Analysis of Capital Structure and Financial Performance of ANZ Bank

VerifiedAdded on 2023/04/23

|18

|3830

|62

AI Summary

This report presents an analysis of the capital structure and financial performance of ANZ Bank, including debt equity ratio, return on equity ratio, and EPS. It also analyzes the impact of changes in interest rates on the bank's profitability and recommends strategies to improve the bank's financial performance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Assessment 3

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

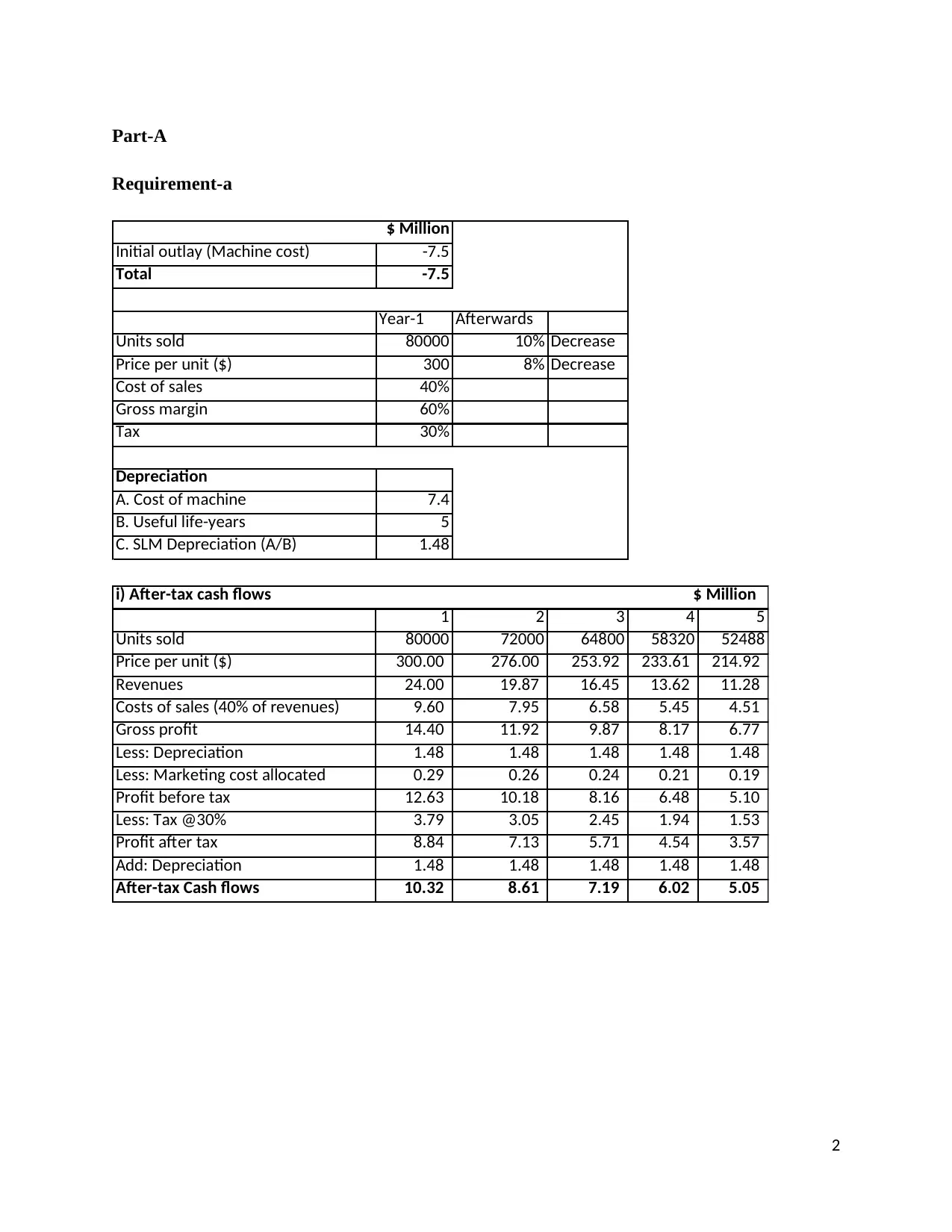

Part-A

Requirement-a

$ Million

Initial outlay (Machine cost) -7.5

Total -7.5

Year-1 Afterwards

Units sold 80000 10% Decrease

Price per unit ($) 300 8% Decrease

Cost of sales 40%

Gross margin 60%

Tax 30%

Depreciation

A. Cost of machine 7.4

B. Useful life-years 5

C. SLM Depreciation (A/B) 1.48

1 2 3 4 5

Units sold 80000 72000 64800 58320 52488

Price per unit ($) 300.00 276.00 253.92 233.61 214.92

Revenues 24.00 19.87 16.45 13.62 11.28

Costs of sales (40% of revenues) 9.60 7.95 6.58 5.45 4.51

Gross profit 14.40 11.92 9.87 8.17 6.77

Less: Depreciation 1.48 1.48 1.48 1.48 1.48

Less: Marketing cost allocated 0.29 0.26 0.24 0.21 0.19

Profit before tax 12.63 10.18 8.16 6.48 5.10

Less: Tax @30% 3.79 3.05 2.45 1.94 1.53

Profit after tax 8.84 7.13 5.71 4.54 3.57

Add: Depreciation 1.48 1.48 1.48 1.48 1.48

After-tax Cash flows 10.32 8.61 7.19 6.02 5.05

i) After-tax cash flows $ Million

2

Requirement-a

$ Million

Initial outlay (Machine cost) -7.5

Total -7.5

Year-1 Afterwards

Units sold 80000 10% Decrease

Price per unit ($) 300 8% Decrease

Cost of sales 40%

Gross margin 60%

Tax 30%

Depreciation

A. Cost of machine 7.4

B. Useful life-years 5

C. SLM Depreciation (A/B) 1.48

1 2 3 4 5

Units sold 80000 72000 64800 58320 52488

Price per unit ($) 300.00 276.00 253.92 233.61 214.92

Revenues 24.00 19.87 16.45 13.62 11.28

Costs of sales (40% of revenues) 9.60 7.95 6.58 5.45 4.51

Gross profit 14.40 11.92 9.87 8.17 6.77

Less: Depreciation 1.48 1.48 1.48 1.48 1.48

Less: Marketing cost allocated 0.29 0.26 0.24 0.21 0.19

Profit before tax 12.63 10.18 8.16 6.48 5.10

Less: Tax @30% 3.79 3.05 2.45 1.94 1.53

Profit after tax 8.84 7.13 5.71 4.54 3.57

Add: Depreciation 1.48 1.48 1.48 1.48 1.48

After-tax Cash flows 10.32 8.61 7.19 6.02 5.05

i) After-tax cash flows $ Million

2

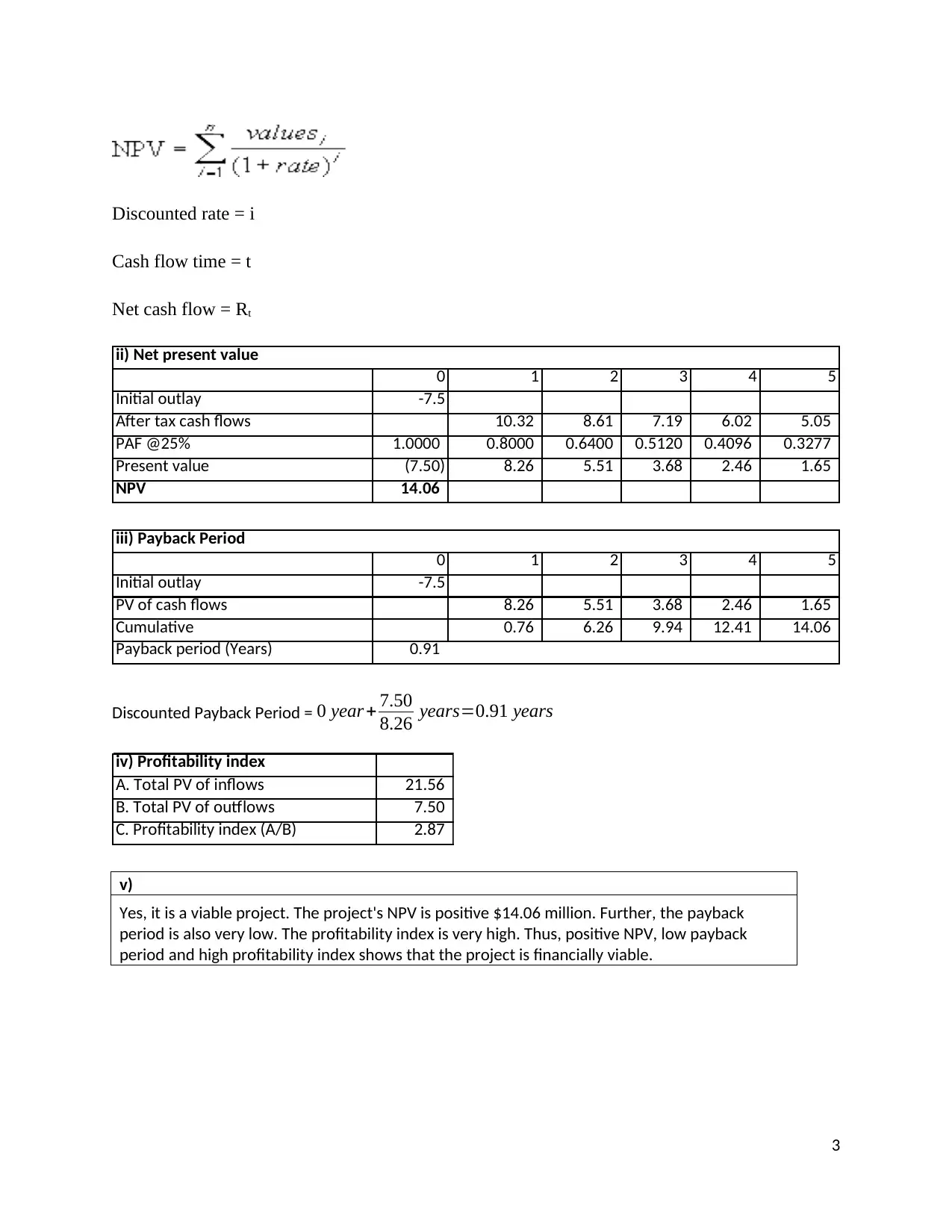

Discounted rate = i

Cash flow time = t

Net cash flow = Rt

0 1 2 3 4 5

Initial outlay -7.5

After tax cash flows 10.32 8.61 7.19 6.02 5.05

PAF @25% 1.0000 0.8000 0.6400 0.5120 0.4096 0.3277

Present value (7.50) 8.26 5.51 3.68 2.46 1.65

NPV 14.06

ii) Net present value

0 1 2 3 4 5

Initial outlay -7.5

PV of cash flows 8.26 5.51 3.68 2.46 1.65

Cumulative 0.76 6.26 9.94 12.41 14.06

Payback period (Years) 0.91

iii) Payback Period

Discounted Payback Period = 0 year+ 7.50

8.26 years=0.91 years

iv) Profitability index

A. Total PV of inflows 21.56

B. Total PV of outflows 7.50

C. Profitability index (A/B) 2.87

v)

Yes, it is a viable project. The project's NPV is positive $14.06 million. Further, the payback

period is also very low. The profitability index is very high. Thus, positive NPV, low payback

period and high profitability index shows that the project is financially viable.

