Major Issues in Activity Based Management (ABM)

VerifiedAdded on 2023/03/17

|13

|2842

|34

AI Summary

This article discusses the major issues in Activity Based Management (ABM) and their impact on stakeholders. It explores the importance of ABM in understanding organizational activities and evaluating business efficiency. The article also provides recommendations for improving ABM practices.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: MAJOR ISSUES IN REGARD TO ACTIVITY BASED MANAGEMENT (ABM)

Major issues in regard to Activity Based Management (ABM)

Name of the Student

Name of the University

Author’s Note

Major issues in regard to Activity Based Management (ABM)

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MAJOR ISSUES IN REGARD TO ACTIVITY BASED MANAGEMENT (ABM)

Table of Contents

1. Introduction..................................................................................................................................2

2. Discussion....................................................................................................................................3

Issues regarding the Activity Based Management (ABM)?........................................................3

Context of performance evaluation.................................................................................................4

Context of supply chain management..............................................................................................5

Context of quality management.......................................................................................................6

Context of environmental sustainability..........................................................................................6

3. Importance of Activity Based Management (ABM) for stakeholders?.......................................8

4. Recommendations........................................................................................................................9

5. Conclusions................................................................................................................................10

References......................................................................................................................................11

Table of Contents

1. Introduction..................................................................................................................................2

2. Discussion....................................................................................................................................3

Issues regarding the Activity Based Management (ABM)?........................................................3

Context of performance evaluation.................................................................................................4

Context of supply chain management..............................................................................................5

Context of quality management.......................................................................................................6

Context of environmental sustainability..........................................................................................6

3. Importance of Activity Based Management (ABM) for stakeholders?.......................................8

4. Recommendations........................................................................................................................9

5. Conclusions................................................................................................................................10

References......................................................................................................................................11

2MAJOR ISSUES IN REGARD TO ACTIVITY BASED MANAGEMENT (ABM)

1. Introduction

ABM is a method for the identification of the activities that take place within the

concerned organisational premises. On the other hand, it is one of the effective tools to

understanding how the various activities in the sub-departments of the organizations are being

carried out. On the other hand, it is also being considered in evaluating the value chain

management and that of the analysis regarding business efficiency. Besides, the use of the

Activity Based Management (ABM), is also undertaken for the sole purpose of the reengineering

process. This reengineering process is being carried out with the vision hat a positive change will

be observed.

The importance of Activity Based Management (ABM), it focuses more on the

responsibility and the set of accountability for completing a particular task. On the other

perspective, it is the tool by which maximization of the overall performance is being targeted

rather than maximizing the efficiency of an individual body. It undertakes the business as a

whole. Besides, it is also a tool of measurement that measures the amount of the cost that is

being spent by each of the performing individual within the organisational premises.

1. Introduction

ABM is a method for the identification of the activities that take place within the

concerned organisational premises. On the other hand, it is one of the effective tools to

understanding how the various activities in the sub-departments of the organizations are being

carried out. On the other hand, it is also being considered in evaluating the value chain

management and that of the analysis regarding business efficiency. Besides, the use of the

Activity Based Management (ABM), is also undertaken for the sole purpose of the reengineering

process. This reengineering process is being carried out with the vision hat a positive change will

be observed.

The importance of Activity Based Management (ABM), it focuses more on the

responsibility and the set of accountability for completing a particular task. On the other

perspective, it is the tool by which maximization of the overall performance is being targeted

rather than maximizing the efficiency of an individual body. It undertakes the business as a

whole. Besides, it is also a tool of measurement that measures the amount of the cost that is

being spent by each of the performing individual within the organisational premises.

3MAJOR ISSUES IN REGARD TO ACTIVITY BASED MANAGEMENT (ABM)

