Macroeconomic Trends in Australia: An In-depth Economics Assignment

VerifiedAdded on 2023/06/12

|12

|4372

|275

Essay

AI Summary

This essay provides an in-depth analysis of Australia's macroeconomic trends, focusing on key indicators such as Real GDP growth rate, inflation rate, unemployment rate, and exchange rates between 1990 and 2016. The analysis reveals that while the Real GDP growth rate experiences considerable fluctuations indicative of a business cycle, the inflation and unemployment rates remain relatively stable. The essay also explores the relationship between net exports and real exchange rates, noting that Australia has primarily been a net importer. A comparison of Australia's Cash Rate with the USA's Federal Fund's Rate suggests limited influence of the latter on the former. Overall, the essay paints a positive outlook for the Australian economy, with a cautionary note on potential future inflationary pressures. Desklib offers this essay as a study resource, providing students access to solved assignments and past papers.

Running head: ECONOMICS ASSIGNMENT

Economics Assignment

Name of the Student

Name of the University

Author Note

Economics Assignment

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ECONOMICS ASSIGNMENT

Executive Summary

The economy of Australia can be considered to be one of the most stable and

impressively growing economies in the global scenario with impressive growth trends in

almost all the economic indicators over the last few decades. The Real GDP growth rate of

the country can be seen to have considerably dynamic and fluctuating trends indicating

towards the presence of business cycle with periods of expansion and recession in the

economy. However, both the unemployment and the inflation rates in the country can be seen

to be less fluctuating than the Real GDP growth rate of the same. The exchange rate of AUD

is also seen to have maintained stability although the country has mostly remained net

importer in spite of exporting significantly to other countries. The Cash Rate of the country,

determined by the inflation targeting system, can be seen to be declining over the last few

years and although this decline has resemblance with the decline in that of the Fed’s Fund

Rate in the USA, the latter does not seem to have high influence on the former. Overall, the

economic trends of the country look positive for the coming years although there remains the

risk of higher inflationary trends for Australia in near future.

Executive Summary

The economy of Australia can be considered to be one of the most stable and

impressively growing economies in the global scenario with impressive growth trends in

almost all the economic indicators over the last few decades. The Real GDP growth rate of

the country can be seen to have considerably dynamic and fluctuating trends indicating

towards the presence of business cycle with periods of expansion and recession in the

economy. However, both the unemployment and the inflation rates in the country can be seen

to be less fluctuating than the Real GDP growth rate of the same. The exchange rate of AUD

is also seen to have maintained stability although the country has mostly remained net

importer in spite of exporting significantly to other countries. The Cash Rate of the country,

determined by the inflation targeting system, can be seen to be declining over the last few

years and although this decline has resemblance with the decline in that of the Fed’s Fund

Rate in the USA, the latter does not seem to have high influence on the former. Overall, the

economic trends of the country look positive for the coming years although there remains the

risk of higher inflationary trends for Australia in near future.

2ECONOMICS ASSIGNMENT

Table of Contents

Introduction................................................................................................................................3

Relationship between Real GDP and Inflation Rate in Australia..............................................3

Relationship between the Rate of Unemployment and Real GDP Growth Rate of Australia...4

Business Cycle in Australia.......................................................................................................5

Net exports and Real Exchange rates (Australia and USA).......................................................6

Relationship between the Cash Rate (Australia) and Federal Fund’s Rate (USA)....................7

Australia: Macroeconomic Outlook...........................................................................................8

Conclusion..................................................................................................................................9

References................................................................................................................................10

Table of Contents

Introduction................................................................................................................................3

Relationship between Real GDP and Inflation Rate in Australia..............................................3

Relationship between the Rate of Unemployment and Real GDP Growth Rate of Australia...4

Business Cycle in Australia.......................................................................................................5

Net exports and Real Exchange rates (Australia and USA).......................................................6

Relationship between the Cash Rate (Australia) and Federal Fund’s Rate (USA)....................7

Australia: Macroeconomic Outlook...........................................................................................8

Conclusion..................................................................................................................................9

References................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ECONOMICS ASSIGNMENT

Introduction

The economy of Australia, has over the decades, developed significantly and

prospered immensely, thereby becoming one of the dominating economies across the globe.

However, the economy has been subjected to considerable fluctuations and dynamics, both

positive as well as negative, much of which can be seen to be seen from the fluctuations in

the macroeconomic indicators (Schneider 2012). Keeping this into consideration, the

concerned assignment tries to analyse and discuss the dynamics in different macroeconomic

indicators, in accordance to the data collected, thereby predicting the future trends in the

economy of the country.

