Management Accounting – Case Study: Make or Buy Decisions

Discuss a case study on whether a company should make or buy a subassembly component based on cost estimates and a supplier's offer.

6 Pages1141 Words105 Views

Added on 2023-05-28

About This Document

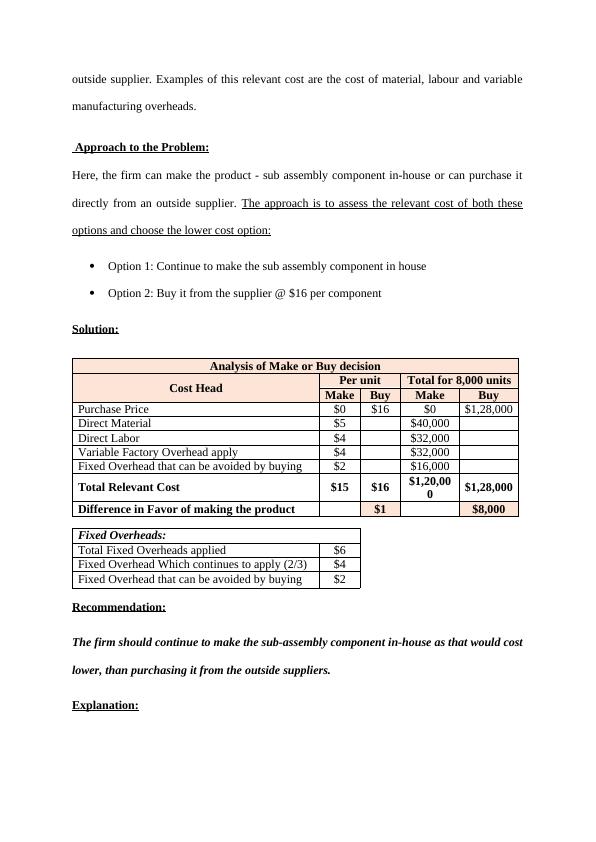

This case study explores the make or buy decision for a firm and the relevant cost analysis approach. The recommendation is to continue making the sub-assembly component in-house. Qualitative and quantitative factors are discussed.

Management Accounting – Case Study: Make or Buy Decisions

Discuss a case study on whether a company should make or buy a subassembly component based on cost estimates and a supplier's offer.

Added on 2023-05-28

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Differential Analysis

|5

|1032

|72

Make-or-Buy Decision: Benefits of Manufacturing or Outsourcing

|7

|1070

|138

Make or Buy Decisions Analysis | Assignment

|10

|1220

|375

Management Accounting Portfolio and Analysis

|6

|891

|32

Assignment on Management Accounting & Control

|13

|4123

|61

1102AFE ACCOUNTING FOR DECISION MAKING - Homework

|3

|742

|40