Comprehensive Cost Analysis Report: Intel Semiconductor, MACB Module

VerifiedAdded on 2021/05/19

|54

|17621

|291

Report

AI Summary

This report provides a comprehensive cost analysis of Intel Semiconductor, examining cost classifications (direct, indirect, fixed, variable), and applying various costing techniques such as absorption costing, marginal costing, Activity-Based Costing (ABC), FIFO, and LIFO methods. It delves into the identification and analysis of cost information within the company, exploring different cost classifications and behaviors. The report also calculates costs for products C1 and C2 using appropriate techniques and analyzes cost data using one, two, and three-dimensional diagrams. Furthermore, it utilizes performance indicators to identify potential improvements and recommends strategies for cost reduction, enhancing value, and implementing Total Quality Management (TQM) to optimize financial performance. The conclusion summarizes the key findings and recommendations for improving cost management and overall efficiency within Intel Semiconductor.

MACB - 1 Prepared by

Table of Contents

I. Introduction.......................................................................................................................................................2

II. Identify and analyse the cost information within Intel Semiconductor Ltd................................................2

1. Using the cost classifications to classify different categories of cost incurred in Intel

Semiconductor.........................................................................................................................................................2

Direct costs............................................................................................................................. 4

Indirect costs.......................................................................................................................... 4

Fixed costs............................................................................................................................. 7

Variable costs......................................................................................................................... 7

Semi-variable costs................................................................................................................ 8

Step costs............................................................................................................................... 9

Product costs........................................................................................................................ 10

Period costs.......................................................................................................................... 10

2. Apply different costing techniques on the given information for Intel Semiconductor.......................11

Absorption costing................................................................................................................ 14

Marginal costing:..................................................................................................................16

3. Using appropriate techniques to calculate costs for product C1 and C2............................................19

Activity Based Costing (ABC) method...............................................................................19

Standard costing............................................................................................................... 24

FIFO method (First in, First out)........................................................................................25

LIFO method (Last in, First out).........................................................................................26

4. Using appropriate techniques to analyse the cost data on the basis of above cost classification. .28

One dimensional/direction diagrams.................................................................................28

Two-dimensional diagrams................................................................................................28

Three-dimensional diagrams.............................................................................................28

5. Utilize performance indicators to find out the potential improvements...............................................37

6. The recommendation for improvements to reduce costs, appreciate the value and quality................44

Cost reduction................................................................................................................... 44

Enhancing value................................................................................................................ 45

Total Quality Management................................................................................................49

III. Conclusion......................................................................................................................................................52

IV. Reference........................................................................................................................................................53

I. Introduction

1

Table of Contents

I. Introduction.......................................................................................................................................................2

II. Identify and analyse the cost information within Intel Semiconductor Ltd................................................2

1. Using the cost classifications to classify different categories of cost incurred in Intel

Semiconductor.........................................................................................................................................................2

Direct costs............................................................................................................................. 4

Indirect costs.......................................................................................................................... 4

Fixed costs............................................................................................................................. 7

Variable costs......................................................................................................................... 7

Semi-variable costs................................................................................................................ 8

Step costs............................................................................................................................... 9

Product costs........................................................................................................................ 10

Period costs.......................................................................................................................... 10

2. Apply different costing techniques on the given information for Intel Semiconductor.......................11

Absorption costing................................................................................................................ 14

Marginal costing:..................................................................................................................16

3. Using appropriate techniques to calculate costs for product C1 and C2............................................19

Activity Based Costing (ABC) method...............................................................................19

Standard costing............................................................................................................... 24

FIFO method (First in, First out)........................................................................................25

LIFO method (Last in, First out).........................................................................................26

4. Using appropriate techniques to analyse the cost data on the basis of above cost classification. .28

One dimensional/direction diagrams.................................................................................28

Two-dimensional diagrams................................................................................................28

Three-dimensional diagrams.............................................................................................28

5. Utilize performance indicators to find out the potential improvements...............................................37

6. The recommendation for improvements to reduce costs, appreciate the value and quality................44

Cost reduction................................................................................................................... 44

Enhancing value................................................................................................................ 45

Total Quality Management................................................................................................49

III. Conclusion......................................................................................................................................................52

IV. Reference........................................................................................................................................................53

I. Introduction

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MACB - 1 Prepared by

In fact, each and every company needs accounting to manage their costs and budgets. Intel

Semiconductor is also no exception. From that point, this report will show how the company

apply Cost Classification to categorize each of their costs into Cost behaviour (Fixed or

Variable) and Management function (Direct or Indirect).

Moreover, in order to value its stock, the report will try to apply both LIFO and FIFO methods for

Intel Semiconductor so that the company can easily choose the most appropriate one.

Besides, this report will also emphasize on Marginal and Absorption costing then

recommending the better method to be applied into the company to reduce tax liability. In

addition, process costing, standard costing, AVCO method, TQM, KPIs will also be introduced

in this report.

II. Identify and analyse the cost information within Intel Semiconductor Ltd.

1. Using the cost classifications to classify different categories of cost incurred in

Intel Semiconductor

There are two main types of accounting including: Management Accounting and Financial

Accounting.

Management Accounting is on the behalf of internal activities, which specifically relate to the

careful calculation of the costs incurred in the company so that Intel Semiconductor can easily

analyse them and based on these results, they can anticipate what will happen in the

forthcoming period. Since then, due to this, the company can improve and fix the situation so

that it can easily increase profits once increasing the productivity effectively. For instance, in

Intel Semiconductor, the company can apply management accounting to foresee how cost will

increase in the next period in terms of the costs for health, welfare system to ensure the fitness

of its human resources, or the level of increase or decrease of some production activities. Since

then, Intel can easily find out the most effective way to balance all the changes in such costs

and then remain the stable situation for the company. Furthermore, as it is just related to

internal activities and operations, Management Accounting can be flexible rather than ensuring

the strict rules and regulations.

In contrast, financial accounting is on the behalf of external activities and instead of predicting

what is going on in the forthcoming period, financial accounting is applied to record, summarise

and analyse the costs that incurred in the past. Besides, as it is referred to the outside activities

of the organization, this type of accounting relate directly to external stakeholders rather than

2

In fact, each and every company needs accounting to manage their costs and budgets. Intel

Semiconductor is also no exception. From that point, this report will show how the company

apply Cost Classification to categorize each of their costs into Cost behaviour (Fixed or

Variable) and Management function (Direct or Indirect).

Moreover, in order to value its stock, the report will try to apply both LIFO and FIFO methods for

Intel Semiconductor so that the company can easily choose the most appropriate one.

Besides, this report will also emphasize on Marginal and Absorption costing then

recommending the better method to be applied into the company to reduce tax liability. In

addition, process costing, standard costing, AVCO method, TQM, KPIs will also be introduced

in this report.

II. Identify and analyse the cost information within Intel Semiconductor Ltd.

1. Using the cost classifications to classify different categories of cost incurred in

Intel Semiconductor

There are two main types of accounting including: Management Accounting and Financial

Accounting.

Management Accounting is on the behalf of internal activities, which specifically relate to the

careful calculation of the costs incurred in the company so that Intel Semiconductor can easily

analyse them and based on these results, they can anticipate what will happen in the

forthcoming period. Since then, due to this, the company can improve and fix the situation so

that it can easily increase profits once increasing the productivity effectively. For instance, in

Intel Semiconductor, the company can apply management accounting to foresee how cost will

increase in the next period in terms of the costs for health, welfare system to ensure the fitness

of its human resources, or the level of increase or decrease of some production activities. Since

then, Intel can easily find out the most effective way to balance all the changes in such costs

and then remain the stable situation for the company. Furthermore, as it is just related to

internal activities and operations, Management Accounting can be flexible rather than ensuring

the strict rules and regulations.

