Manage Budget and Financial Plans

VerifiedAdded on 2023/04/21

|24

|4301

|200

AI Summary

This document provides information on managing budget and financial plans. It covers topics such as double entry bookkeeping, cash accounting, accrual basis of accounting, depreciation, GST, and more. The document includes assignments, essays, and dissertations related to this subject. It is relevant for students studying finance and accounting courses in various colleges and universities.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGE BUDGET AND FINANCIAL PLANS

Manage budget and financial plans

Name of the student

Name of the university

Student ID

Author note

Manage budget and financial plans

Name of the student

Name of the university

Student ID

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MANAGE BUDGET AND FINANCIAL PLANS

Table of Contents

Assessment task 1......................................................................................................................2

Assessment task 2 – Budget planning project............................................................................9

Assessment task 3 – Monitor and control finances project......................................................13

Assessment task 4: Profit and loss review project...................................................................15

Assessment 5: Aged Debtor Report.........................................................................................18

Reference..................................................................................................................................22

Table of Contents

Assessment task 1......................................................................................................................2

Assessment task 2 – Budget planning project............................................................................9

Assessment task 3 – Monitor and control finances project......................................................13

Assessment task 4: Profit and loss review project...................................................................15

Assessment 5: Aged Debtor Report.........................................................................................18

Reference..................................................................................................................................22

2MANAGE BUDGET AND FINANCIAL PLANS

Assessment task 1

Answer 1

Basis principle of the double entry bookkeeping system is there shall always be 2

entries for each transaction. One of the entries is known as credit entry and another entry is

known as the debit entry (Dudin et al., 2015).

Answer 2

The principle of cash accounting is that the entities shall record the expenses when the

expenses are actually paid rather than recording it when it is incurred.

Advantage – while paying tax under cash accounting basis, it is ensured that the taxes are not

paid for the monies that has not been received yet. It improves the cash flows and ensures that

the funds are available for the tax expenses.

Disadvantage – as it is very simple method it does not allow tracking of the accrual dates of

purchase and sales. In addition, it does not provide matching the transaction with specific

inventory items (Dzhandzhugazova et al., 2015).

Answer 3

Under accrual basis of accounting it requires recording of the accounting transaction

under the period in which they are occurred actually and not under the period to which the

cash flow associated to it takes place.

Advantage – it produces more faithful, more accurate financial statement which is turn

constitutes the better representation of the actual circumstances as compared to the cash basis

of accounting.

Assessment task 1

Answer 1

Basis principle of the double entry bookkeeping system is there shall always be 2

entries for each transaction. One of the entries is known as credit entry and another entry is

known as the debit entry (Dudin et al., 2015).

Answer 2

The principle of cash accounting is that the entities shall record the expenses when the

expenses are actually paid rather than recording it when it is incurred.

Advantage – while paying tax under cash accounting basis, it is ensured that the taxes are not

paid for the monies that has not been received yet. It improves the cash flows and ensures that

the funds are available for the tax expenses.

Disadvantage – as it is very simple method it does not allow tracking of the accrual dates of

purchase and sales. In addition, it does not provide matching the transaction with specific

inventory items (Dzhandzhugazova et al., 2015).

Answer 3

Under accrual basis of accounting it requires recording of the accounting transaction

under the period in which they are occurred actually and not under the period to which the

cash flow associated to it takes place.

Advantage – it produces more faithful, more accurate financial statement which is turn

constitutes the better representation of the actual circumstances as compared to the cash basis

of accounting.

3MANAGE BUDGET AND FINANCIAL PLANS

Disadvantage – it requires transactions to be recorded at the time when it takes place.

However, as the invoices do not match with the actual event, this method requires estimation

from the accountant’s end (Kumar, 2017).

Answer 4

Matching principle –depreciation reduces the income of that accounting period though the

expenses do not require any credit or cash payment. Reason behind this expense is complying

with matching principle that is required by the accrual accounting.

Calculation of depreciation expenses – expenses for depreciation can be calculated through

different methods based on the type of the assets, estimated useful life of the asset, expected

business use of the asset and its residual value. Various methods are straight line method,

sum of year’s digit method, units of production method and double declining balance method

(Sofat & Hiro, 2015).

Answer 5

A. Tax periods – tax invoice – purpose of this part is prescribing additional information

required to be included under tax invoices issued for purposes of GST.

B. Financial supplies – this part provides meaning of the term Financial supply. The

financial supplies are the input that is taxed under GST Act.

C. Reduced input tax credits – this part sets out the list for reduced credit acquisitions

that generates an entitlement for reduced input tax credits (Ato.gov.au, 2019).

Answer 6

Goods and services tax – GST is the broad based tax at the rate of 10% that is

imposed on most of the services, goods and different other items sold over Australia.

Based on the turnover, the business required to be registered for GST

Disadvantage – it requires transactions to be recorded at the time when it takes place.

However, as the invoices do not match with the actual event, this method requires estimation

from the accountant’s end (Kumar, 2017).

Answer 4

Matching principle –depreciation reduces the income of that accounting period though the

expenses do not require any credit or cash payment. Reason behind this expense is complying

with matching principle that is required by the accrual accounting.

Calculation of depreciation expenses – expenses for depreciation can be calculated through

different methods based on the type of the assets, estimated useful life of the asset, expected

business use of the asset and its residual value. Various methods are straight line method,

sum of year’s digit method, units of production method and double declining balance method

(Sofat & Hiro, 2015).

Answer 5

A. Tax periods – tax invoice – purpose of this part is prescribing additional information

required to be included under tax invoices issued for purposes of GST.

B. Financial supplies – this part provides meaning of the term Financial supply. The

financial supplies are the input that is taxed under GST Act.

C. Reduced input tax credits – this part sets out the list for reduced credit acquisitions

that generates an entitlement for reduced input tax credits (Ato.gov.au, 2019).

Answer 6

Goods and services tax – GST is the broad based tax at the rate of 10% that is

imposed on most of the services, goods and different other items sold over Australia.

Based on the turnover, the business required to be registered for GST

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MANAGE BUDGET AND FINANCIAL PLANS

Pay as you go – PAYG system allows paying expected tax liability through

instalments. ATO will notify the PAYG obligations

Fringe benefit tax – if certain benefits are provided to the employees or the people

related to employees by the employer the employer will be liable to FBT

Superannuation guarantee obligation – as the employer either minimum level for

superannuation can be set for each of the eligible employees or charge can be paud to

the ATO (Ato.gov.au, 2019).

Answer 7

Some heath and care and medical services

Most basis foods

Precious metals

Farmland (Ato.gov.au, 2019).

Answer 8

If the business is registered under GST, Business activity statement (BAS) shall be

lodged that will help to report and pay GST. If the business is registered with ABN

(Australian business number) and GST, BAS will be automatically sent when it is required to

be lodged

GST reporting shall be one of the following –

Monthly – if the GST turnover amounted to $ 20 million or more

Quarterly – if GST turnover is lower than $ 20 million and no obligation is there to

report monthly

Annually – if voluntarily registered for the GST.

Pay as you go – PAYG system allows paying expected tax liability through

instalments. ATO will notify the PAYG obligations

Fringe benefit tax – if certain benefits are provided to the employees or the people

related to employees by the employer the employer will be liable to FBT

Superannuation guarantee obligation – as the employer either minimum level for

superannuation can be set for each of the eligible employees or charge can be paud to

the ATO (Ato.gov.au, 2019).

