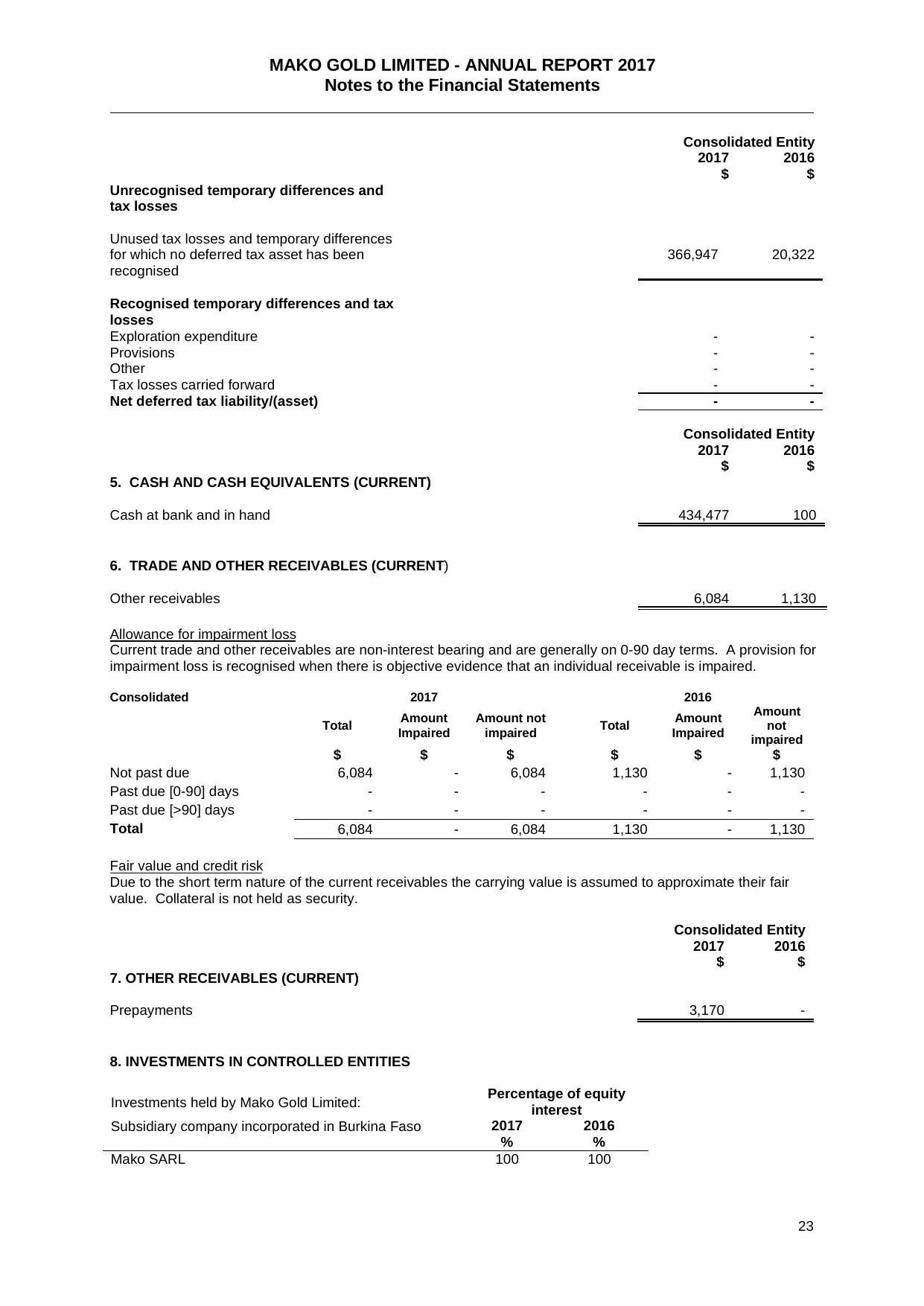

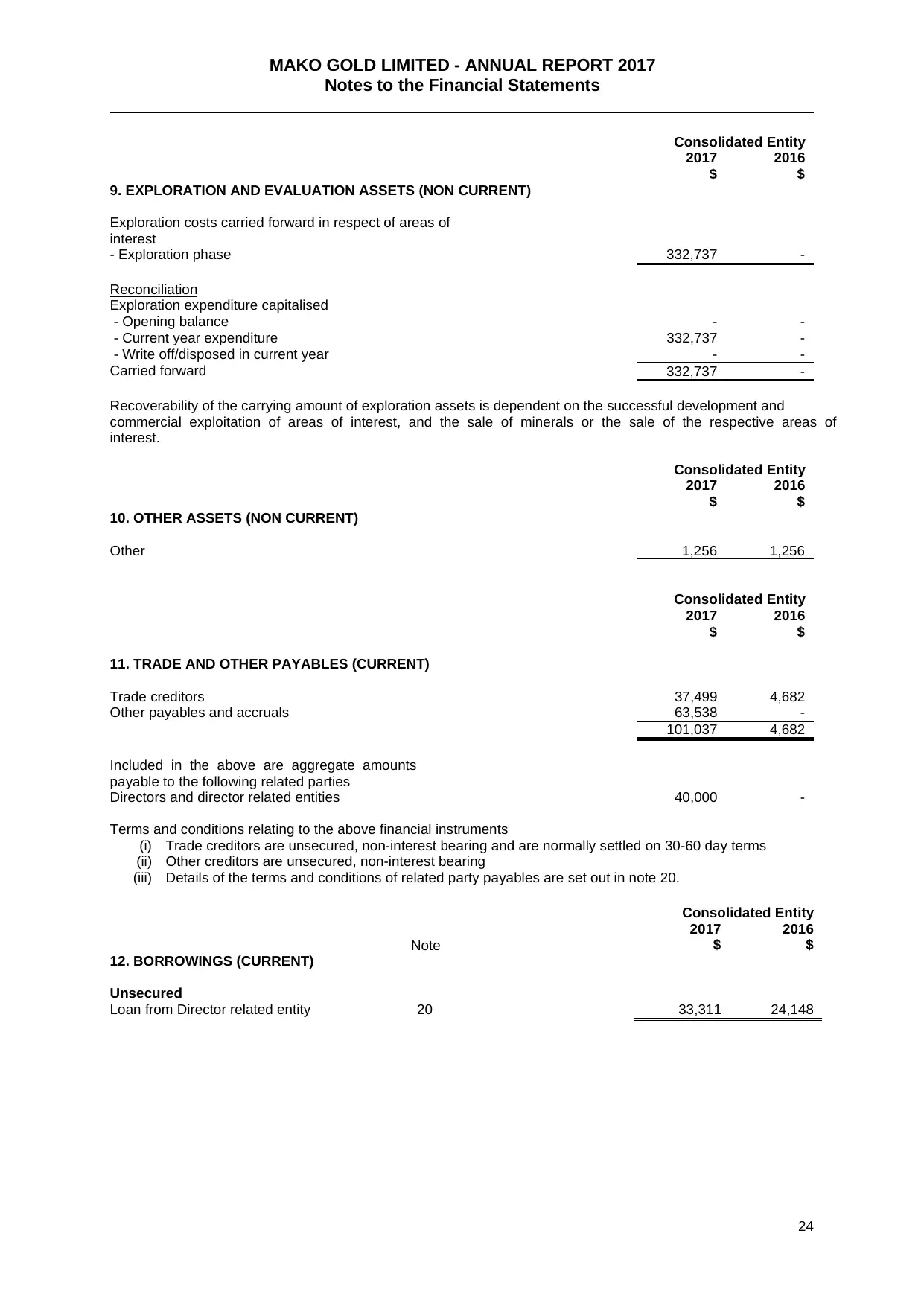

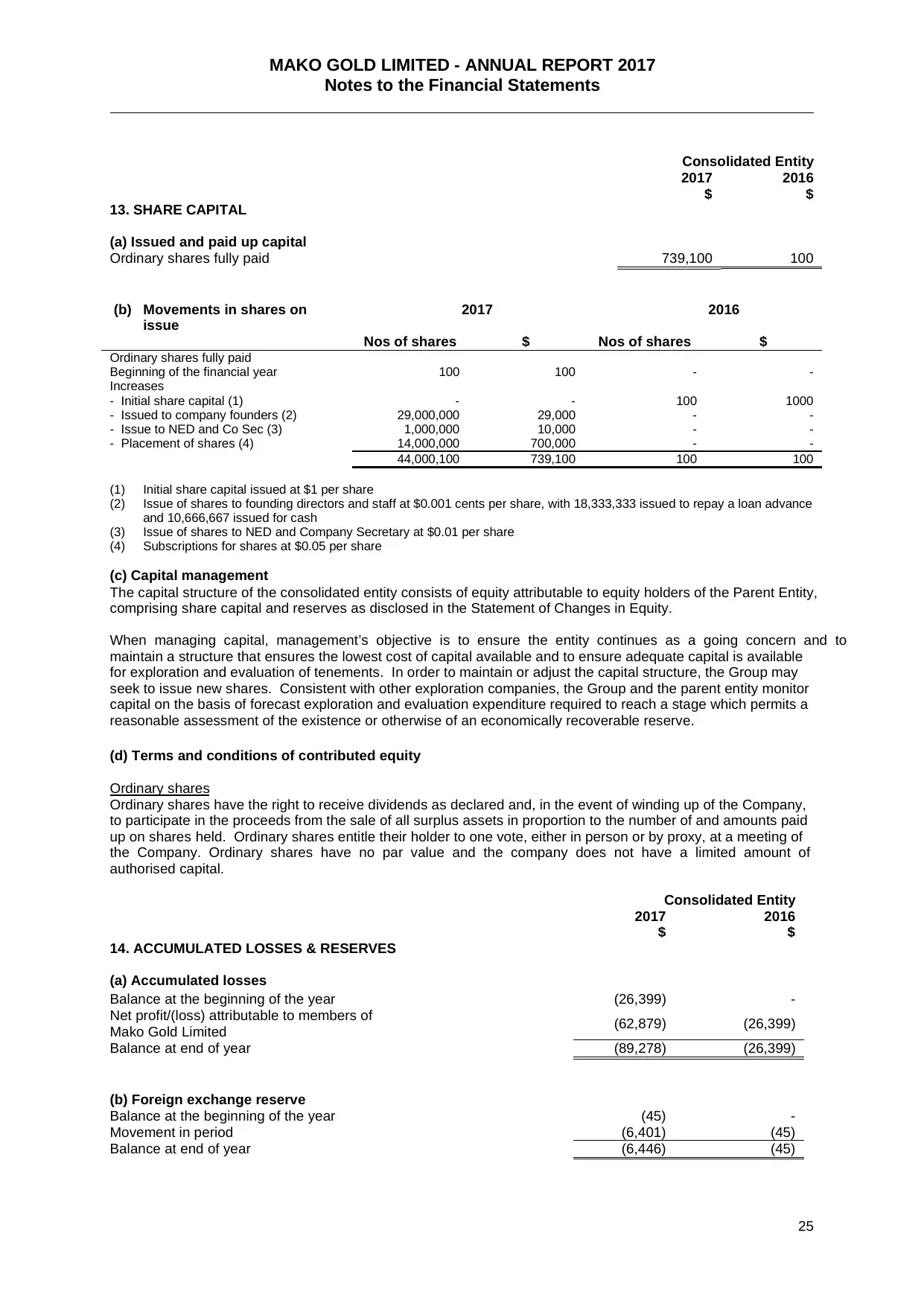

Mako Gold Limited Annual Report 2017

VerifiedAdded on 2023/06/11

|33

|13240

|416

AI Summary

This annual report covers Mako Gold Limited and its subsidiaries, with a focus on the company's exploration for high-grade gold deposits in Burkina Faso and other West African countries. The report includes a review of operations, directors' report, financial statements, and information on the company's corporate structure and capital structure. The report also covers the company's Farm-in and Joint Venture Agreement on the Napié Permit in Côte d’Ivoire with Perseus Mining Limited’s Côte d’Ivoire subsidiary, Occidental Gold SARL.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MAKO GOLD LIMITED

A.C.N. 606 241 829

ANNUAL REPORT 30 JUNE 2017

A.C.N. 606 241 829

ANNUAL REPORT 30 JUNE 2017

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MAKO GOLD LIMITED

ANNUAL REPORT 2017

2

INDEX

Page Number

Corporate Information 3

Review of Operations 4 - 5

Directors’ Report 6 - 10

Auditor Independence Declaration 11

Statement of Comprehensive Income 12

Balance Sheet 13

Statement of Changes in Equity 14

Statement of Cash Flows 15

Notes to the Financial Statements 16 - 30

Directors’ Declaration 31

Independent Auditor’s Report to the Members 32

ANNUAL REPORT 2017

2

INDEX

Page Number

Corporate Information 3

Review of Operations 4 - 5

Directors’ Report 6 - 10

Auditor Independence Declaration 11

Statement of Comprehensive Income 12

Balance Sheet 13

Statement of Changes in Equity 14

Statement of Cash Flows 15

Notes to the Financial Statements 16 - 30

Directors’ Declaration 31

Independent Auditor’s Report to the Members 32

MAKO GOLD LIMITED

ANNUAL REPORT 2017

3

CORPORATE INFORMATION

This annual report covers Mako Gold Limited (“Company” or “Mako”) as a consolidated entity

comprising Mako Gold Limited and its subsidiaries (‘the Consolidated Entity”). A description of the

operations and of the principal activities is included in the directors’ report and the review of

operations. The directors’ report is not part of the financial report.

