Macroeconomics Individual Project on the 2007 US Economic Crisis

VerifiedAdded on 2023/06/18

|13

|3962

|397

AI Summary

This individual project for TECO602 Macroeconomics explains the origin, extent, and effects of the 2007 US economic crisis on GDP, inflation rate, labor market, consumption, investment, and government budget. It also suggests policy remedies for macroeconomic variables.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Individual project for

TECO602

Macroeconomics

TECO602

Macroeconomics

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

1. Explain the origin of this crisis. Provide a summary of this crisis, consisting of the reasons of this

crisis, and the breadth and extent of the crisis. Identify countries and markets involved in the crisis....3

2. Explain the effect of this crisis on USA’s GDP in long-run?..................................................................3

3. Explain the effect of this crisis on USA’s inflation rate in long-run?.....................................................4

4. Explain the effect of this crisis on USA’s labour market in long-run?...................................................4

5. Explain the effect of this crisis on the levels of Americans’ consumption in long-run?.......................5

6. Explain the effect of this crisis on the levels of USA’s investment in long-run?...................................5

7. Explain the effect of this crisis on USA government’s Budget in long-run?.........................................6

8. Assume that you are a policy maker in USA’s government and central bank; how you can recover

the crisis by changing macroeconomic variables?...................................................................................7

9. During the crisis, How USA can recover its output gap if it faces an expansionary gap?.....................9

10. During the crisis, How USA can recover its output gap if it faces a contractionary gap?...................9

REFERENCES..............................................................................................................................................11

1. Explain the origin of this crisis. Provide a summary of this crisis, consisting of the reasons of this

crisis, and the breadth and extent of the crisis. Identify countries and markets involved in the crisis....3

2. Explain the effect of this crisis on USA’s GDP in long-run?..................................................................3

3. Explain the effect of this crisis on USA’s inflation rate in long-run?.....................................................4

4. Explain the effect of this crisis on USA’s labour market in long-run?...................................................4

5. Explain the effect of this crisis on the levels of Americans’ consumption in long-run?.......................5

6. Explain the effect of this crisis on the levels of USA’s investment in long-run?...................................5

7. Explain the effect of this crisis on USA government’s Budget in long-run?.........................................6

8. Assume that you are a policy maker in USA’s government and central bank; how you can recover

the crisis by changing macroeconomic variables?...................................................................................7

9. During the crisis, How USA can recover its output gap if it faces an expansionary gap?.....................9

10. During the crisis, How USA can recover its output gap if it faces a contractionary gap?...................9

REFERENCES..............................................................................................................................................11

1. Explain the origin of this crisis. Provide a summary of this crisis, consisting of the reasons of

this crisis, and the breadth and extent of the crisis. Identify countries and markets involved

in the crisis

The economic crisis in the United States started in 2007 as a result of the decline of the US

home financing industry, which resulted in a significant capacity compression. It was on the

verge of collapsing the worldwide monetary system in terms of a business bank's actions, which

included substantial investments, lending institutions, health insurers, and credit and savings

organizations. Since economic hardship travels regularly and does extend to other nations, a

country's crises can influence the economy of other nations. The hardening of financial

conditions, such as rising interest rates, market transaction slowdowns, and a drop in gain

traction, is the primary determinant of financial upheaval. The confidence collapse in various

institutions resulted in economic crisis in 2007. Several of the causes of the financial crisis are as

follows:

Owning to rule, the mortgage credit crunch gave birth to futures. Notwithstanding all

attempts to address these financial issues, the Global Economic Downturn resulted. Furthermore,

due to a drop in monetary base in the US cost - effective approach by the financial meltdown, the

reserve bank of the United States was a significant role in the onset of the global financial. Many

nations were afflicted by the worldwide development of crises, including Mexico, Ireland,

Hungary, the Baltic states, Ukraine, and Russia in Europe, and Brazil in South America. The

following countries, Hong Kong, China, Japan, and India, had a major impact on Asian region.

2. Explain the effect of this crisis on USA’s GDP in long-run?

Even during financial crisis in 2007, the United States' job expansion was favorable, with a

modest increase. The US country's economic output remained generally steady. Although the

increase of the gross domestic product was largely steady, the inflationary effects on the US

industry were limited.

In the United States of America's business in 2008, the nation's worldwide economic

expansion was important. Nevertheless, as the industry continued to be affected by the recession,

the rate of increase slowed dramatically. The United States of America's annual growth rate in

2008 was favorable, with little influence from the financial meltdown.

this crisis, and the breadth and extent of the crisis. Identify countries and markets involved

in the crisis

The economic crisis in the United States started in 2007 as a result of the decline of the US

home financing industry, which resulted in a significant capacity compression. It was on the

verge of collapsing the worldwide monetary system in terms of a business bank's actions, which

included substantial investments, lending institutions, health insurers, and credit and savings

organizations. Since economic hardship travels regularly and does extend to other nations, a

country's crises can influence the economy of other nations. The hardening of financial

conditions, such as rising interest rates, market transaction slowdowns, and a drop in gain

traction, is the primary determinant of financial upheaval. The confidence collapse in various

institutions resulted in economic crisis in 2007. Several of the causes of the financial crisis are as

follows:

Owning to rule, the mortgage credit crunch gave birth to futures. Notwithstanding all

attempts to address these financial issues, the Global Economic Downturn resulted. Furthermore,

due to a drop in monetary base in the US cost - effective approach by the financial meltdown, the

reserve bank of the United States was a significant role in the onset of the global financial. Many

nations were afflicted by the worldwide development of crises, including Mexico, Ireland,

Hungary, the Baltic states, Ukraine, and Russia in Europe, and Brazil in South America. The

following countries, Hong Kong, China, Japan, and India, had a major impact on Asian region.

2. Explain the effect of this crisis on USA’s GDP in long-run?

Even during financial crisis in 2007, the United States' job expansion was favorable, with a

modest increase. The US country's economic output remained generally steady. Although the

increase of the gross domestic product was largely steady, the inflationary effects on the US

industry were limited.

