Production Planning, Limiting Variables, and Transfer Pricing Report

VerifiedAdded on 2023/06/14

|13

|3589

|493

Report

AI Summary

This report provides a detailed analysis of production planning, focusing on identifying and addressing limiting variables to maximize profit. It includes calculations for optimal production plans, considering factors like machine hours and contribution margins. The report also examines the impact...

Accounts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

QUESTION 1..................................................................................................................................1

QUESTION 3..................................................................................................................................7

REFERENCES..............................................................................................................................11

Contents...........................................................................................................................................2

QUESTION 1..................................................................................................................................1

QUESTION 3..................................................................................................................................7

REFERENCES..............................................................................................................................11

QUESTION 1

Limitation Important Variables: Also called as important components, primary budgeting

variables, or regulating characteristics, these are variables which constrain a firm's potential and

prohibit it from accomplishing an intended outcome, and also prohibiting endless development

and endless income (ABU-TAPANJEH and AL-SARAIRAH, 2021). Some instances of

restricting circumstances, like production or revenue growth restrictions, are listed below:

Resource constraints due to a dearth of required supply grade, prolonged drought of

vendors, quota-imposed regulatory or commercial restrictions, and so forth.

Workforce constraints, either nationally or internationally, extra constraints, etc.

Production capability limitations or a lack of real space to accommodate industrial units.

A financial shortfall that could be broad or specific.

The following are the actions taken throughout the judgement call process to offset the

adverse effects of a major constraint:

Compute the payment rate every piece of output.

Calculate the restricting component required to produce a single piece of output.

Compute the restricting factor's contributions every component.

Depending on the modified supplier and transport combinations, modify the profit

projection (Amnuai, 2019).

The below are the 6 stages that will help the business identify the limiting variables:

To establish if a limiting element exists, the management needs to initially set the

optimum income which the business could reach whilst removing any restricting

variables that effect item manufacturing.

Identifying the limiting variables as the management should figure out what is preventing

the corporation's various commodities from being produced.

Subtract changeable expenditures from the sales cost to determine the contributions of

every item every piece of manufacturing.

Assess the value of every item by piece of limiting component as quantity of funds an

item produces for every piece of scarce item it uses.

Put the goods in precedence way as based on the results of Step 4, the item that

contributes the most per piece of limiting component is rated foremost, following by next

closest, and so forth.

Limitation Important Variables: Also called as important components, primary budgeting

variables, or regulating characteristics, these are variables which constrain a firm's potential and

prohibit it from accomplishing an intended outcome, and also prohibiting endless development

and endless income (ABU-TAPANJEH and AL-SARAIRAH, 2021). Some instances of

restricting circumstances, like production or revenue growth restrictions, are listed below:

Resource constraints due to a dearth of required supply grade, prolonged drought of

vendors, quota-imposed regulatory or commercial restrictions, and so forth.

Workforce constraints, either nationally or internationally, extra constraints, etc.

Production capability limitations or a lack of real space to accommodate industrial units.

A financial shortfall that could be broad or specific.

The following are the actions taken throughout the judgement call process to offset the

adverse effects of a major constraint:

Compute the payment rate every piece of output.

Calculate the restricting component required to produce a single piece of output.

Compute the restricting factor's contributions every component.

Depending on the modified supplier and transport combinations, modify the profit

projection (Amnuai, 2019).

The below are the 6 stages that will help the business identify the limiting variables:

To establish if a limiting element exists, the management needs to initially set the

optimum income which the business could reach whilst removing any restricting

variables that effect item manufacturing.

Identifying the limiting variables as the management should figure out what is preventing

the corporation's various commodities from being produced.

Subtract changeable expenditures from the sales cost to determine the contributions of

every item every piece of manufacturing.

Assess the value of every item by piece of limiting component as quantity of funds an

item produces for every piece of scarce item it uses.

Put the goods in precedence way as based on the results of Step 4, the item that

contributes the most per piece of limiting component is rated foremost, following by next

closest, and so forth.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

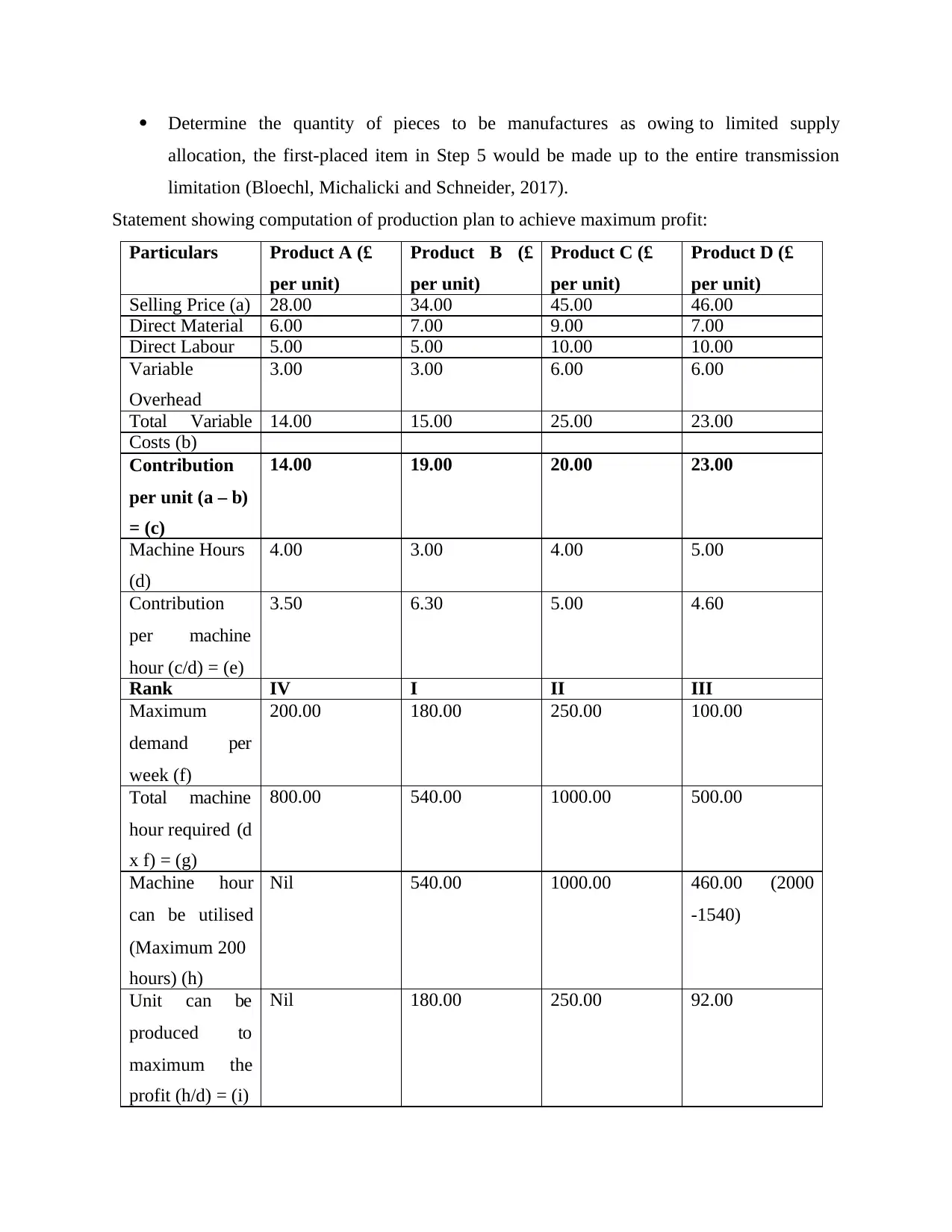

Determine the quantity of pieces to be manufactures as owing to limited supply

allocation, the first-placed item in Step 5 would be made up to the entire transmission