In contrast, financial accounting is on the behalf of external activities and instead of predicting

what is going on in the forthcoming period, financial accounting is applied to record, summarise

and analyse the costs that incurred in the past. Besides, as it is referred to the outside activities

of the organization, this type of accounting relate directly to external stakeholders rather than

2

MACB - 1 Prepared by

internal ones like the first mentioned types of accounting, it includes customers, government,

bank, creditor, debtor, distributor, supplier, etc.

In this report, the main ideas will be emphasised on the first type that mentioned above,

management accounting.

As for business, cost is actually important. In fact, each and every business needs to calculate

the amount that they have to be paid or given up in order to get something. In other words, cost

in business is usually a monetary valuation of its effort, material, labour, time and other

resources or risk incurred as well as opportunity forgone in production and the delivery of

products or services. Therefore, controlling the cost effectively helps businesses achieve their

objectives easily. However, the question here is how to keep control of unexpected changes.

This is the issue that is concerned solely by most of businesses. Intel Semiconductor is also no

exception. In order to control the cost, one of the most important things this technological

company needs to do is to classify all of their incurred cost which related to three elements as

follows:

o Materials

o Labours

o Other expenses

First of all, the cost can be classified as follows:

3

internal ones like the first mentioned types of accounting, it includes customers, government,

bank, creditor, debtor, distributor, supplier, etc.

In this report, the main ideas will be emphasised on the first type that mentioned above,

management accounting.

As for business, cost is actually important. In fact, each and every business needs to calculate

the amount that they have to be paid or given up in order to get something. In other words, cost

in business is usually a monetary valuation of its effort, material, labour, time and other

resources or risk incurred as well as opportunity forgone in production and the delivery of

products or services. Therefore, controlling the cost effectively helps businesses achieve their

objectives easily. However, the question here is how to keep control of unexpected changes.

This is the issue that is concerned solely by most of businesses. Intel Semiconductor is also no

exception. In order to control the cost, one of the most important things this technological

company needs to do is to classify all of their incurred cost which related to three elements as

follows:

o Materials

o Labours

o Other expenses

First of all, the cost can be classified as follows:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MACB - 1 Prepared by

