Financial Ratio Analysis of M&S Plc

VerifiedAdded on 2020/01/16

|10

|1963

|234

AI Summary

This assignment presents a comprehensive analysis of the financial performance of M&S Plc in 2016 using various financial ratios. The analysis compares M&S's performance with its competitors, highlighting its strengths and weaknesses. Key areas examined include profitability, liquidity, solvency, and efficiency. The report concludes with recommendations for M&S to improve its financial position.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Finance

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION......................................................................................................................3

Analyzing financial performance of M&S in against to Debenhams Plc..............................3

Weaknesses of ratio analysis..................................................................................................8

RECOMMENDATIONS...........................................................................................................8

REFERENCES.........................................................................................................................10

INTRODUCTION......................................................................................................................3

Analyzing financial performance of M&S in against to Debenhams Plc..............................3

Weaknesses of ratio analysis..................................................................................................8

RECOMMENDATIONS...........................................................................................................8

REFERENCES.........................................................................................................................10

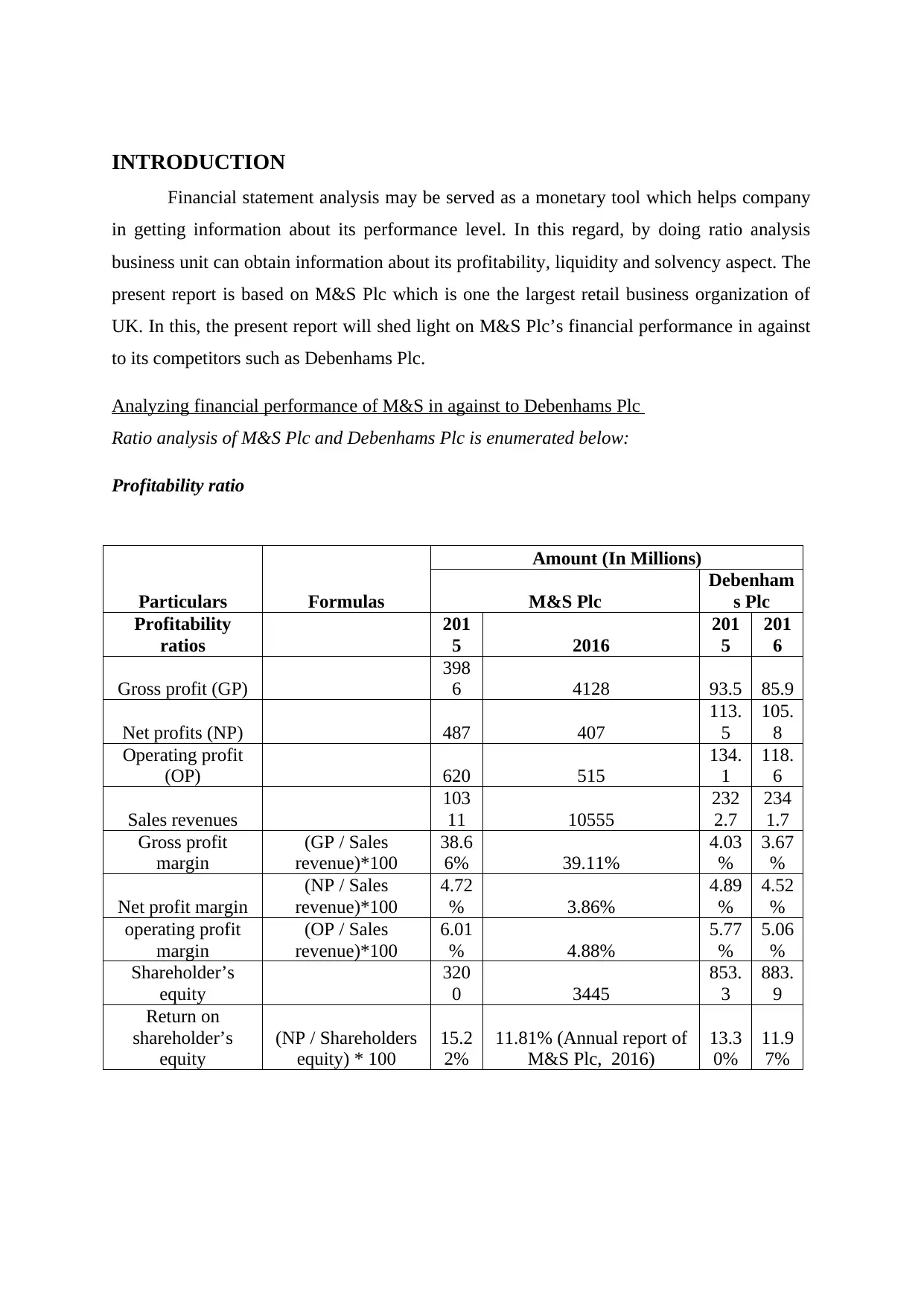

INTRODUCTION

Financial statement analysis may be served as a monetary tool which helps company

in getting information about its performance level. In this regard, by doing ratio analysis

business unit can obtain information about its profitability, liquidity and solvency aspect. The

present report is based on M&S Plc which is one the largest retail business organization of

UK. In this, the present report will shed light on M&S Plc’s financial performance in against

to its competitors such as Debenhams Plc.