3

Cash flow time = t

Net cash flow = Rt

0 1 2 3 4 5

Initial outlay -7.5

After tax cash flows 10.32 8.61 7.19 6.02 5.05

PAF @25% 1.0000 0.8000 0.6400 0.5120 0.4096 0.3277

Present value (7.50) 8.26 5.51 3.68 2.46 1.65

NPV 14.06

ii) Net present value

0 1 2 3 4 5

Initial outlay -7.5

PV of cash flows 8.26 5.51 3.68 2.46 1.65

Cumulative 0.76 6.26 9.94 12.41 14.06

Payback period (Years) 0.91

iii) Payback Period

Discounted Payback Period = 0 year+ 7.50

8.26 years=0.91 years

iv) Profitability index

A. Total PV of inflows 21.56

B. Total PV of outflows 7.50

C. Profitability index (A/B) 2.87

v)

Yes, it is a viable project. The project's NPV is positive $14.06 million. Further, the payback

period is also very low. The profitability index is very high. Thus, positive NPV, low payback

period and high profitability index shows that the project is financially viable.

3

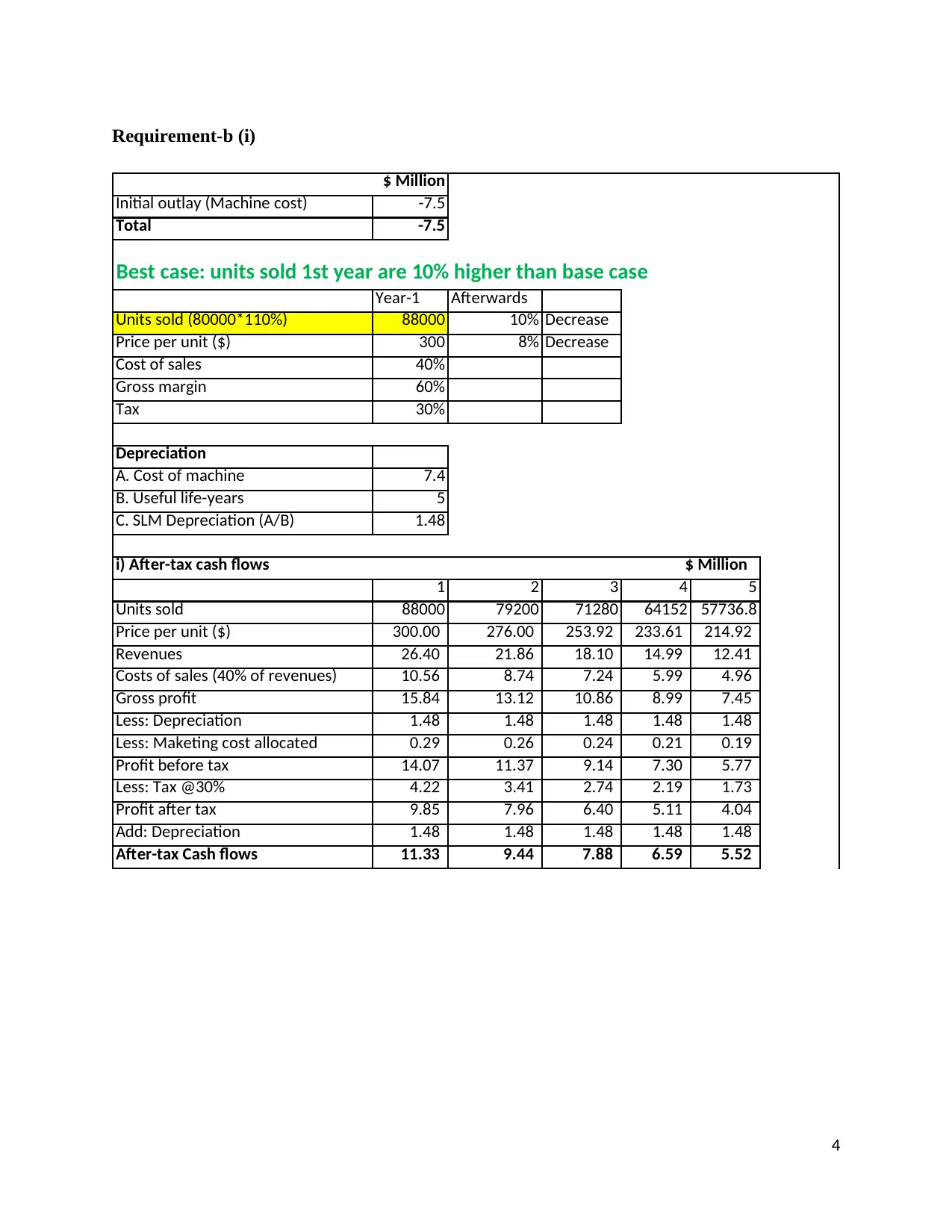

Requirement-b (i)

