Loan Application Process Assessment

VerifiedAdded on 2022/12/29

|29

|4634

|54

AI Summary

This article provides a comprehensive guide to the loan application process and assessment. It covers the documents required, steps involved, and the importance of credit score. The article also discusses the process of completing the customer file and processing the application for credit. It provides insights into loan comments and evidence of income. The subject of loan application and process assessment is explored in detail.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Loan Application

Process Assessment

Process Assessment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Task 1: ...................................................................................................................................1

File notes from first contact through to settlement in chronological order............................1

Authorised Credit Representative Credit Guide and Licensee Credit Guide.........................2

Privacy Statement and Consent form.....................................................................................2

Client Needs Review or Fact Find..........................................................................................3

Combined Credit Quote and Proposal....................................................................................3

Product Comparison Report Preliminary Assessment...........................................................3

Costing sheet for Fees and Charges........................................................................................4

Fully completed Lender Loan Application or Copy of Online lodgement............................5

Lender’s loan Document Check List .....................................................................................6

Task 2: Process application for credit....................................................................................8

A completed serviceability calculator (refer to useful resources)

................................................................................................................................................8

Loan Comments/Lender Comments.......................................................................................8

Evidence of Income ...............................................................................................................8

Evidence of savings/equity and other loan commitments....................................................17

Evidence of Valuation successfully completed....................................................................17

Anti-Money Laundering/Counter Terrorism Financing ID requirements............................22

A Compliance file checklist.................................................................................................22

Task 3: Completing customer file........................................................................................24

Task 4: Customer /referrer data base ...................................................................................25

CONCLUSION..............................................................................................................................26

REFERENCES..............................................................................................................................27

........................................................................................................................................................27

APPENDICES...............................................................................................................................28

AAMC TRAINING DOCUMENT CHECKLIST...............................................................28

.......................................................................................................................................................29

Task 1: ...................................................................................................................................1

File notes from first contact through to settlement in chronological order............................1

Authorised Credit Representative Credit Guide and Licensee Credit Guide.........................2

Privacy Statement and Consent form.....................................................................................2

Client Needs Review or Fact Find..........................................................................................3

Combined Credit Quote and Proposal....................................................................................3

Product Comparison Report Preliminary Assessment...........................................................3

Costing sheet for Fees and Charges........................................................................................4

Fully completed Lender Loan Application or Copy of Online lodgement............................5

Lender’s loan Document Check List .....................................................................................6

Task 2: Process application for credit....................................................................................8

A completed serviceability calculator (refer to useful resources)

................................................................................................................................................8

Loan Comments/Lender Comments.......................................................................................8

Evidence of Income ...............................................................................................................8

Evidence of savings/equity and other loan commitments....................................................17

Evidence of Valuation successfully completed....................................................................17

Anti-Money Laundering/Counter Terrorism Financing ID requirements............................22

A Compliance file checklist.................................................................................................22

Task 3: Completing customer file........................................................................................24

Task 4: Customer /referrer data base ...................................................................................25

CONCLUSION..............................................................................................................................26

REFERENCES..............................................................................................................................27

........................................................................................................................................................27

APPENDICES...............................................................................................................................28

AAMC TRAINING DOCUMENT CHECKLIST...............................................................28

.......................................................................................................................................................29

INTRODUCTION

Everybody in this world needs loan for something or the other in their life. This loan

taking process can be used to fulfil their needs. The individual has to verify various different

documents that the bank is asking if they don't fulfil it the bank will not give them loan. Another

major requirement that the banks nowadays are asking the credit score of the individual. In this

report the individual is needing the loan for building his house.

MAIN BODY

Task 1:

FHOGs is an abbreviation for First Home Owner Grant and it is a scheme that was

founded in 1 July 2000. This was set up in order to offset the effects of GST on Home

Ownership. It is to be considered as a national scheme that is funded by an accumulation of

territories and states and are being administered in accordance to their own legislature.

There has been a substantial decline in the affordability criteria in the housing market of

Australia. This problem of affordability is more excruciating for the first-time buyers and

therefore in order to mitigate this FHOGs are introduced. Any fluctuations in these criteria will

result in the hike of prices for the first-time buyers. And therefore, houses might exceed their

affordability criteria.

File notes from first contact through to settlement in chronological order

The notes taken in the first interaction by the broker associated with the eligible criteria of the

client will revolve around:

1. In order to check the eligibility criteria for loan the credit score of the concerned client

was 750 and therefore he as eligible for the loan.

2. The salary slip of client was taken into consideration in order to make sure that he has

frequent income flow.

3. In order to make sure that the client is eligible for paying the principal amount of the loan

along with the interest, his income was taken into consideration.

4. Client's legal record was also looked at.

Everybody in this world needs loan for something or the other in their life. This loan

taking process can be used to fulfil their needs. The individual has to verify various different

documents that the bank is asking if they don't fulfil it the bank will not give them loan. Another

major requirement that the banks nowadays are asking the credit score of the individual. In this

report the individual is needing the loan for building his house.

MAIN BODY

Task 1:

FHOGs is an abbreviation for First Home Owner Grant and it is a scheme that was

founded in 1 July 2000. This was set up in order to offset the effects of GST on Home

Ownership. It is to be considered as a national scheme that is funded by an accumulation of

territories and states and are being administered in accordance to their own legislature.

There has been a substantial decline in the affordability criteria in the housing market of

Australia. This problem of affordability is more excruciating for the first-time buyers and

therefore in order to mitigate this FHOGs are introduced. Any fluctuations in these criteria will

result in the hike of prices for the first-time buyers. And therefore, houses might exceed their

affordability criteria.

File notes from first contact through to settlement in chronological order

The notes taken in the first interaction by the broker associated with the eligible criteria of the

client will revolve around:

1. In order to check the eligibility criteria for loan the credit score of the concerned client

was 750 and therefore he as eligible for the loan.

2. The salary slip of client was taken into consideration in order to make sure that he has

frequent income flow.

3. In order to make sure that the client is eligible for paying the principal amount of the loan

along with the interest, his income was taken into consideration.

4. Client's legal record was also looked at.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Authorised Credit Representative Credit Guide and Licensee Credit Guide

The guide for the home loan revolves around the aforementioned steps.

Privacy Statement and Consent form

The privacy statement and content form are as follows:

Consent form revolves around making sure the client is compatible with the terms and

conditions of the loan provider. It helps in having a clarity in the contract.

Client Needs Review or Fact Find

1. Client needs the loan because the affordability structure of the marketplace is higher than

the client's savings.

2. The option of loan is taken into consideration because the client does not have to pay the

whole amount of loan at once. He can distribute that amount and pay it in instalments

over a fixed period of time.

3. Since the client is buying a house for the very first time, the prices of house is not

compatible with his pay-out structure.

The guide for the home loan revolves around the aforementioned steps.

Privacy Statement and Consent form

The privacy statement and content form are as follows:

Consent form revolves around making sure the client is compatible with the terms and

conditions of the loan provider. It helps in having a clarity in the contract.

Client Needs Review or Fact Find

1. Client needs the loan because the affordability structure of the marketplace is higher than

the client's savings.

2. The option of loan is taken into consideration because the client does not have to pay the

whole amount of loan at once. He can distribute that amount and pay it in instalments

over a fixed period of time.

3. Since the client is buying a house for the very first time, the prices of house is not

compatible with his pay-out structure.

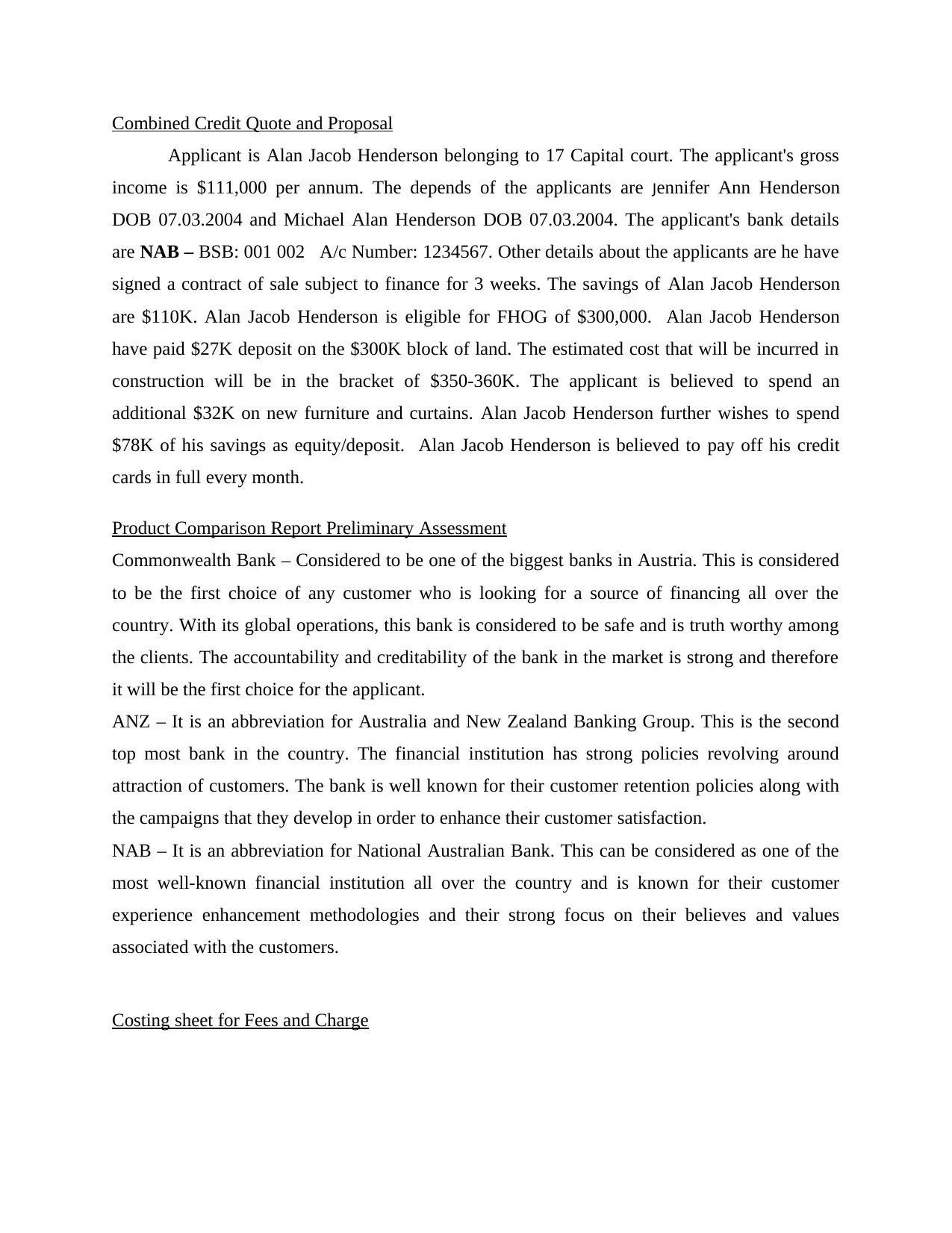

Combined Credit Quote and Proposal

Applicant is Alan Jacob Henderson belonging to 17 Capital court. The applicant's gross

income is $111,000 per annum. The depends of the applicants are Jennifer Ann Henderson

DOB 07.03.2004 and Michael Alan Henderson DOB 07.03.2004. The applicant's bank details

are NAB – BSB: 001 002 A/c Number: 1234567. Other details about the applicants are he have

signed a contract of sale subject to finance for 3 weeks. The savings of Alan Jacob Henderson

are $110K. Alan Jacob Henderson is eligible for FHOG of $300,000. Alan Jacob Henderson

have paid $27K deposit on the $300K block of land. The estimated cost that will be incurred in

construction will be in the bracket of $350-360K. The applicant is believed to spend an

additional $32K on new furniture and curtains. Alan Jacob Henderson further wishes to spend

$78K of his savings as equity/deposit. Alan Jacob Henderson is believed to pay off his credit

cards in full every month.

Product Comparison Report Preliminary Assessment

Commonwealth Bank – Considered to be one of the biggest banks in Austria. This is considered

to be the first choice of any customer who is looking for a source of financing all over the

country. With its global operations, this bank is considered to be safe and is truth worthy among

the clients. The accountability and creditability of the bank in the market is strong and therefore

it will be the first choice for the applicant.

ANZ – It is an abbreviation for Australia and New Zealand Banking Group. This is the second

top most bank in the country. The financial institution has strong policies revolving around

attraction of customers. The bank is well known for their customer retention policies along with

the campaigns that they develop in order to enhance their customer satisfaction.