limitation (Bloechl, Michalicki and Schneider, 2017).

Statement showing computation of production plan to achieve maximum profit:

Particulars Product A (£

per unit)

Product B (£

per unit)

Product C (£

per unit)

Product D (£

per unit)

Selling Price (a) 28.00 34.00 45.00 46.00

Direct Material 6.00 7.00 9.00 7.00

Direct Labour 5.00 5.00 10.00 10.00

Variable

Overhead

3.00 3.00 6.00 6.00

Total Variable 14.00 15.00 25.00 23.00

Costs (b)

Contribution

per unit (a – b)

= (c)

14.00 19.00 20.00 23.00

Machine Hours

(d)

4.00 3.00 4.00 5.00

Contribution

per machine

hour (c/d) = (e)

3.50 6.30 5.00 4.60

Rank IV I II III

Maximum

demand per

week (f)

200.00 180.00 250.00 100.00

Total machine

hour required (d

x f) = (g)

800.00 540.00 1000.00 500.00

Machine hour

can be utilised

(Maximum 200

hours) (h)

Nil 540.00 1000.00 460.00 (2000

-1540)

Unit can be

produced to

maximum the

profit (h/d) = (i)

Nil 180.00 250.00 92.00

allocation, the first-placed item in Step 5 would be made up to the entire transmission

limitation (Bloechl, Michalicki and Schneider, 2017).

Statement showing computation of production plan to achieve maximum profit:

Particulars Product A (£

per unit)

Product B (£

per unit)

Product C (£

per unit)

Product D (£

per unit)

Selling Price (a) 28.00 34.00 45.00 46.00

Direct Material 6.00 7.00 9.00 7.00

Direct Labour 5.00 5.00 10.00 10.00

Variable

Overhead

3.00 3.00 6.00 6.00

Total Variable 14.00 15.00 25.00 23.00

Costs (b)

Contribution

per unit (a – b)

= (c)

14.00 19.00 20.00 23.00

Machine Hours

(d)

4.00 3.00 4.00 5.00

Contribution

per machine

hour (c/d) = (e)

3.50 6.30 5.00 4.60

Rank IV I II III

Maximum

demand per

week (f)

200.00 180.00 250.00 100.00

Total machine

hour required (d

x f) = (g)

800.00 540.00 1000.00 500.00

Machine hour

can be utilised

(Maximum 200

hours) (h)

Nil 540.00 1000.00 460.00 (2000

-1540)

Unit can be

produced to

maximum the

profit (h/d) = (i)

Nil 180.00 250.00 92.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

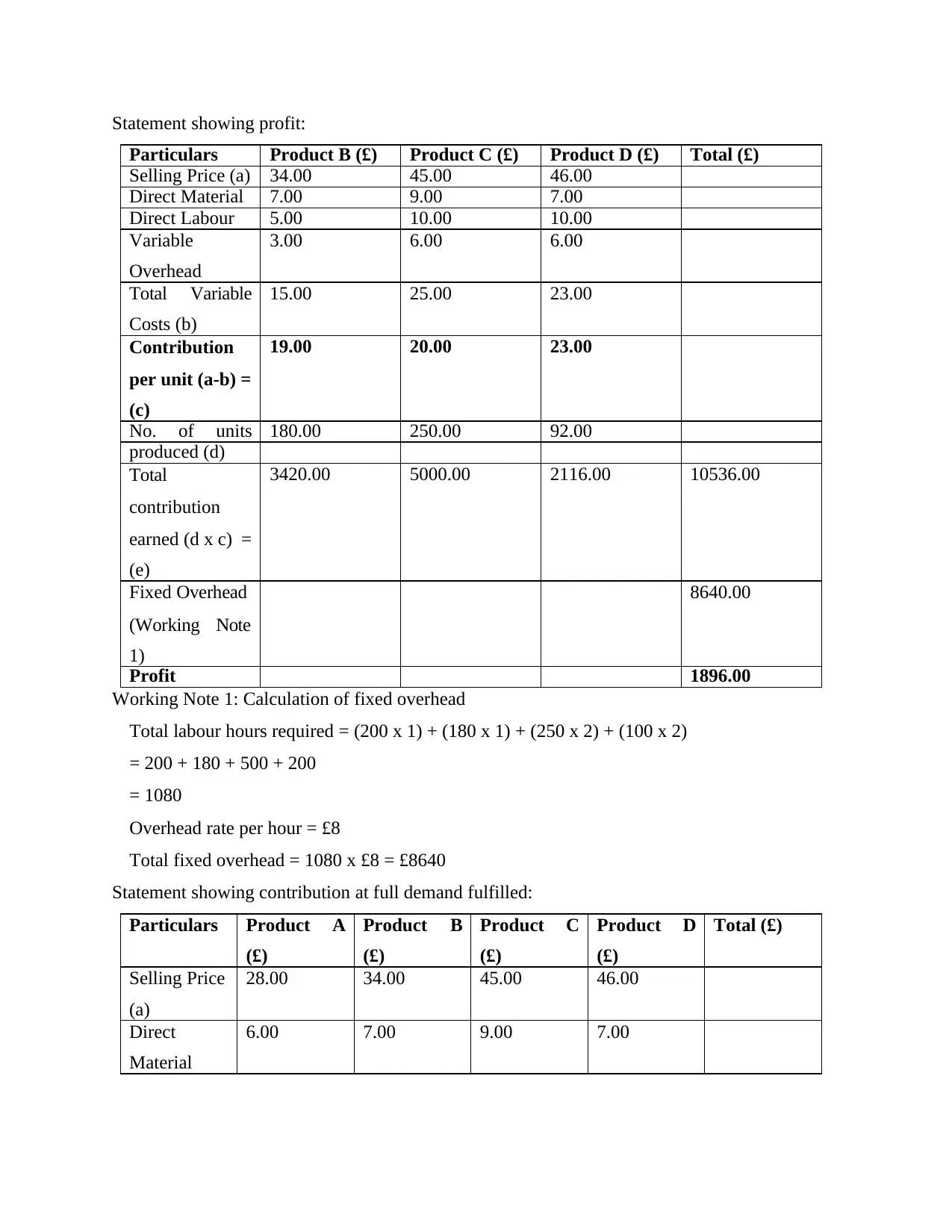

Statement showing profit:

Particulars Product B (£) Product C (£) Product D (£) Total (£)

Selling Price (a) 34.00 45.00 46.00

Direct Material 7.00 9.00 7.00

Direct Labour 5.00 10.00 10.00

Variable

Overhead

3.00 6.00 6.00

Total Variable

Costs (b)

15.00 25.00 23.00

Contribution

per unit (a-b) =

(c)

19.00 20.00 23.00

No. of units 180.00 250.00 92.00

produced (d)

Total

contribution

earned (d x c) =

(e)

3420.00 5000.00 2116.00 10536.00

Fixed Overhead

(Working Note

1)

8640.00

Profit 1896.00

Working Note 1: Calculation of fixed overhead

Total labour hours required = (200 x 1) + (180 x 1) + (250 x 2) + (100 x 2)

= 200 + 180 + 500 + 200

= 1080

Overhead rate per hour = £8

Total fixed overhead = 1080 x £8 = £8640

Statement showing contribution at full demand fulfilled:

Particulars Product A

(£)

Product B

(£)

Product C

(£)

Product D

(£)

Total (£)

Selling Price

(a)

28.00 34.00 45.00 46.00

Direct

Material

6.00 7.00 9.00 7.00

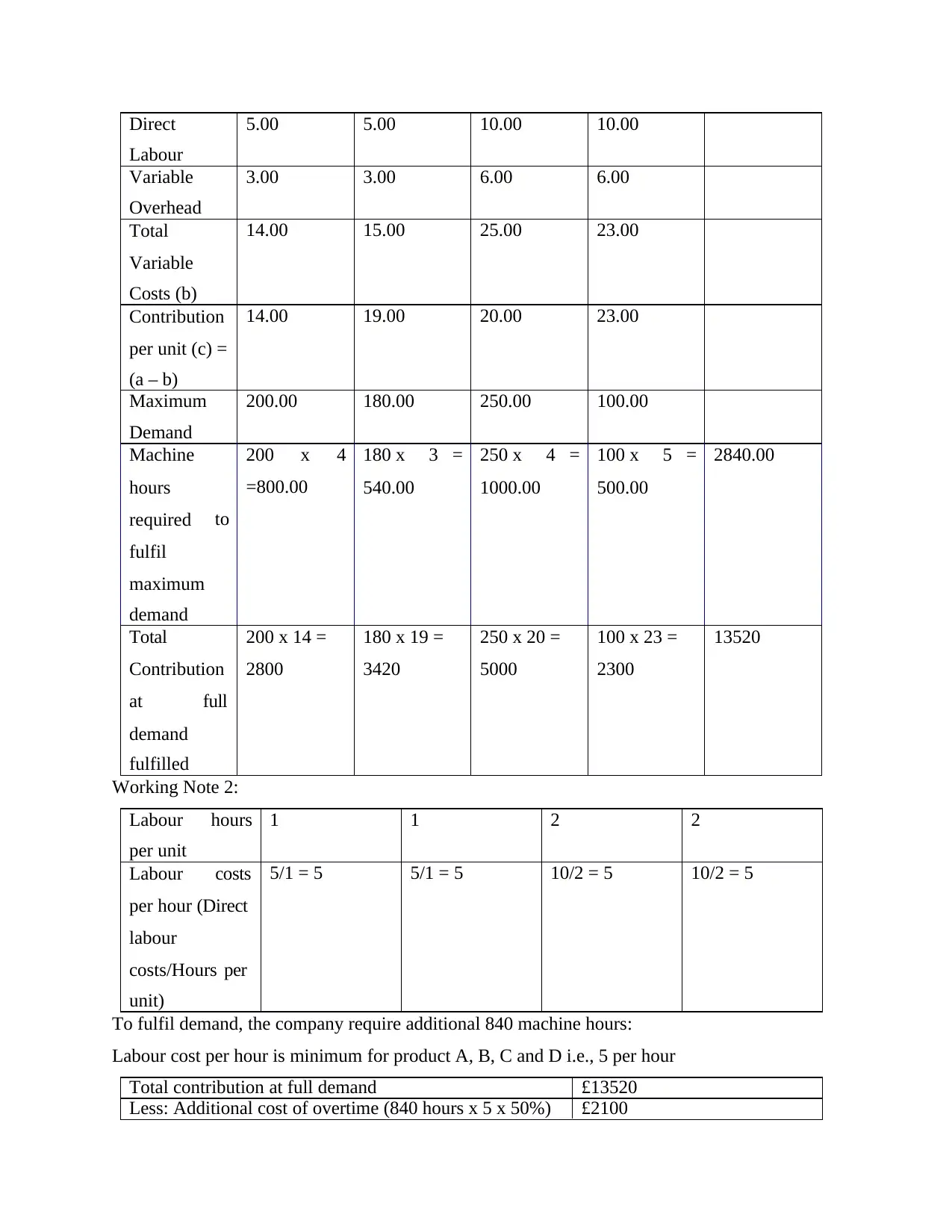

Particulars Product B (£) Product C (£) Product D (£) Total (£)

Selling Price (a) 34.00 45.00 46.00

Direct Material 7.00 9.00 7.00

Direct Labour 5.00 10.00 10.00

Variable

Overhead

3.00 6.00 6.00

Total Variable

Costs (b)

15.00 25.00 23.00

Contribution

per unit (a-b) =

(c)

19.00 20.00 23.00

No. of units 180.00 250.00 92.00

produced (d)

Total

contribution

earned (d x c) =

(e)

3420.00 5000.00 2116.00 10536.00

Fixed Overhead

(Working Note

1)

8640.00

Profit 1896.00

Working Note 1: Calculation of fixed overhead

Total labour hours required = (200 x 1) + (180 x 1) + (250 x 2) + (100 x 2)

= 200 + 180 + 500 + 200

= 1080

Overhead rate per hour = £8

Total fixed overhead = 1080 x £8 = £8640

Statement showing contribution at full demand fulfilled:

Particulars Product A

(£)

Product B

(£)

Product C

(£)

Product D

(£)

Total (£)

Selling Price

(a)

28.00 34.00 45.00 46.00

Direct

Material

6.00 7.00 9.00 7.00

Direct

Labour

5.00 5.00 10.00 10.00

Variable

Overhead

3.00 3.00 6.00 6.00

Total

Variable

Costs (b)

14.00 15.00 25.00 23.00

Contribution

per unit (c) =

(a – b)