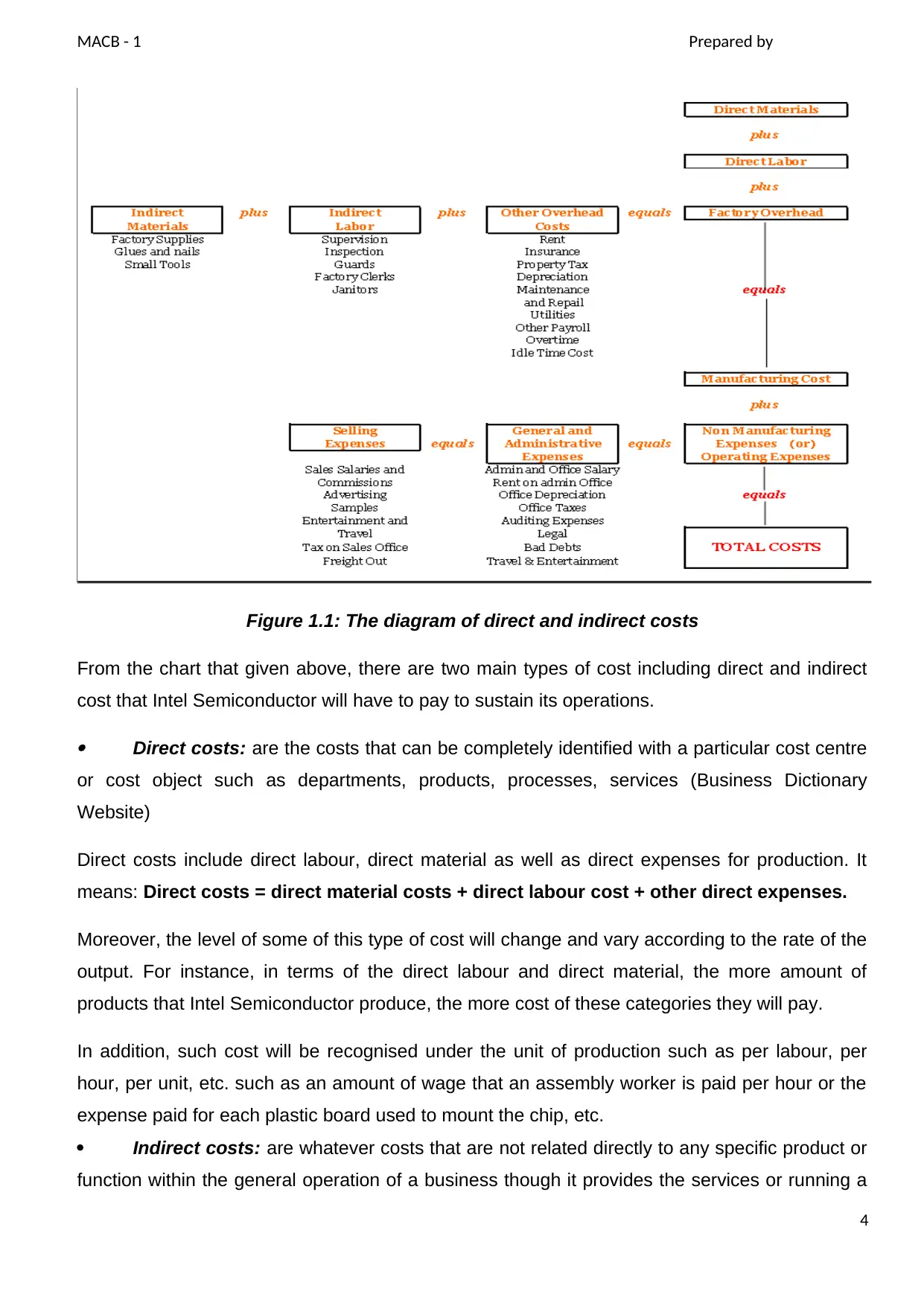

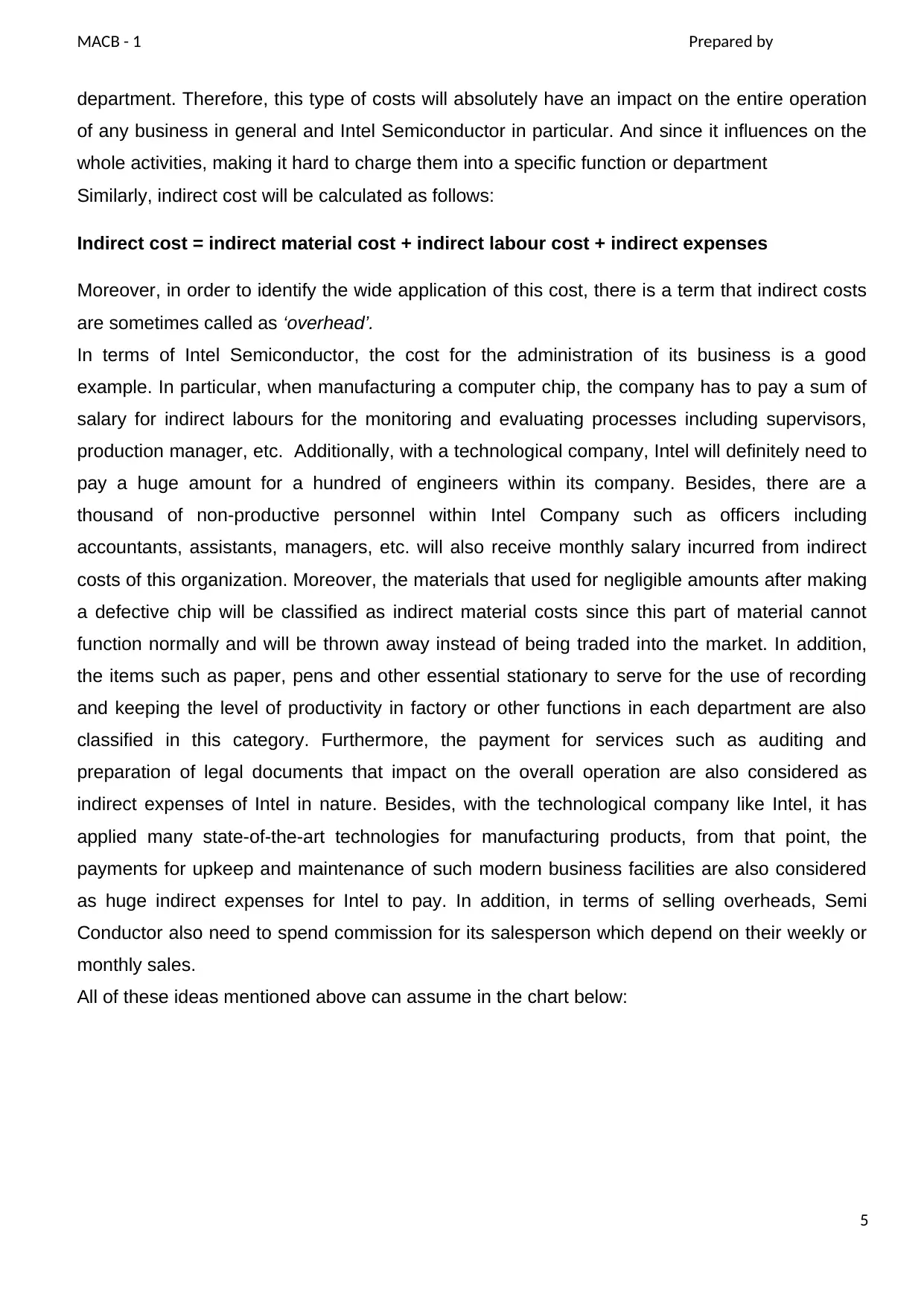

Figure 1.1: The diagram of direct and indirect costs

From the chart that given above, there are two main types of cost including direct and indirect

cost that Intel Semiconductor will have to pay to sustain its operations.

Direct costs: are the costs that can be completely identified with a particular cost centre

or cost object such as departments, products, processes, services (Business Dictionary

Website)

Direct costs include direct labour, direct material as well as direct expenses for production. It

means: Direct costs = direct material costs + direct labour cost + other direct expenses.

Moreover, the level of some of this type of cost will change and vary according to the rate of the

output. For instance, in terms of the direct labour and direct material, the more amount of

products that Intel Semiconductor produce, the more cost of these categories they will pay.

In addition, such cost will be recognised under the unit of production such as per labour, per

hour, per unit, etc. such as an amount of wage that an assembly worker is paid per hour or the

expense paid for each plastic board used to mount the chip, etc.

Indirect costs: are whatever costs that are not related directly to any specific product or

function within the general operation of a business though it provides the services or running a

4

Figure 1.1: The diagram of direct and indirect costs

From the chart that given above, there are two main types of cost including direct and indirect

cost that Intel Semiconductor will have to pay to sustain its operations.

Direct costs: are the costs that can be completely identified with a particular cost centre

or cost object such as departments, products, processes, services (Business Dictionary

Website)

Direct costs include direct labour, direct material as well as direct expenses for production. It

means: Direct costs = direct material costs + direct labour cost + other direct expenses.

Moreover, the level of some of this type of cost will change and vary according to the rate of the

output. For instance, in terms of the direct labour and direct material, the more amount of

products that Intel Semiconductor produce, the more cost of these categories they will pay.

In addition, such cost will be recognised under the unit of production such as per labour, per

hour, per unit, etc. such as an amount of wage that an assembly worker is paid per hour or the

expense paid for each plastic board used to mount the chip, etc.

Indirect costs: are whatever costs that are not related directly to any specific product or

function within the general operation of a business though it provides the services or running a

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MACB - 1 Prepared by

department. Therefore, this type of costs will absolutely have an impact on the entire operation

of any business in general and Intel Semiconductor in particular. And since it influences on the

whole activities, making it hard to charge them into a specific function or department

Similarly, indirect cost will be calculated as follows:

Indirect cost = indirect material cost + indirect labour cost + indirect expenses

Moreover, in order to identify the wide application of this cost, there is a term that indirect costs

are sometimes called as ‘overhead’.

In terms of Intel Semiconductor, the cost for the administration of its business is a good

example. In particular, when manufacturing a computer chip, the company has to pay a sum of

salary for indirect labours for the monitoring and evaluating processes including supervisors,

production manager, etc. Additionally, with a technological company, Intel will definitely need to

pay a huge amount for a hundred of engineers within its company. Besides, there are a

thousand of non-productive personnel within Intel Company such as officers including

accountants, assistants, managers, etc. will also receive monthly salary incurred from indirect

costs of this organization. Moreover, the materials that used for negligible amounts after making

a defective chip will be classified as indirect material costs since this part of material cannot

function normally and will be thrown away instead of being traded into the market. In addition,

the items such as paper, pens and other essential stationary to serve for the use of recording

and keeping the level of productivity in factory or other functions in each department are also

classified in this category. Furthermore, the payment for services such as auditing and

preparation of legal documents that impact on the overall operation are also considered as

indirect expenses of Intel in nature. Besides, with the technological company like Intel, it has

applied many state-of-the-art technologies for manufacturing products, from that point, the

payments for upkeep and maintenance of such modern business facilities are also considered

as huge indirect expenses for Intel to pay. In addition, in terms of selling overheads, Semi

Conductor also need to spend commission for its salesperson which depend on their weekly or

monthly sales.