In the United States of America's business in 2008, the nation's worldwide economic

expansion was important. Nevertheless, as the industry continued to be affected by the recession,

the rate of increase slowed dramatically. The United States of America's annual growth rate in

2008 was favorable, with little influence from the financial meltdown.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

However, since 2007 was the first day of the recession, the cost of productivity expansion

was much smaller. The GDP numbers for 2009 provide some indication of the financial crisis

that afflicted the US regional economy. The United States of America started to see strong

economic growth in the second quarter of 2009. The united state was capable of achieving the

greatest positive increase in gross national product in the final quarter of 2009, reducing the

effects of the crisis on the sector.

3. Explain the effect of this crisis on USA’s inflation rate in long-run?

During the economic years of 2007 and 2009, the economic crisis that started of America did not

subside as predicted. Nonetheless, considering the country's economic resilience and the

accompanying fall in jobless underneath the general macroeconomic level of unemployment, it

has remained consistently lower than the economic growth expectations ever since.

Inflation's influence on the US economy was as follows.

1. The worth of the US dollar drops in value, increasing the amount of imports in that country

and contributing to inflationary.

2. Oil and gasoline costs have been steadily rising.

3. Raise the nation's taxes for a long time.

4. The increase in unused capacity was less than anticipated. The rate of interest was zero, and

there were less bank failures than the previous year. In addition, the primary concern this year

was a high unemployment rate relative to the earlier year.

5. By not reducing prices, the companies were able to retain a steady stream of income.

6. A drop in the price of produced supply as a result of the nation's worldwide downturn.

7. The pound was overvalued in comparison to the precious metal. Also, because to the inflated

currency rate, lower inflation.

4. Explain the effect of this crisis on USA’s labour market in long-run?

As during Global Recession, the proportion of moderately connected and disengaged

employees increased significantly, while the workforce participation rate decreased. The

was much smaller. The GDP numbers for 2009 provide some indication of the financial crisis

that afflicted the US regional economy. The United States of America started to see strong

economic growth in the second quarter of 2009. The united state was capable of achieving the

greatest positive increase in gross national product in the final quarter of 2009, reducing the

effects of the crisis on the sector.

3. Explain the effect of this crisis on USA’s inflation rate in long-run?

During the economic years of 2007 and 2009, the economic crisis that started of America did not

subside as predicted. Nonetheless, considering the country's economic resilience and the

accompanying fall in jobless underneath the general macroeconomic level of unemployment, it

has remained consistently lower than the economic growth expectations ever since.

Inflation's influence on the US economy was as follows.

1. The worth of the US dollar drops in value, increasing the amount of imports in that country

and contributing to inflationary.

2. Oil and gasoline costs have been steadily rising.

3. Raise the nation's taxes for a long time.

4. The increase in unused capacity was less than anticipated. The rate of interest was zero, and

there were less bank failures than the previous year. In addition, the primary concern this year

was a high unemployment rate relative to the earlier year.

5. By not reducing prices, the companies were able to retain a steady stream of income.

6. A drop in the price of produced supply as a result of the nation's worldwide downturn.

7. The pound was overvalued in comparison to the precious metal. Also, because to the inflated

currency rate, lower inflation.

4. Explain the effect of this crisis on USA’s labour market in long-run?

As during Global Recession, the proportion of moderately connected and disengaged

employees increased significantly, while the workforce participation rate decreased. The

percentage of workers who report laboring portion unwillingly for financial reasons is still

significant. At its lowest point, the rate was 17%. As a result, unemployment rates soared in

during Great Recession, house values and investment portfolios fell, and millions of people's

lives were upended. At about the same period, the labour market has been difficult to revive.

While unemployment has returned to which was before norms, it takes roughly 10 years from the

beginning of the Great Recession to accomplish so, considerably longer than prior downswings.

Furthermore, the current unemployment rate's modest but steady reduction conceals a number of

linked facts that point to ongoing labour market instability. As during Great Recession, the

proportion of moderately connected and demoralized employees increased significantly, while

the labor participation rate decreased. According to some estimates, nearly 30 million people out

of work, and the percentage of lengthy unemployed quadrupled from its previous peak.

(1) There will be a considerable rise in the unemployment rate.

(2) Spending will fall as a result of people's tendency to conserve during a downturn.

(3) Investment levels will be reduced as a result of the crisis.

(4) Public spending is expected to rise.

(5) The administration and central bank must employ fiscal policy to modify government

expenditure and monetary policy to enhance monetary policy in order to emerge from the crisis.

(6) Increase state spending while lowering taxation.

(7) Implementation of aggressive monetary policies

5. Explain the effect of this crisis on the levels of Americans’ consumption in long-run?

People are more likely to conserve money during a recession because their confidence is

low. Keynes observed that during the Great Recession, there was a contradiction of frugality, in

which individuals saved even more consumed less, exacerbating the slump by causing additional

reductions in consumption. The few research that explicitly quantify the impact of job loss or

unemployed on consuming usually reveal significant relatively close reductions in spending but

no indications of lengthy consumption increases. Consumption reactions are disproportionately

weighted at the lowest income scale. Additionally, as previously said, when consumption rises

significant. At its lowest point, the rate was 17%. As a result, unemployment rates soared in

during Great Recession, house values and investment portfolios fell, and millions of people's

lives were upended. At about the same period, the labour market has been difficult to revive.

While unemployment has returned to which was before norms, it takes roughly 10 years from the

beginning of the Great Recession to accomplish so, considerably longer than prior downswings.

Furthermore, the current unemployment rate's modest but steady reduction conceals a number of

linked facts that point to ongoing labour market instability. As during Great Recession, the

proportion of moderately connected and demoralized employees increased significantly, while

the labor participation rate decreased. According to some estimates, nearly 30 million people out

of work, and the percentage of lengthy unemployed quadrupled from its previous peak.

