Management Accounting & Financial Tools

VerifiedAdded on 2020/06/06

|18

|4721

|34

AI Summary

This assignment delves into the crucial role of management accounting and reporting in organizational success. It examines various financial tools such as KPIs, Balance Scorecards, and Just-In-Time inventory strategies, highlighting their application in addressing financial challenges and enhancing performance. The case study compares Tech (UK) Limited and 4Com Plc., demonstrating how these tools can be used to analyze financial data, improve operational efficiency, and ultimately achieve growth.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management

Accounting

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1............................................................................................................................................1

P2............................................................................................................................................3

M1:.........................................................................................................................................5

D1...........................................................................................................................................5

TASK 2............................................................................................................................................6

P3............................................................................................................................................6

M2...........................................................................................................................................8

D2...........................................................................................................................................9

TASK 3............................................................................................................................................9

P4............................................................................................................................................9

M3.........................................................................................................................................11

D3:........................................................................................................................................11

TASK 4..........................................................................................................................................11

P5..........................................................................................................................................11

M4.........................................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1............................................................................................................................................1

P2............................................................................................................................................3

M1:.........................................................................................................................................5

D1...........................................................................................................................................5

TASK 2............................................................................................................................................6

P3............................................................................................................................................6

M2...........................................................................................................................................8

D2...........................................................................................................................................9

TASK 3............................................................................................................................................9

P4............................................................................................................................................9

M3.........................................................................................................................................11

D3:........................................................................................................................................11

TASK 4..........................................................................................................................................11

P5..........................................................................................................................................11

M4.........................................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting directs an organisation to achieve desired goals and objectives

through providing relevant information related with financial as well as non-financial

transactions happened on daily basis. It plays an important role in analysing business cost and

operations in order to prepare internal financial report such as Profit and loss a/c, Balance sheet,

cash flow statement etc. Thus, the management of an organisation are held liable to perform

three basic function such as strategic management, performance appraisal and risk reduction.

Tech (UK) Limited company which deals in manufacturing special charger for mobile telephone

and other various gadgets is taken for the purpose of preparing this report. The project covers the

description of management accounting along with their essential requirements in an organisation.

There are different management accounting systems and reports which covers and contains all

relevant information regarding making an effective decision (Baldvinsdottir, Mitchell and

Nørreklit, 2010). Different types of budgets and costing methods which help company in

managing and controlling cost in future project activities are also covered under this report.

TASK 1

P1.

Definitions:

The institute of Certified Management Accountant (CMA) states that the management

accountant should required to utilise their skills and knowledge in order to prepare and

present financial reports which assist in making an effective decision and policies in

order to control business operations.

American Institute of Certified Public Accountants (AICPA) states the management

accounting is a practice of management in order to perform three basic function such as

strategic management, performance appraisal and risk reduction in order to achieve

desired goals and objectives within pre-determined period of time.

Meaning:

Management accounting is the presentation of accounting details in such an effective

way that will help management in formulating policy regarding functioning and operating

business on daily basis. Thus, it helps in providing relevant information through preparing

1

Management accounting directs an organisation to achieve desired goals and objectives

through providing relevant information related with financial as well as non-financial

transactions happened on daily basis. It plays an important role in analysing business cost and

operations in order to prepare internal financial report such as Profit and loss a/c, Balance sheet,

cash flow statement etc. Thus, the management of an organisation are held liable to perform

three basic function such as strategic management, performance appraisal and risk reduction.

Tech (UK) Limited company which deals in manufacturing special charger for mobile telephone

and other various gadgets is taken for the purpose of preparing this report. The project covers the

description of management accounting along with their essential requirements in an organisation.

There are different management accounting systems and reports which covers and contains all

relevant information regarding making an effective decision (Baldvinsdottir, Mitchell and

Nørreklit, 2010). Different types of budgets and costing methods which help company in

managing and controlling cost in future project activities are also covered under this report.

TASK 1

P1.

Definitions:

The institute of Certified Management Accountant (CMA) states that the management

accountant should required to utilise their skills and knowledge in order to prepare and

present financial reports which assist in making an effective decision and policies in

order to control business operations.

American Institute of Certified Public Accountants (AICPA) states the management

accounting is a practice of management in order to perform three basic function such as

strategic management, performance appraisal and risk reduction in order to achieve

desired goals and objectives within pre-determined period of time.

Meaning:

Management accounting is the presentation of accounting details in such an effective

way that will help management in formulating policy regarding functioning and operating

business on daily basis. Thus, it helps in providing relevant information through preparing

1

accounting reports which shows true and fair financial position of company (Christ and Burritt,

2013).

Difference between management and financial accounting

Management accounting Financial Accounting

It helps an organisation to achieve competitive

advantage through utilising relevant

information provided with the help of

management accounting system.

It helps internal as well as external parties to

know the company's actual financial position

so that they can able to take an effective

decision regarding making investment in

company.

It is not yet necessary for company to use

management accounting system.

It is essentially required for company to

prepare financial records on annual basis.

It includes information of both financial as

well as non-financial transaction.

It includes the information of only financial

transaction that happened in an organisation on

daily basis.

There is no specific time to prepare reports as

it mainly depends on the needs and

requirements of the organisation.

It is prepared at the end of accounting year.

It helps internal management to formulate an

effective policies to operate daily business

operation in an effective and efficient manner.

It helps internal as well as external parties to

make an effective decision for their betterment.

Importance of management accounting

Determination of aim: As management accounting system provides various financial as

well as non-financial information which help management in setting up new target for each

departments on the basis of their capabilities (Cinquini and Tenucci, 2010).

Helps in formulation of plans: With the help of information available through

management accounting system, the management are able to prepare an effective decision and

plans for the future business activities. It helps management in identifying the skilled and

knowledgeable employees and defines their roles and responsibilities accordingly.

2

2013).

Difference between management and financial accounting

Management accounting Financial Accounting

It helps an organisation to achieve competitive

advantage through utilising relevant

information provided with the help of

management accounting system.

It helps internal as well as external parties to

know the company's actual financial position

so that they can able to take an effective

decision regarding making investment in

company.

It is not yet necessary for company to use

management accounting system.

It is essentially required for company to

prepare financial records on annual basis.

It includes information of both financial as

well as non-financial transaction.

It includes the information of only financial

transaction that happened in an organisation on

daily basis.

There is no specific time to prepare reports as

it mainly depends on the needs and

requirements of the organisation.

