Manage Budgets, Project Costs & Financial Plans

VerifiedAdded on 2023/01/11

|10

|1691

|38

AI Summary

This document provides guidance on managing budgets, project costs, and financial plans. It includes practical budget applications, budgeted profit & loss analysis, capital budgeting, and budget variance reports. The document also discusses factors influencing the budget, monitoring techniques, and risk analysis. The subject of the document is Finance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGE BUDGETS,

PROJECT COSTS &

FINANCIAL PLANS

PROJECT COSTS &

FINANCIAL PLANS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

PART D...........................................................................................................................................1

PRACTICAL BUDGET APPLICATION.......................................................................................1

1. Budget showing income for the period....................................................................................1

2. Budget showing expenses for the period.................................................................................1

PART E............................................................................................................................................3

BUDGETED PROFIT & LOSS......................................................................................................3

1...................................................................................................................................................3

2...................................................................................................................................................4

3...................................................................................................................................................4

4...................................................................................................................................................4

5...................................................................................................................................................4

6...................................................................................................................................................4

7...................................................................................................................................................4

CAPITAL BUDGETING................................................................................................................5

8...................................................................................................................................................5

9...................................................................................................................................................5

BUDGET VARIANCE REPORT...................................................................................................5

10.................................................................................................................................................5

11.................................................................................................................................................5

12.................................................................................................................................................5

13.................................................................................................................................................6

REFERENCES................................................................................................................................7

APPENDICES.................................................................................................................................8

1st Criteria.....................................................................................................................................8

2nd Criteria....................................................................................................................................8

3rd Criteria....................................................................................................................................9

TABLE OF CONTENTS................................................................................................................2

PART D...........................................................................................................................................1

PRACTICAL BUDGET APPLICATION.......................................................................................1

1. Budget showing income for the period....................................................................................1

2. Budget showing expenses for the period.................................................................................1

PART E............................................................................................................................................3

BUDGETED PROFIT & LOSS......................................................................................................3

1...................................................................................................................................................3

2...................................................................................................................................................4

3...................................................................................................................................................4

4...................................................................................................................................................4

5...................................................................................................................................................4

6...................................................................................................................................................4

7...................................................................................................................................................4

CAPITAL BUDGETING................................................................................................................5

8...................................................................................................................................................5

9...................................................................................................................................................5

BUDGET VARIANCE REPORT...................................................................................................5

10.................................................................................................................................................5

11.................................................................................................................................................5

12.................................................................................................................................................5

13.................................................................................................................................................6

REFERENCES................................................................................................................................7

APPENDICES.................................................................................................................................8

1st Criteria.....................................................................................................................................8

2nd Criteria....................................................................................................................................8

3rd Criteria....................................................................................................................................9