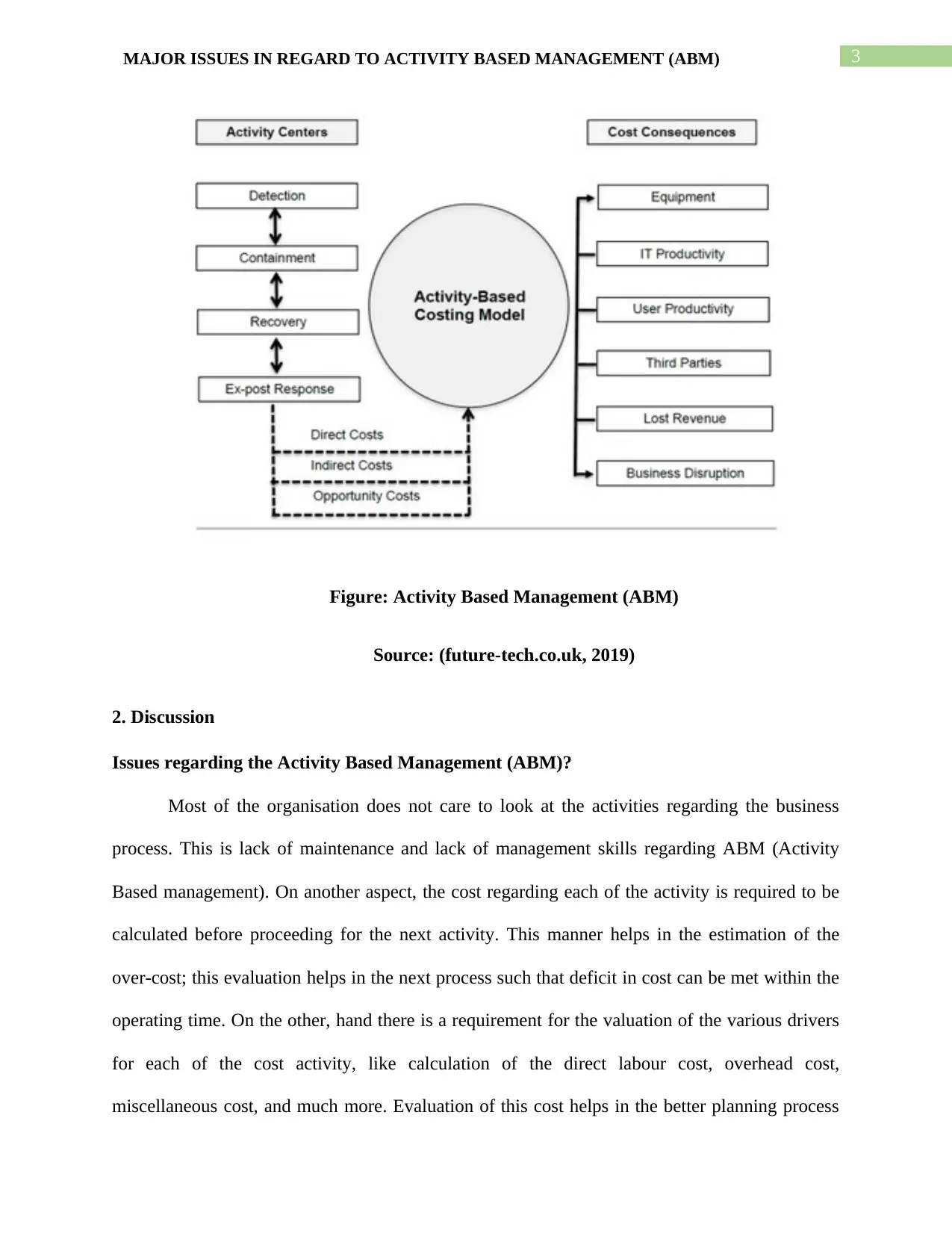

Figure: Activity Based Management (ABM)

Source: (future-tech.co.uk, 2019)

2. Discussion

Issues regarding the Activity Based Management (ABM)?

Most of the organisation does not care to look at the activities regarding the business

process. This is lack of maintenance and lack of management skills regarding ABM (Activity

Based management). On another aspect, the cost regarding each of the activity is required to be

calculated before proceeding for the next activity. This manner helps in the estimation of the

over-cost; this evaluation helps in the next process such that deficit in cost can be met within the

operating time. On the other, hand there is a requirement for the valuation of the various drivers

for each of the cost activity, like calculation of the direct labour cost, overhead cost,

miscellaneous cost, and much more. Evaluation of this cost helps in the better planning process

Figure: Activity Based Management (ABM)

Source: (future-tech.co.uk, 2019)

2. Discussion

Issues regarding the Activity Based Management (ABM)?

Most of the organisation does not care to look at the activities regarding the business

process. This is lack of maintenance and lack of management skills regarding ABM (Activity

Based management). On another aspect, the cost regarding each of the activity is required to be

calculated before proceeding for the next activity. This manner helps in the estimation of the

over-cost; this evaluation helps in the next process such that deficit in cost can be met within the

operating time. On the other, hand there is a requirement for the valuation of the various drivers

for each of the cost activity, like calculation of the direct labour cost, overhead cost,

miscellaneous cost, and much more. Evaluation of this cost helps in the better planning process

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MAJOR ISSUES IN REGARD TO ACTIVITY BASED MANAGEMENT (ABM)

for the distribution of the equal amount of profit among the various stakeholders. There is an

immense requirement to have an immense focus upon the initial stages of the ABM; they are as

follows:

1. Identify the activities that are being performed by the organisation.

2. Each activity cost is required to be calculated.

3. Identification of the cost driver for each activity.

Context of performance evaluation

Besides, there is a requirement to hire professional experts who have sound knowledge

regarding that of the financial activities. Financial reports are being carried out upon having

professional knowledge regarding various cost structures. The lack of professional experts is

another reason for the failure of positive ABM (Activity Based management) (Janamian et al.,

2016).