It is prepared at the end of accounting year.

It helps internal management to formulate an

effective policies to operate daily business

operation in an effective and efficient manner.

It helps internal as well as external parties to

make an effective decision for their betterment.

Importance of management accounting

Determination of aim: As management accounting system provides various financial as

well as non-financial information which help management in setting up new target for each

departments on the basis of their capabilities (Cinquini and Tenucci, 2010).

Helps in formulation of plans: With the help of information available through

management accounting system, the management are able to prepare an effective decision and

plans for the future business activities. It helps management in identifying the skilled and

knowledgeable employees and defines their roles and responsibilities accordingly.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Measurement of performance: Management accounting system provides the information

regrading the performance of each and every employee which help management in improving

their skills and knowledge if any deviation found in their actual and standard performance.

It helps management to get accurate information on the basis of which the management

are able to make decision regarding investment in different areas of department in order

to get profitable outcomes.

It helps in setting up the prices of products after analysing the cost incurred in production

process.

Different management accounting systems

There are many management accounting systems which are described as below:

Cost accounting system: This system must required to adopt by every business

organisation in order to manage and control cost which will incurred in future business activities.

It helps management to fix cost of their cost after analysing the cost incurred in manufacturing

process. With the help of this system, the management are able to prepare budget for deifferen5t

departments according to their needs and requirements so that profitable outcome will received

in near future (Dillard and Roslender, 2011).

Inventory management system: This system is essential used by the management in

order to determine the inventory stock available with an organisation in order to fulfil customer's

needs and requirements. This system provides an opportunity to manager to place an order of

stock on time if any shortage of inventory are found. This will help in running production

process of an organisation without any interruptions. The management should require to make

suitable planning regarding allocation of inventory to different departments on the basis of their

requirements.

Job costing system: This system provides information related with cos and revenue

generated after manufacturing specific product or group of products. The management need to

track different types of direct expenses such as direct labour and direct materials which are

incurred in manufacturing process of particular product. It is important to first forecast the result

after producing specific product and accordingly giving importance in order to achieve

profitability.

3

regrading the performance of each and every employee which help management in improving

their skills and knowledge if any deviation found in their actual and standard performance.

It helps management to get accurate information on the basis of which the management

are able to make decision regarding investment in different areas of department in order

to get profitable outcomes.

It helps in setting up the prices of products after analysing the cost incurred in production

process.

Different management accounting systems

There are many management accounting systems which are described as below:

Cost accounting system: This system must required to adopt by every business

organisation in order to manage and control cost which will incurred in future business activities.

It helps management to fix cost of their cost after analysing the cost incurred in manufacturing

process. With the help of this system, the management are able to prepare budget for deifferen5t

departments according to their needs and requirements so that profitable outcome will received

in near future (Dillard and Roslender, 2011).

Inventory management system: This system is essential used by the management in

order to determine the inventory stock available with an organisation in order to fulfil customer's

needs and requirements. This system provides an opportunity to manager to place an order of

stock on time if any shortage of inventory are found. This will help in running production

process of an organisation without any interruptions. The management should require to make

suitable planning regarding allocation of inventory to different departments on the basis of their

requirements.

Job costing system: This system provides information related with cos and revenue

generated after manufacturing specific product or group of products. The management need to

track different types of direct expenses such as direct labour and direct materials which are

incurred in manufacturing process of particular product. It is important to first forecast the result

after producing specific product and accordingly giving importance in order to achieve

profitability.

3

P2.

There are different types of business activities which are operated in business

organisation with a motive of achieving desired goals and objectives. Management of Tech (UK)

is held required to prepared various accounting reports such as job costing, cost accounting,

inventory management system etc. which contains relevant informations regarding functions of

company. This will help management in making an effective decision and plans for future

growth and success of an organisation (Fullerton, Kennedy and Widener, 2014). Accounting

reports includes profit and loss a/c, Balance sheet, Cash Flow statement etc. which can be used

by internal and external parties to an organisation regarding the decision taken for their

betterment. Therefore, the management should required to prepared various managerial reports

which are described as below;

Budget report: These reports is prepared by management with a motive of allocating cost

to future business activities of different departments in order to execute them without any

interruptions. The management is first required to analyse the performance of different

department after identifying their past performance and accordingly give extra support to them

for operating business activities. Adoption of reporting system provides an opportunity to

management pare an effective budget in order to achieve bets possible result in near future.

Accounts receivable report: This report contains the list of debtors or customers of an

organisation whose payments to company are due or pending. Thus, it helps management to

identify those unpaid customers and make suitable steps to recover due amount from them on

time. Through this, the management ensures inflow of funds which help them in improving

financial position of company (Garrison and et. al., 2010).

Job cost reports: This report contains the information regarding cost and revenue which

are going to incurred on manufacturing specific project in order to evaluate job profitability. It

provides an opportunity to management to focus on important areas which will bring profitable

outcome to them in near future. With the help of using information available through such report,

the manager find no difficulties in allocation of cost to activities of different departments.

Inventory and manufacturing: These reports contains the information regarding current

position of inventory in company. With the help of using information, the management can

easily identify the level of inventory available with company and accordingly decide whether to

place an order of inventory or not.

4

There are different types of business activities which are operated in business

organisation with a motive of achieving desired goals and objectives. Management of Tech (UK)

is held required to prepared various accounting reports such as job costing, cost accounting,

inventory management system etc. which contains relevant informations regarding functions of

company. This will help management in making an effective decision and plans for future

growth and success of an organisation (Fullerton, Kennedy and Widener, 2014). Accounting

reports includes profit and loss a/c, Balance sheet, Cash Flow statement etc. which can be used

by internal and external parties to an organisation regarding the decision taken for their

betterment. Therefore, the management should required to prepared various managerial reports

which are described as below;

Budget report: These reports is prepared by management with a motive of allocating cost

to future business activities of different departments in order to execute them without any

interruptions. The management is first required to analyse the performance of different

department after identifying their past performance and accordingly give extra support to them

for operating business activities. Adoption of reporting system provides an opportunity to

management pare an effective budget in order to achieve bets possible result in near future.

Accounts receivable report: This report contains the list of debtors or customers of an

organisation whose payments to company are due or pending. Thus, it helps management to

identify those unpaid customers and make suitable steps to recover due amount from them on

time. Through this, the management ensures inflow of funds which help them in improving

financial position of company (Garrison and et. al., 2010).