PART D

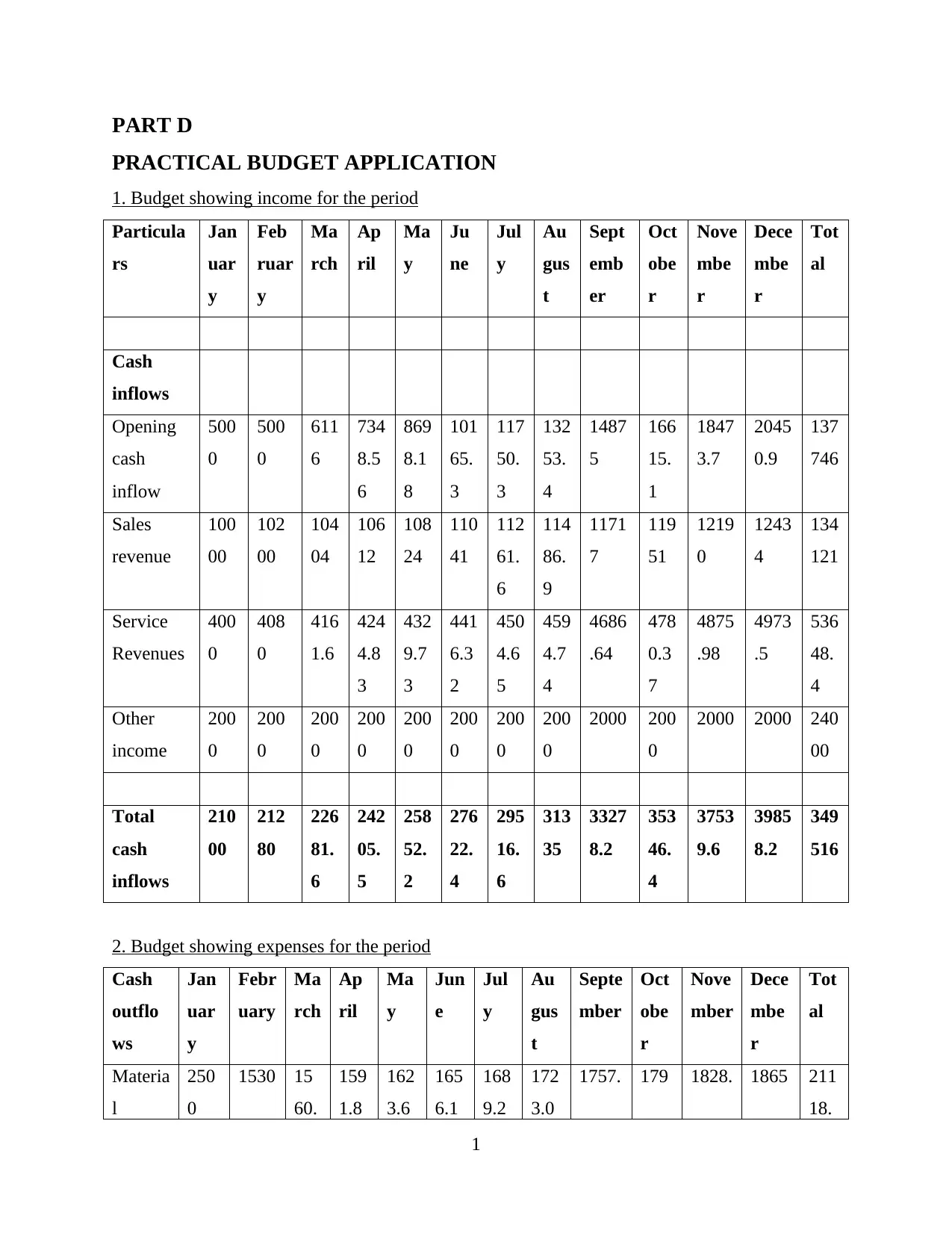

PRACTICAL BUDGET APPLICATION

1. Budget showing income for the period

Particula

rs

Jan

uar

y

Feb

ruar

y

Ma

rch

Ap

ril

Ma

y

Ju

ne

Jul

y

Au

gus

t

Sept

emb

er

Oct

obe

r

Nove

mbe

r

Dece

mbe

r

Tot

al

Cash

inflows

Opening

cash

inflow

500

0

500

0

611

6

734

8.5

6

869

8.1

8

101

65.

3

117

50.

3

132

53.

4

1487

5

166

15.

1

1847

3.7

2045

0.9

137

746

Sales

revenue

100

00

102

00

104

04

106

12

108

24

110

41

112

61.

6

114

86.

9

1171

7

119

51

1219

0

1243

4

134

121

Service

Revenues

400

0

408

0

416

1.6

424

4.8

3

432

9.7

3

441

6.3

2

450

4.6

5

459

4.7

4

4686

.64

478

0.3

7

4875

.98

4973

.5

536

48.

4

Other

income

200

0

200

0

200

0

200

0

200

0

200

0

200

0

200

0

2000 200

0

2000 2000 240

00

Total

cash

inflows

210

00

212

80

226

81.

6

242

05.

5

258

52.

2

276

22.

4

295

16.

6

313

35

3327

8.2

353

46.

4

3753

9.6

3985

8.2

349

516

2. Budget showing expenses for the period

Cash

outflo

ws

Jan

uar

y

Febr

uary

Ma

rch

Ap

ril

Ma

y

Jun

e

Jul

y

Au

gus

t

Septe

mber

Oct

obe

r

Nove

mber

Dece

mbe

r

Tot

al

Materia

l

250

0

1530 15

60.

159

1.8

162

3.6

165

6.1

168

9.2

172

3.0

1757. 179 1828. 1865 211

18.

1

PRACTICAL BUDGET APPLICATION

1. Budget showing income for the period

Particula

rs

Jan

uar

y

Feb

ruar

y

Ma

rch

Ap

ril

Ma

y

Ju

ne

Jul

y

Au

gus

t

Sept

emb

er

Oct

obe

r

Nove

mbe

r

Dece

mbe

r

Tot

al

Cash

inflows

Opening

cash

inflow

500

0

500

0

611

6

734

8.5

6

869

8.1

8

101

65.

3

117

50.

3

132

53.

4

1487

5

166

15.

1

1847

3.7

2045

0.9

137

746

Sales

revenue

100

00

102

00

104

04

106

12

108

24

110

41

112

61.

6

114

86.

9

1171

7

119

51

1219

0

1243

4

134

121

Service

Revenues

400

0

408

0

416

1.6

424

4.8

3

432

9.7

3

441

6.3

2

450

4.6

5

459

4.7

4

4686

.64

478

0.3

7

4875

.98

4973

.5

536

48.

4

Other

income

200

0

200

0

200

0

200

0

200

0

200

0

200

0

200

0

2000 200

0

2000 2000 240

00

Total

cash

inflows

210

00

212

80

226

81.

6

242

05.

5

258

52.

2

276

22.

4

295

16.

6

313

35

3327

8.2

353

46.

4

3753

9.6

3985

8.2

349

516

2. Budget showing expenses for the period

Cash

outflo

ws

Jan

uar

y

Febr

uary

Ma

rch

Ap

ril

Ma

y

Jun

e

Jul

y

Au

gus

t

Septe

mber

Oct

obe

r

Nove

mber

Dece

mbe

r

Tot

al

Materia

l

250

0

1530 15

60.

159

1.8

162

3.6

165

6.1

168

9.2

172

3.0

1757. 179 1828. 1865 211

18.

1

6 1 5 2 4 3 49 2.64 49 .06 1

Labour 200

0

2000 20

00

200

0

200

0

200

0

220

0

220

0

2200 220

0

2200 2200 252

00

Variabl

e

overhe

ad

150

0

1530 15

60.

6

159

1.8

1

162

3.6

5

165

6.1

2

168

9.2

4

172

3.0

3

1757.

49

179

2.64

1828.

49

1865

.06

201

18.

1

Fixed

overhe

ads

300

0

3000 30

00

300

0

300

0

300

0

300

0

300

0

3000 300

0

3000 3000 360

00

Other

expens

es

220

0

2288 23

80

247

5

257

4

267

7

278

3.7

289

5

3011 313

1

3257 3387 330

56.

8

Selling

and

Distrib

ution

800 816 83

2.3

2

848

.96

6

865

.94

6

883

.26

5

900

.93

918

.94

9

937.3

28

956.

074

975.1

96

994.

699

107

29.

7

Admini

stration

expens

es

400

0

4000 40

00

400

0

400

0

400

0

400

0

400

0

4000 400

0

4000 4000 480

00

Total

cash

outflo

ws

160

00

1516

4

15

33

3

155

07.

3

156

86.

9

158

72.

1

162

63.

1

164

60.