The internal management bodies of the organisation are one of the primary reasons for

the failure of the business prospects of the firm. On the other contrary, the top and that of the

middle management body fails to understand that there is a requirement of the periodically based

check-up. This periodic routine based check-up helps in understanding the dynamic changes that

take place within the organisational premises. These changes are to be adopted by the internal

employees of the organisation by making use of the training programmes. On the other hand,

there is a requirement that this body may communicate with that of the external employees as

formulating communication channel with that of the external employees will help in

understanding the level of personality and that of how they undertake their business activities

(Larson et al., 2018).

for the distribution of the equal amount of profit among the various stakeholders. There is an

immense requirement to have an immense focus upon the initial stages of the ABM; they are as

follows:

1. Identify the activities that are being performed by the organisation.

2. Each activity cost is required to be calculated.

3. Identification of the cost driver for each activity.

Context of performance evaluation

Besides, there is a requirement to hire professional experts who have sound knowledge

regarding that of the financial activities. Financial reports are being carried out upon having

professional knowledge regarding various cost structures. The lack of professional experts is

another reason for the failure of positive ABM (Activity Based management) (Janamian et al.,

2016).

The internal management bodies of the organisation are one of the primary reasons for

the failure of the business prospects of the firm. On the other contrary, the top and that of the

middle management body fails to understand that there is a requirement of the periodically based

check-up. This periodic routine based check-up helps in understanding the dynamic changes that

take place within the organisational premises. These changes are to be adopted by the internal

employees of the organisation by making use of the training programmes. On the other hand,

there is a requirement that this body may communicate with that of the external employees as

formulating communication channel with that of the external employees will help in

understanding the level of personality and that of how they undertake their business activities

(Larson et al., 2018).

5MAJOR ISSUES IN REGARD TO ACTIVITY BASED MANAGEMENT (ABM)