Job cost reports: This report contains the information regarding cost and revenue which

are going to incurred on manufacturing specific project in order to evaluate job profitability. It

provides an opportunity to management to focus on important areas which will bring profitable

outcome to them in near future. With the help of using information available through such report,

the manager find no difficulties in allocation of cost to activities of different departments.

Inventory and manufacturing: These reports contains the information regarding current

position of inventory in company. With the help of using information, the management can

easily identify the level of inventory available with company and accordingly decide whether to

place an order of inventory or not.

4

Importance of managerial accounting reports

Decision making: The reports provides relevant information relating to financial as well

as non-financial which help management in making an effective decision in order to achieve

desired target. This helps in future planning, performance management and risk reduction which

enhances profitability of company.

Reduce loss: The information available through management reporting system helps in

identifying the problems or issues that may occurred in future business activities which help

management to ready with their corrective measures in order to overcome deviations and

maximises efficiency. For example, using Job costing method helps in identifying the areas

where the chances of incurring wastage will be more thus it it helps in reducing cost of

production and earn huge profits (Macintosh and Quattrone, 2010).

Increase financial returns: Such reporting system help management in making better

decision and plans for the different departments in order to execute business activities in more

effective and efficient manner. For this, the management need to provide training to employees

so that they can perform delegated roles and responsibilities and bring profitable result to

company in return.

M1:.

Job costing systems

Advantages:

It helps in allocation of cost to produce specific product on the basis of outcomes

received in future.

It helps in enhancing the quality of work of different departments

Inventory management system:

Advantages:

It helps in meeting customer's demands and requirements which brings trust and loyalty

of customers towards company.

It helps in reducing inventory cost due to ordering only when the company needed

(Nandan, 2010).

D1.

Types of reporting Integration with organisational process

5

Decision making: The reports provides relevant information relating to financial as well

as non-financial which help management in making an effective decision in order to achieve

desired target. This helps in future planning, performance management and risk reduction which

enhances profitability of company.

Reduce loss: The information available through management reporting system helps in

identifying the problems or issues that may occurred in future business activities which help

management to ready with their corrective measures in order to overcome deviations and

maximises efficiency. For example, using Job costing method helps in identifying the areas

where the chances of incurring wastage will be more thus it it helps in reducing cost of

production and earn huge profits (Macintosh and Quattrone, 2010).

Increase financial returns: Such reporting system help management in making better

decision and plans for the different departments in order to execute business activities in more

effective and efficient manner. For this, the management need to provide training to employees

so that they can perform delegated roles and responsibilities and bring profitable result to

company in return.

M1:.

Job costing systems

Advantages:

It helps in allocation of cost to produce specific product on the basis of outcomes

received in future.

It helps in enhancing the quality of work of different departments

Inventory management system:

Advantages:

It helps in meeting customer's demands and requirements which brings trust and loyalty

of customers towards company.

It helps in reducing inventory cost due to ordering only when the company needed

(Nandan, 2010).

D1.

Types of reporting Integration with organisational process

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Account receivable report Its helps management to collect due amount

from unpaid debtors which strong financial

position of company.

Job cost report It helps in producing specific product after

identifying its outcome that may received in

future which indirectly helps in ascertainment

of profits.

TASK 2

P3.

Costing refers to the amount of value which is invested in production process in order to

manufacture quality products. Thus, the management is held responsible to first estimate cost

and accordingly prepare budget in order to execute future project activities in more successful

manner. Basically there are two type of costing methods through which the company should able

to calculate actual cost to their product after considering all cost which were incurred starting

from production process to final sale to targeted customers. Such costing methods are:

Marginal costing: It refers to the cost which are incurred in producing additional extra

unit of product. Such costing methods doesn't includes fixed cost as it affects their profitability.

Thus only variable costs has been taken into account as it may changes in production capacity of

company (Nixon and Burns, 2011).

Absorption costing: Under this method, fixed cost has also been included in the total cost

of production along with variable cost. Mostly companies has adopted such costing methods as it

help in increasing their profitability due to adding fixed cost in total cost of production.

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

6

from unpaid debtors which strong financial

position of company.

Job cost report It helps in producing specific product after

identifying its outcome that may received in

future which indirectly helps in ascertainment

of profits.

TASK 2

P3.

Costing refers to the amount of value which is invested in production process in order to

manufacture quality products. Thus, the management is held responsible to first estimate cost

and accordingly prepare budget in order to execute future project activities in more successful

manner. Basically there are two type of costing methods through which the company should able

to calculate actual cost to their product after considering all cost which were incurred starting

from production process to final sale to targeted customers. Such costing methods are:

Marginal costing: It refers to the cost which are incurred in producing additional extra

unit of product. Such costing methods doesn't includes fixed cost as it affects their profitability.

Thus only variable costs has been taken into account as it may changes in production capacity of

company (Nixon and Burns, 2011).

Absorption costing: Under this method, fixed cost has also been included in the total cost

of production along with variable cost. Mostly companies has adopted such costing methods as it

help in increasing their profitability due to adding fixed cost in total cost of production.

