Manage Budgets and Financial Plans

VerifiedAdded on 2023/01/10

|19

|5233

|92

AI Summary

This document provides information on managing budgets and financial plans in organizations. It covers topics such as record keeping, contingency plans, budget variances, and managing travel expenses. It also includes a flowchart for expense submission and a meeting agenda for discussing travel expenses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGE BUDGETS AND

FINANCIAL PLANS

FINANCIAL PLANS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

ASSESSMENT 1.............................................................................................................................1

Written Knowledge Questions.....................................................................................................1

ASSESSMENT 2.............................................................................................................................6

TASK 1........................................................................................................................................6

TASK 2........................................................................................................................................6

TASK 3........................................................................................................................................7

TASK 4........................................................................................................................................8

TASK 5........................................................................................................................................9

TASK 6......................................................................................................................................11

TASK 7......................................................................................................................................11

TASK 8......................................................................................................................................12

ASSESSMENT 3...........................................................................................................................13

Case Study 1..............................................................................................................................13

TASK 1......................................................................................................................................13

TASK 2......................................................................................................................................15

Case Study 2..............................................................................................................................15

REFERENCES..............................................................................................................................18

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

ASSESSMENT 1.............................................................................................................................1

Written Knowledge Questions.....................................................................................................1

ASSESSMENT 2.............................................................................................................................6

TASK 1........................................................................................................................................6

TASK 2........................................................................................................................................6

TASK 3........................................................................................................................................7

TASK 4........................................................................................................................................8

TASK 5........................................................................................................................................9

TASK 6......................................................................................................................................11

TASK 7......................................................................................................................................11

TASK 8......................................................................................................................................12

ASSESSMENT 3...........................................................................................................................13

Case Study 1..............................................................................................................................13

TASK 1......................................................................................................................................13

TASK 2......................................................................................................................................15

Case Study 2..............................................................................................................................15

REFERENCES..............................................................................................................................18

INTRODUTION

Budget and finance are two of the important factors of any organisation. Budget refers to the

spending plan of an organisation. it is prepared by making projections for the future sales and

expenses of the company. Budget is very essential for enabling the organisation to maintain

control over its costs and expenditures. It provides the company to identify the areas where

improvements are required to increase the efficiency and productivity of the organisation. report

of variance analysis provides variations for inspecting the causes of variances. Finance involves

providing the company with funds to manage the business operations. Managers have to carry

out various activities such as procurement, management and utilisation of the funds. it ensures

that the financial funds are utilised in the best efficient manner to increase the profits. Present

report includes planning & implementation of the financial management approaches, working

with the team members that carry out financial operations, controlling finances, monitoring and

evaluating the effectiveness of the financial management process. It is applicable to the managers

that have responsibility to ensure that the financial resources are efficiently and effectively used

for earning adequate returns.

ASSESSMENT 1

Written Knowledge Questions

1. Record keeping and Contingency and mitigation plan for improving the performance.

Every organisation is required to maintain proper records of the financial transactions

carried out during the year. There is set procedure for recording all the transactions properly

according to double entry book keeping method. If the basic records of the transactions are

accurate than the whole records will be incorrect and the financial statements prepared from the

records will provide inaccurate results. Company should establish adequate internal control

process and procedures where the records are properly checked. Internal control helps in

ensuring that the financial records are free from errors and misstatements and gives true and fair

view of the financial position of company. Numbers of important decisions are taken on the basis

of financial records and reports and where the financial records are not accurate decisions taken

will not provide the desired results.

2. Purpose budget and role in supporting the business objectives.

Budget refers to the financial plan of the business for a given period of time. it is also

known as the spending plan of company to be followed over the period. Budgets are prepared by

1

Budget and finance are two of the important factors of any organisation. Budget refers to the

spending plan of an organisation. it is prepared by making projections for the future sales and

expenses of the company. Budget is very essential for enabling the organisation to maintain

control over its costs and expenditures. It provides the company to identify the areas where

improvements are required to increase the efficiency and productivity of the organisation. report

of variance analysis provides variations for inspecting the causes of variances. Finance involves

providing the company with funds to manage the business operations. Managers have to carry

out various activities such as procurement, management and utilisation of the funds. it ensures

that the financial funds are utilised in the best efficient manner to increase the profits. Present

report includes planning & implementation of the financial management approaches, working

with the team members that carry out financial operations, controlling finances, monitoring and

evaluating the effectiveness of the financial management process. It is applicable to the managers

that have responsibility to ensure that the financial resources are efficiently and effectively used

for earning adequate returns.

ASSESSMENT 1

Written Knowledge Questions

1. Record keeping and Contingency and mitigation plan for improving the performance.

Every organisation is required to maintain proper records of the financial transactions

carried out during the year. There is set procedure for recording all the transactions properly

according to double entry book keeping method. If the basic records of the transactions are

accurate than the whole records will be incorrect and the financial statements prepared from the

records will provide inaccurate results. Company should establish adequate internal control

process and procedures where the records are properly checked. Internal control helps in

ensuring that the financial records are free from errors and misstatements and gives true and fair

view of the financial position of company. Numbers of important decisions are taken on the basis

of financial records and reports and where the financial records are not accurate decisions taken

will not provide the desired results.

2. Purpose budget and role in supporting the business objectives.

Budget refers to the financial plan of the business for a given period of time. it is also

known as the spending plan of company to be followed over the period. Budgets are prepared by

1

the organisation to make effective utilisation of the existing resources of company. it involves

making optimum utilisation of the available resources for achieving the targeted goals and

objectives. Various budgets are prepared by the organisation for different activities for achieving

the targets. Budgets help the business in keeping control over their costs and expenditures.

Company also compares the actual and budgeted figures to identify the variances on the basis of

which corrective actions and measures are taken by the enterprise. It helps the business in

achieving the goals and objectives of organisation.

3. Contingency and mitigation plan

3.a Examples of contingency plan

1) Cafe could keep extra coffee machine that could be used at such times. Machine could be

used by the cafe over season sales. It will also help in generating extra revenues. Extra

machine will be having purchase price, electricity charge and depreciation. Over season

sales it will help in generating extra revenues by selling 300 cups of coffee extra every

week.

2) Cafe could also hire machine on rent over such situation from the local suppliers. It could

make contact with the supplier of machine that could provide machine on rent at

reasonable rate for the specified time till the machine is repaired. In this company will be

incurring rent cost and will not generate extra revenues as is replaced for machine being

repaired.

b. Preventive mitigation plan

Company could purchase an extra coffee machine for the cafe which could be new or

second hand as per funds. This will require cafe to bear purchase cost, depreciation and

electricity cost. It could generate additional revenues by using the machine over high sales period

for generating additional revenues.

4 Reviewing budgets

a. The provided budget is sales budget that provides the management information regarding the

sales level to be achieved in the given period of time. it is prepared for ensuring targeted sales

level are achieved for covering cost. Overall sales target of quarter is 19700 units for having

revenues of 306200.

2

making optimum utilisation of the available resources for achieving the targeted goals and

objectives. Various budgets are prepared by the organisation for different activities for achieving

the targets. Budgets help the business in keeping control over their costs and expenditures.

Company also compares the actual and budgeted figures to identify the variances on the basis of

which corrective actions and measures are taken by the enterprise. It helps the business in

achieving the goals and objectives of organisation.

3. Contingency and mitigation plan

3.a Examples of contingency plan

1) Cafe could keep extra coffee machine that could be used at such times. Machine could be

used by the cafe over season sales. It will also help in generating extra revenues. Extra

machine will be having purchase price, electricity charge and depreciation. Over season

sales it will help in generating extra revenues by selling 300 cups of coffee extra every

week.

2) Cafe could also hire machine on rent over such situation from the local suppliers. It could

make contact with the supplier of machine that could provide machine on rent at

reasonable rate for the specified time till the machine is repaired. In this company will be

incurring rent cost and will not generate extra revenues as is replaced for machine being

repaired.

b. Preventive mitigation plan

Company could purchase an extra coffee machine for the cafe which could be new or

second hand as per funds. This will require cafe to bear purchase cost, depreciation and

electricity cost. It could generate additional revenues by using the machine over high sales period

for generating additional revenues.