$ Million

Initial outlay (Machine cost) -7.5

Total -7.5

Best case: units sold 1st year are 10% higher than base case

Year-1 Afterwards

Units sold (80000*110%) 88000 10% Decrease

Price per unit ($) 300 8% Decrease

Cost of sales 40%

Gross margin 60%

Tax 30%

Depreciation

A. Cost of machine 7.4

B. Useful life-years 5

C. SLM Depreciation (A/B) 1.48

1 2 3 4 5

Units sold 88000 79200 71280 64152 57736.8

Price per unit ($) 300.00 276.00 253.92 233.61 214.92

Revenues 26.40 21.86 18.10 14.99 12.41

Costs of sales (40% of revenues) 10.56 8.74 7.24 5.99 4.96

Gross profit 15.84 13.12 10.86 8.99 7.45

Less: Depreciation 1.48 1.48 1.48 1.48 1.48

Less: Maketing cost allocated 0.29 0.26 0.24 0.21 0.19

Profit before tax 14.07 11.37 9.14 7.30 5.77

Less: Tax @30% 4.22 3.41 2.74 2.19 1.73

Profit after tax 9.85 7.96 6.40 5.11 4.04

Add: Depreciation 1.48 1.48 1.48 1.48 1.48

After-tax Cash flows 11.33 9.44 7.88 6.59 5.52

i) After-tax cash flows $ Million

4

$ Million

Initial outlay (Machine cost) -7.5

Total -7.5

Best case: units sold 1st year are 10% higher than base case

Year-1 Afterwards

Units sold (80000*110%) 88000 10% Decrease

Price per unit ($) 300 8% Decrease

Cost of sales 40%

Gross margin 60%

Tax 30%

Depreciation

A. Cost of machine 7.4

B. Useful life-years 5

C. SLM Depreciation (A/B) 1.48

1 2 3 4 5

Units sold 88000 79200 71280 64152 57736.8

Price per unit ($) 300.00 276.00 253.92 233.61 214.92

Revenues 26.40 21.86 18.10 14.99 12.41

Costs of sales (40% of revenues) 10.56 8.74 7.24 5.99 4.96

Gross profit 15.84 13.12 10.86 8.99 7.45

Less: Depreciation 1.48 1.48 1.48 1.48 1.48

Less: Maketing cost allocated 0.29 0.26 0.24 0.21 0.19

Profit before tax 14.07 11.37 9.14 7.30 5.77

Less: Tax @30% 4.22 3.41 2.74 2.19 1.73

Profit after tax 9.85 7.96 6.40 5.11 4.04

Add: Depreciation 1.48 1.48 1.48 1.48 1.48

After-tax Cash flows 11.33 9.44 7.88 6.59 5.52

i) After-tax cash flows $ Million

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

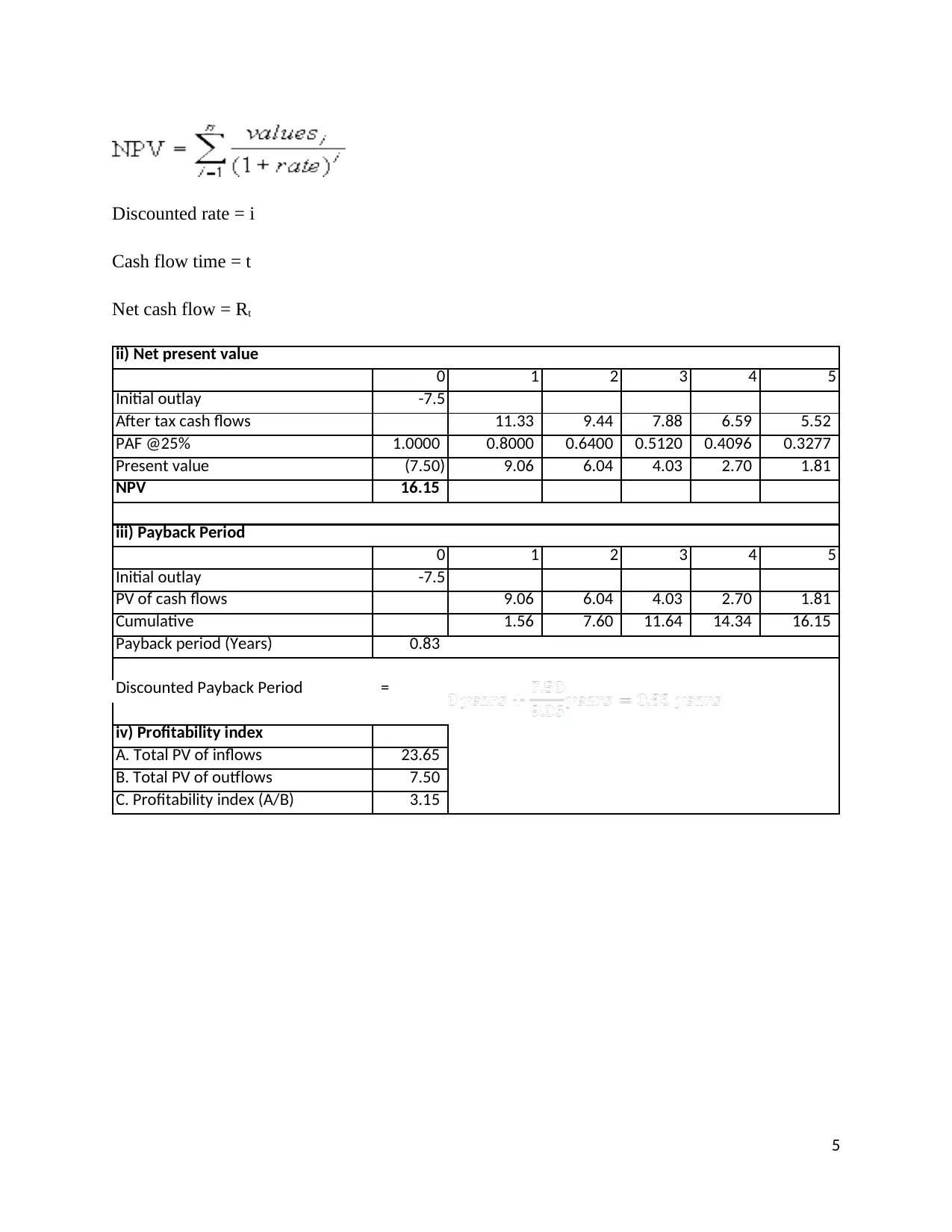

Discounted rate = i

Cash flow time = t

Net cash flow = Rt

0 1 2 3 4 5

Initial outlay -7.5

After tax cash flows 11.33 9.44 7.88 6.59 5.52

PAF @25% 1.0000 0.8000 0.6400 0.5120 0.4096 0.3277

Present value (7.50) 9.06 6.04 4.03 2.70 1.81

NPV 16.15

0 1 2 3 4 5

Initial outlay -7.5

PV of cash flows 9.06 6.04 4.03 2.70 1.81

Cumulative 1.56 7.60 11.64 14.34 16.15

Payback period (Years) 0.83

Discounted Payback Period =

iv) Profitability index

A. Total PV of inflows 23.65

B. Total PV of outflows 7.50

C. Profitability index (A/B) 3.15

ii) Net present value

iii) Payback Period

5

Cash flow time = t

Net cash flow = Rt

0 1 2 3 4 5

Initial outlay -7.5

After tax cash flows 11.33 9.44 7.88 6.59 5.52

PAF @25% 1.0000 0.8000 0.6400 0.5120 0.4096 0.3277

Present value (7.50) 9.06 6.04 4.03 2.70 1.81

NPV 16.15

0 1 2 3 4 5

Initial outlay -7.5

PV of cash flows 9.06 6.04 4.03 2.70 1.81

Cumulative 1.56 7.60 11.64 14.34 16.15

Payback period (Years) 0.83

Discounted Payback Period =

iv) Profitability index

A. Total PV of inflows 23.65

B. Total PV of outflows 7.50

C. Profitability index (A/B) 3.15

ii) Net present value

iii) Payback Period

5

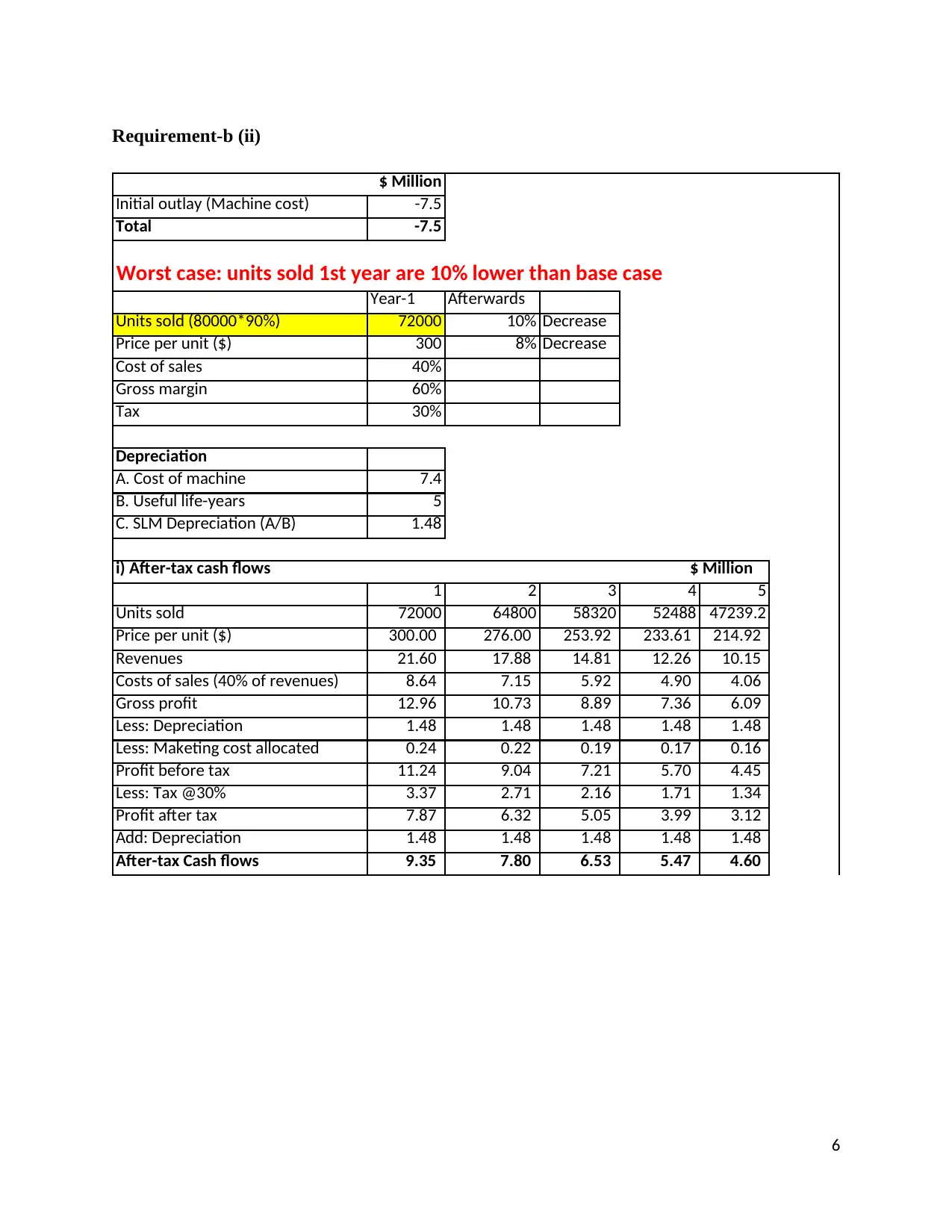

Requirement-b (ii)