Answer 7

Some heath and care and medical services

Most basis foods

Precious metals

Farmland (Ato.gov.au, 2019).

Answer 8

If the business is registered under GST, Business activity statement (BAS) shall be

lodged that will help to report and pay GST. If the business is registered with ABN

(Australian business number) and GST, BAS will be automatically sent when it is required to

be lodged

GST reporting shall be one of the following –

Monthly – if the GST turnover amounted to $ 20 million or more

Quarterly – if GST turnover is lower than $ 20 million and no obligation is there to

report monthly

Annually – if voluntarily registered for the GST.

5MANAGE BUDGET AND FINANCIAL PLANS

Based on the circumstances, cycle can be changed for reporting and paying GST (Ato.gov.au,

2019).

Answer 9

Tax equivalent of top marginal rate in addition to medicare shall be withheld from the

payment to the supplier unless the invoice is provided that is quoted with ABN. From 1st July

2017 the rate is 47% (Ato.gov.au, 2019).

Answer 10

Non-profit organization shall be registered for GST if its turnover exceeds $ 150,000

(Ato.gov.au, 2019).

Answer 11

The document is intended to be the tax invoice

Identity of the seller

ABN number of the seller

Date of invoice issue

Brief description of items sold with the quantity and price

GST amount payable, if any

Extent to which the sales included in invoice is taxable sale (Ato.gov.au, 2019).

Answer 12

Profit and loss statement – it represents the income and expenses of the company and

profit or loss generated from incomes after charging the expenses

Balance sheet – it represents the details regarding assets, liabilities and equities of the

company.

Based on the circumstances, cycle can be changed for reporting and paying GST (Ato.gov.au,

2019).

Answer 9

Tax equivalent of top marginal rate in addition to medicare shall be withheld from the

payment to the supplier unless the invoice is provided that is quoted with ABN. From 1st July

2017 the rate is 47% (Ato.gov.au, 2019).

Answer 10

Non-profit organization shall be registered for GST if its turnover exceeds $ 150,000

(Ato.gov.au, 2019).

Answer 11

The document is intended to be the tax invoice

Identity of the seller

ABN number of the seller

Date of invoice issue

Brief description of items sold with the quantity and price

GST amount payable, if any

Extent to which the sales included in invoice is taxable sale (Ato.gov.au, 2019).

Answer 12

Profit and loss statement – it represents the income and expenses of the company and

profit or loss generated from incomes after charging the expenses

Balance sheet – it represents the details regarding assets, liabilities and equities of the

company.

6MANAGE BUDGET AND FINANCIAL PLANS

Cash flow statement – it records the cash received or expensed by the company from

or towards operating activities, investing activities and financing activities

(McKinney, 2015).

Answer 13

All the ASX listed companies are required to get their financial reports audited.

Answer 14

Purpose of financial audit is to deliver the users of financial statements with the

opinion issued by auditor on whether financial statement of the entity are presented in all

material aspects fairly and as per the applicable framework for financial reporting.

Purpose of the auditor’s report is documenting the reasonable assurances that the

financial statements of the entity are free from the error (Nosheen, Sadiq & Rafay, 2016).

Answer 15

Companies develop the budget for monitoring the progress towards the goals. It

majorly includes 3 aspects – forecast of the income, forecast of expenses and tool for the

decision making (Morgan et al., 2017).

Answer 16

Setting the objectives

Determining the available resources

Estimating the future needs

Matching the future needs to the available resources

Obtaining the final approval

Distributing the approved funds

Cash flow statement – it records the cash received or expensed by the company from

or towards operating activities, investing activities and financing activities

(McKinney, 2015).

Answer 13

All the ASX listed companies are required to get their financial reports audited.

Answer 14

Purpose of financial audit is to deliver the users of financial statements with the

opinion issued by auditor on whether financial statement of the entity are presented in all

material aspects fairly and as per the applicable framework for financial reporting.

Purpose of the auditor’s report is documenting the reasonable assurances that the

financial statements of the entity are free from the error (Nosheen, Sadiq & Rafay, 2016).

Answer 15

Companies develop the budget for monitoring the progress towards the goals. It

majorly includes 3 aspects – forecast of the income, forecast of expenses and tool for the

decision making (Morgan et al., 2017).

Answer 16

Setting the objectives

Determining the available resources

Estimating the future needs

Matching the future needs to the available resources

Obtaining the final approval

Distributing the approved funds

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGE BUDGET AND FINANCIAL PLANS

Evaluating and monitoring (Manasan, 2017).

Answer 17

Performing good forecast – good forecast is as simple as the paper and pencil for

small companies

Evaluate the terms – checking that the suppliers terms and customer terms are

balanced properly

Enforcing the payment discipline – shortening the receivable period

Segmenting the customers, inventories and supplies – while inventory is analysed,

sales volatility must be observed

Making it a priority all over the company – assuring that all the employees

understands the priority

Answer 18

Using the spreadsheet, changes if any made to the budget can be updated instantly for

the entire budget with the total calculation. It can be used for tracking the variance with

actual data and presenting it to the management.

2 key features of spreadsheet while preparing the budget are as follows –

Pivot table – it summarizes large amounts of the excel data from the formatted

database

Sorting and filtering – for making it easier to find the required data, the data can be

picked or reordered as per the requirement.

Answer 19

Financial statements shall present the information simply

Evaluating and monitoring (Manasan, 2017).

Answer 17

Performing good forecast – good forecast is as simple as the paper and pencil for

small companies

Evaluate the terms – checking that the suppliers terms and customer terms are

balanced properly

Enforcing the payment discipline – shortening the receivable period

Segmenting the customers, inventories and supplies – while inventory is analysed,

sales volatility must be observed

Making it a priority all over the company – assuring that all the employees

understands the priority

Answer 18

Using the spreadsheet, changes if any made to the budget can be updated instantly for

the entire budget with the total calculation. It can be used for tracking the variance with

actual data and presenting it to the management.

2 key features of spreadsheet while preparing the budget are as follows –

Pivot table – it summarizes large amounts of the excel data from the formatted

database

Sorting and filtering – for making it easier to find the required data, the data can be

picked or reordered as per the requirement.

Answer 19

Financial statements shall present the information simply

8MANAGE BUDGET AND FINANCIAL PLANS

Shall be cautious regarding the adding additional accounts to chart of accounts

Considering key information required for knowing how well the business is going on (Muli &

Rotich, 2016).

Answer 20

Purpose of the profit and loss account is representing whether the business has made

the profit or loss during the financial year. Key features of profit and loss account are as

follows –

Profit and loss statement is prepared in each year and from it the entity gets the idea

regarding whether the company made the profit or loss

Cash inflows through sales, interest received and dividend received are recorded in

the revenue section of the statement (Morden, 2016).

Shall be cautious regarding the adding additional accounts to chart of accounts

Considering key information required for knowing how well the business is going on (Muli &

Rotich, 2016).

Answer 20

Purpose of the profit and loss account is representing whether the business has made

the profit or loss during the financial year. Key features of profit and loss account are as

follows –

Profit and loss statement is prepared in each year and from it the entity gets the idea

regarding whether the company made the profit or loss

Cash inflows through sales, interest received and dividend received are recorded in

the revenue section of the statement (Morden, 2016).