Analyzing financial performance of M&S in against to Debenhams Plc

Ratio analysis of M&S Plc and Debenhams Plc is enumerated below:

Profitability ratio

Particulars Formulas

Amount (In Millions)

M&S Plc

Debenham

s Plc

Profitability

ratios

201

5 2016

201

5

201

6

Gross profit (GP)

398

6 4128 93.5 85.9

Net profits (NP) 487 407

113.

5

105.

8

Operating profit

(OP) 620 515

134.

1

118.

6

Sales revenues

103

11 10555

232

2.7

234

1.7

Gross profit

margin

(GP / Sales

revenue)*100

38.6

6% 39.11%

4.03

%

3.67

%

Net profit margin

(NP / Sales

revenue)*100

4.72

% 3.86%

4.89

%

4.52

%

operating profit

margin

(OP / Sales

revenue)*100

6.01

% 4.88%

5.77

%

5.06

%

Shareholder’s

equity

320

0 3445

853.

3

883.

9

Return on

shareholder’s

equity

(NP / Shareholders

equity) * 100

15.2

2%

11.81% (Annual report of

M&S Plc, 2016)

13.3

0%

11.9

7%

Financial statement analysis may be served as a monetary tool which helps company

in getting information about its performance level. In this regard, by doing ratio analysis

business unit can obtain information about its profitability, liquidity and solvency aspect. The

present report is based on M&S Plc which is one the largest retail business organization of

UK. In this, the present report will shed light on M&S Plc’s financial performance in against

to its competitors such as Debenhams Plc.

Analyzing financial performance of M&S in against to Debenhams Plc

Ratio analysis of M&S Plc and Debenhams Plc is enumerated below:

Profitability ratio

Particulars Formulas

Amount (In Millions)

M&S Plc

Debenham

s Plc

Profitability

ratios

201

5 2016

201

5

201

6

Gross profit (GP)

398

6 4128 93.5 85.9

Net profits (NP) 487 407

113.

5

105.

8

Operating profit

(OP) 620 515

134.

1

118.

6

Sales revenues

103

11 10555

232

2.7

234

1.7

Gross profit

margin

(GP / Sales

revenue)*100

38.6

6% 39.11%

4.03

%

3.67

%

Net profit margin

(NP / Sales

revenue)*100

4.72

% 3.86%

4.89

%

4.52

%

operating profit

margin

(OP / Sales

revenue)*100

6.01

% 4.88%

5.77

%

5.06

%

Shareholder’s

equity

320

0 3445

853.

3

883.

9

Return on

shareholder’s

equity

(NP / Shareholders

equity) * 100

15.2

2%

11.81% (Annual report of

M&S Plc, 2016)