4 Reviewing budgets

a. The provided budget is sales budget that provides the management information regarding the

sales level to be achieved in the given period of time. it is prepared for ensuring targeted sales

level are achieved for covering cost. Overall sales target of quarter is 19700 units for having

revenues of 306200.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

b. Data tells that company is having sales in March as compared with January and February

month. it could also be seen that it keeps price high in low sales level and decrease prices slightly

when sales volume rises.

c. The budget provided could be verified from the previous trends and sales level. It has to

analyse all the factors that could influence the budget and its effectiveness. To analyse the budget

it could review market conditions, demand and economic conditions.

d. Potential risks in achieving the budget are ability of company to meet the targeted sales level

from the available resources. capacity of the company to meet the demands for March. Adequate

funds for running the operations of business successfully. It could produce extra units in months

of January and February for meeting sales of March.

e. Related to this company has to make allocation of the resources effectively for meeting the

budget targets. Manager could be made understood with the outcomes from the analysis carried

out of various facts.

5. Team members to understand budget and their roles and responsibilities.

It is essential for the member to adequately understand the budget to ensure that process

and work is performed in the defined manner. It avoids confusion and misunderstanding of the

budgets. If the budgets are not properly understood the targeted objectives may not achieved.

Roles and responsibilities of all the employees should be properly defined and allocated so that

the effective use of the resources could be taken. For understanding the budget it is essential that

they are properly communicated.

Oral communication to properly explain the budgets

Written communication so that members have record and written guidance for

performing task

6 GST, requirements and reporting requirements.

GST is defined as goods and service tax that is levied over supply of goods and services.

It is paid by those who have consumed or received goods or services. Businesses registered with

GST have to maintain proper record of all the sales and purchase transactions and pay GST

periodically.

Reporting requirements are sales records, total GST sales, GST invoices, purchases and GST

paid.

3

month. it could also be seen that it keeps price high in low sales level and decrease prices slightly

when sales volume rises.

c. The budget provided could be verified from the previous trends and sales level. It has to

analyse all the factors that could influence the budget and its effectiveness. To analyse the budget

it could review market conditions, demand and economic conditions.

d. Potential risks in achieving the budget are ability of company to meet the targeted sales level

from the available resources. capacity of the company to meet the demands for March. Adequate

funds for running the operations of business successfully. It could produce extra units in months

of January and February for meeting sales of March.

e. Related to this company has to make allocation of the resources effectively for meeting the

budget targets. Manager could be made understood with the outcomes from the analysis carried

out of various facts.

5. Team members to understand budget and their roles and responsibilities.

It is essential for the member to adequately understand the budget to ensure that process

and work is performed in the defined manner. It avoids confusion and misunderstanding of the

budgets. If the budgets are not properly understood the targeted objectives may not achieved.

Roles and responsibilities of all the employees should be properly defined and allocated so that

the effective use of the resources could be taken. For understanding the budget it is essential that

they are properly communicated.

Oral communication to properly explain the budgets

Written communication so that members have record and written guidance for

performing task

6 GST, requirements and reporting requirements.

GST is defined as goods and service tax that is levied over supply of goods and services.

It is paid by those who have consumed or received goods or services. Businesses registered with

GST have to maintain proper record of all the sales and purchase transactions and pay GST

periodically.

Reporting requirements are sales records, total GST sales, GST invoices, purchases and GST

paid.

3

7 Requirements for financial record keeping

Company has to keep all the invoices related to the sales and purchases. They have to

keep proper records of bank and other statement. Records related all the expenses and costs have

to be kept. All the GST related invoices and documents have to be kept. They have to keep

record of all the transactions carried out during the year.

8. Principles of cash flow

Being realistic

Planning for multiple scenarios

Considering income and expenses adequately

Providing about the variable and fixed costs

Including every item of cost.

Techniques for managing cash flow.

Considering only relevant costs.

Paying off debt quickly.

Collection of revenues timely.

Avoiding unproductive costs.

9. Improvement in the financial management processes

It is essential for the business to make timely update the financial management processes

of business. On the basis of analysing records and financial statements company was having

problems regarding increasing cost. On identifying the increasing cost management take

measures for improving the processes to control cost. They analysed the areas from where cost

was increasing. It removed the unproductive costs and expenses which were not generating

returns for company. Removing unproductive cost helps in increasing the profits and enhancing

the financial management process.

10. Budget variance and managing financial performance

Budget variance is a tool used in financial management for making effective utilisation of

the resources. it enables the management to identify the reasons between budgeted and actual

figures. On the basis of variance identified companies take corrective measures for improving the

performance.

11.Explain

4

Company has to keep all the invoices related to the sales and purchases. They have to

keep proper records of bank and other statement. Records related all the expenses and costs have

to be kept. All the GST related invoices and documents have to be kept. They have to keep

record of all the transactions carried out during the year.

8. Principles of cash flow

Being realistic

Planning for multiple scenarios

Considering income and expenses adequately

Providing about the variable and fixed costs

Including every item of cost.

Techniques for managing cash flow.

Considering only relevant costs.

Paying off debt quickly.

Collection of revenues timely.

Avoiding unproductive costs.

9. Improvement in the financial management processes

It is essential for the business to make timely update the financial management processes

of business. On the basis of analysing records and financial statements company was having

problems regarding increasing cost. On identifying the increasing cost management take

measures for improving the processes to control cost. They analysed the areas from where cost

was increasing. It removed the unproductive costs and expenses which were not generating

returns for company. Removing unproductive cost helps in increasing the profits and enhancing

the financial management process.

10. Budget variance and managing financial performance

Budget variance is a tool used in financial management for making effective utilisation of

the resources. it enables the management to identify the reasons between budgeted and actual

figures. On the basis of variance identified companies take corrective measures for improving the

performance.

11.Explain

4

a. GST and collection

Goods and service tax is value added tax in Australia of 10% on sales of goods and services.

GST is collected of business having turnover above the threshold limit. It is collected using two

methods BAS and full reposting method software.

b. Registration

If turnover of the business is more than $75000

If it is expected that turnover will reach threshold limit in initial year.

c. Obligations to record GST and submission of summaries.

They have to record all the sales, invoices for sales, purchases and all the documents

related to the GST. They have to submit the financial summaries over two methods. If turnover is

higher than $10 million by BAS reporting method and BAS reporting method if less than

$10million.

12.

a. Financial records

Bank statements – To prepare cash book and to identify errors.

Invoices – To record transaction and to prepare the financial statements.

Property records – To show title and for making valuations.

b. Requirements for record keeping

Financial record keeping is done on the basis of transactions carried out by the business. it

requires invoices of the sales, purchases and expenses incurred by the company. It is maintained

for preparing the financial statements to represent the financial position and performance of the

company. Accountants are required to record every transaction in the journals, posting them in

ledgers, preparing trial balance and financial statements. All the invoices related to the

transactions will be kept in relevant files. Transactions will be recorded daily in the computer

and all the records will be maintained safely.

13. Financial statement analysis

a. Profit or loss statement – To identify the profitability of business. it includes costs and

incomes of the company to take decisions related to performance

b. Balance sheet – It provides about financial position of firm. It includes assets and liabilities

that representing obligations and financial risks that helps business in taking decisions for

improving the position.

5

Goods and service tax is value added tax in Australia of 10% on sales of goods and services.

GST is collected of business having turnover above the threshold limit. It is collected using two

methods BAS and full reposting method software.

b. Registration

If turnover of the business is more than $75000

If it is expected that turnover will reach threshold limit in initial year.

c. Obligations to record GST and submission of summaries.

They have to record all the sales, invoices for sales, purchases and all the documents

related to the GST. They have to submit the financial summaries over two methods. If turnover is

higher than $10 million by BAS reporting method and BAS reporting method if less than

$10million.

12.

a. Financial records

Bank statements – To prepare cash book and to identify errors.

Invoices – To record transaction and to prepare the financial statements.

Property records – To show title and for making valuations.

b. Requirements for record keeping

Financial record keeping is done on the basis of transactions carried out by the business. it

requires invoices of the sales, purchases and expenses incurred by the company. It is maintained

for preparing the financial statements to represent the financial position and performance of the

company. Accountants are required to record every transaction in the journals, posting them in

ledgers, preparing trial balance and financial statements. All the invoices related to the

transactions will be kept in relevant files. Transactions will be recorded daily in the computer

and all the records will be maintained safely.