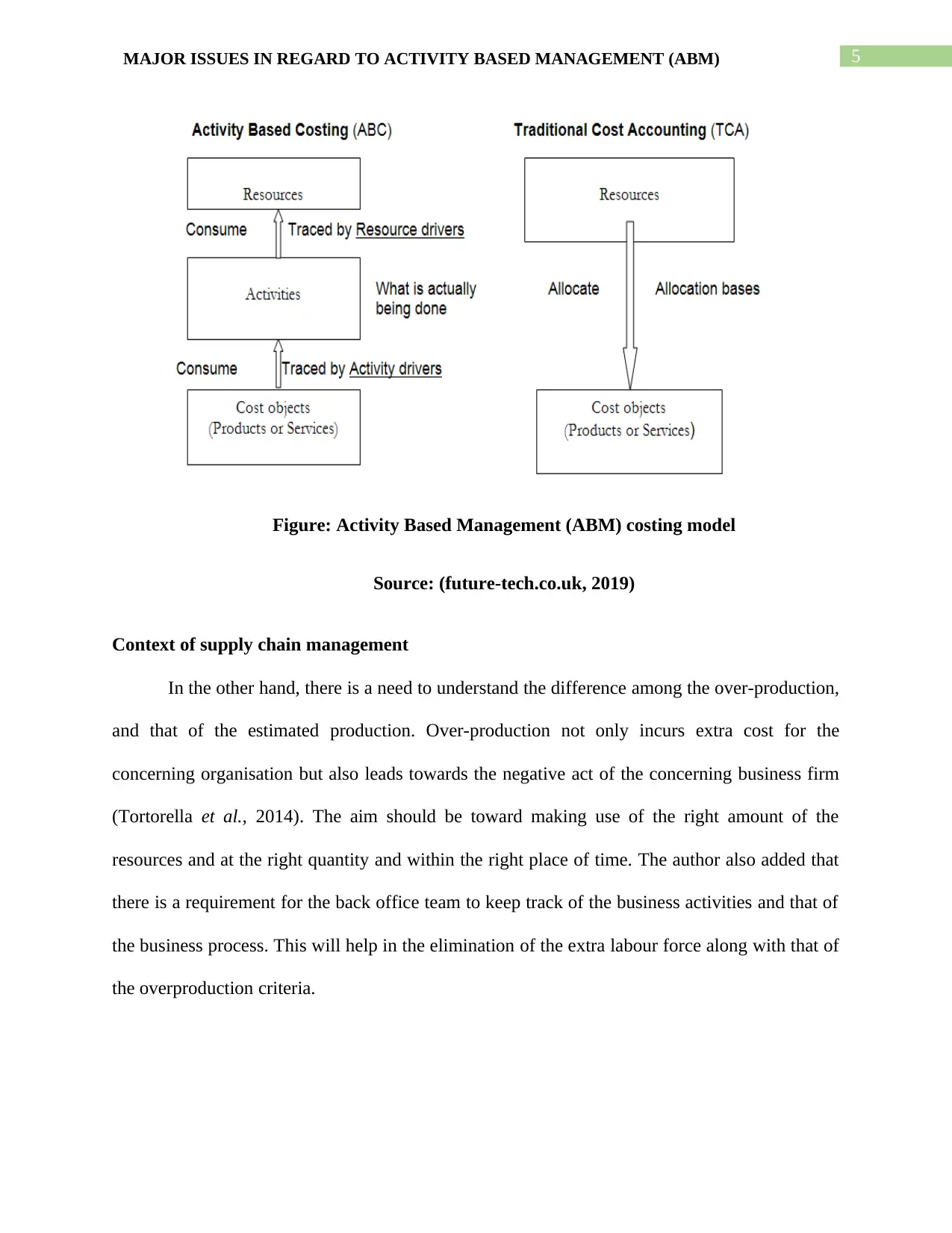

Figure: Activity Based Management (ABM) costing model

Source: (future-tech.co.uk, 2019)

Context of supply chain management

In the other hand, there is a need to understand the difference among the over-production,

and that of the estimated production. Over-production not only incurs extra cost for the

concerning organisation but also leads towards the negative act of the concerning business firm

(Tortorella et al., 2014). The aim should be toward making use of the right amount of the

resources and at the right quantity and within the right place of time. The author also added that

there is a requirement for the back office team to keep track of the business activities and that of

the business process. This will help in the elimination of the extra labour force along with that of

the overproduction criteria.

Figure: Activity Based Management (ABM) costing model

Source: (future-tech.co.uk, 2019)

Context of supply chain management

In the other hand, there is a need to understand the difference among the over-production,

and that of the estimated production. Over-production not only incurs extra cost for the

concerning organisation but also leads towards the negative act of the concerning business firm

(Tortorella et al., 2014). The aim should be toward making use of the right amount of the

resources and at the right quantity and within the right place of time. The author also added that

there is a requirement for the back office team to keep track of the business activities and that of

the business process. This will help in the elimination of the extra labour force along with that of

the overproduction criteria.

6MAJOR ISSUES IN REGARD TO ACTIVITY BASED MANAGEMENT (ABM)

Context of quality management

Another author (Goetsch et al., 2014) proposes that there have been major issues within

the accounting department as well. The finance department is required to make sure that the

various cost channels are being calculated and linked with that of the various aspects of the cost

drivers. The formulation of the financial reports helps in the predictions of the cost that is going

to be incurred for various organisational business activity. This activity of report generation

helps in dealing with that of the crisis regarding the financial report. Moreover, comparison of

this report with one another helps in better understanding of the areas where cost can be

minimised by effective use of the capital resources. Hence, much of the cost can be secured by

the firm which can be used for various other purposes.

There are some professional along with that of the concerning business firm who

do not care much towards the quality management of their end outputs. Such that this

professional only aims at the production in bulk amount but does not undertake measure towards

sustaining this output. They should understand that there is an immense to have a concern

towards the output or end products as there are several situations which might lead towards the

hampering of this end products. The author also added that this specific issue could be overcome

by making use of the professional experts who g making use of the charts and predictions graph

can understand the production scenario of the concerning firm.

Context of environmental sustainability

By taking the initiative towards the CSR programme, it helps the concerning firm to

formulate a positive image in the eye of the general public. This image being formulated helps in

the creation of future business prospects for the firm. It is the faith of the public that is the sole

Context of quality management

Another author (Goetsch et al., 2014) proposes that there have been major issues within

the accounting department as well. The finance department is required to make sure that the

various cost channels are being calculated and linked with that of the various aspects of the cost

drivers. The formulation of the financial reports helps in the predictions of the cost that is going

to be incurred for various organisational business activity. This activity of report generation

helps in dealing with that of the crisis regarding the financial report. Moreover, comparison of

this report with one another helps in better understanding of the areas where cost can be

minimised by effective use of the capital resources. Hence, much of the cost can be secured by

the firm which can be used for various other purposes.

