property is not allowed as a deduction from the

assessable income as per the rulings of the ATO. However, when assessing the capital

gains earned on the asset, this fees can be added to the cost of the asset by the taxpayer.

Application

On applying the relevant laws mentioned above to your situation, we can suggest you the

following matters from our side:

work-related expenses exceed $300, then written records must be maintained to claim

deductions on those expenses;

- Office rent and client’s dinner expense are allowed as a deduction due to the fact that

they are incurred as a part of conducting the business;

- As per section 63 of ITAA 1936 and paragraph 25-35(1)(a) of ITAA 1997, to be able to

write off a bad debt, the bad debt should have existed in the first place. This means that

the service was provided to a customer and the customer had become bankrupt before the

payment of the same.

- Amount spent on the education and the repayment of the HECS/HELP debt are allowed

as a deduction from the amount on which tax is to be paid in a given year;

- Speeding fine incurred during the course of the employment are not deductible by a

person under section 26-5 of ITAA 1997;

- Section 40.25 of the ITAA 1997 suggests that the depreciation charged on the value of an

asset can be deducted from the value of the asset (Legislation.gov.au. 2019). Hence,

depreciation charged on the fixed assets is allowed as a deduction. However, the

percentage of the asset that is put for private usage is not allowed as a deduction on the

value of the asset; and

- The agent’s fees paid on the sale of the property is not allowed as a deduction from the

assessable income as per the rulings of the ATO. However, when assessing the capital

gains earned on the asset, this fees can be added to the cost of the asset by the taxpayer.

Application

On applying the relevant laws mentioned above to your situation, we can suggest you the

following matters from our side:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6LETTER OF ADVICE

- As your income statement suggests that you have withholding tax remaining from

previous years, you are liable to pay taxes on the amount earned by you during this year;

- As the company Widget Inc has terminated your contract on a sudden basis and you have

entered into an agreement with the entity for not conducting any further trade or supply

of the products for a further period of three years, you are eligible for a 50% CGT

deduction on the amount earned due to the termination of the agreement. However, this

will be applicable only if you are a small business whose annual turnover does not exceed

$ 2 million and the net assets owned by you at any point do not exceed $6 million.

Further information will be needed in this regard to provide you with appropriate advice;

- As the dividends received by you from Compass Airways Ltd. is franked, you are not

required to pay taxes on the same. This is because the company has already paid taxes on

it. As the franked credits have already been separately stated in your dividend statement,

you are exempt from paying taxes on the dividend received during the related financial

year;

- As the property that was purchased by you in Brighton, Victoria on 1 October 2016 was

used only as an investment property and not used for producing any income during the

course of the business, you will be charged CGT on the amount received from the sale of

the property. However, costs incurred on the property like the stamp duty, legal fees and

the renovation of the property are all needed to be added to the cost of the asset in

calculating the capital gains earned from the asset. In your case, the capital gains on the

sale of property are $250390 (not including any indexation);

- The $18000 commission paid to the agent on the disposal of this property is not allowed

as a deduction from the amount earned from the sale of the property by you;

- As your income statement suggests that you have withholding tax remaining from

previous years, you are liable to pay taxes on the amount earned by you during this year;

- As the company Widget Inc has terminated your contract on a sudden basis and you have

entered into an agreement with the entity for not conducting any further trade or supply

of the products for a further period of three years, you are eligible for a 50% CGT

deduction on the amount earned due to the termination of the agreement. However, this

will be applicable only if you are a small business whose annual turnover does not exceed

$ 2 million and the net assets owned by you at any point do not exceed $6 million.

Further information will be needed in this regard to provide you with appropriate advice;

- As the dividends received by you from Compass Airways Ltd. is franked, you are not

required to pay taxes on the same. This is because the company has already paid taxes on

it. As the franked credits have already been separately stated in your dividend statement,

you are exempt from paying taxes on the dividend received during the related financial

year;

- As the property that was purchased by you in Brighton, Victoria on 1 October 2016 was

used only as an investment property and not used for producing any income during the

course of the business, you will be charged CGT on the amount received from the sale of

the property. However, costs incurred on the property like the stamp duty, legal fees and

the renovation of the property are all needed to be added to the cost of the asset in

calculating the capital gains earned from the asset. In your case, the capital gains on the

sale of property are $250390 (not including any indexation);

- The $18000 commission paid to the agent on the disposal of this property is not allowed

as a deduction from the amount earned from the sale of the property by you;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7LETTER OF ADVICE