9MANAGE BUDGET AND FINANCIAL PLANS

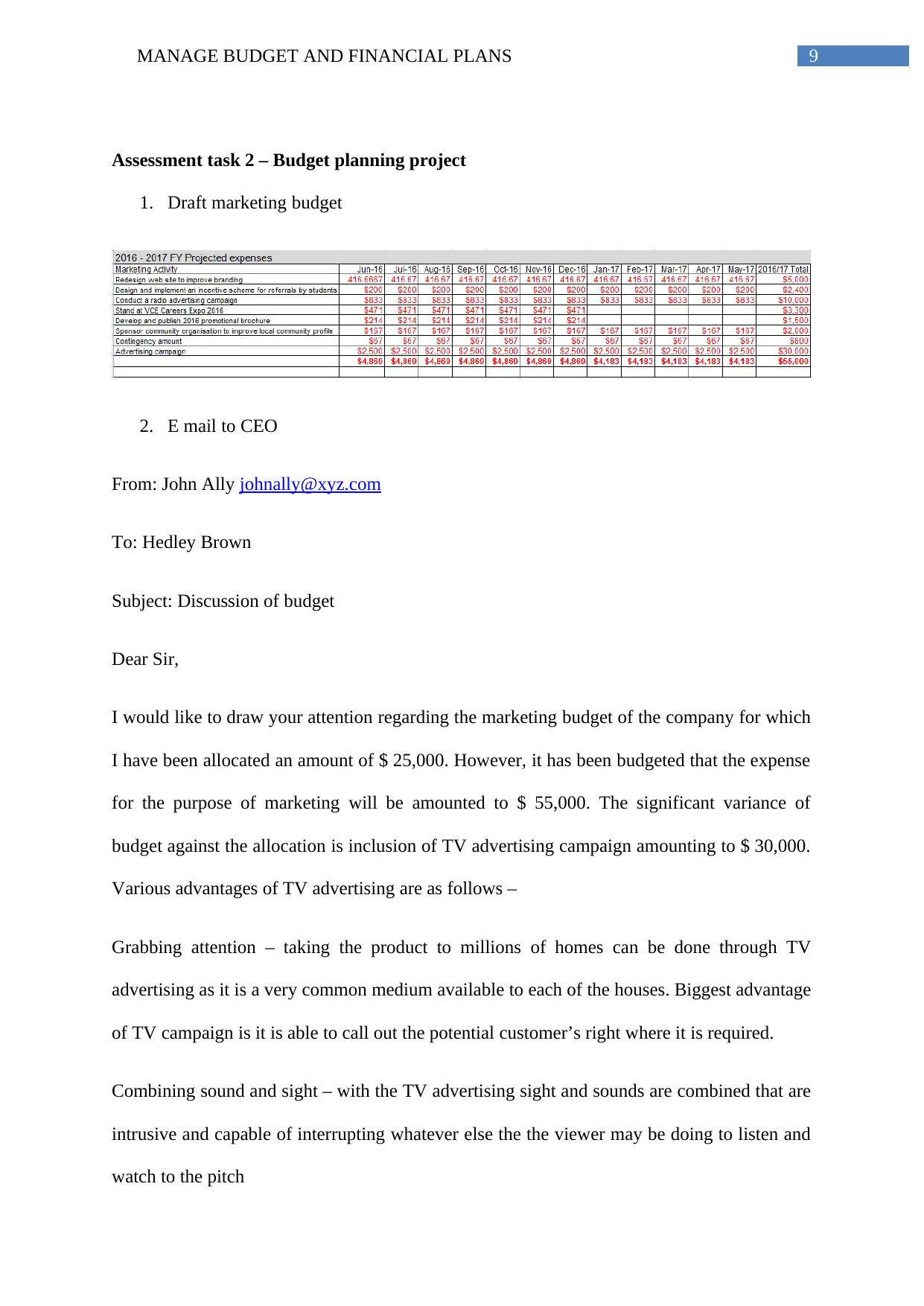

Assessment task 2 – Budget planning project

1. Draft marketing budget

2. E mail to CEO

From: John Ally johnally@xyz.com

To: Hedley Brown

Subject: Discussion of budget

Dear Sir,

I would like to draw your attention regarding the marketing budget of the company for which

I have been allocated an amount of $ 25,000. However, it has been budgeted that the expense

for the purpose of marketing will be amounted to $ 55,000. The significant variance of

budget against the allocation is inclusion of TV advertising campaign amounting to $ 30,000.

Various advantages of TV advertising are as follows –

Grabbing attention – taking the product to millions of homes can be done through TV

advertising as it is a very common medium available to each of the houses. Biggest advantage

of TV campaign is it is able to call out the potential customer’s right where it is required.

Combining sound and sight – with the TV advertising sight and sounds are combined that are

intrusive and capable of interrupting whatever else the the viewer may be doing to listen and

watch to the pitch

Assessment task 2 – Budget planning project

1. Draft marketing budget

2. E mail to CEO

From: John Ally johnally@xyz.com

To: Hedley Brown

Subject: Discussion of budget

Dear Sir,

I would like to draw your attention regarding the marketing budget of the company for which

I have been allocated an amount of $ 25,000. However, it has been budgeted that the expense

for the purpose of marketing will be amounted to $ 55,000. The significant variance of

budget against the allocation is inclusion of TV advertising campaign amounting to $ 30,000.

Various advantages of TV advertising are as follows –

Grabbing attention – taking the product to millions of homes can be done through TV

advertising as it is a very common medium available to each of the houses. Biggest advantage

of TV campaign is it is able to call out the potential customer’s right where it is required.

Combining sound and sight – with the TV advertising sight and sounds are combined that are

intrusive and capable of interrupting whatever else the the viewer may be doing to listen and

watch to the pitch

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10MANAGE BUDGET AND FINANCIAL PLANS

Hence, for discussing the budget please allow me a time and date for a meeting with you at

your convenient time.