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

6

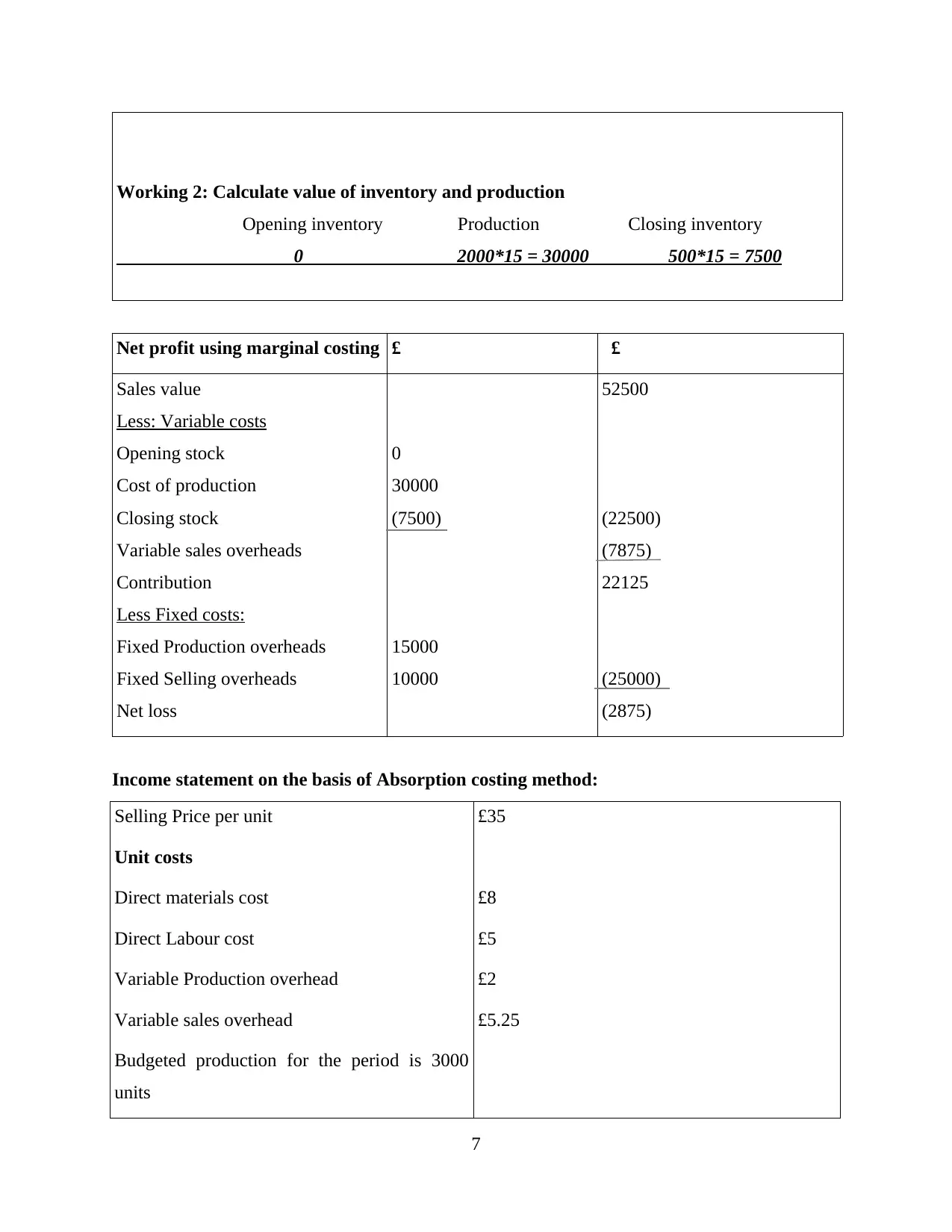

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Cost of production

Closing stock

Variable sales overheads

Contribution

Less Fixed costs:

Fixed Production overheads

Fixed Selling overheads

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

Income statement on the basis of Absorption costing method:

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

7

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Cost of production

Closing stock

Variable sales overheads

Contribution

Less Fixed costs:

Fixed Production overheads

Fixed Selling overheads

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

Income statement on the basis of Absorption costing method:

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

7

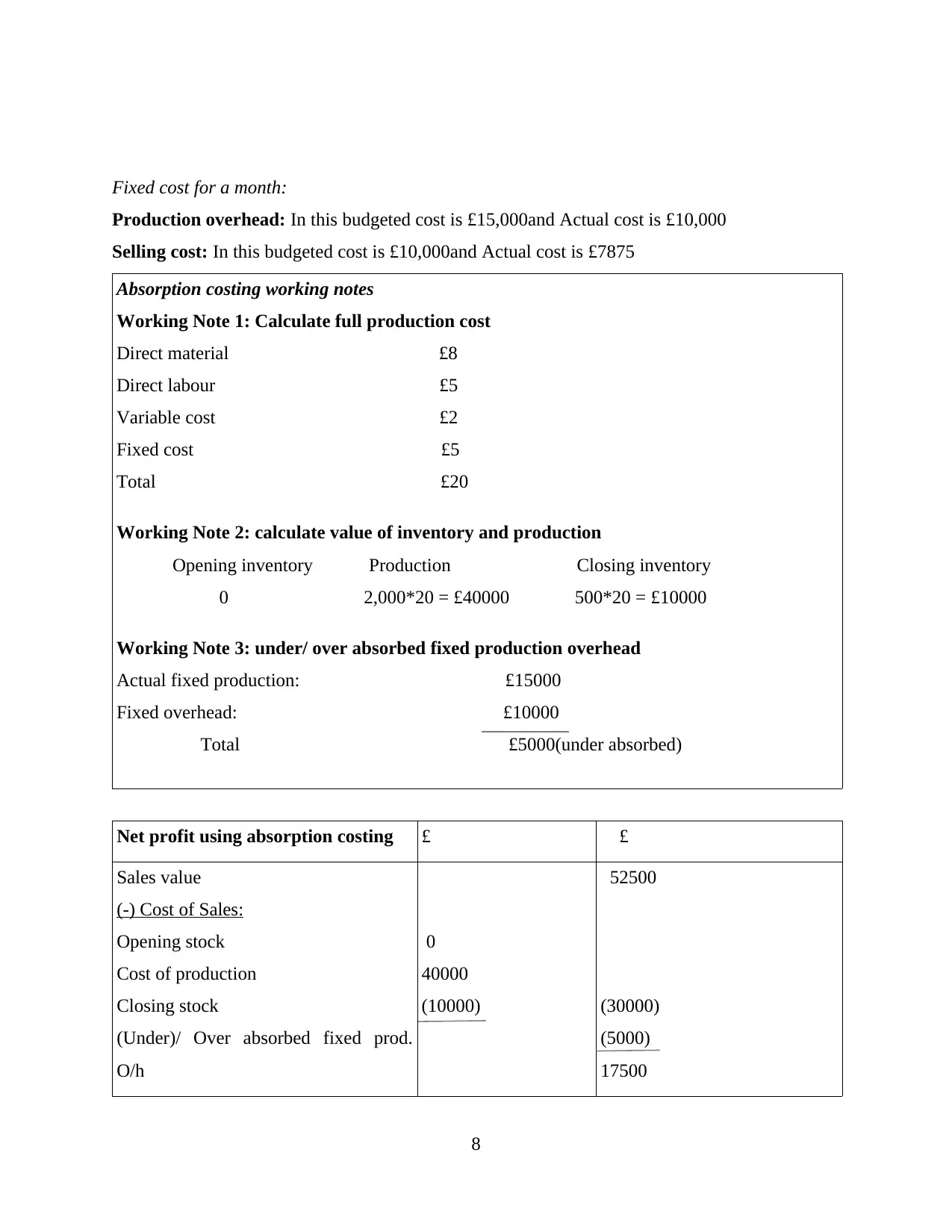

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Net profit using absorption costing £ £