13.3

0%

11.9

7%

(GP / Sales

revenue)*100 (NP / Sales

revenue)*100 (OP / Sales

revenue)*100

Gross profit

margin Net profit

margin operating profit

margin

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

2015 M&S

2015 Debehams Plc

Gross profit

margin Net profit

margin operating profit

margin

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

2016 M&S

2016 Debehams Plc

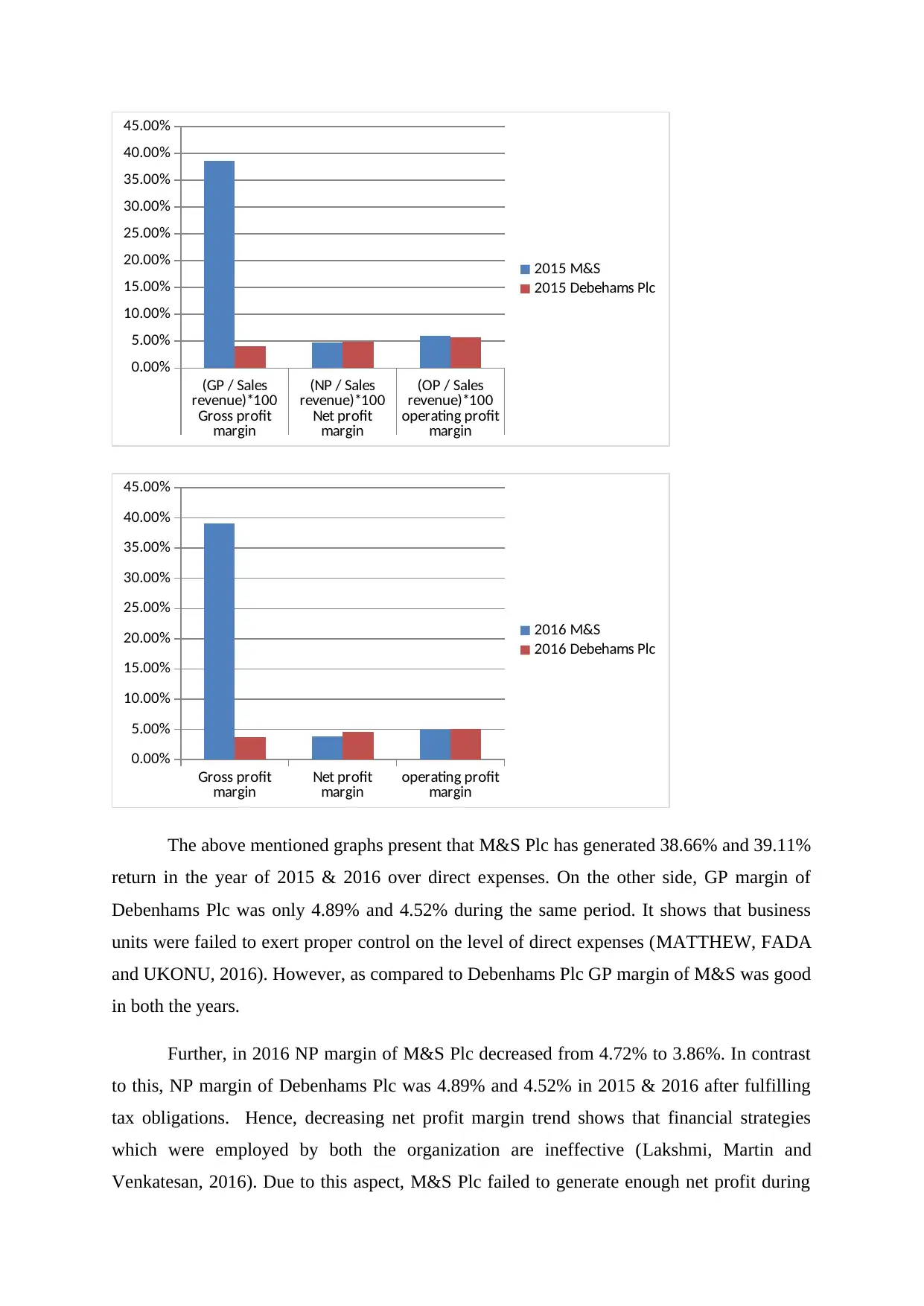

The above mentioned graphs present that M&S Plc has generated 38.66% and 39.11%

return in the year of 2015 & 2016 over direct expenses. On the other side, GP margin of

Debenhams Plc was only 4.89% and 4.52% during the same period. It shows that business

units were failed to exert proper control on the level of direct expenses (MATTHEW, FADA

and UKONU, 2016). However, as compared to Debenhams Plc GP margin of M&S was good

in both the years.

Further, in 2016 NP margin of M&S Plc decreased from 4.72% to 3.86%. In contrast

to this, NP margin of Debenhams Plc was 4.89% and 4.52% in 2015 & 2016 after fulfilling

tax obligations. Hence, decreasing net profit margin trend shows that financial strategies

which were employed by both the organization are ineffective (Lakshmi, Martin and

Venkatesan, 2016). Due to this aspect, M&S Plc failed to generate enough net profit during

revenue)*100 (NP / Sales

revenue)*100 (OP / Sales

revenue)*100

Gross profit

margin Net profit

margin operating profit

margin

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

2015 M&S

2015 Debehams Plc

Gross profit

margin Net profit

margin operating profit

margin

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

2016 M&S

2016 Debehams Plc

The above mentioned graphs present that M&S Plc has generated 38.66% and 39.11%

return in the year of 2015 & 2016 over direct expenses. On the other side, GP margin of

Debenhams Plc was only 4.89% and 4.52% during the same period. It shows that business

units were failed to exert proper control on the level of direct expenses (MATTHEW, FADA

and UKONU, 2016). However, as compared to Debenhams Plc GP margin of M&S was good

in both the years.

Further, in 2016 NP margin of M&S Plc decreased from 4.72% to 3.86%. In contrast

to this, NP margin of Debenhams Plc was 4.89% and 4.52% in 2015 & 2016 after fulfilling

tax obligations. Hence, decreasing net profit margin trend shows that financial strategies

which were employed by both the organization are ineffective (Lakshmi, Martin and

Venkatesan, 2016). Due to this aspect, M&S Plc failed to generate enough net profit during

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

the period of 2015 and 2016. Hence, by taking into consideration all such aspects it can be

said that profitability aspect of M&S Plc was sound in against to competitor firm.

Return on shareholders’ equity measure entails that in 2016 M&S failed to attain

generate high profit from shareholders equity. Moreover, in the financial year 2016, ROE of

M&S decreased from 15.22% to 11.81%. On the other side, such measure of Debenhams Plc