Thanks & Regards,

John Ally,

Accounting manager

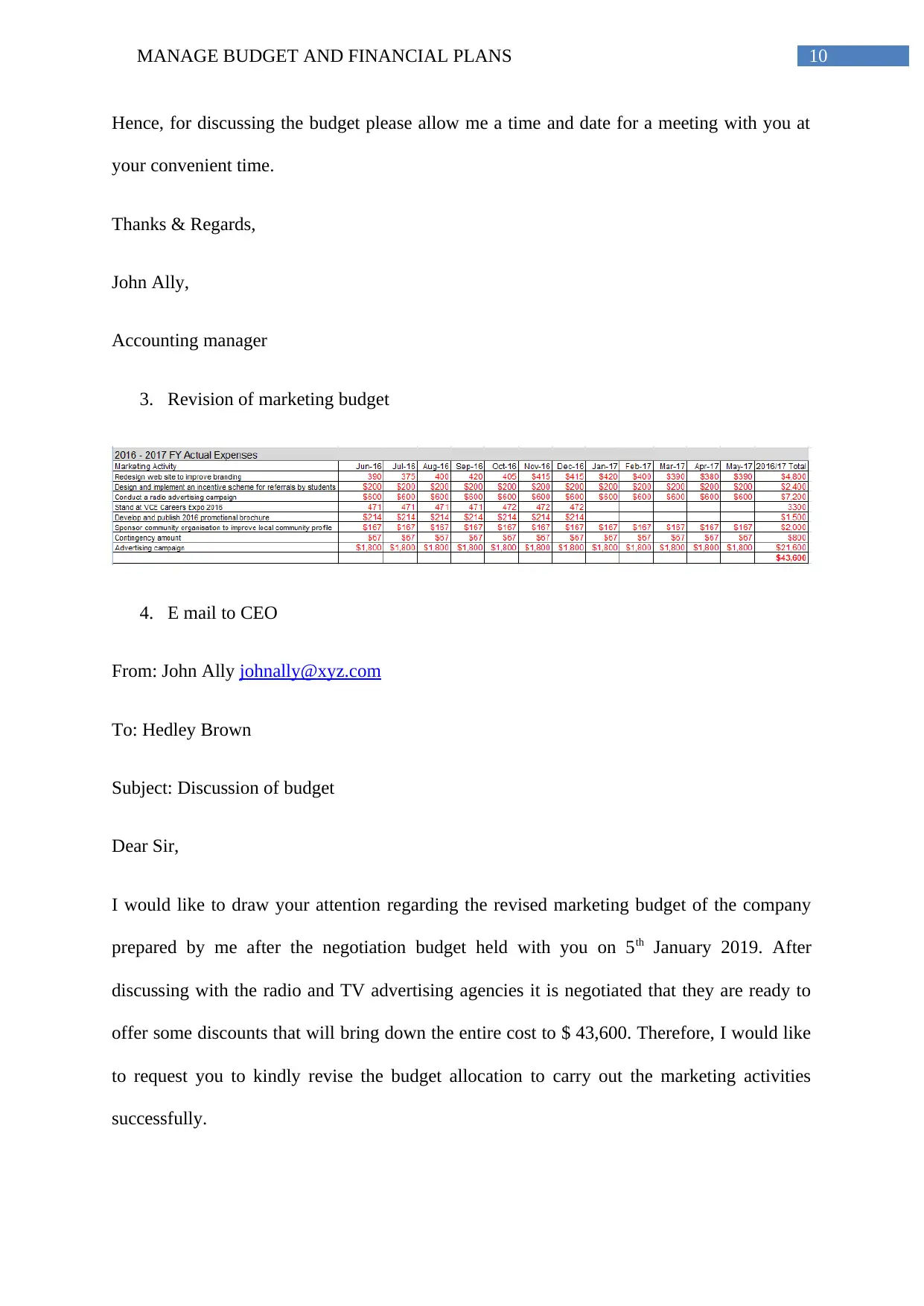

3. Revision of marketing budget

4. E mail to CEO

From: John Ally johnally@xyz.com

To: Hedley Brown

Subject: Discussion of budget

Dear Sir,

I would like to draw your attention regarding the revised marketing budget of the company

prepared by me after the negotiation budget held with you on 5th January 2019. After

discussing with the radio and TV advertising agencies it is negotiated that they are ready to

offer some discounts that will bring down the entire cost to $ 43,600. Therefore, I would like

to request you to kindly revise the budget allocation to carry out the marketing activities

successfully.

Hence, for discussing the budget please allow me a time and date for a meeting with you at

your convenient time.

Thanks & Regards,

John Ally,

Accounting manager

3. Revision of marketing budget

4. E mail to CEO

From: John Ally johnally@xyz.com

To: Hedley Brown

Subject: Discussion of budget

Dear Sir,

I would like to draw your attention regarding the revised marketing budget of the company

prepared by me after the negotiation budget held with you on 5th January 2019. After

discussing with the radio and TV advertising agencies it is negotiated that they are ready to

offer some discounts that will bring down the entire cost to $ 43,600. Therefore, I would like

to request you to kindly revise the budget allocation to carry out the marketing activities

successfully.

11MANAGE BUDGET AND FINANCIAL PLANS

Hence, for discussing the budget please allow me a time and date for a meeting with you at

your convenient time.

Thanks & Regards,

John Ally,

Accounting manager

5. Meeting with the team

Overall budget allocation

As per the discussion with the CEO the total allocated amount for budget was $

44,000 whereas the revised budget amount was $ 43,600. Major expenses will be towards

radio advertising expenses amounting to $ 7,200 and for TV advertising campaign it will be $

21,600. Stand at the VCE careers Expo for 2016 and Develop and publish 2016 promotional

brochure will be expensed for 2016 only (Renz, 2016). Expenses for redesigning the web

sites for improving the branding will be reduced to $ 4,800 from $ 5,000.

Amounts allocated for each marketing activity –

Redesign web site to improve branding – $ 4800

Design and implement an incentive scheme for referrals by students - $ 2400

Conduct a radio advertising campaign - $ 7200

Stand at VCE Careers Expo 2016 - $ 3300

Develop and publish 2016 promotional brochure - $ 1500

Sponsor community organisation to improve local community profile - $ 2,000

Contingency amount - $ 800

TV Advertising campaign - $ 21,600

Hence, for discussing the budget please allow me a time and date for a meeting with you at

your convenient time.

Thanks & Regards,

John Ally,

Accounting manager

5. Meeting with the team

Overall budget allocation

As per the discussion with the CEO the total allocated amount for budget was $

44,000 whereas the revised budget amount was $ 43,600. Major expenses will be towards

radio advertising expenses amounting to $ 7,200 and for TV advertising campaign it will be $

21,600. Stand at the VCE careers Expo for 2016 and Develop and publish 2016 promotional

brochure will be expensed for 2016 only (Renz, 2016). Expenses for redesigning the web

sites for improving the branding will be reduced to $ 4,800 from $ 5,000.

Amounts allocated for each marketing activity –

Redesign web site to improve branding – $ 4800

Design and implement an incentive scheme for referrals by students - $ 2400

Conduct a radio advertising campaign - $ 7200

Stand at VCE Careers Expo 2016 - $ 3300

Develop and publish 2016 promotional brochure - $ 1500

Sponsor community organisation to improve local community profile - $ 2,000

Contingency amount - $ 800

TV Advertising campaign - $ 21,600

12MANAGE BUDGET AND FINANCIAL PLANS

Allocated amount for contingencies

Amount allocated for the purpose of contingencies amounted to $ 800 that will be

expenses equally in each month at $ 67.

Outline of finance policies

To achieve the budget target the management as well as employees shall be provided

with proper training activities that will enable them to use various scarce resources in

efficient manner. Different segments for which the training is required are using of the

spreadsheet for maintaining the expenses, handling cash and complying with the financial

policies of the company (Lasserre, 2017). Further, for reimbursement of the expenses

incurred by the employees on behalf of the company shall be made only upon providing

proper bills and attachments. Moreover, cash amounting to more than $ 1,000 shall be

immediately deposited in bank account. Cash amounted to lower than $100 can be disbursed

any time from the petty cash.

Allocated amount for contingencies

Amount allocated for the purpose of contingencies amounted to $ 800 that will be

expenses equally in each month at $ 67.

