Taxation Law Case Study: Individual Tax Return, Calculation & Advice

VerifiedAdded on 2023/04/22

|8

|1184

|94

Case Study

AI Summary

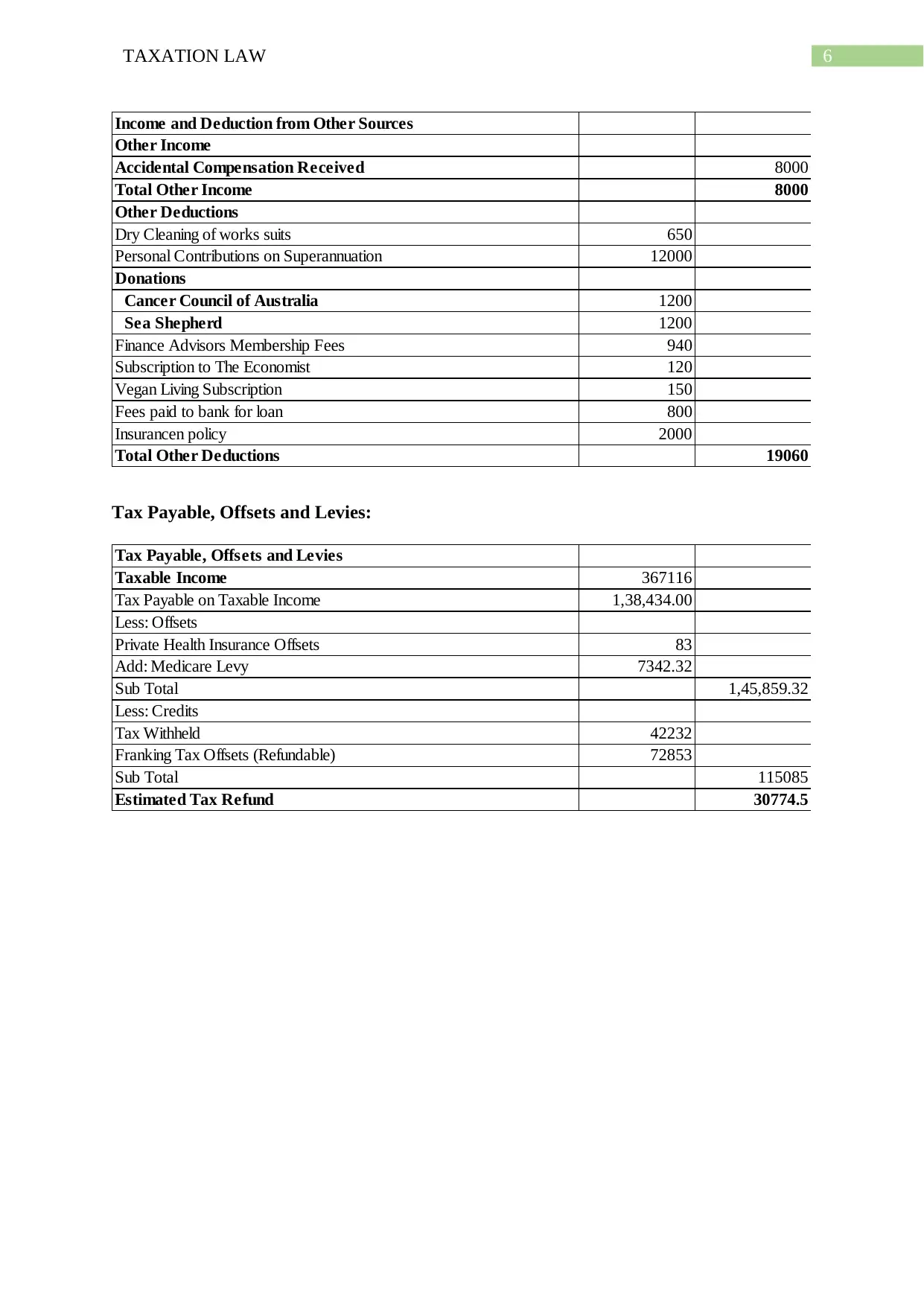

This taxation law case study provides a detailed analysis of an individual's income tax situation, including the preparation of workpapers, calculation of taxable income, and the creation of an individual tax return accompanied by a letter of advice. The case addresses various aspects of income, deductions, and offsets, such as gross salary, superannuation contributions, capital gains (including pre-CGT assets and capital losses), rental property income, and other sources of income like accidental compensation. It also delves into allowable deductions for work-related expenses, rental property expenses, and other eligible deductions. The study culminates in the calculation of tax payable, considering offsets like private health insurance and levies like the Medicare levy, ultimately determining the estimated tax refund. The analysis adheres to relevant sections of the ITAA 1997, providing a comprehensive overview of the client's tax obligations and potential benefits.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.