- The salary and redundancy payments made by you to the employees are allowed as an

expenditure and can be deducted from the annual income earned by you. These expenses

are a part of the expenditure incurred in relation to your business. This is also the case

with the advertisement expenses and office furniture purchased by you;

- The speeding fine that was paid by you is not allowed as a deduction from the income

even if was incurred during the course of the year;

- Other expenses incurred in relation to your employment like the skin care expenses,

uniform and laundry are all allowed as an expenditure as they are incurred as a part of the

employment and have written records for the same;

- Office rent will be allowed as an expenditure while the outstanding debts written off will

be allowed to be deducted from the annual income as well;

- The stock that remains with you can be revalued at the end of the year and any decline in

value can be reduced from the stock remaining with you;

Conclusion

On the basis of the above discussion, it can be suggested that your tax liability can mostly

be accurately calculated during the year. However, some additional information like the annual

turnover of your business and whether you are a small business is necessary to make suggestions

about the payment received on the termination of the contract. The records maintained by you

with respect to different aspects like the dividend received, employment related expenditure and

fixed assets are all satisfactory and sufficient in nature. Any further doubts that you may have in

relation to your tax liability can be raised in the next meeting.

- The salary and redundancy payments made by you to the employees are allowed as an

expenditure and can be deducted from the annual income earned by you. These expenses

are a part of the expenditure incurred in relation to your business. This is also the case

with the advertisement expenses and office furniture purchased by you;

- The speeding fine that was paid by you is not allowed as a deduction from the income

even if was incurred during the course of the year;

- Other expenses incurred in relation to your employment like the skin care expenses,

uniform and laundry are all allowed as an expenditure as they are incurred as a part of the

employment and have written records for the same;

- Office rent will be allowed as an expenditure while the outstanding debts written off will

be allowed to be deducted from the annual income as well;

- The stock that remains with you can be revalued at the end of the year and any decline in

value can be reduced from the stock remaining with you;

Conclusion

On the basis of the above discussion, it can be suggested that your tax liability can mostly

be accurately calculated during the year. However, some additional information like the annual

turnover of your business and whether you are a small business is necessary to make suggestions

about the payment received on the termination of the contract. The records maintained by you

with respect to different aspects like the dividend received, employment related expenditure and

fixed assets are all satisfactory and sufficient in nature. Any further doubts that you may have in

relation to your tax liability can be raised in the next meeting.

8LETTER OF ADVICE

References

Ato.gov.au. 2019. Capital gains tax property exemption tool. [online] Available at:

https://www.ato.gov.au/Calculators-and-tools/Capital-gains-tax-property-exemption-tool/

[Accessed 24 Sep. 2019].

Ato.gov.au. 2019. CGT assets and exemptions. [online] Available at:

https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/ [Accessed 24 Sep.

2019].

Ato.gov.au. 2019. Employment termination payments. [online] Available at:

https://www.ato.gov.au/Individuals/Working/Working-as-an-employee/Leaving-your-job/

Employment-termination-payments/ [Accessed 24 Sep. 2019].

Ato.gov.au. 2019. Rent. [online] Available at:

https://www.ato.gov.au/Individuals/myTax/2018/In-detail/Rent/?page=13 [Accessed 24 Sep.

2019].

Legislation.gov.au. 2019. Income Tax Assessment Act 1997. [online] Available at:

https://www.legislation.gov.au/Details/C2017C00336/Controls/ [Accessed 24 Sep. 2019].

References

Ato.gov.au. 2019. Capital gains tax property exemption tool. [online] Available at:

https://www.ato.gov.au/Calculators-and-tools/Capital-gains-tax-property-exemption-tool/

[Accessed 24 Sep. 2019].

Ato.gov.au. 2019. CGT assets and exemptions. [online] Available at:

https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/ [Accessed 24 Sep.

2019].

Ato.gov.au. 2019. Employment termination payments. [online] Available at:

https://www.ato.gov.au/Individuals/Working/Working-as-an-employee/Leaving-your-job/

Employment-termination-payments/ [Accessed 24 Sep. 2019].

Ato.gov.au. 2019. Rent. [online] Available at:

https://www.ato.gov.au/Individuals/myTax/2018/In-detail/Rent/?page=13 [Accessed 24 Sep.

2019].