13. Financial statement analysis

a. Profit or loss statement – To identify the profitability of business. it includes costs and

incomes of the company to take decisions related to performance

b. Balance sheet – It provides about financial position of firm. It includes assets and liabilities

that representing obligations and financial risks that helps business in taking decisions for

improving the position.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

c. General Ledger – It represents the balances of different accounts of company to analyse the

transactions carried out during the year. Management could identify the accounts in which no

transactions are carried out and ensuring that accounts are properly prepared.

ASSESSMENT 2

TASK 1

Bliss & Me Travel and Expense Policy

a. Employee responsibilities

To ensure that cost is minimised where possible and to abide by the budgets outlined in

the policy.

To contact with line manager where flexibility is required by employees in extenuating

circumstances.

They have to provide all the receipts and invoices for the travel.

b. Daily travel allowance for the staff that are travelling interstate for business

Daily travel allowance of the employees is $830 and expenses exceeding the budget has to be

approved by respective managers.

c. Process of submitting expenses with the corporate credit card.

To claim the expenses incurred from credit card employees is required to document all

the expenses in spreadsheet and expense spreadsheet along with actual receipts are to be sent to

line managers within 48 hours of purchase for approval.

d. Document whether allowance allocations include GST.

The allowance allocations to the employees of company are exclusive of GST which

means GST is not included in the cost.

TASK 2

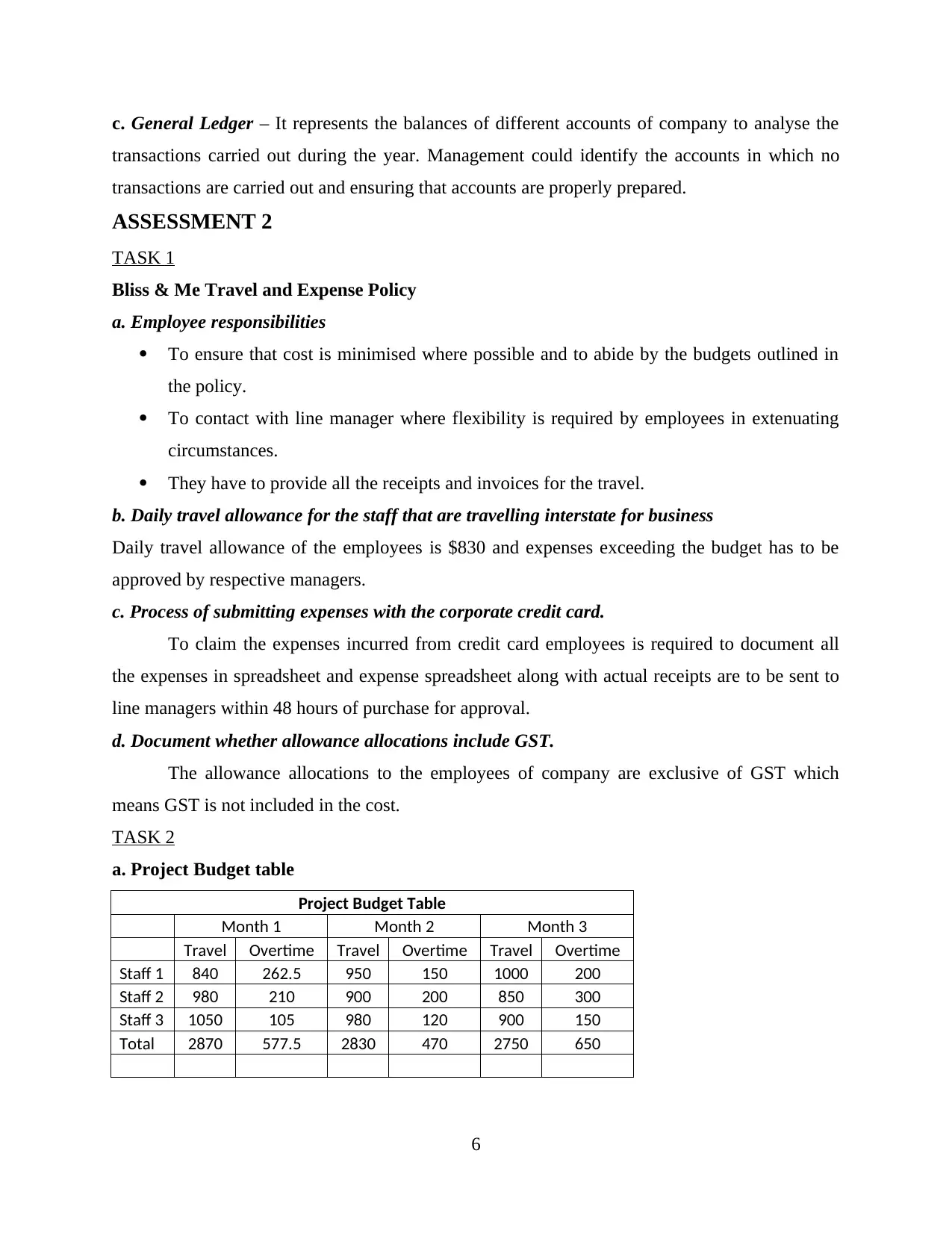

a. Project Budget table

Project Budget Table

Month 1 Month 2 Month 3

Travel Overtime Travel Overtime Travel Overtime

Staff 1 840 262.5 950 150 1000 200

Staff 2 980 210 900 200 850 300

Staff 3 1050 105 980 120 900 150

Total 2870 577.5 2830 470 2750 650

6

transactions carried out during the year. Management could identify the accounts in which no

transactions are carried out and ensuring that accounts are properly prepared.

ASSESSMENT 2

TASK 1

Bliss & Me Travel and Expense Policy

a. Employee responsibilities

To ensure that cost is minimised where possible and to abide by the budgets outlined in

the policy.

To contact with line manager where flexibility is required by employees in extenuating

circumstances.

They have to provide all the receipts and invoices for the travel.

b. Daily travel allowance for the staff that are travelling interstate for business

Daily travel allowance of the employees is $830 and expenses exceeding the budget has to be

approved by respective managers.

c. Process of submitting expenses with the corporate credit card.

To claim the expenses incurred from credit card employees is required to document all

the expenses in spreadsheet and expense spreadsheet along with actual receipts are to be sent to

line managers within 48 hours of purchase for approval.

d. Document whether allowance allocations include GST.

The allowance allocations to the employees of company are exclusive of GST which

means GST is not included in the cost.

TASK 2

a. Project Budget table

Project Budget Table

Month 1 Month 2 Month 3

Travel Overtime Travel Overtime Travel Overtime

Staff 1 840 262.5 950 150 1000 200

Staff 2 980 210 900 200 850 300

Staff 3 1050 105 980 120 900 150

Total 2870 577.5 2830 470 2750 650

6

b. Evaluation of Project cost.

The allocated budget has provided the costs and expenses for the travel by employees.

The project could not be said as sufficient for cost of the project. Cost of the project should be

based on the distance travelled. Lunch is not available at same price as of dinner which is very

low. It has to increase the cost for breakfast. Expenses for breakfast and dinner are sufficient.

Expenses of flight to be set as per the longest area covered for sales. Overtime costs of the

project are adequate and sufficient. Budget for miscellaneous expenses is not sufficient as they

have to travel from one place to another that may cost such as taxi fares and such other costs.

TASK 3

a. Flowchart of expense submission

b. Meeting Agenda

Agenda – To discuss the travelling expenses

Looking at the increased variation in travel expenses meeting has been organised to

discuss the issues and to come out with possible solutions and keeping the travel expenses within

the budget.

As per the budget per month travelling cost is $940 and overtime cost is $52.5. The

budget has been prepared reviewing all the travel cost where the business deals. However

discrepancies and ups and downs may be seen due to circumstances. Expenses are passed on

7

The allocated budget has provided the costs and expenses for the travel by employees.

The project could not be said as sufficient for cost of the project. Cost of the project should be

based on the distance travelled. Lunch is not available at same price as of dinner which is very

low. It has to increase the cost for breakfast. Expenses for breakfast and dinner are sufficient.