was showed c

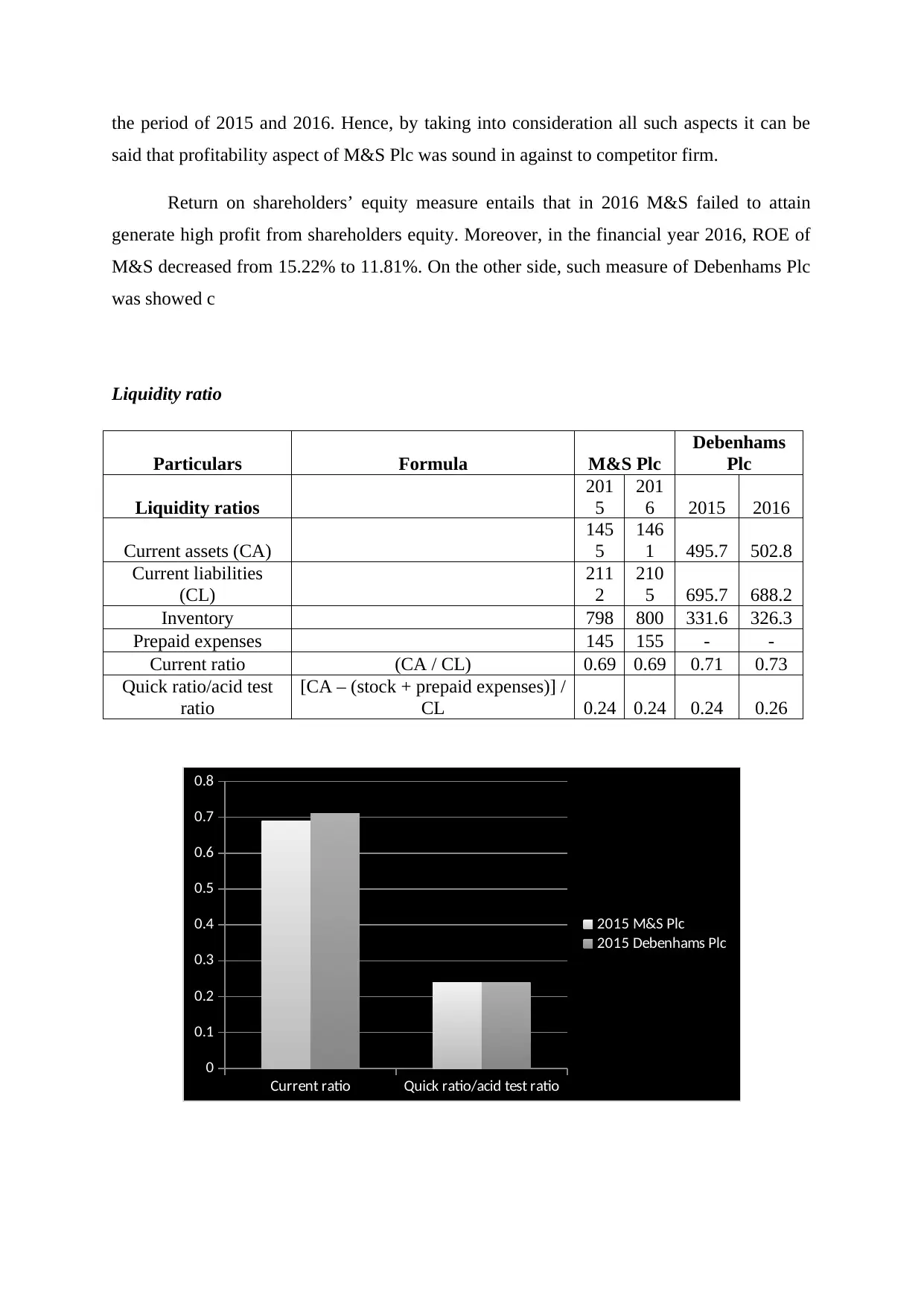

Liquidity ratio

Particulars Formula M&S Plc

Debenhams

Plc

Liquidity ratios

201

5

201

6 2015 2016

Current assets (CA)

145

5

146

1 495.7 502.8

Current liabilities

(CL)

