Manage Finance

VerifiedAdded on 2023/03/30

|17

|2666

|98

AI Summary

This document provides study material on managing finance, including budget development, compliance requirements, financial management software, and accounting principles. It also includes a case study on Stott's Pty Ltd and their budgeting approach. The document is relevant for students studying finance or related subjects.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGE FINANCE

Manage finance

Name of the student

Name of the university

Student ID

Author note

Manage finance

Name of the student

Name of the university

Student ID

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MANAGE FINANCEReference

Table of Contents

Assignment 1...................................................................................................................................2

Part A...........................................................................................................................................2

a. Budget development.........................................................................................................2

b. Developing budget notes...................................................................................................4

Part B...........................................................................................................................................5

1. Statutory requirement to comply with the tax...................................................................5

2. Compliance requirement and liabilities under Corporation Act 2001..............................6

3. Financial management software........................................................................................7

4. Accounting principles.......................................................................................................7

5. Implication of probity.......................................................................................................8

6. Critical dates and initiatives..............................................................................................8

7. Recommendation for inclusion of items...........................................................................9

8. Modified list for internal control.......................................................................................9

Assessment 2.................................................................................................................................10

a. Issues involved in budget....................................................................................................10

b. Variance..............................................................................................................................10

c. Performance........................................................................................................................11

Table of Contents

Assignment 1...................................................................................................................................2

Part A...........................................................................................................................................2

a. Budget development.........................................................................................................2

b. Developing budget notes...................................................................................................4

Part B...........................................................................................................................................5

1. Statutory requirement to comply with the tax...................................................................5

2. Compliance requirement and liabilities under Corporation Act 2001..............................6

3. Financial management software........................................................................................7

4. Accounting principles.......................................................................................................7

5. Implication of probity.......................................................................................................8

6. Critical dates and initiatives..............................................................................................8

7. Recommendation for inclusion of items...........................................................................9

8. Modified list for internal control.......................................................................................9

Assessment 2.................................................................................................................................10

a. Issues involved in budget....................................................................................................10

b. Variance..............................................................................................................................10

c. Performance........................................................................................................................11

2MANAGE FINANCEReference

d. Recommendation................................................................................................................12

e. Financial management process...........................................................................................13

Reference.......................................................................................................................................14

d. Recommendation................................................................................................................12

e. Financial management process...........................................................................................13

Reference.......................................................................................................................................14