Sales value

(-) Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

0

40000

(10000)

52500

(30000)

(5000)

17500

8

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Net profit using absorption costing £ £

Sales value

(-) Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

0

40000

(10000)

52500

(30000)

(5000)

17500

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

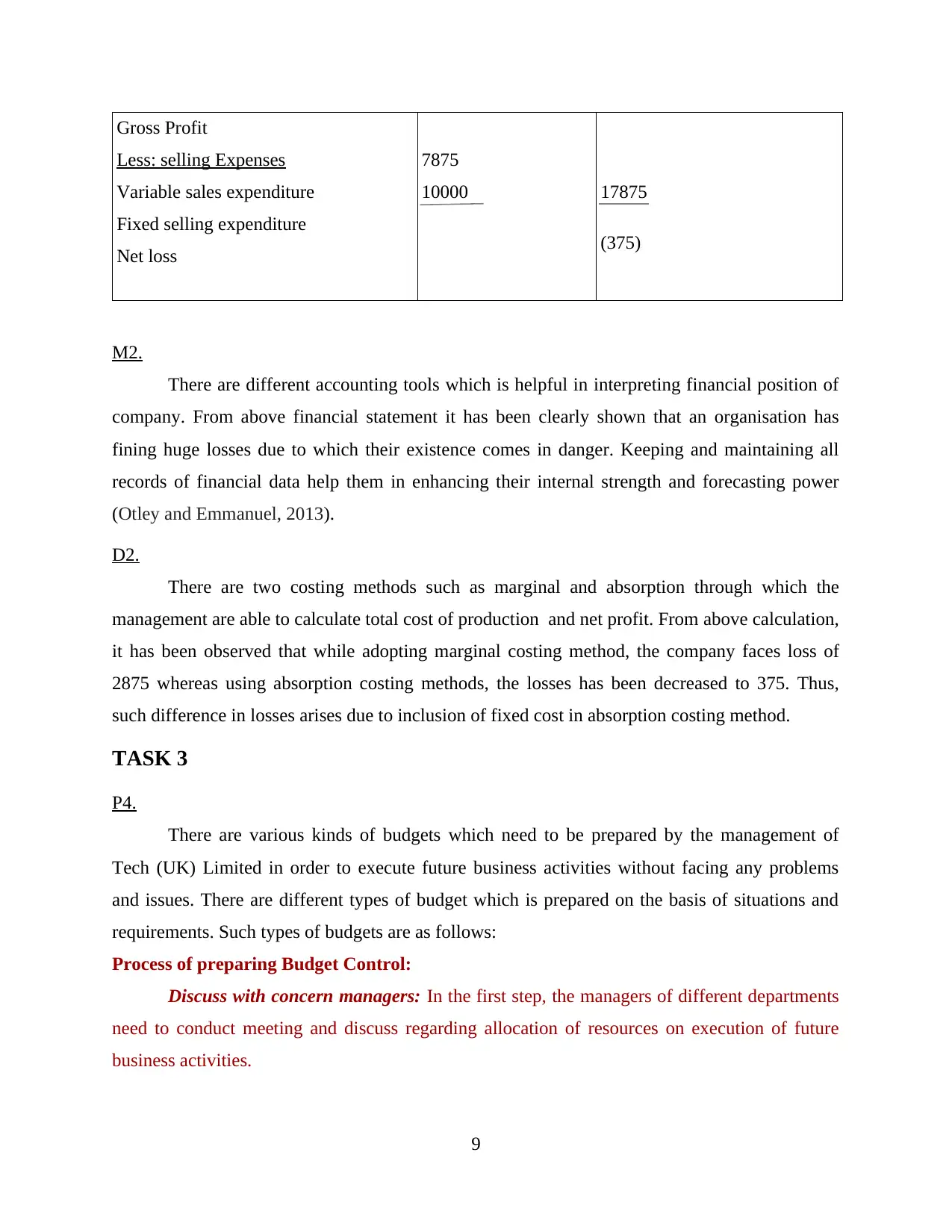

Gross Profit

Less: selling Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

7875

10000 17875

(375)

M2.

There are different accounting tools which is helpful in interpreting financial position of

company. From above financial statement it has been clearly shown that an organisation has

fining huge losses due to which their existence comes in danger. Keeping and maintaining all

records of financial data help them in enhancing their internal strength and forecasting power

(Otley and Emmanuel, 2013).

D2.

There are two costing methods such as marginal and absorption through which the

management are able to calculate total cost of production and net profit. From above calculation,

it has been observed that while adopting marginal costing method, the company faces loss of

2875 whereas using absorption costing methods, the losses has been decreased to 375. Thus,

such difference in losses arises due to inclusion of fixed cost in absorption costing method.

TASK 3

P4.

There are various kinds of budgets which need to be prepared by the management of

Tech (UK) Limited in order to execute future business activities without facing any problems

and issues. There are different types of budget which is prepared on the basis of situations and

requirements. Such types of budgets are as follows:

Process of preparing Budget Control:

Discuss with concern managers: In the first step, the managers of different departments

need to conduct meeting and discuss regarding allocation of resources on execution of future

business activities.

9

Less: selling Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

7875

10000 17875

(375)

M2.

There are different accounting tools which is helpful in interpreting financial position of

company. From above financial statement it has been clearly shown that an organisation has

fining huge losses due to which their existence comes in danger. Keeping and maintaining all

records of financial data help them in enhancing their internal strength and forecasting power

(Otley and Emmanuel, 2013).

D2.

There are two costing methods such as marginal and absorption through which the

management are able to calculate total cost of production and net profit. From above calculation,

it has been observed that while adopting marginal costing method, the company faces loss of

2875 whereas using absorption costing methods, the losses has been decreased to 375. Thus,

such difference in losses arises due to inclusion of fixed cost in absorption costing method.

TASK 3

P4.

There are various kinds of budgets which need to be prepared by the management of

Tech (UK) Limited in order to execute future business activities without facing any problems

and issues. There are different types of budget which is prepared on the basis of situations and

requirements. Such types of budgets are as follows:

Process of preparing Budget Control:

Discuss with concern managers: In the first step, the managers of different departments

need to conduct meeting and discuss regarding allocation of resources on execution of future

business activities.