211

2

210

5 695.7 688.2

Inventory 798 800 331.6 326.3

Prepaid expenses 145 155 - -

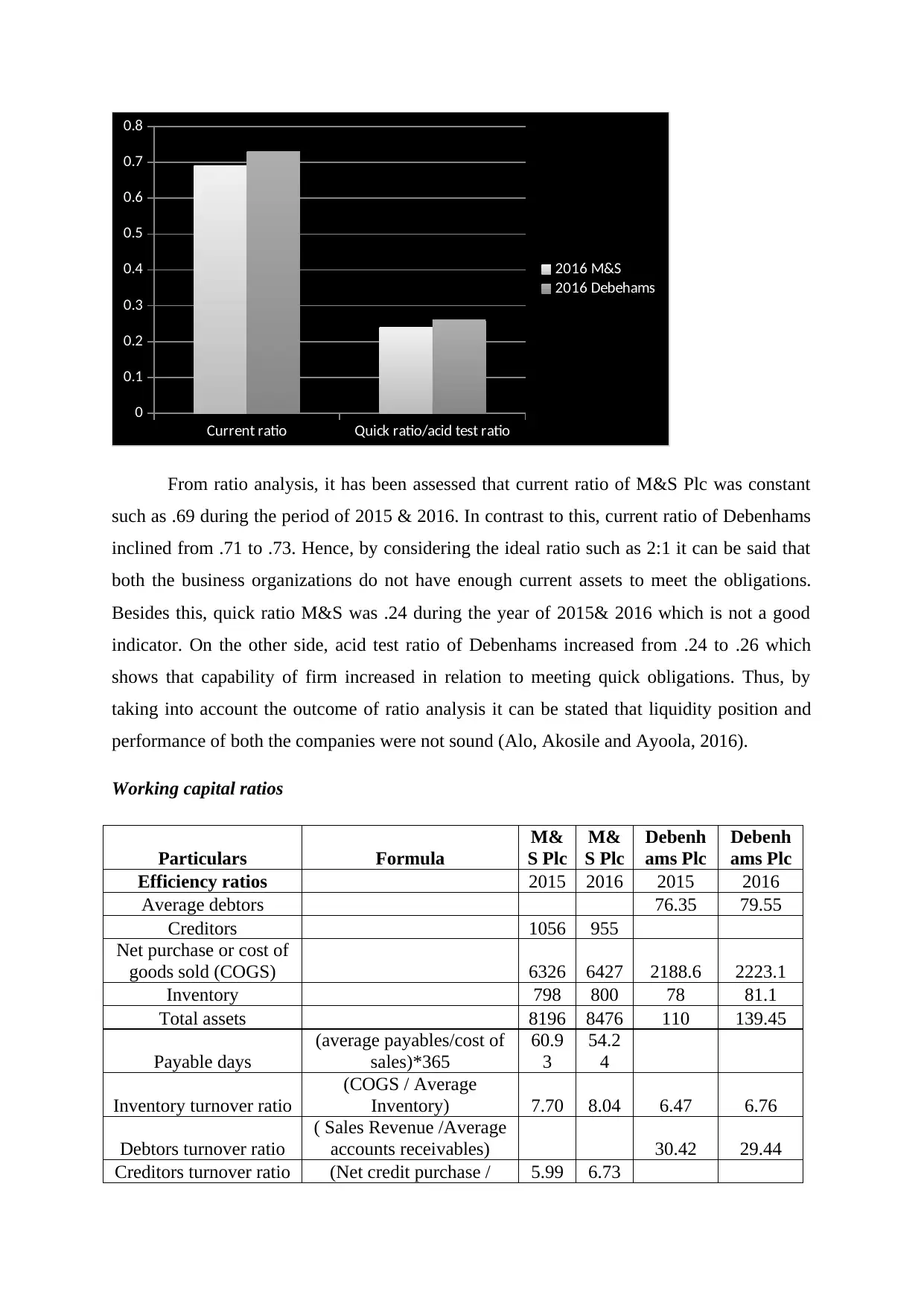

Current ratio (CA / CL) 0.69 0.69 0.71 0.73

Quick ratio/acid test

ratio

[CA – (stock + prepaid expenses)] /

CL 0.24 0.24 0.24 0.26

Current ratio Quick ratio/acid test ratio

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

2015 M&S Plc

2015 Debenhams Plc

said that profitability aspect of M&S Plc was sound in against to competitor firm.

Return on shareholders’ equity measure entails that in 2016 M&S failed to attain

generate high profit from shareholders equity. Moreover, in the financial year 2016, ROE of

M&S decreased from 15.22% to 11.81%. On the other side, such measure of Debenhams Plc

was showed c

Liquidity ratio

Particulars Formula M&S Plc

Debenhams

Plc

Liquidity ratios

201

5

201

6 2015 2016

Current assets (CA)

145

5

146

1 495.7 502.8

Current liabilities

(CL)

211

2

210

5 695.7 688.2

Inventory 798 800 331.6 326.3

Prepaid expenses 145 155 - -

Current ratio (CA / CL) 0.69 0.69 0.71 0.73

Quick ratio/acid test

ratio

[CA – (stock + prepaid expenses)] /

CL 0.24 0.24 0.24 0.26

Current ratio Quick ratio/acid test ratio

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

2015 M&S Plc

2015 Debenhams Plc

Current ratio Quick ratio/acid test ratio

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

2016 M&S

2016 Debehams

From ratio analysis, it has been assessed that current ratio of M&S Plc was constant

such as .69 during the period of 2015 & 2016. In contrast to this, current ratio of Debenhams

inclined from .71 to .73. Hence, by considering the ideal ratio such as 2:1 it can be said that

both the business organizations do not have enough current assets to meet the obligations.

Besides this, quick ratio M&S was .24 during the year of 2015& 2016 which is not a good

indicator. On the other side, acid test ratio of Debenhams increased from .24 to .26 which

shows that capability of firm increased in relation to meeting quick obligations. Thus, by

taking into account the outcome of ratio analysis it can be stated that liquidity position and

performance of both the companies were not sound (Alo, Akosile and Ayoola, 2016).