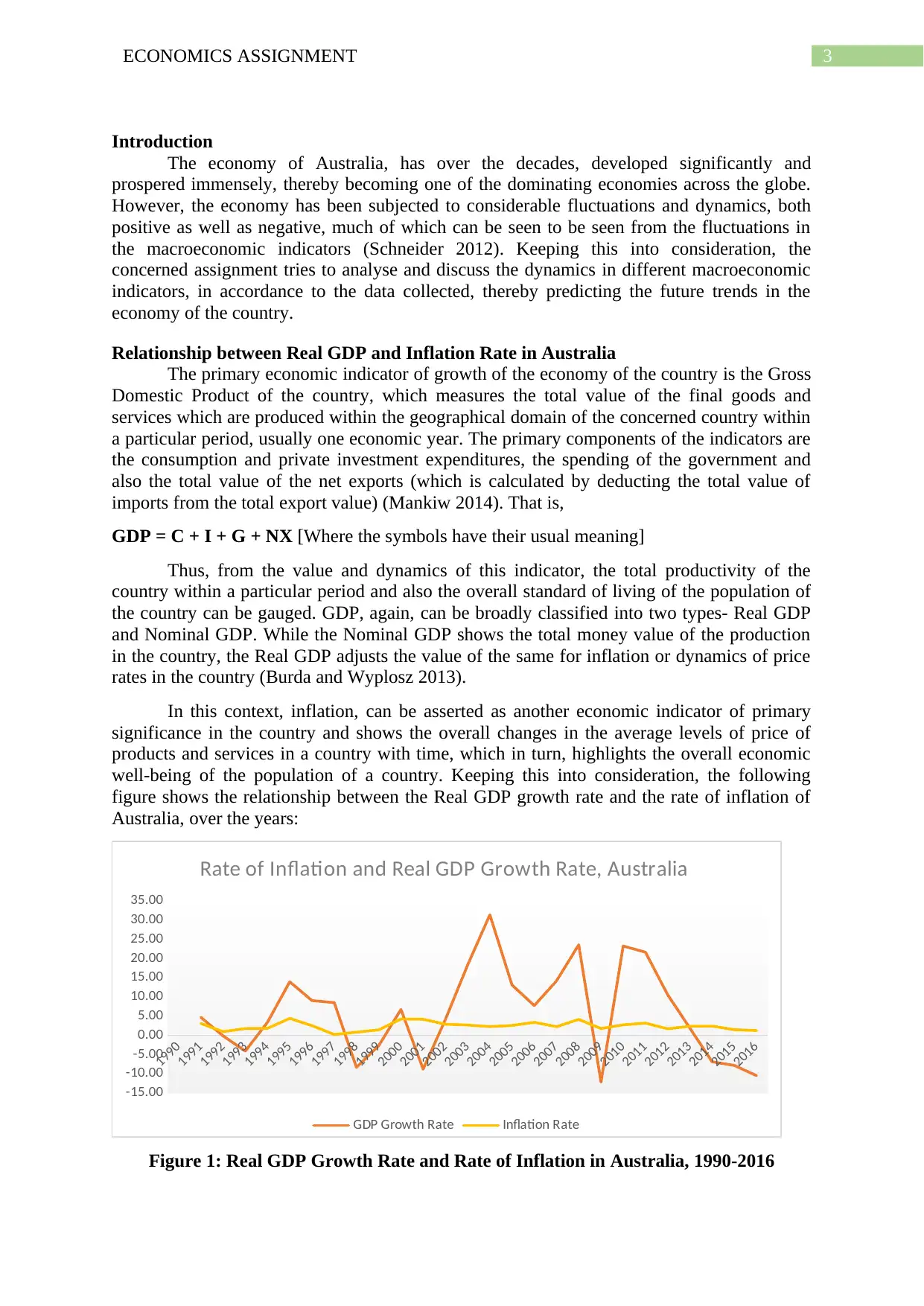

Relationship between Real GDP and Inflation Rate in Australia

The primary economic indicator of growth of the economy of the country is the Gross

Domestic Product of the country, which measures the total value of the final goods and

services which are produced within the geographical domain of the concerned country within

a particular period, usually one economic year. The primary components of the indicators are

the consumption and private investment expenditures, the spending of the government and

also the total value of the net exports (which is calculated by deducting the total value of

imports from the total export value) (Mankiw 2014). That is,

GDP = C + I + G + NX [Where the symbols have their usual meaning]

Thus, from the value and dynamics of this indicator, the total productivity of the

country within a particular period and also the overall standard of living of the population of

the country can be gauged. GDP, again, can be broadly classified into two types- Real GDP

and Nominal GDP. While the Nominal GDP shows the total money value of the production

in the country, the Real GDP adjusts the value of the same for inflation or dynamics of price

rates in the country (Burda and Wyplosz 2013).

In this context, inflation, can be asserted as another economic indicator of primary

significance in the country and shows the overall changes in the average levels of price of

products and services in a country with time, which in turn, highlights the overall economic

well-being of the population of a country. Keeping this into consideration, the following

figure shows the relationship between the Real GDP growth rate and the rate of inflation of

Australia, over the years:

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

Rate of Inflation and Real GDP Growth Rate, Australia

GDP Growth Rate Inflation Rate

Figure 1: Real GDP Growth Rate and Rate of Inflation in Australia, 1990-2016

Introduction

The economy of Australia, has over the decades, developed significantly and

prospered immensely, thereby becoming one of the dominating economies across the globe.

However, the economy has been subjected to considerable fluctuations and dynamics, both

positive as well as negative, much of which can be seen to be seen from the fluctuations in

the macroeconomic indicators (Schneider 2012). Keeping this into consideration, the

concerned assignment tries to analyse and discuss the dynamics in different macroeconomic

indicators, in accordance to the data collected, thereby predicting the future trends in the

economy of the country.

Relationship between Real GDP and Inflation Rate in Australia

The primary economic indicator of growth of the economy of the country is the Gross

Domestic Product of the country, which measures the total value of the final goods and

services which are produced within the geographical domain of the concerned country within

a particular period, usually one economic year. The primary components of the indicators are

the consumption and private investment expenditures, the spending of the government and

also the total value of the net exports (which is calculated by deducting the total value of

imports from the total export value) (Mankiw 2014). That is,

GDP = C + I + G + NX [Where the symbols have their usual meaning]

Thus, from the value and dynamics of this indicator, the total productivity of the

country within a particular period and also the overall standard of living of the population of

the country can be gauged. GDP, again, can be broadly classified into two types- Real GDP

and Nominal GDP. While the Nominal GDP shows the total money value of the production

in the country, the Real GDP adjusts the value of the same for inflation or dynamics of price

rates in the country (Burda and Wyplosz 2013).