Expenses of flight to be set as per the longest area covered for sales. Overtime costs of the

project are adequate and sufficient. Budget for miscellaneous expenses is not sufficient as they

have to travel from one place to another that may cost such as taxi fares and such other costs.

TASK 3

a. Flowchart of expense submission

b. Meeting Agenda

Agenda – To discuss the travelling expenses

Looking at the increased variation in travel expenses meeting has been organised to

discuss the issues and to come out with possible solutions and keeping the travel expenses within

the budget.

As per the budget per month travelling cost is $940 and overtime cost is $52.5. The

budget has been prepared reviewing all the travel cost where the business deals. However

discrepancies and ups and downs may be seen due to circumstances. Expenses are passed on

7

providing authentic proof and genuine reasons for the overspendings. Though it is argued that

cost of travelling to Sydney is higher but the other cost such as food and accommodation could

be found at lower rates.

All the allowances as per the budgeted schedule are exclusive of GST. It refers to goods

and service tax applied over goods and services and consumed and to be paid to state authorities.

The allocated amounts are adequate and based after considering overall cost of travel to different

places. Process of submitting expense is also adequate and simple and does not complex and

lengthy procedure for clearance subject to certain conditions.

Allocated overtime payments to the three staff are 300, 250, 315 for the first month.

Overtime rates are calculated after assessing the time spends and including premium over normal

labour rates.

c. Minutes

Meeting for travel expenses held.

ABC held the chair and started agenda.

Discussion on existing allowances

No changes in existing allowance

Overtime payments discussed

Meeting concluded without change in existing allowances.

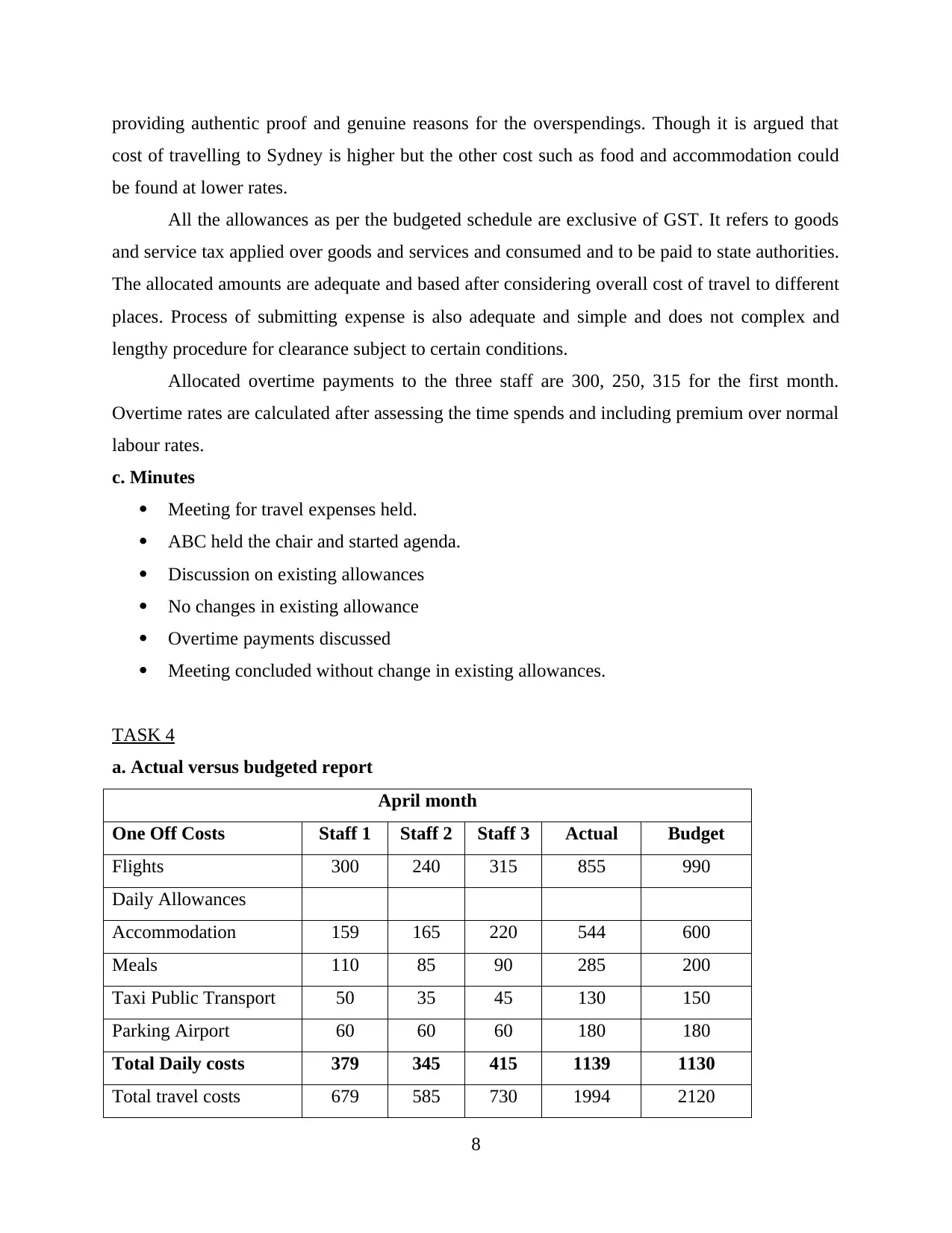

TASK 4

a. Actual versus budgeted report

April month

One Off Costs Staff 1 Staff 2 Staff 3 Actual Budget

Flights 300 240 315 855 990

Daily Allowances

Accommodation 159 165 220 544 600

Meals 110 85 90 285 200

Taxi Public Transport 50 35 45 130 150

Parking Airport 60 60 60 180 180

Total Daily costs 379 345 415 1139 1130

Total travel costs 679 585 730 1994 2120

8

cost of travelling to Sydney is higher but the other cost such as food and accommodation could

be found at lower rates.

All the allowances as per the budgeted schedule are exclusive of GST. It refers to goods

and service tax applied over goods and services and consumed and to be paid to state authorities.

The allocated amounts are adequate and based after considering overall cost of travel to different

places. Process of submitting expense is also adequate and simple and does not complex and

lengthy procedure for clearance subject to certain conditions.

Allocated overtime payments to the three staff are 300, 250, 315 for the first month.

Overtime rates are calculated after assessing the time spends and including premium over normal

labour rates.

c. Minutes

Meeting for travel expenses held.

ABC held the chair and started agenda.

Discussion on existing allowances

No changes in existing allowance

Overtime payments discussed

Meeting concluded without change in existing allowances.

TASK 4

a. Actual versus budgeted report

April month

One Off Costs Staff 1 Staff 2 Staff 3 Actual Budget

Flights 300 240 315 855 990

Daily Allowances

Accommodation 159 165 220 544 600

Meals 110 85 90 285 200

Taxi Public Transport 50 35 45 130 150

Parking Airport 60 60 60 180 180

Total Daily costs 379 345 415 1139 1130

Total travel costs 679 585 730 1994 2120

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Overtime 300 250 385 935 950

Total costs 979 835 1115 2929 3070

b. Travel Expense monthly report

To Finance Manager

It could be evaluated that the travel cost of the staff is increasing due to uncertain

situations. It is essential for the manager to control these increasing costs as this will affect other

factors and increase overall expense. Staff has to ensure that they spend over only necessities and

ensure that optimum use of funds is made as if their own. They have to confirm the manager

before spending over clients like dinners or such other costs. No expenses will be passes if done

without prior permission of manager.

TASK 5

a. Reviewing the travel process

It could be found that budget regarding the accommodation of staff was not included and

breakfast and snacks were not required. In place of separate food expense single meal expense

will be provided and also conveyance will be provided in place of transfer. Other things remain

the same in allocated arrangements.