Working capital ratios

Particulars Formula

M&

S Plc

M&

S Plc

Debenh

ams Plc

Debenh

ams Plc

Efficiency ratios 2015 2016 2015 2016

Average debtors 76.35 79.55

Creditors 1056 955

Net purchase or cost of

goods sold (COGS) 6326 6427 2188.6 2223.1

Inventory 798 800 78 81.1

Total assets 8196 8476 110 139.45

Payable days

(average payables/cost of

sales)*365

60.9

3

54.2

4

Inventory turnover ratio

(COGS / Average

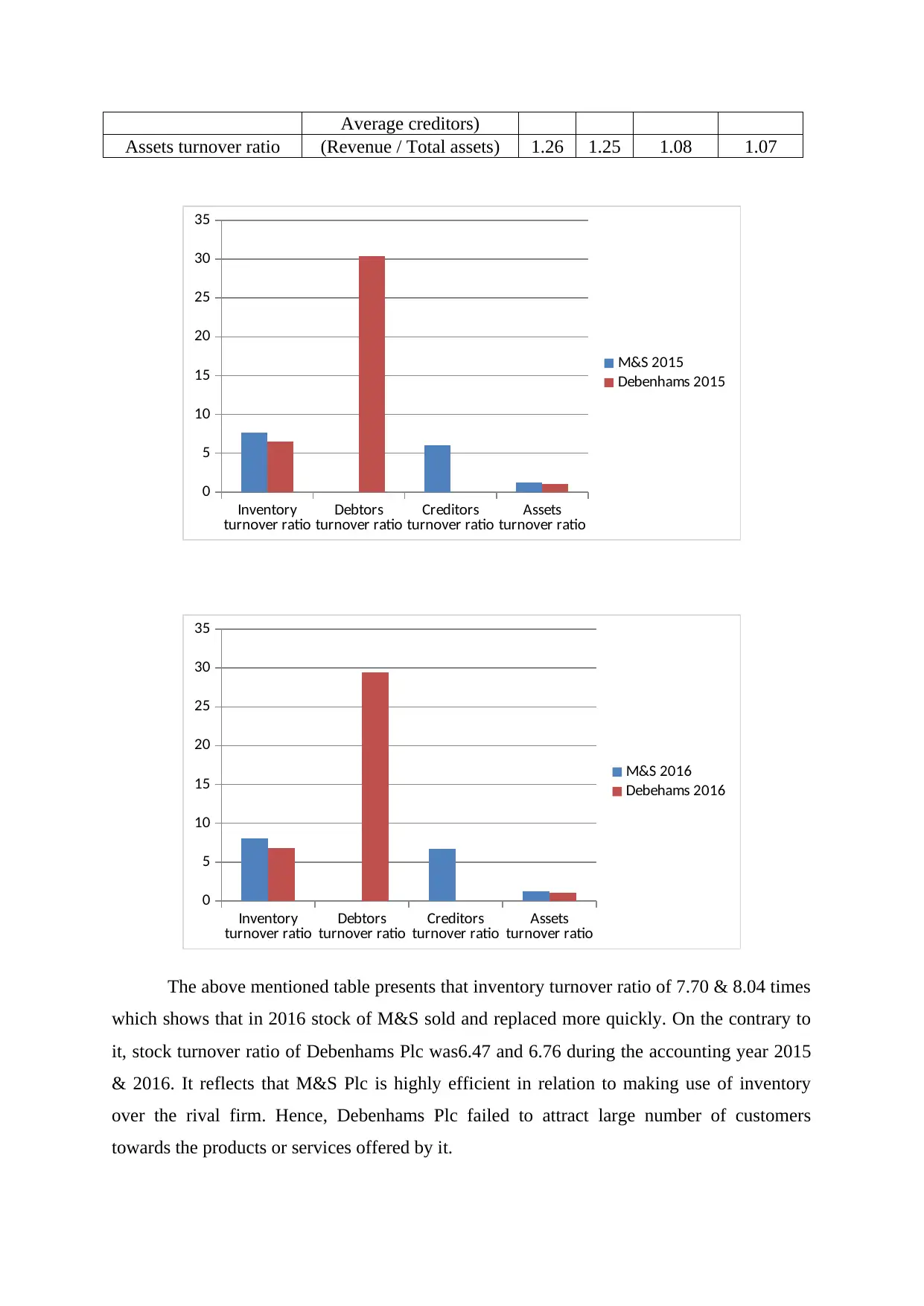

Inventory) 7.70 8.04 6.47 6.76

Debtors turnover ratio

( Sales Revenue /Average

accounts receivables) 30.42 29.44

Creditors turnover ratio (Net credit purchase / 5.99 6.73

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

2016 M&S

2016 Debehams

From ratio analysis, it has been assessed that current ratio of M&S Plc was constant

such as .69 during the period of 2015 & 2016. In contrast to this, current ratio of Debenhams

inclined from .71 to .73. Hence, by considering the ideal ratio such as 2:1 it can be said that

both the business organizations do not have enough current assets to meet the obligations.

Besides this, quick ratio M&S was .24 during the year of 2015& 2016 which is not a good

indicator. On the other side, acid test ratio of Debenhams increased from .24 to .26 which

shows that capability of firm increased in relation to meeting quick obligations. Thus, by

taking into account the outcome of ratio analysis it can be stated that liquidity position and

performance of both the companies were not sound (Alo, Akosile and Ayoola, 2016).

Working capital ratios

Particulars Formula

M&

S Plc

M&

S Plc

Debenh

ams Plc

Debenh

ams Plc

Efficiency ratios 2015 2016 2015 2016

Average debtors 76.35 79.55

Creditors 1056 955

Net purchase or cost of

goods sold (COGS) 6326 6427 2188.6 2223.1

Inventory 798 800 78 81.1

Total assets 8196 8476 110 139.45

Payable days

(average payables/cost of

sales)*365

60.9

3

54.2

4

Inventory turnover ratio

(COGS / Average

Inventory) 7.70 8.04 6.47 6.76

Debtors turnover ratio

( Sales Revenue /Average

accounts receivables) 30.42 29.44

Creditors turnover ratio (Net credit purchase / 5.99 6.73

Average creditors)

Assets turnover ratio (Revenue / Total assets) 1.26 1.25 1.08 1.07

Inventory

turnover ratio Debtors

turnover ratio Creditors

turnover ratio Assets

turnover ratio

0

5

10

15

20

25

30

35

M&S 2015

Debenhams 2015

Inventory

turnover ratio Debtors

turnover ratio Creditors

turnover ratio Assets

turnover ratio

0

5

10

15

20

25

30

35

M&S 2016

Debehams 2016

The above mentioned table presents that inventory turnover ratio of 7.70 & 8.04 times

which shows that in 2016 stock of M&S sold and replaced more quickly. On the contrary to

it, stock turnover ratio of Debenhams Plc was6.47 and 6.76 during the accounting year 2015

& 2016. It reflects that M&S Plc is highly efficient in relation to making use of inventory

over the rival firm. Hence, Debenhams Plc failed to attract large number of customers

towards the products or services offered by it.