In this context, inflation, can be asserted as another economic indicator of primary

significance in the country and shows the overall changes in the average levels of price of

products and services in a country with time, which in turn, highlights the overall economic

well-being of the population of a country. Keeping this into consideration, the following

figure shows the relationship between the Real GDP growth rate and the rate of inflation of

Australia, over the years:

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

Rate of Inflation and Real GDP Growth Rate, Australia

GDP Growth Rate Inflation Rate

Figure 1: Real GDP Growth Rate and Rate of Inflation in Australia, 1990-2016

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ECONOMICS ASSIGNMENT

(Source: Abs.gov.au 2018)

From the above figure, showing the dynamics of the rate of inflation and that of the

Real GDP Growth Rate of Australia, over the years (1990-2016), it can be asserted that the

GDP Growth Rate of the country has been subjected to considerable fluctuations, both

positive as well as negative, over the years, with the rate becoming negative in 1993,1998,

2001, 2009 and 2014-2015 onwards (Dyster and Meredith 2012). Much of this can be

attributes to the national or international financial and economic crisis periods (like that in

2008-2009, which marked the occurrence of the Global Financial Crisis) and so on. Again,

the indicator also shows growth rates as high as 30% in 2004 and nearly 25% in 2011.

However, the rate of inflation of the country, unlike that of the former indicator,

shows a highly stable and more or less moderate trend over the concerned period, with the

rates ranging between 1% to 4%. This in turn, indicates towards the presence of an economic

stability and a good health of the economy as a whole contributing to the overall well-being

of the residents of the country (Gregory and Smith 2016).

Relationship between the Rate of Unemployment and Real GDP Growth Rate of

Australia

Apart from the rate of inflation, another economic indicator of considerable

significance in a country, is that of the rate of unemployment in the country. This is because

the level of employment and job creation in a country depicts the economic welfare of the

population of the country as a whole, their purchasing power, demand patterns, which in turn

have implications on the overall economic productivity or GDP of the concerned country

(Argy and Nevile 2016). Keeping this into consideration, the relationship between the rate of

unemployment and Growth Rate of Real GDP can be seen as follows:

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

-15

-10

-5

0

5

10

15

20

25

30

35

Rate of Unemployment and Real GDP Growth Rate

GDP Growth Rate Unemployment Rate

Figure 2: Rate of Unemployment and Growth Rate of Real GDP in Australia, 1990-2016

(Source: Abs.gov.au 2018)

In the theoretical framework of economics, there is a concept known as the Okun’s

Law, which indicates towards the presence of a relationship between the rate of

(Source: Abs.gov.au 2018)

From the above figure, showing the dynamics of the rate of inflation and that of the

Real GDP Growth Rate of Australia, over the years (1990-2016), it can be asserted that the

GDP Growth Rate of the country has been subjected to considerable fluctuations, both

positive as well as negative, over the years, with the rate becoming negative in 1993,1998,

2001, 2009 and 2014-2015 onwards (Dyster and Meredith 2012). Much of this can be

attributes to the national or international financial and economic crisis periods (like that in

2008-2009, which marked the occurrence of the Global Financial Crisis) and so on. Again,

the indicator also shows growth rates as high as 30% in 2004 and nearly 25% in 2011.

However, the rate of inflation of the country, unlike that of the former indicator,

shows a highly stable and more or less moderate trend over the concerned period, with the

rates ranging between 1% to 4%. This in turn, indicates towards the presence of an economic

stability and a good health of the economy as a whole contributing to the overall well-being

of the residents of the country (Gregory and Smith 2016).

Relationship between the Rate of Unemployment and Real GDP Growth Rate of

Australia

Apart from the rate of inflation, another economic indicator of considerable

significance in a country, is that of the rate of unemployment in the country. This is because

the level of employment and job creation in a country depicts the economic welfare of the

population of the country as a whole, their purchasing power, demand patterns, which in turn

have implications on the overall economic productivity or GDP of the concerned country

(Argy and Nevile 2016). Keeping this into consideration, the relationship between the rate of

unemployment and Growth Rate of Real GDP can be seen as follows:

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

-15

-10

-5

0

5

10

15

20

25

30

35

Rate of Unemployment and Real GDP Growth Rate

GDP Growth Rate Unemployment Rate

Figure 2: Rate of Unemployment and Growth Rate of Real GDP in Australia, 1990-2016

(Source: Abs.gov.au 2018)

In the theoretical framework of economics, there is a concept known as the Okun’s

Law, which indicates towards the presence of a relationship between the rate of

5ECONOMICS ASSIGNMENT

unemployment and GDP in a country. As per this law, with 1% fall in the GDP of the

country, the unemployment usually increases by 2% and vice versa.

Keeping this into consideration, in case of Australia, it can be seen that during 1990-

1991, both the indicators showed increasing trends, thereby denying the Okun’s Law.

However, in 2001-2004, the trends in the concerned indicators are seen to follow the Okun’s

Law, as can be seen from the increasing trend of the GDP and a simultaneously decreasing

trend in unemployment of the concerned country. Again, during 2008-2009, at the times of

Global Financial Crisis, the GDP of Australia can be seen to be decreasing sharply and the

unemployment also increased to some extent, which also asserts the previous observations

(Blanchflower et al. 2014). However, in an overall framework, the rate of unemployment of

the concerned country can be seen to be more stable than that of the Real GDP of Australia.

Business Cycle in Australia

The term “Business Cycle”, in the conceptual framework of economics, refers to the

series of cycles of contraction and expansion of economies with time, which in other words

refers to the natural dynamics in the economic growth of a country or a region over time. In

general, a business cycle consists of four stages which are:

Expansion

Peak

Contraction

Trough (Galí 2015)

Figure 3: Business Cycle in an economy

(Source: As created by the author)

The nature of business cycle in an economy helps in analysing the trends as well as

the overall health of the economy over a period.

Keeping this into consideration, in case of Australian economy, the presence of a

business cycle can be clearly asserted. The economy of Australia experienced expansionary

phases in 2001-2004, 2006-2008. On the other hand, in 2008-2009, the growth of the

economy of the country experienced immense decline, owing to the occurrence of the Global

Financial Crisis, which affected the country considerably and this period, which drove the

unemployment and GDP in a country. As per this law, with 1% fall in the GDP of the

country, the unemployment usually increases by 2% and vice versa.