$ Million

Initial outlay (Machine cost) -7.5

Total -7.5

Worst case: units sold 1st year are 10% lower than base case

Year-1 Afterwards

Units sold (80000*90%) 72000 10% Decrease

Price per unit ($) 300 8% Decrease

Cost of sales 40%

Gross margin 60%

Tax 30%

Depreciation

A. Cost of machine 7.4

B. Useful life-years 5

C. SLM Depreciation (A/B) 1.48

1 2 3 4 5

Units sold 72000 64800 58320 52488 47239.2

Price per unit ($) 300.00 276.00 253.92 233.61 214.92

Revenues 21.60 17.88 14.81 12.26 10.15

Costs of sales (40% of revenues) 8.64 7.15 5.92 4.90 4.06

Gross profit 12.96 10.73 8.89 7.36 6.09

Less: Depreciation 1.48 1.48 1.48 1.48 1.48

Less: Maketing cost allocated 0.24 0.22 0.19 0.17 0.16

Profit before tax 11.24 9.04 7.21 5.70 4.45

Less: Tax @30% 3.37 2.71 2.16 1.71 1.34

Profit after tax 7.87 6.32 5.05 3.99 3.12

Add: Depreciation 1.48 1.48 1.48 1.48 1.48

After-tax Cash flows 9.35 7.80 6.53 5.47 4.60

i) After-tax cash flows $ Million

6

$ Million

Initial outlay (Machine cost) -7.5

Total -7.5

Worst case: units sold 1st year are 10% lower than base case

Year-1 Afterwards

Units sold (80000*90%) 72000 10% Decrease

Price per unit ($) 300 8% Decrease

Cost of sales 40%

Gross margin 60%

Tax 30%

Depreciation

A. Cost of machine 7.4

B. Useful life-years 5

C. SLM Depreciation (A/B) 1.48

1 2 3 4 5

Units sold 72000 64800 58320 52488 47239.2

Price per unit ($) 300.00 276.00 253.92 233.61 214.92

Revenues 21.60 17.88 14.81 12.26 10.15

Costs of sales (40% of revenues) 8.64 7.15 5.92 4.90 4.06

Gross profit 12.96 10.73 8.89 7.36 6.09

Less: Depreciation 1.48 1.48 1.48 1.48 1.48

Less: Maketing cost allocated 0.24 0.22 0.19 0.17 0.16

Profit before tax 11.24 9.04 7.21 5.70 4.45

Less: Tax @30% 3.37 2.71 2.16 1.71 1.34

Profit after tax 7.87 6.32 5.05 3.99 3.12

Add: Depreciation 1.48 1.48 1.48 1.48 1.48

After-tax Cash flows 9.35 7.80 6.53 5.47 4.60

i) After-tax cash flows $ Million

6

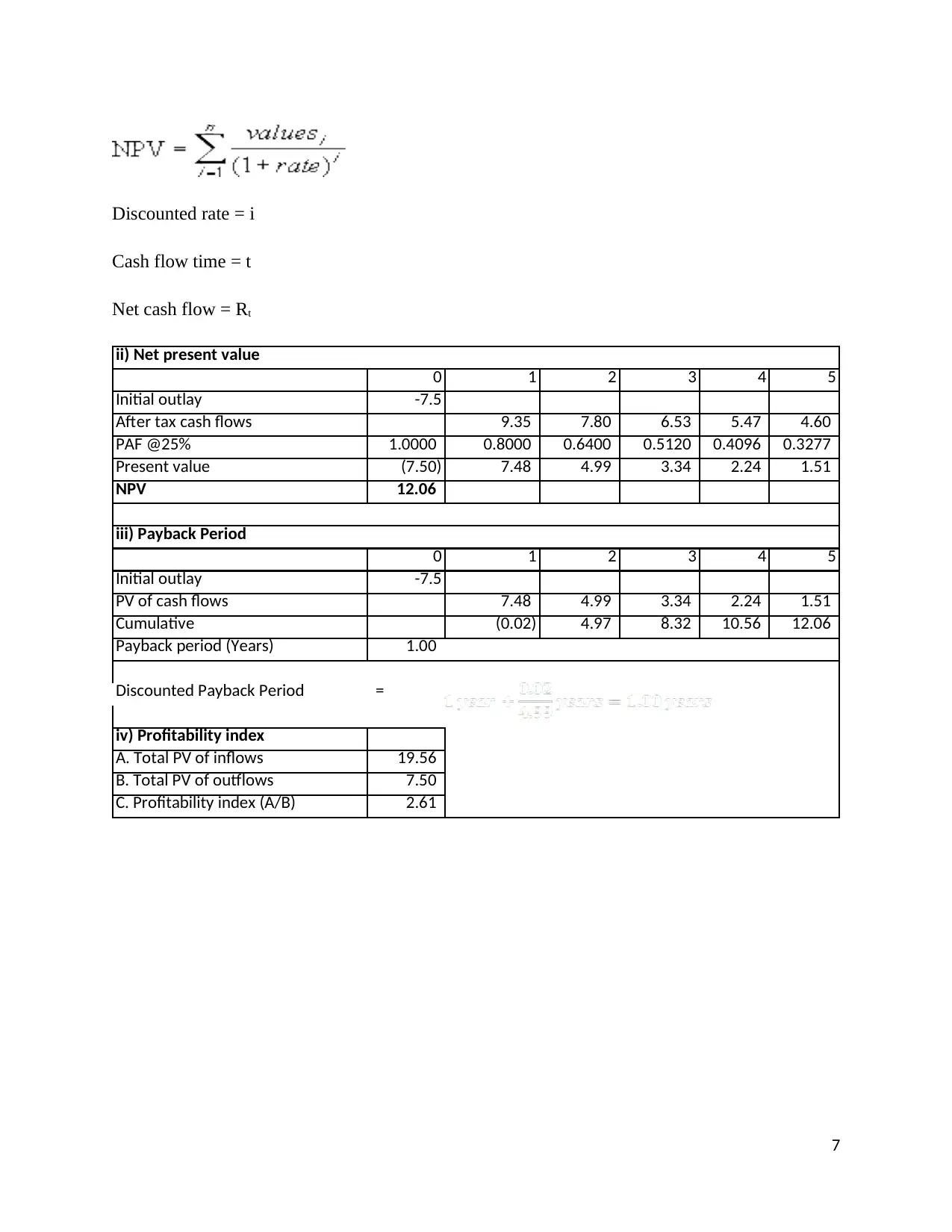

Discounted rate = i

Cash flow time = t

Net cash flow = Rt

0 1 2 3 4 5

Initial outlay -7.5

After tax cash flows 9.35 7.80 6.53 5.47 4.60

PAF @25% 1.0000 0.8000 0.6400 0.5120 0.4096 0.3277

Present value (7.50) 7.48 4.99 3.34 2.24 1.51

NPV 12.06

0 1 2 3 4 5

Initial outlay -7.5

PV of cash flows 7.48 4.99 3.34 2.24 1.51

Cumulative (0.02) 4.97 8.32 10.56 12.06

Payback period (Years) 1.00

Discounted Payback Period =

iv) Profitability index

A. Total PV of inflows 19.56

B. Total PV of outflows 7.50

C. Profitability index (A/B) 2.61

ii) Net present value

iii) Payback Period

7

Cash flow time = t

Net cash flow = Rt

0 1 2 3 4 5

Initial outlay -7.5

After tax cash flows 9.35 7.80 6.53 5.47 4.60

PAF @25% 1.0000 0.8000 0.6400 0.5120 0.4096 0.3277

Present value (7.50) 7.48 4.99 3.34 2.24 1.51

NPV 12.06

0 1 2 3 4 5

Initial outlay -7.5

PV of cash flows 7.48 4.99 3.34 2.24 1.51

Cumulative (0.02) 4.97 8.32 10.56 12.06

Payback period (Years) 1.00

Discounted Payback Period =

iv) Profitability index

A. Total PV of inflows 19.56

B. Total PV of outflows 7.50

C. Profitability index (A/B) 2.61

ii) Net present value

iii) Payback Period

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part-A (b) (iii)

Under the best case scenario, the NPV of the project increases from $14.06 million to $16.15 million.

The increased sales increase the after tax cash flows which causes increase in the NPV. Further, due to

increase in the after tax cash flows, the payback period reduces from 0.91 years to 0.83 year. The

profitability index is also improved from 2.86 times to 3.15 times. Under the worst case scenario, the

after tax cash flows reduces which reduction in the NPV to $12.06 million. The payback period

increases a little reaching to 1 year and profitability index shrinks to 2.61 times.

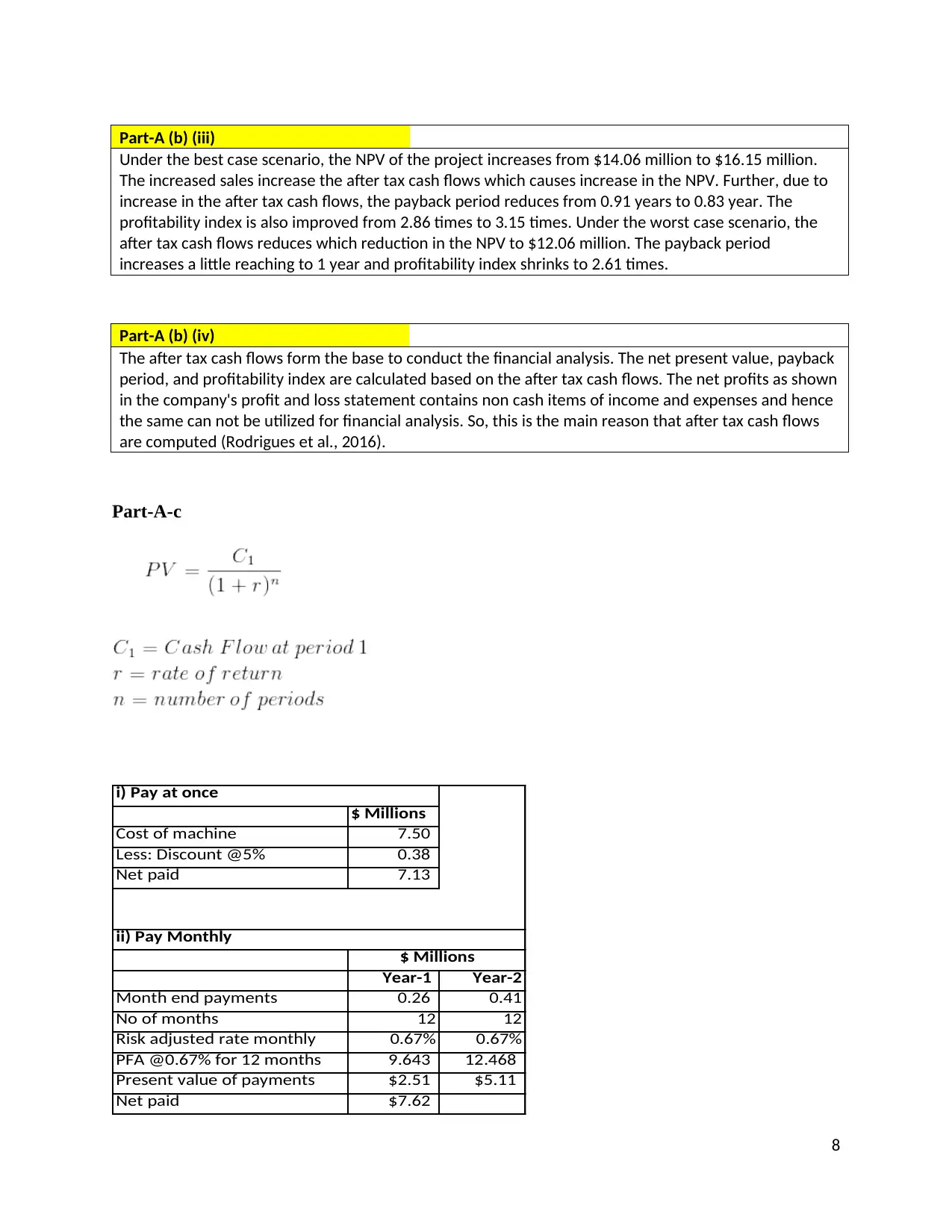

Part-A (b) (iv)

The after tax cash flows form the base to conduct the financial analysis. The net present value, payback

period, and profitability index are calculated based on the after tax cash flows. The net profits as shown

in the company's profit and loss statement contains non cash items of income and expenses and hence

the same can not be utilized for financial analysis. So, this is the main reason that after tax cash flows

are computed (Rodrigues et al., 2016).

Part-A-c

$ Millions

Cost of machine 7.50

Less: Discount @5% 0.38

Net paid 7.13

Year-1 Year-2

Month end payments 0.26 0.41

No of months 12 12

Risk adjusted rate monthly 0.67% 0.67%

PFA @0.67% for 12 months 9.643 12.468

Present value of payments $2.51 $5.11

Net paid $7.62

i) Pay at once

$ Millions

ii) Pay Monthly

8

Under the best case scenario, the NPV of the project increases from $14.06 million to $16.15 million.

The increased sales increase the after tax cash flows which causes increase in the NPV. Further, due to

increase in the after tax cash flows, the payback period reduces from 0.91 years to 0.83 year. The

profitability index is also improved from 2.86 times to 3.15 times. Under the worst case scenario, the

after tax cash flows reduces which reduction in the NPV to $12.06 million. The payback period

increases a little reaching to 1 year and profitability index shrinks to 2.61 times.

Part-A (b) (iv)

The after tax cash flows form the base to conduct the financial analysis. The net present value, payback

period, and profitability index are calculated based on the after tax cash flows. The net profits as shown

in the company's profit and loss statement contains non cash items of income and expenses and hence

the same can not be utilized for financial analysis. So, this is the main reason that after tax cash flows

are computed (Rodrigues et al., 2016).