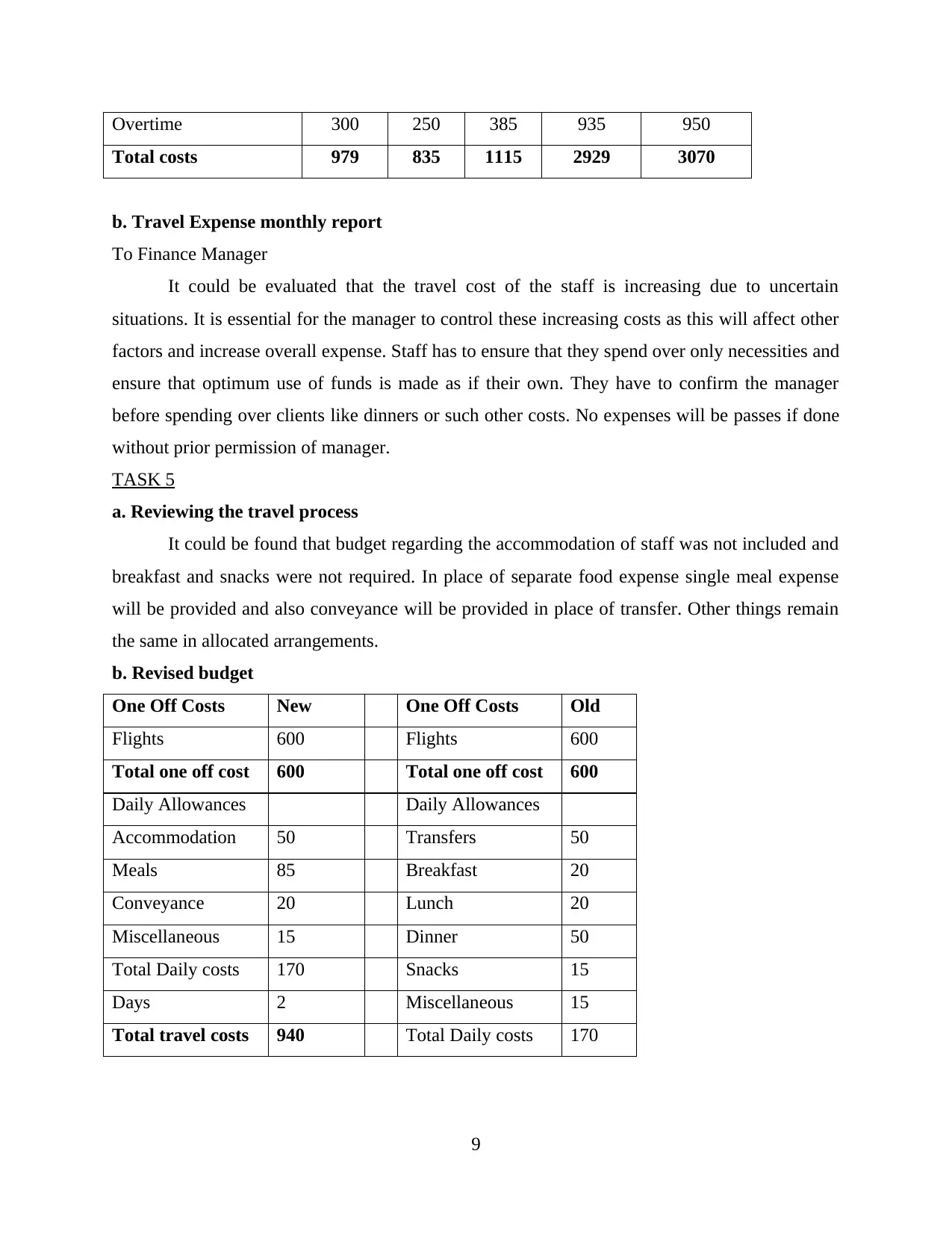

b. Revised budget

One Off Costs New One Off Costs Old

Flights 600 Flights 600

Total one off cost 600 Total one off cost 600

Daily Allowances Daily Allowances

Accommodation 50 Transfers 50

Meals 85 Breakfast 20

Conveyance 20 Lunch 20

Miscellaneous 15 Dinner 50

Total Daily costs 170 Snacks 15

Days 2 Miscellaneous 15

Total travel costs 940 Total Daily costs 170

9

Total costs 979 835 1115 2929 3070

b. Travel Expense monthly report

To Finance Manager

It could be evaluated that the travel cost of the staff is increasing due to uncertain

situations. It is essential for the manager to control these increasing costs as this will affect other

factors and increase overall expense. Staff has to ensure that they spend over only necessities and

ensure that optimum use of funds is made as if their own. They have to confirm the manager

before spending over clients like dinners or such other costs. No expenses will be passes if done

without prior permission of manager.

TASK 5

a. Reviewing the travel process

It could be found that budget regarding the accommodation of staff was not included and

breakfast and snacks were not required. In place of separate food expense single meal expense

will be provided and also conveyance will be provided in place of transfer. Other things remain

the same in allocated arrangements.

b. Revised budget

One Off Costs New One Off Costs Old

Flights 600 Flights 600

Total one off cost 600 Total one off cost 600

Daily Allowances Daily Allowances

Accommodation 50 Transfers 50

Meals 85 Breakfast 20

Conveyance 20 Lunch 20

Miscellaneous 15 Dinner 50

Total Daily costs 170 Snacks 15

Days 2 Miscellaneous 15

Total travel costs 940 Total Daily costs 170

9

Overtime cost per

hour

52.5 Days 2

Total costs 992.5 Total travel costs 940

Overtime cost per

hour

52.5

Total costs 992.5

Variances is seen in accommodation, conveyance and meals which were not provided in

the previous budget. Revised budget will provide about the above mentioned expenses separately

that were causing overspendings. This will require staff to spend within budget and prevent

spending over breakfast as they are provided with accommodation free.

c. Names, roles and responsibilities

Names Roles Responsibilities

Alex Manager To convince staff to spend

within new budget.

James Staff 1 To provide alternate solutions

Samantha Staff 2 To argue against budgeted

allowance

Lisa Staff 3 Asking about based over

actual spending.

d. Meeting

Due to overspendings following process will be followed

Flights will be booked from office with return tickets 2 hrs later from meeting.

Accommodation will be booked by the company.

Cost of meals to be properly invoiced

Conveyance for taxi as charged.

Airport parking fixed

Overtime will be allocated over distance travelled

Budgets have to be managed adequately and followed strictly.

e. Recommendation

10

hour

52.5 Days 2

Total costs 992.5 Total travel costs 940

Overtime cost per

hour

52.5

Total costs 992.5

Variances is seen in accommodation, conveyance and meals which were not provided in

the previous budget. Revised budget will provide about the above mentioned expenses separately

that were causing overspendings. This will require staff to spend within budget and prevent

spending over breakfast as they are provided with accommodation free.

c. Names, roles and responsibilities

Names Roles Responsibilities

Alex Manager To convince staff to spend

within new budget.

James Staff 1 To provide alternate solutions

Samantha Staff 2 To argue against budgeted

allowance

Lisa Staff 3 Asking about based over

actual spending.

d. Meeting

Due to overspendings following process will be followed

Flights will be booked from office with return tickets 2 hrs later from meeting.

Accommodation will be booked by the company.

Cost of meals to be properly invoiced

Conveyance for taxi as charged.

Airport parking fixed

Overtime will be allocated over distance travelled

Budgets have to be managed adequately and followed strictly.

e. Recommendation

10

It is recommended to follow the stated budget by the employees. Also suggestions are

welcomed to make it more manageable within the prescribed limits. Separate allocation of the

expenses will allow staff to properly manage the spending and aggregating meal expense will

allow them to manage as per their wish.

TASK 6

a. In case of contingencies with the interstate travel Finance manager will provide for additional

funds on satisfaction of prescribed conditions. Staff needs to consult manager in case of

contingencies so that most suitable arrangements could be made within the budget.

b. 1 –> In case of additional accommodation the overtime expense rate will be reduced. It will

encourage staff to complete work on time.

2 –> In case of additional conveyance expense it will have to ensure that cost of other travelling

expenses are saves ensuring that overall budget of the three staff does not exceeds.