14.00 19.00 20.00 23.00

Maximum

Demand

200.00 180.00 250.00 100.00

Machine

hours

required

fulfil

maximum

demand

to

200 x

=800.00

4 180 x

540.00

3 = 250 x

1000.00

4 = 100 x

500.00

5 = 2840.00

Total

Contribution

at full

demand

fulfilled

200 x 14 =

2800

180 x 19 =

3420

250 x 20 =

5000

100 x 23 =

2300

13520

Working Note 2:

Labour hours

per unit

1 1 2 2

Labour costs

per hour (Direct

labour

costs/Hours per

unit)

5/1 = 5 5/1 = 5 10/2 = 5 10/2 = 5

To fulfil demand, the company require additional 840 machine hours:

Labour cost per hour is minimum for product A, B, C and D i.e., 5 per hour

Total contribution at full demand £13520

Less: Additional cost of overtime (840 hours x 5 x 50%) £2100

Labour

5.00 5.00 10.00 10.00

Variable

Overhead

3.00 3.00 6.00 6.00

Total

Variable

Costs (b)

14.00 15.00 25.00 23.00

Contribution

per unit (c) =

(a – b)

14.00 19.00 20.00 23.00

Maximum

Demand

200.00 180.00 250.00 100.00

Machine

hours

required

fulfil

maximum

demand

to

200 x

=800.00

4 180 x

540.00

3 = 250 x

1000.00

4 = 100 x

500.00

5 = 2840.00

Total

Contribution

at full

demand

fulfilled

200 x 14 =

2800

180 x 19 =

3420

250 x 20 =

5000

100 x 23 =

2300

13520

Working Note 2:

Labour hours

per unit

1 1 2 2

Labour costs

per hour (Direct

labour

costs/Hours per

unit)

5/1 = 5 5/1 = 5 10/2 = 5 10/2 = 5

To fulfil demand, the company require additional 840 machine hours:

Labour cost per hour is minimum for product A, B, C and D i.e., 5 per hour

Total contribution at full demand £13520

Less: Additional cost of overtime (840 hours x 5 x 50%) £2100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

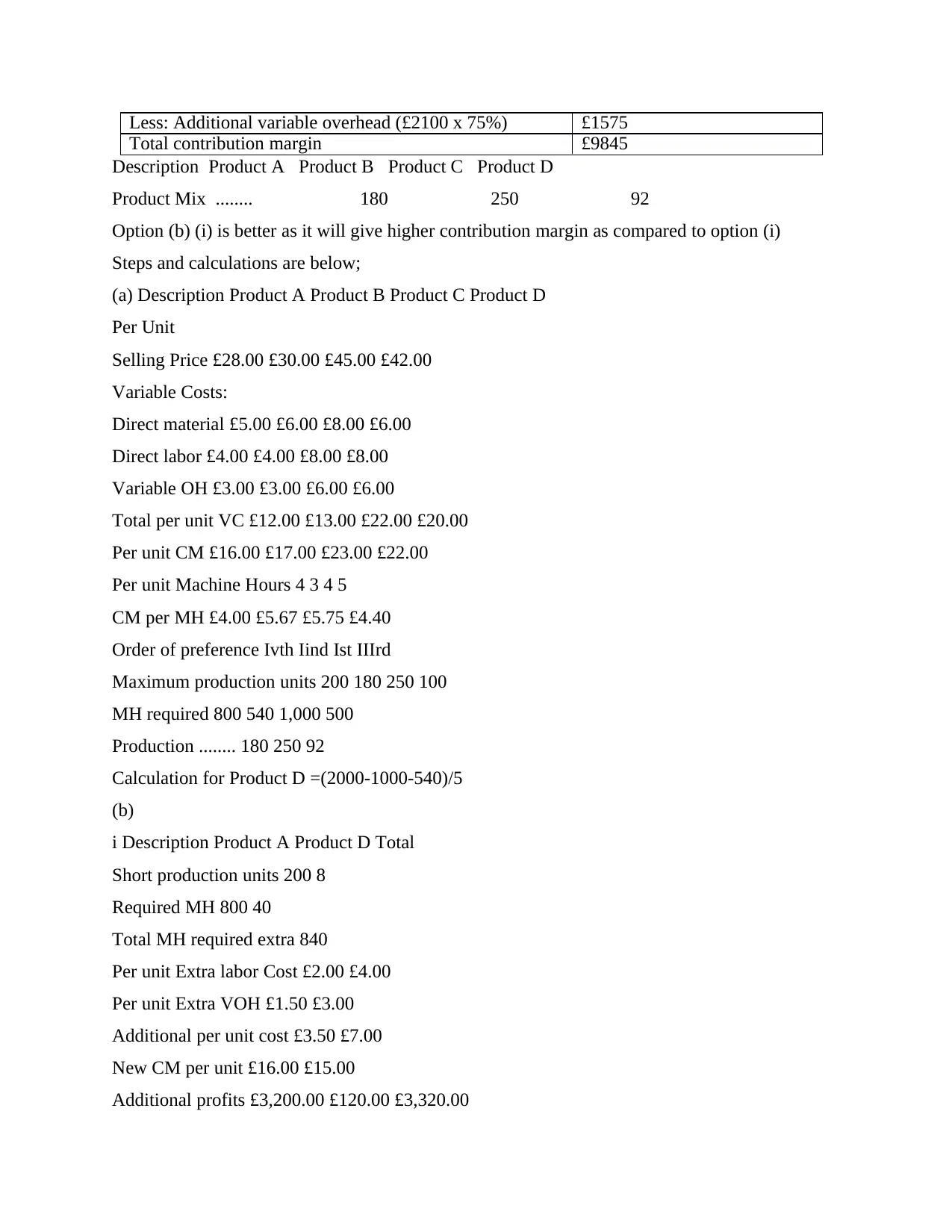

Less: Additional variable overhead (£2100 x 75%) £1575

Total contribution margin £9845

Description Product A Product B Product C Product D

Product Mix ........ 180 250 92

Option (b) (i) is better as it will give higher contribution margin as compared to option (i)

Steps and calculations are below;

(a) Description Product A Product B Product C Product D

Per Unit

Selling Price £28.00 £30.00 £45.00 £42.00

Variable Costs:

Direct material £5.00 £6.00 £8.00 £6.00

Direct labor £4.00 £4.00 £8.00 £8.00

Variable OH £3.00 £3.00 £6.00 £6.00

Total per unit VC £12.00 £13.00 £22.00 £20.00

Per unit CM £16.00 £17.00 £23.00 £22.00

Per unit Machine Hours 4 3 4 5

CM per MH £4.00 £5.67 £5.75 £4.40

Order of preference Ivth Iind Ist IIIrd

Maximum production units 200 180 250 100

MH required 800 540 1,000 500

Production ........ 180 250 92

Calculation for Product D =(2000-1000-540)/5

(b)

i Description Product A Product D Total

Short production units 200 8

Required MH 800 40

Total MH required extra 840

Per unit Extra labor Cost £2.00 £4.00

Per unit Extra VOH £1.50 £3.00

Additional per unit cost £3.50 £7.00

New CM per unit £16.00 £15.00

Additional profits £3,200.00 £120.00 £3,320.00

Total contribution margin £9845

Description Product A Product B Product C Product D

Product Mix ........ 180 250 92

Option (b) (i) is better as it will give higher contribution margin as compared to option (i)