Outline of finance policies

To achieve the budget target the management as well as employees shall be provided

with proper training activities that will enable them to use various scarce resources in

efficient manner. Different segments for which the training is required are using of the

spreadsheet for maintaining the expenses, handling cash and complying with the financial

policies of the company (Lasserre, 2017). Further, for reimbursement of the expenses

incurred by the employees on behalf of the company shall be made only upon providing

proper bills and attachments. Moreover, cash amounting to more than $ 1,000 shall be

immediately deposited in bank account. Cash amounted to lower than $100 can be disbursed

any time from the petty cash.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13MANAGE BUDGET AND FINANCIAL PLANS

Assessment task 3 – Monitor and control finances project

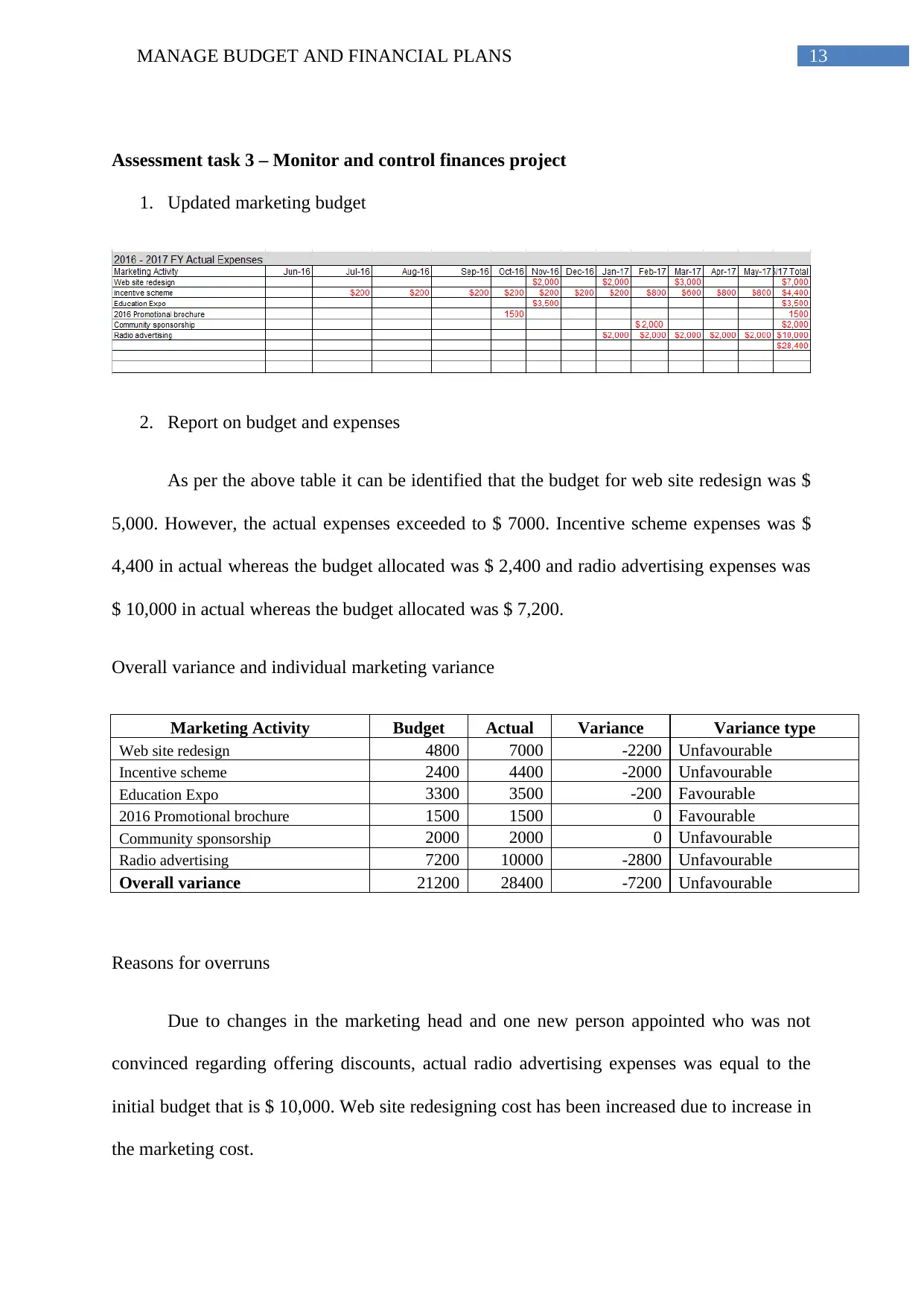

1. Updated marketing budget

2. Report on budget and expenses

As per the above table it can be identified that the budget for web site redesign was $

5,000. However, the actual expenses exceeded to $ 7000. Incentive scheme expenses was $

4,400 in actual whereas the budget allocated was $ 2,400 and radio advertising expenses was

$ 10,000 in actual whereas the budget allocated was $ 7,200.

Overall variance and individual marketing variance

Marketing Activity Budget Actual Variance Variance type

Web site redesign 4800 7000 -2200 Unfavourable

Incentive scheme 2400 4400 -2000 Unfavourable

Education Expo 3300 3500 -200 Favourable

2016 Promotional brochure 1500 1500 0 Favourable

Community sponsorship 2000 2000 0 Unfavourable

Radio advertising 7200 10000 -2800 Unfavourable

Overall variance 21200 28400 -7200 Unfavourable

Reasons for overruns

Due to changes in the marketing head and one new person appointed who was not

convinced regarding offering discounts, actual radio advertising expenses was equal to the

initial budget that is $ 10,000. Web site redesigning cost has been increased due to increase in

the marketing cost.

Assessment task 3 – Monitor and control finances project

1. Updated marketing budget

2. Report on budget and expenses

As per the above table it can be identified that the budget for web site redesign was $

5,000. However, the actual expenses exceeded to $ 7000. Incentive scheme expenses was $

4,400 in actual whereas the budget allocated was $ 2,400 and radio advertising expenses was

$ 10,000 in actual whereas the budget allocated was $ 7,200.

Overall variance and individual marketing variance

Marketing Activity Budget Actual Variance Variance type

Web site redesign 4800 7000 -2200 Unfavourable

Incentive scheme 2400 4400 -2000 Unfavourable

Education Expo 3300 3500 -200 Favourable

2016 Promotional brochure 1500 1500 0 Favourable

Community sponsorship 2000 2000 0 Unfavourable

Radio advertising 7200 10000 -2800 Unfavourable

Overall variance 21200 28400 -7200 Unfavourable

Reasons for overruns

Due to changes in the marketing head and one new person appointed who was not

convinced regarding offering discounts, actual radio advertising expenses was equal to the

initial budget that is $ 10,000. Web site redesigning cost has been increased due to increase in

the marketing cost.

14MANAGE BUDGET AND FINANCIAL PLANS

3. E-mail to CEO

From: John Ally johnally@xyz.com

To: Hedley Brown

Subject: Discussion of budget

Dear Sir,

I would like to draw your attention regarding the actual marketing expenses against budgeted

expenses. It was found that the actual expenses for the marketing expenses amounted to $

28,400 against the budgeted expenses of $ 21,200. Hence, the all over unfavourable variances

were amounted to $ 7,200. The attached documents will provide details regarding the actual

budget and variances for each activity.

Hence, I, therefore, request you to kindly go through the attached documents for details of

actual expenses and variance.

Thanks & Regards,

John Ally,

Accounting manager

3. E-mail to CEO

From: John Ally johnally@xyz.com

To: Hedley Brown

Subject: Discussion of budget

Dear Sir,

I would like to draw your attention regarding the actual marketing expenses against budgeted

expenses. It was found that the actual expenses for the marketing expenses amounted to $

28,400 against the budgeted expenses of $ 21,200. Hence, the all over unfavourable variances

were amounted to $ 7,200. The attached documents will provide details regarding the actual

budget and variances for each activity.

Hence, I, therefore, request you to kindly go through the attached documents for details of

actual expenses and variance.