DIRECTORS

Mark Elliott (Non-Executive Chairman)

Peter Ledwidge (Managing Director)

Michele Muscillo (Non-Executive Director)

SECRETARY

Paul Marshall

AUSTRALIAN BUSINESS NUMBER

ABN 84 606 241 829

REGISTERED OFFICE

Level 8

Waterfront Place

1 Eagle St

Brisbane Qld 4000

Telephone: (07) 3108 3500

Facsimile: (07) 3108 3501

Email: admin@makogold.com.au

Web: www.makogold.com.au

AUDITORS

BDO Audit Pty Ltd

Level 10,

12 Creek St

Brisbane QLD 4000

SOLICITORS

HopgoodGanim

Level 8

Waterfront Place

1 Eagle St

Brisbane Qld 4000

ANNUAL REPORT 2017

3

CORPORATE INFORMATION

This annual report covers Mako Gold Limited (“Company” or “Mako”) as a consolidated entity

comprising Mako Gold Limited and its subsidiaries (‘the Consolidated Entity”). A description of the

operations and of the principal activities is included in the directors’ report and the review of

operations. The directors’ report is not part of the financial report.

DIRECTORS

Mark Elliott (Non-Executive Chairman)

Peter Ledwidge (Managing Director)

Michele Muscillo (Non-Executive Director)

SECRETARY

Paul Marshall

AUSTRALIAN BUSINESS NUMBER

ABN 84 606 241 829

REGISTERED OFFICE

Level 8

Waterfront Place

1 Eagle St

Brisbane Qld 4000

Telephone: (07) 3108 3500

Facsimile: (07) 3108 3501

Email: admin@makogold.com.au

Web: www.makogold.com.au

AUDITORS

BDO Audit Pty Ltd

Level 10,

12 Creek St

Brisbane QLD 4000

SOLICITORS

HopgoodGanim

Level 8

Waterfront Place

1 Eagle St

Brisbane Qld 4000

MAKO GOLD LIMITED

ANNUAL REPORT 2017

4

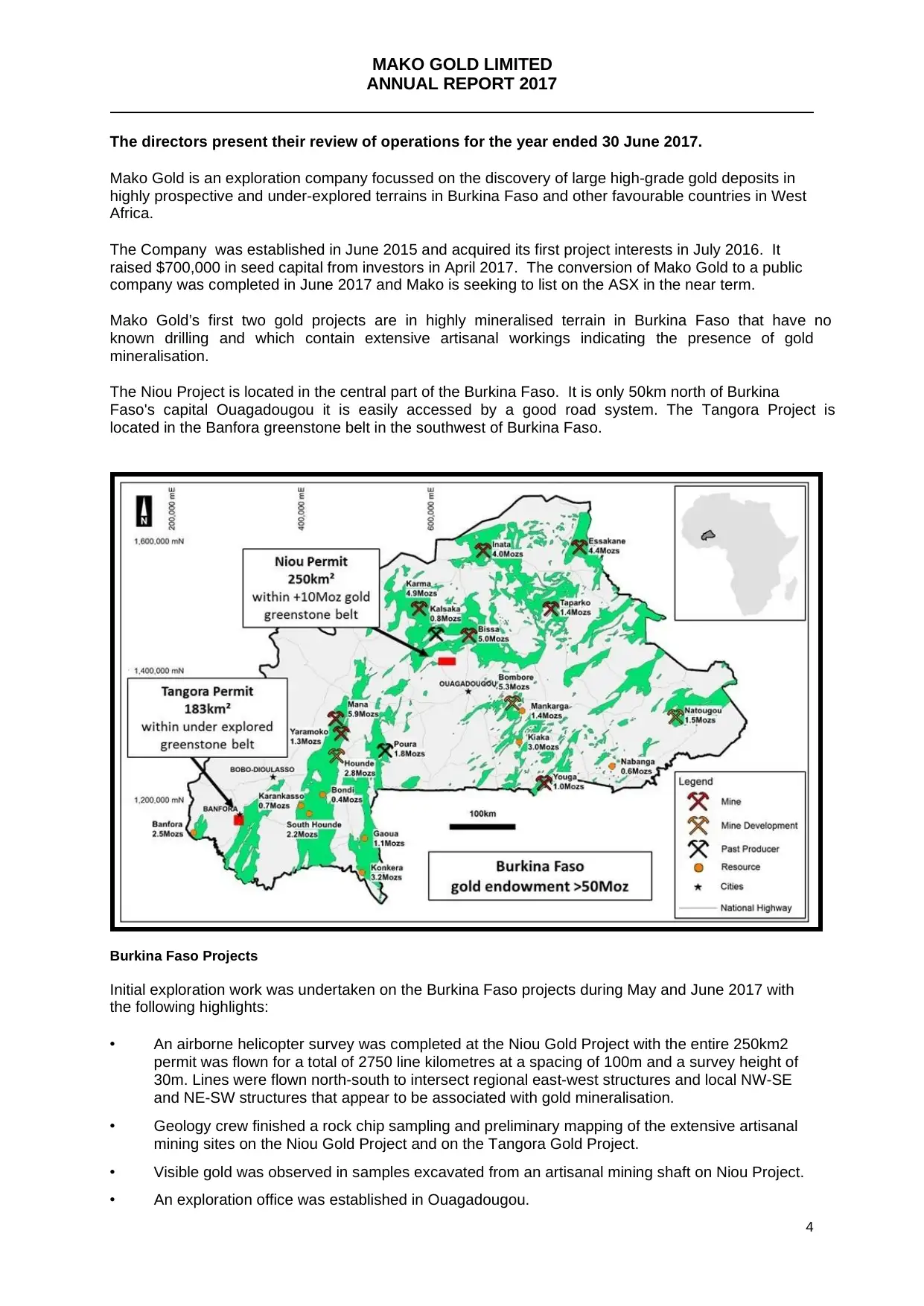

The directors present their review of operations for the year ended 30 June 2017.

Mako Gold is an exploration company focussed on the discovery of large high-grade gold deposits in

highly prospective and under-explored terrains in Burkina Faso and other favourable countries in West

Africa.

The Company was established in June 2015 and acquired its first project interests in July 2016. It

raised $700,000 in seed capital from investors in April 2017. The conversion of Mako Gold to a public

company was completed in June 2017 and Mako is seeking to list on the ASX in the near term.

Mako Gold’s first two gold projects are in highly mineralised terrain in Burkina Faso that have no

known drilling and which contain extensive artisanal workings indicating the presence of gold

mineralisation.

The Niou Project is located in the central part of the Burkina Faso. It is only 50km north of Burkina

Faso's capital Ouagadougou it is easily accessed by a good road system. The Tangora Project is

located in the Banfora greenstone belt in the southwest of Burkina Faso.

Burkina Faso Projects

Initial exploration work was undertaken on the Burkina Faso projects during May and June 2017 with

the following highlights:

• An airborne helicopter survey was completed at the Niou Gold Project with the entire 250km2

permit was flown for a total of 2750 line kilometres at a spacing of 100m and a survey height of

30m. Lines were flown north-south to intersect regional east-west structures and local NW-SE

and NE-SW structures that appear to be associated with gold mineralisation.

• Geology crew finished a rock chip sampling and preliminary mapping of the extensive artisanal

mining sites on the Niou Gold Project and on the Tangora Gold Project.

• Visible gold was observed in samples excavated from an artisanal mining shaft on Niou Project.

• An exploration office was established in Ouagadougou.

ANNUAL REPORT 2017

4

The directors present their review of operations for the year ended 30 June 2017.

Mako Gold is an exploration company focussed on the discovery of large high-grade gold deposits in

highly prospective and under-explored terrains in Burkina Faso and other favourable countries in West

Africa.

The Company was established in June 2015 and acquired its first project interests in July 2016. It

raised $700,000 in seed capital from investors in April 2017. The conversion of Mako Gold to a public

company was completed in June 2017 and Mako is seeking to list on the ASX in the near term.

Mako Gold’s first two gold projects are in highly mineralised terrain in Burkina Faso that have no

known drilling and which contain extensive artisanal workings indicating the presence of gold

mineralisation.

The Niou Project is located in the central part of the Burkina Faso. It is only 50km north of Burkina

Faso's capital Ouagadougou it is easily accessed by a good road system. The Tangora Project is

located in the Banfora greenstone belt in the southwest of Burkina Faso.

Burkina Faso Projects

Initial exploration work was undertaken on the Burkina Faso projects during May and June 2017 with

the following highlights:

• An airborne helicopter survey was completed at the Niou Gold Project with the entire 250km2

permit was flown for a total of 2750 line kilometres at a spacing of 100m and a survey height of

30m. Lines were flown north-south to intersect regional east-west structures and local NW-SE

and NE-SW structures that appear to be associated with gold mineralisation.

• Geology crew finished a rock chip sampling and preliminary mapping of the extensive artisanal

mining sites on the Niou Gold Project and on the Tangora Gold Project.

• Visible gold was observed in samples excavated from an artisanal mining shaft on Niou Project.

• An exploration office was established in Ouagadougou.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MAKO GOLD LIMITED