Keeping this into consideration, in case of Australia, it can be seen that during 1990-

1991, both the indicators showed increasing trends, thereby denying the Okun’s Law.

However, in 2001-2004, the trends in the concerned indicators are seen to follow the Okun’s

Law, as can be seen from the increasing trend of the GDP and a simultaneously decreasing

trend in unemployment of the concerned country. Again, during 2008-2009, at the times of

Global Financial Crisis, the GDP of Australia can be seen to be decreasing sharply and the

unemployment also increased to some extent, which also asserts the previous observations

(Blanchflower et al. 2014). However, in an overall framework, the rate of unemployment of

the concerned country can be seen to be more stable than that of the Real GDP of Australia.

Business Cycle in Australia

The term “Business Cycle”, in the conceptual framework of economics, refers to the

series of cycles of contraction and expansion of economies with time, which in other words

refers to the natural dynamics in the economic growth of a country or a region over time. In

general, a business cycle consists of four stages which are:

Expansion

Peak

Contraction

Trough (Galí 2015)

Figure 3: Business Cycle in an economy

(Source: As created by the author)

The nature of business cycle in an economy helps in analysing the trends as well as

the overall health of the economy over a period.

Keeping this into consideration, in case of Australian economy, the presence of a

business cycle can be clearly asserted. The economy of Australia experienced expansionary

phases in 2001-2004, 2006-2008. On the other hand, in 2008-2009, the growth of the

economy of the country experienced immense decline, owing to the occurrence of the Global

Financial Crisis, which affected the country considerably and this period, which drove the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ECONOMICS ASSIGNMENT

economic growth rate from its peak in 2008, to a negative trough in 2009, can be termed as a

recessionary or contractionary phase for the country, following which the economy of the

country can be seen to enter into a phase of recovery. These movements in the economic

growth of the country indicates towards the clear presence of business cycle in the economy

of Australia (Morley and Piger 2012).

Net exports and Real Exchange rates (Australia and USA)

A significant component of the GDP of a country, as discussed above, is the value of

the net exports of the country, which in turn shows the value of total exports less the value of

total imports by the same. On the other hand, the exchange rate of the domestic currency of a

country is the price of the same in terms of the value of the domestic currency of the country

in comparison. In general, while measuring the exchange rate dynamics of a country, the

value of the currency of the USA, that is the value of US dollar is taken as a yardstick and the

concerned currency and its exchange rate is measured with respect to the value of the dollar.

Keeping this into account, the exchange rate of AUD against USD and the net exports

of the same, within the time period of 1990-2016, as well as the relationship between the two

variables (if any) can be seen from the following figure:

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

-30.00

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

Net Exports and Exchange Rate

Exchange Rate Net Exports

Figure 4: Relationship between the Real exchange rate and Net Exports

(Source: Abs.gov.au 2018)

As is evident from the above figure, the rate of change of the exchange rate of the

domestic currency of Australia with that of the US dollars, has remained more or less stable,

over the concerned period of time. However, as far as the international trade dynamics of the

country is concerned, it can be seen that the net exports of Australia, barring a few

fluctuations, has most of the time, remained negative, which in turn, indicates towards the

fact that country has over the years remained a net importer of goods and services from other

countries. Only in 2011, the country can be seen to have positive net exports (Handley 2014).

Australia in general exports minerals, precious metals like gold, iron ore, coal and petroleum

gas and is the 23rd largest exporting countries in the global scenario. However, the country is

one of the biggest importers in the world, the import basket of the country mainly consisting

of automobiles, refined petroleum, computers and technological commodities.

economic growth rate from its peak in 2008, to a negative trough in 2009, can be termed as a

recessionary or contractionary phase for the country, following which the economy of the

country can be seen to enter into a phase of recovery. These movements in the economic

growth of the country indicates towards the clear presence of business cycle in the economy

of Australia (Morley and Piger 2012).

Net exports and Real Exchange rates (Australia and USA)

A significant component of the GDP of a country, as discussed above, is the value of

the net exports of the country, which in turn shows the value of total exports less the value of

total imports by the same. On the other hand, the exchange rate of the domestic currency of a

country is the price of the same in terms of the value of the domestic currency of the country

in comparison. In general, while measuring the exchange rate dynamics of a country, the

value of the currency of the USA, that is the value of US dollar is taken as a yardstick and the

concerned currency and its exchange rate is measured with respect to the value of the dollar.

Keeping this into account, the exchange rate of AUD against USD and the net exports

of the same, within the time period of 1990-2016, as well as the relationship between the two

variables (if any) can be seen from the following figure:

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

-30.00

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

Net Exports and Exchange Rate

Exchange Rate Net Exports

Figure 4: Relationship between the Real exchange rate and Net Exports

(Source: Abs.gov.au 2018)

As is evident from the above figure, the rate of change of the exchange rate of the

domestic currency of Australia with that of the US dollars, has remained more or less stable,

over the concerned period of time. However, as far as the international trade dynamics of the

country is concerned, it can be seen that the net exports of Australia, barring a few

fluctuations, has most of the time, remained negative, which in turn, indicates towards the

fact that country has over the years remained a net importer of goods and services from other

countries. Only in 2011, the country can be seen to have positive net exports (Handley 2014).

Australia in general exports minerals, precious metals like gold, iron ore, coal and petroleum

gas and is the 23rd largest exporting countries in the global scenario. However, the country is

one of the biggest importers in the world, the import basket of the country mainly consisting

of automobiles, refined petroleum, computers and technological commodities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ECONOMICS ASSIGNMENT

In order to analyse the presence or absence of any relationship between the net

exports and the exchange rate of the concerned country, it is of utmost importance to define

and differentiate the concepts of real and nominal exchange rates of the currency of a

country. While the latter shows the amount of the domestic currency of the concerned

country which needs to be exchanged in order to receive one unit of the foreign currency, the

former shows the bundle of domestic commodities and services which needs to be exchanged

in order to acquire a specific bundle of foreign goods and services.