9

Determination of effective assumption: In the second step, the manager need to forecast

the expenses incurred in future business activities and on the basis of assumptions an effective

strategies should be made.

Set organisational data for budget to achieve goals: In this step, all the information

collected from the different departments and assemble data in order to execute future business

activities.

Measurement of information with actual: In this step, the management of company need

to measure performance of company through comparing actual information with standard in

order to find out exact position of company.

Review analysis: In this last step. All above step should be reviewed carefully in order to

ensure to get profitable outcome in near future.

Master budget: It is the combination of all lower-level budgets produced by a company's

various functional areas and also included budgeted financial statements, a cash forecast and a

financial plan. It is interrelated with many budgets of different departments of company. These

budget are used by manager of company with a motive of making an effective plans and set

performance objectives (Parker, 2012).

Operational budget: This budget is prepared with a motive of managing and controlling

cost incurred in daily business operations. It is prepare on the basis of estimation that how much

cost should be incurred in particular business operation so as to achieve best possible outcome in

near future. This will help management in identifying the revenue that may generated after

incurring cost on producing particular product.

Cash flow statement: This type of budget is prepared with a motive of identifying the

ability of company to lend money from the market and capability to pay out. These budget helps

management to manage cash flow of company which ensures in having adequacy of funds during

executing project activities..

Activity based budget: This is such type of budget which is prepared on the basis of

activities execute in future. As there are various activities are performed thus make decision

regarding allocation of cost to different activities should be required.

10

the expenses incurred in future business activities and on the basis of assumptions an effective

strategies should be made.

Set organisational data for budget to achieve goals: In this step, all the information

collected from the different departments and assemble data in order to execute future business

activities.

Measurement of information with actual: In this step, the management of company need

to measure performance of company through comparing actual information with standard in

order to find out exact position of company.

Review analysis: In this last step. All above step should be reviewed carefully in order to

ensure to get profitable outcome in near future.

Master budget: It is the combination of all lower-level budgets produced by a company's

various functional areas and also included budgeted financial statements, a cash forecast and a

financial plan. It is interrelated with many budgets of different departments of company. These

budget are used by manager of company with a motive of making an effective plans and set

performance objectives (Parker, 2012).

Operational budget: This budget is prepared with a motive of managing and controlling

cost incurred in daily business operations. It is prepare on the basis of estimation that how much

cost should be incurred in particular business operation so as to achieve best possible outcome in

near future. This will help management in identifying the revenue that may generated after

incurring cost on producing particular product.

Cash flow statement: This type of budget is prepared with a motive of identifying the

ability of company to lend money from the market and capability to pay out. These budget helps

management to manage cash flow of company which ensures in having adequacy of funds during

executing project activities..

Activity based budget: This is such type of budget which is prepared on the basis of

activities execute in future. As there are various activities are performed thus make decision

regarding allocation of cost to different activities should be required.

10

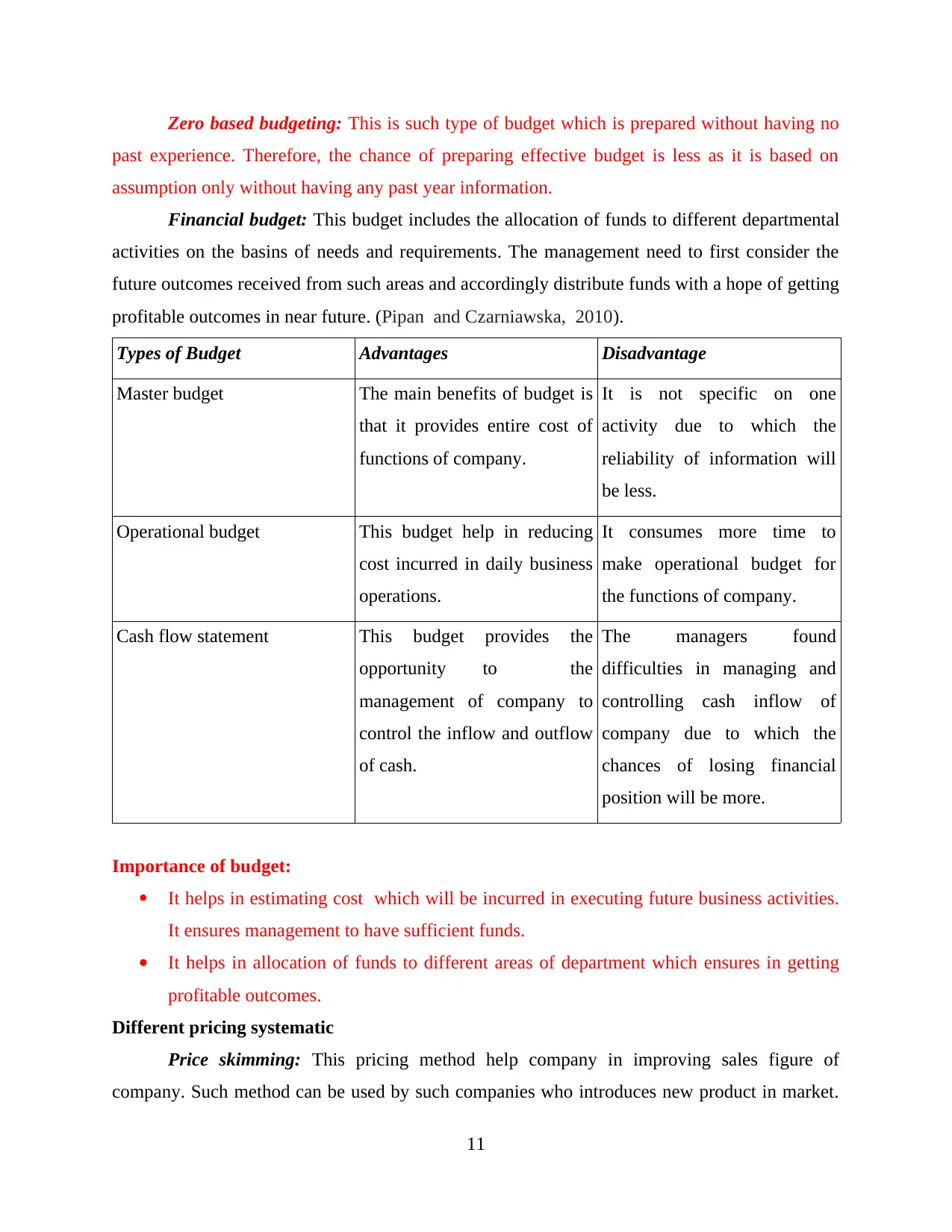

Zero based budgeting: This is such type of budget which is prepared without having no

past experience. Therefore, the chance of preparing effective budget is less as it is based on

assumption only without having any past year information.