Part-A-c

$ Millions

Cost of machine 7.50

Less: Discount @5% 0.38

Net paid 7.13

Year-1 Year-2

Month end payments 0.26 0.41

No of months 12 12

Risk adjusted rate monthly 0.67% 0.67%

PFA @0.67% for 12 months 9.643 12.468

Present value of payments $2.51 $5.11

Net paid $7.62

i) Pay at once

$ Millions

ii) Pay Monthly

8

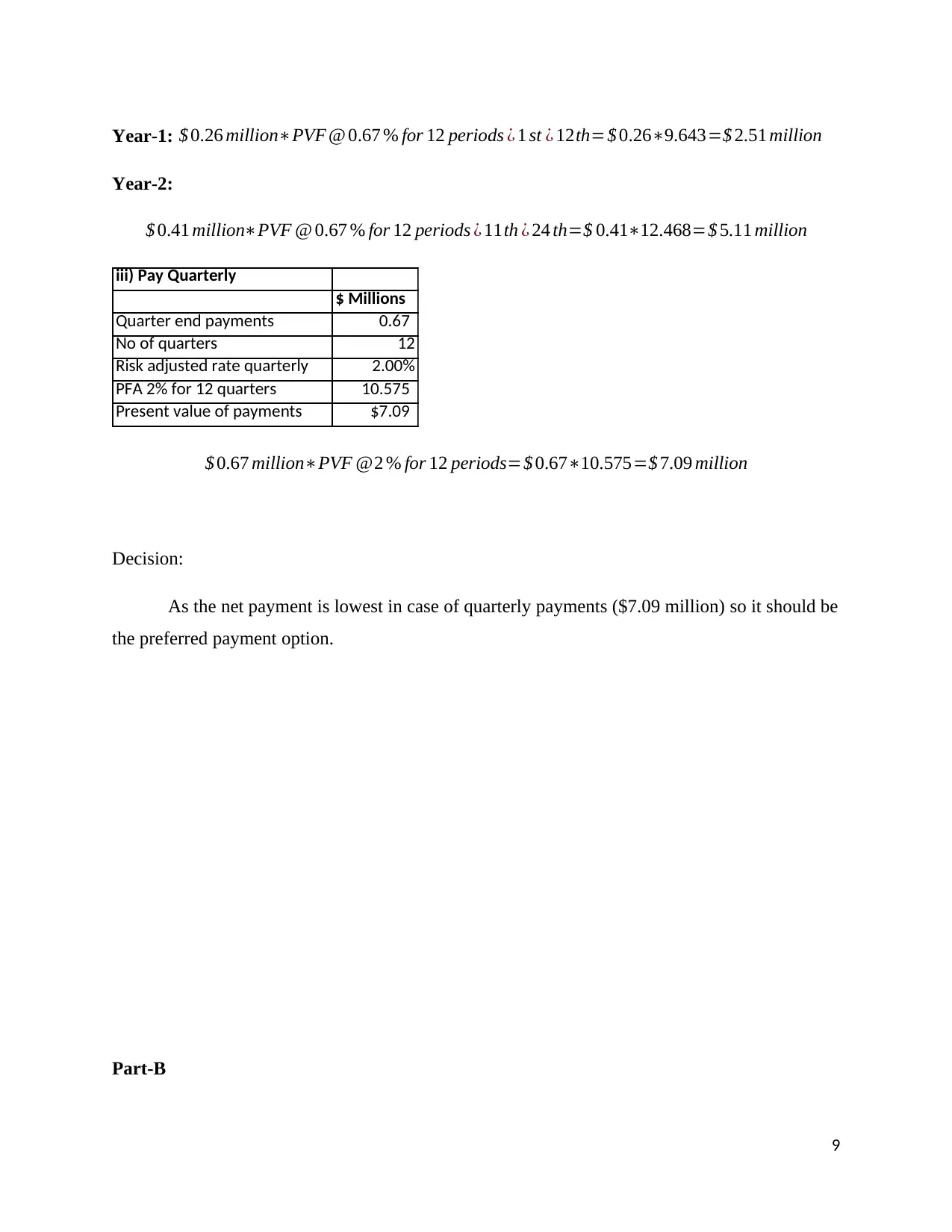

Year-1: $ 0.26 million∗PVF @ 0.67 % for 12 periods ¿ 1 st ¿ 12th=$ 0.26∗9.643=$ 2.51 million

Year-2:

$ 0.41 million∗PVF @ 0.67 % for 12 periods ¿ 11th ¿ 24 th=$ 0.41∗12.468=$ 5.11 million

iii) Pay Quarterly

$ Millions

Quarter end payments 0.67

No of quarters 12

Risk adjusted rate quarterly 2.00%

PFA 2% for 12 quarters 10.575

Present value of payments $7.09

$ 0.67 million∗PVF @2 % for 12 periods=$ 0.67∗10.575=$ 7.09 million

Decision:

As the net payment is lowest in case of quarterly payments ($7.09 million) so it should be

the preferred payment option.

Part-B

9

Year-2:

$ 0.41 million∗PVF @ 0.67 % for 12 periods ¿ 11th ¿ 24 th=$ 0.41∗12.468=$ 5.11 million

iii) Pay Quarterly

$ Millions

Quarter end payments 0.67

No of quarters 12

Risk adjusted rate quarterly 2.00%

PFA 2% for 12 quarters 10.575

Present value of payments $7.09

$ 0.67 million∗PVF @2 % for 12 periods=$ 0.67∗10.575=$ 7.09 million

Decision:

As the net payment is lowest in case of quarterly payments ($7.09 million) so it should be

the preferred payment option.

Part-B

9

Executive Summary

This report presents an analysis of the capital structure and financial performance of ANZ

Bank. The capital structure of the bank has been static with little or few changes in the

composition of debt and equity. More or less, the debt equity ratio of the bank has been found to

be 0.86:1, which indicates that the bank is using more debt than equity. Further, the return on

equity ratio (11.90%) and EPS (237.1 cents) show improvement in the profitability. The liquidity

position of the bank is also good as shown by the improved liquidity coverage ratio (135%).

Introduction

The report presented here deals with the financial analysis of ANZ Bank. The ANZ Bank

is one of the top most banks operating in Australia and New Zealand. The report presents an

analysis of the capital structure and cost of capital of the bank. Further, the report also puts light

on the financial performance of the bank.

Analysis of the Capital Structure of ANZ

The capital structure of a firm shows the composition of its capital funds. A firm may

arrange funds from various sources which mainly fall in two primary categories such as equity

and debt. Different sources of funds have incurs different costs and have different risk

characteristics. Therefore, it becomes essential for a firm to analyze its capital structure and

optimize the cost of capital and risk.

The capital structure of ANZ Bank for the year 2017 has been analyzed as under:

10

This report presents an analysis of the capital structure and financial performance of ANZ

Bank. The capital structure of the bank has been static with little or few changes in the

composition of debt and equity. More or less, the debt equity ratio of the bank has been found to

be 0.86:1, which indicates that the bank is using more debt than equity. Further, the return on

equity ratio (11.90%) and EPS (237.1 cents) show improvement in the profitability. The liquidity

position of the bank is also good as shown by the improved liquidity coverage ratio (135%).

Introduction

The report presented here deals with the financial analysis of ANZ Bank. The ANZ Bank

is one of the top most banks operating in Australia and New Zealand. The report presents an

analysis of the capital structure and cost of capital of the bank. Further, the report also puts light

on the financial performance of the bank.

Analysis of the Capital Structure of ANZ

The capital structure of a firm shows the composition of its capital funds. A firm may

arrange funds from various sources which mainly fall in two primary categories such as equity

and debt. Different sources of funds have incurs different costs and have different risk

characteristics. Therefore, it becomes essential for a firm to analyze its capital structure and

optimize the cost of capital and risk.

The capital structure of ANZ Bank for the year 2017 has been analyzed as under:

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

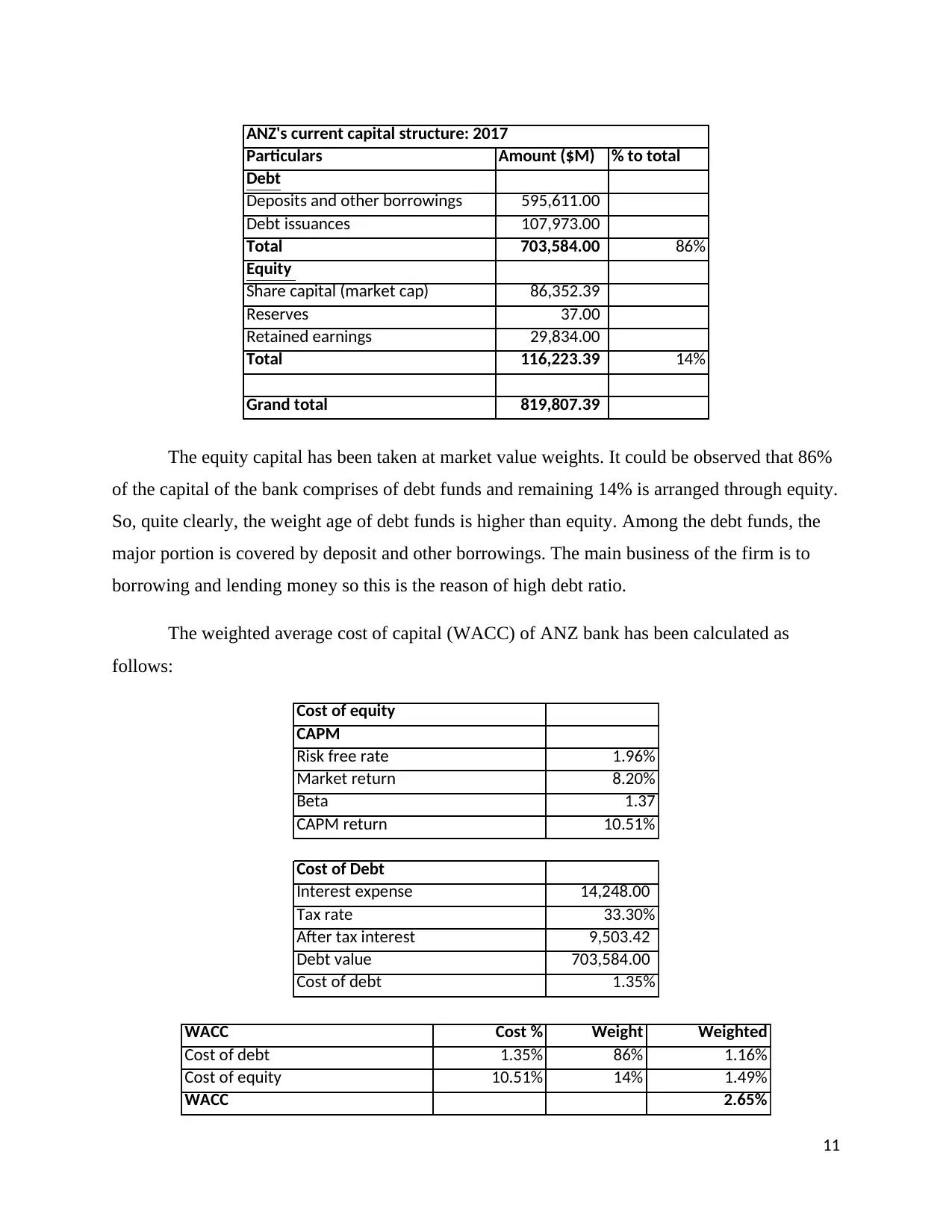

Particulars Amount ($M) % to total

Debt

Deposits and other borrowings 595,611.00

Debt issuances 107,973.00

Total 703,584.00 86%

Equity

Share capital (market cap) 86,352.39

Reserves 37.00

Retained earnings 29,834.00

Total 116,223.39 14%

Grand total 819,807.39

ANZ's current capital structure: 2017

The equity capital has been taken at market value weights. It could be observed that 86%

of the capital of the bank comprises of debt funds and remaining 14% is arranged through equity.

So, quite clearly, the weight age of debt funds is higher than equity. Among the debt funds, the

major portion is covered by deposit and other borrowings. The main business of the firm is to

borrowing and lending money so this is the reason of high debt ratio.

The weighted average cost of capital (WACC) of ANZ bank has been calculated as

follows:

Cost of equity

CAPM

Risk free rate 1.96%

Market return 8.20%

Beta 1.37

CAPM return 10.51%

Cost of Debt

Interest expense 14,248.00

Tax rate 33.30%

After tax interest 9,503.42

Debt value 703,584.00

Cost of debt 1.35%

WACC Cost % Weight Weighted

Cost of debt 1.35% 86% 1.16%

Cost of equity 10.51% 14% 1.49%

WACC 2.65%

11

Debt

Deposits and other borrowings 595,611.00

Debt issuances 107,973.00

Total 703,584.00 86%

Equity

Share capital (market cap) 86,352.39

Reserves 37.00

Retained earnings 29,834.00

Total 116,223.39 14%

Grand total 819,807.39

ANZ's current capital structure: 2017

The equity capital has been taken at market value weights. It could be observed that 86%

of the capital of the bank comprises of debt funds and remaining 14% is arranged through equity.