1

1666

3.2

168

72.6

1708

8.7

1731

1.6

194

223

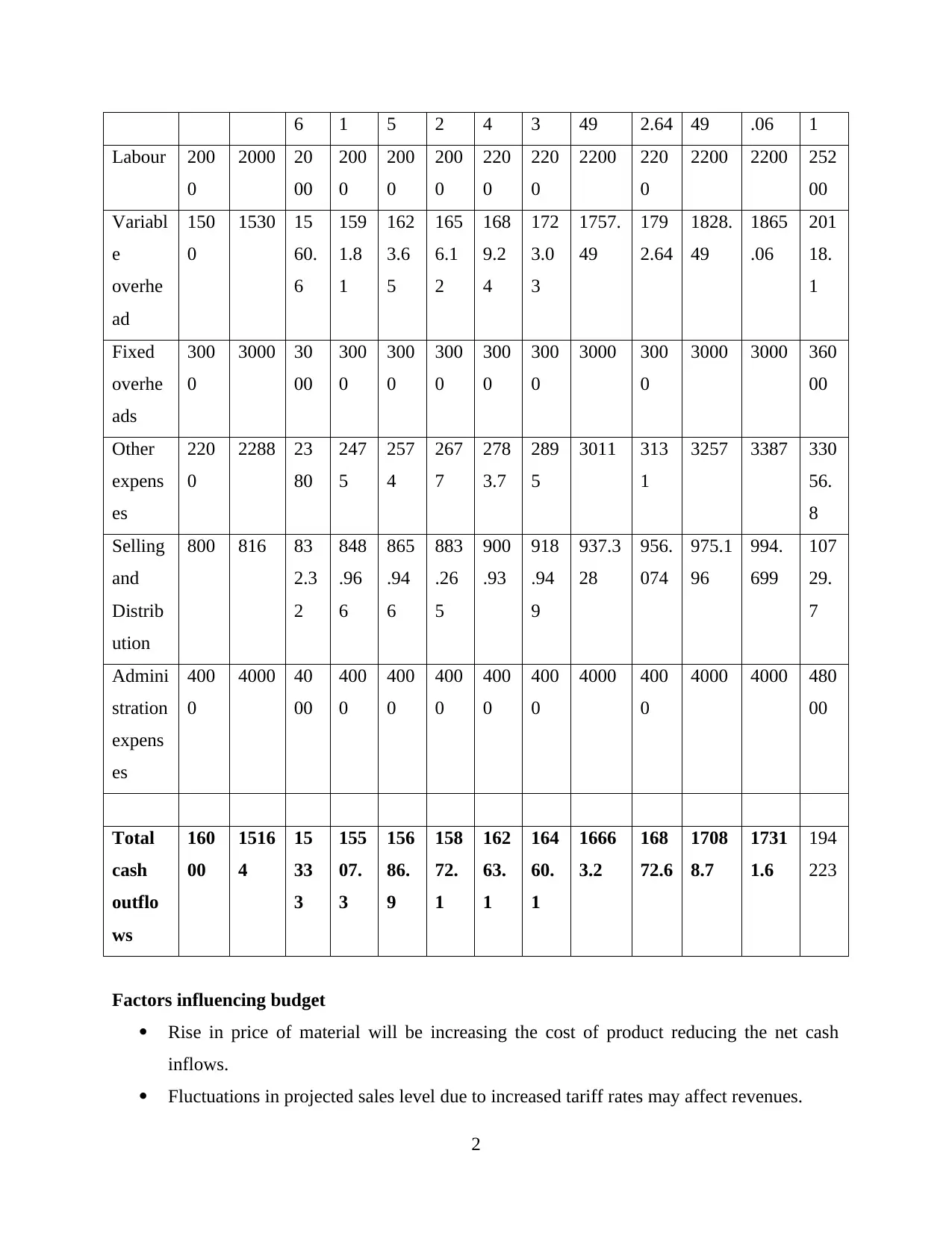

Factors influencing budget

Rise in price of material will be increasing the cost of product reducing the net cash

inflows.

Fluctuations in projected sales level due to increased tariff rates may affect revenues.

2

Labour 200

0

2000 20

00

200

0

200

0

200

0

220

0

220

0

2200 220

0

2200 2200 252

00

Variabl

e

overhe

ad

150

0

1530 15

60.

6

159

1.8

1

162

3.6

5

165

6.1

2

168

9.2

4

172

3.0

3

1757.

49

179

2.64

1828.

49

1865

.06

201

18.

1

Fixed

overhe

ads

300

0

3000 30

00

300

0

300

0

300

0

300

0

300

0

3000 300

0

3000 3000 360

00

Other

expens

es

220

0

2288 23

80

247

5

257

4

267

7

278

3.7

289

5

3011 313

1

3257 3387 330

56.

8

Selling

and

Distrib

ution

800 816 83

2.3

2

848

.96

6

865

.94

6

883

.26

5

900

.93

918

.94

9

937.3

28

956.

074

975.1

96

994.

699

107

29.

7

Admini

stration

expens

es

400

0

4000 40

00

400

0

400

0

400

0

400

0

400

0

4000 400

0

4000 4000 480

00

Total

cash

outflo

ws

160

00

1516

4

15

33

3

155

07.

3

156

86.

9

158

72.

1

162

63.

1

164

60.

1

1666

3.2

168

72.6

1708

8.7

1731

1.6

194

223

Factors influencing budget

Rise in price of material will be increasing the cost of product reducing the net cash

inflows.