In general, there exists robust relationship between the real exchange rate in the

country and the net exports of the same, in the sense that with an increase in the real

exchange rate, the capacity to import foreign goods and services and the value of the

domestic currency with respect to that of the foreign currency in comparison increase, which

in turn leads to an increase in the overall imports and vice versa (Thurbon 2015).

In this context, it can be seen that in case of Australia, the exchange rate can be seen

to be seen to be more or less stable in terms of USD over the period, with the rates fluctuating

little and remaining within the range of 0.6 to 1 USD in general. On the contrary, the net

exports and trade balance of the country can be seen to be considerably fluctuating within the

concerned period of time.

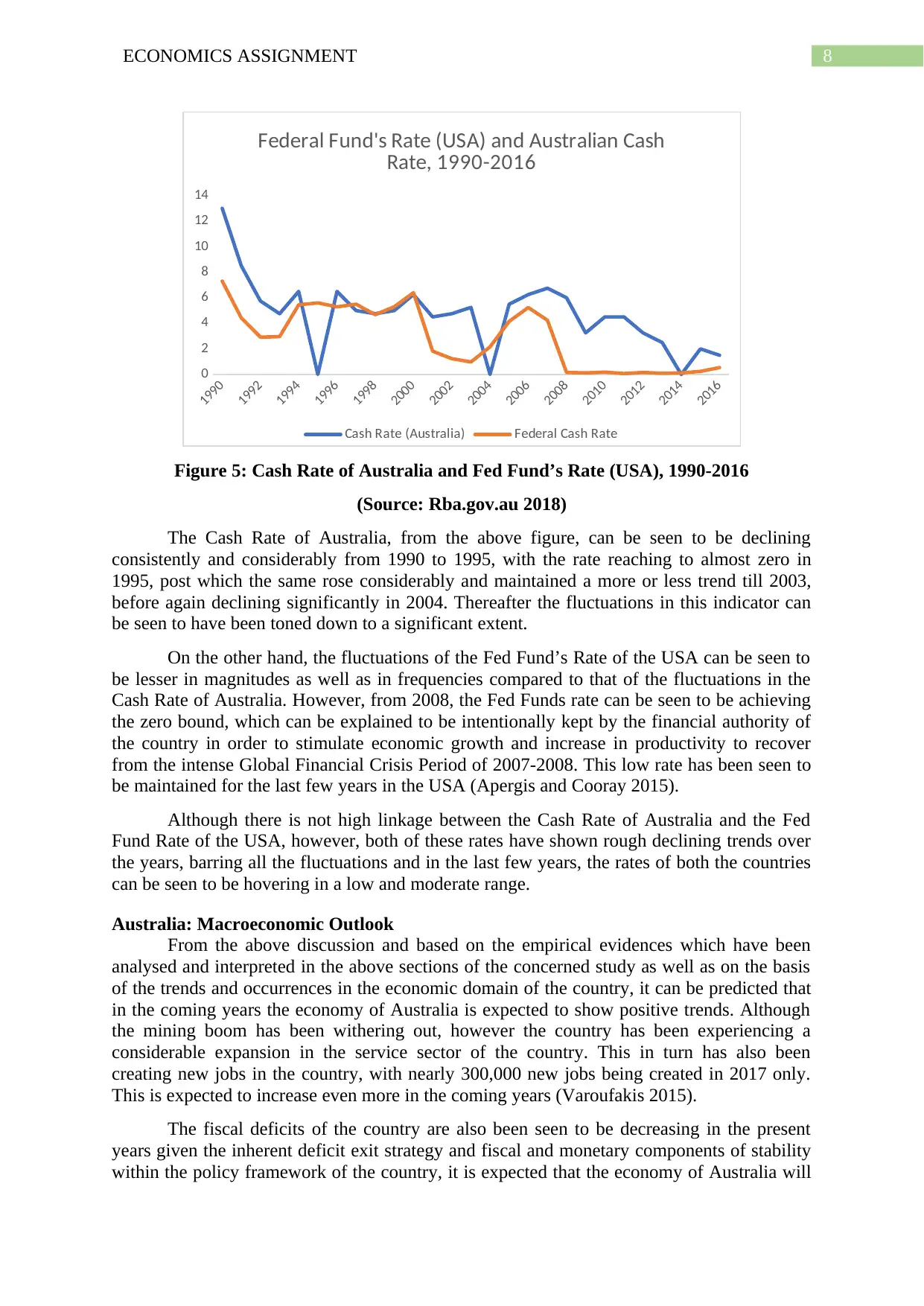

Relationship between the Cash Rate (Australia) and Federal Fund’s Rate (USA)

The Cash Rate in case of Australia or the Fed Funds Rate in case of the USA, refers to

the rate of interest which the central monetary institutions of the countries charge from the

commercial banks in case of overnight borrowings of money by the latter from the former.

This in turn, acts as one of the primary variables in the monetary market mechanism as well

as the monetary policy decisions in the country and also provides an insight about the

inflation dynamics in the country.

In case of Australia, specifically, the monetary authority, that is, the Reserve Bank of

Australia, forms the monetary policies with the objectives of inflation targeting in general, in

the domain of which a targeted inflation rate is set at the beginning of a period and then the

policy frameworks are designed to achieve the targeted rate of inflation, of which the cash

rate is an integral tool. When the rate of inflation existing in the economy of Australia is less

than the targeted level to be achieved, the RBA general lowers the cash rate, which in turn

leads to a decline in the rate of interest in the economy as a whole, thereby encouraging

borrowings of money and increase in the aggregate demand as a whole (Deans and Stewart

2012). This in turn raises the overall price levels in the economy, thereby taking the rate of

inflation to the targeted level and vice-versa.