So, quite clearly, the weight age of debt funds is higher than equity. Among the debt funds, the

major portion is covered by deposit and other borrowings. The main business of the firm is to

borrowing and lending money so this is the reason of high debt ratio.

The weighted average cost of capital (WACC) of ANZ bank has been calculated as

follows:

Cost of equity

CAPM

Risk free rate 1.96%

Market return 8.20%

Beta 1.37

CAPM return 10.51%

Cost of Debt

Interest expense 14,248.00

Tax rate 33.30%

After tax interest 9,503.42

Debt value 703,584.00

Cost of debt 1.35%

WACC Cost % Weight Weighted

Cost of debt 1.35% 86% 1.16%

Cost of equity 10.51% 14% 1.49%

WACC 2.65%

11

The cost of equity has been computed applying the CAPM model. The cost of equity is

10.51% which is higher than the cost of debt of 1.35%. The weight of debt in the total capital of

the bank is 86%. So, the bank is using low cost funds more than the equity which incurs high

cost. Due to this composition, the weighted average cost of capital of the bank is 2.65% which

can be said to be quite low.

The CAPM return provides an approximation to the minimum required rate of return for

the equity investors. The equity investors can analyze that whether the firm is able to provide

them adequate return by comparing the CAPM return with the actual return on equity (ROE) of

the firm (Hou & Van Dijk, 2018). In the case of ANZ Bank, the CAPM return is 10.51% while

the return on equity is 11.90% (ANZ Bank, 2017), which indicates that the bank has been able to

provide adequate return to its equity investors.

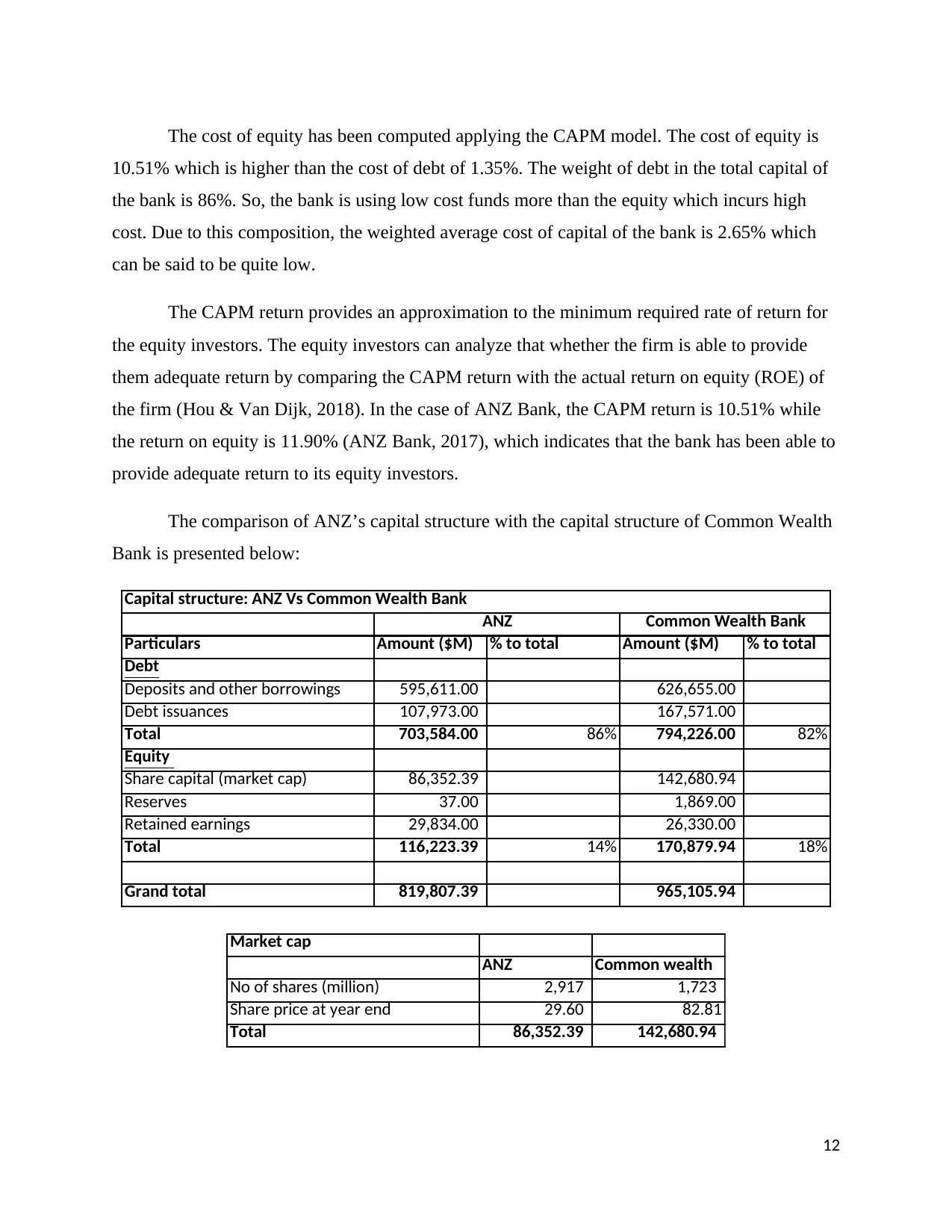

The comparison of ANZ’s capital structure with the capital structure of Common Wealth

Bank is presented below:

Particulars Amount ($M) % to total Amount ($M) % to total

Debt

Deposits and other borrowings 595,611.00 626,655.00

Debt issuances 107,973.00 167,571.00

Total 703,584.00 86% 794,226.00 82%

Equity

Share capital (market cap) 86,352.39 142,680.94

Reserves 37.00 1,869.00

Retained earnings 29,834.00 26,330.00

Total 116,223.39 14% 170,879.94 18%

Grand total 819,807.39 965,105.94

Capital structure: ANZ Vs Common Wealth Bank

ANZ Common Wealth Bank

Market cap

ANZ Common wealth

No of shares (million) 2,917 1,723

Share price at year end 29.60 82.81

Total 86,352.39 142,680.94

12

10.51% which is higher than the cost of debt of 1.35%. The weight of debt in the total capital of

the bank is 86%. So, the bank is using low cost funds more than the equity which incurs high

cost. Due to this composition, the weighted average cost of capital of the bank is 2.65% which

can be said to be quite low.

The CAPM return provides an approximation to the minimum required rate of return for

the equity investors. The equity investors can analyze that whether the firm is able to provide

them adequate return by comparing the CAPM return with the actual return on equity (ROE) of

the firm (Hou & Van Dijk, 2018). In the case of ANZ Bank, the CAPM return is 10.51% while

the return on equity is 11.90% (ANZ Bank, 2017), which indicates that the bank has been able to

provide adequate return to its equity investors.

The comparison of ANZ’s capital structure with the capital structure of Common Wealth

Bank is presented below:

Particulars Amount ($M) % to total Amount ($M) % to total

Debt

Deposits and other borrowings 595,611.00 626,655.00

Debt issuances 107,973.00 167,571.00

Total 703,584.00 86% 794,226.00 82%

Equity

Share capital (market cap) 86,352.39 142,680.94

Reserves 37.00 1,869.00

Retained earnings 29,834.00 26,330.00

Total 116,223.39 14% 170,879.94 18%

Grand total 819,807.39 965,105.94

Capital structure: ANZ Vs Common Wealth Bank

ANZ Common Wealth Bank

Market cap

ANZ Common wealth

No of shares (million) 2,917 1,723

Share price at year end 29.60 82.81

Total 86,352.39 142,680.94

12

The Common Wealth Bank is one of the core competitors of ANZ Bank. The comparison

of capital structure of ANZ Bank with the capital structure of Common Wealth Bank shows that

ANZ uses more debt. The Common Wealth Bank uses 82% debt while ANZ uses 86%. Use of

more debt signifies that Bank is relies more on debt than equity funds. However, it may be noted

that keeping financing structure this way may help the company to keep the cost of capital low

but at the same time it also gives rise to risk of solvency.