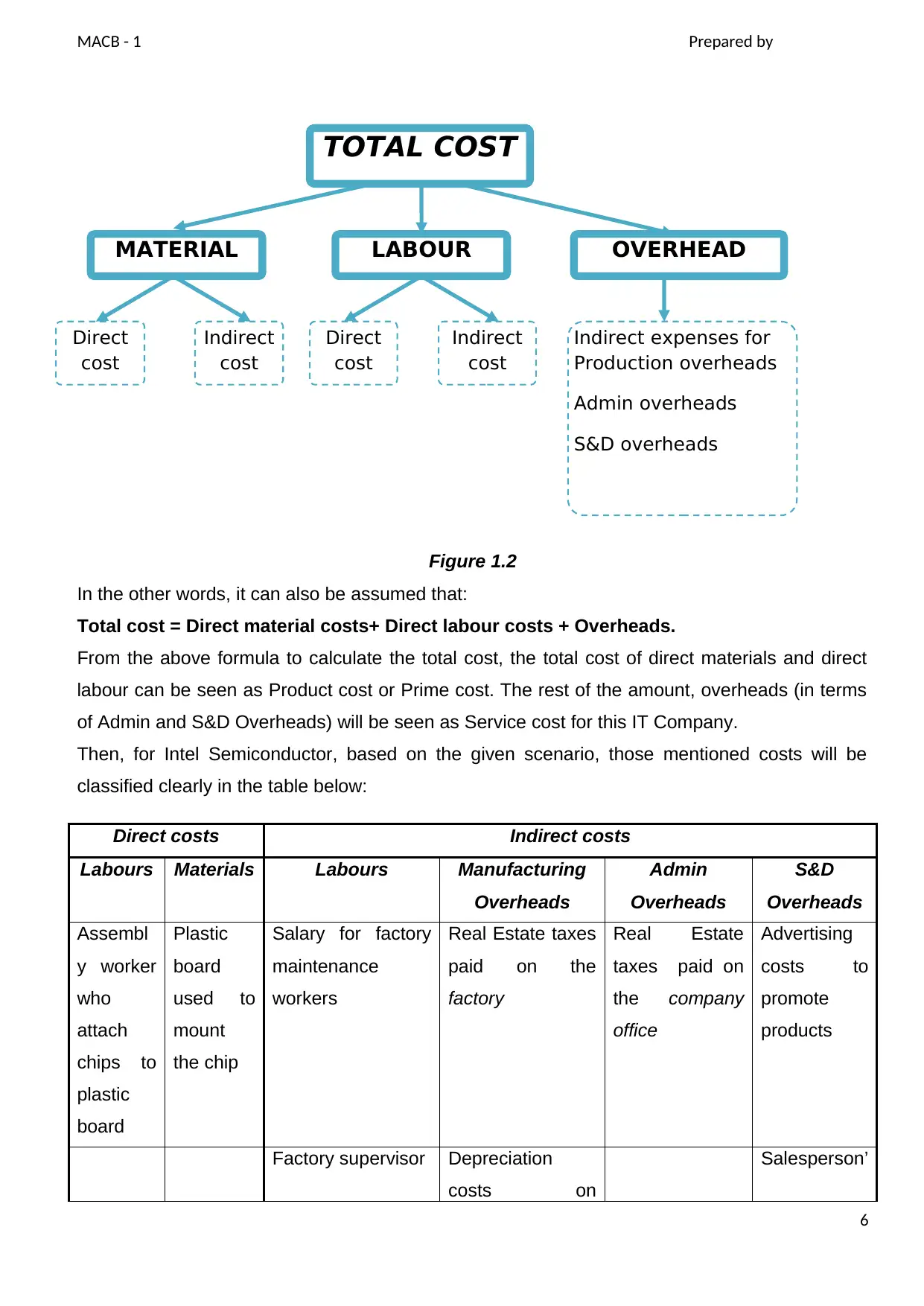

All of these ideas mentioned above can assume in the chart below:

5

department. Therefore, this type of costs will absolutely have an impact on the entire operation

of any business in general and Intel Semiconductor in particular. And since it influences on the

whole activities, making it hard to charge them into a specific function or department

Similarly, indirect cost will be calculated as follows:

Indirect cost = indirect material cost + indirect labour cost + indirect expenses

Moreover, in order to identify the wide application of this cost, there is a term that indirect costs

are sometimes called as ‘overhead’.

In terms of Intel Semiconductor, the cost for the administration of its business is a good

example. In particular, when manufacturing a computer chip, the company has to pay a sum of

salary for indirect labours for the monitoring and evaluating processes including supervisors,

production manager, etc. Additionally, with a technological company, Intel will definitely need to

pay a huge amount for a hundred of engineers within its company. Besides, there are a

thousand of non-productive personnel within Intel Company such as officers including

accountants, assistants, managers, etc. will also receive monthly salary incurred from indirect

costs of this organization. Moreover, the materials that used for negligible amounts after making

a defective chip will be classified as indirect material costs since this part of material cannot

function normally and will be thrown away instead of being traded into the market. In addition,

the items such as paper, pens and other essential stationary to serve for the use of recording

and keeping the level of productivity in factory or other functions in each department are also

classified in this category. Furthermore, the payment for services such as auditing and

preparation of legal documents that impact on the overall operation are also considered as

indirect expenses of Intel in nature. Besides, with the technological company like Intel, it has

applied many state-of-the-art technologies for manufacturing products, from that point, the

payments for upkeep and maintenance of such modern business facilities are also considered

as huge indirect expenses for Intel to pay. In addition, in terms of selling overheads, Semi

Conductor also need to spend commission for its salesperson which depend on their weekly or

monthly sales.

All of these ideas mentioned above can assume in the chart below:

5

MACB - 1 Prepared by

Figure 1.2

In the other words, it can also be assumed that:

Total cost = Direct material costs+ Direct labour costs + Overheads.

From the above formula to calculate the total cost, the total cost of direct materials and direct

labour can be seen as Product cost or Prime cost. The rest of the amount, overheads (in terms

of Admin and S&D Overheads) will be seen as Service cost for this IT Company.

Then, for Intel Semiconductor, based on the given scenario, those mentioned costs will be

classified clearly in the table below:

Direct costs Indirect costs

Labours Materials Labours Manufacturing

Overheads

Admin

Overheads

S&D

Overheads

Assembl

y worker

who

attach

chips to

plastic

board

Plastic

board

used to

mount

the chip

Salary for factory

maintenance

workers

Real Estate taxes

paid on the

factory

Real Estate

taxes paid on

the company

office

Advertising

costs to

promote

products

Factory supervisor Depreciation

costs on

Salesperson’

6

MATERIAL OVERHEADLABOUR

Direct

cost

Direct

cost

Indirect

cost

Indirect

cost

Indirect expenses for

Production overheads

Admin overheads

S&D overheads

TOTAL COST

Figure 1.2

In the other words, it can also be assumed that:

Total cost = Direct material costs+ Direct labour costs + Overheads.

From the above formula to calculate the total cost, the total cost of direct materials and direct

labour can be seen as Product cost or Prime cost. The rest of the amount, overheads (in terms

of Admin and S&D Overheads) will be seen as Service cost for this IT Company.

Then, for Intel Semiconductor, based on the given scenario, those mentioned costs will be

classified clearly in the table below:

Direct costs Indirect costs

Labours Materials Labours Manufacturing

Overheads

Admin

Overheads

S&D

Overheads

Assembl

y worker

who

attach

chips to

plastic

board

Plastic

board

used to

mount

the chip

Salary for factory

maintenance

workers

Real Estate taxes

paid on the

factory

Real Estate

taxes paid on

the company

office

Advertising

costs to

promote

products

Factory supervisor Depreciation

costs on

Salesperson’

6

MATERIAL OVERHEADLABOUR

Direct

cost

Direct

cost

Indirect

cost

Indirect

cost

Indirect expenses for

Production overheads

Admin overheads

S&D overheads

TOTAL COST

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MACB - 1 Prepared by

machinery commissions

Salary for the chief

financial officer

From the above table, there are only two direct costs including the assembly workers and

plastic boards. The rest of them are overheads in terms of manufacturing, selling and

administration overheads.

Secondly, based on Cost behaviour, apart from the above classification, cost can also be

classified into three other small groups including fix, variable and semi-variable costs. Let’s

have a look to examine the characteristics of each single group as follows:

Fixed costs: are the costs that do not vary or depend on the increase or decrease of

production or the level of other operations. It tends to be time-related such as the monthly

salaries or payments of rent and often relate to the overhead costs. For instance, Intel

Semiconductor will need to pay salaries for officers, accountants, managers, etc. no matter how

high level in sales or productions.Besides, the expenses for advertising, marketing, R&D after

manufacturing chips are also a good example for fixed costs that this company has to pay.

However, this type of costs is not permanently fixed at all, they may change over time, they just

fix in relation to the quantity of production in the relevant period. For example, Intel

Semiconductor will need to pay just a fixed amount of renting for their ware houses within the

period that they signed in the contract with the owner.

Variable costs: is in contrast to fixed costs as such variable costs are changed in

proportion to the activity of a business.This type of costs is sometimes called unit-level costs as

they vary with the number of units produced (Wikipedia Website). Let’s take an example of the

payment of labour in Intel Semiconductor, when the activity is decreased, fewer labours are

needed, so the spending for labours falls. By contrast, once the level of operation in factory is

increased as the demand for computer chips grows unexpectedly, the number of labours

needed to manufacture will definitely increase, it is when the spending for labours is higher than

the previous mentioned period.

7

machinery commissions

Salary for the chief

financial officer

From the above table, there are only two direct costs including the assembly workers and

plastic boards. The rest of them are overheads in terms of manufacturing, selling and

administration overheads.

Secondly, based on Cost behaviour, apart from the above classification, cost can also be

classified into three other small groups including fix, variable and semi-variable costs. Let’s

have a look to examine the characteristics of each single group as follows:

Fixed costs: are the costs that do not vary or depend on the increase or decrease of

production or the level of other operations. It tends to be time-related such as the monthly

salaries or payments of rent and often relate to the overhead costs. For instance, Intel

Semiconductor will need to pay salaries for officers, accountants, managers, etc. no matter how

high level in sales or productions.Besides, the expenses for advertising, marketing, R&D after

manufacturing chips are also a good example for fixed costs that this company has to pay.