Fluctuations in projected sales level due to increased tariff rates may affect revenues.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

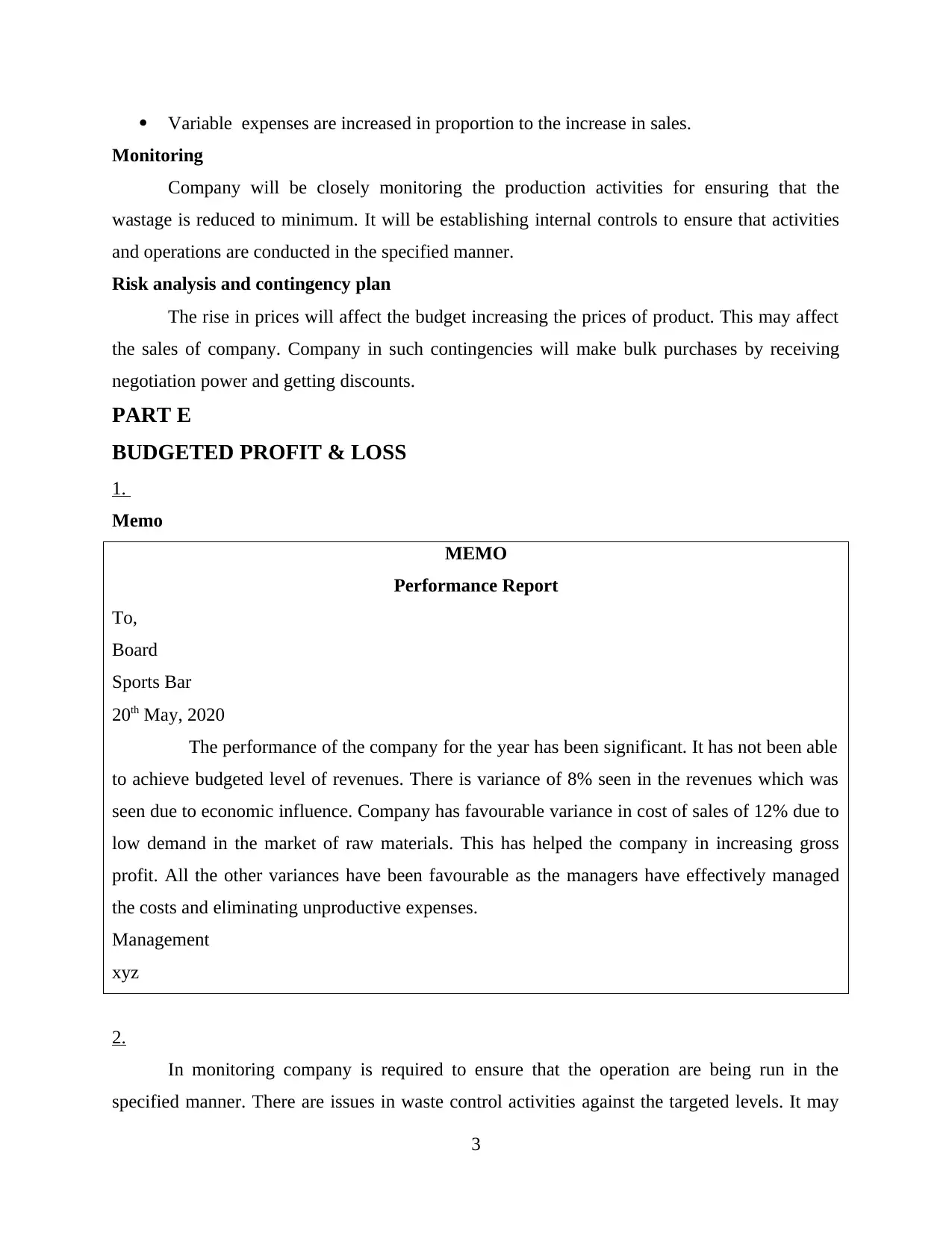

Variable expenses are increased in proportion to the increase in sales.

Monitoring

Company will be closely monitoring the production activities for ensuring that the

wastage is reduced to minimum. It will be establishing internal controls to ensure that activities

and operations are conducted in the specified manner.

Risk analysis and contingency plan

The rise in prices will affect the budget increasing the prices of product. This may affect

the sales of company. Company in such contingencies will make bulk purchases by receiving

negotiation power and getting discounts.

PART E

BUDGETED PROFIT & LOSS

1.

Memo

MEMO

Performance Report

To,

Board

Sports Bar

20th May, 2020

The performance of the company for the year has been significant. It has not been able

to achieve budgeted level of revenues. There is variance of 8% seen in the revenues which was

seen due to economic influence. Company has favourable variance in cost of sales of 12% due to

low demand in the market of raw materials. This has helped the company in increasing gross

profit. All the other variances have been favourable as the managers have effectively managed

the costs and eliminating unproductive expenses.

Management

xyz

2.

In monitoring company is required to ensure that the operation are being run in the

specified manner. There are issues in waste control activities against the targeted levels. It may

3

Monitoring

Company will be closely monitoring the production activities for ensuring that the

wastage is reduced to minimum. It will be establishing internal controls to ensure that activities

and operations are conducted in the specified manner.

Risk analysis and contingency plan

The rise in prices will affect the budget increasing the prices of product. This may affect

the sales of company. Company in such contingencies will make bulk purchases by receiving

negotiation power and getting discounts.

PART E

BUDGETED PROFIT & LOSS

1.

Memo

MEMO

Performance Report

To,

Board

Sports Bar

20th May, 2020

The performance of the company for the year has been significant. It has not been able

to achieve budgeted level of revenues. There is variance of 8% seen in the revenues which was

seen due to economic influence. Company has favourable variance in cost of sales of 12% due to

low demand in the market of raw materials. This has helped the company in increasing gross

profit. All the other variances have been favourable as the managers have effectively managed

the costs and eliminating unproductive expenses.

Management

xyz

2.