There are some professional along with that of the concerning business firm who

do not care much towards the quality management of their end outputs. Such that this

professional only aims at the production in bulk amount but does not undertake measure towards

sustaining this output. They should understand that there is an immense to have a concern

towards the output or end products as there are several situations which might lead towards the

hampering of this end products. The author also added that this specific issue could be overcome

by making use of the professional experts who g making use of the charts and predictions graph

can understand the production scenario of the concerning firm.

Context of environmental sustainability

By taking the initiative towards the CSR programme, it helps the concerning firm to

formulate a positive image in the eye of the general public. This image being formulated helps in

the creation of future business prospects for the firm. It is the faith of the public that is the sole

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MAJOR ISSUES IN REGARD TO ACTIVITY BASED MANAGEMENT (ABM)

requirement for any concerning business. By obtaining their faith, it helps the firm to generate

revenues and profits by undertaking trade activities with that of the potential consumer market.

The author supported its statement by stating that communication and getting engaged

with that of the professional experts help in the better understanding of the external business

factors along with that of the internal business factors. On the other side, getting engaged helps

in the outcome of the new business-related ideas. This specific business idea can be implemented

in the future activities of the concerning business firm.

Figure: Activity Based Management (ABM) strategy model

Source: (future-tech.co.uk, 2019)

requirement for any concerning business. By obtaining their faith, it helps the firm to generate

revenues and profits by undertaking trade activities with that of the potential consumer market.

The author supported its statement by stating that communication and getting engaged

with that of the professional experts help in the better understanding of the external business

factors along with that of the internal business factors. On the other side, getting engaged helps

in the outcome of the new business-related ideas. This specific business idea can be implemented

in the future activities of the concerning business firm.

Figure: Activity Based Management (ABM) strategy model

Source: (future-tech.co.uk, 2019)

8MAJOR ISSUES IN REGARD TO ACTIVITY BASED MANAGEMENT (ABM)

3. Importance of Activity Based Management (ABM) for stakeholders?

Another issue within the organisational premises is the lack of official ABM (Activity

Based management), this management activity provides basic tools. Moreover, it helps in having

an appropriate assessment regarding that of the company’s expenditures. Activity-based

management (ABM) is the only system that provides the basic tools to perfectly assess the

outflow involved regarding that of the tightly knit supply chain and enables understanding not

only of the total cost of ownership (TCO) but also how these costs should be allocated (Oseifuah

et al., 2014). Supply Chain Cost Control Using Activity-Based Management discusses the

competitive advantage that cost analysis and management can bring to companies within a

supply chain.

Addressing the numerous number of strategies for the sole purpose of evaluating

the total cost inherent in a customer-supplier relationship, ANM makes use of the TCO, activity-

based costing (ABC), and that of the ABM (Activity Based management), for the sole purpose of

analysing and controlling the supply chain costs. ABM (Activity Based management) is a tool

that makes use of the industry survey data to examine the cost structure, process structure, supply

chain and that of quality of the workflow.

Moreover, it serves as an assessment tool in determining which factors affect the usage

regarding that of the supply chain and whether they are producing results (Delic et al., 2014).

The author further supported its statement by stating that cost reduction should be one of the key

strategies for competitive business environments.

Supply Chain Cost Control Using Activity-Based Management shows the importance of

partnerships in applying ABM principles to suppliers and demonstrates the positive results that

3. Importance of Activity Based Management (ABM) for stakeholders?

Another issue within the organisational premises is the lack of official ABM (Activity

Based management), this management activity provides basic tools. Moreover, it helps in having

an appropriate assessment regarding that of the company’s expenditures. Activity-based

management (ABM) is the only system that provides the basic tools to perfectly assess the

outflow involved regarding that of the tightly knit supply chain and enables understanding not

only of the total cost of ownership (TCO) but also how these costs should be allocated (Oseifuah

et al., 2014). Supply Chain Cost Control Using Activity-Based Management discusses the

competitive advantage that cost analysis and management can bring to companies within a

supply chain.

Addressing the numerous number of strategies for the sole purpose of evaluating

the total cost inherent in a customer-supplier relationship, ANM makes use of the TCO, activity-

based costing (ABC), and that of the ABM (Activity Based management), for the sole purpose of

analysing and controlling the supply chain costs. ABM (Activity Based management) is a tool

that makes use of the industry survey data to examine the cost structure, process structure, supply

chain and that of quality of the workflow.