Assets turnover ratio (Revenue / Total assets) 1.26 1.25 1.08 1.07

Inventory

turnover ratio Debtors

turnover ratio Creditors

turnover ratio Assets

turnover ratio

0

5

10

15

20

25

30

35

M&S 2015

Debenhams 2015

Inventory

turnover ratio Debtors

turnover ratio Creditors

turnover ratio Assets

turnover ratio

0

5

10

15

20

25

30

35

M&S 2016

Debehams 2016

The above mentioned table presents that inventory turnover ratio of 7.70 & 8.04 times

which shows that in 2016 stock of M&S sold and replaced more quickly. On the contrary to

it, stock turnover ratio of Debenhams Plc was6.47 and 6.76 during the accounting year 2015

& 2016. It reflects that M&S Plc is highly efficient in relation to making use of inventory

over the rival firm. Hence, Debenhams Plc failed to attract large number of customers

towards the products or services offered by it.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Debtor’s turnover ratio of Debenhams Plc was decreased from 30.42 to 29.44 in the

financial year 2016. This in turn helps in making improvement in the working capital aspect

of firm. Moreover, such outcome shows that company received payment from debtors within

quick which in turn aid in its financial position (Rakićević and et.al., 2016).

Payable turnover ratio of M&S Plc was 5.99 in 2015, whereas it inclined in 2016 such

as 6.73. On the basis of this aspect, time in relation to making payment to creditors increased

in 2016. However, such turnover ratio is lower which in turn creates financial burden in front

of M&S Plc.

Ratio analysis presents that M&S Plc has made optimum use of assets while carry out

business activities and functions. The reason behind this, asset turnover ratio increased from

1.26 to 1.25. On the other side, such performance level of Debenhams Plc was decreased

from 1.08 to 1.07 in the financial year ended at 2016. Thus, asset turnover ratio of M&S Plc

was good in 2016 as compared to previous years.

Cash flow statement analysis of M&S and Debenhams Plc

Particulars Formula M&S Plc Debenhams Plc

2015 2016 2015 2016

Free cash flow /

net income

Free cash flow =

[Net profit +

(Depreciation –

changes in working

capital )] / Net

income

1.19 1.63 .90 1.02

Free cash flow /

sales revenue %

Free cash flow =

[Net profit +

(Depreciation –

changes in working

capital )] / sales

revenue %

5.61 6.27 3.64 3.73

The above mentioned table presents that M&S Plc has transformed more amount into

cash at the end of 2016. In the period of 2015 and 2016 free cash flow to sales ratio of M&S

Plc was 5.61 & 6.27. On the other side, such ratio of Debenhams Plc was increased from 3.64

to 3.73. In addition to this, high net income has been generated by M&S Plc from free cash

financial year 2016. This in turn helps in making improvement in the working capital aspect

of firm. Moreover, such outcome shows that company received payment from debtors within

quick which in turn aid in its financial position (Rakićević and et.al., 2016).

Payable turnover ratio of M&S Plc was 5.99 in 2015, whereas it inclined in 2016 such

as 6.73. On the basis of this aspect, time in relation to making payment to creditors increased

in 2016. However, such turnover ratio is lower which in turn creates financial burden in front

of M&S Plc.

Ratio analysis presents that M&S Plc has made optimum use of assets while carry out

business activities and functions. The reason behind this, asset turnover ratio increased from

1.26 to 1.25. On the other side, such performance level of Debenhams Plc was decreased

from 1.08 to 1.07 in the financial year ended at 2016. Thus, asset turnover ratio of M&S Plc

was good in 2016 as compared to previous years.

Cash flow statement analysis of M&S and Debenhams Plc

Particulars Formula M&S Plc Debenhams Plc

2015 2016 2015 2016

Free cash flow /

net income

Free cash flow =

[Net profit +

(Depreciation –

changes in working

capital )] / Net

income

1.19 1.63 .90 1.02

Free cash flow /

sales revenue %

Free cash flow =

[Net profit +

(Depreciation –

changes in working

capital )] / sales

revenue %

5.61 6.27 3.64 3.73

The above mentioned table presents that M&S Plc has transformed more amount into

cash at the end of 2016. In the period of 2015 and 2016 free cash flow to sales ratio of M&S

Plc was 5.61 & 6.27. On the other side, such ratio of Debenhams Plc was increased from 3.64

to 3.73. In addition to this, high net income has been generated by M&S Plc from free cash

flow in the period of 2016. Hence, by considering all such aspects it can be said cash position

of M&S Plc was sound in comparison to the rival firms.

Weaknesses of ratio analysis

Ratio analysis technique provides deeper insight to the organization about financial

performance of itself as well as in against to competitors. However, there are some

deficiencies which closely influence the significance of ratio analysis. Accounting principles

and standards are highly differing from one company to another (Atoom, Malkawi and Share,

2017). For instance: M&S Plc follows IAS 12 for recognizing the amount of deferred tax,

whereas others are not. Due to this, companies are unable to

RECOMMENDATIONS

It is recommended to M&S Plc to develop highly competent monetary framework for

making control on both direct and indirect expenses. In this regard, by employing

budgetary control techniques business unit can reduce overspending and thereby

would become able to improve its gross and net profit margin.