ANNUAL REPORT 2017

5

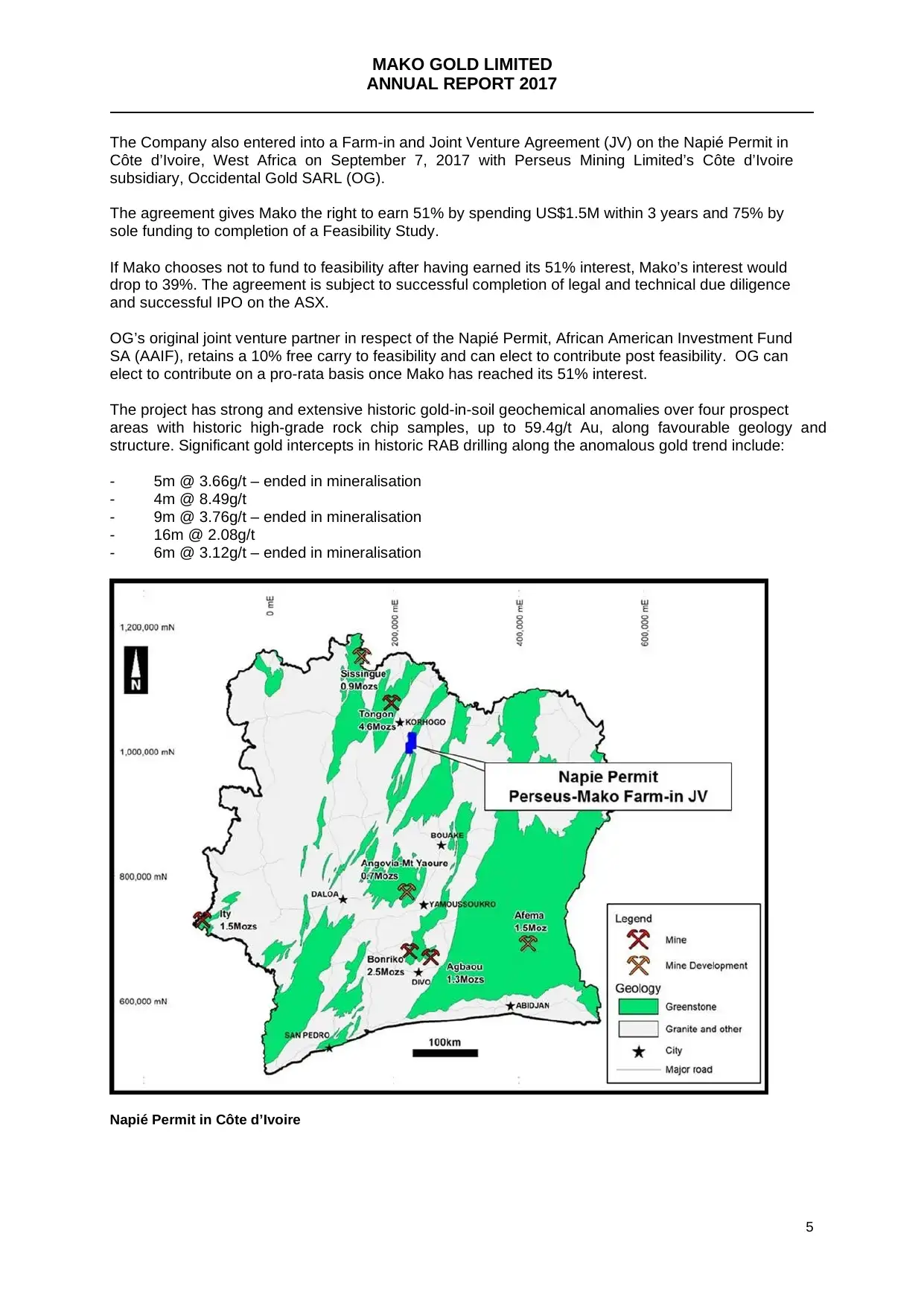

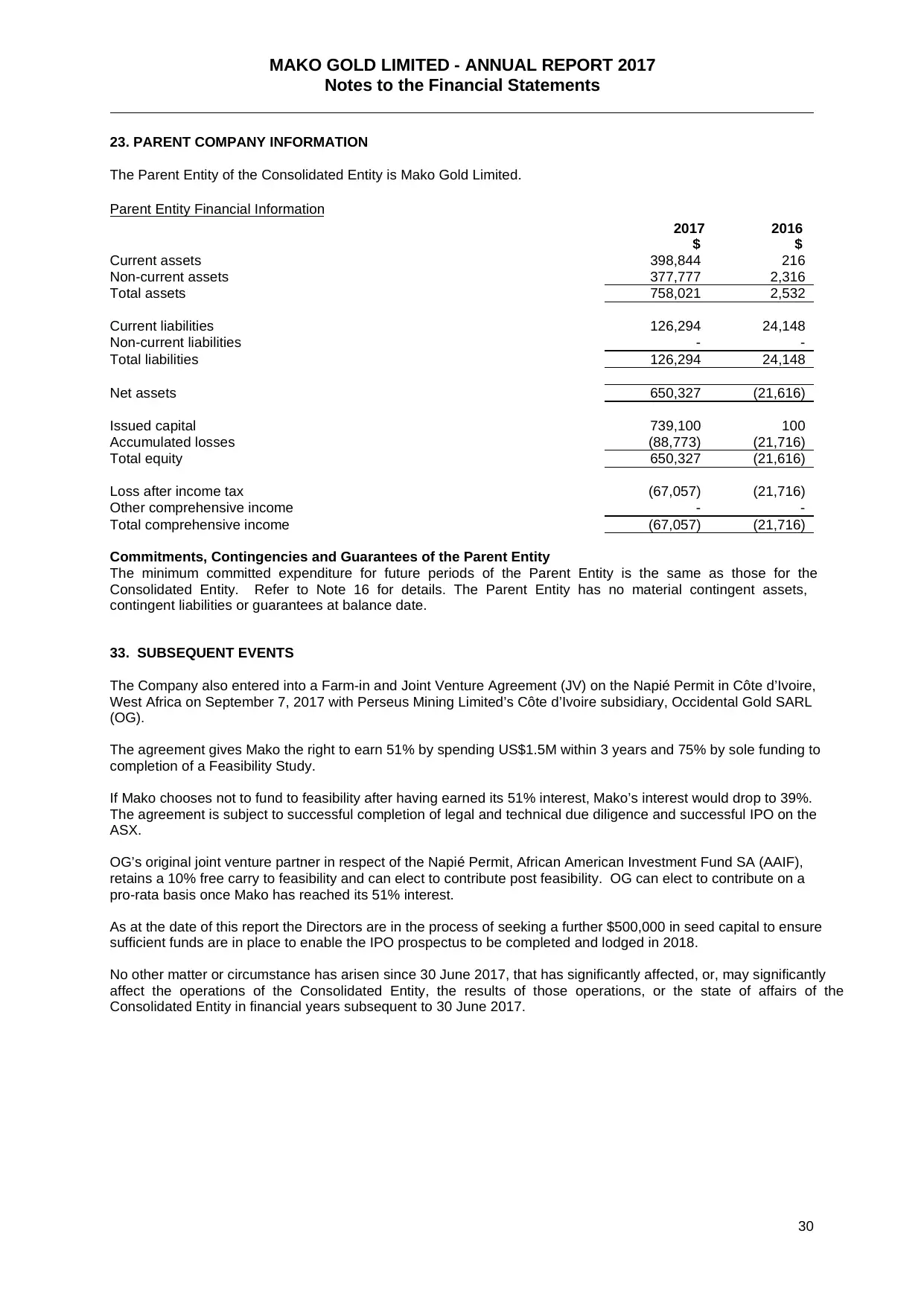

The Company also entered into a Farm-in and Joint Venture Agreement (JV) on the Napié Permit in

Côte d’Ivoire, West Africa on September 7, 2017 with Perseus Mining Limited’s Côte d’Ivoire

subsidiary, Occidental Gold SARL (OG).

The agreement gives Mako the right to earn 51% by spending US$1.5M within 3 years and 75% by

sole funding to completion of a Feasibility Study.

If Mako chooses not to fund to feasibility after having earned its 51% interest, Mako’s interest would

drop to 39%. The agreement is subject to successful completion of legal and technical due diligence

and successful IPO on the ASX.

OG’s original joint venture partner in respect of the Napié Permit, African American Investment Fund

SA (AAIF), retains a 10% free carry to feasibility and can elect to contribute post feasibility. OG can

elect to contribute on a pro-rata basis once Mako has reached its 51% interest.

The project has strong and extensive historic gold-in-soil geochemical anomalies over four prospect

areas with historic high-grade rock chip samples, up to 59.4g/t Au, along favourable geology and

structure. Significant gold intercepts in historic RAB drilling along the anomalous gold trend include:

- 5m @ 3.66g/t – ended in mineralisation

- 4m @ 8.49g/t

- 9m @ 3.76g/t – ended in mineralisation

- 16m @ 2.08g/t

- 6m @ 3.12g/t – ended in mineralisation

Napié Permit in Côte d’Ivoire

ANNUAL REPORT 2017

5

The Company also entered into a Farm-in and Joint Venture Agreement (JV) on the Napié Permit in

Côte d’Ivoire, West Africa on September 7, 2017 with Perseus Mining Limited’s Côte d’Ivoire

subsidiary, Occidental Gold SARL (OG).

The agreement gives Mako the right to earn 51% by spending US$1.5M within 3 years and 75% by

sole funding to completion of a Feasibility Study.

If Mako chooses not to fund to feasibility after having earned its 51% interest, Mako’s interest would

drop to 39%. The agreement is subject to successful completion of legal and technical due diligence

and successful IPO on the ASX.

OG’s original joint venture partner in respect of the Napié Permit, African American Investment Fund

SA (AAIF), retains a 10% free carry to feasibility and can elect to contribute post feasibility. OG can

elect to contribute on a pro-rata basis once Mako has reached its 51% interest.

The project has strong and extensive historic gold-in-soil geochemical anomalies over four prospect

areas with historic high-grade rock chip samples, up to 59.4g/t Au, along favourable geology and

structure. Significant gold intercepts in historic RAB drilling along the anomalous gold trend include:

- 5m @ 3.66g/t – ended in mineralisation

- 4m @ 8.49g/t

- 9m @ 3.76g/t – ended in mineralisation

- 16m @ 2.08g/t

- 6m @ 3.12g/t – ended in mineralisation

Napié Permit in Côte d’Ivoire

MAKO GOLD LIMITED

ANNUAL REPORT 2017

6

Directors’ Report

The directors present their report on Mako Gold Limited and its controlled entities (the “company”,

“consolidated entity”, “Group” or “Mako”) for the year ended 30 June 2017.

Directors

The names and details of the Company’s directors in office during the financial year and until the date

of this report are as follows. Directors were in office for the entire period unless otherwise stated.

Names, qualifications, experience and special responsibilities

SM Elliott (Non-Executive Chairman) Dip Appl Geology, PhD, FAICD, FAusIMM(CP Geol), FAIG,

FSEG

Appointed 14 March 2017

Mark Elliott, a founder of Mako Gold, is a Chartered Professional (CP) geologist with over 40 years’

experience in economic geology, exploration, mining, project development and in corporate

management roles as chairman and managing director for a number of ASX-listed resource

companies.

Mark has extensive experience in managing companies and exploration/mining operations in a wide

range of commodities including gold. His management experience includes founding IPOs from

commencement of project acquisition, exploration to production, capital raising and negotiating joint

ventures. Dr Elliott is a Non-Executive Director of environmental audit and hazardous materials

analytical laboratory and geothermal developer company HRL Holdings Limited and a Non-Executive

Director of Western Australian Archean gold explorer, Nexus Minerals Limited.

P Ledwidge (Managing Director) BSc Geology, MAusIMM

Appointed 4 June 2015

Peter Ledwidge, a founder of Mako Gold, is a qualified geologist with over 30 years’ experience in the

exploration and mining industry. His career has focussed primarily on gold exploration along with

some base metals exploration. Peter has worked extensively in Canada, Africa and Australia, in a

variety of roles in exploration, development and mining projects.

Most recently he spent six years working for ASX-listed Orbis Gold in progressive senior management

roles whereby he secured all of Orbis’ permits in Burkina Faso and Côte d’Ivoire. Peter played a

critical role in the discovery of the Nabanga gold deposit in Burkina Faso and thereafter contributed

geological ideas which helped achieve success for the company including the discovery of the

Natougou gold deposit, currently being developed by TSX-listed Semafo.

Peter is fluently bilingual in French and has established and maintained good professional contacts in

Burkina Faso and Cote d’Ivoire in government as well as the private sector.

M Muscillo (Non-Executive Director) LLB

Appointed 20 April 2017

Michele Muscillo is a Partner specialising in corporate law with HopgoodGanim Lawyers. He is an

admitted Solicitor and has a practice focusing almost exclusively on mergers and acquisitions, and

capital raising. He has a Bachelor of Laws from Queensland University of Technology and was a

recipient of the QUT University Medal.

In his role with HopgoodGanim Lawyers, Mr Muscillo has acted on a variety of corporate transactions

including initial public offerings, takeovers and other acquisitions. Michele’s experience brings to the

Board expertise on corporate regulation, governance and compliance matters.

Mr Muscillo was previously a director of ASX-Listed Orbis Gold Limited until its takeover by TSX-Listed

Semafo, and is a non-executive director of ASX-Listed Aeris Resources Limited.

ANNUAL REPORT 2017

6

Directors’ Report

The directors present their report on Mako Gold Limited and its controlled entities (the “company”,

“consolidated entity”, “Group” or “Mako”) for the year ended 30 June 2017.

Directors

The names and details of the Company’s directors in office during the financial year and until the date

of this report are as follows. Directors were in office for the entire period unless otherwise stated.

Names, qualifications, experience and special responsibilities

SM Elliott (Non-Executive Chairman) Dip Appl Geology, PhD, FAICD, FAusIMM(CP Geol), FAIG,

FSEG

Appointed 14 March 2017

Mark Elliott, a founder of Mako Gold, is a Chartered Professional (CP) geologist with over 40 years’

experience in economic geology, exploration, mining, project development and in corporate

management roles as chairman and managing director for a number of ASX-listed resource

companies.

Mark has extensive experience in managing companies and exploration/mining operations in a wide

range of commodities including gold. His management experience includes founding IPOs from

commencement of project acquisition, exploration to production, capital raising and negotiating joint

ventures. Dr Elliott is a Non-Executive Director of environmental audit and hazardous materials

analytical laboratory and geothermal developer company HRL Holdings Limited and a Non-Executive

Director of Western Australian Archean gold explorer, Nexus Minerals Limited.

P Ledwidge (Managing Director) BSc Geology, MAusIMM

Appointed 4 June 2015

Peter Ledwidge, a founder of Mako Gold, is a qualified geologist with over 30 years’ experience in the

exploration and mining industry. His career has focussed primarily on gold exploration along with

some base metals exploration. Peter has worked extensively in Canada, Africa and Australia, in a

variety of roles in exploration, development and mining projects.

Most recently he spent six years working for ASX-listed Orbis Gold in progressive senior management

roles whereby he secured all of Orbis’ permits in Burkina Faso and Côte d’Ivoire. Peter played a

critical role in the discovery of the Nabanga gold deposit in Burkina Faso and thereafter contributed

geological ideas which helped achieve success for the company including the discovery of the

Natougou gold deposit, currently being developed by TSX-listed Semafo.

Peter is fluently bilingual in French and has established and maintained good professional contacts in

Burkina Faso and Cote d’Ivoire in government as well as the private sector.

M Muscillo (Non-Executive Director) LLB

Appointed 20 April 2017

Michele Muscillo is a Partner specialising in corporate law with HopgoodGanim Lawyers. He is an

admitted Solicitor and has a practice focusing almost exclusively on mergers and acquisitions, and

capital raising. He has a Bachelor of Laws from Queensland University of Technology and was a

recipient of the QUT University Medal.

In his role with HopgoodGanim Lawyers, Mr Muscillo has acted on a variety of corporate transactions

including initial public offerings, takeovers and other acquisitions. Michele’s experience brings to the

Board expertise on corporate regulation, governance and compliance matters.