However, this type of costs is not permanently fixed at all, they may change over time, they just

fix in relation to the quantity of production in the relevant period. For example, Intel

Semiconductor will need to pay just a fixed amount of renting for their ware houses within the

period that they signed in the contract with the owner.

Variable costs: is in contrast to fixed costs as such variable costs are changed in

proportion to the activity of a business.This type of costs is sometimes called unit-level costs as

they vary with the number of units produced (Wikipedia Website). Let’s take an example of the

payment of labour in Intel Semiconductor, when the activity is decreased, fewer labours are

needed, so the spending for labours falls. By contrast, once the level of operation in factory is

increased as the demand for computer chips grows unexpectedly, the number of labours

needed to manufacture will definitely increase, it is when the spending for labours is higher than

the previous mentioned period.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MACB - 1 Prepared by

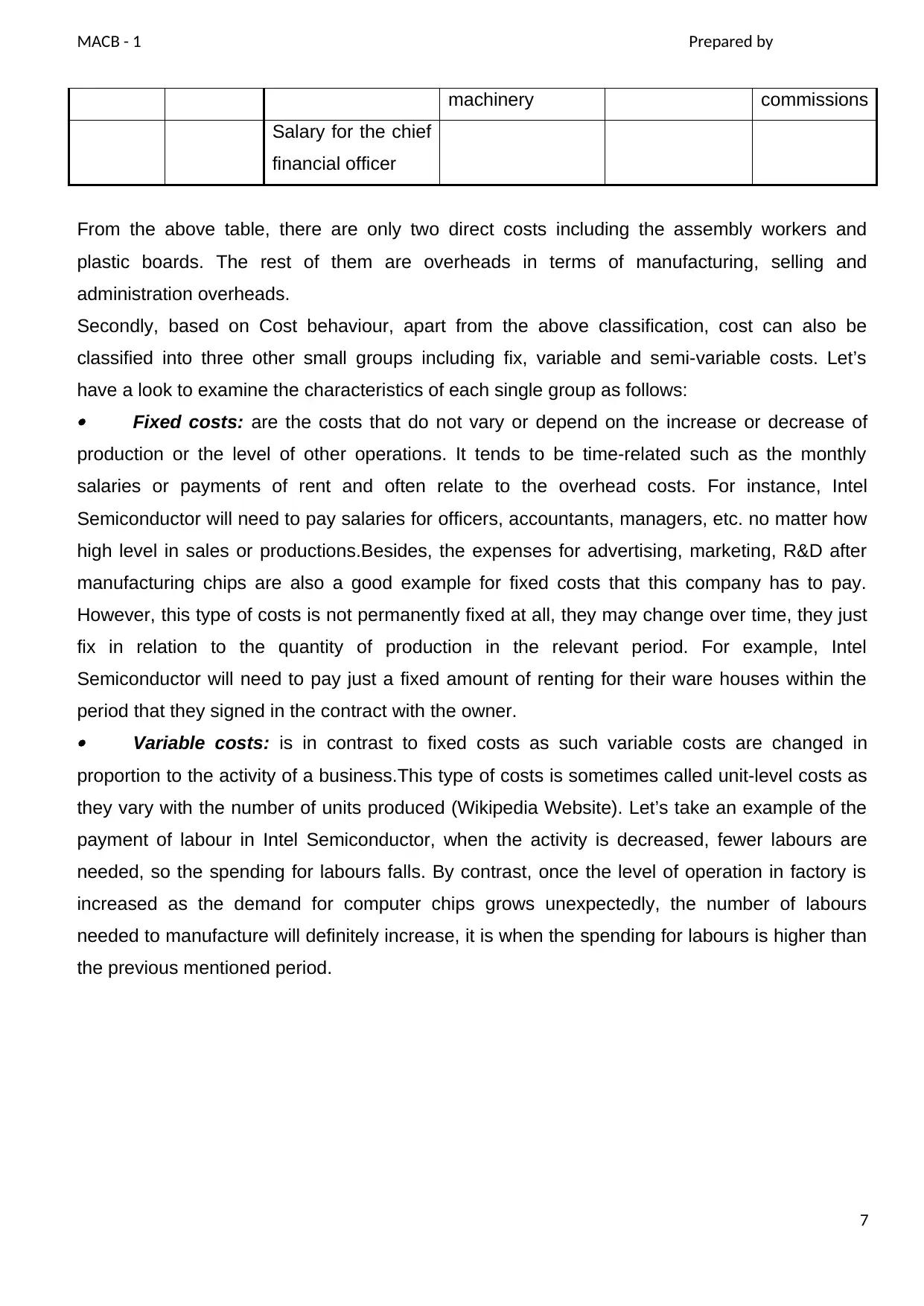

Figure 1.3

(Source: Wikipedia)

From the chart, the horizontal line shows the amount of fixed costs and the going-up line

represent for variable costs. It is easy to figure out that fixed costs and variable costs made up

the two components of total costs. Direct costs, can be easily associated with a particular cost

object. However, not all variable costs are direct costs. In Intel Semiconductor, for example, the

commissions for salespersons are variable and increase according to the higher number of

goods sold, but it is seen as indirect expense for the company.

Semi-variable costs: are expenses that consist of the mix characteristics of both fixed

costs and variable costs (Wikipedia Website). In fact, the fixed cost element is a part of the cost

that needs to be paid without considering or being influenced by the level of activity. On the

other hand, the variable component of the cost is considered as a payable amount according to

the proportion of the level of activity. For example, Intel Semiconductor will pay for maintenance

fees in each period regardless of how much power gets used. It shows similarities to some

electrical equipment such as air conditioning, lighting, etc. They also may be kept running even

in periods of low activity. In this period, these expenses can be classified as fixed. However,

beyond this, the company will use electricity to run machinery or other plants as required. Since

then, when the output is experienced changes, the demand ramps up, therefore the busier the

company, the more power will be required and run. For this reason, the more electricity gets

used as the cost of electrical energy will rise accordingly as the production activities increase.

This extra expense can be regarded as variable. Another example is salaries for salesperson

who receive commissions. Although this group is paid on a fixed salary, they still can get reward

(which is regarded as variable) based on the volume of sales that they achieved

In the given scenario about Intel Semiconductor, those costs can also be classified into these

mentioned categories of costs based on Cost behaviour as follows:

8

Figure 1.3

(Source: Wikipedia)

From the chart, the horizontal line shows the amount of fixed costs and the going-up line

represent for variable costs. It is easy to figure out that fixed costs and variable costs made up

the two components of total costs. Direct costs, can be easily associated with a particular cost

object. However, not all variable costs are direct costs. In Intel Semiconductor, for example, the

commissions for salespersons are variable and increase according to the higher number of

goods sold, but it is seen as indirect expense for the company.

Semi-variable costs: are expenses that consist of the mix characteristics of both fixed

costs and variable costs (Wikipedia Website). In fact, the fixed cost element is a part of the cost

that needs to be paid without considering or being influenced by the level of activity. On the

other hand, the variable component of the cost is considered as a payable amount according to

the proportion of the level of activity. For example, Intel Semiconductor will pay for maintenance

fees in each period regardless of how much power gets used. It shows similarities to some

electrical equipment such as air conditioning, lighting, etc. They also may be kept running even

in periods of low activity. In this period, these expenses can be classified as fixed. However,

beyond this, the company will use electricity to run machinery or other plants as required. Since

then, when the output is experienced changes, the demand ramps up, therefore the busier the

company, the more power will be required and run. For this reason, the more electricity gets

used as the cost of electrical energy will rise accordingly as the production activities increase.