(1) There will be a considerable rise in the unemployment rate.

(2) Spending will fall as a result of people's tendency to conserve during a downturn.

(3) Investment levels will be reduced as a result of the crisis.

(4) Public spending is expected to rise.

(5) The administration and central bank must employ fiscal policy to modify government

expenditure and monetary policy to enhance monetary policy in order to emerge from the crisis.

(6) Increase state spending while lowering taxation.

(7) Implementation of aggressive monetary policies

5. Explain the effect of this crisis on the levels of Americans’ consumption in long-run?

People are more likely to conserve money during a recession because their confidence is

low. Keynes observed that during the Great Recession, there was a contradiction of frugality, in

which individuals saved even more consumed less, exacerbating the slump by causing additional

reductions in consumption. The few research that explicitly quantify the impact of job loss or

unemployed on consuming usually reveal significant relatively close reductions in spending but

no indications of lengthy consumption increases. Consumption reactions are disproportionately

weighted at the lowest income scale. Additionally, as previously said, when consumption rises

(in an inefficient manner, as we will see later), the economic base must extend to satisfy

development and associated needs. Whereas if economic base extends to include other person's

territories, these individuals may not be able to use the commodities. The economy shrank

dramatically during the "Great Recession," which lasted from late 2007 to mid-2009, and over

8.7 million jobs have been lost. 6 Average spending has dropped to its lowest level since Second

World War. In reaction to decreases in earnings, assets, security, and credit availability,

households curtailed spending, paid off debt, and boosted their saving account rate. From 2007

and 2010, labor sustained by U.S. consumer spending fell by an estimated 3.2 million jobs,

accounting for over a third of all job losses during that time period. User employment, as

contrasted to the entire economy, has shown considerable resiliency, rebounding in 2012.

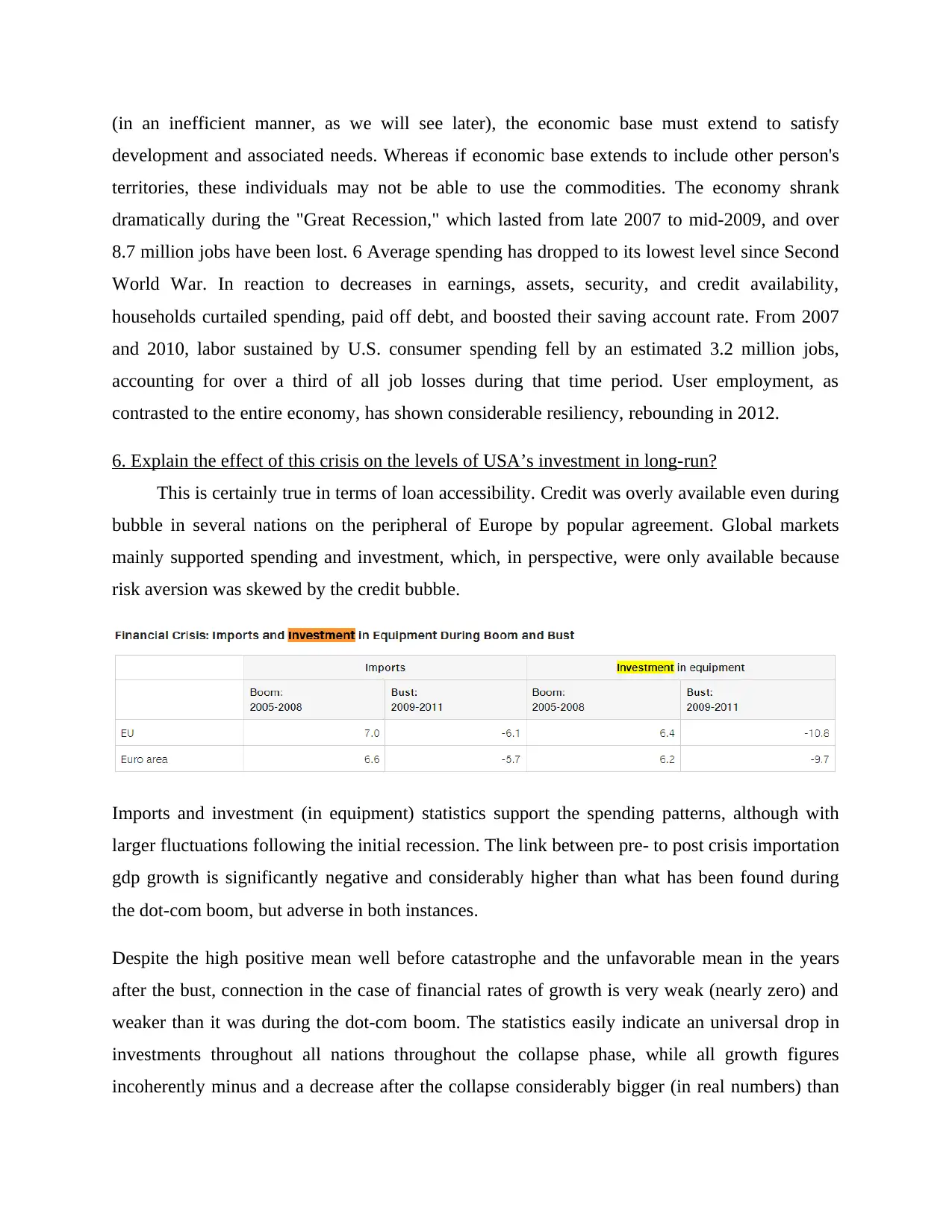

6. Explain the effect of this crisis on the levels of USA’s investment in long-run?

This is certainly true in terms of loan accessibility. Credit was overly available even during

bubble in several nations on the peripheral of Europe by popular agreement. Global markets

mainly supported spending and investment, which, in perspective, were only available because

risk aversion was skewed by the credit bubble.