In contrast, the structure implemented by the Federal Reserve, that is, the monetary

authority of the USA, for controlling and manipulating the funds rate, is that of the forward

guidance method. Under this method, the central monetary institution of the country makes

the monetary policies on the basis of their own forecasts and future expectations regarding

the levels of prices and interest rates in the economy. The Fed adopts this policy framework

and manipulates the interest rates accordingly for the monetary welfare of the economy as a

whole.

Keeping this into consideration, the dynamics in the Cash Rate of Australia and the

Fed Funds Rate of the USA, within the time period of 1990-2016 and their inter-relationships

and connections (if any), within the concerned period, can be seen from the following figure:

In order to analyse the presence or absence of any relationship between the net

exports and the exchange rate of the concerned country, it is of utmost importance to define

and differentiate the concepts of real and nominal exchange rates of the currency of a

country. While the latter shows the amount of the domestic currency of the concerned

country which needs to be exchanged in order to receive one unit of the foreign currency, the

former shows the bundle of domestic commodities and services which needs to be exchanged

in order to acquire a specific bundle of foreign goods and services.

In general, there exists robust relationship between the real exchange rate in the

country and the net exports of the same, in the sense that with an increase in the real

exchange rate, the capacity to import foreign goods and services and the value of the

domestic currency with respect to that of the foreign currency in comparison increase, which

in turn leads to an increase in the overall imports and vice versa (Thurbon 2015).

In this context, it can be seen that in case of Australia, the exchange rate can be seen

to be seen to be more or less stable in terms of USD over the period, with the rates fluctuating

little and remaining within the range of 0.6 to 1 USD in general. On the contrary, the net

exports and trade balance of the country can be seen to be considerably fluctuating within the

concerned period of time.

Relationship between the Cash Rate (Australia) and Federal Fund’s Rate (USA)

The Cash Rate in case of Australia or the Fed Funds Rate in case of the USA, refers to

the rate of interest which the central monetary institutions of the countries charge from the

commercial banks in case of overnight borrowings of money by the latter from the former.

This in turn, acts as one of the primary variables in the monetary market mechanism as well

as the monetary policy decisions in the country and also provides an insight about the

inflation dynamics in the country.

In case of Australia, specifically, the monetary authority, that is, the Reserve Bank of

Australia, forms the monetary policies with the objectives of inflation targeting in general, in

the domain of which a targeted inflation rate is set at the beginning of a period and then the

policy frameworks are designed to achieve the targeted rate of inflation, of which the cash

rate is an integral tool. When the rate of inflation existing in the economy of Australia is less

than the targeted level to be achieved, the RBA general lowers the cash rate, which in turn

leads to a decline in the rate of interest in the economy as a whole, thereby encouraging

borrowings of money and increase in the aggregate demand as a whole (Deans and Stewart

2012). This in turn raises the overall price levels in the economy, thereby taking the rate of

inflation to the targeted level and vice-versa.

In contrast, the structure implemented by the Federal Reserve, that is, the monetary

authority of the USA, for controlling and manipulating the funds rate, is that of the forward

guidance method. Under this method, the central monetary institution of the country makes

the monetary policies on the basis of their own forecasts and future expectations regarding

the levels of prices and interest rates in the economy. The Fed adopts this policy framework

and manipulates the interest rates accordingly for the monetary welfare of the economy as a

whole.

Keeping this into consideration, the dynamics in the Cash Rate of Australia and the

Fed Funds Rate of the USA, within the time period of 1990-2016 and their inter-relationships

and connections (if any), within the concerned period, can be seen from the following figure:

8ECONOMICS ASSIGNMENT

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

0

2

4

6

8

10

12

14

Federal Fund's Rate (USA) and Australian Cash

Rate, 1990-2016

Cash Rate (Australia) Federal Cash Rate

Figure 5: Cash Rate of Australia and Fed Fund’s Rate (USA), 1990-2016

(Source: Rba.gov.au 2018)

The Cash Rate of Australia, from the above figure, can be seen to be declining

consistently and considerably from 1990 to 1995, with the rate reaching to almost zero in

1995, post which the same rose considerably and maintained a more or less trend till 2003,

before again declining significantly in 2004. Thereafter the fluctuations in this indicator can

be seen to have been toned down to a significant extent.

On the other hand, the fluctuations of the Fed Fund’s Rate of the USA can be seen to

be lesser in magnitudes as well as in frequencies compared to that of the fluctuations in the

Cash Rate of Australia. However, from 2008, the Fed Funds rate can be seen to be achieving

the zero bound, which can be explained to be intentionally kept by the financial authority of

the country in order to stimulate economic growth and increase in productivity to recover

from the intense Global Financial Crisis Period of 2007-2008. This low rate has been seen to

be maintained for the last few years in the USA (Apergis and Cooray 2015).

Although there is not high linkage between the Cash Rate of Australia and the Fed

Fund Rate of the USA, however, both of these rates have shown rough declining trends over

the years, barring all the fluctuations and in the last few years, the rates of both the countries

can be seen to be hovering in a low and moderate range.

Australia: Macroeconomic Outlook

From the above discussion and based on the empirical evidences which have been

analysed and interpreted in the above sections of the concerned study as well as on the basis

of the trends and occurrences in the economic domain of the country, it can be predicted that

in the coming years the economy of Australia is expected to show positive trends. Although

the mining boom has been withering out, however the country has been experiencing a

considerable expansion in the service sector of the country. This in turn has also been

creating new jobs in the country, with nearly 300,000 new jobs being created in 2017 only.

This is expected to increase even more in the coming years (Varoufakis 2015).