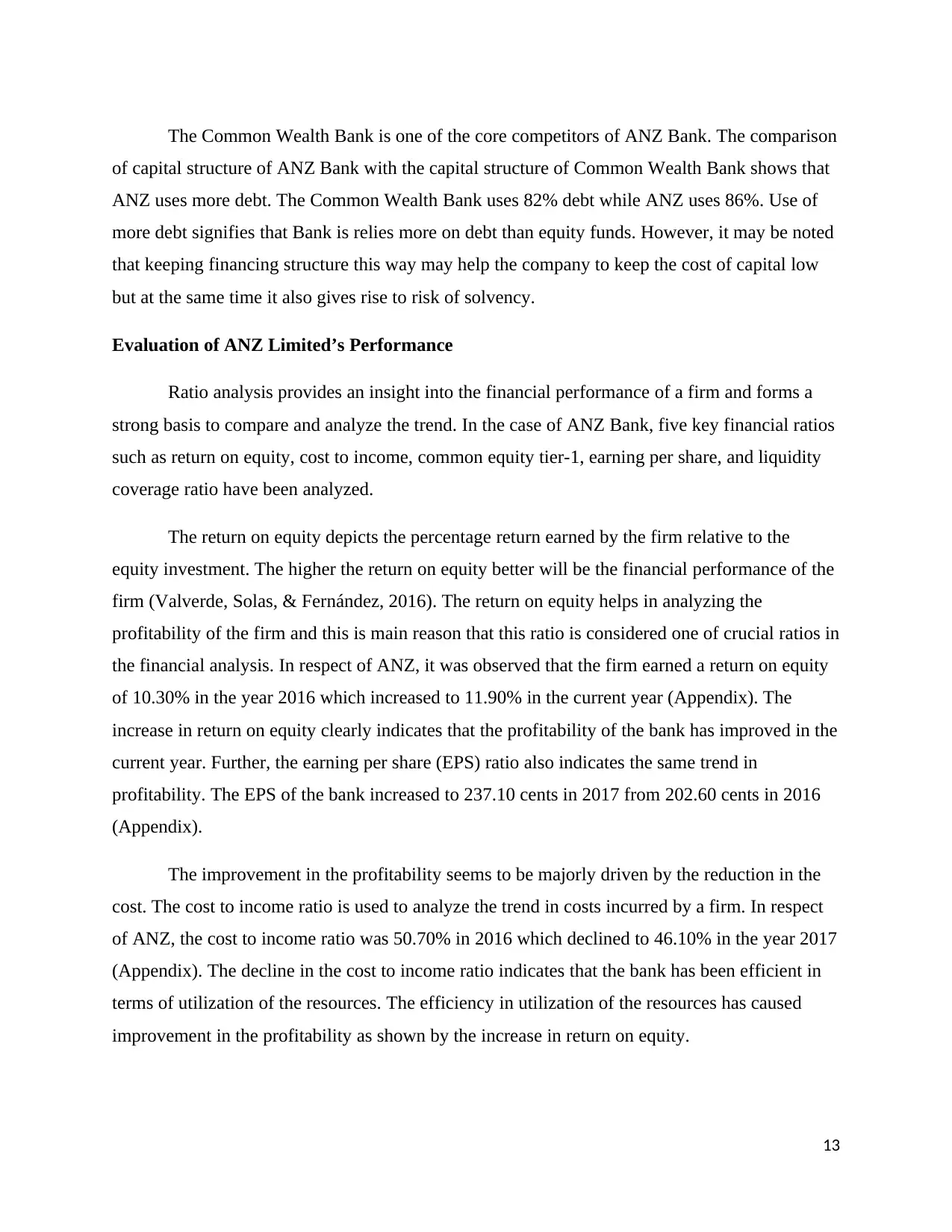

Evaluation of ANZ Limited’s Performance

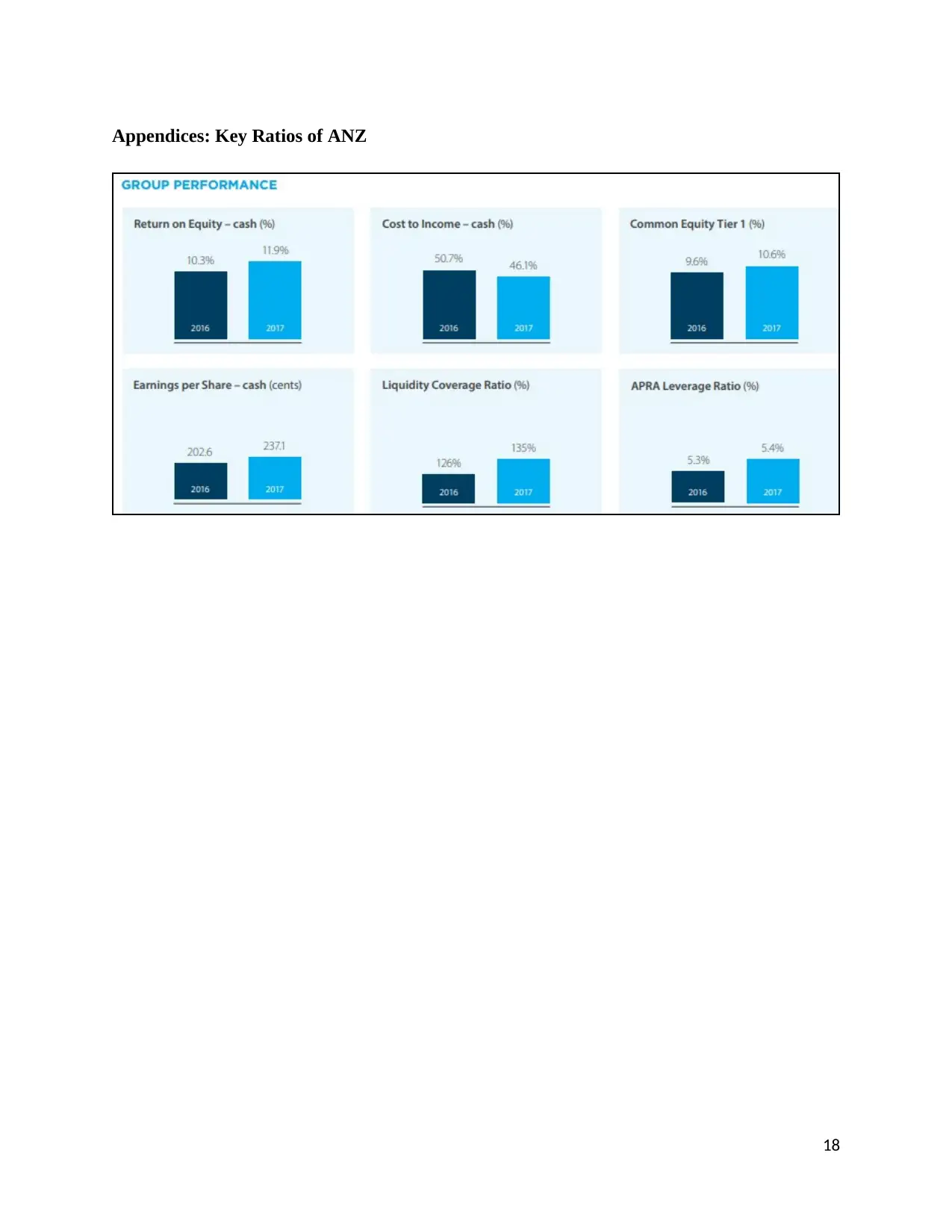

Ratio analysis provides an insight into the financial performance of a firm and forms a

strong basis to compare and analyze the trend. In the case of ANZ Bank, five key financial ratios

such as return on equity, cost to income, common equity tier-1, earning per share, and liquidity

coverage ratio have been analyzed.

The return on equity depicts the percentage return earned by the firm relative to the

equity investment. The higher the return on equity better will be the financial performance of the

firm (Valverde, Solas, & Fernández, 2016). The return on equity helps in analyzing the

profitability of the firm and this is main reason that this ratio is considered one of crucial ratios in

the financial analysis. In respect of ANZ, it was observed that the firm earned a return on equity

of 10.30% in the year 2016 which increased to 11.90% in the current year (Appendix). The

increase in return on equity clearly indicates that the profitability of the bank has improved in the

current year. Further, the earning per share (EPS) ratio also indicates the same trend in

profitability. The EPS of the bank increased to 237.10 cents in 2017 from 202.60 cents in 2016

(Appendix).

The improvement in the profitability seems to be majorly driven by the reduction in the

cost. The cost to income ratio is used to analyze the trend in costs incurred by a firm. In respect

of ANZ, the cost to income ratio was 50.70% in 2016 which declined to 46.10% in the year 2017

(Appendix). The decline in the cost to income ratio indicates that the bank has been efficient in

terms of utilization of the resources. The efficiency in utilization of the resources has caused

improvement in the profitability as shown by the increase in return on equity.

13

of capital structure of ANZ Bank with the capital structure of Common Wealth Bank shows that

ANZ uses more debt. The Common Wealth Bank uses 82% debt while ANZ uses 86%. Use of

more debt signifies that Bank is relies more on debt than equity funds. However, it may be noted

that keeping financing structure this way may help the company to keep the cost of capital low

but at the same time it also gives rise to risk of solvency.

Evaluation of ANZ Limited’s Performance

Ratio analysis provides an insight into the financial performance of a firm and forms a

strong basis to compare and analyze the trend. In the case of ANZ Bank, five key financial ratios

such as return on equity, cost to income, common equity tier-1, earning per share, and liquidity

coverage ratio have been analyzed.

The return on equity depicts the percentage return earned by the firm relative to the

equity investment. The higher the return on equity better will be the financial performance of the

firm (Valverde, Solas, & Fernández, 2016). The return on equity helps in analyzing the

profitability of the firm and this is main reason that this ratio is considered one of crucial ratios in

the financial analysis. In respect of ANZ, it was observed that the firm earned a return on equity

of 10.30% in the year 2016 which increased to 11.90% in the current year (Appendix). The

increase in return on equity clearly indicates that the profitability of the bank has improved in the

current year. Further, the earning per share (EPS) ratio also indicates the same trend in

profitability. The EPS of the bank increased to 237.10 cents in 2017 from 202.60 cents in 2016

(Appendix).

The improvement in the profitability seems to be majorly driven by the reduction in the

cost. The cost to income ratio is used to analyze the trend in costs incurred by a firm. In respect

of ANZ, the cost to income ratio was 50.70% in 2016 which declined to 46.10% in the year 2017

(Appendix). The decline in the cost to income ratio indicates that the bank has been efficient in

terms of utilization of the resources. The efficiency in utilization of the resources has caused

improvement in the profitability as shown by the increase in return on equity.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

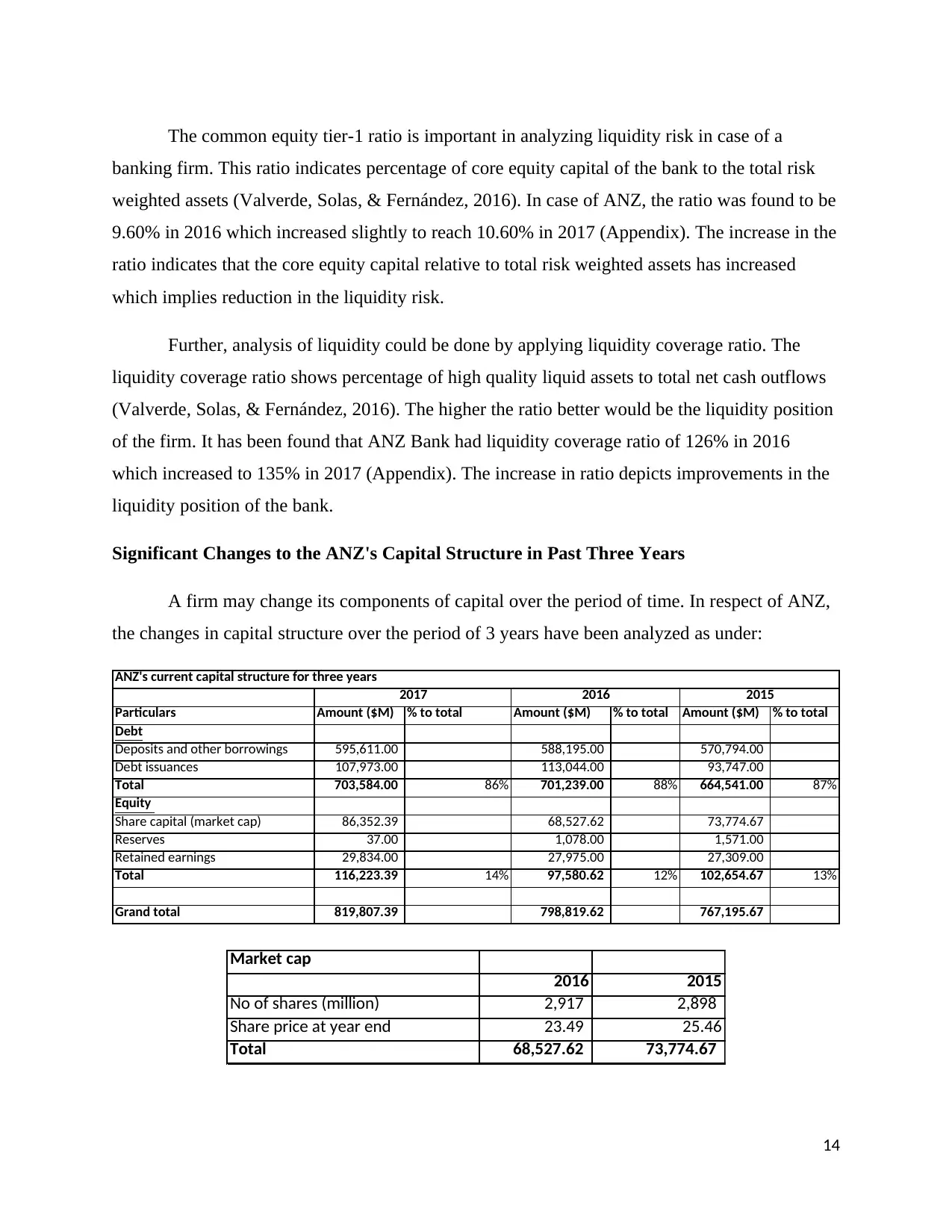

The common equity tier-1 ratio is important in analyzing liquidity risk in case of a

banking firm. This ratio indicates percentage of core equity capital of the bank to the total risk

weighted assets (Valverde, Solas, & Fernández, 2016). In case of ANZ, the ratio was found to be

9.60% in 2016 which increased slightly to reach 10.60% in 2017 (Appendix). The increase in the

ratio indicates that the core equity capital relative to total risk weighted assets has increased

which implies reduction in the liquidity risk.

