Loan Application Process for Frederick John and Margaret Anne

VerifiedAdded on 2020/07/23

|11

|1407

|194

AI Summary

The assignment details the loan application process for Frederick John and Margaret Anne. It begins with a customer contact sheet record, followed by advice on loan approval, document sign-up, and settlement preparation. The process involves approaching the client, collecting information from them, taking referrals, and developing a professional relationship. The finance broker must also ensure that documents are properly signed and that necessary information is provided to clients regarding insurance and settlement checklists. Finally, the assignment concludes with advice on transaction completion and finalization, including conducting customer satisfaction surveys and making necessary improvements.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Loan Application Process

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

PART A...........................................................................................................................................3

PART B...........................................................................................................................................8

PART C...........................................................................................................................................9

Completion of a customer file.....................................................................................................9

PART D.........................................................................................................................................10

A................................................................................................................................................10

B.................................................................................................................................................10

1.................................................................................................................................................10

2.................................................................................................................................................10

3.................................................................................................................................................10

4.................................................................................................................................................10

5.................................................................................................................................................11

6.................................................................................................................................................11

REFERENCES..............................................................................................................................12

PART A...........................................................................................................................................3

PART B...........................................................................................................................................8

PART C...........................................................................................................................................9

Completion of a customer file.....................................................................................................9

PART D.........................................................................................................................................10

A................................................................................................................................................10

B.................................................................................................................................................10

1.................................................................................................................................................10

2.................................................................................................................................................10

3.................................................................................................................................................10

4.................................................................................................................................................10

5.................................................................................................................................................11

6.................................................................................................................................................11

REFERENCES..............................................................................................................................12

PART A

Case study: Residential Mortgage

Client’s interview

On the basis of cited case situation, Frederick John and Margaret Anne wishes to

purchase their own home. From assessment, it has found that client has $184 plus FHOG

available. Purchase price of land and construction cost accounts for $240 K and 350-360K.

Along with this, from interview it has assessed that client will further spend $60k on furbishing

and garden. Through interview, it has also found that such couple will undertake insurance

policies for safeguarding then in against to illness and accidents. In interview, couple presented

that there is no such requirement in relation to making changes in the lifestyle.

Proposed loan strategies

Diversification: by using capped interest rate

Taking loan from banks using safety net

Targeting low-cost flexible loans.

From assessment, it has identified that Frederick John and Margaret Anne are eligible to get

grants from state commission office (Apply for the First Home Owner Grant, 2018).

NOTES TO LENDER TEMPLATE \

Loan application for XXXXXX & XXXXXXXX

Loan amount $466000

Latest date for approval ………/………/…………

Date: 28th April 2018

Please find loan attached application for the above clients.

Reasons behind taking loan

The reason behind taking loan by Frederick John and Margaret Anne is that they want to purchase their

Case study: Residential Mortgage

Client’s interview

On the basis of cited case situation, Frederick John and Margaret Anne wishes to

purchase their own home. From assessment, it has found that client has $184 plus FHOG

available. Purchase price of land and construction cost accounts for $240 K and 350-360K.

Along with this, from interview it has assessed that client will further spend $60k on furbishing

and garden. Through interview, it has also found that such couple will undertake insurance

policies for safeguarding then in against to illness and accidents. In interview, couple presented

that there is no such requirement in relation to making changes in the lifestyle.

Proposed loan strategies

Diversification: by using capped interest rate

Taking loan from banks using safety net

Targeting low-cost flexible loans.

From assessment, it has identified that Frederick John and Margaret Anne are eligible to get

grants from state commission office (Apply for the First Home Owner Grant, 2018).

NOTES TO LENDER TEMPLATE \

Loan application for XXXXXX & XXXXXXXX

Loan amount $466000

Latest date for approval ………/………/…………

Date: 28th April 2018

Please find loan attached application for the above clients.

Reasons behind taking loan

The reason behind taking loan by Frederick John and Margaret Anne is that they want to purchase their

own house and settle into one area.

Employment

Frederick working with BHP Billiton on their mining projects.

Margaret (qualified nurse): Working in child care centre on a permanent/part time basis

Joshua: Full time employed

Current income level

Frederick (annual income): $115,000

Margaret Anne: Earns $29,000 annually

Joshua: $75.00

Recommendations

Good financial position (couple and their one child is earning, only one child is dependent)

High employment stability

High security in new investment

Sincerely

Borrower

EVIDENCE ENCLOSED

Y N N/ A

1. A fully completed

AAMC Training

Assessment Cover Sheet

2. A fully completed

AAMC Training

Document Checklist

(this page) Case Study -

Loan Application

Preparation (Task 1)

Employment

Frederick working with BHP Billiton on their mining projects.