Mr Muscillo was previously a director of ASX-Listed Orbis Gold Limited until its takeover by TSX-Listed

Semafo, and is a non-executive director of ASX-Listed Aeris Resources Limited.

MAKO GOLD LIMITED

ANNUAL REPORT 2017

7

Company Secretary

P Marshall LLB, ACA

Appointed 13 April 2017

Paul Marshall holds a Bachelor of Law degree and is a Chartered Accountant. He has more than

thirty years experience including over twenty years spent in commercial roles as Company Secretary

and CFO for a number of listed and unlisted companies mainly in the resources sector.

Ann Ledwidge BSc Geology (hon), MAusIMM

Appointed 16 May 2016, resigned 13 April 2017

Ann Ledwidge, the Company’s Exploration Manager, was the initial Company Secretary from the date

of Mako’s incorporation up to the appointment of Paul Marshall in April 2017.

Interests in the shares and options of the Company

Interests of the directors in the shares and options of the Company as at the date of this report are:

Ordinary Shares

Mark Elliott 8,666,667

Peter Ledwidge 18,333,433

Michele Muscillo 500,000

Corporate Information

Corporate Structure

Mako Gold Limited is a company limited by shares that is incorporated and domiciled in Australia.

Mako Gold Limited has prepared a consolidated financial report encompassing the entities that it

controlled or had significant influence over during the financial year: Mako Gold Limited had the

following investments in controlled companies throughout the financial year:

- Mako Gold SARL (Incorporated in Burkina Faso - 100%)

Principal Activities

The principal activities of the consolidated entity during the year were the acquisition of and

exploration of gold tenements.

Operating Results

During the year Mako acquired its first project interests in Burkina Faso.

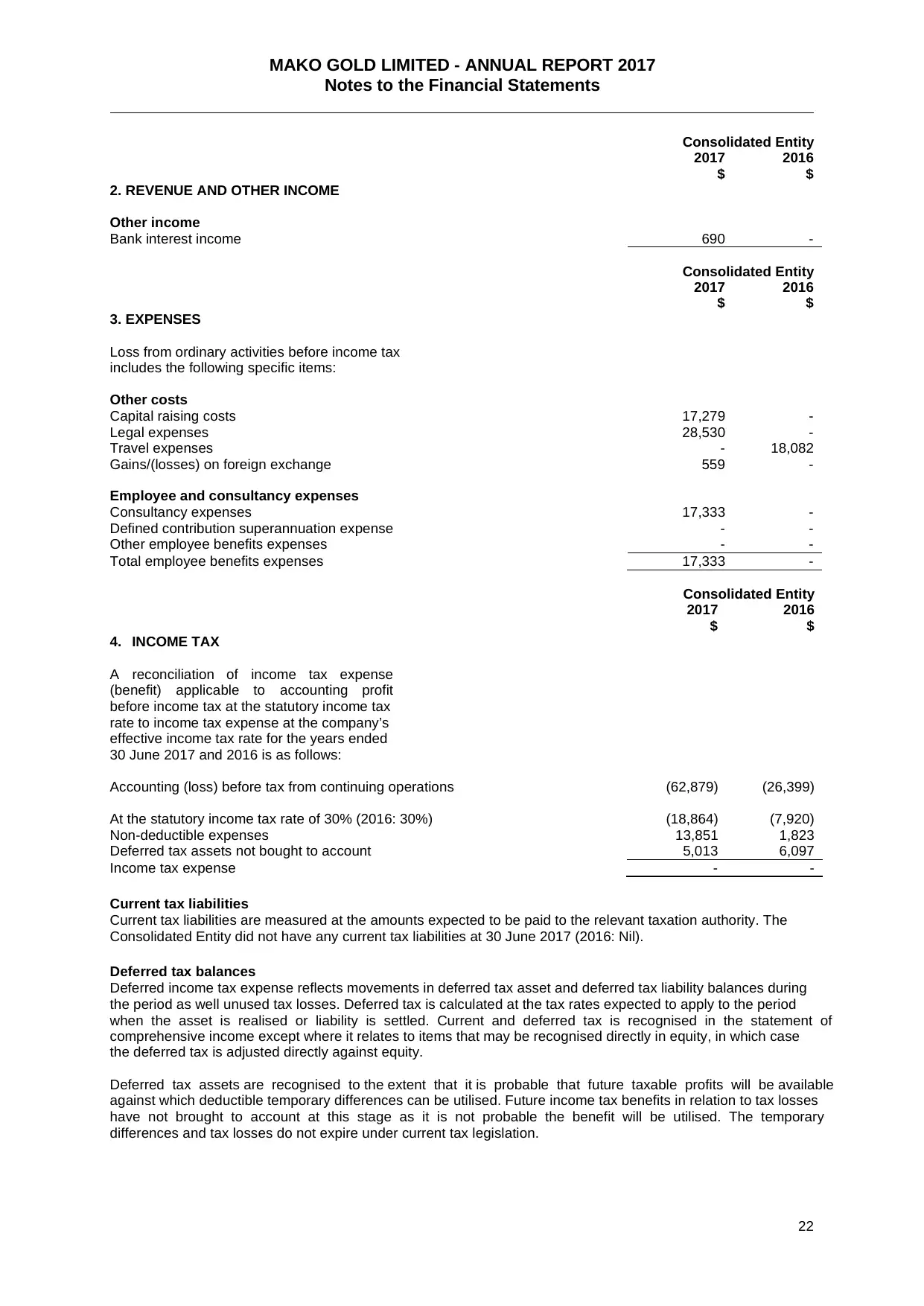

Revenue

As an early stage exploration company, Mako Gold Limited does not generate any income.

Expenses

The Consolidated Entity’s main sources of expenses are as follows:

2017

$

Employment and consultancy expenses 17,333

Corporate & Administration expenses 46,235

Total expenses 53,568

ANNUAL REPORT 2017

7

Company Secretary

P Marshall LLB, ACA

Appointed 13 April 2017

Paul Marshall holds a Bachelor of Law degree and is a Chartered Accountant. He has more than

thirty years experience including over twenty years spent in commercial roles as Company Secretary

and CFO for a number of listed and unlisted companies mainly in the resources sector.

Ann Ledwidge BSc Geology (hon), MAusIMM

Appointed 16 May 2016, resigned 13 April 2017

Ann Ledwidge, the Company’s Exploration Manager, was the initial Company Secretary from the date

of Mako’s incorporation up to the appointment of Paul Marshall in April 2017.

Interests in the shares and options of the Company

Interests of the directors in the shares and options of the Company as at the date of this report are:

Ordinary Shares

Mark Elliott 8,666,667

Peter Ledwidge 18,333,433

Michele Muscillo 500,000

Corporate Information

Corporate Structure

Mako Gold Limited is a company limited by shares that is incorporated and domiciled in Australia.

Mako Gold Limited has prepared a consolidated financial report encompassing the entities that it

controlled or had significant influence over during the financial year: Mako Gold Limited had the

following investments in controlled companies throughout the financial year:

- Mako Gold SARL (Incorporated in Burkina Faso - 100%)

Principal Activities

The principal activities of the consolidated entity during the year were the acquisition of and

exploration of gold tenements.

Operating Results

During the year Mako acquired its first project interests in Burkina Faso.

Revenue

As an early stage exploration company, Mako Gold Limited does not generate any income.

Expenses

The Consolidated Entity’s main sources of expenses are as follows:

2017

$

Employment and consultancy expenses 17,333

Corporate & Administration expenses 46,235

Total expenses 53,568

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MAKO GOLD LIMITED

ANNUAL REPORT 2017

8

Comparison with Prior Year

For the year ended 30 June 2017, the loss for the Consolidated Entity after providing for income tax

was $62,879 (2016: loss of $26,399):

2017 2016

$ $

Revenue and other income 690 -

Employment costs (17,333) -

Travel costs - (18,082)

Other expenses (46,235) (8,317)

Loss before income tax (62,879) (26,399)

This increase is attributable to:

$

Increase in employee costs 17,333

Reduction in travel costs (18,082)

Other net changes in sundry revenue, administrative and other costs 37,229

36,480

Review of Financial Condition

Capital structure

In the 2017 financial year Mako issued the following new securities:

• April 2017 issue of founders shares - 29,000,000 at $0.001 per share

• April 2017 issue of 1,000,000 shares to NED & Company Secretary at $.01 per share

• May 2017 issue of 14,000,000 shares at $0.05 to seed capital applicants

At 30 June 2017, the Company had 44,000,100 ordinary shares on issue.

Treasury policy

The Company does not have a formally established treasury function. The Board is responsible for

managing the Company’s currency risks and finance facilities.

Liquidity and funding

The Company has in the 2017 financial year raised initial seed capital of $700,000 (before costs of

issue) with the aim being that these funds will be sufficient to see the company through to an IPO and

a listing on ASX.

Dividends

No dividend was paid during the year and none is recommended as at 30 June 2017.

Significant Changes in the State of Affairs

There were no significant changes in the State of Affairs of the Consolidated Entity during the year

apart from those items covered in the review of operations above.

Matters Subsequent to the End of the Financial Year

The Company also entered into a Farm-in and Joint Venture Agreement (JV) on the Napié Permit in

Côte d’Ivoire, West Africa on September 7, 2017 with Perseus Mining Limited’s Côte d’Ivoire

subsidiary, Occidental Gold SARL (OG).

The agreement gives Mako the right to earn 51% by spending US$1.5M within 3 years and 75% by

sole funding to completion of a Feasibility Study.

ANNUAL REPORT 2017

8

Comparison with Prior Year

For the year ended 30 June 2017, the loss for the Consolidated Entity after providing for income tax

was $62,879 (2016: loss of $26,399):

2017 2016

$ $

Revenue and other income 690 -

Employment costs (17,333) -

Travel costs - (18,082)

Other expenses (46,235) (8,317)

Loss before income tax (62,879) (26,399)

This increase is attributable to:

$

Increase in employee costs 17,333

Reduction in travel costs (18,082)

Other net changes in sundry revenue, administrative and other costs 37,229

36,480

Review of Financial Condition

Capital structure

In the 2017 financial year Mako issued the following new securities:

• April 2017 issue of founders shares - 29,000,000 at $0.001 per share

• April 2017 issue of 1,000,000 shares to NED & Company Secretary at $.01 per share

• May 2017 issue of 14,000,000 shares at $0.05 to seed capital applicants

At 30 June 2017, the Company had 44,000,100 ordinary shares on issue.

Treasury policy

The Company does not have a formally established treasury function. The Board is responsible for

managing the Company’s currency risks and finance facilities.

Liquidity and funding

The Company has in the 2017 financial year raised initial seed capital of $700,000 (before costs of

issue) with the aim being that these funds will be sufficient to see the company through to an IPO and

a listing on ASX.

Dividends

No dividend was paid during the year and none is recommended as at 30 June 2017.

Significant Changes in the State of Affairs

There were no significant changes in the State of Affairs of the Consolidated Entity during the year

apart from those items covered in the review of operations above.

Matters Subsequent to the End of the Financial Year

The Company also entered into a Farm-in and Joint Venture Agreement (JV) on the Napié Permit in

Côte d’Ivoire, West Africa on September 7, 2017 with Perseus Mining Limited’s Côte d’Ivoire

subsidiary, Occidental Gold SARL (OG).

The agreement gives Mako the right to earn 51% by spending US$1.5M within 3 years and 75% by

sole funding to completion of a Feasibility Study.

MAKO GOLD LIMITED

ANNUAL REPORT 2017

9

If Mako chooses not to fund to feasibility after having earned its 51% interest, Mako’s interest would

drop to 39%. The agreement is subject to successful completion of legal and technical due diligence

and successful IPO on the ASX.

OG’s original joint venture partner in respect of the Napié Permit, African American Investment Fund

SA (AAIF), retains a 10% free carry to feasibility and can elect to contribute post feasibility. OG can

elect to contribute on a pro-rata basis once Mako has reached its 51% interest.

No other matter or circumstance has arisen since 30 June 2017, that has significantly affected, or, may

significantly affect the operations of the Consolidated Entity, the results of those operations, or the

state of affairs of the Consolidated Entity in financial years subsequent to 30 June 2017.

Likely Developments and Expected Results of Operations

There are no developments of which the directors are aware which could be expected to affect the

results of the Consolidated Entity’s operations in subsequent financial years other than information

which the directors believe comment on or disclosure of, would prejudice the interests of the

Consolidated Entity.

Share Options

At balance date and at the date of this report there are no options outstanding.

Meetings of Directors

The following table sets out the number of director’s meetings held during the year ended 30 June

2017 and the number of meetings attended by each director. There are no separate Board

Committees.

Directors’ Meetings

Director A B

M Elliott 3 3

P Ledwidge 3 3

M Muscillo 1 1

A = Number of meetings held during the time the Director held office during the year.

B = Number of meetings attended.