NAB – It is an abbreviation for National Australian Bank. This can be considered as one of the

most well-known financial institution all over the country and is known for their customer

experience enhancement methodologies and their strong focus on their believes and values

associated with the customers.

Costing sheet for Fees and Charge

Applicant is Alan Jacob Henderson belonging to 17 Capital court. The applicant's gross

income is $111,000 per annum. The depends of the applicants are Jennifer Ann Henderson

DOB 07.03.2004 and Michael Alan Henderson DOB 07.03.2004. The applicant's bank details

are NAB – BSB: 001 002 A/c Number: 1234567. Other details about the applicants are he have

signed a contract of sale subject to finance for 3 weeks. The savings of Alan Jacob Henderson

are $110K. Alan Jacob Henderson is eligible for FHOG of $300,000. Alan Jacob Henderson

have paid $27K deposit on the $300K block of land. The estimated cost that will be incurred in

construction will be in the bracket of $350-360K. The applicant is believed to spend an

additional $32K on new furniture and curtains. Alan Jacob Henderson further wishes to spend

$78K of his savings as equity/deposit. Alan Jacob Henderson is believed to pay off his credit

cards in full every month.

Product Comparison Report Preliminary Assessment

Commonwealth Bank – Considered to be one of the biggest banks in Austria. This is considered

to be the first choice of any customer who is looking for a source of financing all over the

country. With its global operations, this bank is considered to be safe and is truth worthy among

the clients. The accountability and creditability of the bank in the market is strong and therefore

it will be the first choice for the applicant.

ANZ – It is an abbreviation for Australia and New Zealand Banking Group. This is the second

top most bank in the country. The financial institution has strong policies revolving around

attraction of customers. The bank is well known for their customer retention policies along with

the campaigns that they develop in order to enhance their customer satisfaction.

NAB – It is an abbreviation for National Australian Bank. This can be considered as one of the

most well-known financial institution all over the country and is known for their customer

experience enhancement methodologies and their strong focus on their believes and values

associated with the customers.

Costing sheet for Fees and Charge

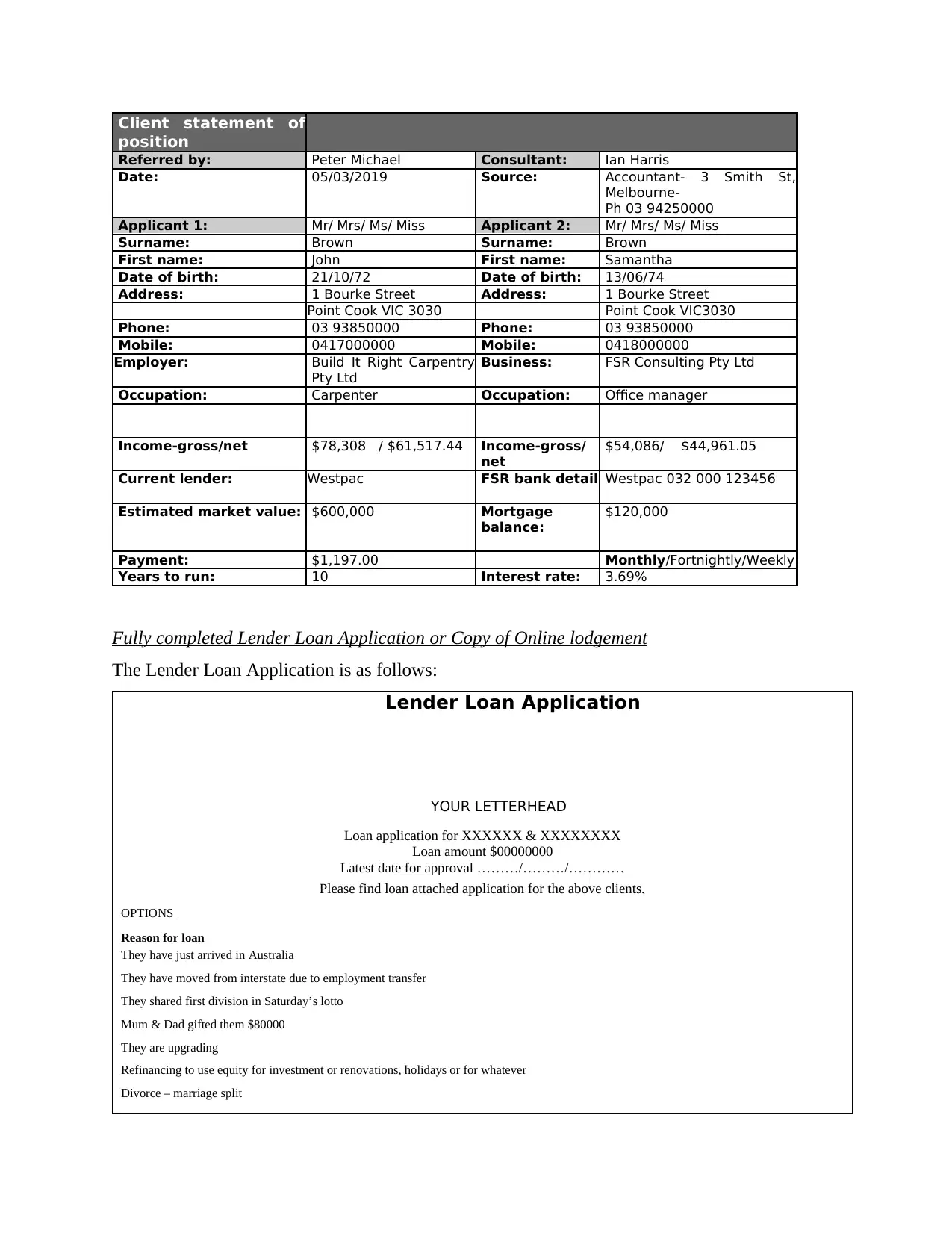

Client statement of

position

Referred by: Peter Michael Consultant: Ian Harris

Date: 05/03/2019 Source: Accountant- 3 Smith St,

Melbourne-

Ph 03 94250000

Applicant 1: Mr/ Mrs/ Ms/ Miss Applicant 2: Mr/ Mrs/ Ms/ Miss

Surname: Brown Surname: Brown

First name: John First name: Samantha

Date of birth: 21/10/72 Date of birth: 13/06/74

Address: 1 Bourke Street Address: 1 Bourke Street

Point Cook VIC 3030 Point Cook VIC3030

Phone: 03 93850000 Phone: 03 93850000

Mobile: 0417000000 Mobile: 0418000000

Employer: Build It Right Carpentry

Pty Ltd

Business: FSR Consulting Pty Ltd

Occupation: Carpenter Occupation: Office manager

Income-gross/net $78,308 / $61,517.44 Income-gross/

net

$54,086/ $44,961.05

Current lender: Westpac FSR bank detail Westpac 032 000 123456

Estimated market value: $600,000 Mortgage

balance:

$120,000

Payment: $1,197.00 Monthly/Fortnightly/Weekly

Years to run: 10 Interest rate: 3.69%

Fully completed Lender Loan Application or Copy of Online lodgement

The Lender Loan Application is as follows:

Lender Loan Application

YOUR LETTERHEAD

Loan application for XXXXXX & XXXXXXXX

Loan amount $00000000

Latest date for approval ………/………/…………

Please find loan attached application for the above clients.

OPTIONS

Reason for loan

They have just arrived in Australia

They have moved from interstate due to employment transfer

They shared first division in Saturday’s lotto

Mum & Dad gifted them $80000

They are upgrading

Refinancing to use equity for investment or renovations, holidays or for whatever

Divorce – marriage split

position

Referred by: Peter Michael Consultant: Ian Harris

Date: 05/03/2019 Source: Accountant- 3 Smith St,

Melbourne-

Ph 03 94250000

Applicant 1: Mr/ Mrs/ Ms/ Miss Applicant 2: Mr/ Mrs/ Ms/ Miss

Surname: Brown Surname: Brown

First name: John First name: Samantha

Date of birth: 21/10/72 Date of birth: 13/06/74

Address: 1 Bourke Street Address: 1 Bourke Street

Point Cook VIC 3030 Point Cook VIC3030

Phone: 03 93850000 Phone: 03 93850000

Mobile: 0417000000 Mobile: 0418000000

Employer: Build It Right Carpentry

Pty Ltd

Business: FSR Consulting Pty Ltd

Occupation: Carpenter Occupation: Office manager

Income-gross/net $78,308 / $61,517.44 Income-gross/

net

$54,086/ $44,961.05

Current lender: Westpac FSR bank detail Westpac 032 000 123456

Estimated market value: $600,000 Mortgage

balance:

$120,000

Payment: $1,197.00 Monthly/Fortnightly/Weekly

Years to run: 10 Interest rate: 3.69%

Fully completed Lender Loan Application or Copy of Online lodgement

The Lender Loan Application is as follows:

Lender Loan Application

YOUR LETTERHEAD

Loan application for XXXXXX & XXXXXXXX

Loan amount $00000000

Latest date for approval ………/………/…………

Please find loan attached application for the above clients.

OPTIONS

Reason for loan

They have just arrived in Australia

They have moved from interstate due to employment transfer

They shared first division in Saturday’s lotto

Mum & Dad gifted them $80000

They are upgrading

Refinancing to use equity for investment or renovations, holidays or for whatever

Divorce – marriage split

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Downgrading- kids left home

Employment

Just received promotion

Changed jobs for more income and permanency

Stable employment

Interstate transfer

Income

Single income is supported by Serviceability Assessment

Joint

Permanent staff for long period and expecting promotion.

RECOMMENDATION

We recommend this application in view of the following:

Stable employment

Stable address

Sound financial position

Sound income

Nothing adverse known

Security is in new expanding area

We recommend this application in view of the following:

SIGNED…………………………………………………………… Date…………/…………/………………

Lender’s loan Document Check List

Documents Availability

Two years personal tax returns. Yes

Two years personal tax assessment notices. Yes

Two years company/partnership/trust tax

returns.

Yes

Two years financial statements (if available). Yes

Employment

Just received promotion

Changed jobs for more income and permanency

Stable employment

Interstate transfer

Income

Single income is supported by Serviceability Assessment

Joint

Permanent staff for long period and expecting promotion.

RECOMMENDATION

We recommend this application in view of the following:

Stable employment

Stable address

Sound financial position

Sound income

Nothing adverse known

Security is in new expanding area

We recommend this application in view of the following:

SIGNED…………………………………………………………… Date…………/…………/………………

Lender’s loan Document Check List

Documents Availability

Two years personal tax returns. Yes

Two years personal tax assessment notices. Yes

Two years company/partnership/trust tax

returns.