Margaret (qualified nurse): Working in child care centre on a permanent/part time basis

Joshua: Full time employed

Current income level

Frederick (annual income): $115,000

Margaret Anne: Earns $29,000 annually

Joshua: $75.00

Recommendations

Good financial position (couple and their one child is earning, only one child is dependent)

High employment stability

High security in new investment

Sincerely

Borrower

EVIDENCE ENCLOSED

Y N N/ A

1. A fully completed

AAMC Training

Assessment Cover Sheet

2. A fully completed

AAMC Training

Document Checklist

(this page) Case Study -

Loan Application

Preparation (Task 1)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

3. File notes from first

contact through to

settlement in

chronological order

4. Authorised Credit

Representative Credit

Guide and Licensee

Credit Guide

5. Client Needs Review

or Fact Find

6. Privacy Statement

and Consent form

7. Combined Credit

Quote and Proposal

8. Product Comparison

Report (at least three

options)

9. Preliminary

Assessment

10. Costing sheet for

Fees and Charges

11. Fully completed

Lender Loan

Application or Copy of

Online lodgement

contact through to

settlement in

chronological order

4. Authorised Credit

Representative Credit

Guide and Licensee

Credit Guide

5. Client Needs Review

or Fact Find

6. Privacy Statement

and Consent form

7. Combined Credit

Quote and Proposal

8. Product Comparison

Report (at least three

options)

9. Preliminary

Assessment

10. Costing sheet for

Fees and Charges

11. Fully completed

Lender Loan

Application or Copy of

Online lodgement

12. Lender’s loan

Document Check List

(Normally forms part of

loan application) ☐ ☐

☐ Process Applications

for Credit (Task 2)

13. A completed

serviceability calculator

(refer to useful

resources)

14. Loan

Comments/Lender

Comments

15. Evidence of Income

(Pay slips, Employers

Letter, PAYG

Summaries)

16. Evidence of an

Offer & Acceptance or a

Contract of Sale or a

Purchase contract

17. Evidence of Council

approved plans (House

and Land , Off the Plan

packages) Plus a Fixed

Price Building Contract

Document Check List

(Normally forms part of

loan application) ☐ ☐

☐ Process Applications

for Credit (Task 2)

13. A completed

serviceability calculator

(refer to useful

resources)

14. Loan

Comments/Lender

Comments

15. Evidence of Income

(Pay slips, Employers

Letter, PAYG

Summaries)

16. Evidence of an

Offer & Acceptance or a

Contract of Sale or a

Purchase contract

17. Evidence of Council

approved plans (House

and Land , Off the Plan

packages) Plus a Fixed

Price Building Contract

18. Evidence of savings/

equity and other loan

commitments

19. First Home Owners’

Grant application

(These can be

downloaded from your

Office of State

Revenue)

20. Anti Money

Laundering/Counter

Terrorism Financing ID

requirements Note: 2

forms of identification

is required for each

applicant to the loan and

a separate AML ID

form is required for

each applicant.

21. Evidence of

Valuation successfully

completed

22. A Compliance file

checklist Completing

Customer File (Task 3)

23. Fully completed

Settlement document

pack (Refer to the

Settlement

equity and other loan

commitments

19. First Home Owners’

Grant application

(These can be

downloaded from your

Office of State

Revenue)

20. Anti Money

Laundering/Counter

Terrorism Financing ID

requirements Note: 2

forms of identification

is required for each

applicant to the loan and

a separate AML ID

form is required for

each applicant.

21. Evidence of

Valuation successfully

completed

22. A Compliance file

checklist Completing

Customer File (Task 3)

23. Fully completed

Settlement document

pack (Refer to the

Settlement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

24. Create a

customer/referrer

database (Task 4 A)

You are required to

prepare and submit your

data-base on contacts

made from this

transaction by using

your internal CRM or a

suitable program i.e.

Excel.