Indemnification of Officers or Auditor

The Company has entered into Deeds of Indemnity with each of the Directors. The Company has not

indemnified its auditor.

Proceedings on Behalf of the Company

No person has applied for leave of Court to bring proceedings on behalf of the Consolidated Entity or

intervene in any proceedings to which the Consolidated Entity is a party for the purpose of taking

responsibility on behalf of the Consolidated Entity for all or any part of those proceedings. The

Consolidated Entity was not a party to any such proceedings during the year.

Environmental Regulation and Performance

The Company held authorisations under various exploration licences. There have been no known

breaches of the authorisation or licence conditions.

ANNUAL REPORT 2017

9

If Mako chooses not to fund to feasibility after having earned its 51% interest, Mako’s interest would

drop to 39%. The agreement is subject to successful completion of legal and technical due diligence

and successful IPO on the ASX.

OG’s original joint venture partner in respect of the Napié Permit, African American Investment Fund

SA (AAIF), retains a 10% free carry to feasibility and can elect to contribute post feasibility. OG can

elect to contribute on a pro-rata basis once Mako has reached its 51% interest.

No other matter or circumstance has arisen since 30 June 2017, that has significantly affected, or, may

significantly affect the operations of the Consolidated Entity, the results of those operations, or the

state of affairs of the Consolidated Entity in financial years subsequent to 30 June 2017.

Likely Developments and Expected Results of Operations

There are no developments of which the directors are aware which could be expected to affect the

results of the Consolidated Entity’s operations in subsequent financial years other than information

which the directors believe comment on or disclosure of, would prejudice the interests of the

Consolidated Entity.

Share Options

At balance date and at the date of this report there are no options outstanding.

Meetings of Directors

The following table sets out the number of director’s meetings held during the year ended 30 June

2017 and the number of meetings attended by each director. There are no separate Board

Committees.

Directors’ Meetings

Director A B

M Elliott 3 3

P Ledwidge 3 3

M Muscillo 1 1

A = Number of meetings held during the time the Director held office during the year.

B = Number of meetings attended.

Indemnification of Officers or Auditor

The Company has entered into Deeds of Indemnity with each of the Directors. The Company has not

indemnified its auditor.

Proceedings on Behalf of the Company

No person has applied for leave of Court to bring proceedings on behalf of the Consolidated Entity or

intervene in any proceedings to which the Consolidated Entity is a party for the purpose of taking

responsibility on behalf of the Consolidated Entity for all or any part of those proceedings. The

Consolidated Entity was not a party to any such proceedings during the year.

Environmental Regulation and Performance

The Company held authorisations under various exploration licences. There have been no known

breaches of the authorisation or licence conditions.

MAKO GOLD LIMITED

ANNUAL REPORT 2017

10

The Auditor’s Independence Declaration is attached and forms part of the Director’s Report for the

year ended 30 June 2017.

BDO Audit Pty Ltd continues in office in accordance with section 327 of the Corporations Act 2001.

The Company may decide to employ the auditor on assignments additional to their statutory audit

duties where the auditor's expertise and experience with the Company and/or the group are important.

The Board of Directors has considered the position and are satisfied that the provision of the non-audit

services is compatible with the general standard of independence for auditors imposed by the

Corporations Act 2001. The Directors are satisfied that the provision of non-audit services by the

auditor, as set out below, did not compromise the auditor independence requirements of the

Corporations Act 2001 for the following reasons:

• all non-audit services have been reviewed by the Board of Directors to ensure they do not

impact the impartiality and objectivity of the auditor

• none of the services undermine the general principles relating to auditor independence as set

out in APES 110 Code of Ethics for Professional Accountants.

During the year no fees were paid or are payable for non-audit services provided by the auditor of the

parent entity, BDO Audit Pty Ltd and its related practices.

Signed in accordance with a resolution of the Board of Directors

M Elliott

Chairman

Brisbane, 28 November 2017

ANNUAL REPORT 2017

10

The Auditor’s Independence Declaration is attached and forms part of the Director’s Report for the

year ended 30 June 2017.

BDO Audit Pty Ltd continues in office in accordance with section 327 of the Corporations Act 2001.

The Company may decide to employ the auditor on assignments additional to their statutory audit

duties where the auditor's expertise and experience with the Company and/or the group are important.

The Board of Directors has considered the position and are satisfied that the provision of the non-audit

services is compatible with the general standard of independence for auditors imposed by the

Corporations Act 2001. The Directors are satisfied that the provision of non-audit services by the

auditor, as set out below, did not compromise the auditor independence requirements of the

Corporations Act 2001 for the following reasons:

• all non-audit services have been reviewed by the Board of Directors to ensure they do not

impact the impartiality and objectivity of the auditor

• none of the services undermine the general principles relating to auditor independence as set

out in APES 110 Code of Ethics for Professional Accountants.

During the year no fees were paid or are payable for non-audit services provided by the auditor of the

parent entity, BDO Audit Pty Ltd and its related practices.

Signed in accordance with a resolution of the Board of Directors

M Elliott

Chairman

Brisbane, 28 November 2017

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MAKO GOLD LIMITED

ANNUAL REPORT 2016

AUDITOR’S INDEPENDENCE DECLARATION

Tel: +61 7 3237 5999

Fax: +61 7 3221 9227

www.bdo.com.au

Level 10, 12 Creek St

Brisbane QLD 4000

GPO Box 457 Brisbane QLD 4001

Australia

BDO Audit Pty Ltd ABN 33 134 022 870 is a member of a national association of independent entities which are all members of BDO Australia Ltd ABN 77 050

110 275, an Australian company limited by guarantee. BDO Audit Pty Ltd and BDO Australia Ltd are members of BDO International Ltd, a UK company limited

by guarantee, and form part of the international BDO network of independent member firms. Liability limited by a scheme approved under Professional

Standards Legislation, other than for the acts or omissions of financial services licensees.

DECLARATION OF INDEPENDENCE BY D P WRIGHT TO THE DIRECTORS OF MAKO GOLD LIMIT

As lead auditor of Mako Gold Limited for the year ended 30 June 2017, I declare that, to the best of my

knowledge and belief, there have been:

1. No contraventions of the auditor independence requirements of the Corporations Act 2001 in

relation to the audit; and

2. No contraventions of any applicable code of professional conduct in relation to the audit.

This declaration is in respect of Mako Gold Limited and the entity it controlled during the period.

D P Wright

Director

BDO Audit Pty Ltd

Brisbane, 5 December 2017

11

ANNUAL REPORT 2016

AUDITOR’S INDEPENDENCE DECLARATION

Tel: +61 7 3237 5999

Fax: +61 7 3221 9227

www.bdo.com.au

Level 10, 12 Creek St

Brisbane QLD 4000

GPO Box 457 Brisbane QLD 4001

Australia

BDO Audit Pty Ltd ABN 33 134 022 870 is a member of a national association of independent entities which are all members of BDO Australia Ltd ABN 77 050

110 275, an Australian company limited by guarantee. BDO Audit Pty Ltd and BDO Australia Ltd are members of BDO International Ltd, a UK company limited

by guarantee, and form part of the international BDO network of independent member firms. Liability limited by a scheme approved under Professional

Standards Legislation, other than for the acts or omissions of financial services licensees.

DECLARATION OF INDEPENDENCE BY D P WRIGHT TO THE DIRECTORS OF MAKO GOLD LIMIT

As lead auditor of Mako Gold Limited for the year ended 30 June 2017, I declare that, to the best of my

knowledge and belief, there have been:

1. No contraventions of the auditor independence requirements of the Corporations Act 2001 in

relation to the audit; and

2. No contraventions of any applicable code of professional conduct in relation to the audit.

This declaration is in respect of Mako Gold Limited and the entity it controlled during the period.

D P Wright

Director

BDO Audit Pty Ltd

Brisbane, 5 December 2017

11

MAKO GOLD LIMITED

ANNUAL REPORT 2017

12

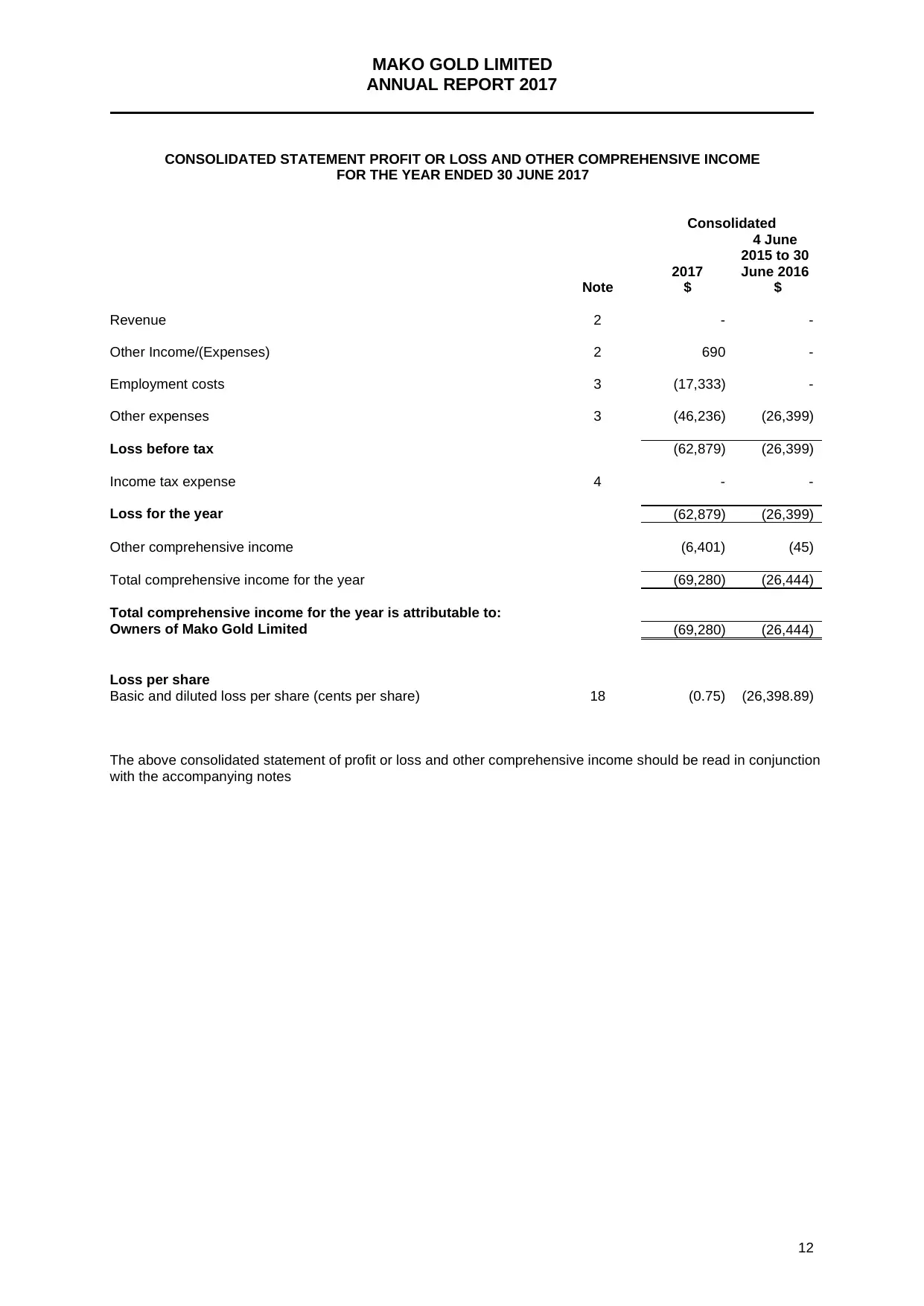

CONSOLIDATED STATEMENT PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

FOR THE YEAR ENDED 30 JUNE 2017

Consolidated

2017

4 June

2015 to 30

June 2016

Note $ $

Revenue 2 - -

Other Income/(Expenses) 2 690 -

Employment costs 3 (17,333) -

Other expenses 3 (46,236) (26,399)

Loss before tax (62,879) (26,399)

Income tax expense 4 - -

Loss for the year (62,879) (26,399)

Other comprehensive income (6,401) (45)

Total comprehensive income for the year (69,280) (26,444)

Total comprehensive income for the year is attributable to:

Owners of Mako Gold Limited (69,280) (26,444)

Loss per share

Basic and diluted loss per share (cents per share) 18 (0.75) (26,398.89)

The above consolidated statement of profit or loss and other comprehensive income should be read in conjunction

with the accompanying notes

ANNUAL REPORT 2017

12

CONSOLIDATED STATEMENT PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

FOR THE YEAR ENDED 30 JUNE 2017

Consolidated

2017

4 June

2015 to 30

June 2016

Note $ $

Revenue 2 - -

Other Income/(Expenses) 2 690 -

Employment costs 3 (17,333) -

Other expenses 3 (46,236) (26,399)

Loss before tax (62,879) (26,399)

Income tax expense 4 - -

Loss for the year (62,879) (26,399)