TASK 7

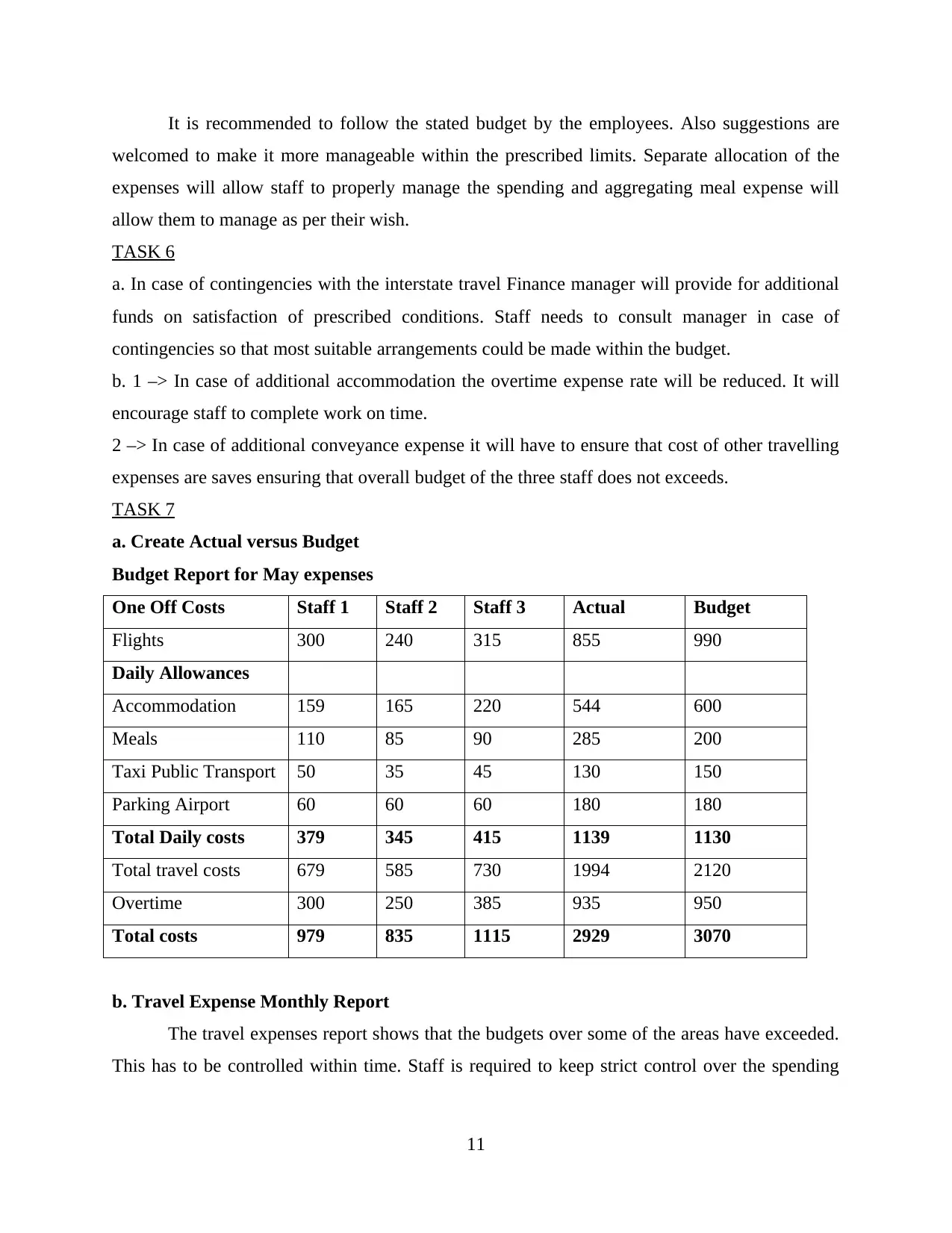

a. Create Actual versus Budget

Budget Report for May expenses

One Off Costs Staff 1 Staff 2 Staff 3 Actual Budget

Flights 300 240 315 855 990

Daily Allowances

Accommodation 159 165 220 544 600

Meals 110 85 90 285 200

Taxi Public Transport 50 35 45 130 150

Parking Airport 60 60 60 180 180

Total Daily costs 379 345 415 1139 1130

Total travel costs 679 585 730 1994 2120

Overtime 300 250 385 935 950

Total costs 979 835 1115 2929 3070

b. Travel Expense Monthly Report

The travel expenses report shows that the budgets over some of the areas have exceeded.

This has to be controlled within time. Staff is required to keep strict control over the spending

11

welcomed to make it more manageable within the prescribed limits. Separate allocation of the

expenses will allow staff to properly manage the spending and aggregating meal expense will

allow them to manage as per their wish.

TASK 6

a. In case of contingencies with the interstate travel Finance manager will provide for additional

funds on satisfaction of prescribed conditions. Staff needs to consult manager in case of

contingencies so that most suitable arrangements could be made within the budget.

b. 1 –> In case of additional accommodation the overtime expense rate will be reduced. It will

encourage staff to complete work on time.

2 –> In case of additional conveyance expense it will have to ensure that cost of other travelling

expenses are saves ensuring that overall budget of the three staff does not exceeds.

TASK 7

a. Create Actual versus Budget

Budget Report for May expenses

One Off Costs Staff 1 Staff 2 Staff 3 Actual Budget

Flights 300 240 315 855 990

Daily Allowances

Accommodation 159 165 220 544 600

Meals 110 85 90 285 200

Taxi Public Transport 50 35 45 130 150

Parking Airport 60 60 60 180 180

Total Daily costs 379 345 415 1139 1130

Total travel costs 679 585 730 1994 2120

Overtime 300 250 385 935 950

Total costs 979 835 1115 2929 3070

b. Travel Expense Monthly Report

The travel expenses report shows that the budgets over some of the areas have exceeded.

This has to be controlled within time. Staff is required to keep strict control over the spending

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and to ensure that it does not exceeds the budget. They have to take prior consultation with

manager before making any expenses that are not essential.

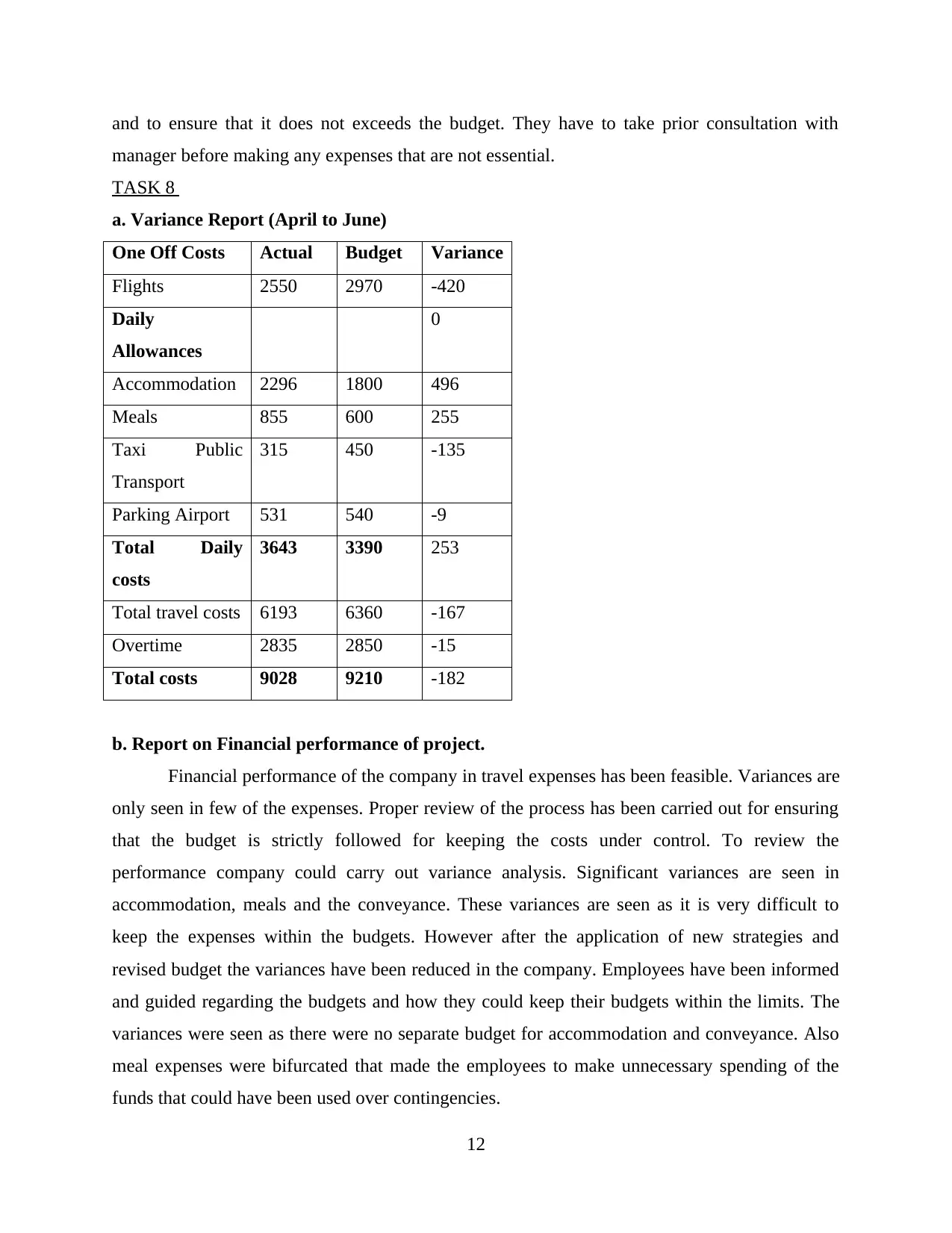

TASK 8

a. Variance Report (April to June)