Steps and calculations are below;

(a) Description Product A Product B Product C Product D

Per Unit

Selling Price £28.00 £30.00 £45.00 £42.00

Variable Costs:

Direct material £5.00 £6.00 £8.00 £6.00

Direct labor £4.00 £4.00 £8.00 £8.00

Variable OH £3.00 £3.00 £6.00 £6.00

Total per unit VC £12.00 £13.00 £22.00 £20.00

Per unit CM £16.00 £17.00 £23.00 £22.00

Per unit Machine Hours 4 3 4 5

CM per MH £4.00 £5.67 £5.75 £4.40

Order of preference Ivth Iind Ist IIIrd

Maximum production units 200 180 250 100

MH required 800 540 1,000 500

Production ........ 180 250 92

Calculation for Product D =(2000-1000-540)/5

(b)

i Description Product A Product D Total

Short production units 200 8

Required MH 800 40

Total MH required extra 840

Per unit Extra labor Cost £2.00 £4.00

Per unit Extra VOH £1.50 £3.00

Additional per unit cost £3.50 £7.00

New CM per unit £16.00 £15.00

Additional profits £3,200.00 £120.00 £3,320.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

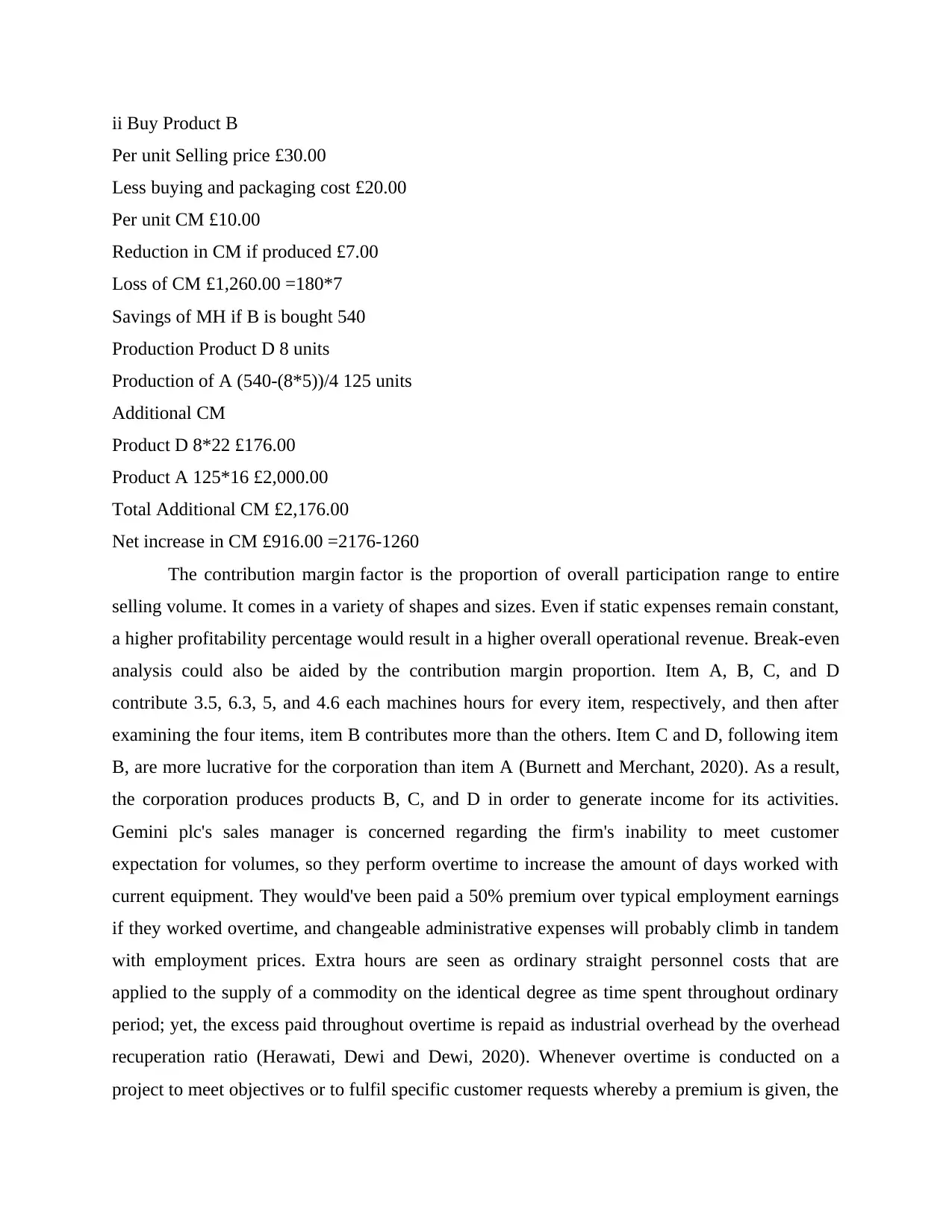

ii Buy Product B

Per unit Selling price £30.00

Less buying and packaging cost £20.00

Per unit CM £10.00

Reduction in CM if produced £7.00

Loss of CM £1,260.00 =180*7

Savings of MH if B is bought 540

Production Product D 8 units

Production of A (540-(8*5))/4 125 units

Additional CM

Product D 8*22 £176.00

Product A 125*16 £2,000.00

Total Additional CM £2,176.00

Net increase in CM £916.00 =2176-1260

The contribution margin factor is the proportion of overall participation range to entire

selling volume. It comes in a variety of shapes and sizes. Even if static expenses remain constant,

a higher profitability percentage would result in a higher overall operational revenue. Break-even

analysis could also be aided by the contribution margin proportion. Item A, B, C, and D

contribute 3.5, 6.3, 5, and 4.6 each machines hours for every item, respectively, and then after

examining the four items, item B contributes more than the others. Item C and D, following item

B, are more lucrative for the corporation than item A (Burnett and Merchant, 2020). As a result,

the corporation produces products B, C, and D in order to generate income for its activities.