Imports and investment (in equipment) statistics support the spending patterns, although with

larger fluctuations following the initial recession. The link between pre- to post crisis importation

gdp growth is significantly negative and considerably higher than what has been found during

the dot-com boom, but adverse in both instances.

Despite the high positive mean well before catastrophe and the unfavorable mean in the years

after the bust, connection in the case of financial rates of growth is very weak (nearly zero) and

weaker than it was during the dot-com boom. The statistics easily indicate an universal drop in

investments throughout all nations throughout the collapse phase, while all growth figures

incoherently minus and a decrease after the collapse considerably bigger (in real numbers) than

development and associated needs. Whereas if economic base extends to include other person's

territories, these individuals may not be able to use the commodities. The economy shrank

dramatically during the "Great Recession," which lasted from late 2007 to mid-2009, and over

8.7 million jobs have been lost. 6 Average spending has dropped to its lowest level since Second

World War. In reaction to decreases in earnings, assets, security, and credit availability,

households curtailed spending, paid off debt, and boosted their saving account rate. From 2007

and 2010, labor sustained by U.S. consumer spending fell by an estimated 3.2 million jobs,

accounting for over a third of all job losses during that time period. User employment, as

contrasted to the entire economy, has shown considerable resiliency, rebounding in 2012.

6. Explain the effect of this crisis on the levels of USA’s investment in long-run?

This is certainly true in terms of loan accessibility. Credit was overly available even during

bubble in several nations on the peripheral of Europe by popular agreement. Global markets

mainly supported spending and investment, which, in perspective, were only available because

risk aversion was skewed by the credit bubble.

Imports and investment (in equipment) statistics support the spending patterns, although with

larger fluctuations following the initial recession. The link between pre- to post crisis importation

gdp growth is significantly negative and considerably higher than what has been found during

the dot-com boom, but adverse in both instances.

Despite the high positive mean well before catastrophe and the unfavorable mean in the years

after the bust, connection in the case of financial rates of growth is very weak (nearly zero) and

weaker than it was during the dot-com boom. The statistics easily indicate an universal drop in

investments throughout all nations throughout the collapse phase, while all growth figures

incoherently minus and a decrease after the collapse considerably bigger (in real numbers) than

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the rise during in the bubble. Economic uncertainty grew substantially throughout 2008/9, as

according financial sector indices.

7. Explain the effect of this crisis on USA government’s Budget in long-run?

Around the time of the Great Recession, the elements of the federal budget altered

dramatically. As per a latest Economic Synopses piece, meanwhile, the national budget hasn't

changed quite as much.

Chief Economist Fernando Martin began by looking at the federal budget's four major

variables: revenue, disbursements, deficit, and fiscal deficit. In terms of GDP, each four were

investigated (GDP). Members also addressed the Budgetary Office's (CBO) estimates for the

next ten years.

Revenues: Martin pointed out that tax provisions enacted in the aftermath of the previous two

downturns resulted in lower tax collections, which represented 17.5 percent of GDP in the

months prior the Great Recession. Earnings accounted for 15.6 percent of GDP from 2008 to

2013. Nonetheless, substantial tax cuts enacted in 2013 aided the restoration of revenues to

average limits. From over ensuing years, they're anticipated to grow at a rate of around 18.1

percent on average.

Outlays: Outlays as a proportion of GDP fell in the 1990s, but rose again in the 2000s, according

to Martin. Owing to financial policy measures to the Global Recession, they also increased,

totaling 24.4 percent of GDP in 2009. Although “outlays remain excessive previous

corresponding period rates and are expected to keep growing within next couple of years,”

Martin said. For the years 2014-16, outlays are anticipated to average 20.7 percent of GDP,

rising to an average of 22.0 percent for the years 2017-26.

Deficit: “The decline in receipts and the growth in outlays from around period of the Global

Recession generated extraordinary deficits (for the post war era),” Martin wrote about

imbalances. The deficit reached 6.8% from 2008 to 2013, after averaged 1.8 percent over the

previous seven years. He pointed out that the deficit, like outlays, surged in 2009, is still high at

the moment, and is expected to increase further.

according financial sector indices.

7. Explain the effect of this crisis on USA government’s Budget in long-run?

Around the time of the Great Recession, the elements of the federal budget altered

dramatically. As per a latest Economic Synopses piece, meanwhile, the national budget hasn't

changed quite as much.

Chief Economist Fernando Martin began by looking at the federal budget's four major

variables: revenue, disbursements, deficit, and fiscal deficit. In terms of GDP, each four were

investigated (GDP). Members also addressed the Budgetary Office's (CBO) estimates for the

next ten years.

Revenues: Martin pointed out that tax provisions enacted in the aftermath of the previous two

downturns resulted in lower tax collections, which represented 17.5 percent of GDP in the

months prior the Great Recession. Earnings accounted for 15.6 percent of GDP from 2008 to

2013. Nonetheless, substantial tax cuts enacted in 2013 aided the restoration of revenues to

average limits. From over ensuing years, they're anticipated to grow at a rate of around 18.1

percent on average.

Outlays: Outlays as a proportion of GDP fell in the 1990s, but rose again in the 2000s, according

to Martin. Owing to financial policy measures to the Global Recession, they also increased,

totaling 24.4 percent of GDP in 2009. Although “outlays remain excessive previous

corresponding period rates and are expected to keep growing within next couple of years,”

Martin said. For the years 2014-16, outlays are anticipated to average 20.7 percent of GDP,

rising to an average of 22.0 percent for the years 2017-26.

Deficit: “The decline in receipts and the growth in outlays from around period of the Global

Recession generated extraordinary deficits (for the post war era),” Martin wrote about

imbalances. The deficit reached 6.8% from 2008 to 2013, after averaged 1.8 percent over the

previous seven years. He pointed out that the deficit, like outlays, surged in 2009, is still high at

the moment, and is expected to increase further.

8. Assume that you are a policy maker in USA’s government and central bank; how you can

recover the crisis by changing macroeconomic variables?