The fiscal deficits of the country are also been seen to be decreasing in the present

years given the inherent deficit exit strategy and fiscal and monetary components of stability

within the policy framework of the country, it is expected that the economy of Australia will

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

0

2

4

6

8

10

12

14

Federal Fund's Rate (USA) and Australian Cash

Rate, 1990-2016

Cash Rate (Australia) Federal Cash Rate

Figure 5: Cash Rate of Australia and Fed Fund’s Rate (USA), 1990-2016

(Source: Rba.gov.au 2018)

The Cash Rate of Australia, from the above figure, can be seen to be declining

consistently and considerably from 1990 to 1995, with the rate reaching to almost zero in

1995, post which the same rose considerably and maintained a more or less trend till 2003,

before again declining significantly in 2004. Thereafter the fluctuations in this indicator can

be seen to have been toned down to a significant extent.

On the other hand, the fluctuations of the Fed Fund’s Rate of the USA can be seen to

be lesser in magnitudes as well as in frequencies compared to that of the fluctuations in the

Cash Rate of Australia. However, from 2008, the Fed Funds rate can be seen to be achieving

the zero bound, which can be explained to be intentionally kept by the financial authority of

the country in order to stimulate economic growth and increase in productivity to recover

from the intense Global Financial Crisis Period of 2007-2008. This low rate has been seen to

be maintained for the last few years in the USA (Apergis and Cooray 2015).

Although there is not high linkage between the Cash Rate of Australia and the Fed

Fund Rate of the USA, however, both of these rates have shown rough declining trends over

the years, barring all the fluctuations and in the last few years, the rates of both the countries

can be seen to be hovering in a low and moderate range.

Australia: Macroeconomic Outlook

From the above discussion and based on the empirical evidences which have been

analysed and interpreted in the above sections of the concerned study as well as on the basis

of the trends and occurrences in the economic domain of the country, it can be predicted that

in the coming years the economy of Australia is expected to show positive trends. Although

the mining boom has been withering out, however the country has been experiencing a

considerable expansion in the service sector of the country. This in turn has also been

creating new jobs in the country, with nearly 300,000 new jobs being created in 2017 only.

This is expected to increase even more in the coming years (Varoufakis 2015).

The fiscal deficits of the country are also been seen to be decreasing in the present

years given the inherent deficit exit strategy and fiscal and monetary components of stability

within the policy framework of the country, it is expected that the economy of Australia will

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ECONOMICS ASSIGNMENT

mitigate any unanticipated downturn in the economy, provided the magnitude of the

downturn is not considerably huge and unmanageable and also given that the exogenous

economic condition of the world maintains stable trends. In the recent period, the inflation of

the country can be seen to be remaining at a moderate and stable rate while the

unemployment trait shows a gradual decline. This, clubbed with the impressive dynamics in

the GDP of the country together indicate towards positive economic growth trend in the

coming years. However, with the increase in the level of employments and the purchasing

power of a greater share of population of the country, the aggregate demand is expected to

increase, which may lead to a higher inflationary pressure in the coming years.

Conclusion

From the above discussions and analysis of the empirical evidences collected and

evaluated, it can be concluded that the economy of Australia has been in an overall stable

state in the current period. This can be seen from the performances of the primary indicators

like GDP, inflation and unemployment rates in the country. The exchange rate of AUD can

be seen to have maintained stability although significant dynamics could be observed in the

aspects of net export volumes, the trends being mostly negative. However, with new jobs

being created and with the rise in the aggregate demand in the country, Australia is expected

to face an inflationary pressure in the coming years.

mitigate any unanticipated downturn in the economy, provided the magnitude of the

downturn is not considerably huge and unmanageable and also given that the exogenous

economic condition of the world maintains stable trends. In the recent period, the inflation of

the country can be seen to be remaining at a moderate and stable rate while the

unemployment trait shows a gradual decline. This, clubbed with the impressive dynamics in

the GDP of the country together indicate towards positive economic growth trend in the

coming years. However, with the increase in the level of employments and the purchasing

power of a greater share of population of the country, the aggregate demand is expected to

increase, which may lead to a higher inflationary pressure in the coming years.

Conclusion

From the above discussions and analysis of the empirical evidences collected and

evaluated, it can be concluded that the economy of Australia has been in an overall stable

state in the current period. This can be seen from the performances of the primary indicators

like GDP, inflation and unemployment rates in the country. The exchange rate of AUD can

be seen to have maintained stability although significant dynamics could be observed in the

aspects of net export volumes, the trends being mostly negative. However, with new jobs

being created and with the rise in the aggregate demand in the country, Australia is expected

to face an inflationary pressure in the coming years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ECONOMICS ASSIGNMENT

References

Abs.gov.au (2018). 1345.0 - Key Economic Indicators, 2018. [online] Abs.gov.au. Available

at: http://www.abs.gov.au/AUSSTATS/abs@.nsf/mf/1345.0?

opendocument#LabourForceandDemography [Accessed 22 May 2018].

Abs.gov.au (2018). 5206.0 - Australian National Accounts: National Income, Expenditure

and Product, Dec 2017. [online] Abs.gov.au. Available at:

http://www.abs.gov.au/ausstats/abs@.nsf/mf/5206.0 [Accessed 22 May 2018].

Abs.gov.au (2018). 5368.0 - International Trade in Goods and Services, Australia, Mar

2018. [online] Abs.gov.au. Available at:

http://www.abs.gov.au/ausstats/abs@.nsf/0/A5FB33BD2E3CC68FCA257496001547A1?

Opendocument [Accessed 22 May 2018].

Abs.gov.au (2018). 6401.0 - Consumer Price Index, Australia, Mar 2018. [online]

Abs.gov.au. Available at:

http://www.abs.gov.au/ausstats/abs@.nsf/0/938DA570A34A8EDACA2568A900139350?

Opendocument [Accessed 22 May 2018].