Moreover, it serves as an assessment tool in determining which factors affect the usage

regarding that of the supply chain and whether they are producing results (Delic et al., 2014).

The author further supported its statement by stating that cost reduction should be one of the key

strategies for competitive business environments.

Supply Chain Cost Control Using Activity-Based Management shows the importance of

partnerships in applying ABM principles to suppliers and demonstrates the positive results that

9MAJOR ISSUES IN REGARD TO ACTIVITY BASED MANAGEMENT (ABM)

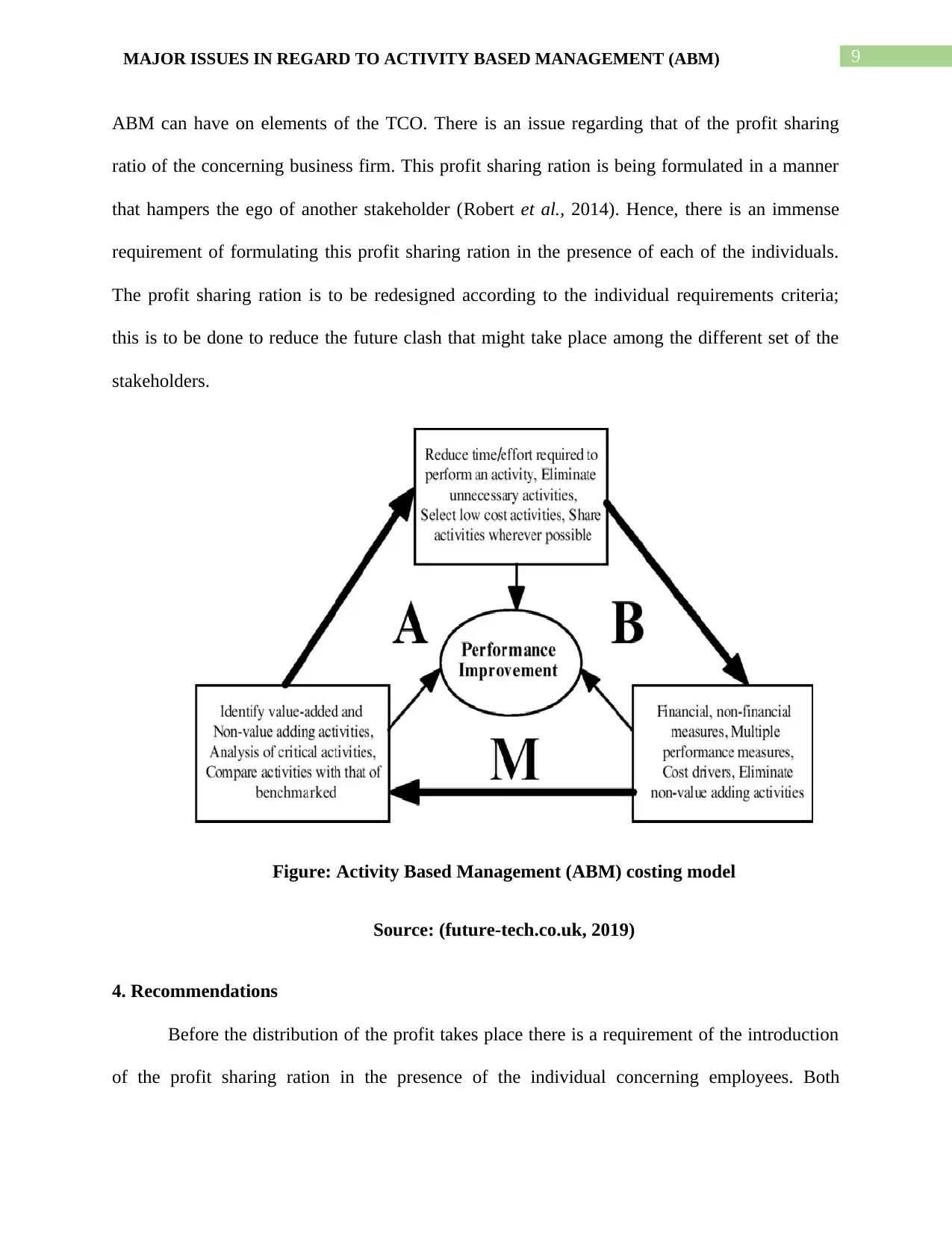

ABM can have on elements of the TCO. There is an issue regarding that of the profit sharing

ratio of the concerning business firm. This profit sharing ration is being formulated in a manner

that hampers the ego of another stakeholder (Robert et al., 2014). Hence, there is an immense

requirement of formulating this profit sharing ration in the presence of each of the individuals.