I should state right now that my current emphasis will be on the United States'

macroeconomic issues, as well as policy remedies. Monetary displacements and their effects

have, nevertheless, being experienced all over the world since financial markets and investment

firms are interconnected internationally. Furthermore, other nations have implemented policies

comparable to those implemented in the United States, such as standard and unconventional

financial regulation, financial assistance programmers, and quantitative easing. This is a really

worldwide problem, and it is reassuring to see that the necessity for strong policy solutions to the

major difficulties we confront is widely acknowledged.

Since the present episode's danger to political prosperity has been so tightly connected to

financial industry difficulties, most national policies have concentrated on financial markets, as

well as the availability of money to consumers and companies. That most of these regulations

were implemented in response to the tightness of market circumstances that ensued as bankers

grew more risk cautious and sought to preserve cash and flexibility. Towards that aim, the

Federal Reserve has decided to reduce, provided private money lenders with alternative funding

options, using its existing loan portfolio to attempt to resuscitate a set of investment sectors. In

fact, the Federal Reserve, the Treasury, and the Consumer Financial Protection Bureau (FDIC)

have implemented a variety of actions to strengthen and repair financial companies in order to

minimize their inclination to refuse to lend and, as a result, exacerbate the drop in expenditure.

The monetary policymaker must therefore strike a balance between pricing and production goals.

Even central banks that exclusively pursue deflation, such as the European Central Bank (ECB),

confess that they often actually listen to production stabilization and keeping the country at

economic growth.

Other government initiatives work at the crossroads of the financial and real worlds.

Bankruptcy prevention, for instance, must not only help families return home, but also help

lenders decrease loan losses. Lastly, stimuli spending specifically relating on consumption,

circumventing the banking sector during its first impacts; by increasing consumer spending, it

should also assist relieve lender pressures and assist to breaking the negative spiral. Despite the

fact that I'll be addressing every one of these national policies independently, it's crucial to bear

recover the crisis by changing macroeconomic variables?

I should state right now that my current emphasis will be on the United States'

macroeconomic issues, as well as policy remedies. Monetary displacements and their effects

have, nevertheless, being experienced all over the world since financial markets and investment

firms are interconnected internationally. Furthermore, other nations have implemented policies

comparable to those implemented in the United States, such as standard and unconventional

financial regulation, financial assistance programmers, and quantitative easing. This is a really

worldwide problem, and it is reassuring to see that the necessity for strong policy solutions to the

major difficulties we confront is widely acknowledged.

Since the present episode's danger to political prosperity has been so tightly connected to

financial industry difficulties, most national policies have concentrated on financial markets, as

well as the availability of money to consumers and companies. That most of these regulations

were implemented in response to the tightness of market circumstances that ensued as bankers

grew more risk cautious and sought to preserve cash and flexibility. Towards that aim, the

Federal Reserve has decided to reduce, provided private money lenders with alternative funding

options, using its existing loan portfolio to attempt to resuscitate a set of investment sectors. In

fact, the Federal Reserve, the Treasury, and the Consumer Financial Protection Bureau (FDIC)

have implemented a variety of actions to strengthen and repair financial companies in order to

minimize their inclination to refuse to lend and, as a result, exacerbate the drop in expenditure.

The monetary policymaker must therefore strike a balance between pricing and production goals.

Even central banks that exclusively pursue deflation, such as the European Central Bank (ECB),

confess that they often actually listen to production stabilization and keeping the country at

economic growth.

Other government initiatives work at the crossroads of the financial and real worlds.

Bankruptcy prevention, for instance, must not only help families return home, but also help

lenders decrease loan losses. Lastly, stimuli spending specifically relating on consumption,

circumventing the banking sector during its first impacts; by increasing consumer spending, it

should also assist relieve lender pressures and assist to breaking the negative spiral. Despite the

fact that I'll be addressing every one of these national policies independently, it's crucial to bear

in mind how they connect. At various places in the cycle of action and reaction, and afterwards

causation over, they all seek to escape into that unfavourable feedback mechanism we've been

discussing. The likelihood of recovery is based in part on the economic growth inherent

rehabilitative capacities, but it also relies on the impacts of different policy initiatives

complementing one another: A good financial plan is essential for achieving the benefits of fiscal

and monetary policy; absent fiscal and monetary stimulation to boost expenditure and improve

credit conditions, the monetary sector will not recover fast.

Whenever a central bank comments publically on fiscal policy, it focuses primarily on the

bond yields it wants to see rather than a precise dollar value (While adjustments in the monetary

base may be required to obtain the appropriate lending rates). Central banks typically concentrate

on a single "policy rate," which is arguably the most common, often nightly, percentage that

companies lend each other to obtain cash.

9. During the crisis, How USA can recover its output gap if it faces an expansionary gap?

The term "expansionary gap" refers to the fact that the country's economic current

production exceeds its productive capacity. Whenever the country's economic consumer

spending exceeds its production, an expansionary gap arises.

The present output deficit expands from $666 billion to $816 billion based on these projections.

Considering a liberal multiplier of 0.4, a baseline quantitative easing of $1.66 trillion is required

to return to near maximum output, and a total stimulus spending of $2 trillion is required to reach

optimum gainful livelihood.

Individuals amounts, however, are basic minimum requirements for restoring the economy to its

full capacity and funding "back pay" for those who have been forced to take lower pay at

replacement employment or who suffered a complete loss of living conditions. This excludes any

measures to upgrade the economy's deteriorating foundation.