PART B

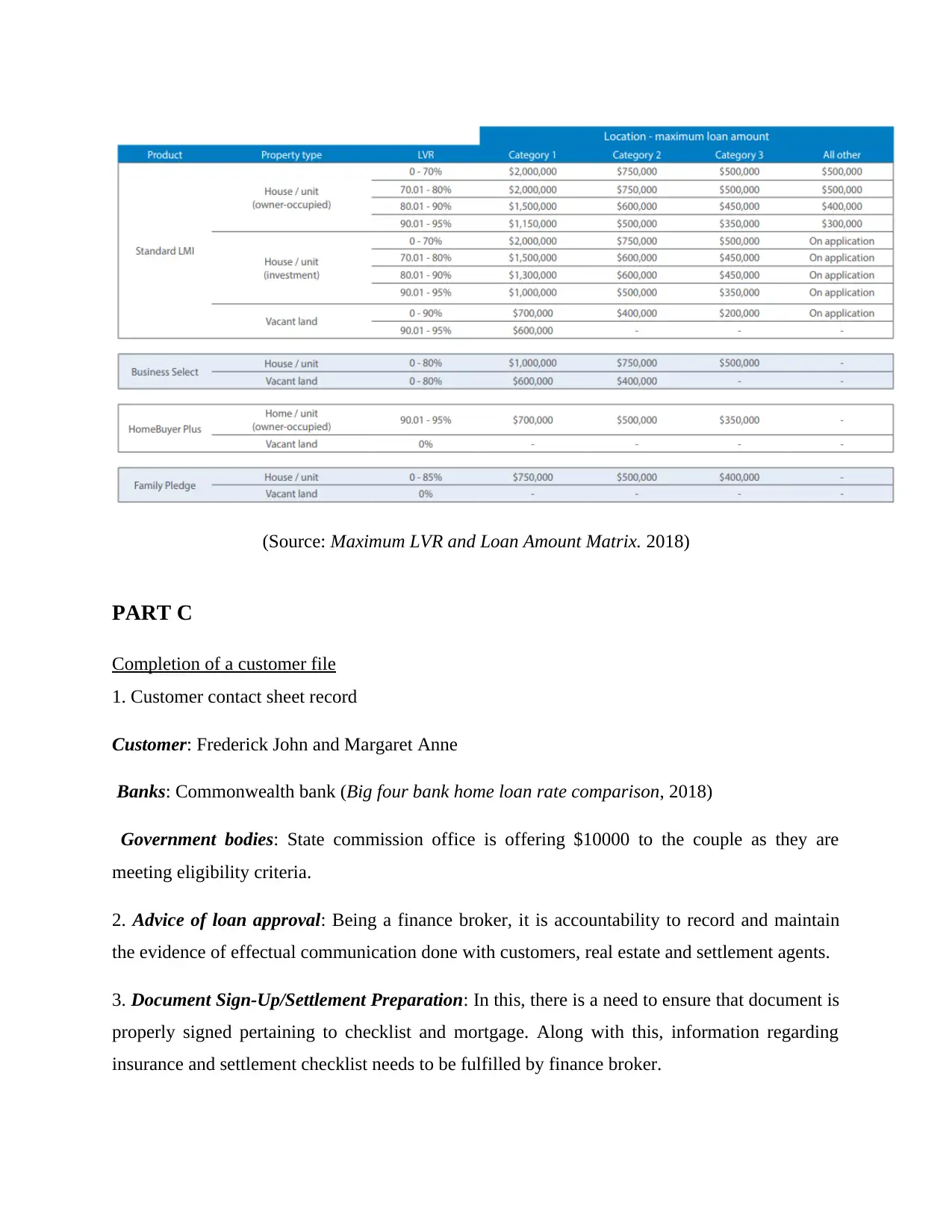

On the basis of Lender Mortgage Insurers guidelines following aspects need to be met for

the purpose of loan approval. Below mentioned image shows that loan volume ratio varies as per

investment type. In the case of mortgage case scenario, pertaining to vacant land, under the

category of 90.1% to 95% loan ratio, maximum amount implies for $600000 respectively. On

the other side, in the case of 0-90% loan volume ratio, maximum loan amount implies for

$700000, $400000 & $200000 respectively from category 1 to 3. Hence, as per the guidelines

provided by lender mortgage insurer, depicted below, loan application will be verified and then

approved. Further, lenders analyst need to ensure that firm is following the aspects of responsible

lending conduct obligations as per National Consumer Credit Protection Act 2009 in checking,

verifying and maintaining records (Responsible lending, 2018).

customer/referrer

database (Task 4 A)

You are required to

prepare and submit your

data-base on contacts

made from this

transaction by using

your internal CRM or a

suitable program i.e.

Excel.