In monitoring company is required to ensure that the operation are being run in the

specified manner. There are issues in waste control activities against the targeted levels. It may

3

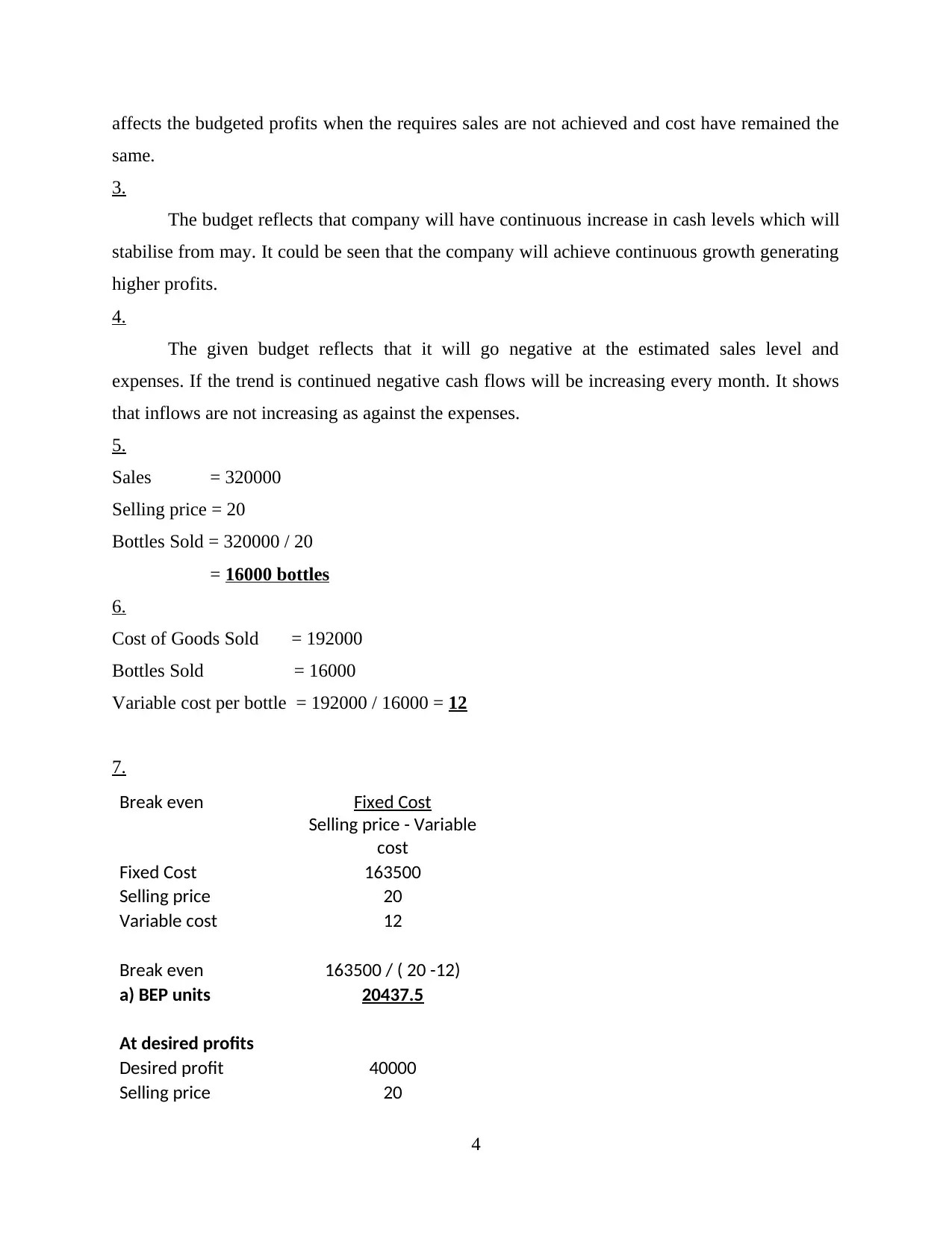

affects the budgeted profits when the requires sales are not achieved and cost have remained the

same.

3.

The budget reflects that company will have continuous increase in cash levels which will

stabilise from may. It could be seen that the company will achieve continuous growth generating

higher profits.

4.

The given budget reflects that it will go negative at the estimated sales level and

expenses. If the trend is continued negative cash flows will be increasing every month. It shows

that inflows are not increasing as against the expenses.

5.

Sales = 320000

Selling price = 20

Bottles Sold = 320000 / 20

= 16000 bottles

6.

Cost of Goods Sold = 192000

Bottles Sold = 16000

Variable cost per bottle = 192000 / 16000 = 12

7.

Break even Fixed Cost

Selling price - Variable

cost

Fixed Cost 163500

Selling price 20

Variable cost 12

Break even 163500 / ( 20 -12)

a) BEP units 20437.5

At desired profits

Desired profit 40000

Selling price 20

4

same.

3.

The budget reflects that company will have continuous increase in cash levels which will

stabilise from may. It could be seen that the company will achieve continuous growth generating

higher profits.

4.

The given budget reflects that it will go negative at the estimated sales level and

expenses. If the trend is continued negative cash flows will be increasing every month. It shows

that inflows are not increasing as against the expenses.

5.

Sales = 320000

Selling price = 20

Bottles Sold = 320000 / 20

= 16000 bottles

6.

Cost of Goods Sold = 192000

Bottles Sold = 16000

Variable cost per bottle = 192000 / 16000 = 12

7.

Break even Fixed Cost

Selling price - Variable

cost

Fixed Cost 163500

Selling price 20

Variable cost 12

Break even 163500 / ( 20 -12)