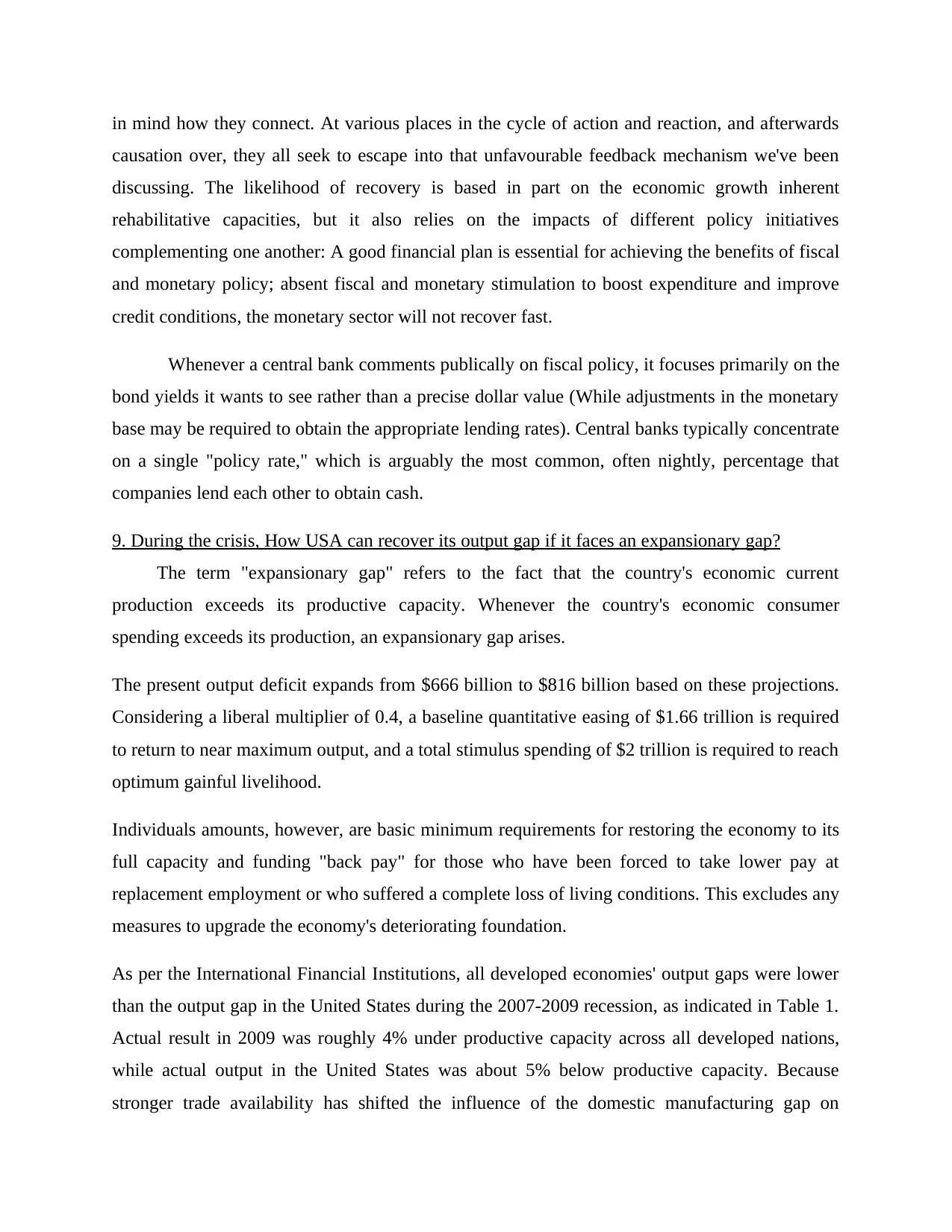

As per the International Financial Institutions, all developed economies' output gaps were lower

than the output gap in the United States during the 2007-2009 recession, as indicated in Table 1.

Actual result in 2009 was roughly 4% under productive capacity across all developed nations,

while actual output in the United States was about 5% below productive capacity. Because

stronger trade availability has shifted the influence of the domestic manufacturing gap on

causation over, they all seek to escape into that unfavourable feedback mechanism we've been

discussing. The likelihood of recovery is based in part on the economic growth inherent

rehabilitative capacities, but it also relies on the impacts of different policy initiatives

complementing one another: A good financial plan is essential for achieving the benefits of fiscal

and monetary policy; absent fiscal and monetary stimulation to boost expenditure and improve

credit conditions, the monetary sector will not recover fast.

Whenever a central bank comments publically on fiscal policy, it focuses primarily on the

bond yields it wants to see rather than a precise dollar value (While adjustments in the monetary

base may be required to obtain the appropriate lending rates). Central banks typically concentrate

on a single "policy rate," which is arguably the most common, often nightly, percentage that

companies lend each other to obtain cash.

9. During the crisis, How USA can recover its output gap if it faces an expansionary gap?

The term "expansionary gap" refers to the fact that the country's economic current

production exceeds its productive capacity. Whenever the country's economic consumer

spending exceeds its production, an expansionary gap arises.

The present output deficit expands from $666 billion to $816 billion based on these projections.

Considering a liberal multiplier of 0.4, a baseline quantitative easing of $1.66 trillion is required

to return to near maximum output, and a total stimulus spending of $2 trillion is required to reach

optimum gainful livelihood.

Individuals amounts, however, are basic minimum requirements for restoring the economy to its

full capacity and funding "back pay" for those who have been forced to take lower pay at

replacement employment or who suffered a complete loss of living conditions. This excludes any

measures to upgrade the economy's deteriorating foundation.

As per the International Financial Institutions, all developed economies' output gaps were lower

than the output gap in the United States during the 2007-2009 recession, as indicated in Table 1.

Actual result in 2009 was roughly 4% under productive capacity across all developed nations,

while actual output in the United States was about 5% below productive capacity. Because

stronger trade availability has shifted the influence of the domestic manufacturing gap on

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

inflation to the worldwide output gap, the lower output gap among some other developed nations

may assist to understand the surprisingly moderate drop in prices following the 2007-2009 crisis.