Yes

Two years financial statements (if available). Yes

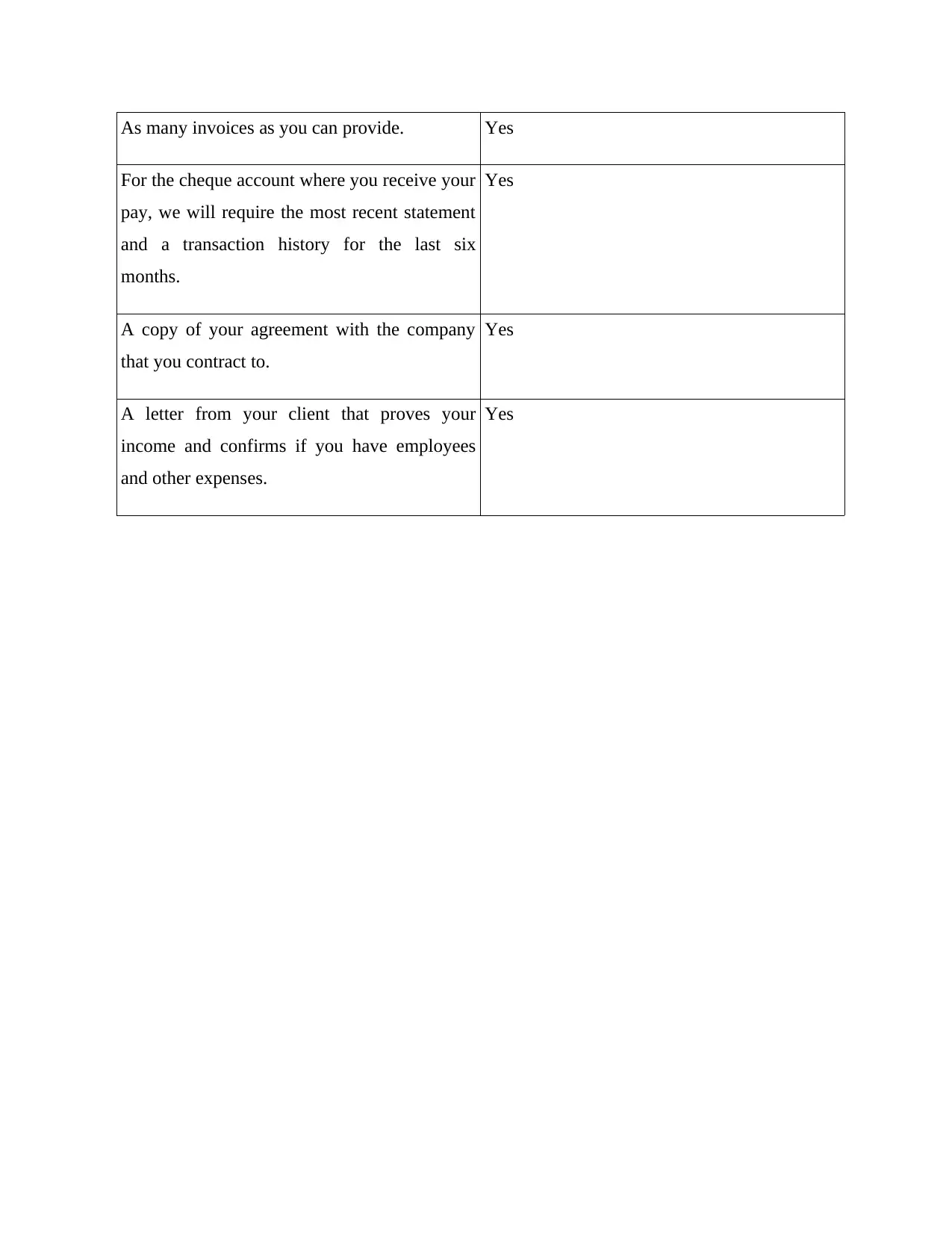

As many invoices as you can provide. Yes

For the cheque account where you receive your

pay, we will require the most recent statement

and a transaction history for the last six

months.

Yes

A copy of your agreement with the company

that you contract to.

Yes

A letter from your client that proves your

income and confirms if you have employees

and other expenses.

Yes

For the cheque account where you receive your

pay, we will require the most recent statement

and a transaction history for the last six

months.

Yes

A copy of your agreement with the company

that you contract to.

Yes

A letter from your client that proves your

income and confirms if you have employees

and other expenses.

Yes

Task 2: Process application for credit.

Loan Comments/Lender Comments

This part covers the information about the loan comments from the manager as the

documents needed for the loan application is complete and applicant is eligible for taking the

loan. The procedure of the loan includes several documents such as the bank statement or income

statement and the information regarding the nationality of the applicant to make sure that

applicant belongs to the Australia and applicant is the citizen of Australia (Chuang et al 2018).

In order to complete the loan procedure these documents in particular is needed first of all the

document which is needed to apply for the housing loan is the amount of loan which is required

by the applicant after that applicant have to mention its income and provide its annual income

statement to the bank which helps bank to determine that applicant is capable or not to repay the

loan. Next document which is important to complete the procedure is the identity of the applicant

in order to make sure that the applicant belongs from Australia and not committing any type of

fraud with the bank. There are documents required by the bank for the current property of

applicant and the proof of residence is also mandatory for the applicant to submit to the bank.

The other documents which is needed by the bank is the proof of age and the photographs of the

applicant in order to prepare the application (Ebekozien et al 2018). At last the employee of the

member checks all the mandatory documents and it's authenticity and after cross checking all the

documents loan is sanctioned to the applicant and provided to the applicant in the instalments.

Evidence of Income

The applicant's pay slip is as follows:

FSR Consulting PVT Ltd

PAYSLIP

ABN: 11 123 456 789

ACN: 123 456 789

1 King Street, Melbourne VIC 3000

Employee ID: 5245 Bookkeeper

Loan Comments/Lender Comments

This part covers the information about the loan comments from the manager as the

documents needed for the loan application is complete and applicant is eligible for taking the

loan. The procedure of the loan includes several documents such as the bank statement or income

statement and the information regarding the nationality of the applicant to make sure that

applicant belongs to the Australia and applicant is the citizen of Australia (Chuang et al 2018).

In order to complete the loan procedure these documents in particular is needed first of all the

document which is needed to apply for the housing loan is the amount of loan which is required

by the applicant after that applicant have to mention its income and provide its annual income

statement to the bank which helps bank to determine that applicant is capable or not to repay the

loan. Next document which is important to complete the procedure is the identity of the applicant

in order to make sure that the applicant belongs from Australia and not committing any type of

fraud with the bank. There are documents required by the bank for the current property of

applicant and the proof of residence is also mandatory for the applicant to submit to the bank.

The other documents which is needed by the bank is the proof of age and the photographs of the

applicant in order to prepare the application (Ebekozien et al 2018). At last the employee of the

member checks all the mandatory documents and it's authenticity and after cross checking all the

documents loan is sanctioned to the applicant and provided to the applicant in the instalments.

Evidence of Income

The applicant's pay slip is as follows:

FSR Consulting PVT Ltd

PAYSLIP

ABN: 11 123 456 789

ACN: 123 456 789

1 King Street, Melbourne VIC 3000

Employee ID: 5245 Bookkeeper

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

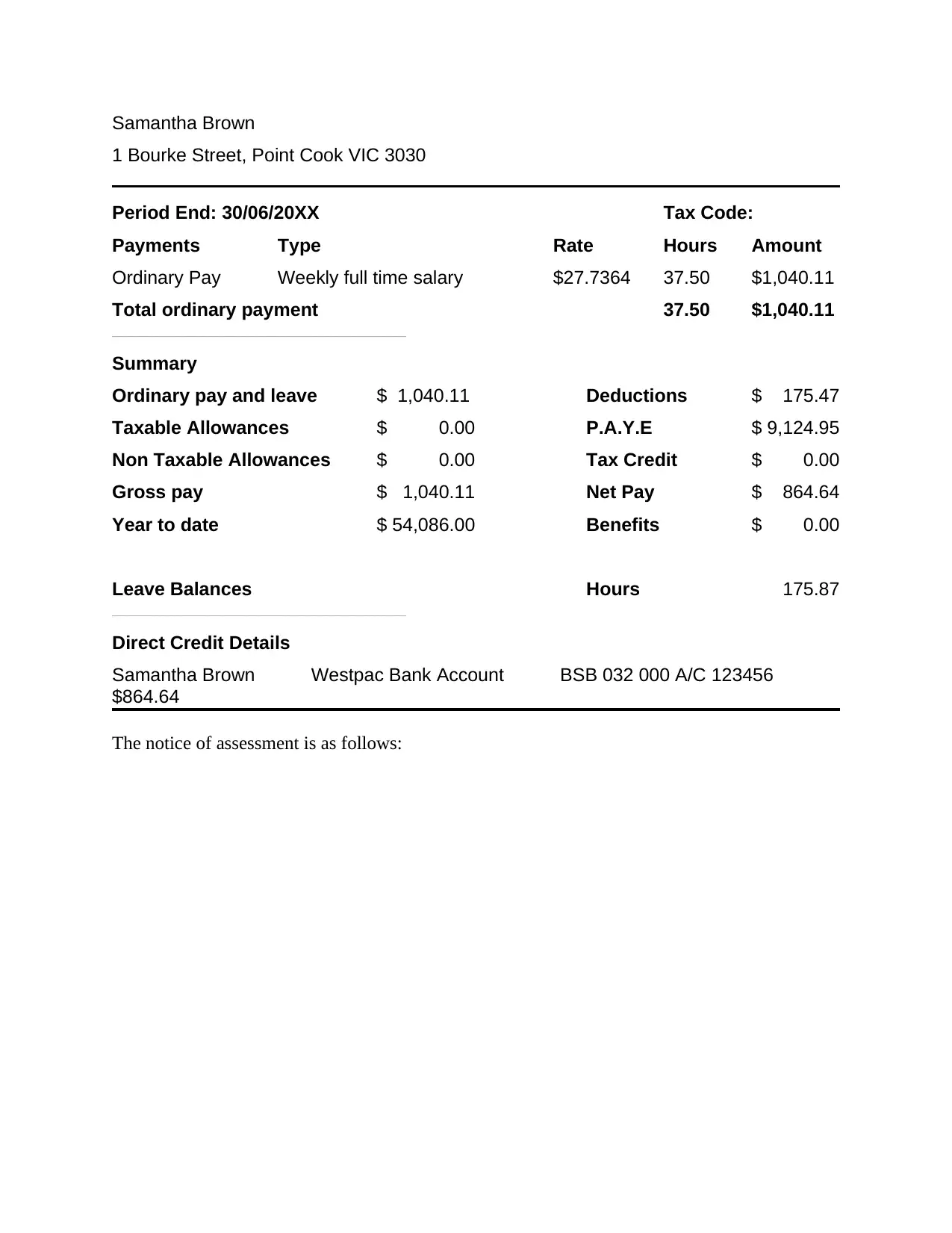

Samantha Brown

1 Bourke Street, Point Cook VIC 3030

Period End: 30/06/20XX Tax Code:

Payments Type Rate Hours Amount

Ordinary Pay Weekly full time salary $27.7364 37.50 $1,040.11

Total ordinary payment 37.50 $1,040.11

_____________________________________________________________________________________

Summary

Ordinary pay and leave $ 1,040.11 Deductions $ 175.47

Taxable Allowances $ 0.00 P.A.Y.E $ 9,124.95

Non Taxable Allowances $ 0.00 Tax Credit $ 0.00

Gross pay $ 1,040.11 Net Pay $ 864.64

Year to date $ 54,086.00 Benefits $ 0.00

Leave Balances Hours 175.87

_____________________________________________________________________________________

Direct Credit Details

Samantha Brown Westpac Bank Account BSB 032 000 A/C 123456

$864.64

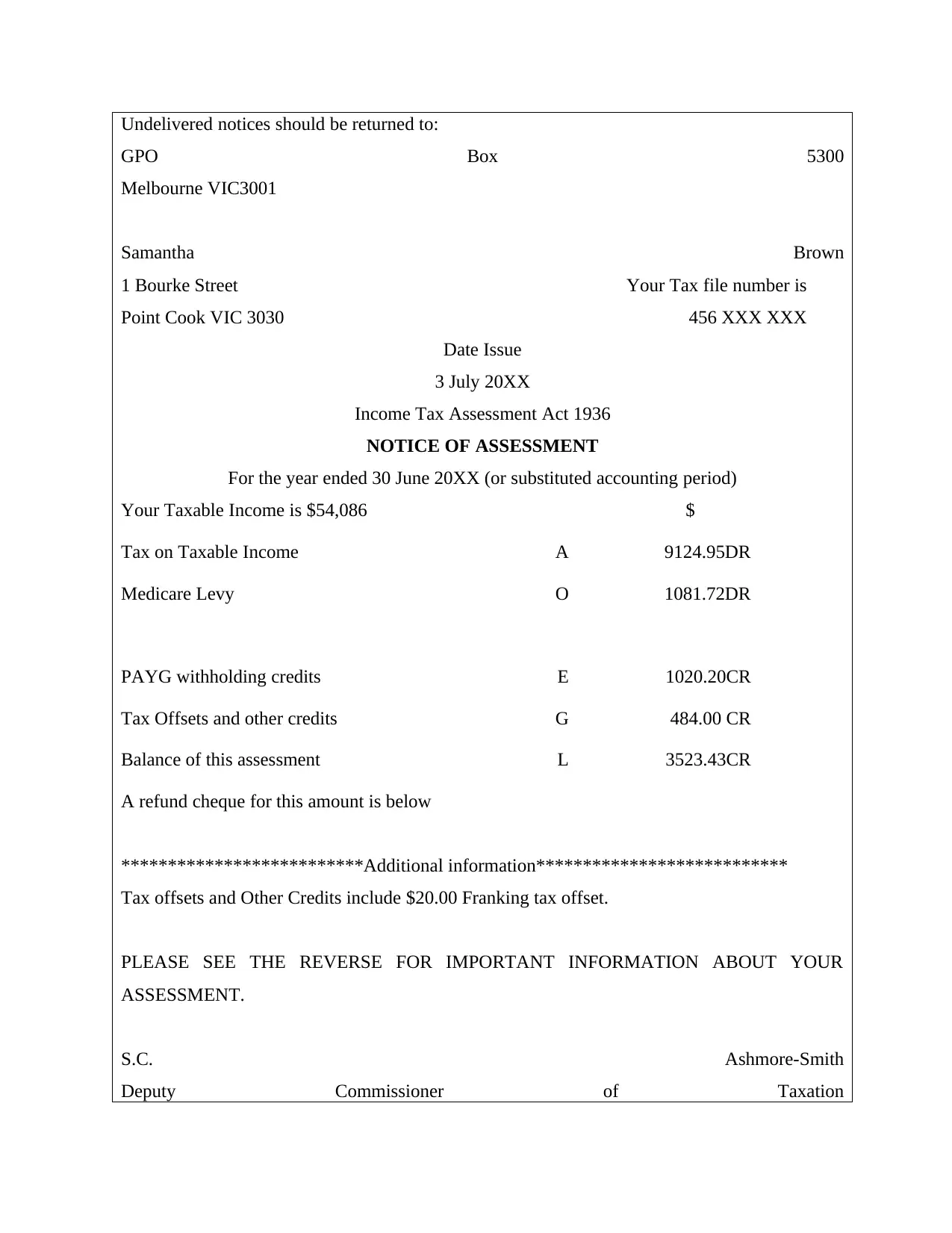

The notice of assessment is as follows:

1 Bourke Street, Point Cook VIC 3030

Period End: 30/06/20XX Tax Code:

Payments Type Rate Hours Amount

Ordinary Pay Weekly full time salary $27.7364 37.50 $1,040.11

Total ordinary payment 37.50 $1,040.11

_____________________________________________________________________________________

Summary

Ordinary pay and leave $ 1,040.11 Deductions $ 175.47

Taxable Allowances $ 0.00 P.A.Y.E $ 9,124.95

Non Taxable Allowances $ 0.00 Tax Credit $ 0.00

Gross pay $ 1,040.11 Net Pay $ 864.64

Year to date $ 54,086.00 Benefits $ 0.00

Leave Balances Hours 175.87

_____________________________________________________________________________________

Direct Credit Details

Samantha Brown Westpac Bank Account BSB 032 000 A/C 123456

$864.64

The notice of assessment is as follows:

Undelivered notices should be returned to:

GPO Box 5300

Melbourne VIC3001

Samantha Brown

1 Bourke Street Your Tax file number is

Point Cook VIC 3030 456 XXX XXX

Date Issue

3 July 20XX

Income Tax Assessment Act 1936

NOTICE OF ASSESSMENT

For the year ended 30 June 20XX (or substituted accounting period)

Your Taxable Income is $54,086 $

Tax on Taxable Income A 9124.95DR

Medicare Levy O 1081.72DR

PAYG withholding credits E 1020.20CR

Tax Offsets and other credits G 484.00 CR

Balance of this assessment L 3523.43CR

A refund cheque for this amount is below

**************************Additional information***************************

Tax offsets and Other Credits include $20.00 Franking tax offset.

PLEASE SEE THE REVERSE FOR IMPORTANT INFORMATION ABOUT YOUR

ASSESSMENT.

S.C. Ashmore-Smith

Deputy Commissioner of Taxation

GPO Box 5300

Melbourne VIC3001

Samantha Brown

1 Bourke Street Your Tax file number is

Point Cook VIC 3030 456 XXX XXX

Date Issue

3 July 20XX

Income Tax Assessment Act 1936

NOTICE OF ASSESSMENT

For the year ended 30 June 20XX (or substituted accounting period)

Your Taxable Income is $54,086 $

Tax on Taxable Income A 9124.95DR

Medicare Levy O 1081.72DR

PAYG withholding credits E 1020.20CR

Tax Offsets and other credits G 484.00 CR

Balance of this assessment L 3523.43CR

A refund cheque for this amount is below

**************************Additional information***************************

Tax offsets and Other Credits include $20.00 Franking tax offset.

PLEASE SEE THE REVERSE FOR IMPORTANT INFORMATION ABOUT YOUR

ASSESSMENT.

S.C. Ashmore-Smith

Deputy Commissioner of Taxation

Sydney Office, Sydney NSW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Evidence of Council approved plans

Burrows Holden

ACN: 009 071 444

ABN: 47 009 071 444

To:

John and Samantha Brown

F

o

r

d

e

l

i

v

e

r

y

t

o

:

J

o

h

n

a

n

d

S

a

m

a

n

t

h

a

B

r

o

w

n

INVOICE DATE INVOICE/STOCK NO NEW/USED VEHICLE MAKE

17/10/20XX 1425361 NEW HOLDEN

ENGINE NUMBER CHASSIS NUMBER COMPLIANCE DATE COLOUR

QR25230948 JNITBNT30A0044491 20XX TWILIGHT

ACN: 009 071 444

ABN: 47 009 071 444

To:

John and Samantha Brown

F

o

r

d

e

l

i

v

e

r

y

t

o

:

J

o

h

n

a

n

d

S

a

m

a

n

t

h

a

B

r

o

w

n

INVOICE DATE INVOICE/STOCK NO NEW/USED VEHICLE MAKE

17/10/20XX 1425361 NEW HOLDEN

ENGINE NUMBER CHASSIS NUMBER COMPLIANCE DATE COLOUR

QR25230948 JNITBNT30A0044491 20XX TWILIGHT

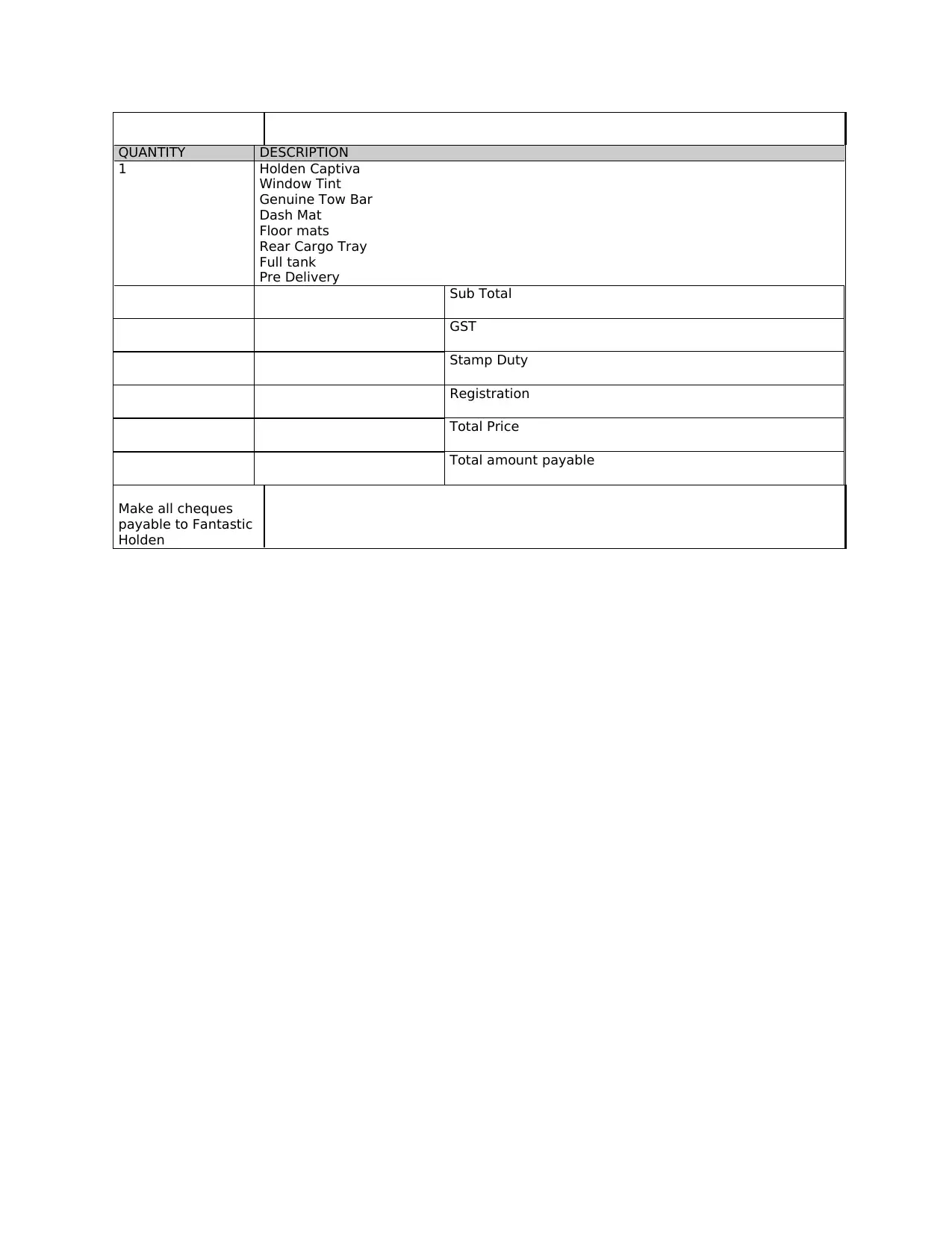

QUANTITY DESCRIPTION

1 Holden Captiva

Window Tint

Genuine Tow Bar

Dash Mat

Floor mats

Rear Cargo Tray

Full tank

Pre Delivery

Sub Total

GST

Stamp Duty

Registration

Total Price

Total amount payable

Make all cheques

payable to Fantastic

Holden

1 Holden Captiva

Window Tint

Genuine Tow Bar

Dash Mat

Floor mats

Rear Cargo Tray

Full tank

Pre Delivery

Sub Total

GST

Stamp Duty

Registration

Total Price

Total amount payable

Make all cheques

payable to Fantastic

Holden

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

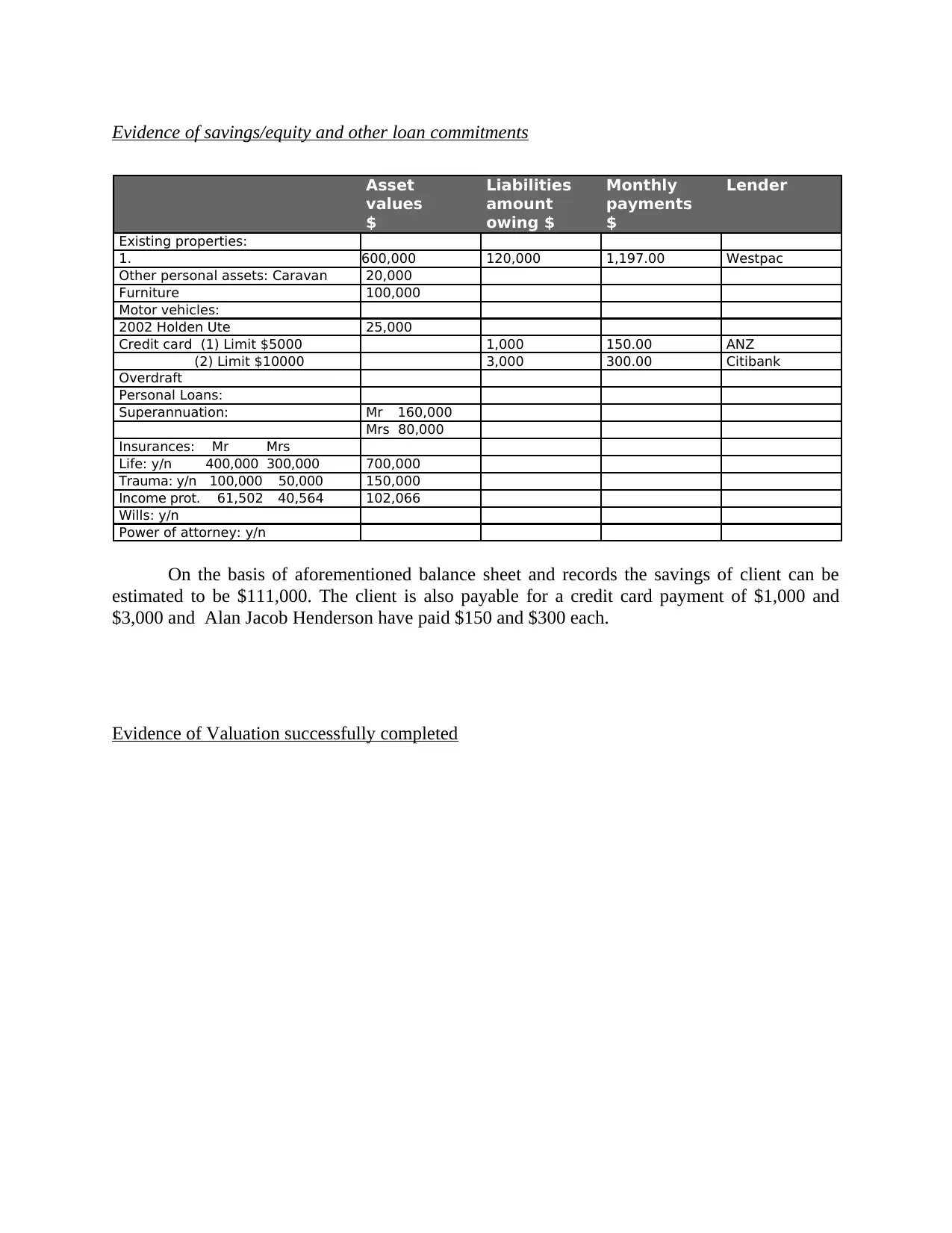

Evidence of savings/equity and other loan commitments

Asset

values

$

Liabilities

amount

owing $

Monthly

payments

$

Lender

Existing properties:

1. 600,000 120,000 1,197.00 Westpac

Other personal assets: Caravan 20,000

Furniture 100,000

Motor vehicles:

2002 Holden Ute 25,000

Credit card (1) Limit $5000 1,000 150.00 ANZ

(2) Limit $10000 3,000 300.00 Citibank

Overdraft

Personal Loans:

Superannuation: Mr 160,000

Mrs 80,000

Insurances: Mr Mrs

Life: y/n 400,000 300,000 700,000

Trauma: y/n 100,000 50,000 150,000

Income prot. 61,502 40,564 102,066

Wills: y/n

Power of attorney: y/n

On the basis of aforementioned balance sheet and records the savings of client can be

estimated to be $111,000. The client is also payable for a credit card payment of $1,000 and

$3,000 and Alan Jacob Henderson have paid $150 and $300 each.

Evidence of Valuation successfully completed

Asset

values

$

Liabilities

amount

owing $

Monthly

payments

$

Lender

Existing properties:

1. 600,000 120,000 1,197.00 Westpac

Other personal assets: Caravan 20,000

Furniture 100,000

Motor vehicles:

2002 Holden Ute 25,000

Credit card (1) Limit $5000 1,000 150.00 ANZ

(2) Limit $10000 3,000 300.00 Citibank

Overdraft

Personal Loans:

Superannuation: Mr 160,000

Mrs 80,000

Insurances: Mr Mrs

Life: y/n 400,000 300,000 700,000

Trauma: y/n 100,000 50,000 150,000

Income prot. 61,502 40,564 102,066

Wills: y/n

Power of attorney: y/n

On the basis of aforementioned balance sheet and records the savings of client can be

estimated to be $111,000. The client is also payable for a credit card payment of $1,000 and

$3,000 and Alan Jacob Henderson have paid $150 and $300 each.

Evidence of Valuation successfully completed

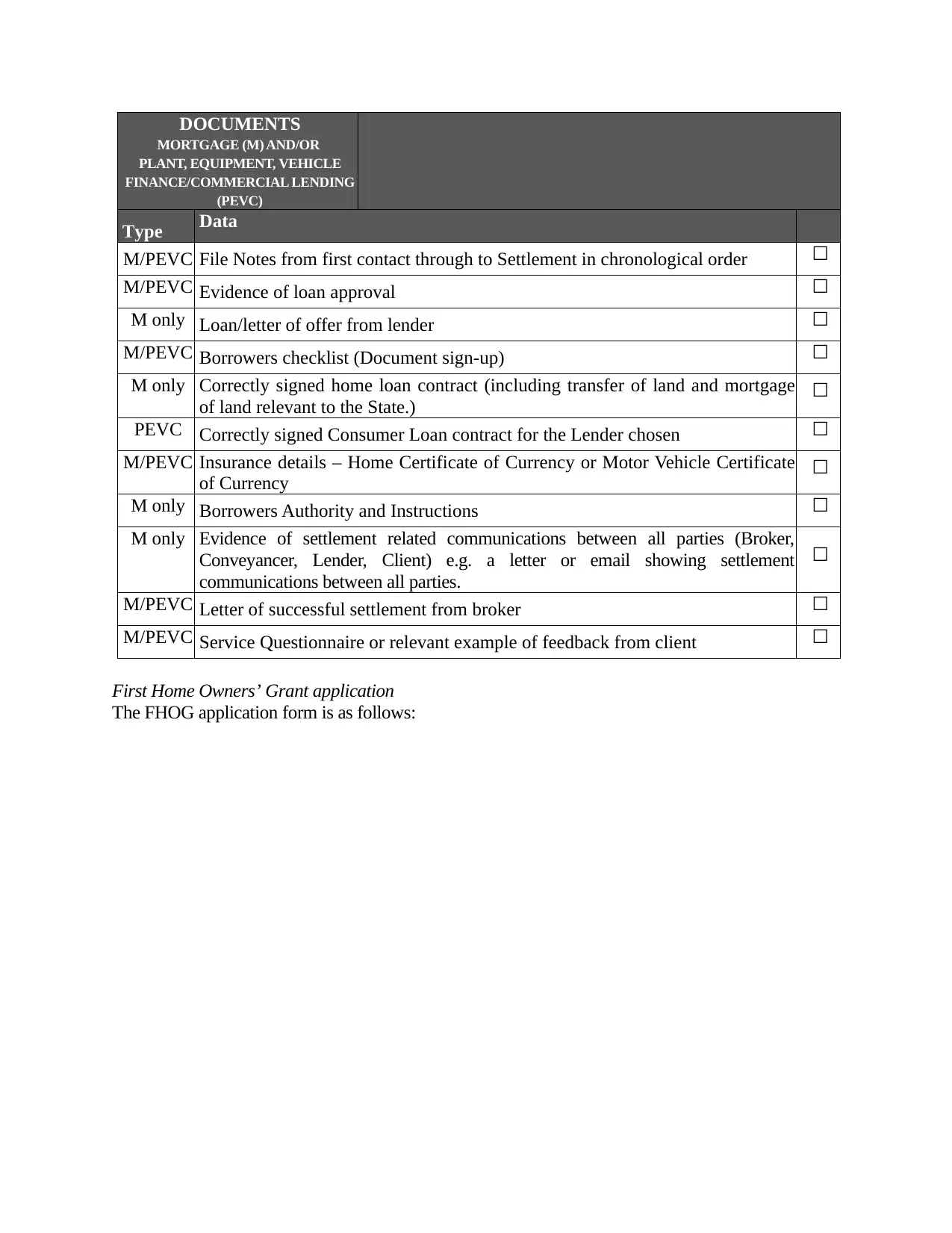

DOCUMENTS

MORTGAGE (M) AND/OR

PLANT, EQUIPMENT, VEHICLE

FINANCE/COMMERCIAL LENDING

(PEVC)

Type Data

M/PEVC File Notes from first contact through to Settlement in chronological order ☐

M/PEVC Evidence of loan approval ☐

M only Loan/letter of offer from lender ☐

M/PEVC Borrowers checklist (Document sign-up) ☐

M only Correctly signed home loan contract (including transfer of land and mortgage

of land relevant to the State.) ☐

PEVC Correctly signed Consumer Loan contract for the Lender chosen ☐

M/PEVC Insurance details – Home Certificate of Currency or Motor Vehicle Certificate

of Currency ☐

M only Borrowers Authority and Instructions ☐

M only Evidence of settlement related communications between all parties (Broker,

Conveyancer, Lender, Client) e.g. a letter or email showing settlement

communications between all parties.