The profit sharing ration is to be redesigned according to the individual requirements criteria;

this is to be done to reduce the future clash that might take place among the different set of the

stakeholders.

Figure: Activity Based Management (ABM) costing model

Source: (future-tech.co.uk, 2019)

4. Recommendations

Before the distribution of the profit takes place there is a requirement of the introduction

of the profit sharing ration in the presence of the individual concerning employees. Both

ABM can have on elements of the TCO. There is an issue regarding that of the profit sharing

ratio of the concerning business firm. This profit sharing ration is being formulated in a manner

that hampers the ego of another stakeholder (Robert et al., 2014). Hence, there is an immense

requirement of formulating this profit sharing ration in the presence of each of the individuals.

The profit sharing ration is to be redesigned according to the individual requirements criteria;

this is to be done to reduce the future clash that might take place among the different set of the

stakeholders.

Figure: Activity Based Management (ABM) costing model

Source: (future-tech.co.uk, 2019)

4. Recommendations

Before the distribution of the profit takes place there is a requirement of the introduction

of the profit sharing ration in the presence of the individual concerning employees. Both

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10MAJOR ISSUES IN REGARD TO ACTIVITY BASED MANAGEMENT (ABM)

internally and those of the external stakeholders. On the other, perspective there is an urgency of

the introduction of the formal agreement that outlays each of the statement regarding that of the

profit sharing ratio. This agreement is to be signed by each of the individual stakeholder parties

such that any clash within the future period will be eliminated. This specific formal agreement

will act as legal proof in the future era of time. Thus it helps in dealing with the conflicts. This is

one of the formal and basic strategic moves that most of the corporate firm fails to make use of.

5. Conclusions

Thus, it is being concluded that the planning stage is the primary stage for any concerning

the business firm. It is the planning phase that decided the entire future business prospects of the

concerning business firm. The planning stage should be undertaken under the supervision of the

top professionals and is not a task of one particular body or that of the task of one particular sub-

departments of the company. As such that this planning stage is required to be formulated in the

supervision of the top professionals and that of the professional marketing experts. It is very

often found that the sole motive of penetrating the international market is failed because of the

lack of knowledge that stays within the hand of the concerning business firm.

One of the major reason for the conflict among the stakeholders both internally and that

of the externally is because of the lack of market penetration within the consumer market. The

author further added that there is a requirement for the constant innovation product such that the

potential rival firms fail to obtain any competitive advantage upon the concerning business firm

(Dixon-Woods et al., 2016). On the other hand, the market always seeks for a new product

offering they have certain expectation from that of the specific set of the business firm. It is their

level of satisfaction that pulls the consumer back towards the concerning business firm.

internally and those of the external stakeholders. On the other, perspective there is an urgency of

the introduction of the formal agreement that outlays each of the statement regarding that of the

profit sharing ratio. This agreement is to be signed by each of the individual stakeholder parties

such that any clash within the future period will be eliminated. This specific formal agreement

will act as legal proof in the future era of time. Thus it helps in dealing with the conflicts. This is

one of the formal and basic strategic moves that most of the corporate firm fails to make use of.

5. Conclusions

Thus, it is being concluded that the planning stage is the primary stage for any concerning

the business firm. It is the planning phase that decided the entire future business prospects of the

concerning business firm. The planning stage should be undertaken under the supervision of the

top professionals and is not a task of one particular body or that of the task of one particular sub-

departments of the company. As such that this planning stage is required to be formulated in the

supervision of the top professionals and that of the professional marketing experts. It is very

often found that the sole motive of penetrating the international market is failed because of the

lack of knowledge that stays within the hand of the concerning business firm.

One of the major reason for the conflict among the stakeholders both internally and that

of the externally is because of the lack of market penetration within the consumer market. The

author further added that there is a requirement for the constant innovation product such that the

potential rival firms fail to obtain any competitive advantage upon the concerning business firm

(Dixon-Woods et al., 2016). On the other hand, the market always seeks for a new product

offering they have certain expectation from that of the specific set of the business firm. It is their

level of satisfaction that pulls the consumer back towards the concerning business firm.

11MAJOR ISSUES IN REGARD TO ACTIVITY BASED MANAGEMENT (ABM)

References

Brajer-Marczak, R. (2014). Employee engagement in continuous improvement of processes.

Management, 18(2), 88-103.

Cardos, I.R. and Cardos, V.D., 2014. Measuring customer profitability with activity-based

costing and balanced scorecard. Annales Universitatis Apulensis: Series Oeconomica,

16(1), p.52.