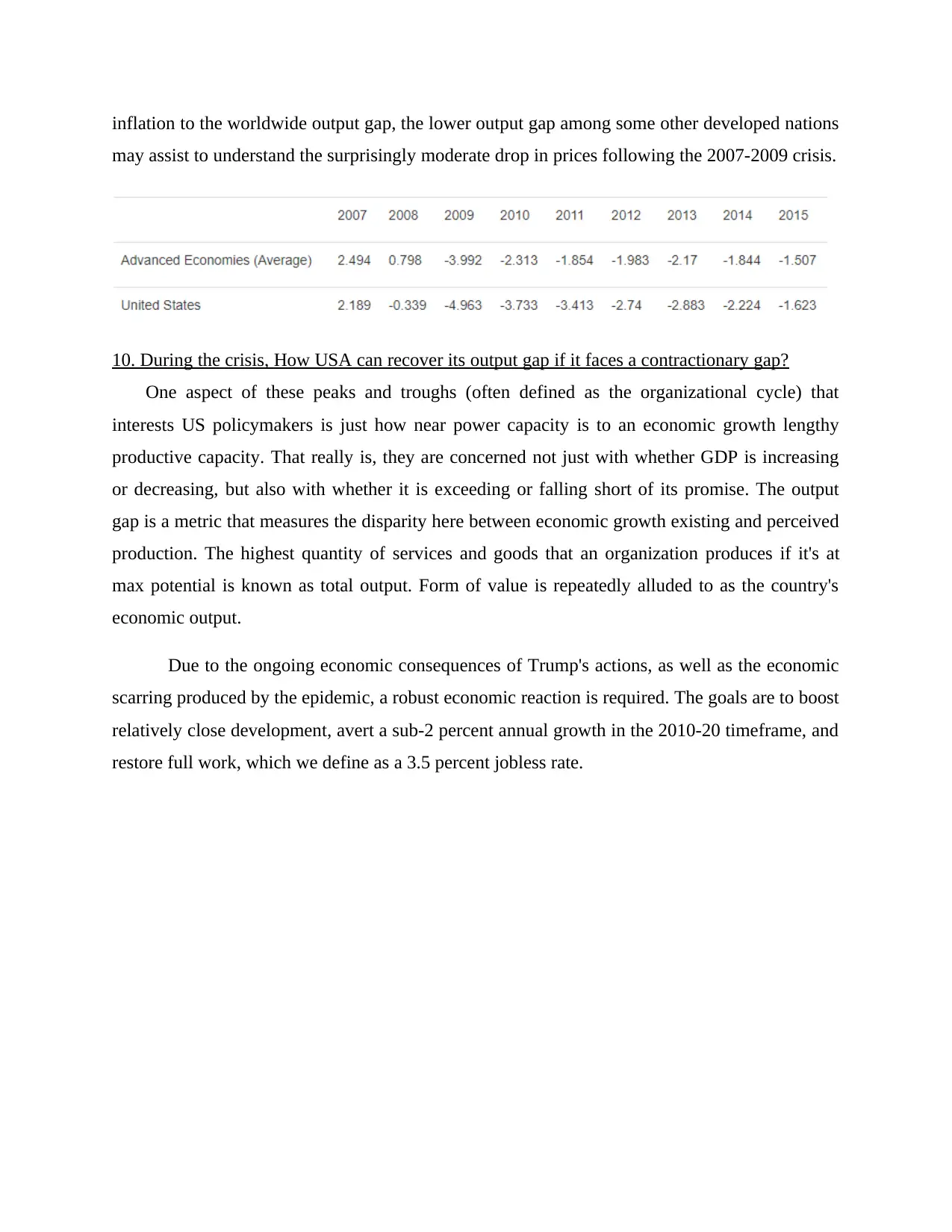

10. During the crisis, How USA can recover its output gap if it faces a contractionary gap?

One aspect of these peaks and troughs (often defined as the organizational cycle) that

interests US policymakers is just how near power capacity is to an economic growth lengthy

productive capacity. That really is, they are concerned not just with whether GDP is increasing

or decreasing, but also with whether it is exceeding or falling short of its promise. The output

gap is a metric that measures the disparity here between economic growth existing and perceived

production. The highest quantity of services and goods that an organization produces if it's at

max potential is known as total output. Form of value is repeatedly alluded to as the country's

economic output.

Due to the ongoing economic consequences of Trump's actions, as well as the economic

scarring produced by the epidemic, a robust economic reaction is required. The goals are to boost

relatively close development, avert a sub-2 percent annual growth in the 2010-20 timeframe, and

restore full work, which we define as a 3.5 percent jobless rate.

may assist to understand the surprisingly moderate drop in prices following the 2007-2009 crisis.

10. During the crisis, How USA can recover its output gap if it faces a contractionary gap?

One aspect of these peaks and troughs (often defined as the organizational cycle) that

interests US policymakers is just how near power capacity is to an economic growth lengthy

productive capacity. That really is, they are concerned not just with whether GDP is increasing

or decreasing, but also with whether it is exceeding or falling short of its promise. The output

gap is a metric that measures the disparity here between economic growth existing and perceived

production. The highest quantity of services and goods that an organization produces if it's at

max potential is known as total output. Form of value is repeatedly alluded to as the country's

economic output.

Due to the ongoing economic consequences of Trump's actions, as well as the economic

scarring produced by the epidemic, a robust economic reaction is required. The goals are to boost

relatively close development, avert a sub-2 percent annual growth in the 2010-20 timeframe, and

restore full work, which we define as a 3.5 percent jobless rate.

Economists who believe the global production gap has an impact on household inflation have

tried to see if the degree of this influence has expanded in tandem with increased trade

liberalization. Nevertheless, the severity of the effects of the global production gap on local

inflation appears to be independent to changes in market liberalization. Based on this data, it is

doubtful that recent increases in trade liberalization and a reduced production gap overseas

contributed to the surprisingly moderate drop in inflation following the 2007-2009 recession.

REFERENCES

Books and Journal

Marane, B. and Asaad, Z., 2021. Envisaging Macroeconomics Antecedent Effect on Stock

Market Return in India. Sivarethinamohan, R., ASAAD, ZA, MARANE, BMR, & Sujatha,

S.(2021). Envisaging Macroeconomics Antecedent Effect on Stock Market Return in

India. The Journal of Asian Finance, Economics and Business, 8(8), pp.311-324.