a) BEP units 20437.5

At desired profits

Desired profit 40000

Selling price 20

4

Variable cost 12

Break even units 20437

[40000/(20-12)]+20437

b) Required Bottles 25437

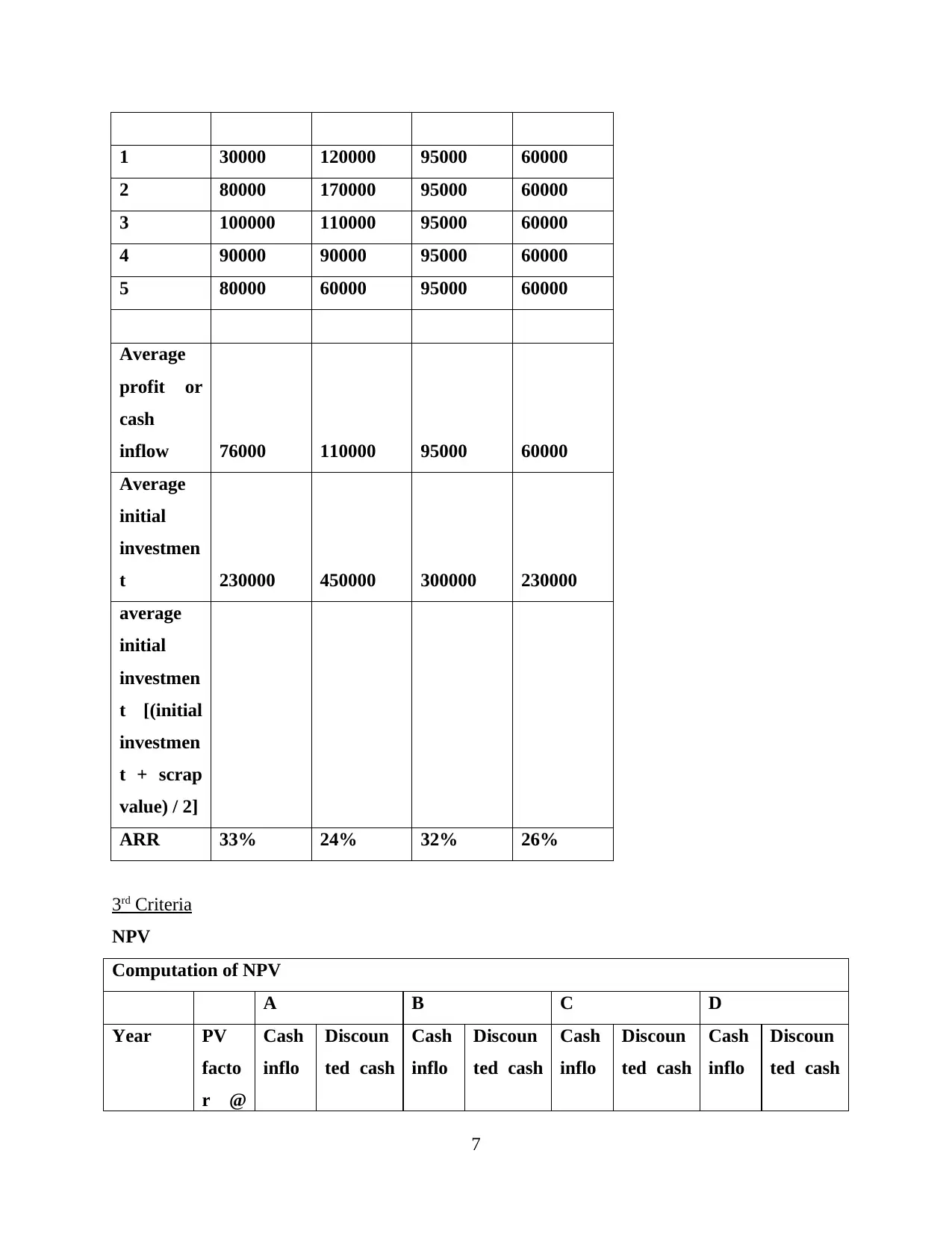

CAPITAL BUDGETING

A B C D

Payback period 3.4 3.5 3.2 3.8

ARR 33% 24% 32% 26%

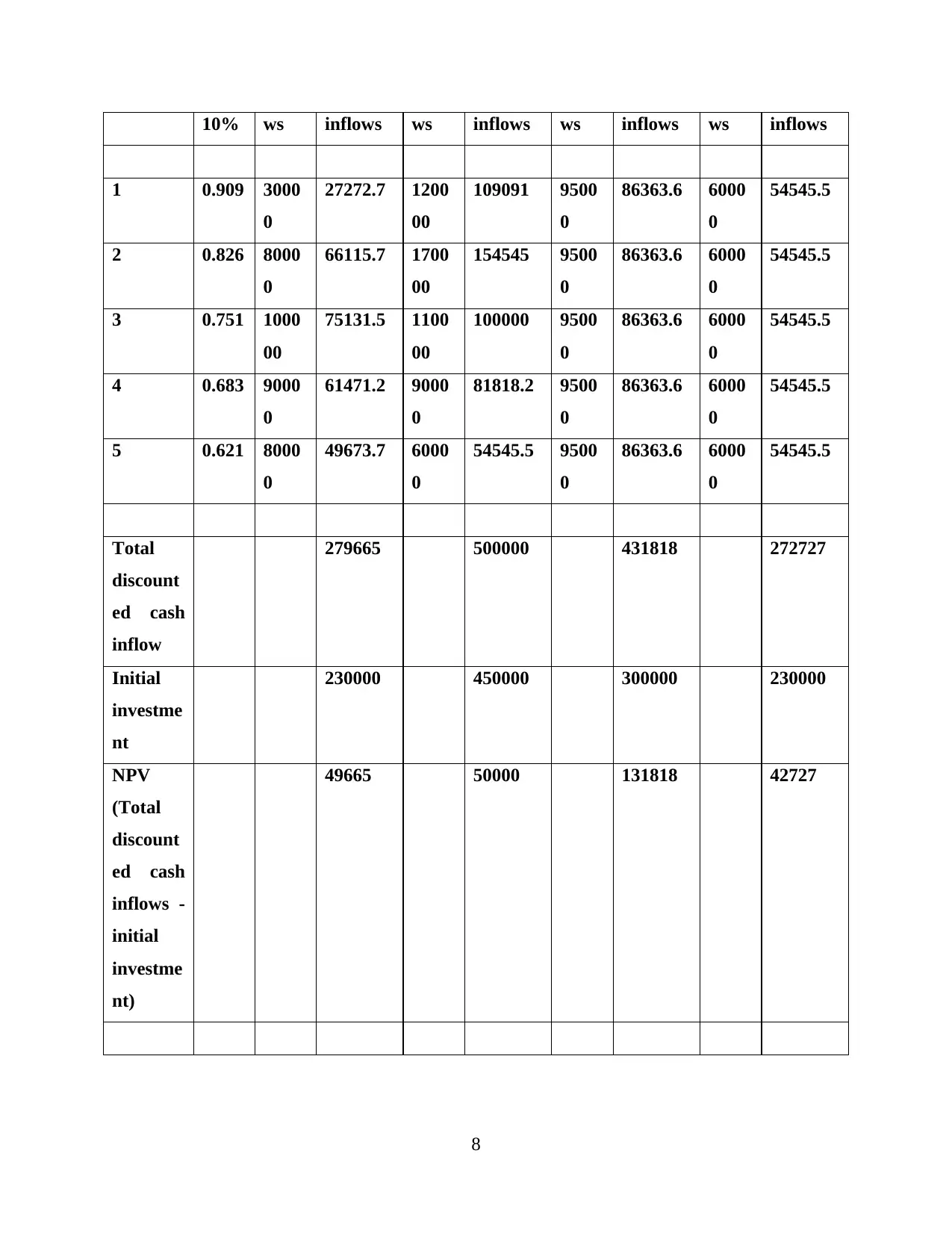

NPV 49665 50000 131818 42727

8.

Given the virtually unlimited funds Proposals A, B & C pass the criteria.

9.

Given virtually limited funds company should accept Proposal C.

BUDGET VARIANCE REPORT

10.

Report shows that the variances are adverse and there is adverse variation of 20% in sales

and 48% in operating profit even after a favourable variance in gross profit due to significant

increase in advertising cost.

11.

Company should is required to put more focus over cost of sales by adopting cost

efficient strategies as advertising is essential for promoting the sales.

12.

Report shows healthy performance as the sales are higher than the budgeted and it has

maintained effective control over cost of goods sold. The efficient management of operational

activities has helped in achieving profits higher than budgeted.

13.

Company is required to increase its production as the meeting demand on immediate basis

cost high to company. it should focus over its operational expenses reducing costs..