One Off Costs Actual Budget Variance

Flights 2550 2970 -420

Daily

Allowances

0

Accommodation 2296 1800 496

Meals 855 600 255

Taxi Public

Transport

315 450 -135

Parking Airport 531 540 -9

Total Daily

costs

3643 3390 253

Total travel costs 6193 6360 -167

Overtime 2835 2850 -15

Total costs 9028 9210 -182

b. Report on Financial performance of project.

Financial performance of the company in travel expenses has been feasible. Variances are

only seen in few of the expenses. Proper review of the process has been carried out for ensuring

that the budget is strictly followed for keeping the costs under control. To review the

performance company could carry out variance analysis. Significant variances are seen in

accommodation, meals and the conveyance. These variances are seen as it is very difficult to

keep the expenses within the budgets. However after the application of new strategies and

revised budget the variances have been reduced in the company. Employees have been informed

and guided regarding the budgets and how they could keep their budgets within the limits. The

variances were seen as there were no separate budget for accommodation and conveyance. Also

meal expenses were bifurcated that made the employees to make unnecessary spending of the

funds that could have been used over contingencies.

12

manager before making any expenses that are not essential.

TASK 8

a. Variance Report (April to June)

One Off Costs Actual Budget Variance

Flights 2550 2970 -420

Daily

Allowances

0

Accommodation 2296 1800 496

Meals 855 600 255

Taxi Public

Transport

315 450 -135

Parking Airport 531 540 -9

Total Daily

costs

3643 3390 253

Total travel costs 6193 6360 -167

Overtime 2835 2850 -15

Total costs 9028 9210 -182

b. Report on Financial performance of project.

Financial performance of the company in travel expenses has been feasible. Variances are

only seen in few of the expenses. Proper review of the process has been carried out for ensuring

that the budget is strictly followed for keeping the costs under control. To review the

performance company could carry out variance analysis. Significant variances are seen in

accommodation, meals and the conveyance. These variances are seen as it is very difficult to

keep the expenses within the budgets. However after the application of new strategies and

revised budget the variances have been reduced in the company. Employees have been informed

and guided regarding the budgets and how they could keep their budgets within the limits. The

variances were seen as there were no separate budget for accommodation and conveyance. Also

meal expenses were bifurcated that made the employees to make unnecessary spending of the

funds that could have been used over contingencies.

12

ASSESSMENT 3

Case Study 1

TASK 1

Monitor and control finances

Review of the Nerdus Budget Variance Report

a. Positive and negative financial performance outcomes

Variance analysis is conducted by the organisation to verify the budgeted transactions of

company during the year. This helps the company to identify areas of improvement so that

corrective actions and measures can be taken for the same to reduce the variances.

Positive Outcomes

From the budget variance report of Nerdus it could be identified that it has achieved

higher sales in Victorian as against the budgeted figures. This has made the increase in total sales

from the budget which is not achieved by any other region. Cost of sales of Western Australia

has shown decline from budgets that shows it has been successful in managing the costs. Control

over cost is only achieved by Western Australia.

Negative outcomes

It could be evaluated from the budget report that South Australia has not achieved the

budgeted sales level that shows negative variance. Western Australia has sales exactly up to the

budgeted figures. On the other cost of sales of Victorian has increased from the budgeted figures.

The increased is also due to the higher sales as compared with the budget. Therefore the increase

in cost will be adjusted by the increased sales. There is no increase in total sales of Nerdus.

Departments have not been able to reach the sales targets with reduced cost of sales.

b. Negative and positive financial performance trends

It is essential for the business to identify the positive and negative performance of the

business. This enables the management to identify whether the strategies established are working

or not so that corrective measures could be taken.

Positive financial performance

It could be analysed that the management has shown positive outcomes from some of the

region sales. South Australia has shown positive results as variances are reduced in the 2nd month

13

Case Study 1

TASK 1

Monitor and control finances

Review of the Nerdus Budget Variance Report

a. Positive and negative financial performance outcomes

Variance analysis is conducted by the organisation to verify the budgeted transactions of

company during the year. This helps the company to identify areas of improvement so that

corrective actions and measures can be taken for the same to reduce the variances.

Positive Outcomes

From the budget variance report of Nerdus it could be identified that it has achieved

higher sales in Victorian as against the budgeted figures. This has made the increase in total sales

from the budget which is not achieved by any other region. Cost of sales of Western Australia

has shown decline from budgets that shows it has been successful in managing the costs. Control

over cost is only achieved by Western Australia.

Negative outcomes

It could be evaluated from the budget report that South Australia has not achieved the

budgeted sales level that shows negative variance. Western Australia has sales exactly up to the

budgeted figures. On the other cost of sales of Victorian has increased from the budgeted figures.

The increased is also due to the higher sales as compared with the budget. Therefore the increase

in cost will be adjusted by the increased sales. There is no increase in total sales of Nerdus.

Departments have not been able to reach the sales targets with reduced cost of sales.

b. Negative and positive financial performance trends

It is essential for the business to identify the positive and negative performance of the

business. This enables the management to identify whether the strategies established are working

or not so that corrective measures could be taken.

Positive financial performance

It could be analysed that the management has shown positive outcomes from some of the

region sales. South Australia has shown positive results as variances are reduced in the 2nd month

13

by application of improvement measures. It could be seen that the sales level of Victoria is

showing rising trend and achieved even higher sales. Over the two months negative variance has

turned positive due to increase in sales from Victoria. Cost of sales of WA have not been

controlled they are negative over both the months It could be identified that total cost of sales

have zero variance over the 2nd month that shows positive trend.

Negative performance trend

Variances have not reduced to considerable extent of SA.. It could be seen that negative

trend is not seen in other regions. Cost of sales of Victoria has shown negative trend.

Performance of company is good as negative trend is only seen in Western Australia. In the

previous month Nerdus was having negative variance in total sales as well as total cost.

c. Contingency plans to implement across the groups.

Contingency plan is prepared by the organisation for situations where company is not

achieving the planned objectives. From the trends of South Australia it could be identified that

sales variance is reducing. It has to make new promotions for the sales of units over the region.

Sales of Victoria is increasing every month for which it has to increase its capacity to meet the

high demand of units. This will enable the company to achieve the target sales level. Same plans

have to be implemented over Western Australia.

To achieve the budgeted cost of regions it has to increase the budgets for Victoria as sales

are increasing every month that increases the cost of sales. Proper control over processes will be

taken to ensure that costs are controlled. The contingency planning will enable the company to

achieve the region totals by effectively managing the variances if any occurs in the regions.

Increase in variance of one region will set off the other adequately as per the contingency plan.

d. Report to manager

Sales performance of Victoria

It could be analysed that the Sales of Victoria is showing positive trend over two months.

This has been achieved due to the new strategies undertaken for increasing the revenues and

sales. Region is expecting further increase in sales from the market analysis for which it has to

increase the capacity. Due to increased demand cost of materials is charged at higher rates.

Therefore, it is planning to buy 20% higher raw materials and other equipments so that costs

could be controlled and variances could be managed by the region.