Liao, L.K., Fan, Y.W. and Shih, M.H., 2020. What drives social responsibility indices returns?

Macroeconomics matters. Corporate Social Responsibility and Environmental

Management, 27(2), pp.514-524.

Whalen, C.J., 2020. Symposium on the Monetary Macroeconomics of John R.

Commons. Journal of Economic Issues, 54(4), pp.903-906.

tried to see if the degree of this influence has expanded in tandem with increased trade

liberalization. Nevertheless, the severity of the effects of the global production gap on local

inflation appears to be independent to changes in market liberalization. Based on this data, it is

doubtful that recent increases in trade liberalization and a reduced production gap overseas

contributed to the surprisingly moderate drop in inflation following the 2007-2009 recession.

REFERENCES

Books and Journal

Marane, B. and Asaad, Z., 2021. Envisaging Macroeconomics Antecedent Effect on Stock

Market Return in India. Sivarethinamohan, R., ASAAD, ZA, MARANE, BMR, & Sujatha,

S.(2021). Envisaging Macroeconomics Antecedent Effect on Stock Market Return in

India. The Journal of Asian Finance, Economics and Business, 8(8), pp.311-324.

Liao, L.K., Fan, Y.W. and Shih, M.H., 2020. What drives social responsibility indices returns?

Macroeconomics matters. Corporate Social Responsibility and Environmental

Management, 27(2), pp.514-524.

Whalen, C.J., 2020. Symposium on the Monetary Macroeconomics of John R.

Commons. Journal of Economic Issues, 54(4), pp.903-906.

Millmow, A., 2021. Macroeconomics and the Pursuit of Ruralism. In The Gypsy Economist (pp.

169-185). Palgrave Macmillan, Singapore.

Ardhani, I.A., Effendi, J. and Irfany, M.I., 2020. The effect of macroeconomics variables to Net

Asset Value (NAV) growth of sharia mutual funds in Indonesia. Jurnal Ekonomi dan

Keuangan Islam, 6(2), pp.134-148.

Li, J. and Stone, G., 2020. Applications of Optimization Theory to Social Benefit Maximizations

in Macroeconomics with Uncertainty. Numerical Functional Analysis and

Optimization, 41(11), pp.1287-1307.

Feng, D. and Liu, M., 2021. Curriculum Construction and Reform of Macroeconomics from the

Perspective of Curriculum Ideological and Political. Frontiers in Economics and

Management, 2(6), pp.99-103.

Fuad, A. and Disman, D., 2020. The effect of macroeconomics on the performance of

commercial banks in Indonesia. In Advances in Business, Management and

Entrepreneurship (pp. 89-94). CRC Press.

Ojuolape, A., 2021. The Effects Of Fragility On Macroeconomics Variables In West

Africa. CHIANG MAI UNIVERSITY JOURNAL OF ECONOMICS, 25(1), pp.17-37.

Zeng, Y., 2021. Discovery of" Curriculum Ideological and Political" Elements of

Macroeconomics and Exploration of Teaching Reform. International Journal of Social

Science and Education Research, 4(7), pp.485-490.

Sukmawati, F.N. and Haryono, N.A., 2021. Cointegration of Macroeconomics Variables and

Dow Jones Industrial Average Index on the Composite Stock Price Index In 2015-

2019. Journal of Business and Management Review, 2(3), pp.178-191.

Gao, X., 2020. Essays on firms, technology, and macroeconomics (Doctoral dissertation, The

London School of Economics and Political Science (LSE)).

Mokhlis, N.H.M., Ariffin, M.N.A. and Mustapha, W.H.W., 2020. Analysing Macroeconomics

Factors of Housing Price in Malaysia. International Journal of Advanced Research in

Economics and Finance, 2(3), pp.1-7.

169-185). Palgrave Macmillan, Singapore.

Ardhani, I.A., Effendi, J. and Irfany, M.I., 2020. The effect of macroeconomics variables to Net

Asset Value (NAV) growth of sharia mutual funds in Indonesia. Jurnal Ekonomi dan

Keuangan Islam, 6(2), pp.134-148.

Li, J. and Stone, G., 2020. Applications of Optimization Theory to Social Benefit Maximizations

in Macroeconomics with Uncertainty. Numerical Functional Analysis and

Optimization, 41(11), pp.1287-1307.

Feng, D. and Liu, M., 2021. Curriculum Construction and Reform of Macroeconomics from the

Perspective of Curriculum Ideological and Political. Frontiers in Economics and

Management, 2(6), pp.99-103.

Fuad, A. and Disman, D., 2020. The effect of macroeconomics on the performance of

commercial banks in Indonesia. In Advances in Business, Management and

Entrepreneurship (pp. 89-94). CRC Press.

Ojuolape, A., 2021. The Effects Of Fragility On Macroeconomics Variables In West

Africa. CHIANG MAI UNIVERSITY JOURNAL OF ECONOMICS, 25(1), pp.17-37.

Zeng, Y., 2021. Discovery of" Curriculum Ideological and Political" Elements of

Macroeconomics and Exploration of Teaching Reform. International Journal of Social

Science and Education Research, 4(7), pp.485-490.

Sukmawati, F.N. and Haryono, N.A., 2021. Cointegration of Macroeconomics Variables and

Dow Jones Industrial Average Index on the Composite Stock Price Index In 2015-

2019. Journal of Business and Management Review, 2(3), pp.178-191.

Gao, X., 2020. Essays on firms, technology, and macroeconomics (Doctoral dissertation, The

London School of Economics and Political Science (LSE)).

Mokhlis, N.H.M., Ariffin, M.N.A. and Mustapha, W.H.W., 2020. Analysing Macroeconomics

Factors of Housing Price in Malaysia. International Journal of Advanced Research in

Economics and Finance, 2(3), pp.1-7.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.