Gemini plc's sales manager is concerned regarding the firm's inability to meet customer

expectation for volumes, so they perform overtime to increase the amount of days worked with

current equipment. They would've been paid a 50% premium over typical employment earnings

if they worked overtime, and changeable administrative expenses will probably climb in tandem

with employment prices. Extra hours are seen as ordinary straight personnel costs that are

applied to the supply of a commodity on the identical degree as time spent throughout ordinary

period; yet, the excess paid throughout overtime is repaid as industrial overhead by the overhead

recuperation ratio (Herawati, Dewi and Dewi, 2020). Whenever overtime is conducted on a

project to meet objectives or to fulfil specific customer requests whereby a premium is given, the

Per unit Selling price £30.00

Less buying and packaging cost £20.00

Per unit CM £10.00

Reduction in CM if produced £7.00

Loss of CM £1,260.00 =180*7

Savings of MH if B is bought 540

Production Product D 8 units

Production of A (540-(8*5))/4 125 units

Additional CM

Product D 8*22 £176.00

Product A 125*16 £2,000.00

Total Additional CM £2,176.00

Net increase in CM £916.00 =2176-1260

The contribution margin factor is the proportion of overall participation range to entire

selling volume. It comes in a variety of shapes and sizes. Even if static expenses remain constant,

a higher profitability percentage would result in a higher overall operational revenue. Break-even

analysis could also be aided by the contribution margin proportion. Item A, B, C, and D

contribute 3.5, 6.3, 5, and 4.6 each machines hours for every item, respectively, and then after

examining the four items, item B contributes more than the others. Item C and D, following item

B, are more lucrative for the corporation than item A (Burnett and Merchant, 2020). As a result,

the corporation produces products B, C, and D in order to generate income for its activities.

Gemini plc's sales manager is concerned regarding the firm's inability to meet customer

expectation for volumes, so they perform overtime to increase the amount of days worked with

current equipment. They would've been paid a 50% premium over typical employment earnings

if they worked overtime, and changeable administrative expenses will probably climb in tandem

with employment prices. Extra hours are seen as ordinary straight personnel costs that are

applied to the supply of a commodity on the identical degree as time spent throughout ordinary

period; yet, the excess paid throughout overtime is repaid as industrial overhead by the overhead

recuperation ratio (Herawati, Dewi and Dewi, 2020). Whenever overtime is conducted on a

project to meet objectives or to fulfil specific customer requests whereby a premium is given, the

entire personnel expenditure is applied to the contract as direct personnel expenditure. It is vital

to maintain control of overtime because it has the ability to grow and constitute a typical strategy

for obtaining extra funds. It has a detrimental effect on professional well-being and enthusiasm,

and also on productivity. It could also lead to a significant absence percentage. As a

consequence, the number of overtime worked hours could be closely controlled. Overtime work

must only be allowed if strictly needed. Authorized overtime labour must be closely managed to

assure the most better use of available. It is typically one and a half to two times the average

hourly income. The amount payable in excess to the standard salary ceiling is known as the

overtime surcharge. The direct labour expense includes standard pay. The overtime bonus should

be determined depend on the situation under which it was done, and the prior authorization

amount should be deducted as a consequence.

QUESTION 3

Transfer pricing is utilised whenever one part of a company needs to pay another part of the

identical corporation for goods and goods it provide. For instance, division A may develop a part

which is used in an item made by the similar company, but which may simultaneously be

marketed to the general public, especially rivals of department B's item. As a consequence, A

will be able to generate 2 types of income.

Exterior selling to certain other organisations generate income.

Interior selling income from selling to different commitment units throughout the single

company, assessed at the transaction value (Lepistö and Ihantola, 2018).

Transfer pricing is the process of transferring an item through one division to someone inside

a firm. This technique is employed to assess a primary firm's subsidiaries as separate revenue

generators. Transfer pricing does have an impact on branch purchasing decisions, which could

have corporate taxation implications for the entire company. Here are some crucial topics to

think about:

The cost of a product supplied beyond the company is handled in the similar manner by

the management of a branch on the grounds of income. Since it is component of his

branch's revenue, it is critical to the monetary outcomes for that they were evaluated.

Consumers who already are prioritised; in this instance, the shift supervisor has the

option of selling their goods to other departments within the same organisation or to

clients. If the departmental director is dissatisfied with the transmission cost offered by

to maintain control of overtime because it has the ability to grow and constitute a typical strategy

for obtaining extra funds. It has a detrimental effect on professional well-being and enthusiasm,

and also on productivity. It could also lead to a significant absence percentage. As a

consequence, the number of overtime worked hours could be closely controlled. Overtime work

must only be allowed if strictly needed. Authorized overtime labour must be closely managed to

assure the most better use of available. It is typically one and a half to two times the average

hourly income. The amount payable in excess to the standard salary ceiling is known as the

overtime surcharge. The direct labour expense includes standard pay. The overtime bonus should

be determined depend on the situation under which it was done, and the prior authorization

amount should be deducted as a consequence.

QUESTION 3

Transfer pricing is utilised whenever one part of a company needs to pay another part of the

identical corporation for goods and goods it provide. For instance, division A may develop a part

which is used in an item made by the similar company, but which may simultaneously be

marketed to the general public, especially rivals of department B's item. As a consequence, A

will be able to generate 2 types of income.

Exterior selling to certain other organisations generate income.

Interior selling income from selling to different commitment units throughout the single

company, assessed at the transaction value (Lepistö and Ihantola, 2018).

Transfer pricing is the process of transferring an item through one division to someone inside

a firm. This technique is employed to assess a primary firm's subsidiaries as separate revenue

generators. Transfer pricing does have an impact on branch purchasing decisions, which could

have corporate taxation implications for the entire company. Here are some crucial topics to

think about:

The cost of a product supplied beyond the company is handled in the similar manner by

the management of a branch on the grounds of income. Since it is component of his

branch's revenue, it is critical to the monetary outcomes for that they were evaluated.

Consumers who already are prioritised; in this instance, the shift supervisor has the

option of selling their goods to other departments within the same organisation or to

clients. If the departmental director is dissatisfied with the transmission cost offered by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

another division, they could market their goods to external clients who have paid a higher

amount (Mukhametzyanov, Nugaev and Muhametzyanova, 2017).

Recommended network operators, in this scenario, the departmental director has the

option of purchasing coming from external vendors or from another division within the

business in order to cost customers cheaper. If the cost supplied by external vendors is

acceptable to the supervisor, they will buy through them instead of from different

division within the identical organisation.

Additional aspect which influences overall company profitability is the financial benefit

taxation received each year. If a corporation has branches in many taxation countries,

transferring charges can be utilized to change its branch's claimed profitability. In an ideal world,

the main firm would concentrate on earning the greatest amount of reported revenue in taxation

regimes having reduced corporation revenue taxation. This will be achieved by lowering the

expenses of shifting parts to companies in taxation jurisdictions with the cheapest levels of

taxation. Transfer pricing can be used by a firm to obtain the best operating earnings with the

total production of the business (Oesterreich and Teuteberg, 2019). This nearly always implies

that perhaps the corporation will fix the selling cost to be the product's acquisition cost, as stated

previously in the discussion of corporate taxation identification. By establishing ready to trade to

both external and inner firms, local branches could be possible to manufacture extra revenue for

the firm overall. Branches are urged to develop their manufacturing capacities in particular to

embark on more projects.