5

Break even units 20437

[40000/(20-12)]+20437

b) Required Bottles 25437

CAPITAL BUDGETING

A B C D

Payback period 3.4 3.5 3.2 3.8

ARR 33% 24% 32% 26%

NPV 49665 50000 131818 42727

8.

Given the virtually unlimited funds Proposals A, B & C pass the criteria.

9.

Given virtually limited funds company should accept Proposal C.

BUDGET VARIANCE REPORT

10.

Report shows that the variances are adverse and there is adverse variation of 20% in sales

and 48% in operating profit even after a favourable variance in gross profit due to significant

increase in advertising cost.

11.

Company should is required to put more focus over cost of sales by adopting cost

efficient strategies as advertising is essential for promoting the sales.

12.

Report shows healthy performance as the sales are higher than the budgeted and it has

maintained effective control over cost of goods sold. The efficient management of operational

activities has helped in achieving profits higher than budgeted.

13.

Company is required to increase its production as the meeting demand on immediate basis

cost high to company. it should focus over its operational expenses reducing costs..

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDICES

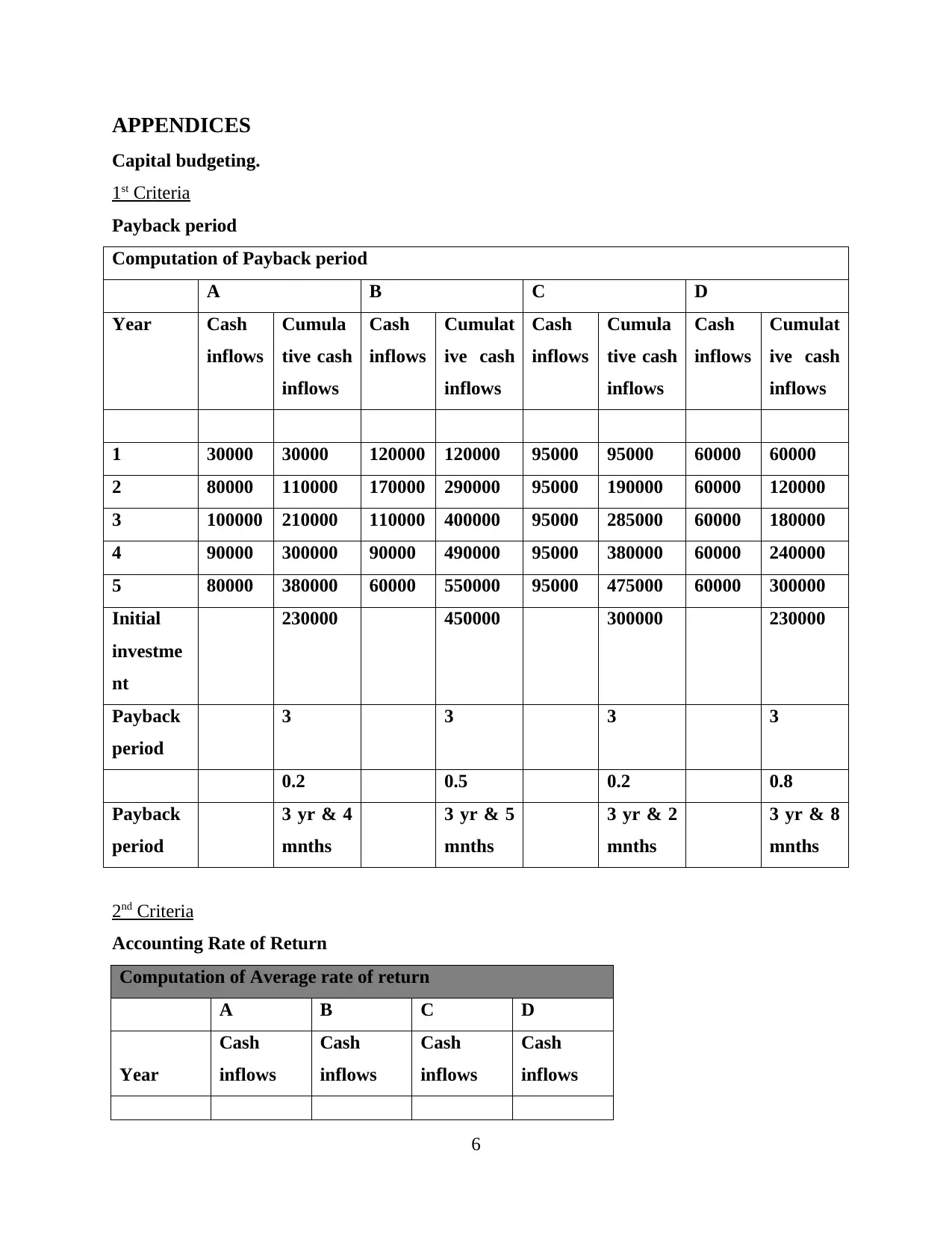

Capital budgeting.