This extra expense can be regarded as variable. Another example is salaries for salesperson

who receive commissions. Although this group is paid on a fixed salary, they still can get reward

(which is regarded as variable) based on the volume of sales that they achieved

In the given scenario about Intel Semiconductor, those costs can also be classified into these

mentioned categories of costs based on Cost behaviour as follows:

8

MACB - 1 Prepared by

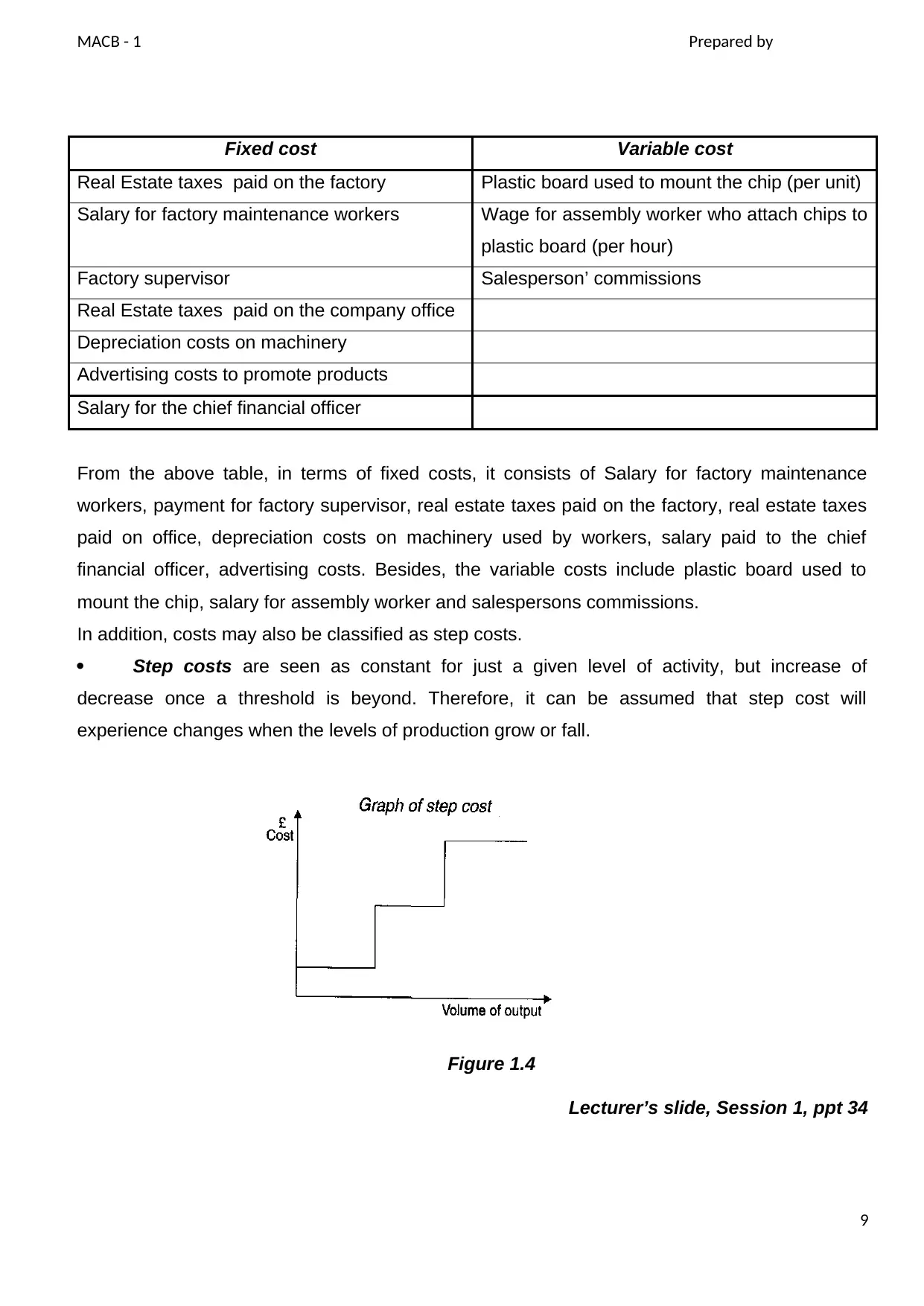

Fixed cost Variable cost

Real Estate taxes paid on the factory Plastic board used to mount the chip (per unit)

Salary for factory maintenance workers Wage for assembly worker who attach chips to

plastic board (per hour)

Factory supervisor Salesperson’ commissions

Real Estate taxes paid on the company office

Depreciation costs on machinery

Advertising costs to promote products

Salary for the chief financial officer

From the above table, in terms of fixed costs, it consists of Salary for factory maintenance

workers, payment for factory supervisor, real estate taxes paid on the factory, real estate taxes

paid on office, depreciation costs on machinery used by workers, salary paid to the chief

financial officer, advertising costs. Besides, the variable costs include plastic board used to

mount the chip, salary for assembly worker and salespersons commissions.

In addition, costs may also be classified as step costs.

Step costs are seen as constant for just a given level of activity, but increase of

decrease once a threshold is beyond. Therefore, it can be assumed that step cost will

experience changes when the levels of production grow or fall.

Lecturer’s slide, Session 1, ppt 34

9

Figure 1.4

Fixed cost Variable cost

Real Estate taxes paid on the factory Plastic board used to mount the chip (per unit)

Salary for factory maintenance workers Wage for assembly worker who attach chips to

plastic board (per hour)

Factory supervisor Salesperson’ commissions

Real Estate taxes paid on the company office

Depreciation costs on machinery

Advertising costs to promote products

Salary for the chief financial officer

From the above table, in terms of fixed costs, it consists of Salary for factory maintenance

workers, payment for factory supervisor, real estate taxes paid on the factory, real estate taxes

paid on office, depreciation costs on machinery used by workers, salary paid to the chief

financial officer, advertising costs. Besides, the variable costs include plastic board used to

mount the chip, salary for assembly worker and salespersons commissions.

In addition, costs may also be classified as step costs.

Step costs are seen as constant for just a given level of activity, but increase of

decrease once a threshold is beyond. Therefore, it can be assumed that step cost will

experience changes when the levels of production grow or fall.

Lecturer’s slide, Session 1, ppt 34

9

Figure 1.4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MACB - 1 Prepared by

One good example for Intel Semiconductor in this step of cost is the number of labour. In

particular, the factory may need 200 workers to assemble 1000 units of product. If the company

just need to manufacture from 0 to 1000 units at that time, they will only need to pay the cost of

having 200 workers. However, if Intel Semiconductor starts to provide 2000 units of product for

its customers, the company must hire 100 more workers, increasing its costs of doing business.

Furthermore, costs can also be classified into two other main types including Product costs and

Period costs.

Product costs: are costs consist of direct labour, direct material and manufacturing overheads

that are consumed to create a finished product. In Intel Semiconductor, Product costs include:

o Wage for assembly worker who attach chips to plastic board (per hour) (Direct labour)

o Plastic board used to mount the chip (per unit) (Direct material)

o Real Estate taxes paid on the factory (Manufacturing overhead)

o Depreciation costs on machinery (Manufacturing overhead)

Moreover, the cost of a product on a unit basis is typically compiled the costs associated with a

batch of units, and dividing by the number of units manufactured. The calculation is

Totaldirectlabour +Totaldirectmaterials+Totalallocatedoverhead

Totalnumberofunits =Product unit cost

Period costs: are more closely associated with the duration of time rather than with the event

of activity. As it is charged to expenses at once, it may more appropriately be called a period

expense. This type of cost is not included within the cost of goods sold on the income

statement. Instead, it is typically included the administrative, S&D expenses, etc.

(AccountingTools Website)

In terms of Semiconductor, from the scenario, the company has already paid for advertising

costs to promote and spread its products more widely.