Financial budget: This budget includes the allocation of funds to different departmental

activities on the basins of needs and requirements. The management need to first consider the

future outcomes received from such areas and accordingly distribute funds with a hope of getting

profitable outcomes in near future. (Pipan and Czarniawska, 2010).

Types of Budget Advantages Disadvantage

Master budget The main benefits of budget is

that it provides entire cost of

functions of company.

It is not specific on one

activity due to which the

reliability of information will

be less.

Operational budget This budget help in reducing

cost incurred in daily business

operations.

It consumes more time to

make operational budget for

the functions of company.

Cash flow statement This budget provides the

opportunity to the

management of company to

control the inflow and outflow

of cash.

The managers found

difficulties in managing and

controlling cash inflow of

company due to which the

chances of losing financial

position will be more.

Importance of budget:

It helps in estimating cost which will be incurred in executing future business activities.

It ensures management to have sufficient funds.

It helps in allocation of funds to different areas of department which ensures in getting

profitable outcomes.

Different pricing systematic

Price skimming: This pricing method help company in improving sales figure of

company. Such method can be used by such companies who introduces new product in market.

11

past experience. Therefore, the chance of preparing effective budget is less as it is based on

assumption only without having any past year information.

Financial budget: This budget includes the allocation of funds to different departmental

activities on the basins of needs and requirements. The management need to first consider the

future outcomes received from such areas and accordingly distribute funds with a hope of getting

profitable outcomes in near future. (Pipan and Czarniawska, 2010).

Types of Budget Advantages Disadvantage

Master budget The main benefits of budget is

that it provides entire cost of

functions of company.

It is not specific on one

activity due to which the

reliability of information will

be less.

Operational budget This budget help in reducing

cost incurred in daily business

operations.

It consumes more time to

make operational budget for

the functions of company.

Cash flow statement This budget provides the

opportunity to the

management of company to

control the inflow and outflow

of cash.

The managers found

difficulties in managing and

controlling cash inflow of

company due to which the

chances of losing financial

position will be more.

Importance of budget:

It helps in estimating cost which will be incurred in executing future business activities.

It ensures management to have sufficient funds.

It helps in allocation of funds to different areas of department which ensures in getting

profitable outcomes.

Different pricing systematic

Price skimming: This pricing method help company in improving sales figure of

company. Such method can be used by such companies who introduces new product in market.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The management first charge low prices on their product in order to attract maximum number of

customers and once the product is successfully launched then they slowly increases the price of

products in order to gain profit.

Economy pricing: With the help of this method, the company lower its prices of products

so as to influence and buying behaviour of customers towards purchasing their product. They

offers products to those customers who are more price conscious consumers (Qian, Burritt and

Monroe, 2011).

Different costing systems

Direct costing: Under this method of costing, co0st to product has includes such cost

which varies with change in volume. It includes different cost which are related with direct

material, labour, variable manufacturing expenses etc.

Standard costing: This system help in monitoring cost and identifying the changes which

are arise in comparison to standards. The different activities to which regard it is used is

valuation of stock, WIP and fixing selling prices.

M3.

There are several planning tools such as forecasting and scenario tools which must

required to adopt by an organisation in order to make an effective budgets. This will help

company in achieving desired goals and objectives through directing and guiding employees to

perform their best. Such planning tools has some disadvantage as well as if estimation gone

wrong then it will brings negative result to company as well (Shah, Malik and Malik, 2011).

D3:.

It has been observed earlier that an organisation faces losses due to lots of issues arises at

workplace. Thus, adoption of planning tools helps them to overcome financial issues in an

effective manner. For example forecasting tools helps in identifying the internal as well as

external factors which make either negative or positive impact on the performance of company.

Thus, it help management to make an effective strategy to deal with such factors in best possible

way.

12

customers and once the product is successfully launched then they slowly increases the price of

products in order to gain profit.

Economy pricing: With the help of this method, the company lower its prices of products

so as to influence and buying behaviour of customers towards purchasing their product. They

offers products to those customers who are more price conscious consumers (Qian, Burritt and

Monroe, 2011).

Different costing systems

Direct costing: Under this method of costing, co0st to product has includes such cost

which varies with change in volume. It includes different cost which are related with direct

material, labour, variable manufacturing expenses etc.

Standard costing: This system help in monitoring cost and identifying the changes which

are arise in comparison to standards. The different activities to which regard it is used is

valuation of stock, WIP and fixing selling prices.

M3.

There are several planning tools such as forecasting and scenario tools which must

required to adopt by an organisation in order to make an effective budgets. This will help

company in achieving desired goals and objectives through directing and guiding employees to

perform their best. Such planning tools has some disadvantage as well as if estimation gone

wrong then it will brings negative result to company as well (Shah, Malik and Malik, 2011).

D3:.

It has been observed earlier that an organisation faces losses due to lots of issues arises at

workplace. Thus, adoption of planning tools helps them to overcome financial issues in an

effective manner. For example forecasting tools helps in identifying the internal as well as

external factors which make either negative or positive impact on the performance of company.

Thus, it help management to make an effective strategy to deal with such factors in best possible

way.

12

TASK 4

P5.

Tech (UK) Limited offers special charger for mobile phones and other gadgets to retail

outlets of UK. It has been recently identified that the company has been facing a losses of 1.5

million which clearly shows that the company has facing financial problems due to which they

find difficulties in sustaining in competitive market world (Vaivio and Sirén, 2010). Therefore,

to remove such circumstances the management need to focus on implementing various financial

tools such as Balance scorecard approach, Key Performance Indicator, Just in Time etc. These all

are further described as under:

Key Performance Indicators: It is an effective tool which help in measuring

performance and actual capability of employees in order to identify whether they have

employees having sufficient skilled and knowledge to perform different business activities in an

effective and efficient manner. KPI are used at different level with the purpose of evaluating the

success and ability of achieving desired goals and objectives. It is of two types such as financial

as well as non-financial. Financial KPI includes P&L a/c, Balance sheet etc. which shows

profitability situation of company whereas Non-financial indicators includes employee relation

etc. in order to gain trust of employees (Van Helden and Northcott, 2010).