14

showing rising trend and achieved even higher sales. Over the two months negative variance has

turned positive due to increase in sales from Victoria. Cost of sales of WA have not been

controlled they are negative over both the months It could be identified that total cost of sales

have zero variance over the 2nd month that shows positive trend.

Negative performance trend

Variances have not reduced to considerable extent of SA.. It could be seen that negative

trend is not seen in other regions. Cost of sales of Victoria has shown negative trend.

Performance of company is good as negative trend is only seen in Western Australia. In the

previous month Nerdus was having negative variance in total sales as well as total cost.

c. Contingency plans to implement across the groups.

Contingency plan is prepared by the organisation for situations where company is not

achieving the planned objectives. From the trends of South Australia it could be identified that

sales variance is reducing. It has to make new promotions for the sales of units over the region.

Sales of Victoria is increasing every month for which it has to increase its capacity to meet the

high demand of units. This will enable the company to achieve the target sales level. Same plans

have to be implemented over Western Australia.

To achieve the budgeted cost of regions it has to increase the budgets for Victoria as sales

are increasing every month that increases the cost of sales. Proper control over processes will be

taken to ensure that costs are controlled. The contingency planning will enable the company to

achieve the region totals by effectively managing the variances if any occurs in the regions.

Increase in variance of one region will set off the other adequately as per the contingency plan.

d. Report to manager

Sales performance of Victoria

It could be analysed that the Sales of Victoria is showing positive trend over two months.

This has been achieved due to the new strategies undertaken for increasing the revenues and

sales. Region is expecting further increase in sales from the market analysis for which it has to

increase the capacity. Due to increased demand cost of materials is charged at higher rates.

Therefore, it is planning to buy 20% higher raw materials and other equipments so that costs

could be controlled and variances could be managed by the region.

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TASK 2

Review and evaluation of financial management

Budget variance report provides about the variances between the budgeted and actual

figures. The report helps the management in identifying the areas that are working effectively

and those showing variances so that effective measures could be taken. There are also other

reports that enable the management in improving the financial management process.

Two reports that could be developed and used for improving financial performance of company

are cost reports and break even analysis report.

Cost report provides about the cost information of all the expenses carried out by company

related to the product. Cost report enables the management to identify the different costs that are

incurred for producing the units or services. Using the cost information management could

identify the areas where costs are increasing or unproductive costs. It will focus over eliminating

the unproductive cost of the firm. Controlling the cost it could make advertisement and

promotions for the sales of product. This will help company to achieve the sales budgets.

Promotions and advertisements could be made by reducing cost from unproductive expenses.

Report will also help the managers to make effective utilisation of the resources over the period

that will enable the company to increase its productivity and efficiency. Complete information

about the variable and fixed costs could be evaluated to identify the cost of each expense.

Break even report provides about the sales level required for covering the cost. it is

prepared by the organisation to analyse the sales level at which cost are equal to the revenues.

This is point where there is no profit or loss. The report could be used by the management to

decide the profit margins for the products and services. Using the break even point manager will

frame the strategies and policies that will enable it to achieve the sales level. It will help manager

in making promotions for the product and services to achieve the sales. Report is very useful as

without knowing the sales required to be achieved they cannot make strategies to achieve the

sales level. The report helps manager to analyse the processes to ensure that production is cost

effective so that prices are reasonable.

Case Study 2

Review of the Operating budget

a. Sales results of Oct-Dec 2015 and effects of sales over financial cash flow.

It could be seen that the sales level of company shows increasing trend over the period.

15

Review and evaluation of financial management

Budget variance report provides about the variances between the budgeted and actual

figures. The report helps the management in identifying the areas that are working effectively

and those showing variances so that effective measures could be taken. There are also other

reports that enable the management in improving the financial management process.

Two reports that could be developed and used for improving financial performance of company

are cost reports and break even analysis report.

Cost report provides about the cost information of all the expenses carried out by company

related to the product. Cost report enables the management to identify the different costs that are

incurred for producing the units or services. Using the cost information management could

identify the areas where costs are increasing or unproductive costs. It will focus over eliminating

the unproductive cost of the firm. Controlling the cost it could make advertisement and

promotions for the sales of product. This will help company to achieve the sales budgets.

Promotions and advertisements could be made by reducing cost from unproductive expenses.

Report will also help the managers to make effective utilisation of the resources over the period

that will enable the company to increase its productivity and efficiency. Complete information

about the variable and fixed costs could be evaluated to identify the cost of each expense.

Break even report provides about the sales level required for covering the cost. it is

prepared by the organisation to analyse the sales level at which cost are equal to the revenues.

This is point where there is no profit or loss. The report could be used by the management to

decide the profit margins for the products and services. Using the break even point manager will

frame the strategies and policies that will enable it to achieve the sales level. It will help manager

in making promotions for the product and services to achieve the sales. Report is very useful as

without knowing the sales required to be achieved they cannot make strategies to achieve the

sales level. The report helps manager to analyse the processes to ensure that production is cost

effective so that prices are reasonable.

Case Study 2

Review of the Operating budget

a. Sales results of Oct-Dec 2015 and effects of sales over financial cash flow.

It could be seen that the sales level of company shows increasing trend over the period.

15

There are highest sales in month of December and proportion of credit sales is higher in

November.

Sales of a company significantly affect the cash flows of business. Sales generate cash

inflows that are essential for meeting the expenses and costs. Without adequate sales level it will

not generate funds to run the operations of business enterprise adequately. If the adequate level

of sales are not generated all the operations are disrupted of the organisation. It will not be able

to meet the expenses and have effective cash flows if it is not able to have required level of sales.

Cash flows can go negative if the cash inflows are not adequate of the firm.

b. Costs of Oct-Dec 2015

Cost of sales is increasing with the same proportion as that of sales over the period Oct-

Dec 2015.

There is significant control over the cost of sales as major fluctuations are not seen in the

cost due to change in sales level.

c. Two variable and fixed costs

Two variable costs

I. Light, power and heat

II. Wages

Two Fixed costs

I. Insurance

II. Rent

d. Variances between the actual of 2015 and budget of 2016.

Two variances between actual of Oct-Dec 2015 and budget of Oct-Dec 2016

1. Total Revenues

Actual – 74381 92890 119288

Budget – 100000 100000 175000

Variance – 25691 7110 55712

2. Total cost of sales

Actual – 28580 42328 52800

Budget – 52000 52000 95000

Variance – 23420 9672 42200

16

November.

Sales of a company significantly affect the cash flows of business. Sales generate cash

inflows that are essential for meeting the expenses and costs. Without adequate sales level it will

not generate funds to run the operations of business enterprise adequately. If the adequate level

of sales are not generated all the operations are disrupted of the organisation. It will not be able

to meet the expenses and have effective cash flows if it is not able to have required level of sales.

Cash flows can go negative if the cash inflows are not adequate of the firm.

b. Costs of Oct-Dec 2015

Cost of sales is increasing with the same proportion as that of sales over the period Oct-

Dec 2015.

There is significant control over the cost of sales as major fluctuations are not seen in the

cost due to change in sales level.

c. Two variable and fixed costs

Two variable costs

I. Light, power and heat

II. Wages

Two Fixed costs

I. Insurance

II. Rent

d. Variances between the actual of 2015 and budget of 2016.

Two variances between actual of Oct-Dec 2015 and budget of Oct-Dec 2016

1. Total Revenues

Actual – 74381 92890 119288

Budget – 100000 100000 175000

Variance – 25691 7110 55712

2. Total cost of sales

Actual – 28580 42328 52800

Budget – 52000 52000 95000

Variance – 23420 9672 42200

16

e. Prioritising recommendation

First and foremost it has to enhance the marketing strategies for achieving the budgeted

level of sales.

Cost of sales is showing significant variations it has to maintain control over the costs.

It has to maintain effective control over operating expenses as increase in variance will

case significant variations and decrease the profit levels.

There is considerable variation in gross profit margins and net profits for which it is

required to take strategic decisions.

17

First and foremost it has to enhance the marketing strategies for achieving the budgeted

level of sales.

Cost of sales is showing significant variations it has to maintain control over the costs.

It has to maintain effective control over operating expenses as increase in variance will

case significant variations and decrease the profit levels.

There is considerable variation in gross profit margins and net profits for which it is

required to take strategic decisions.

17

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.