Thanks & Regards,

John Ally,

Accounting manager

15MANAGE BUDGET AND FINANCIAL PLANS

Assessment task 4: Profit and loss review project

1. Report to CEO

Introduction

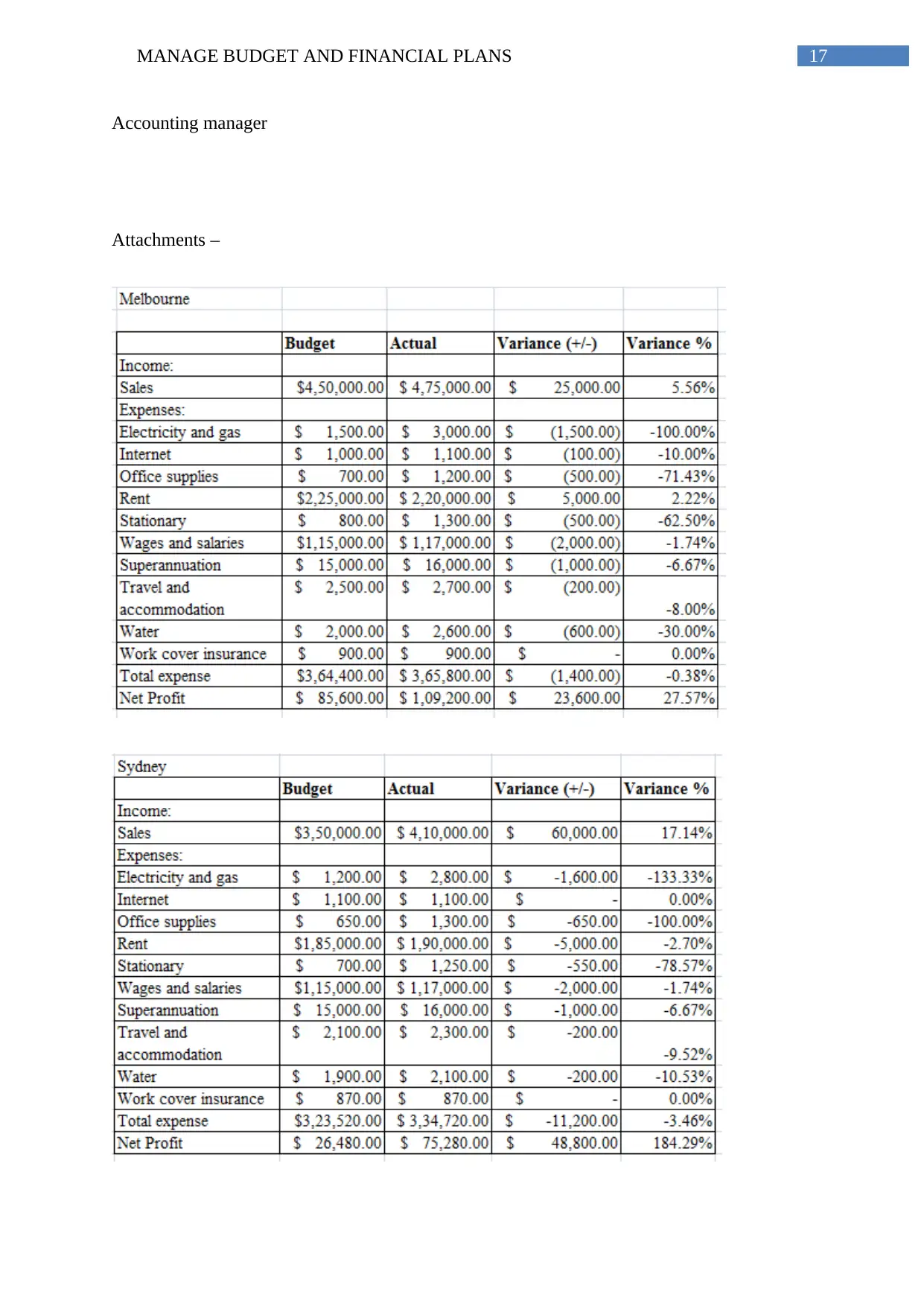

Main objective of the report is to focus on the performance of Melbourne campus and

Sydney campus for the period ended six months based on the given details. It will compare

the performance of each campus and recommend solutions regarding expenses where the

variances are more than 10% (Bryce, 2017).

Discussion

It can be identified from the details provided in the profit and loss account for the

period ended six months that the sales of Melbourne campus was more by 5.56% as

compared to the budget. On the other hand, sales of Sydney campus were more by 17.14% as

compared to the budget. Total expenses of Melbourne campus was more by 0.38% as

compared to the budget. On the other hand, expenses of Sydney campus were more by 3.46%

as compared to the budget. Profit for Melbourne campus exceeded by 27.57% and for Sydney

campus it exceeded by 184.29%. However, if the absolute value is considered, it can be

identified that the profit for Melbourne campus is significantly higher as compared to Sydney

campus (Ginter, Duncan & Swayne, 2018).

Variances higher than 10% for Sydney campus are – electricity and gas expenses,

internet, office supplies, stationary, and water and net profit. On the other hand, Variances

higher than 10% for Melbourne campus are – sales, electricity and gas expenses, office

supplies, stationary, and water and net profit.

Recommendation

Assessment task 4: Profit and loss review project

1. Report to CEO

Introduction

Main objective of the report is to focus on the performance of Melbourne campus and

Sydney campus for the period ended six months based on the given details. It will compare

the performance of each campus and recommend solutions regarding expenses where the

variances are more than 10% (Bryce, 2017).

Discussion

It can be identified from the details provided in the profit and loss account for the

period ended six months that the sales of Melbourne campus was more by 5.56% as

compared to the budget. On the other hand, sales of Sydney campus were more by 17.14% as

compared to the budget. Total expenses of Melbourne campus was more by 0.38% as

compared to the budget. On the other hand, expenses of Sydney campus were more by 3.46%

as compared to the budget. Profit for Melbourne campus exceeded by 27.57% and for Sydney

campus it exceeded by 184.29%. However, if the absolute value is considered, it can be

identified that the profit for Melbourne campus is significantly higher as compared to Sydney

campus (Ginter, Duncan & Swayne, 2018).

Variances higher than 10% for Sydney campus are – electricity and gas expenses,

internet, office supplies, stationary, and water and net profit. On the other hand, Variances

higher than 10% for Melbourne campus are – sales, electricity and gas expenses, office

supplies, stationary, and water and net profit.

Recommendation

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16MANAGE BUDGET AND FINANCIAL PLANS

Based on the above discussion it can be recommended that both the campuses shall

try to enhance their sales through spending in advertisement campaign. Expenses of office

supplies shall be tried to be minimized through taking quotations from other suppliers.

2. Report to CEO

From: John Ally johnally@xyz.com

To: Hedley Brown

Subject: Discussion of profit and loss

Dear Sir,

I would like to draw your attention regarding the performances of Melbourne campus and

Sydney campus regarding their profit status. It can be identified from the details provided in

the profit and loss account for the period ended six months that the sales of Melbourne

campus was more by 5.56% as compared to the budget. On the other hand, sales of Sydney

campus were more by 17.14% as compared to the budget. Total expenses of Melbourne

campus was more by 0.38% as compared to the budget. On the other hand, expenses of

Sydney campus were more by 3.46% as compared to the budget. Profit for Melbourne

campus exceeded by 27.57% and for Sydney campus it exceeded by 184.29%. However, if

the absolute value is considered, it can be identified that the profit for Melbourne campus is

significantly higher as compared to Sydney campus. Details attachments are attached

herewith for your review.

Hence, I, therefore request you to kindly go through the attachment.

Thanks & Regards,

John Ally,

Based on the above discussion it can be recommended that both the campuses shall

try to enhance their sales through spending in advertisement campaign. Expenses of office

supplies shall be tried to be minimized through taking quotations from other suppliers.