Other comprehensive income (6,401) (45)

Total comprehensive income for the year (69,280) (26,444)

Total comprehensive income for the year is attributable to:

Owners of Mako Gold Limited (69,280) (26,444)

Loss per share

Basic and diluted loss per share (cents per share) 18 (0.75) (26,398.89)

The above consolidated statement of profit or loss and other comprehensive income should be read in conjunction

with the accompanying notes

MAKO GOLD LIMITED

ANNUAL REPORT 2017

13

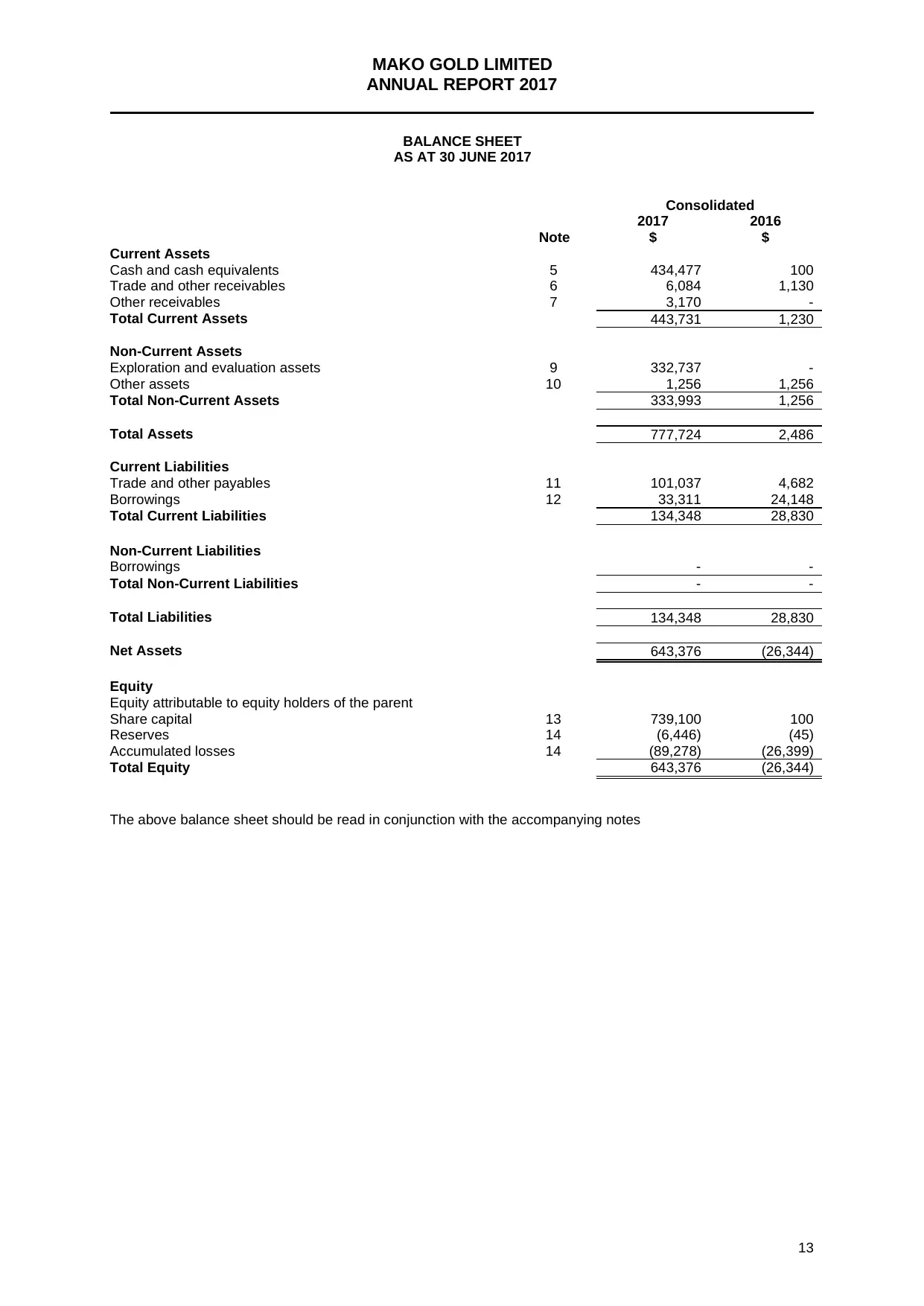

BALANCE SHEET

AS AT 30 JUNE 2017

Consolidated

2017 2016

Note $ $

Current Assets

Cash and cash equivalents 5 434,477 100

Trade and other receivables 6 6,084 1,130

Other receivables 7 3,170 -

Total Current Assets 443,731 1,230

Non-Current Assets

Exploration and evaluation assets 9 332,737 -

Other assets 10 1,256 1,256

Total Non-Current Assets 333,993 1,256

Total Assets 777,724 2,486

Current Liabilities

Trade and other payables 11 101,037 4,682

Borrowings 12 33,311 24,148

Total Current Liabilities 134,348 28,830

Non-Current Liabilities

Borrowings - -

Total Non-Current Liabilities - -

Total Liabilities 134,348 28,830

Net Assets 643,376 (26,344)

Equity

Equity attributable to equity holders of the parent

Share capital 13 739,100 100

Reserves 14 (6,446) (45)

Accumulated losses 14 (89,278) (26,399)

Total Equity 643,376 (26,344)

The above balance sheet should be read in conjunction with the accompanying notes

ANNUAL REPORT 2017

13

BALANCE SHEET

AS AT 30 JUNE 2017

Consolidated

2017 2016

Note $ $

Current Assets

Cash and cash equivalents 5 434,477 100

Trade and other receivables 6 6,084 1,130

Other receivables 7 3,170 -

Total Current Assets 443,731 1,230

Non-Current Assets

Exploration and evaluation assets 9 332,737 -

Other assets 10 1,256 1,256

Total Non-Current Assets 333,993 1,256

Total Assets 777,724 2,486

Current Liabilities

Trade and other payables 11 101,037 4,682

Borrowings 12 33,311 24,148

Total Current Liabilities 134,348 28,830

Non-Current Liabilities

Borrowings - -

Total Non-Current Liabilities - -

Total Liabilities 134,348 28,830

Net Assets 643,376 (26,344)

Equity

Equity attributable to equity holders of the parent

Share capital 13 739,100 100

Reserves 14 (6,446) (45)

Accumulated losses 14 (89,278) (26,399)

Total Equity 643,376 (26,344)

The above balance sheet should be read in conjunction with the accompanying notes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MAKO GOLD LIMITED

ANNUAL REPORT 2017

14

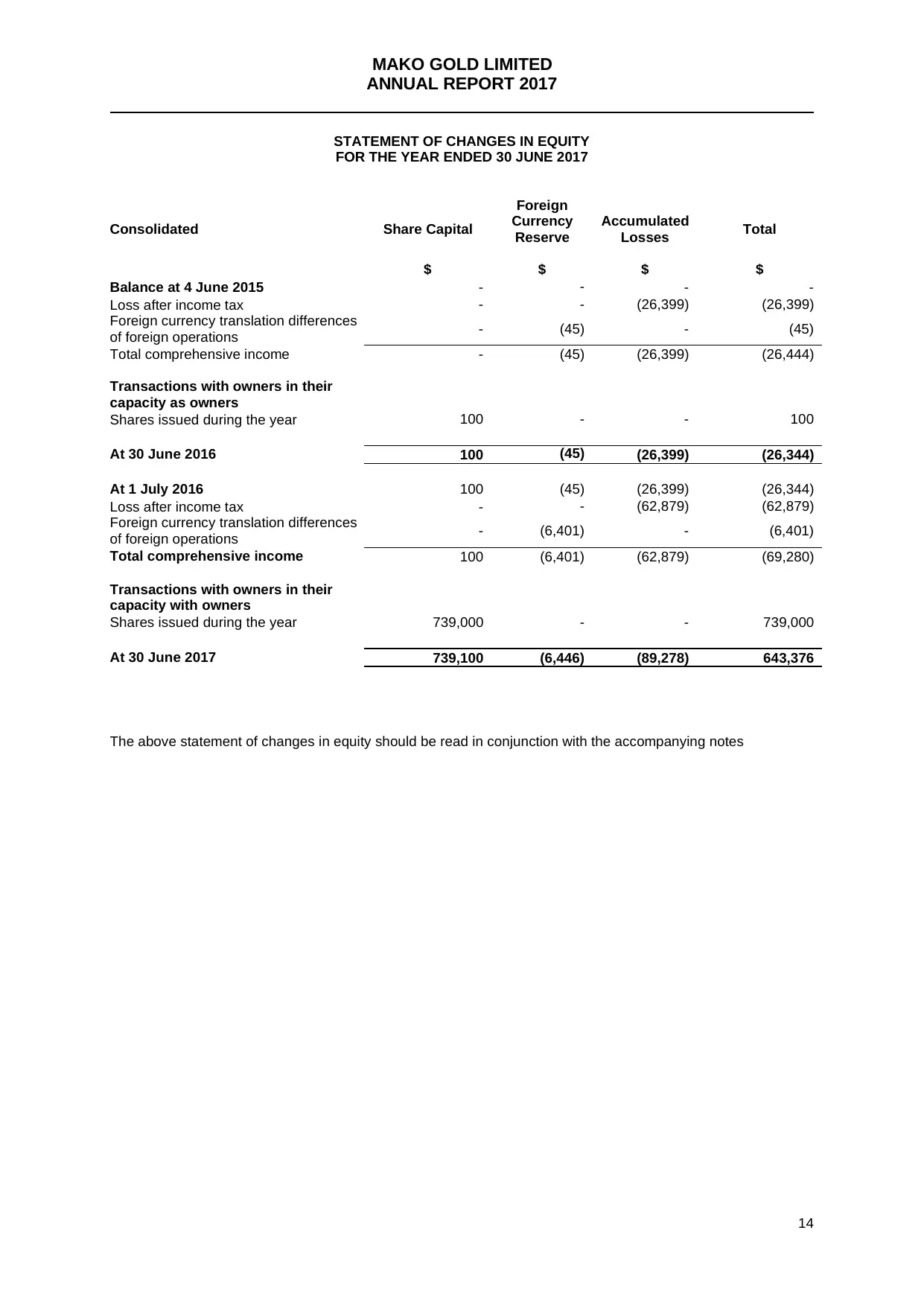

STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED 30 JUNE 2017

Consolidated Share Capital

Foreign

Currency

Reserve

Accumulated

Losses Total

$ $ $ $

Balance at 4 June 2015 - - - -

Loss after income tax - - (26,399) (26,399)

Foreign currency translation differences

of foreign operations - (45) - (45)

Total comprehensive income - (45) (26,399) (26,444)

Transactions with owners in their

capacity as owners

Shares issued during the year 100 - - 100

At 30 June 2016 100 (45) (26,399) (26,344)

At 1 July 2016 100 (45) (26,399) (26,344)

Loss after income tax - - (62,879) (62,879)

Foreign currency translation differences

of foreign operations - (6,401) - (6,401)

Total comprehensive income 100 (6,401) (62,879) (69,280)

Transactions with owners in their

capacity with owners

Shares issued during the year 739,000 - - 739,000

At 30 June 2017 739,100 (6,446) (89,278) 643,376

The above statement of changes in equity should be read in conjunction with the accompanying notes

ANNUAL REPORT 2017

14

STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED 30 JUNE 2017

Consolidated Share Capital

Foreign

Currency

Reserve

Accumulated

Losses Total

$ $ $ $

Balance at 4 June 2015 - - - -

Loss after income tax - - (26,399) (26,399)

Foreign currency translation differences

of foreign operations - (45) - (45)

Total comprehensive income - (45) (26,399) (26,444)

Transactions with owners in their

capacity as owners

Shares issued during the year 100 - - 100

At 30 June 2016 100 (45) (26,399) (26,344)

At 1 July 2016 100 (45) (26,399) (26,344)

Loss after income tax - - (62,879) (62,879)

Foreign currency translation differences

of foreign operations - (6,401) - (6,401)

Total comprehensive income 100 (6,401) (62,879) (69,280)

Transactions with owners in their

capacity with owners

Shares issued during the year 739,000 - - 739,000

At 30 June 2017 739,100 (6,446) (89,278) 643,376

The above statement of changes in equity should be read in conjunction with the accompanying notes