Further, M&S should make focus on maintaining proper current assets such as stock,

cash, receivables etc. By improving financial capability in relation to meeting

obligations business unit can strengthen its liquidity position to a great extent.

M&S Plc should also make focus on the maintenance of assets which in turn assists

company in enhancing the level of output. Besides this, firm also needs to motivate

personnel to reduce the wastage of assets and thereby fulfill the aims and objectives.

of M&S Plc was sound in comparison to the rival firms.

Weaknesses of ratio analysis

Ratio analysis technique provides deeper insight to the organization about financial

performance of itself as well as in against to competitors. However, there are some

deficiencies which closely influence the significance of ratio analysis. Accounting principles

and standards are highly differing from one company to another (Atoom, Malkawi and Share,

2017). For instance: M&S Plc follows IAS 12 for recognizing the amount of deferred tax,

whereas others are not. Due to this, companies are unable to

RECOMMENDATIONS

It is recommended to M&S Plc to develop highly competent monetary framework for

making control on both direct and indirect expenses. In this regard, by employing

budgetary control techniques business unit can reduce overspending and thereby

would become able to improve its gross and net profit margin.

Further, M&S should make focus on maintaining proper current assets such as stock,

cash, receivables etc. By improving financial capability in relation to meeting

obligations business unit can strengthen its liquidity position to a great extent.

M&S Plc should also make focus on the maintenance of assets which in turn assists

company in enhancing the level of output. Besides this, firm also needs to motivate

personnel to reduce the wastage of assets and thereby fulfill the aims and objectives.

REFERENCES

Books and Journals

Alo, E.A., Akosile, A.I. and Ayoola, A.O., 2016. The Statistical Evaluation of the

Performance of Financial Ratio Analysis in Nigerian Manufacturing Industry: An

Empirical Study of Guinness Nigeria PLC. The International Journal of Business &

Management, 4(1), p.295.

Atoom, R., Malkawi, E. and Share, B.A., 2017. Utilizing Australian Shareholders'

Association (ASA): Fifteen Top Financial Ratios to Evaluate Jordanian Banks'

Performance. Journal of Applied Finance & Banking. 7(1). pp.119-141.

Lakshmi, T .M., Martin, A. and Venkatesan, V. P., 2016. A Genetic Bankrupt Ratio Analysis

Tool Using a Genetic Algorithm to Identify Influencing Financial Ratios. IEEE

Transactions on Evolutionary Computation, 20(1), pp.38-51.

MATTHEW, D. A. A., FADA, A. and UKONU, I. C., 2016. ROLE OF FINANCIAL

RATIO ANALYSIS IN ASSESSING BUSINESS PERFORMANCE IN THE

HOSPITALITY AND TOURISM OPERATIONS. Development. 4(4).

Rakićević, A. and et.al., 2016. DuPont Financial Ratio Analysis Using Logical Aggregation.

In Soft Computing Applications (pp. 727-739). Springer International Publishing.

Online

Annual report of M&S Plc. 2016. Online. Available through: <

http://www.thedrum.com/profile/project/244193/marks-and-spencer-plc-reporting-suite-

2015 >. [Accessed on 28th January 2017].

Key ratios related to the cash flow statement. 2015. Online. Available through:

<https://www.equitymaster.com/detail.asp?date=12/16/2009&story=4&title=Key-ratios-

related-%20to-the-cashflow-statement>. [Accessed on 28th January 2017].

REFERENCES

Books and Journals

Alo, E.A., Akosile, A.I. and Ayoola, A.O., 2016. The Statistical Evaluation of the

Performance of Financial Ratio Analysis in Nigerian Manufacturing Industry: An

Empirical Study of Guinness Nigeria PLC. The International Journal of Business &

Management, 4(1), p.295.

Atoom, R., Malkawi, E. and Share, B.A., 2017. Utilizing Australian Shareholders'

Association (ASA): Fifteen Top Financial Ratios to Evaluate Jordanian Banks'

Performance. Journal of Applied Finance & Banking. 7(1). pp.119-141.

Lakshmi, T .M., Martin, A. and Venkatesan, V. P., 2016. A Genetic Bankrupt Ratio Analysis

Tool Using a Genetic Algorithm to Identify Influencing Financial Ratios. IEEE

Transactions on Evolutionary Computation, 20(1), pp.38-51.

MATTHEW, D. A. A., FADA, A. and UKONU, I. C., 2016. ROLE OF FINANCIAL

RATIO ANALYSIS IN ASSESSING BUSINESS PERFORMANCE IN THE

HOSPITALITY AND TOURISM OPERATIONS. Development. 4(4).

Rakićević, A. and et.al., 2016. DuPont Financial Ratio Analysis Using Logical Aggregation.

In Soft Computing Applications (pp. 727-739). Springer International Publishing.

Online

Annual report of M&S Plc. 2016. Online. Available through: <

http://www.thedrum.com/profile/project/244193/marks-and-spencer-plc-reporting-suite-

2015 >. [Accessed on 28th January 2017].

Key ratios related to the cash flow statement. 2015. Online. Available through:

<https://www.equitymaster.com/detail.asp?date=12/16/2009&story=4&title=Key-ratios-

related-%20to-the-cashflow-statement>. [Accessed on 28th January 2017].

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.