Transfer Pricing's Objective- The following are the most important considerations when

putting in place a transferable price strategy:

Distinct revenue estimations must be generated for every section, and every division's

results must be examined separately.

Assist in the integration of manufacturing, selling, and price choices across divisions.

Executives are becoming more conscious of the relevance of products and solutions in

those other areas of the organisation as a result of transmission percentage.

Employing transferring price, the firm would create profit (or price) projections for every

sector separately.

The transfer pricing affects not only the stated profitability of every location, but also

how a firm's assets are assigned (Romadhoni, 2016).

amount (Mukhametzyanov, Nugaev and Muhametzyanova, 2017).

Recommended network operators, in this scenario, the departmental director has the

option of purchasing coming from external vendors or from another division within the

business in order to cost customers cheaper. If the cost supplied by external vendors is

acceptable to the supervisor, they will buy through them instead of from different

division within the identical organisation.

Additional aspect which influences overall company profitability is the financial benefit

taxation received each year. If a corporation has branches in many taxation countries,

transferring charges can be utilized to change its branch's claimed profitability. In an ideal world,

the main firm would concentrate on earning the greatest amount of reported revenue in taxation

regimes having reduced corporation revenue taxation. This will be achieved by lowering the

expenses of shifting parts to companies in taxation jurisdictions with the cheapest levels of

taxation. Transfer pricing can be used by a firm to obtain the best operating earnings with the

total production of the business (Oesterreich and Teuteberg, 2019). This nearly always implies

that perhaps the corporation will fix the selling cost to be the product's acquisition cost, as stated

previously in the discussion of corporate taxation identification. By establishing ready to trade to

both external and inner firms, local branches could be possible to manufacture extra revenue for

the firm overall. Branches are urged to develop their manufacturing capacities in particular to

embark on more projects.

Transfer Pricing's Objective- The following are the most important considerations when

putting in place a transferable price strategy:

Distinct revenue estimations must be generated for every section, and every division's

results must be examined separately.

Assist in the integration of manufacturing, selling, and price choices across divisions.

Executives are becoming more conscious of the relevance of products and solutions in

those other areas of the organisation as a result of transmission percentage.

Employing transferring price, the firm would create profit (or price) projections for every

sector separately.

The transfer pricing affects not only the stated profitability of every location, but also

how a firm's assets are assigned (Romadhoni, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Transfer price techniques include:

Market-based strategy: If transferable goods have had an outside cost level,

profitability zone management would've been notified of the value company might receive and

then have to spend on the international markets for particular goods, and that they should

eventually link this cost to the transaction value. While the external marketplace for the product

seems to be well, effective, and consistent, firms apply the marketplace cost as a maximum

bound for the transferring pricing.

Fears about market-based transferring price abound- If rivals are offering at reduced

prices or using one of numerous "unique" price approaches, relying on market-based transferring

prices might distort interior decision-making while the exterior marketplace is ineffective and

uncertain. Moreover, reliance on share prices creates issues when it comes to safeguarding

"newer" parts.

Benefits:

Interior transference can be forecast in specific cases in which the transferring pricing is

at marketplace pricing, allowing the purchasing department to benefit from additional

services, increased freedom, and supplier reliability. All departments could profit from

reduced administration, marketing, and shipping charges. As a consequence, utilising the

marketplace value as the transferring pricing would lead to actions that are in the finest

interests of the organisation as a whole.

In a fragmented organisation, departmental leaders must have the authority to determine

manufacturing, marketing, and buying choices which appear to be in the greatest

advantage of the branch's performance (Zhong and Fan, 2021).

Drawbacks:

The marketplace pricing might well be transient due to adverse macroeconomic

conditions or selling, and it can be set by the profitability centre’s scale of output

supplied to the international markets.

A market-worth transferring pricing could act as a barrier to deploying any regional

excess capacity in some instances. A pricing based on additional expenditure, on the

other hand, could offer a chance for using up excess resources in addition to contribute

marginally to profitability.

Market-based strategy: If transferable goods have had an outside cost level,

profitability zone management would've been notified of the value company might receive and

then have to spend on the international markets for particular goods, and that they should

eventually link this cost to the transaction value. While the external marketplace for the product

seems to be well, effective, and consistent, firms apply the marketplace cost as a maximum

bound for the transferring pricing.

Fears about market-based transferring price abound- If rivals are offering at reduced

prices or using one of numerous "unique" price approaches, relying on market-based transferring

prices might distort interior decision-making while the exterior marketplace is ineffective and

uncertain. Moreover, reliance on share prices creates issues when it comes to safeguarding

"newer" parts.

Benefits:

Interior transference can be forecast in specific cases in which the transferring pricing is

at marketplace pricing, allowing the purchasing department to benefit from additional

services, increased freedom, and supplier reliability. All departments could profit from

reduced administration, marketing, and shipping charges. As a consequence, utilising the

marketplace value as the transferring pricing would lead to actions that are in the finest

interests of the organisation as a whole.

In a fragmented organisation, departmental leaders must have the authority to determine

manufacturing, marketing, and buying choices which appear to be in the greatest

advantage of the branch's performance (Zhong and Fan, 2021).

Drawbacks:

The marketplace pricing might well be transient due to adverse macroeconomic

conditions or selling, and it can be set by the profitability centre’s scale of output

supplied to the international markets.

A market-worth transferring pricing could act as a barrier to deploying any regional

excess capacity in some instances. A pricing based on additional expenditure, on the

other hand, could offer a chance for using up excess resources in addition to contribute

marginally to profitability.

The transported item might have had a relatively weak market, forcing the transferring

unit to reduce its resale value in terms of selling more internationally.

Negotiated transferring price- In this scenario, the corporation does not provide any rules

for calculating transferring rates. Regional managers are urged to negotiate a pricing

arrangement which is agreeable to all stakeholders. Unregulated availability is frequently paired

with negotiable transferring price. The leadership of some corporations has the power to manage

disputes and impose an "adjudicated" solution. Transferring pricing is also negotiated by the

executives of the providing and recipient divisions (Левицька, 2017). In such conversations,

marketplace pricing, and also optimum and total expenses are frequently employed as variables.

Benefits:

Urge the managers of the company’s sales to devote more emphasis to expense reduction.

Help the procurement department by acquiring the item at a lower cost than that of the

competition.

Set the stage for a much more reasonable assessment of regional performance, which

leaders generally may track through agreements.

Drawbacks:

The management' negotiating talents and ability to negotiate may affect the agreed

transferring pricing, and the end outcome would not be optimal.