MAKO GOLD LIMITED

ANNUAL REPORT 2017

15

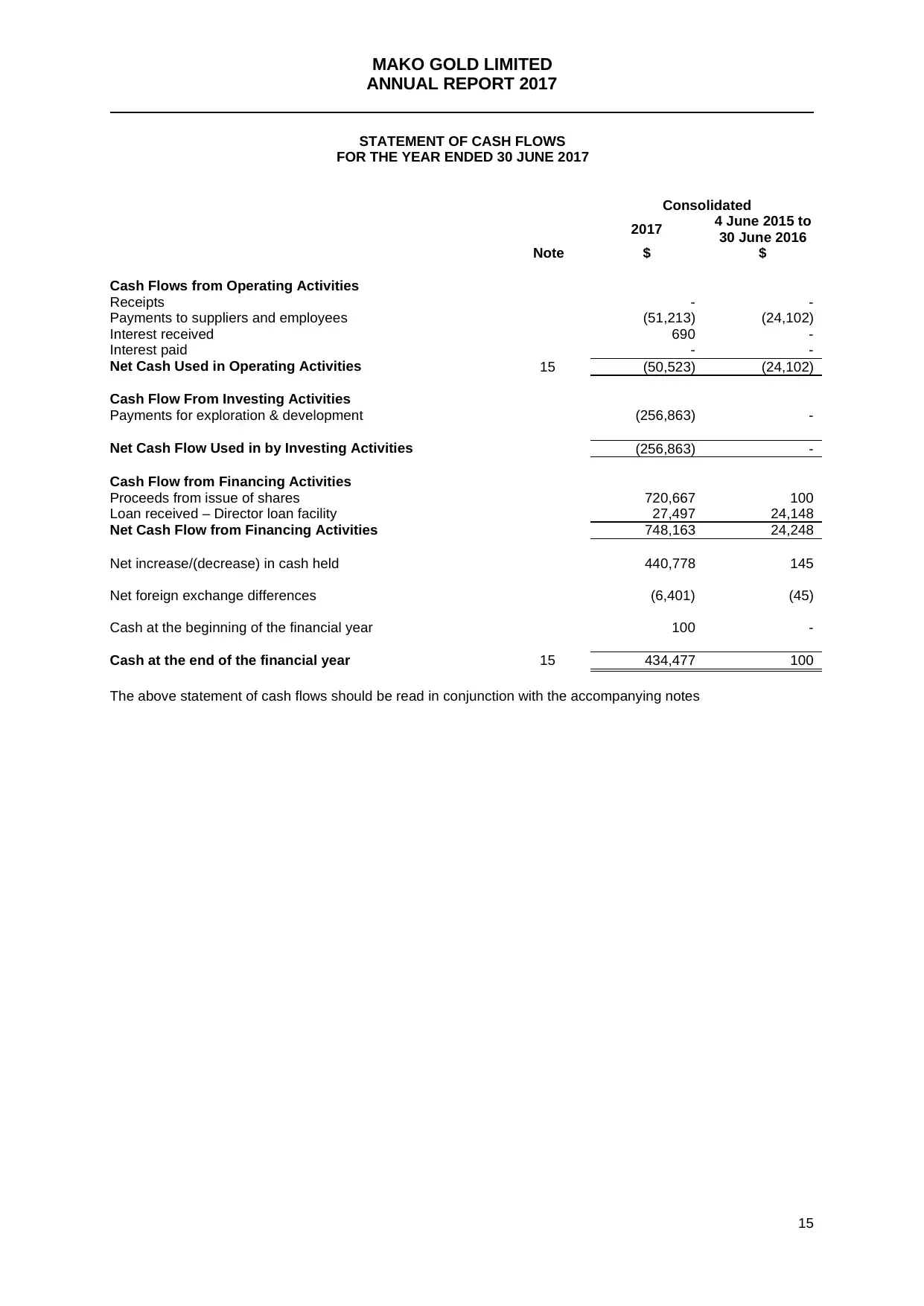

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED 30 JUNE 2017

Consolidated

2017 4 June 2015 to

30 June 2016

Note $ $

Cash Flows from Operating Activities

Receipts - -

Payments to suppliers and employees (51,213) (24,102)

Interest received 690 -

Interest paid - -

Net Cash Used in Operating Activities 15 (50,523) (24,102)

Cash Flow From Investing Activities

Payments for exploration & development (256,863) -

Net Cash Flow Used in by Investing Activities (256,863) -

Cash Flow from Financing Activities

Proceeds from issue of shares 720,667 100

Loan received – Director loan facility 27,497 24,148

Net Cash Flow from Financing Activities 748,163 24,248

Net increase/(decrease) in cash held 440,778 145

Net foreign exchange differences (6,401) (45)

Cash at the beginning of the financial year 100 -

Cash at the end of the financial year 15 434,477 100

The above statement of cash flows should be read in conjunction with the accompanying notes

ANNUAL REPORT 2017

15

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED 30 JUNE 2017

Consolidated

2017 4 June 2015 to

30 June 2016

Note $ $

Cash Flows from Operating Activities

Receipts - -

Payments to suppliers and employees (51,213) (24,102)

Interest received 690 -

Interest paid - -

Net Cash Used in Operating Activities 15 (50,523) (24,102)

Cash Flow From Investing Activities

Payments for exploration & development (256,863) -

Net Cash Flow Used in by Investing Activities (256,863) -

Cash Flow from Financing Activities

Proceeds from issue of shares 720,667 100

Loan received – Director loan facility 27,497 24,148

Net Cash Flow from Financing Activities 748,163 24,248

Net increase/(decrease) in cash held 440,778 145

Net foreign exchange differences (6,401) (45)

Cash at the beginning of the financial year 100 -

Cash at the end of the financial year 15 434,477 100

The above statement of cash flows should be read in conjunction with the accompanying notes

MAKO GOLD LIMITED - ANNUAL REPORT 2017

Notes to the Financial Statements

16

1. CORPORATE INFORMATION

Introduction

Mako Gold Limited is incorporated and domiciled in Australia.

Operations and principal activities

Principal activities comprise of acquisition of projects for mineral exploration and development.

Scope of financial statements

The consolidated financial statements consist of Mako Gold Limited and the entities it controlled at the end of, or

during, the year ended 30 June 2017.

Currency

The financial report is presented in Australia dollars and rounded to the nearest one dollar.

Authorisation of financial report

The financial report was authorised for issue on 10 November 2017.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of preparation

These general purpose financial statements have been prepared in accordance with Australian Accounting

Standards and Interpretations issued by the Australian Accounting Standards Board and the Corporations Act

2001. Mako Gold Limited is a for-profit entity for the purpose of preparing the financial statements.

The following is a summary of the material accounting policies adopted by the consolidated entity in the

preparation of the financial report. The accounting policies have been consistently applied, unless otherwise

stated.

Compliance with IFRS

The consolidated financial statements of Mako Gold Limited group also comply with International Financial

Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB).

Historical cost convention

These financial statements have been prepared under the historical cost convention.

Critical accounting estimates and judgements

The preparation of financial statements in conformity with Australian Accounting Standards requires the use of

certain critical accounting estimates. It also requires management to exercise its judgement in the process of

applying the Group’s accounting policies. The areas involving a higher degree of judgement or complexity, or

areas where assumptions and estimates are significant to the financial statements are disclosed below:

Key judgements – exploration & evaluation assets

The consolidated entity performs regular reviews on each area of interest to determine the appropriateness of

continuing to carry forward costs in relation to that area of interest. These reviews are based on detailed surveys

and analysis of drilling results performed to balance date.

The Directors have assessed that for the exploration and evaluation assets recognised at 30 June 2017, the facts

and circumstances do not suggest that the carrying amount of an asset may exceed its recoverable amount. In

considering this the Directors have had regard to the facts and circumstances that indicate a need for impairment

as noted in Accounting Standard AASB 6 “Exploration for and Evaluation of Mineral Resources”.

Going concern basis for accounting

The Group does not generate revenue to fund operations and ongoing investment in exploration activities. The

ability of the Group to continue as a going concern is dependent on its ability to raise additional equity.

Based on the success of the seed capital raising and on the anticipation of being able to complete a listing on

ASX in the 2017/18 financial year, the Directors have prepared the financial statements on a going concern basis,

which contemplates the continuity of normal business activities and the realisation of assets and discharge of

liabilities in the ordinary course of business. As at the date of this report the Directors are in the process of

seeking a further $500,000 in seed capital to ensure sufficient funds are in place to enable the IPO prospectus to

be completed and lodged in 2018.

Notes to the Financial Statements

16

1. CORPORATE INFORMATION

Introduction

Mako Gold Limited is incorporated and domiciled in Australia.

Operations and principal activities

Principal activities comprise of acquisition of projects for mineral exploration and development.

Scope of financial statements

The consolidated financial statements consist of Mako Gold Limited and the entities it controlled at the end of, or

during, the year ended 30 June 2017.

Currency

The financial report is presented in Australia dollars and rounded to the nearest one dollar.

Authorisation of financial report

The financial report was authorised for issue on 10 November 2017.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of preparation

These general purpose financial statements have been prepared in accordance with Australian Accounting

Standards and Interpretations issued by the Australian Accounting Standards Board and the Corporations Act

2001. Mako Gold Limited is a for-profit entity for the purpose of preparing the financial statements.

The following is a summary of the material accounting policies adopted by the consolidated entity in the

preparation of the financial report. The accounting policies have been consistently applied, unless otherwise

stated.

Compliance with IFRS

The consolidated financial statements of Mako Gold Limited group also comply with International Financial

Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB).

Historical cost convention

These financial statements have been prepared under the historical cost convention.

Critical accounting estimates and judgements

The preparation of financial statements in conformity with Australian Accounting Standards requires the use of

certain critical accounting estimates. It also requires management to exercise its judgement in the process of

applying the Group’s accounting policies. The areas involving a higher degree of judgement or complexity, or

areas where assumptions and estimates are significant to the financial statements are disclosed below:

Key judgements – exploration & evaluation assets

The consolidated entity performs regular reviews on each area of interest to determine the appropriateness of

continuing to carry forward costs in relation to that area of interest. These reviews are based on detailed surveys

and analysis of drilling results performed to balance date.

The Directors have assessed that for the exploration and evaluation assets recognised at 30 June 2017, the facts

and circumstances do not suggest that the carrying amount of an asset may exceed its recoverable amount. In

considering this the Directors have had regard to the facts and circumstances that indicate a need for impairment

as noted in Accounting Standard AASB 6 “Exploration for and Evaluation of Mineral Resources”.

Going concern basis for accounting

The Group does not generate revenue to fund operations and ongoing investment in exploration activities. The

ability of the Group to continue as a going concern is dependent on its ability to raise additional equity.

Based on the success of the seed capital raising and on the anticipation of being able to complete a listing on

ASX in the 2017/18 financial year, the Directors have prepared the financial statements on a going concern basis,

which contemplates the continuity of normal business activities and the realisation of assets and discharge of

liabilities in the ordinary course of business. As at the date of this report the Directors are in the process of

seeking a further $500,000 in seed capital to ensure sufficient funds are in place to enable the IPO prospectus to

be completed and lodged in 2018.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MAKO GOLD LIMITED - ANNUAL REPORT 2017

Notes to the Financial Statements

17

The Directors are confident of securing funds as and when necessary to meet the Consolidated Entity’s

obligations as and when they fall due.

These conditions indicate the existence of a material uncertainty that may cast significant doubt about the

Consolidated Entity’s ability to continue as a going concern and therefore, the Consolidated Entity may be unable

to realise its assets and discharge its liabilities in the normal course of business.

No adjustment have been made to the financial statements relating to the recoverability and classification of

recorded asset amounts or to the amounts and classification of liabilities that might be necessary should the

Consolidated Entity not be able to continue as a going concern.

Should the consolidated entity be unable to continue as a going concern, it may be required to realise its assets

and extinguish its liabilities other than in the ordinary course of business, and at amounts that differ from those

stated in the financial statements.

This financial report does not include any adjustments relating to the recoverability and classification of recorded

asset amounts or the amounts or classification of liabilities and appropriate disclosures that may be necessary

should the consolidated entity be unable to continue as a going concern.

Principles of Consolidation

Subsidiaries

Subsidiaries are all entities (including structured entities) over which the consolidated entity has control. The

consolidated entity controls an entity when the consolidated entity is exposed to, or has rights to, variable returns

from its involvement with the entity and has the ability to affect those returns through its power to direct the

activities of the entity. Subsidiaries are fully consolidated from the date on which control is transferred to the

consolidated entity. They are deconsolidated from the date that control ceases.

The acquisition method of accounting is used to account for business combinations by the consolidated entity.

Intercompany transactions, balances and unrealised gains on transactions between consolidated entity

companies are eliminated. Unrealised losses are also eliminated unless the transaction provides evidence of an

impairment of the transferred asset. Accounting policies of subsidiaries have been changed where necessary to

ensure consistency with the policies adopted by the consolidated entity.

Non-controlling interests in the results and equity of subsidiaries are shown separately in the consolidated

statement of comprehensive income, statement of changes in equity and balance sheet respectively.

Joint Ventures

The consolidated entity’s share of the assets, liabilities, revenue and expenses of joint ventures are included in

the appropriate items of the consolidated financial statements.

Foreign Currencies

Items included in the financial statements of each of the Group entities are measured using the currency of the

primary economic environment in which the entity operates (‘the functional currency’). The consolidated financial

statements are presented in Australian dollars, which is the Company’s functional and presentation currency.