Further, analysis of liquidity could be done by applying liquidity coverage ratio. The

liquidity coverage ratio shows percentage of high quality liquid assets to total net cash outflows

(Valverde, Solas, & Fernández, 2016). The higher the ratio better would be the liquidity position

of the firm. It has been found that ANZ Bank had liquidity coverage ratio of 126% in 2016

which increased to 135% in 2017 (Appendix). The increase in ratio depicts improvements in the

liquidity position of the bank.

Significant Changes to the ANZ's Capital Structure in Past Three Years

A firm may change its components of capital over the period of time. In respect of ANZ,

the changes in capital structure over the period of 3 years have been analyzed as under:

Particulars Amount ($M) % to total Amount ($M) % to total Amount ($M) % to total

Debt

Deposits and other borrowings 595,611.00 588,195.00 570,794.00

Debt issuances 107,973.00 113,044.00 93,747.00

Total 703,584.00 86% 701,239.00 88% 664,541.00 87%

Equity

Share capital (market cap) 86,352.39 68,527.62 73,774.67

Reserves 37.00 1,078.00 1,571.00

Retained earnings 29,834.00 27,975.00 27,309.00

Total 116,223.39 14% 97,580.62 12% 102,654.67 13%

Grand total 819,807.39 798,819.62 767,195.67

2015

ANZ's current capital structure for three years

2017 2016

Market cap

2016 2015

No of shares (million) 2,917 2,898

Share price at year end 23.49 25.46

Total 68,527.62 73,774.67

14

banking firm. This ratio indicates percentage of core equity capital of the bank to the total risk

weighted assets (Valverde, Solas, & Fernández, 2016). In case of ANZ, the ratio was found to be

9.60% in 2016 which increased slightly to reach 10.60% in 2017 (Appendix). The increase in the

ratio indicates that the core equity capital relative to total risk weighted assets has increased

which implies reduction in the liquidity risk.

Further, analysis of liquidity could be done by applying liquidity coverage ratio. The

liquidity coverage ratio shows percentage of high quality liquid assets to total net cash outflows

(Valverde, Solas, & Fernández, 2016). The higher the ratio better would be the liquidity position

of the firm. It has been found that ANZ Bank had liquidity coverage ratio of 126% in 2016

which increased to 135% in 2017 (Appendix). The increase in ratio depicts improvements in the

liquidity position of the bank.

Significant Changes to the ANZ's Capital Structure in Past Three Years

A firm may change its components of capital over the period of time. In respect of ANZ,

the changes in capital structure over the period of 3 years have been analyzed as under:

Particulars Amount ($M) % to total Amount ($M) % to total Amount ($M) % to total

Debt

Deposits and other borrowings 595,611.00 588,195.00 570,794.00

Debt issuances 107,973.00 113,044.00 93,747.00

Total 703,584.00 86% 701,239.00 88% 664,541.00 87%

Equity

Share capital (market cap) 86,352.39 68,527.62 73,774.67

Reserves 37.00 1,078.00 1,571.00

Retained earnings 29,834.00 27,975.00 27,309.00

Total 116,223.39 14% 97,580.62 12% 102,654.67 13%

Grand total 819,807.39 798,819.62 767,195.67

2015

ANZ's current capital structure for three years

2017 2016

Market cap

2016 2015

No of shares (million) 2,917 2,898

Share price at year end 23.49 25.46

Total 68,527.62 73,774.67

14

The data presented above shows that there has not been any significant change in the

components of the capital used by the bank over the period of three years. In the year 2015, the

bank was running its business with 87% debt and 13% equity. This changed slightly in the year

2016 showing increase in debt to 88% and reduction in equity to 12%. In the year 2017, the bank

again lowered the debt portion to keep to 86%.

Analysis of Reputation Risk of ANZ

It is the primary duty of the directors to act with integrity and assume accountability to

improve financial performance of the business and ensure that business runs in the best of its

stakeholder’s interest. The board of directors of a firm sits at the top the governance system. The

success of the business lies in strengthening the governance mechanism within the firm and

ensuring adequate transparency. Transparency implies bringing all facts to the knowledge of

relevant stakeholder. So, the board of director being the supreme governing body of the firm

should ensure that all the stakeholders of the business are informed adequately on the matters of

their concern. For this purpose, the board should ensure that the adequate and appropriate

disclosures are made in the annual report of the company.

The findings of Banking Royal Commission reveal that ANZ bank has been found to be

involved in conducting misleading business. The ANZ Bank has misled its customers as well as

its investors. ANZ’s Chief Shyane Elliott agreed to the misconducts of the bank and assured to

regain the lost faith of its customers and investors. The results of enquiry show that the bank was

offering fraudulent products to its customers. The bank brought in a new investment scheme

which purposefully framed in such a manner that ultimately was to put the customer at losing

end. ANZ bank is at the verge of losing its licence because of introducing fraudulent products for

sale to its customers.

The findings of Banking Royal Commission clearly indicate that all was not going well in

the bank and there were many things which should have been brought to the notice of the

stakeholders. However, the board of directors of the company failed in making adequate and

appropriate disclosures. The board of directors concealed the facts of misconduct which were

brought to the light by the Banking Royal Commission. Thus, it could be said that the bank has

15

components of the capital used by the bank over the period of three years. In the year 2015, the

bank was running its business with 87% debt and 13% equity. This changed slightly in the year

2016 showing increase in debt to 88% and reduction in equity to 12%. In the year 2017, the bank

again lowered the debt portion to keep to 86%.

Analysis of Reputation Risk of ANZ

It is the primary duty of the directors to act with integrity and assume accountability to

improve financial performance of the business and ensure that business runs in the best of its

stakeholder’s interest. The board of directors of a firm sits at the top the governance system. The

success of the business lies in strengthening the governance mechanism within the firm and

ensuring adequate transparency. Transparency implies bringing all facts to the knowledge of

relevant stakeholder. So, the board of director being the supreme governing body of the firm

should ensure that all the stakeholders of the business are informed adequately on the matters of

their concern. For this purpose, the board should ensure that the adequate and appropriate

disclosures are made in the annual report of the company.

The findings of Banking Royal Commission reveal that ANZ bank has been found to be

involved in conducting misleading business. The ANZ Bank has misled its customers as well as

its investors. ANZ’s Chief Shyane Elliott agreed to the misconducts of the bank and assured to

regain the lost faith of its customers and investors. The results of enquiry show that the bank was

offering fraudulent products to its customers. The bank brought in a new investment scheme

which purposefully framed in such a manner that ultimately was to put the customer at losing

end. ANZ bank is at the verge of losing its licence because of introducing fraudulent products for

sale to its customers.

The findings of Banking Royal Commission clearly indicate that all was not going well in

the bank and there were many things which should have been brought to the notice of the

stakeholders. However, the board of directors of the company failed in making adequate and

appropriate disclosures. The board of directors concealed the facts of misconduct which were

brought to the light by the Banking Royal Commission. Thus, it could be said that the bank has

15

not been able to manage its reputational risk adequately. The faith of its investors and customers

has lost which is causing decline in the share price of the bank.

In order to restore the faith of the investors, the board of directors of the bank should

come up in front of the stakeholders and address their grievances. The bank should also think of

devising a policy to compensate to the loss of investors and customers. However, the board of

directors of ANZ has failed in doing so.

Conclusion

It could be concluded from the discussion done in this report that the analysis of capital

structure and WACC is essential for a firm. ANZ Bank’s WACC has been found to be 2.65%

with debt and equity being in the ratio of 86% and 14%. The financial performance of the bank

being analyzed by applying ratio analysis shows that the bank has shown improvements.

16

has lost which is causing decline in the share price of the bank.

In order to restore the faith of the investors, the board of directors of the bank should

come up in front of the stakeholders and address their grievances. The bank should also think of

devising a policy to compensate to the loss of investors and customers. However, the board of

directors of ANZ has failed in doing so.

Conclusion

It could be concluded from the discussion done in this report that the analysis of capital

structure and WACC is essential for a firm. ANZ Bank’s WACC has been found to be 2.65%

with debt and equity being in the ratio of 86% and 14%. The financial performance of the bank

being analyzed by applying ratio analysis shows that the bank has shown improvements.

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

References

ANZ Bank. (2017). Annual report of ANZ Bank for the year 2017. Retrieved from

https://shareholder.anz.com/sites/default/files/2017_anz_annual_report.pdf

Hou, K., & Van Dijk, M. A. (2018). Resurrecting the size effect: Firm size, profitability shocks,

and expected stock returns. Charles A. Dice Center Working Paper, (2010-1).

Rodrigues, S., Torabikalaki, R., Faria, F., Cafôfo, N., Chen, X., Ivaki, A. R., ... & Morgado-Dias,

F. J. S. E. (2016). Economic feasibility analysis of small scale PV systems in different

countries. Solar Energy, 131, 81-95.

Valverde, S. C., Solas, P. J. C., & Fernández, F. R. (Eds.). (2016). Liquidity Risk, Efficiency and

New Bank Business Models. Springer.

17

ANZ Bank. (2017). Annual report of ANZ Bank for the year 2017. Retrieved from

https://shareholder.anz.com/sites/default/files/2017_anz_annual_report.pdf

Hou, K., & Van Dijk, M. A. (2018). Resurrecting the size effect: Firm size, profitability shocks,

and expected stock returns. Charles A. Dice Center Working Paper, (2010-1).

Rodrigues, S., Torabikalaki, R., Faria, F., Cafôfo, N., Chen, X., Ivaki, A. R., ... & Morgado-Dias,

F. J. S. E. (2016). Economic feasibility analysis of small scale PV systems in different

countries. Solar Energy, 131, 81-95.

Valverde, S. C., Solas, P. J. C., & Fernández, F. R. (Eds.). (2016). Liquidity Risk, Efficiency and

New Bank Business Models. Springer.

17

Appendices: Key Ratios of ANZ

18

18

1 out of 18

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.