To sum up, as cost is important for each and every business around the world, it is

necessary for Semi Conductors to classify all of its costs so that the company can

effectively anticipate unexpected changes in their expenses in the forthcoming period.

Besides, thanks to the above part of this report, this IT Company can also calculate

easily all the incurred costs by using their accounting calculation and then, find out its

exact revenues, profits.

10

One good example for Intel Semiconductor in this step of cost is the number of labour. In

particular, the factory may need 200 workers to assemble 1000 units of product. If the company

just need to manufacture from 0 to 1000 units at that time, they will only need to pay the cost of

having 200 workers. However, if Intel Semiconductor starts to provide 2000 units of product for

its customers, the company must hire 100 more workers, increasing its costs of doing business.

Furthermore, costs can also be classified into two other main types including Product costs and

Period costs.

Product costs: are costs consist of direct labour, direct material and manufacturing overheads

that are consumed to create a finished product. In Intel Semiconductor, Product costs include:

o Wage for assembly worker who attach chips to plastic board (per hour) (Direct labour)

o Plastic board used to mount the chip (per unit) (Direct material)

o Real Estate taxes paid on the factory (Manufacturing overhead)

o Depreciation costs on machinery (Manufacturing overhead)

Moreover, the cost of a product on a unit basis is typically compiled the costs associated with a

batch of units, and dividing by the number of units manufactured. The calculation is

Totaldirectlabour +Totaldirectmaterials+Totalallocatedoverhead

Totalnumberofunits =Product unit cost

Period costs: are more closely associated with the duration of time rather than with the event

of activity. As it is charged to expenses at once, it may more appropriately be called a period

expense. This type of cost is not included within the cost of goods sold on the income

statement. Instead, it is typically included the administrative, S&D expenses, etc.

(AccountingTools Website)

In terms of Semiconductor, from the scenario, the company has already paid for advertising

costs to promote and spread its products more widely.

To sum up, as cost is important for each and every business around the world, it is

necessary for Semi Conductors to classify all of its costs so that the company can

effectively anticipate unexpected changes in their expenses in the forthcoming period.

Besides, thanks to the above part of this report, this IT Company can also calculate

easily all the incurred costs by using their accounting calculation and then, find out its

exact revenues, profits.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MACB - 1 Prepared by

2. Apply different costing techniques on the given information for Intel

Semiconductor

Costing methods are accounting techniques used to help organizations understand the value of

inputs and outputs in the process of manufacturing. By recording and categorizing this data and

information according to a rigorous accounting system, the organization can determine with a

high degree of accuracy the cost per unit of production as well as make other key performance

indicators. Besides, management needs this information in order to make informed decisions

about production levels, pricing, competitive strategy, future investment, etc. This report will

mention three costing methods including: Process costing, Absorption & Marginal costing

Process costing

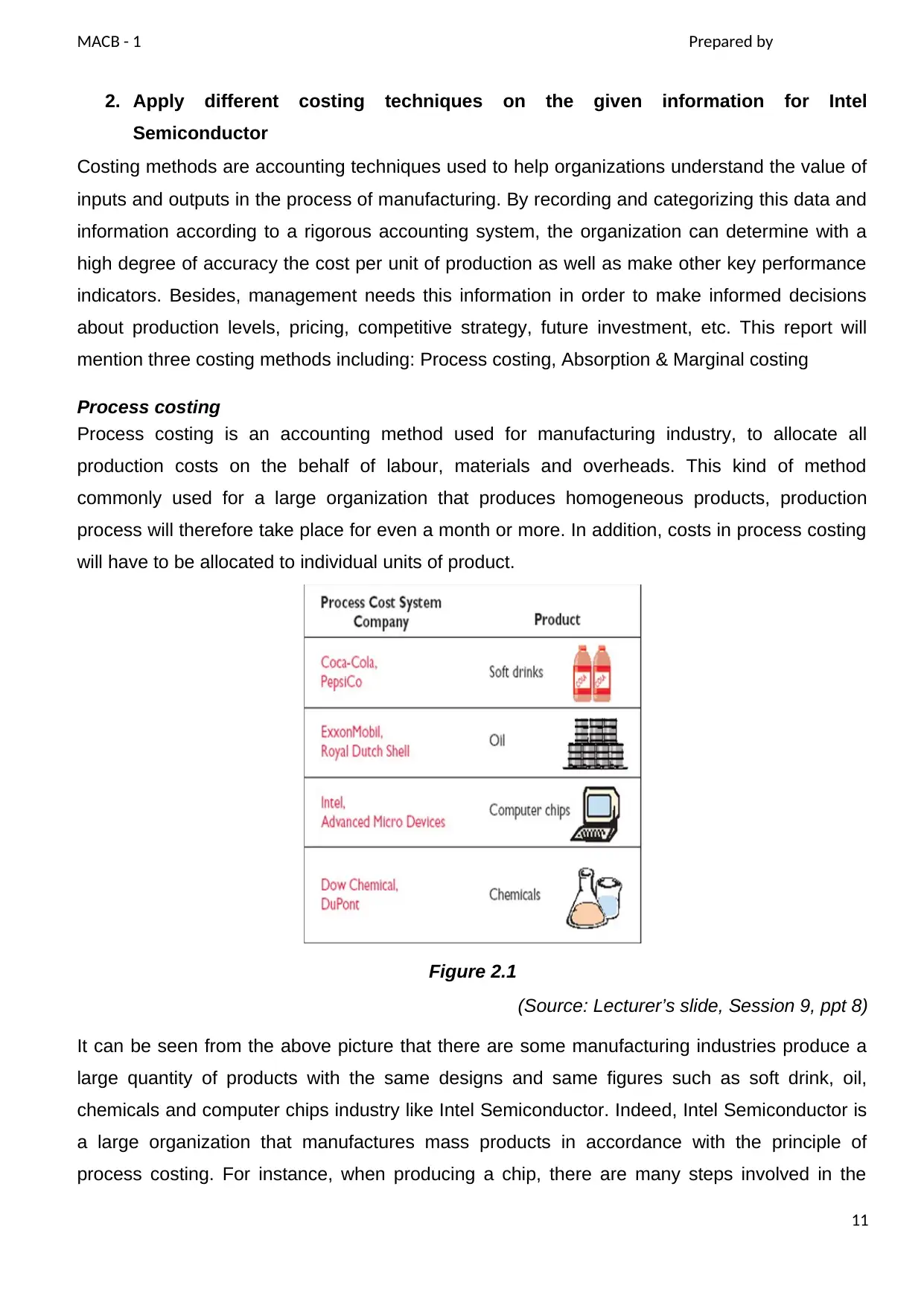

Process costing is an accounting method used for manufacturing industry, to allocate all

production costs on the behalf of labour, materials and overheads. This kind of method

commonly used for a large organization that produces homogeneous products, production

process will therefore take place for even a month or more. In addition, costs in process costing

will have to be allocated to individual units of product.

Figure 2.1

(Source: Lecturer’s slide, Session 9, ppt 8)

It can be seen from the above picture that there are some manufacturing industries produce a

large quantity of products with the same designs and same figures such as soft drink, oil,

chemicals and computer chips industry like Intel Semiconductor. Indeed, Intel Semiconductor is

a large organization that manufactures mass products in accordance with the principle of

process costing. For instance, when producing a chip, there are many steps involved in the

11

2. Apply different costing techniques on the given information for Intel

Semiconductor

Costing methods are accounting techniques used to help organizations understand the value of

inputs and outputs in the process of manufacturing. By recording and categorizing this data and

information according to a rigorous accounting system, the organization can determine with a

high degree of accuracy the cost per unit of production as well as make other key performance

indicators. Besides, management needs this information in order to make informed decisions

about production levels, pricing, competitive strategy, future investment, etc. This report will

mention three costing methods including: Process costing, Absorption & Marginal costing

Process costing

Process costing is an accounting method used for manufacturing industry, to allocate all

production costs on the behalf of labour, materials and overheads. This kind of method

commonly used for a large organization that produces homogeneous products, production

process will therefore take place for even a month or more. In addition, costs in process costing

will have to be allocated to individual units of product.