Foreign currency transactions are translated into the functional currency using the exchange rates prevailing at

the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of such

transactions and from the translation at year end exchange rates of monetary assets and liabilities denominated

in foreign currencies are recognised in profit or loss.

Exploration and Evaluation Assets

Costs carried forward

Exploration, evaluation and development expenditure incurred is accumulated in respect of each identifiable area

of interest. Such expenditures comprise net direct costs and an appropriate portion of related overhead

expenditure but does not include overheads or administration expenditure not having a specific nexus with a

particular area of interest. These costs are only carried forward to the extent that they are expected to be

recouped through the successful development of the area or where activities in the area have not yet reached a

stage which permits reasonable assessment of the existence of economically recoverable reserves and active or

significant operations in relation to the area are continuing.

Notes to the Financial Statements

17

The Directors are confident of securing funds as and when necessary to meet the Consolidated Entity’s

obligations as and when they fall due.

These conditions indicate the existence of a material uncertainty that may cast significant doubt about the

Consolidated Entity’s ability to continue as a going concern and therefore, the Consolidated Entity may be unable

to realise its assets and discharge its liabilities in the normal course of business.

No adjustment have been made to the financial statements relating to the recoverability and classification of

recorded asset amounts or to the amounts and classification of liabilities that might be necessary should the

Consolidated Entity not be able to continue as a going concern.

Should the consolidated entity be unable to continue as a going concern, it may be required to realise its assets

and extinguish its liabilities other than in the ordinary course of business, and at amounts that differ from those

stated in the financial statements.

This financial report does not include any adjustments relating to the recoverability and classification of recorded

asset amounts or the amounts or classification of liabilities and appropriate disclosures that may be necessary

should the consolidated entity be unable to continue as a going concern.

Principles of Consolidation

Subsidiaries

Subsidiaries are all entities (including structured entities) over which the consolidated entity has control. The

consolidated entity controls an entity when the consolidated entity is exposed to, or has rights to, variable returns

from its involvement with the entity and has the ability to affect those returns through its power to direct the

activities of the entity. Subsidiaries are fully consolidated from the date on which control is transferred to the

consolidated entity. They are deconsolidated from the date that control ceases.

The acquisition method of accounting is used to account for business combinations by the consolidated entity.

Intercompany transactions, balances and unrealised gains on transactions between consolidated entity

companies are eliminated. Unrealised losses are also eliminated unless the transaction provides evidence of an

impairment of the transferred asset. Accounting policies of subsidiaries have been changed where necessary to

ensure consistency with the policies adopted by the consolidated entity.

Non-controlling interests in the results and equity of subsidiaries are shown separately in the consolidated

statement of comprehensive income, statement of changes in equity and balance sheet respectively.

Joint Ventures

The consolidated entity’s share of the assets, liabilities, revenue and expenses of joint ventures are included in

the appropriate items of the consolidated financial statements.

Foreign Currencies

Items included in the financial statements of each of the Group entities are measured using the currency of the

primary economic environment in which the entity operates (‘the functional currency’). The consolidated financial

statements are presented in Australian dollars, which is the Company’s functional and presentation currency.

Foreign currency transactions are translated into the functional currency using the exchange rates prevailing at

the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of such

transactions and from the translation at year end exchange rates of monetary assets and liabilities denominated

in foreign currencies are recognised in profit or loss.

Exploration and Evaluation Assets

Costs carried forward

Exploration, evaluation and development expenditure incurred is accumulated in respect of each identifiable area

of interest. Such expenditures comprise net direct costs and an appropriate portion of related overhead

expenditure but does not include overheads or administration expenditure not having a specific nexus with a

particular area of interest. These costs are only carried forward to the extent that they are expected to be

recouped through the successful development of the area or where activities in the area have not yet reached a

stage which permits reasonable assessment of the existence of economically recoverable reserves and active or

significant operations in relation to the area are continuing.

MAKO GOLD LIMITED - ANNUAL REPORT 2017

Notes to the Financial Statements

18

Restoration costs

Restoration costs that are expected to be incurred are provided for as part of the cost of the exploration,

evaluation, development, construction and production phases that give rise to the need for restoration.

Accordingly, these costs are recognised gradually over the life of the facility as these phases occur. The costs

include obligations relating to reclamation, waste site closure, plant closure and other costs associated with the

restoration of the site. In determining the restoration obligations, the entity has assumed no significant changes

will occur in the relevant Federal and State legislation in relation to restoration of such mines in the future.

Both for close down and restoration and for environmental clean-up costs, provision is made in the accounting

period when the related disturbance occurs, based on the net present value of estimated future costs.

For close down and restoration costs, which include the dismantling and demolition of infrastructure, removal of

residual materials and remediation of disturbed areas, movements in provision other than the amortisation of the

discount, such as those resulting from changes in the cost estimates, lives of operations or discount rates, are

capitalised into the carrying amount of development and amortised against future production.

Revenue Recognition

Amounts disclosed as revenue are net of returns, trade allowances and duties and taxes paid.

Interest revenue is accrued on a time basis, by reference to the principle outstanding and at the effective interest

rate applicable, which is the rate that exactly discounts estimate future cash receipts through the expected life of

the financial asset to that asset’s net carrying value.

Taxes

Income taxes

The income tax expense or benefit for the period is the tax payable on the current periods taxable income based

on the notional income tax rate adjusted by changes in deferred tax assets and liabilities attributable to temporary

differences between the tax bases of assets and liabilities and their carrying amounts in the financial statements,

and to unused tax losses.

Deferred tax assets and liabilities are recognised for temporary differences at the tax rates expected to apply

when the assets are recovered or liabilities are settled, based on those tax rates which are enacted or

substantively enacted for each jurisdiction. The relevant tax rates are applied to the cumulative amounts of

deductible and taxable temporary differences to measure the deferred tax asset or liability. An exception is made

for certain temporary differences arising from the initial recognition of an asset or a liability. No deferred tax asset

or liability is recognised in relation to these temporary differences if they arose in a transaction, other than a

business combination, that at the time of the transaction did not affect either accounting profit or taxable profit or

loss.

Deferred tax assets are recognised for deductible temporary differences and unused tax losses only if it is

probable that future taxable amounts will be available to utilise those temporary differences and losses. Deferred

tax liabilities and assets are not recognised for temporary differences between the carrying amount and tax bases

of investments in controlled entities where the parent entity is able to control the timing of the reversal of the

temporary differences and it is probable that the differences will not reverse in the foreseeable future.

Current and deferred tax balances attributable to amounts recognised directly in equity are also recognised

directly in equity.

Goods and Services Tax (GST)

Revenues, expenses, and assets are recognised net of the amount of GST, except where the GST incurred on a

purchase of goods or services is not recoverable from the taxation authority, in which case the GST is recognised

as part of the cost of acquisition of the assets or as part of the expense item as applicable, and except for

receivables and payables which are stated inclusive of GST.

Cash flows are included in the Statement of Cash Flows on a gross basis and the GST component of cash flows

arising from investing and financing activities which is recoverable from or payable to the taxation authority are

classified as operating cash flows. The net amount of GST recoverable from or payable to the taxation authority is

included as part of receivables or payables in the balance sheet. Commitments and contingencies are disclosed

net of the amount of GST recoverable from or payable to the taxation authority.

Notes to the Financial Statements

18

Restoration costs

Restoration costs that are expected to be incurred are provided for as part of the cost of the exploration,

evaluation, development, construction and production phases that give rise to the need for restoration.

Accordingly, these costs are recognised gradually over the life of the facility as these phases occur. The costs

include obligations relating to reclamation, waste site closure, plant closure and other costs associated with the

restoration of the site. In determining the restoration obligations, the entity has assumed no significant changes

will occur in the relevant Federal and State legislation in relation to restoration of such mines in the future.

Both for close down and restoration and for environmental clean-up costs, provision is made in the accounting

period when the related disturbance occurs, based on the net present value of estimated future costs.

For close down and restoration costs, which include the dismantling and demolition of infrastructure, removal of

residual materials and remediation of disturbed areas, movements in provision other than the amortisation of the

discount, such as those resulting from changes in the cost estimates, lives of operations or discount rates, are

capitalised into the carrying amount of development and amortised against future production.

Revenue Recognition

Amounts disclosed as revenue are net of returns, trade allowances and duties and taxes paid.

Interest revenue is accrued on a time basis, by reference to the principle outstanding and at the effective interest

rate applicable, which is the rate that exactly discounts estimate future cash receipts through the expected life of

the financial asset to that asset’s net carrying value.

Taxes

Income taxes

The income tax expense or benefit for the period is the tax payable on the current periods taxable income based

on the notional income tax rate adjusted by changes in deferred tax assets and liabilities attributable to temporary

differences between the tax bases of assets and liabilities and their carrying amounts in the financial statements,

and to unused tax losses.

Deferred tax assets and liabilities are recognised for temporary differences at the tax rates expected to apply

when the assets are recovered or liabilities are settled, based on those tax rates which are enacted or

substantively enacted for each jurisdiction. The relevant tax rates are applied to the cumulative amounts of

deductible and taxable temporary differences to measure the deferred tax asset or liability. An exception is made

for certain temporary differences arising from the initial recognition of an asset or a liability. No deferred tax asset

or liability is recognised in relation to these temporary differences if they arose in a transaction, other than a

business combination, that at the time of the transaction did not affect either accounting profit or taxable profit or

loss.

Deferred tax assets are recognised for deductible temporary differences and unused tax losses only if it is

probable that future taxable amounts will be available to utilise those temporary differences and losses. Deferred

tax liabilities and assets are not recognised for temporary differences between the carrying amount and tax bases

of investments in controlled entities where the parent entity is able to control the timing of the reversal of the

temporary differences and it is probable that the differences will not reverse in the foreseeable future.

Current and deferred tax balances attributable to amounts recognised directly in equity are also recognised

directly in equity.

Goods and Services Tax (GST)

Revenues, expenses, and assets are recognised net of the amount of GST, except where the GST incurred on a

purchase of goods or services is not recoverable from the taxation authority, in which case the GST is recognised

as part of the cost of acquisition of the assets or as part of the expense item as applicable, and except for

receivables and payables which are stated inclusive of GST.

Cash flows are included in the Statement of Cash Flows on a gross basis and the GST component of cash flows

arising from investing and financing activities which is recoverable from or payable to the taxation authority are

classified as operating cash flows. The net amount of GST recoverable from or payable to the taxation authority is

included as part of receivables or payables in the balance sheet. Commitments and contingencies are disclosed

net of the amount of GST recoverable from or payable to the taxation authority.

MAKO GOLD LIMITED - ANNUAL REPORT 2017

Notes to the Financial Statements

19

Cash and Cash Equivalents

For purposes of the Statement of Cash Flows, cash and cash equivalents includes cash on hand, deposits at call

with financial institutions and other highly liquid investments with short periods to maturity which are readily

convertible to cash on hand and are subject to an insignificant risk of changes in value, net of outstanding bank

overdrafts.

Receivables

All trade receivables are recognised at the amounts receivable as they are due for settlement no more than 30

days from the date of recognition.

Collectability of trade receivables is reviewed on an ongoing basis. Debts which are known to be uncollectible are

written off. A provision of doubtful receivables is established when there is objective evidence that the

consolidated entity will not be able to collect all amounts due according to the original terms of receivables. The

amount of the provision is the difference between the assets carrying amount and the present value of the

estimated future cash flows, discounted at the effective interest rate. The amount of the provision is recognised in

profit or loss.

The carrying amounts of the loans are reviewed at each balance date to determine whether there is any indication

of impairment. If any such indication exists, the loan is impaired to its recoverable amount. The recoverable

amount of the receivables carried at amortised cost is calculated as the present value of estimated future cash

flows, discounted at the original effective interest rate.

Investments and Other Financial Assets

The consolidated entity classifies its investments in the following categories: financial assets at fair value through

profit or loss, loans and receivables, held-to-maturity investments, and available-for-sale financial assets. The

classification depends on the purpose for which the investments were acquired. Management determines the

classification of its investments at initial recognition and, in the case of assets classified as held-to-maturity, re-

evaluates this designation at each reporting date.

(i) Financial Assets at fair value through profit or loss

Financial assets at fair value through profit or loss are financial assets held for trading which are acquired

principally for the purpose of selling in the short term with the intention of making a profit. Derivatives are also

categorised as held for trading unless they are designated as hedges.

(ii) Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted

in an active market. They arise when the consolidated entity provides money, goods or services directly to a

debtor with no intention of selling the receivable. They are included in current assets, except for those with

maturities greater than 12 months after the balance sheet date which are classified as non-current assets. Such

assets are carried at amortised cost using the effective rate interest method. Gains and losses are recognised in

profit and loss when the loans and receivables are derecognised or impaired, as well as through the amortisation

process.

(iii) Held-to-maturity investments

Held-to-maturity investments are non-derivative financial assets with fixed or determinable payments and fixed