Delić, M., Radlovački, V., Kamberović, B., Maksimović, R., & Pečujlija, M. (2014). Examining

relationships between quality management and organisational performance in transitional

economies. Total Quality Management & Business Excellence, 25(3-4), 367-382.

Dixon-Woods, M., & Martin, G. P. (2016). Does quality improvement improve quality?. Future

Hospital Journal, 3(3), 191-194.

Goetsch, D.L. and Davis, S.B., 2014. Quality management for organizational excellence. Upper

Saddle River, NJ: pearson.

Hamid, F.A.H., 2014. The Impact of Activity-Based Costing System Application on Enhancing

Company’s Financial Performance (Doctoral dissertation, Sudan University of Science

And Technology).

Janamian, T., Upham, S. J., Crossland, L., & Jackson, C. L. (2016). Quality tools and resources

to support organisational improvement integral to high‐quality primary care: a systematic

review of published and grey literature. Medical Journal of Australia, 204(S7), S22-S28.

Larson, P. D., & Foropon, C. (2018). Process improvement in humanitarian operations: an

organisational theory perspective. International Journal of Production Research, 56(21),

6828-6841.

References

Brajer-Marczak, R. (2014). Employee engagement in continuous improvement of processes.

Management, 18(2), 88-103.

Cardos, I.R. and Cardos, V.D., 2014. Measuring customer profitability with activity-based

costing and balanced scorecard. Annales Universitatis Apulensis: Series Oeconomica,

16(1), p.52.

Delić, M., Radlovački, V., Kamberović, B., Maksimović, R., & Pečujlija, M. (2014). Examining

relationships between quality management and organisational performance in transitional

economies. Total Quality Management & Business Excellence, 25(3-4), 367-382.

Dixon-Woods, M., & Martin, G. P. (2016). Does quality improvement improve quality?. Future

Hospital Journal, 3(3), 191-194.

Goetsch, D.L. and Davis, S.B., 2014. Quality management for organizational excellence. Upper

Saddle River, NJ: pearson.

Hamid, F.A.H., 2014. The Impact of Activity-Based Costing System Application on Enhancing

Company’s Financial Performance (Doctoral dissertation, Sudan University of Science

And Technology).

Janamian, T., Upham, S. J., Crossland, L., & Jackson, C. L. (2016). Quality tools and resources

to support organisational improvement integral to high‐quality primary care: a systematic

review of published and grey literature. Medical Journal of Australia, 204(S7), S22-S28.

Larson, P. D., & Foropon, C. (2018). Process improvement in humanitarian operations: an

organisational theory perspective. International Journal of Production Research, 56(21),

6828-6841.

12MAJOR ISSUES IN REGARD TO ACTIVITY BASED MANAGEMENT (ABM)

McCabe, S. (2014). Quality Improvement Techniques in Construction: Principles and Methods.

Routledge.

Oseifuah, E.K., 2014. Activity based costing (ABC) in the public sector: Benefits and

challenges. Problems and Perspectives in Management, 12(4), pp.581-588.

Robert, G., & Fulop, N. (2014). The role of context in successful improvement. Perspectives on

context. A selection of essays considering the role of context in successful quality

improvement. London: Health Foundation, 31.

Tortorella, G. L., & Fogliatto, F. S. (2014). Method for assessing human resources management

practices and organisational learning factors in a company under lean manufacturing

implementation. International Journal of Production Research, 52(15), 4623-4645.

Vindrola-Padros, C., Pape, T., Utley, M., & Fulop, N. J. (2017). The role of embedded research

in quality improvement: a narrative review. BMJ Qual Saf, 26(1), 70-80.

McCabe, S. (2014). Quality Improvement Techniques in Construction: Principles and Methods.

Routledge.

Oseifuah, E.K., 2014. Activity based costing (ABC) in the public sector: Benefits and

challenges. Problems and Perspectives in Management, 12(4), pp.581-588.

Robert, G., & Fulop, N. (2014). The role of context in successful improvement. Perspectives on

context. A selection of essays considering the role of context in successful quality

improvement. London: Health Foundation, 31.

Tortorella, G. L., & Fogliatto, F. S. (2014). Method for assessing human resources management

practices and organisational learning factors in a company under lean manufacturing

implementation. International Journal of Production Research, 52(15), 4623-4645.

Vindrola-Padros, C., Pape, T., Utley, M., & Fulop, N. J. (2017). The role of embedded research

in quality improvement: a narrative review. BMJ Qual Saf, 26(1), 70-80.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.