☐

M/PEVC Letter of successful settlement from broker ☐

M/PEVC Service Questionnaire or relevant example of feedback from client ☐

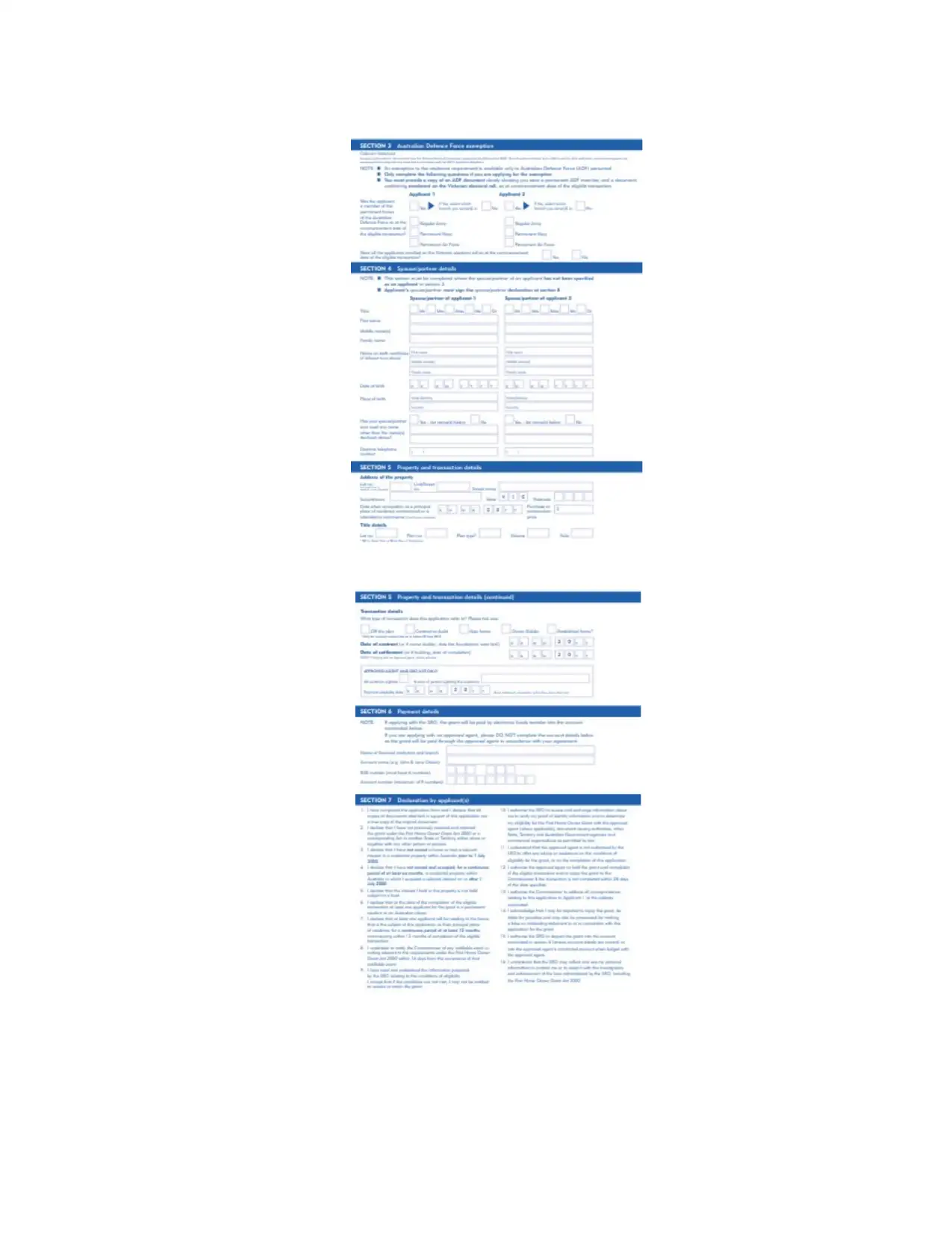

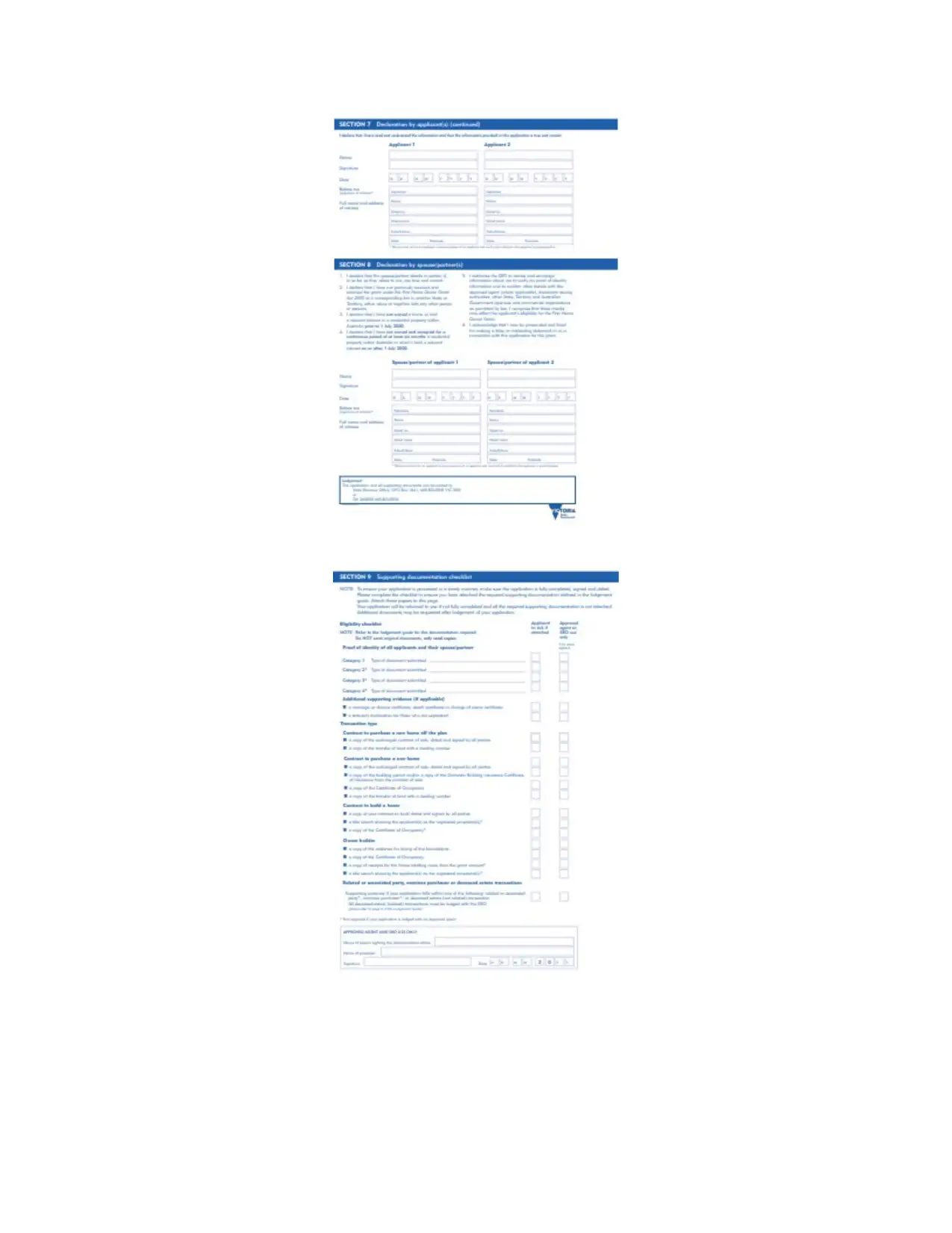

First Home Owners’ Grant application

The FHOG application form is as follows:

MORTGAGE (M) AND/OR

PLANT, EQUIPMENT, VEHICLE

FINANCE/COMMERCIAL LENDING

(PEVC)

Type Data

M/PEVC File Notes from first contact through to Settlement in chronological order ☐

M/PEVC Evidence of loan approval ☐

M only Loan/letter of offer from lender ☐

M/PEVC Borrowers checklist (Document sign-up) ☐

M only Correctly signed home loan contract (including transfer of land and mortgage

of land relevant to the State.) ☐

PEVC Correctly signed Consumer Loan contract for the Lender chosen ☐

M/PEVC Insurance details – Home Certificate of Currency or Motor Vehicle Certificate

of Currency ☐

M only Borrowers Authority and Instructions ☐

M only Evidence of settlement related communications between all parties (Broker,

Conveyancer, Lender, Client) e.g. a letter or email showing settlement

communications between all parties.

☐

M/PEVC Letter of successful settlement from broker ☐

M/PEVC Service Questionnaire or relevant example of feedback from client ☐

First Home Owners’ Grant application

The FHOG application form is as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

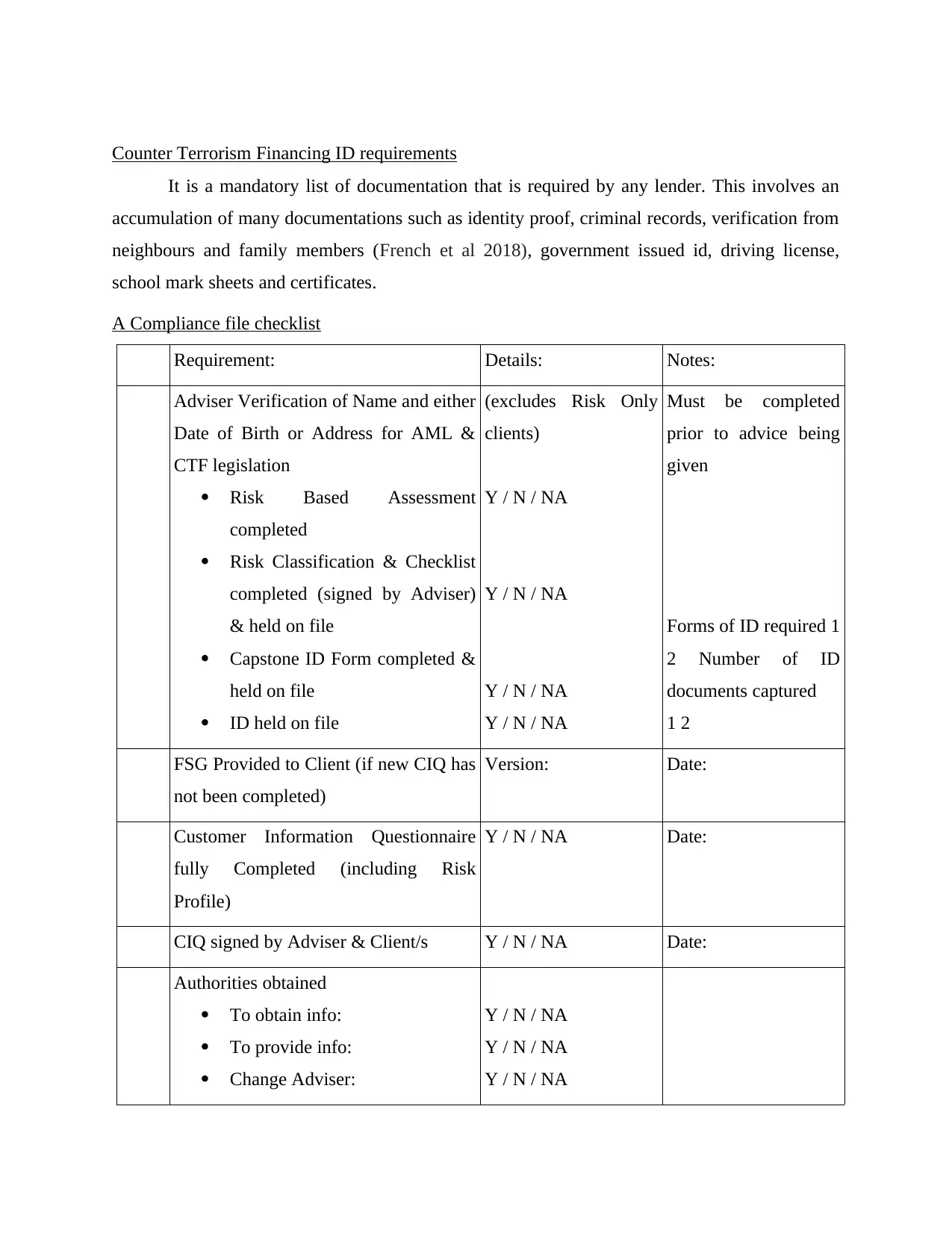

Counter Terrorism Financing ID requirements

It is a mandatory list of documentation that is required by any lender. This involves an

accumulation of many documentations such as identity proof, criminal records, verification from

neighbours and family members (French et al 2018), government issued id, driving license,

school mark sheets and certificates.

A Compliance file checklist

Requirement: Details: Notes:

Adviser Verification of Name and either

Date of Birth or Address for AML &

CTF legislation

Risk Based Assessment

completed

Risk Classification & Checklist

completed (signed by Adviser)

& held on file

Capstone ID Form completed &

held on file

ID held on file

(excludes Risk Only

clients)

Y / N / NA

Y / N / NA

Y / N / NA

Y / N / NA

Must be completed

prior to advice being

given

Forms of ID required 1

2 Number of ID

documents captured

1 2

FSG Provided to Client (if new CIQ has

not been completed)

Version: Date:

Customer Information Questionnaire

fully Completed (including Risk

Profile)

Y / N / NA Date:

CIQ signed by Adviser & Client/s Y / N / NA Date:

Authorities obtained

To obtain info:

To provide info:

Change Adviser:

Y / N / NA

Y / N / NA

Y / N / NA

It is a mandatory list of documentation that is required by any lender. This involves an

accumulation of many documentations such as identity proof, criminal records, verification from

neighbours and family members (French et al 2018), government issued id, driving license,

school mark sheets and certificates.

A Compliance file checklist

Requirement: Details: Notes:

Adviser Verification of Name and either

Date of Birth or Address for AML &

CTF legislation

Risk Based Assessment

completed

Risk Classification & Checklist

completed (signed by Adviser)

& held on file

Capstone ID Form completed &

held on file

ID held on file

(excludes Risk Only

clients)

Y / N / NA

Y / N / NA

Y / N / NA

Y / N / NA

Must be completed

prior to advice being

given

Forms of ID required 1

2 Number of ID

documents captured

1 2

FSG Provided to Client (if new CIQ has

not been completed)

Version: Date:

Customer Information Questionnaire

fully Completed (including Risk

Profile)

Y / N / NA Date:

CIQ signed by Adviser & Client/s Y / N / NA Date:

Authorities obtained

To obtain info:

To provide info:

Change Adviser:

Y / N / NA

Y / N / NA

Y / N / NA

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

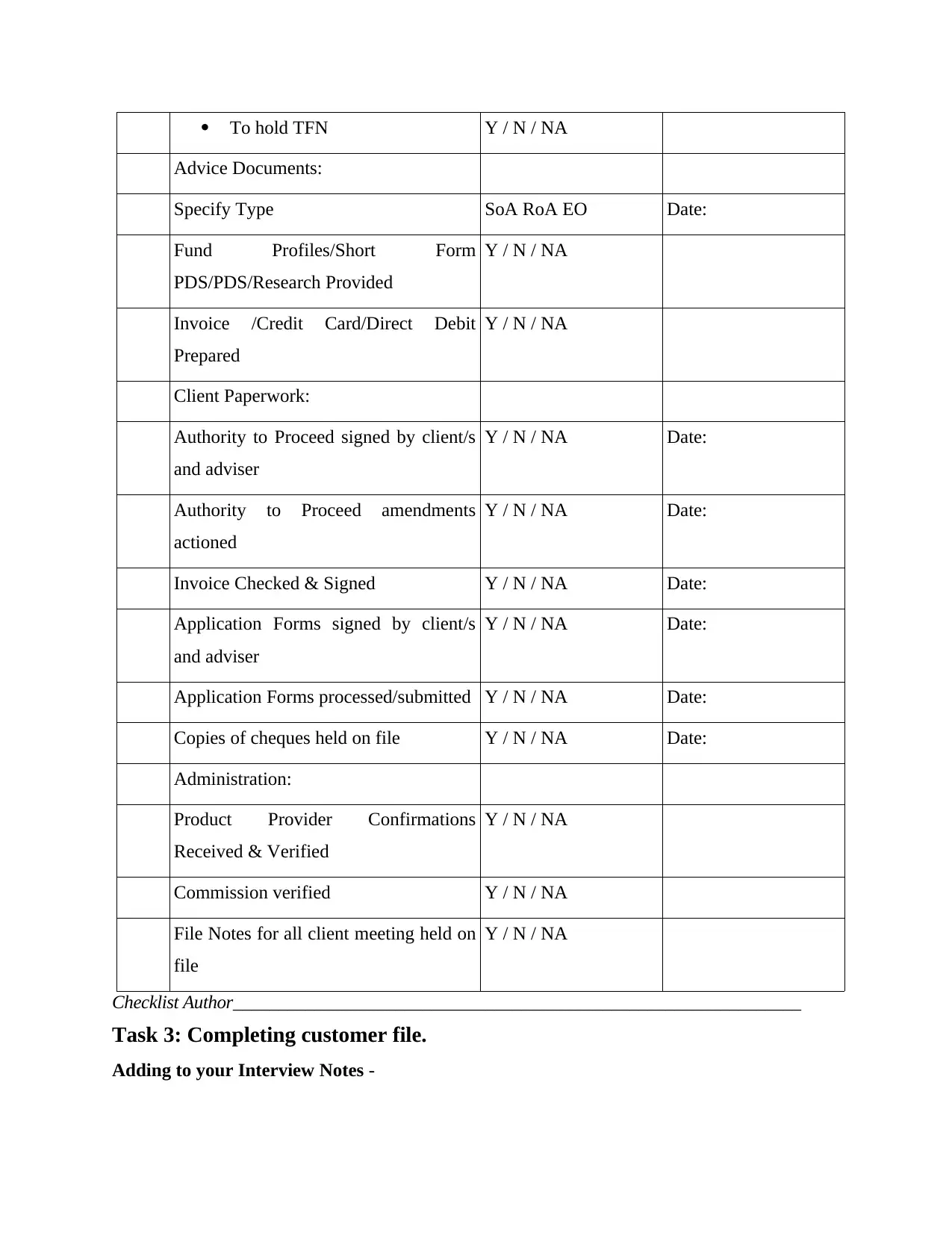

To hold TFN Y / N / NA

Advice Documents:

Specify Type SoA RoA EO Date:

Fund Profiles/Short Form

PDS/PDS/Research Provided

Y / N / NA

Invoice /Credit Card/Direct Debit

Prepared

Y / N / NA

Client Paperwork:

Authority to Proceed signed by client/s

and adviser

Y / N / NA Date:

Authority to Proceed amendments

actioned

Y / N / NA Date:

Invoice Checked & Signed Y / N / NA Date:

Application Forms signed by client/s

and adviser

Y / N / NA Date:

Application Forms processed/submitted Y / N / NA Date:

Copies of cheques held on file Y / N / NA Date:

Administration:

Product Provider Confirmations

Received & Verified

Y / N / NA

Commission verified Y / N / NA

File Notes for all client meeting held on

file

Y / N / NA

Checklist Author_______________________________________________________________

Task 3: Completing customer file.

Adding to your Interview Notes -

Advice Documents:

Specify Type SoA RoA EO Date:

Fund Profiles/Short Form

PDS/PDS/Research Provided

Y / N / NA

Invoice /Credit Card/Direct Debit

Prepared

Y / N / NA

Client Paperwork:

Authority to Proceed signed by client/s

and adviser

Y / N / NA Date:

Authority to Proceed amendments

actioned

Y / N / NA Date:

Invoice Checked & Signed Y / N / NA Date:

Application Forms signed by client/s

and adviser

Y / N / NA Date:

Application Forms processed/submitted Y / N / NA Date:

Copies of cheques held on file Y / N / NA Date:

Administration:

Product Provider Confirmations

Received & Verified

Y / N / NA

Commission verified Y / N / NA

File Notes for all client meeting held on

file

Y / N / NA

Checklist Author_______________________________________________________________

Task 3: Completing customer file.

Adding to your Interview Notes -

Customer – The interaction with customers concluded that the prices in UK housing

market are way too high and the loan acquisition criteria is very complex (Miu et al 2018). The

interview also suggested let the bank set associated with giving out the loans have the eligibility

criteria which is very hard to achieve. When it comes to the referrers in order for them to the

person that they are referring should be e granted the loan and since the eligibility criteria is so

hard to achieve loan acquisition becomes difficult. Concerned authorities which include

government bodies and stamp duties are doing their best to subdue the housing crisis in Australia

in order to do so FHOG was founded. The property

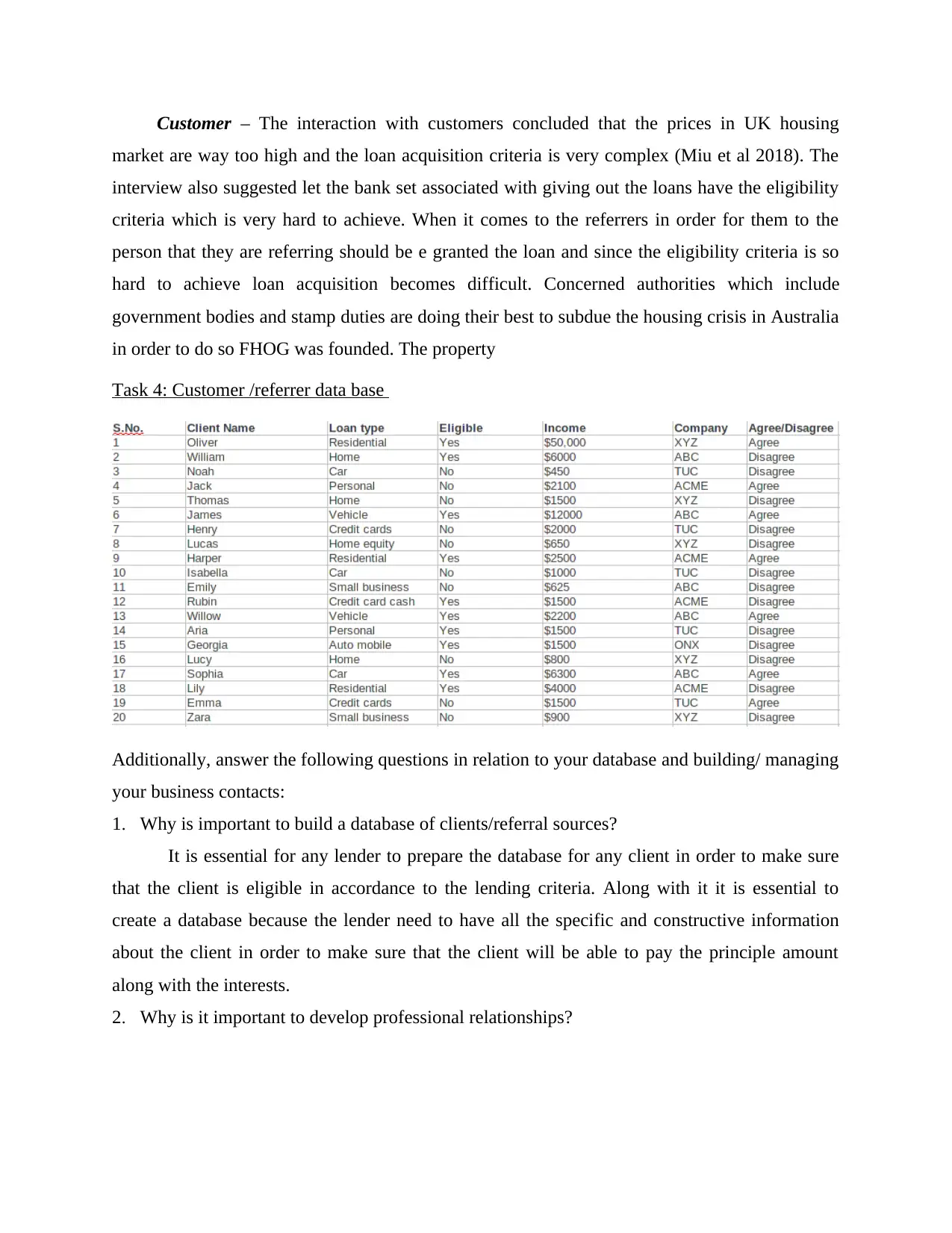

Task 4: Customer /referrer data base

Additionally, answer the following questions in relation to your database and building/ managing

your business contacts:

1. Why is important to build a database of clients/referral sources?

It is essential for any lender to prepare the database for any client in order to make sure

that the client is eligible in accordance to the lending criteria. Along with it it is essential to

create a database because the lender need to have all the specific and constructive information

about the client in order to make sure that the client will be able to pay the principle amount

along with the interests.

2. Why is it important to develop professional relationships?

market are way too high and the loan acquisition criteria is very complex (Miu et al 2018). The

interview also suggested let the bank set associated with giving out the loans have the eligibility

criteria which is very hard to achieve. When it comes to the referrers in order for them to the

person that they are referring should be e granted the loan and since the eligibility criteria is so

hard to achieve loan acquisition becomes difficult. Concerned authorities which include

government bodies and stamp duties are doing their best to subdue the housing crisis in Australia

in order to do so FHOG was founded. The property

Task 4: Customer /referrer data base

Additionally, answer the following questions in relation to your database and building/ managing

your business contacts:

1. Why is important to build a database of clients/referral sources?

It is essential for any lender to prepare the database for any client in order to make sure

that the client is eligible in accordance to the lending criteria. Along with it it is essential to

create a database because the lender need to have all the specific and constructive information

about the client in order to make sure that the client will be able to pay the principle amount

along with the interests.

2. Why is it important to develop professional relationships?

It is essential to build professional relationships because these all things accumulate

together when it comes to future opportunities. It is impossible for anyone to acquire loans in

absence of this.

3. When is it not appropriate to contact a person and why?

It is not appropriate to contact any person when the contact is not based on that particular

person's consent.

4. Why is it important to have effective interpersonal styles and methods when dealing with

clients/referrers? Why is it important to consider special needs, culture, race, religion, origin,

demographics?

It is essential to have these skills in order to enhance the overall experience of the

associated customer.

5. Explain why you think it would be important to follow up any business referrers as quickly

as possible.

It is essential to do so in order to take full benefits of the offer.

6. What methods could you use in developing new business i.e.; advertising and promotion of

your services?

In today's world where everything is based on mobiles and computers. Digital landscape

and the operations associated with are the best approaches for business development.

CONCLUSION

From the above report it is conclude that there are various documentation that are

required during the time when the individual is taking house loan. The loan will only get

sanctioned if the individual is maintaining good credit score. The bank while lending the loan to

the individual will also look for the present bank statement and various different things.

together when it comes to future opportunities. It is impossible for anyone to acquire loans in

absence of this.

3. When is it not appropriate to contact a person and why?

It is not appropriate to contact any person when the contact is not based on that particular

person's consent.

4. Why is it important to have effective interpersonal styles and methods when dealing with

clients/referrers? Why is it important to consider special needs, culture, race, religion, origin,

demographics?

It is essential to have these skills in order to enhance the overall experience of the

associated customer.

5. Explain why you think it would be important to follow up any business referrers as quickly

as possible.

It is essential to do so in order to take full benefits of the offer.

6. What methods could you use in developing new business i.e.; advertising and promotion of

your services?

In today's world where everything is based on mobiles and computers. Digital landscape

and the operations associated with are the best approaches for business development.

CONCLUSION

From the above report it is conclude that there are various documentation that are

required during the time when the individual is taking house loan. The loan will only get

sanctioned if the individual is maintaining good credit score. The bank while lending the loan to

the individual will also look for the present bank statement and various different things.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Chuang, M.C., Yang, W.R., Chen, M.C. and Lin, S.K., 2018. Pricing mortgage insurance

contracts under housing price cycles with jump risk: evidence from the UK housing

market. The European Journal of Finance. 24(11), pp.909-943.

Byrne, M., 2020. Generation rent and the financialization of housing: A comparative exploration

of the growth of the private rental sector in Ireland, the UK and Spain. Housing

studies, 35(4), pp.743-765.

French, D., McKillop, D. and Sharma, T., 2018. What determines UK housing equity withdrawal

in later life?. Regional Science and Urban Economics, 73, pp.143-154.

Miu, L.M., Wisniewska, N., Mazur, C., Hardy, J. and Hawkes, A., 2018. A simple assessment of

housing retrofit policies for the UK: what should succeed the energy company

obligation?. Energies, 11(8), p.2070.

Ebekozien, A., Abdul-Aziz, A.R. and Jaafar, M., 2019. Remedies to inaccessibility of low-cost

housing loan in Malaysia: using the qualitative approach. Pacific Rim Property Research

Journal, 25(2), pp.159-174.

Bright, S., Weatherall, D. and Willis, R., 2019. Exploring the complexities of energy retrofit in

mixed tenure social housing: a case study from England, UK. Energy Efficiency, 12(1),

pp.157-174.

Burrows, V., 2018. The impact of house prices on consumption in the uk: A new

perspective. Economica, 85(337), pp.92-123.

Udoka, C.O. and Kpataene, M., 2017. Mortgage financing and housing development in

Nigeria. International Journal of Research-Granthaalayah, 5(5), pp.182-206.

Sanderson, D.C., Shakurina, F. and Lim, J., 2019. The impact of sale and leaseback on

commercial real estate prices and initial yields in the UK. Journal of Property

Research, 36(3), pp.245-271.