They could produce departmental disagreement, and overcoming these disagreements

might need some senior leadership intervention.

They consume a significant amount of effort for the management involved, especially if

there are numerous operations (Серая and Слабая, 2016).

unit to reduce its resale value in terms of selling more internationally.

Negotiated transferring price- In this scenario, the corporation does not provide any rules

for calculating transferring rates. Regional managers are urged to negotiate a pricing

arrangement which is agreeable to all stakeholders. Unregulated availability is frequently paired

with negotiable transferring price. The leadership of some corporations has the power to manage

disputes and impose an "adjudicated" solution. Transferring pricing is also negotiated by the

executives of the providing and recipient divisions (Левицька, 2017). In such conversations,

marketplace pricing, and also optimum and total expenses are frequently employed as variables.

Benefits:

Urge the managers of the company’s sales to devote more emphasis to expense reduction.

Help the procurement department by acquiring the item at a lower cost than that of the

competition.

Set the stage for a much more reasonable assessment of regional performance, which

leaders generally may track through agreements.

Drawbacks:

The management' negotiating talents and ability to negotiate may affect the agreed

transferring pricing, and the end outcome would not be optimal.

They could produce departmental disagreement, and overcoming these disagreements

might need some senior leadership intervention.

They consume a significant amount of effort for the management involved, especially if

there are numerous operations (Серая and Слабая, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journals

ABU-TAPANJEH, A.M. and AL-SARAIRAH, T.M.K., 2021. The Availability of Forensic

Accounting Application Factors to Enhance the Auditors Efficiency in Jordan. The

Journal of Asian Finance, Economics and Business, 8(3), pp.807-819.

Amnuai, W., 2019. Analyses of rhetorical moves and linguistic realizations in accounting

research article abstracts published in international and Thai-based journals. Sage Open,

9(1), p.2158244018822384.

Bloechl, S.J., Michalicki, M. and Schneider, M., 2017. Simulation game for lean leadership–

shopfloor management combined with accounting for lean. Procedia Manufacturing, 9,

pp.97-105.

Burnett, C. and Merchant, G., 2020. Literacy-as-event: Accounting for relationality in literacy

research. Discourse: Studies in the cultural politics of education, 41(1), pp.45-56.

Herawati, N.T., Dewi, L.G.K. and Dewi, G.A.K.R.S., 2020, December. Development of

Android-Based Accounting Cycle Learning Applications to Improve Technology Skills

in Accounting Students. In 5th International Conference on Tourism, Economics,

Accounting, Management and Social Science (TEAMS 2020) (pp. 98-104). Atlantis

Press.

Lepistö, L. and Ihantola, E.M., 2018. Understanding the recruitment and selection processes of

management accountants. Qualitative Research in Accounting & Management.

Mukhametzyanov, R.Z., Nugaev, F.S. and Muhametzyanova, L.Z., 2017. History of accounting

development. Journal of History Culture and Art Research, 6(4), pp.1227-1236.

Oesterreich, T.D. and Teuteberg, F., 2019. The role of business analytics in the controllers and

management accountants’ competence profiles. Journal of accounting & organizational

change.

Romadhoni, R., 2016. Penerapan Enviromental Management Accounting (Ema) Dalam

Meningkatkan Eco-Effieciency Pada Home Industry Tahu Paritan-Jombang (Doctoral

dissertation, Universitas Brawijaya).

Zhong, M. and Fan, T., 2021, March. Research on the Integration of Corporate Financial

Accounting and Management Accounting under Big Data and Block Chain. In Journal

of Physics: Conference Series (Vol. 1827, No. 1, p. 012202). IOP Publishing.

Левицька, С.О., 2017. Еволюція становлення управлінського обліку та його місце в

системі корпоративного управління (Evolution of formation of managerial

accounting and its place in corporate management). Наукові записки Національного

університету «Острозька академія». Серія «Економіка»: науковий журнал, (4

(32)), pp.218-221.

Серая, Н.Н. and Слабая, М.А., 2016. Особенности оценки материально-производственных

запасов в системе управленческого учета. Инновационная экономика:

перспективы развития и совершенствования, (3 (13)).

Books and journals

ABU-TAPANJEH, A.M. and AL-SARAIRAH, T.M.K., 2021. The Availability of Forensic

Accounting Application Factors to Enhance the Auditors Efficiency in Jordan. The

Journal of Asian Finance, Economics and Business, 8(3), pp.807-819.

Amnuai, W., 2019. Analyses of rhetorical moves and linguistic realizations in accounting

research article abstracts published in international and Thai-based journals. Sage Open,

9(1), p.2158244018822384.

Bloechl, S.J., Michalicki, M. and Schneider, M., 2017. Simulation game for lean leadership–

shopfloor management combined with accounting for lean. Procedia Manufacturing, 9,

pp.97-105.

Burnett, C. and Merchant, G., 2020. Literacy-as-event: Accounting for relationality in literacy

research. Discourse: Studies in the cultural politics of education, 41(1), pp.45-56.

Herawati, N.T., Dewi, L.G.K. and Dewi, G.A.K.R.S., 2020, December. Development of

Android-Based Accounting Cycle Learning Applications to Improve Technology Skills

in Accounting Students. In 5th International Conference on Tourism, Economics,

Accounting, Management and Social Science (TEAMS 2020) (pp. 98-104). Atlantis

Press.

Lepistö, L. and Ihantola, E.M., 2018. Understanding the recruitment and selection processes of

management accountants. Qualitative Research in Accounting & Management.

Mukhametzyanov, R.Z., Nugaev, F.S. and Muhametzyanova, L.Z., 2017. History of accounting

development. Journal of History Culture and Art Research, 6(4), pp.1227-1236.

Oesterreich, T.D. and Teuteberg, F., 2019. The role of business analytics in the controllers and

management accountants’ competence profiles. Journal of accounting & organizational

change.

Romadhoni, R., 2016. Penerapan Enviromental Management Accounting (Ema) Dalam

Meningkatkan Eco-Effieciency Pada Home Industry Tahu Paritan-Jombang (Doctoral

dissertation, Universitas Brawijaya).

Zhong, M. and Fan, T., 2021, March. Research on the Integration of Corporate Financial

Accounting and Management Accounting under Big Data and Block Chain. In Journal

of Physics: Conference Series (Vol. 1827, No. 1, p. 012202). IOP Publishing.

Левицька, С.О., 2017. Еволюція становлення управлінського обліку та його місце в

системі корпоративного управління (Evolution of formation of managerial

accounting and its place in corporate management). Наукові записки Національного

університету «Острозька академія». Серія «Економіка»: науковий журнал, (4

(32)), pp.218-221.

Серая, Н.Н. and Слабая, М.А., 2016. Особенности оценки материально-производственных

запасов в системе управленческого учета. Инновационная экономика:

перспективы развития и совершенствования, (3 (13)).

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.