Apergis, N. and Cooray, A., 2015. Asymmetric interest rate pass-through in the US, the UK

and Australia: New evidence from selected individual banks. Journal of

Macroeconomics, 45, pp.155-172.

Argy, V.E. and Nevile, J. eds., 2016. Inflation and Unemployment: Theory, Experience and

Policy Making. Routledge.

Blanchflower, D.G., Bell, D.N., Montagnoli, A. and Moro, M., 2014. The Happiness Trade‐

Off between Unemployment and Inflation. Journal of Money, Credit and Banking, 46(S2),

pp.117-141.

Burda, M. and Wyplosz, C., 2013. Macroeconomics: a European text. Oxford university

press.

Deans, C. and Stewart, C., 2012. Banks’ funding costs and lending rates. Reserve Bank of

Australia Bulletin, 2012, pp.37-43.

Dyster, B. and Meredith, D., 2012. Australia in the global economy: continuity and change.

Cambridge University Press.

Galí, J., 2015. Monetary policy, inflation, and the business cycle: an introduction to the new

Keynesian framework and its applications. Princeton University Press.

Gregory, R.G. and Smith, R.E., 2016. 15 Unemployment, Inflation and Job Creation Policies

in Australia. Inflation and Unemployment: Theory, Experience and Policy Making, p.325.

Handley, K., 2014. Exporting under trade policy uncertainty: Theory and evidence. Journal

of International Economics, 94(1), pp.50-66.

Mankiw, N.G., 2014. Principles of macroeconomics. Cengage Learning.

Morley, J. and Piger, J., 2012. The asymmetric business cycle. Review of Economics and

Statistics, 94(1), pp.208-221.

Rba.gov.au (2018). Cash Rate | RBA. [online] Reserve Bank of Australia. Available at:

http://www.rba.gov.au/statistics/cash-rate/ [Accessed 22 May 2018].

References

Abs.gov.au (2018). 1345.0 - Key Economic Indicators, 2018. [online] Abs.gov.au. Available

at: http://www.abs.gov.au/AUSSTATS/abs@.nsf/mf/1345.0?

opendocument#LabourForceandDemography [Accessed 22 May 2018].

Abs.gov.au (2018). 5206.0 - Australian National Accounts: National Income, Expenditure

and Product, Dec 2017. [online] Abs.gov.au. Available at:

http://www.abs.gov.au/ausstats/abs@.nsf/mf/5206.0 [Accessed 22 May 2018].

Abs.gov.au (2018). 5368.0 - International Trade in Goods and Services, Australia, Mar

2018. [online] Abs.gov.au. Available at:

http://www.abs.gov.au/ausstats/abs@.nsf/0/A5FB33BD2E3CC68FCA257496001547A1?

Opendocument [Accessed 22 May 2018].

Abs.gov.au (2018). 6401.0 - Consumer Price Index, Australia, Mar 2018. [online]

Abs.gov.au. Available at:

http://www.abs.gov.au/ausstats/abs@.nsf/0/938DA570A34A8EDACA2568A900139350?

Opendocument [Accessed 22 May 2018].

Apergis, N. and Cooray, A., 2015. Asymmetric interest rate pass-through in the US, the UK

and Australia: New evidence from selected individual banks. Journal of

Macroeconomics, 45, pp.155-172.

Argy, V.E. and Nevile, J. eds., 2016. Inflation and Unemployment: Theory, Experience and

Policy Making. Routledge.

Blanchflower, D.G., Bell, D.N., Montagnoli, A. and Moro, M., 2014. The Happiness Trade‐

Off between Unemployment and Inflation. Journal of Money, Credit and Banking, 46(S2),

pp.117-141.

Burda, M. and Wyplosz, C., 2013. Macroeconomics: a European text. Oxford university

press.

Deans, C. and Stewart, C., 2012. Banks’ funding costs and lending rates. Reserve Bank of

Australia Bulletin, 2012, pp.37-43.

Dyster, B. and Meredith, D., 2012. Australia in the global economy: continuity and change.

Cambridge University Press.

Galí, J., 2015. Monetary policy, inflation, and the business cycle: an introduction to the new

Keynesian framework and its applications. Princeton University Press.

Gregory, R.G. and Smith, R.E., 2016. 15 Unemployment, Inflation and Job Creation Policies

in Australia. Inflation and Unemployment: Theory, Experience and Policy Making, p.325.

Handley, K., 2014. Exporting under trade policy uncertainty: Theory and evidence. Journal

of International Economics, 94(1), pp.50-66.

Mankiw, N.G., 2014. Principles of macroeconomics. Cengage Learning.

Morley, J. and Piger, J., 2012. The asymmetric business cycle. Review of Economics and

Statistics, 94(1), pp.208-221.

Rba.gov.au (2018). Cash Rate | RBA. [online] Reserve Bank of Australia. Available at:

http://www.rba.gov.au/statistics/cash-rate/ [Accessed 22 May 2018].

11ECONOMICS ASSIGNMENT

Schneider, F., 2012. Size and development of the shadow economy of 31 European and 5

other OECD countries from 2003 to 2012: some new facts. Accessed June, 13, p.2015.

Thurbon, E., 2015. 10 years after the Australia-US free trade agreement: where to for

Australia’s trade policy?. Australian Journal of International Affairs, 69(5), pp.463-467.

Varoufakis, Y., 2015. The global minotaur: America, Europe and the future of the global

economy. Zed Books Ltd..

Schneider, F., 2012. Size and development of the shadow economy of 31 European and 5

other OECD countries from 2003 to 2012: some new facts. Accessed June, 13, p.2015.

Thurbon, E., 2015. 10 years after the Australia-US free trade agreement: where to for

Australia’s trade policy?. Australian Journal of International Affairs, 69(5), pp.463-467.

Varoufakis, Y., 2015. The global minotaur: America, Europe and the future of the global

economy. Zed Books Ltd..

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.