Balance scorecard approach: This approach is used with a motive of combining

business activities with the vision and strategies of organisations through proper coordination

and communication with the employees. Thus, it is important for management to provide

training and learning programs to their employees in order to enhance their skills and knowledge

and gives their maximum efforts in achieving desired objectives. The main purpose for adoption

of such approach are as follows:

To enhance performance of company by focusing on important matters.

To direct and motivate employees to perform better so as to achieve desired target.

Reducing communication gap between the management and employees.

Four perspectives of Balance scorecard approach Financial: In this, a organisation mainly focuses on improving financial performance

through utilising available resources in an optimum manner which directly enhance their

profitability.

13

P5.

Tech (UK) Limited offers special charger for mobile phones and other gadgets to retail

outlets of UK. It has been recently identified that the company has been facing a losses of 1.5

million which clearly shows that the company has facing financial problems due to which they

find difficulties in sustaining in competitive market world (Vaivio and Sirén, 2010). Therefore,

to remove such circumstances the management need to focus on implementing various financial

tools such as Balance scorecard approach, Key Performance Indicator, Just in Time etc. These all

are further described as under:

Key Performance Indicators: It is an effective tool which help in measuring

performance and actual capability of employees in order to identify whether they have

employees having sufficient skilled and knowledge to perform different business activities in an

effective and efficient manner. KPI are used at different level with the purpose of evaluating the

success and ability of achieving desired goals and objectives. It is of two types such as financial

as well as non-financial. Financial KPI includes P&L a/c, Balance sheet etc. which shows

profitability situation of company whereas Non-financial indicators includes employee relation

etc. in order to gain trust of employees (Van Helden and Northcott, 2010).

Balance scorecard approach: This approach is used with a motive of combining

business activities with the vision and strategies of organisations through proper coordination

and communication with the employees. Thus, it is important for management to provide

training and learning programs to their employees in order to enhance their skills and knowledge

and gives their maximum efforts in achieving desired objectives. The main purpose for adoption

of such approach are as follows:

To enhance performance of company by focusing on important matters.

To direct and motivate employees to perform better so as to achieve desired target.

Reducing communication gap between the management and employees.

Four perspectives of Balance scorecard approach Financial: In this, a organisation mainly focuses on improving financial performance

through utilising available resources in an optimum manner which directly enhance their

profitability.

13

Customer and stakeholder: In this perspective, the main motive is to provide quality

product to customers in order to maximise their level of satisfaction. This will help

company in retaining loyal customers for longer period of time. Internal process: Under this, the main aim is to develop internal process through bring

efficiency in the different business operations. It helps in improving the quality of work.

Organisational capacity or learning and growth: Under this, the main aim is to enhance

the capacity of an organisation with the help of using human capital, infrastructure,

technology, culture and other capacities (Ward, 2012).

Just in time: It is an effective inventory strategy in which the management place an

order of inventory only when they are needed in the production process thus it helps in reducing

inventory cost. For this, the management need to first forecast the demand and accordingly

ordered material to fulfil customer's needs and requirements. It directly make an impact on the

profitability and productivity of company and respond the financial problems more effectively (.

Management accounting and its importance, 2017).

Comparison among Tech (UK) Limited and 4Com Plc

Tech (UK) Limited 4Com Plc.

Such company deals in providing special

charger of mobile phones and others gadgets.

Such company are also deals in providing

business communication products to

customers.

Evaluation of useful data can be done on the

basis of historical and present year

performances.

The manager of company need to use KPI in

order to measure performance of employees.

The management of company need to apply

Balance scorecard approach in order to

eliminate issues and problems and enhance the

existing performance.

The management of company need to evaluate

financial data in order to reduce financial

problems.

M4.

Tech (UK) Limited facing huge losses due to which they may lose its competitive

position in market. Thus, the management ned to properly analysis such financial problems and

14

product to customers in order to maximise their level of satisfaction. This will help

company in retaining loyal customers for longer period of time. Internal process: Under this, the main aim is to develop internal process through bring

efficiency in the different business operations. It helps in improving the quality of work.

Organisational capacity or learning and growth: Under this, the main aim is to enhance

the capacity of an organisation with the help of using human capital, infrastructure,

technology, culture and other capacities (Ward, 2012).

Just in time: It is an effective inventory strategy in which the management place an

order of inventory only when they are needed in the production process thus it helps in reducing

inventory cost. For this, the management need to first forecast the demand and accordingly

ordered material to fulfil customer's needs and requirements. It directly make an impact on the

profitability and productivity of company and respond the financial problems more effectively (.

Management accounting and its importance, 2017).

Comparison among Tech (UK) Limited and 4Com Plc

Tech (UK) Limited 4Com Plc.

Such company deals in providing special

charger of mobile phones and others gadgets.

Such company are also deals in providing

business communication products to

customers.

Evaluation of useful data can be done on the

basis of historical and present year

performances.

The manager of company need to use KPI in

order to measure performance of employees.

The management of company need to apply

Balance scorecard approach in order to

eliminate issues and problems and enhance the

existing performance.

The management of company need to evaluate

financial data in order to reduce financial

problems.

M4.

Tech (UK) Limited facing huge losses due to which they may lose its competitive

position in market. Thus, the management ned to properly analysis such financial problems and

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

accordingly adopt various financial tools such as KPI, Balance scorecard approach etc. in order

to resolve them in an effective and efficient manner.

CONCLUSION

It has been concluded from the above project report that management accounting and

reporting system plays a valuable role in achieving growth and success of an organisation

through providing relevant and important information related with financial as well as non-

financial. There are various financial tools such KPI, Balance scorecard, just in time etc. which

help an organisation in resolving all financial issues or problems. The management is required to

focus on preparing different budgets and using various costing methods in order to calculate total

cost of production.

REFERENCES

Books and Journals

15

to resolve them in an effective and efficient manner.

CONCLUSION

It has been concluded from the above project report that management accounting and

reporting system plays a valuable role in achieving growth and success of an organisation

through providing relevant and important information related with financial as well as non-

financial. There are various financial tools such KPI, Balance scorecard, just in time etc. which

help an organisation in resolving all financial issues or problems. The management is required to

focus on preparing different budgets and using various costing methods in order to calculate total

cost of production.

REFERENCES

Books and Journals

15

Online:

16

16

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.