2. Report to CEO

From: John Ally johnally@xyz.com

To: Hedley Brown

Subject: Discussion of profit and loss

Dear Sir,

I would like to draw your attention regarding the performances of Melbourne campus and

Sydney campus regarding their profit status. It can be identified from the details provided in

the profit and loss account for the period ended six months that the sales of Melbourne

campus was more by 5.56% as compared to the budget. On the other hand, sales of Sydney

campus were more by 17.14% as compared to the budget. Total expenses of Melbourne

campus was more by 0.38% as compared to the budget. On the other hand, expenses of

Sydney campus were more by 3.46% as compared to the budget. Profit for Melbourne

campus exceeded by 27.57% and for Sydney campus it exceeded by 184.29%. However, if

the absolute value is considered, it can be identified that the profit for Melbourne campus is

significantly higher as compared to Sydney campus. Details attachments are attached

herewith for your review.

Hence, I, therefore request you to kindly go through the attachment.

Thanks & Regards,

John Ally,

17MANAGE BUDGET AND FINANCIAL PLANS

Accounting manager

Attachments –

Accounting manager

Attachments –

18MANAGE BUDGET AND FINANCIAL PLANS

Assessment 5: Aged Debtor Report

Report to CEO

Introduction

This report would look to address the report that has been derived from the aged

debtor report. This report is based on a six month period and this will be helpful in creating

an understanding of the performance of the company with respect to their debtors.

Discussion

The assessment of the report addresses the fact that the company has been effective

aged debtor management process. It is seen that the payment system is 14 days from invoice

and therefore the debtors are satisfied with the service that they receive.

In this manner, the debtors are able to receive their balance payment within a short

time period and therefore the transaction process is very fast and smooth. The aged debtor’s

process is a smooth and effective one and therefore the operational activities of the company

are better than their competitors.

Recommendation

There are certain recommendations that can be given to the company and they are as follows;

1. Assess the aged summary from time to time

2. Maintain healthy relationship with the debtors

3. Understand their issues and problems

4. Maintain proper debtor management process

5. Assess the debtor management process that is undertaken by their rival companies.

Assessment 5: Aged Debtor Report

Report to CEO

Introduction

This report would look to address the report that has been derived from the aged

debtor report. This report is based on a six month period and this will be helpful in creating

an understanding of the performance of the company with respect to their debtors.

Discussion

The assessment of the report addresses the fact that the company has been effective

aged debtor management process. It is seen that the payment system is 14 days from invoice

and therefore the debtors are satisfied with the service that they receive.

In this manner, the debtors are able to receive their balance payment within a short

time period and therefore the transaction process is very fast and smooth. The aged debtor’s

process is a smooth and effective one and therefore the operational activities of the company

are better than their competitors.

Recommendation

There are certain recommendations that can be given to the company and they are as follows;

1. Assess the aged summary from time to time

2. Maintain healthy relationship with the debtors

3. Understand their issues and problems

4. Maintain proper debtor management process

5. Assess the debtor management process that is undertaken by their rival companies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19MANAGE BUDGET AND FINANCIAL PLANS

2.

From: John Ally johnally@xyz.com

To: Hedley Brown

Subject: Discussion of profit and loss

Respected Sir,

This is to inform you that we have gone through the aged debtor report and have assessed the

summary report as well. The results have indicated the fact that the summary report is quite

good and the performance of the company with respect to the aged debtor report has been

proper. The payment process for the debtors is precise and timely. It is due to this fact that the

debtors are satisfied.

This process can be continued even though certain improvements can be made that has been

mentioned in the report. It can be said that the incorporation of these suggestions can improve

the performance of the company to the next level.

Kindly go through the attachment

Thanks and Regards

John Ally

Attachments:

Client Name

120+

Days

90

Days

60

Days

30

Days Current Total

2.

From: John Ally johnally@xyz.com

To: Hedley Brown

Subject: Discussion of profit and loss

Respected Sir,

This is to inform you that we have gone through the aged debtor report and have assessed the

summary report as well. The results have indicated the fact that the summary report is quite

good and the performance of the company with respect to the aged debtor report has been

proper. The payment process for the debtors is precise and timely. It is due to this fact that the

debtors are satisfied.

This process can be continued even though certain improvements can be made that has been

mentioned in the report. It can be said that the incorporation of these suggestions can improve

the performance of the company to the next level.

Kindly go through the attachment

Thanks and Regards

John Ally

Attachments:

Client Name

120+

Days

90

Days

60

Days

30

Days Current Total

20MANAGE BUDGET AND FINANCIAL PLANS

Client 1 $2,800 $1,560

$

1,440.0

0

$

2,160.0

0

$

1,800.0

0

$

9,760.0

0

Client 2 $2,600 $1,320 $1,000 $2,400 $2,320

$

9,640.0

0

Client 3 $1,450 $1,780 $2,450 $950 $3,100

$

9,730.0

0

Totals

6,850.0

0

4,660.0

0

4,890.0

0

5,510.0

0

7,220.0

0

Client Name

120+

Days 90 Days 60 Days 30 Days Current Total

Client 1

$3,476.

00

$4,356.

00

$1,250.

00

$2,100.

00

$4,314.

00

$15,496.

00

Client 2

$2,714.

00

$2,780.

00

$4,120.

00

$2,450.

00

$5,000.

00

$17,064.

00

Client 3

$4,210.

00

$2,870.

00

$3,781.

00

$6,751.

00

$1,870.

00

$19,482.

00

Client 1 $2,800 $1,560

$

1,440.0

0

$

2,160.0

0

$

1,800.0

0

$

9,760.0

0

Client 2 $2,600 $1,320 $1,000 $2,400 $2,320

$

9,640.0

0

Client 3 $1,450 $1,780 $2,450 $950 $3,100

$

9,730.0

0

Totals

6,850.0

0

4,660.0

0

4,890.0

0

5,510.0

0

7,220.0

0

Client Name

120+

Days 90 Days 60 Days 30 Days Current Total

Client 1

$3,476.

00

$4,356.

00

$1,250.

00

$2,100.

00

$4,314.

00

$15,496.

00

Client 2

$2,714.

00

$2,780.

00

$4,120.

00

$2,450.

00

$5,000.

00

$17,064.

00

Client 3

$4,210.

00

$2,870.

00

$3,781.

00

$6,751.

00

$1,870.

00

$19,482.