Figure 2.1

(Source: Lecturer’s slide, Session 9, ppt 8)

It can be seen from the above picture that there are some manufacturing industries produce a

large quantity of products with the same designs and same figures such as soft drink, oil,

chemicals and computer chips industry like Intel Semiconductor. Indeed, Intel Semiconductor is

a large organization that manufactures mass products in accordance with the principle of

process costing. For instance, when producing a chip, there are many steps involved in the

11

MACB - 1 Prepared by

manufacturing process in terms of material transferring, assembling parts, quality testing, etc.

Each step of producing product must be finished before continuing to the next step of the

process. With the use of this process costing, the cost of manufacturing operations of a product

at each stage will be allocated on the behalf of labour, material and overhead.

From that point, it can be sure that process costing is completely appropriate for the It company

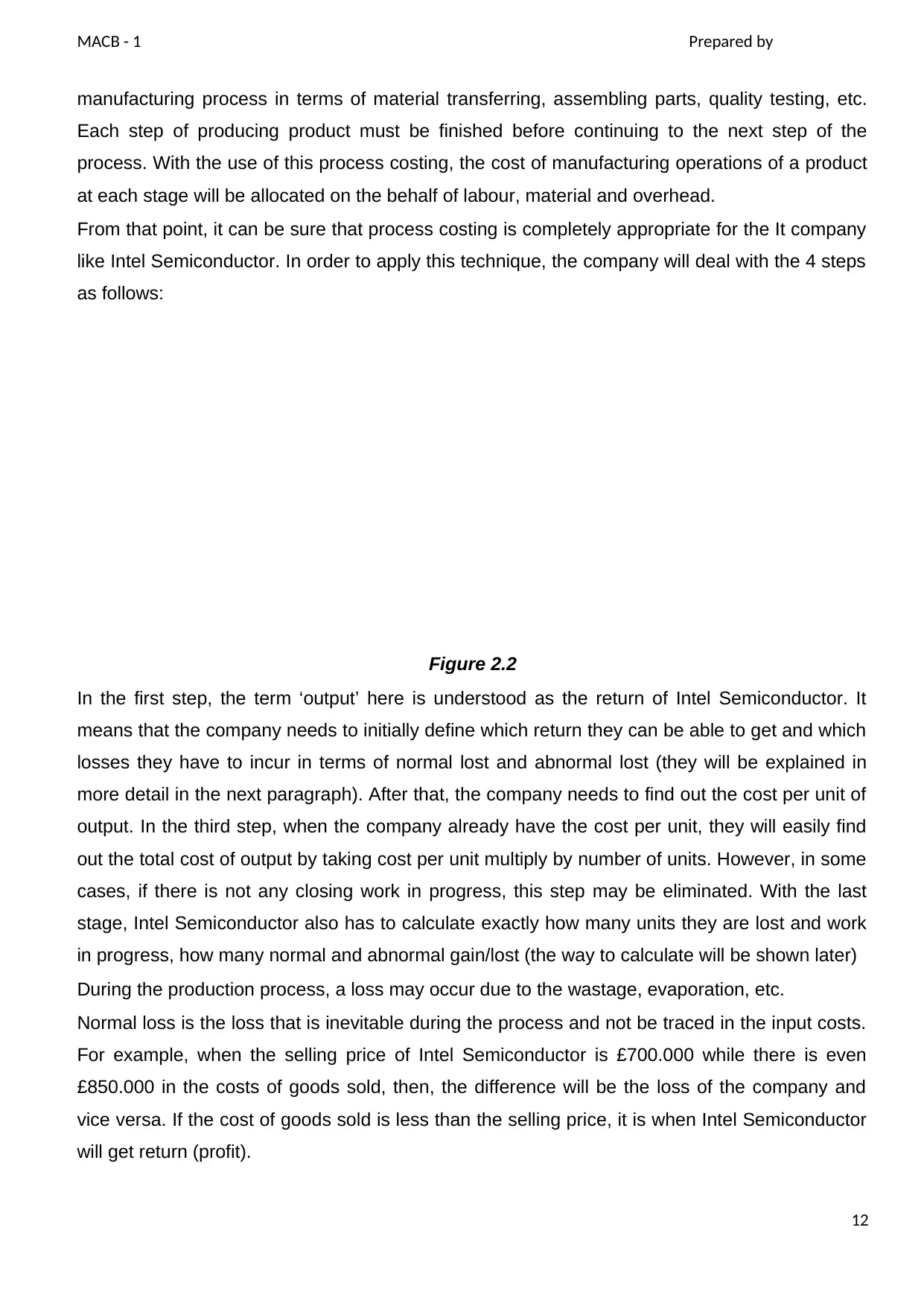

like Intel Semiconductor. In order to apply this technique, the company will deal with the 4 steps

as follows:

Figure 2.2

In the first step, the term ‘output’ here is understood as the return of Intel Semiconductor. It

means that the company needs to initially define which return they can be able to get and which

losses they have to incur in terms of normal lost and abnormal lost (they will be explained in

more detail in the next paragraph). After that, the company needs to find out the cost per unit of

output. In the third step, when the company already have the cost per unit, they will easily find

out the total cost of output by taking cost per unit multiply by number of units. However, in some

cases, if there is not any closing work in progress, this step may be eliminated. With the last

stage, Intel Semiconductor also has to calculate exactly how many units they are lost and work

in progress, how many normal and abnormal gain/lost (the way to calculate will be shown later)

During the production process, a loss may occur due to the wastage, evaporation, etc.

Normal loss is the loss that is inevitable during the process and not be traced in the input costs.

For example, when the selling price of Intel Semiconductor is £700.000 while there is even

£850.000 in the costs of goods sold, then, the difference will be the loss of the company and

vice versa. If the cost of goods sold is less than the selling price, it is when Intel Semiconductor

will get return (profit).

12

Step1:Determineoutput&lossesStep2:Calculatecostperunitofoutput,lossesandWIPStep3:Calculatetotalcostofoutput,lossesandWIPStep4:completeaccounts

manufacturing process in terms of material transferring, assembling parts, quality testing, etc.

Each step of producing product must be finished before continuing to the next step of the

process. With the use of this process costing, the cost of manufacturing operations of a product

at each stage will be allocated on the behalf of labour, material and overhead.

From that point, it can be sure that process costing is completely appropriate for the It company

like Intel Semiconductor. In order to apply this technique, the company will deal with the 4 steps

as follows:

Figure 2.2

In the first step, the term ‘output’ here is understood as the return of Intel Semiconductor. It

means that the company needs to initially define which return they can be able to get and which

losses they have to incur in terms of normal lost and abnormal lost (they will be explained in

more detail in the next paragraph). After that, the company needs to find out the cost per unit of

output. In the third step, when the company already have the cost per unit, they will easily find

out the total cost of output by taking cost per unit multiply by number of units. However, in some

cases, if there is not any closing work in progress, this step may be eliminated. With the last

stage, Intel Semiconductor also has to calculate exactly how many units they are lost and work

in progress, how many normal and abnormal gain/lost (the way to calculate will be shown later)

During the production process, a loss may occur due to the wastage, evaporation, etc.

Normal loss is the loss that is inevitable during the process and not be traced in the input costs.

For example, when the selling price of Intel Semiconductor is £700.000 while there is even

£850.000 in the costs of goods sold, then, the difference will be the loss of the company and

vice versa. If the cost of goods sold is less than the selling price, it is when Intel Semiconductor

will get return (profit).

12

Step1:Determineoutput&lossesStep2:Calculatecostperunitofoutput,lossesandWIPStep3:Calculatetotalcostofoutput,lossesandWIPStep4:completeaccounts

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 54

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.