PART B

On the basis of Lender Mortgage Insurers guidelines following aspects need to be met for

the purpose of loan approval. Below mentioned image shows that loan volume ratio varies as per

investment type. In the case of mortgage case scenario, pertaining to vacant land, under the

category of 90.1% to 95% loan ratio, maximum amount implies for $600000 respectively. On

the other side, in the case of 0-90% loan volume ratio, maximum loan amount implies for

$700000, $400000 & $200000 respectively from category 1 to 3. Hence, as per the guidelines

provided by lender mortgage insurer, depicted below, loan application will be verified and then

approved. Further, lenders analyst need to ensure that firm is following the aspects of responsible

lending conduct obligations as per National Consumer Credit Protection Act 2009 in checking,

verifying and maintaining records (Responsible lending, 2018).

(Source: Maximum LVR and Loan Amount Matrix. 2018)

PART C

Completion of a customer file

1. Customer contact sheet record

Customer: Frederick John and Margaret Anne

Banks: Commonwealth bank (Big four bank home loan rate comparison, 2018)

Government bodies: State commission office is offering $10000 to the couple as they are

meeting eligibility criteria.

2. Advice of loan approval: Being a finance broker, it is accountability to record and maintain

the evidence of effectual communication done with customers, real estate and settlement agents.

3. Document Sign-Up/Settlement Preparation: In this, there is a need to ensure that document is

properly signed pertaining to checklist and mortgage. Along with this, information regarding

insurance and settlement checklist needs to be fulfilled by finance broker.

PART C

Completion of a customer file

1. Customer contact sheet record

Customer: Frederick John and Margaret Anne

Banks: Commonwealth bank (Big four bank home loan rate comparison, 2018)

Government bodies: State commission office is offering $10000 to the couple as they are

meeting eligibility criteria.

2. Advice of loan approval: Being a finance broker, it is accountability to record and maintain

the evidence of effectual communication done with customers, real estate and settlement agents.

3. Document Sign-Up/Settlement Preparation: In this, there is a need to ensure that document is

properly signed pertaining to checklist and mortgage. Along with this, information regarding

insurance and settlement checklist needs to be fulfilled by finance broker.

4. Advice of Transaction Completed/Finalised: At this step, communication in relation to the

successful settlement is done. Further, for finalising deal prominently there is a need to conduct

client satisfaction survey and thereby make necessary changes for improvement.

PART D

A

Date Database

28/4 Approaching to the customer

29/4 Information Collection from customer

30/4 Taking referrals from the client

B

1.

Database furnishes information about the extent to which client is capable in relation to

meeting obligations.

2.

Professional relationship development is highly required for achieving success and

enhancing brand image.

3.

Individuals or customers with the history of credit defaults should not be contacted.

4.

Interpersonal style or skills are highly required in the context of finance broker.

Moreover, without having effectual communication skills broker would not become able to

convince or deal with the customers. Further, customer’s requirement in relation to the loan

policies and process also differ as per demographical aspects. Thus, broker should keep in mind

all such aspects while dealing with the clients.

successful settlement is done. Further, for finalising deal prominently there is a need to conduct

client satisfaction survey and thereby make necessary changes for improvement.

PART D

A

Date Database

28/4 Approaching to the customer

29/4 Information Collection from customer

30/4 Taking referrals from the client

B

1.

Database furnishes information about the extent to which client is capable in relation to

meeting obligations.

2.

Professional relationship development is highly required for achieving success and

enhancing brand image.

3.

Individuals or customers with the history of credit defaults should not be contacted.

4.

Interpersonal style or skills are highly required in the context of finance broker.

Moreover, without having effectual communication skills broker would not become able to

convince or deal with the customers. Further, customer’s requirement in relation to the loan

policies and process also differ as per demographical aspects. Thus, broker should keep in mind

all such aspects while dealing with the clients.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5.

Being a finance broker, it is highly required to take follow-up from the business referrers

as it helps in checking or evaluating the credential of the concerned customer.

6.

For the development of new business focus will be placed on undertaking traditional and

modern promotional aspects. In other words, by placing advertisements on social sites awareness

among the customers can be developed regarding the services and thereby customer base as well

as sales revenue.

Being a finance broker, it is highly required to take follow-up from the business referrers

as it helps in checking or evaluating the credential of the concerned customer.

6.

For the development of new business focus will be placed on undertaking traditional and

modern promotional aspects. In other words, by placing advertisements on social sites awareness

among the customers can be developed regarding the services and thereby customer base as well

as sales revenue.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.