Legislation.gov.au. 2019. Income Tax Assessment Act 1997. [online] Available at:

https://www.legislation.gov.au/Details/C2017C00336/Controls/ [Accessed 24 Sep. 2019].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9LETTER OF ADVICE

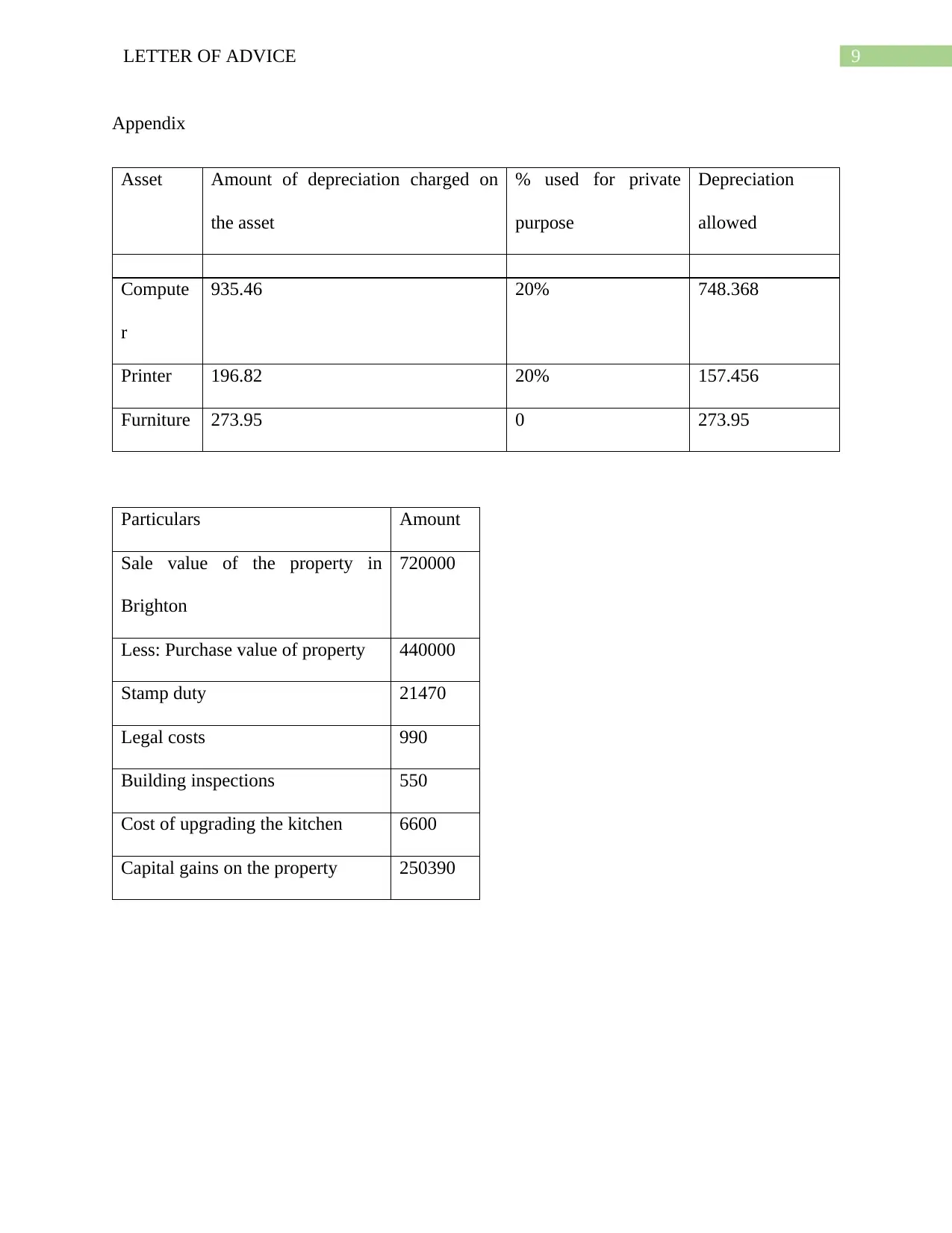

Appendix

Asset Amount of depreciation charged on

the asset

% used for private

purpose

Depreciation

allowed

Compute

r

935.46 20% 748.368

Printer 196.82 20% 157.456

Furniture 273.95 0 273.95

Particulars Amount

Sale value of the property in

Brighton

720000

Less: Purchase value of property 440000

Stamp duty 21470

Legal costs 990

Building inspections 550

Cost of upgrading the kitchen 6600

Capital gains on the property 250390

Appendix

Asset Amount of depreciation charged on

the asset

% used for private

purpose

Depreciation

allowed

Compute

r

935.46 20% 748.368

Printer 196.82 20% 157.456

Furniture 273.95 0 273.95

Particulars Amount

Sale value of the property in

Brighton

720000

Less: Purchase value of property 440000

Stamp duty 21470

Legal costs 990

Building inspections 550

Cost of upgrading the kitchen 6600

Capital gains on the property 250390

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.