00

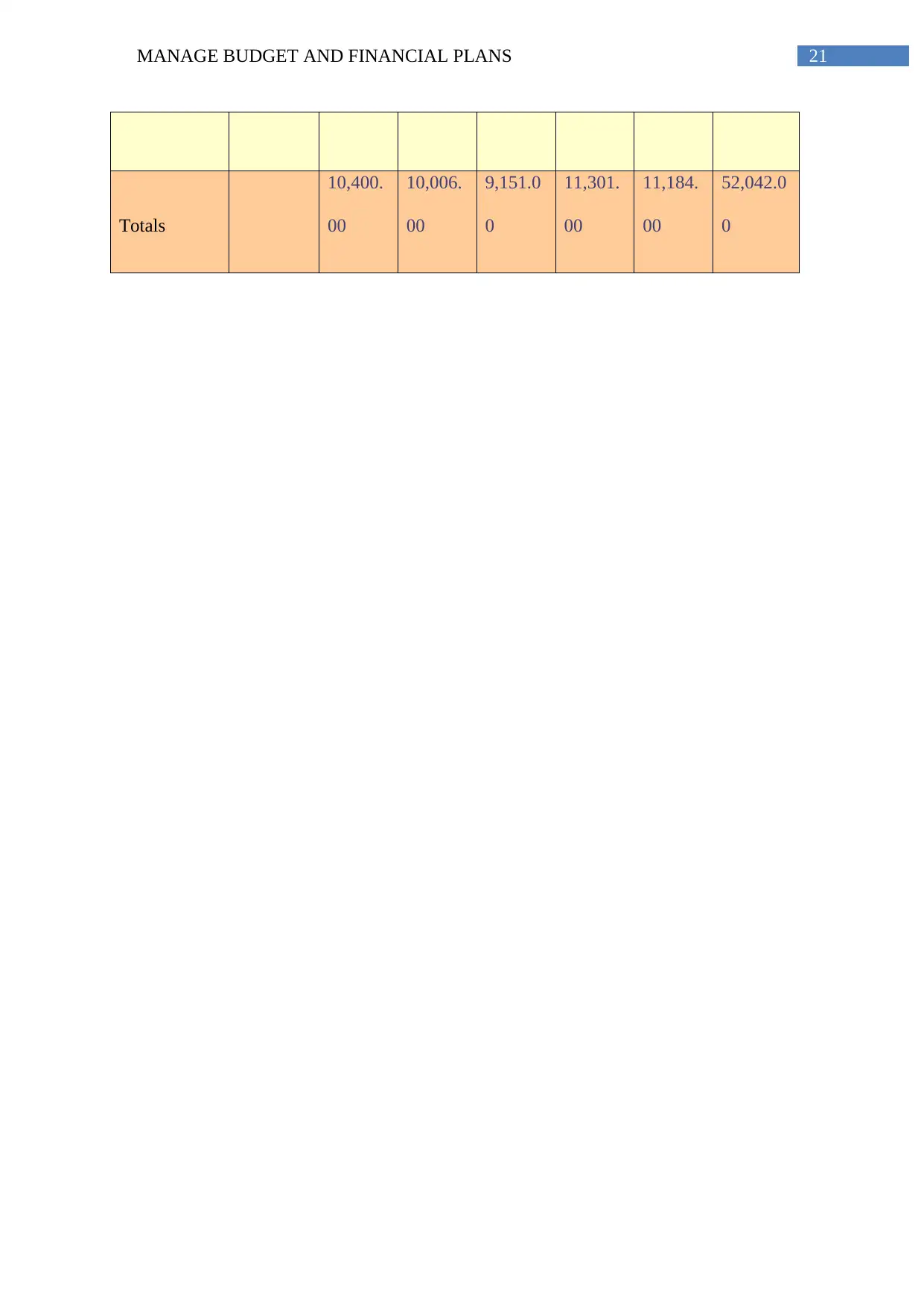

21MANAGE BUDGET AND FINANCIAL PLANS

Totals

10,400.

00

10,006.

00

9,151.0

0

11,301.

00

11,184.

00

52,042.0

0

Totals

10,400.

00

10,006.

00

9,151.0

0

11,301.

00

11,184.

00

52,042.0

0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22MANAGE BUDGET AND FINANCIAL PLANS

Reference

Ato.gov.au. (2019). Home page. Retrieved 7 January 2019, from https://www.ato.gov.au/

Bryce, H. J. (2017). Financial and strategic management for nonprofit organizations. Walter

de Gruyter GmbH & Co KG.

Dudin, M., Prokofev, M., Fedorova, I., Frygin, A., & Kucuri, G. (2015). International

Practice of Generation of the National Budget Income on the Basis of the Generally

Accepted Financial Reporting Standards (IFRS).

Dzhandzhugazova, E. A., Zaitseva, N. A., Larionova, A. A., Petrovskaya, M. V., &

Chaplyuk, V. Z. (2015). Methodological aspects of strategic management of financial

risks during construction of hotel business objects. Asian Social Science, 11(20), 229.

Ginter, P. M., Duncan, W. J., & Swayne, L. E. (2018). The strategic management of health

care organizations. John Wiley & Sons.

Kumar, R. (2017). Strategic Financial Management Casebook. Academic Press.

Lasserre, P. (2017). Global strategic management. Macmillan International Higher

Education.

Manasan, R. G. (2017). Reforming the legal framework for the budget process.

McKinney, J. B. (2015). Effective financial management in public and nonprofit agencies.

ABC-CLIO.

Morden, T. (2016). Principles of strategic management. Routledge.

Reference

Ato.gov.au. (2019). Home page. Retrieved 7 January 2019, from https://www.ato.gov.au/

Bryce, H. J. (2017). Financial and strategic management for nonprofit organizations. Walter

de Gruyter GmbH & Co KG.

Dudin, M., Prokofev, M., Fedorova, I., Frygin, A., & Kucuri, G. (2015). International

Practice of Generation of the National Budget Income on the Basis of the Generally

Accepted Financial Reporting Standards (IFRS).

Dzhandzhugazova, E. A., Zaitseva, N. A., Larionova, A. A., Petrovskaya, M. V., &

Chaplyuk, V. Z. (2015). Methodological aspects of strategic management of financial

risks during construction of hotel business objects. Asian Social Science, 11(20), 229.

Ginter, P. M., Duncan, W. J., & Swayne, L. E. (2018). The strategic management of health

care organizations. John Wiley & Sons.

Kumar, R. (2017). Strategic Financial Management Casebook. Academic Press.

Lasserre, P. (2017). Global strategic management. Macmillan International Higher

Education.

Manasan, R. G. (2017). Reforming the legal framework for the budget process.

McKinney, J. B. (2015). Effective financial management in public and nonprofit agencies.

ABC-CLIO.

Morden, T. (2016). Principles of strategic management. Routledge.

23MANAGE BUDGET AND FINANCIAL PLANS

Morgan, D., Robinson, K. S., Strachota, D., & Hough, J. A. (2017). The Budget Cycle:

Characteristics and Consequences. In Budgeting for Local Governments and

Communities (pp. 135-164). Routledge.

Muli, B. M., & Rotich, G. (2016). Effect of financial management practices on budget

implementation of county governments: A case of Machakos County. Strategic

Journal of Business & Change Management, 3(4).

Nosheen, S., Sadiq, R., & Rafay, A. (2016, September). The primacy of innovation in

strategic financial management-understanding the impact of innovation and

performance on capital structure. In Management of Innovation and Technology

(ICMIT), 2016 IEEE International Conference on(pp. 280-285). IEEE.

Renz, D. O. (2016). The Jossey-Bass handbook of nonprofit leadership and management.

John Wiley & Sons.

Sofat, R., & Hiro, P. (2015). Strategic financial management. PHI Learning Pvt. Ltd.

Morgan, D., Robinson, K. S., Strachota, D., & Hough, J. A. (2017). The Budget Cycle:

Characteristics and Consequences. In Budgeting for Local Governments and

Communities (pp. 135-164). Routledge.

Muli, B. M., & Rotich, G. (2016). Effect of financial management practices on budget

implementation of county governments: A case of Machakos County. Strategic

Journal of Business & Change Management, 3(4).

Nosheen, S., Sadiq, R., & Rafay, A. (2016, September). The primacy of innovation in

strategic financial management-understanding the impact of innovation and

performance on capital structure. In Management of Innovation and Technology

(ICMIT), 2016 IEEE International Conference on(pp. 280-285). IEEE.

Renz, D. O. (2016). The Jossey-Bass handbook of nonprofit leadership and management.

John Wiley & Sons.

Sofat, R., & Hiro, P. (2015). Strategic financial management. PHI Learning Pvt. Ltd.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.