Roos, C., 2019. The (de-) politicization of EU freedom of movement: political parties,

opportunities, and policy framing in Germany and the UK. Comparative

European Politics, 17(5), pp.631-650.

Cowell, F., Karagiannaki, E. and McKnight, A., 2019. The changing distribution of wealth in the

pre-crisis US and UK: the role of socio-economic factors. Oxford Economic

Papers, 71(1), pp.1-24.

Ebekozien, A., Abdul-Aziz, A.R. and Jaafar, M., 2019. THE ROLE OF FEDERALISM IN

MALAYSIAN LOW-COST HOUSING PROVISION: THE UNEXPLORED

DIMENSION. Kajian Malaysia: Journal of Malaysian Studies, 37(1).

Arundel, R. and Hochstenbach, C., 2020. Divided access and the spatial polarization of housing

wealth. Urban Geography, 41(4), pp.497-523.

Murie, A., 2018. Shrinking the state in housing: challenges, transitions and

ambiguities. Cambridge Journal of Regions, Economy and Society, 11(3), pp.485-

501.

Farrar, S., Moizer, J., Lean, J. and Hyde, M., 2019. Gender, financial literacy, and preretirement

planning in the UK. Journal of Women & Aging, 31(4), pp.319-339.

Chuang, M.C., Yang, W.R., Chen, M.C. and Lin, S.K., 2018. Pricing mortgage insurance

contracts under housing price cycles with jump risk: evidence from the UK housing

market. The European Journal of Finance. 24(11), pp.909-943.

Byrne, M., 2020. Generation rent and the financialization of housing: A comparative exploration

of the growth of the private rental sector in Ireland, the UK and Spain. Housing

studies, 35(4), pp.743-765.

French, D., McKillop, D. and Sharma, T., 2018. What determines UK housing equity withdrawal

in later life?. Regional Science and Urban Economics, 73, pp.143-154.

Miu, L.M., Wisniewska, N., Mazur, C., Hardy, J. and Hawkes, A., 2018. A simple assessment of

housing retrofit policies for the UK: what should succeed the energy company

obligation?. Energies, 11(8), p.2070.

Ebekozien, A., Abdul-Aziz, A.R. and Jaafar, M., 2019. Remedies to inaccessibility of low-cost

housing loan in Malaysia: using the qualitative approach. Pacific Rim Property Research

Journal, 25(2), pp.159-174.

Bright, S., Weatherall, D. and Willis, R., 2019. Exploring the complexities of energy retrofit in

mixed tenure social housing: a case study from England, UK. Energy Efficiency, 12(1),

pp.157-174.

Burrows, V., 2018. The impact of house prices on consumption in the uk: A new

perspective. Economica, 85(337), pp.92-123.

Udoka, C.O. and Kpataene, M., 2017. Mortgage financing and housing development in

Nigeria. International Journal of Research-Granthaalayah, 5(5), pp.182-206.

Sanderson, D.C., Shakurina, F. and Lim, J., 2019. The impact of sale and leaseback on

commercial real estate prices and initial yields in the UK. Journal of Property

Research, 36(3), pp.245-271.

Roos, C., 2019. The (de-) politicization of EU freedom of movement: political parties,

opportunities, and policy framing in Germany and the UK. Comparative

European Politics, 17(5), pp.631-650.

Cowell, F., Karagiannaki, E. and McKnight, A., 2019. The changing distribution of wealth in the

pre-crisis US and UK: the role of socio-economic factors. Oxford Economic

Papers, 71(1), pp.1-24.

Ebekozien, A., Abdul-Aziz, A.R. and Jaafar, M., 2019. THE ROLE OF FEDERALISM IN

MALAYSIAN LOW-COST HOUSING PROVISION: THE UNEXPLORED

DIMENSION. Kajian Malaysia: Journal of Malaysian Studies, 37(1).

Arundel, R. and Hochstenbach, C., 2020. Divided access and the spatial polarization of housing

wealth. Urban Geography, 41(4), pp.497-523.

Murie, A., 2018. Shrinking the state in housing: challenges, transitions and

ambiguities. Cambridge Journal of Regions, Economy and Society, 11(3), pp.485-

501.

Farrar, S., Moizer, J., Lean, J. and Hyde, M., 2019. Gender, financial literacy, and preretirement

planning in the UK. Journal of Women & Aging, 31(4), pp.319-339.

APPENDICES

AAMC TRAINING DOCUMENT

CHECKLIST

LOAN APPLICATION PROCESS

ASSESSMENT

MORTGAGE FINANCE

Must be completed and included in your

uploaded Assessment

EVIDENCE

1. A fully completed AAMC Training Assessment Cover Sheet

2. A fully completed AAMC Training Document Checklist (this page)

Case Study - Loan Application Preparation (Task 1)

3. File notes from first contact through to settlement in chronological order

4. Authorised Credit Representative Credit Guide and Licensee Credit Guide

5. Privacy Statement and Consent form

6. Client Needs Review or Fact Find

7. Combined Credit Quote and Proposal

8. Product Comparison Report (at least three options)

9. Preliminary Assessment

10. Costing sheet for Fees and Charges

11. Fully completed Lender Loan Application or Copy of Online lodgement

Select a lender of your choice there are some forms in useful resources.

12. Lender’s loan Document Check List (Normally forms part of loan application)

Select a lender of your choice there are some forms in useful resources.

Process Applications for Credit (Task 2)

13. A completed serviceability calculator (refer to useful resources)

Select a lender of your choice there are some calculators in useful resources.

14. Loan Comments/Lender Comments. Notes to the lender in support of the application.

15. Evidence of Income (Pay slips, Employers Letter, PAYG Summaries)

16. Evidence of an Offer & Acceptance or a Contract of Sale or a Purchase contract

AAMC TRAINING DOCUMENT

CHECKLIST

LOAN APPLICATION PROCESS

ASSESSMENT

MORTGAGE FINANCE

Must be completed and included in your

uploaded Assessment

EVIDENCE

1. A fully completed AAMC Training Assessment Cover Sheet

2. A fully completed AAMC Training Document Checklist (this page)

Case Study - Loan Application Preparation (Task 1)

3. File notes from first contact through to settlement in chronological order

4. Authorised Credit Representative Credit Guide and Licensee Credit Guide

5. Privacy Statement and Consent form

6. Client Needs Review or Fact Find

7. Combined Credit Quote and Proposal

8. Product Comparison Report (at least three options)

9. Preliminary Assessment

10. Costing sheet for Fees and Charges

11. Fully completed Lender Loan Application or Copy of Online lodgement

Select a lender of your choice there are some forms in useful resources.

12. Lender’s loan Document Check List (Normally forms part of loan application)

Select a lender of your choice there are some forms in useful resources.

Process Applications for Credit (Task 2)

13. A completed serviceability calculator (refer to useful resources)

Select a lender of your choice there are some calculators in useful resources.

14. Loan Comments/Lender Comments. Notes to the lender in support of the application.

15. Evidence of Income (Pay slips, Employers Letter, PAYG Summaries)

16. Evidence of an Offer & Acceptance or a Contract of Sale or a Purchase contract

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

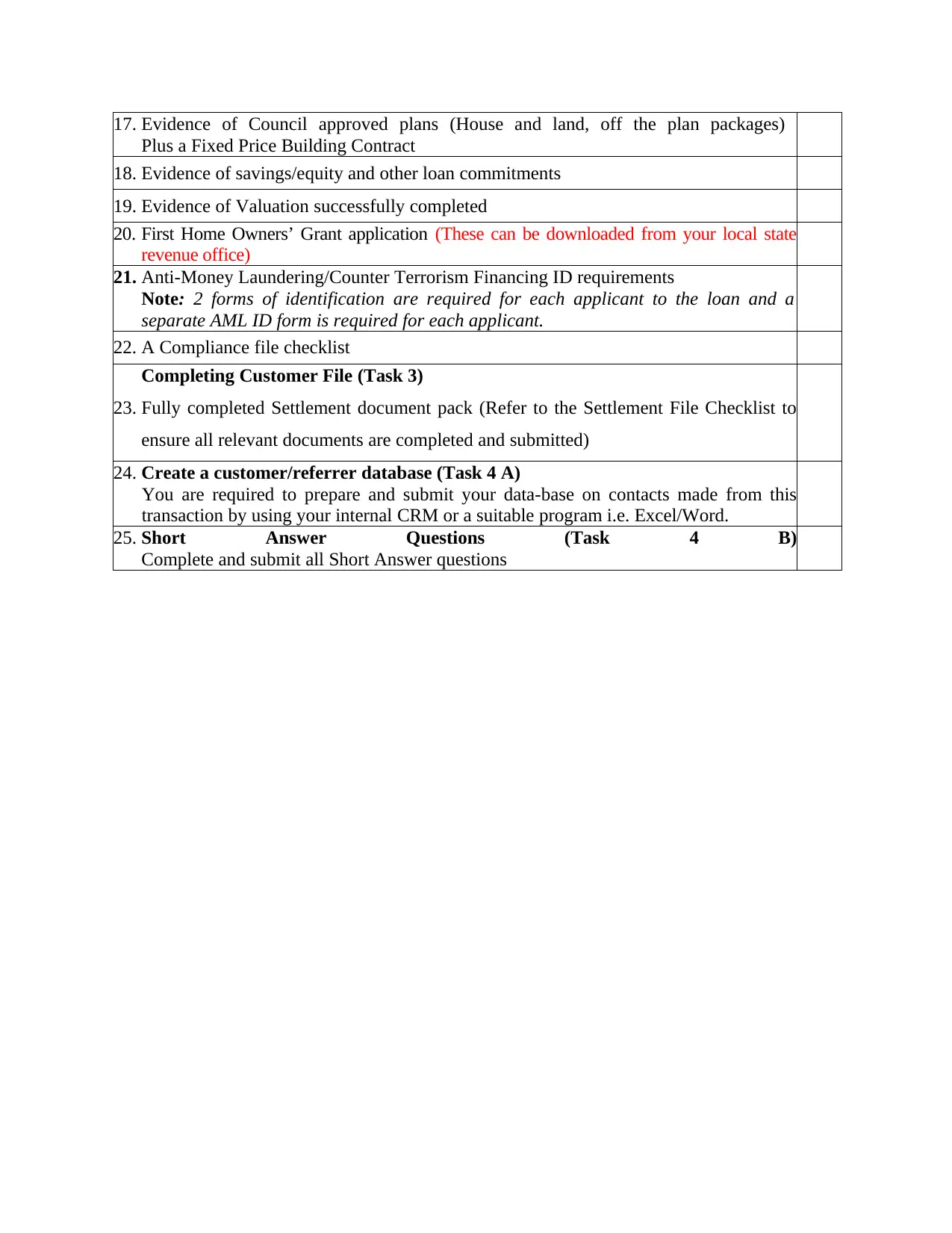

17. Evidence of Council approved plans (House and land, off the plan packages)

Plus a Fixed Price Building Contract

18. Evidence of savings/equity and other loan commitments

19. Evidence of Valuation successfully completed

20. First Home Owners’ Grant application (These can be downloaded from your local state

revenue office)

21. Anti-Money Laundering/Counter Terrorism Financing ID requirements

Note: 2 forms of identification are required for each applicant to the loan and a

separate AML ID form is required for each applicant.

22. A Compliance file checklist

Completing Customer File (Task 3)

23. Fully completed Settlement document pack (Refer to the Settlement File Checklist to

ensure all relevant documents are completed and submitted)

24. Create a customer/referrer database (Task 4 A)

You are required to prepare and submit your data-base on contacts made from this

transaction by using your internal CRM or a suitable program i.e. Excel/Word.

25. Short Answer Questions (Task 4 B)

Complete and submit all Short Answer questions

Plus a Fixed Price Building Contract

18. Evidence of savings/equity and other loan commitments

19. Evidence of Valuation successfully completed

20. First Home Owners’ Grant application (These can be downloaded from your local state

revenue office)

21. Anti-Money Laundering/Counter Terrorism Financing ID requirements

Note: 2 forms of identification are required for each applicant to the loan and a

separate AML ID form is required for each applicant.

22. A Compliance file checklist

Completing Customer File (Task 3)

23. Fully completed Settlement document pack (Refer to the Settlement File Checklist to

ensure all relevant documents are completed and submitted)

24. Create a customer/referrer database (Task 4 A)

You are required to prepare and submit your data-base on contacts made from this

transaction by using your internal CRM or a suitable program i.e. Excel/Word.

25. Short Answer Questions (Task 4 B)

Complete and submit all Short Answer questions

1 out of 29

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.