1st Criteria

Payback period

Computation of Payback period

A B C D

Year Cash

inflows

Cumula

tive cash

inflows

Cash

inflows

Cumulat

ive cash

inflows

Cash

inflows

Cumula

tive cash

inflows

Cash

inflows

Cumulat

ive cash

inflows

1 30000 30000 120000 120000 95000 95000 60000 60000

2 80000 110000 170000 290000 95000 190000 60000 120000

3 100000 210000 110000 400000 95000 285000 60000 180000

4 90000 300000 90000 490000 95000 380000 60000 240000

5 80000 380000 60000 550000 95000 475000 60000 300000

Initial

investme

nt

230000 450000 300000 230000

Payback

period

3 3 3 3

0.2 0.5 0.2 0.8

Payback

period

3 yr & 4

mnths

3 yr & 5

mnths

3 yr & 2

mnths

3 yr & 8

mnths

2nd Criteria

Accounting Rate of Return

Computation of Average rate of return

A B C D

Year

Cash

inflows

Cash

inflows

Cash

inflows

Cash

inflows

6

Capital budgeting.

1st Criteria

Payback period

Computation of Payback period

A B C D

Year Cash

inflows

Cumula

tive cash

inflows

Cash

inflows

Cumulat

ive cash

inflows

Cash

inflows

Cumula

tive cash

inflows

Cash

inflows

Cumulat

ive cash

inflows

1 30000 30000 120000 120000 95000 95000 60000 60000

2 80000 110000 170000 290000 95000 190000 60000 120000

3 100000 210000 110000 400000 95000 285000 60000 180000

4 90000 300000 90000 490000 95000 380000 60000 240000

5 80000 380000 60000 550000 95000 475000 60000 300000

Initial

investme

nt

230000 450000 300000 230000

Payback

period

3 3 3 3

0.2 0.5 0.2 0.8

Payback

period

3 yr & 4

mnths

3 yr & 5

mnths

3 yr & 2

mnths

3 yr & 8

mnths

2nd Criteria

Accounting Rate of Return

Computation of Average rate of return

A B C D

Year

Cash

inflows

Cash

inflows

Cash

inflows

Cash

inflows

6

1 30000 120000 95000 60000

2 80000 170000 95000 60000

3 100000 110000 95000 60000

4 90000 90000 95000 60000

5 80000 60000 95000 60000

Average

profit or

cash

inflow 76000 110000 95000 60000

Average

initial

investmen

t 230000 450000 300000 230000

average

initial

investmen

t [(initial

investmen

t + scrap

value) / 2]

ARR 33% 24% 32% 26%

3rd Criteria

NPV

Computation of NPV

A B C D

Year PV

facto

r @

Cash

inflo

Discoun

ted cash

Cash

inflo

Discoun

ted cash

Cash

inflo

Discoun

ted cash

Cash

inflo

Discoun

ted cash

7

2 80000 170000 95000 60000

3 100000 110000 95000 60000

4 90000 90000 95000 60000

5 80000 60000 95000 60000

Average

profit or

cash

inflow 76000 110000 95000 60000

Average

initial

investmen

t 230000 450000 300000 230000

average

initial

investmen

t [(initial

investmen

t + scrap

value) / 2]

ARR 33% 24% 32% 26%

3rd Criteria

NPV

Computation of NPV

A B C D

Year PV

facto

r @

Cash

inflo

Discoun

ted cash

Cash

inflo

Discoun

ted cash

Cash

inflo

Discoun

ted cash

Cash

inflo

Discoun

ted cash

7

10% ws inflows ws inflows ws inflows ws inflows

1 0.909 3000

0

27272.7 1200

00

109091 9500

0

86363.6 6000

0

54545.5

2 0.826 8000

0

66115.7 1700

00

154545 9500

0

86363.6 6000

0

54545.5

3 0.751 1000

00

75131.5 1100

00

100000 9500

0

86363.6 6000

0

54545.5

4 0.683 9000

0

61471.2 9000

0

81818.2 9500

0

86363.6 6000

0

54545.5

5 0.621 8000

0

49673.7 6000

0

54545.5 9500

0

86363.6 6000

0

54545.5

Total

discount

ed cash

inflow

279665 500000 431818 272727

Initial

investme

nt

230000 450000 300000 230000

NPV

(Total

discount

ed cash

inflows -

initial

investme

nt)

49665 50000 131818 42727

8

1 0.909 3000

0

27272.7 1200

00

109091 9500

0

86363.6 6000

0

54545.5

2 0.826 8000

0

66115.7 1700

00

154545 9500

0

86363.6 6000

0

54545.5

3 0.751 1000

00

75131.5 1100

00

100000 9500

0

86363.6 6000

0

54545.5

4 0.683 9000

0

61471.2 9000

0

81818.2 9500

0

86363.6 6000

0

54545.5

5 0.621 8000

0

49673.7 6000

0

54545.5 9500

0

86363.6 6000

0

54545.5

Total

discount

ed cash

inflow

279665 500000 431818 272727

Initial

investme

nt

230000 450000 300000 230000

NPV

(Total

discount

ed cash

inflows -

initial

investme

nt)

49665 50000 131818 42727

8

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.