3MANAGE FINANCEReference

Assignment 1

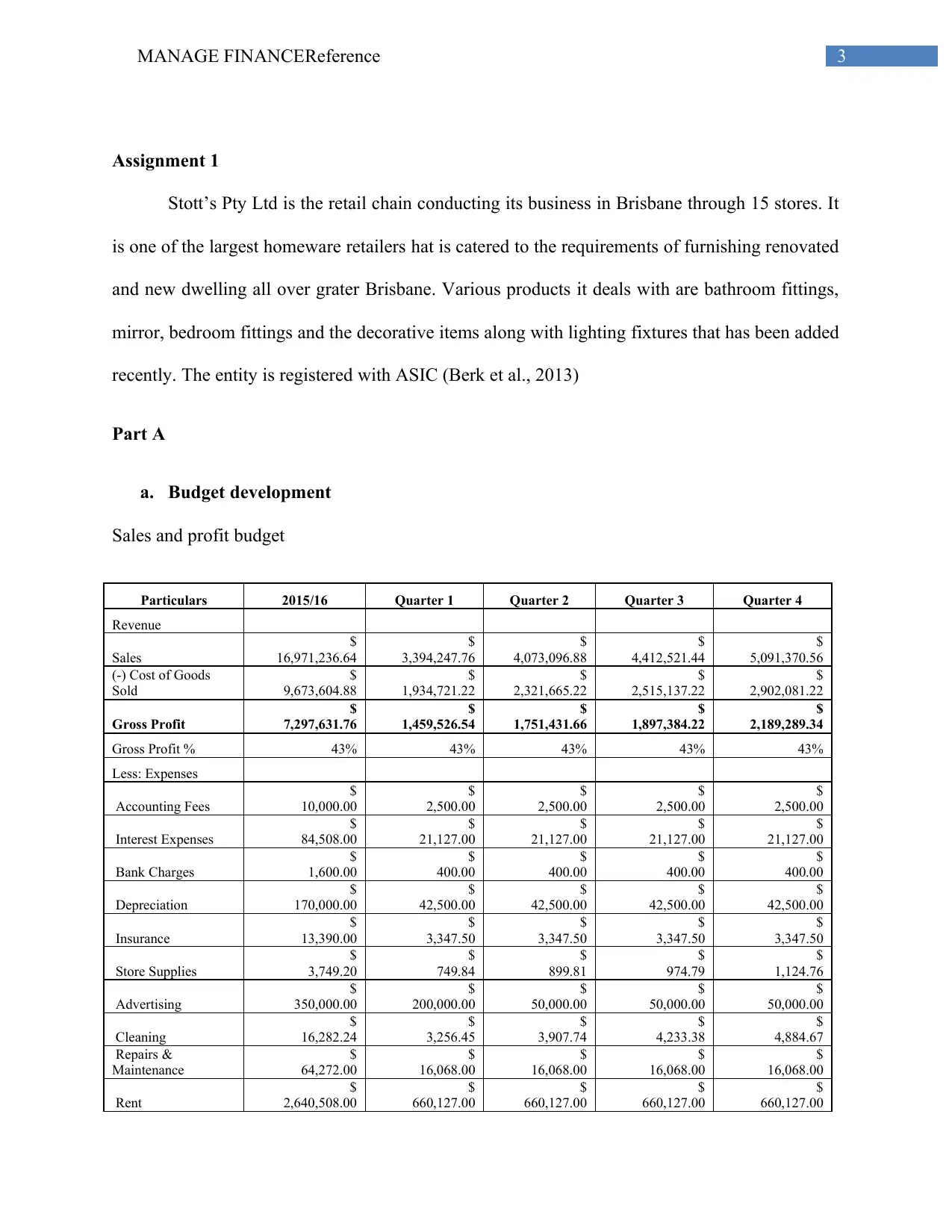

Stott’s Pty Ltd is the retail chain conducting its business in Brisbane through 15 stores. It

is one of the largest homeware retailers hat is catered to the requirements of furnishing renovated

and new dwelling all over grater Brisbane. Various products it deals with are bathroom fittings,

mirror, bedroom fittings and the decorative items along with lighting fixtures that has been added

recently. The entity is registered with ASIC (Berk et al., 2013)

Part A

a. Budget development

Sales and profit budget

Particulars 2015/16 Quarter 1 Quarter 2 Quarter 3 Quarter 4

Revenue

Sales

$

16,971,236.64

$

3,394,247.76

$

4,073,096.88

$

4,412,521.44

$

5,091,370.56

(-) Cost of Goods

Sold

$

9,673,604.88

$

1,934,721.22

$

2,321,665.22

$

2,515,137.22

$

2,902,081.22

Gross Profit

$

7,297,631.76

$

1,459,526.54

$

1,751,431.66

$

1,897,384.22

$

2,189,289.34

Gross Profit % 43% 43% 43% 43% 43%

Less: Expenses

Accounting Fees

$

10,000.00

$

2,500.00

$

2,500.00

$

2,500.00

$

2,500.00

Interest Expenses

$

84,508.00

$

21,127.00

$

21,127.00

$

21,127.00

$

21,127.00

Bank Charges

$

1,600.00

$

400.00

$

400.00

$

400.00

$

400.00

Depreciation

$

170,000.00

$

42,500.00

$

42,500.00

$

42,500.00

$

42,500.00

Insurance

$

13,390.00

$

3,347.50

$

3,347.50

$

3,347.50

$

3,347.50

Store Supplies

$

3,749.20

$

749.84

$

899.81

$

974.79

$

1,124.76

Advertising

$

350,000.00

$

200,000.00

$

50,000.00

$

50,000.00

$

50,000.00

Cleaning

$

16,282.24

$

3,256.45

$

3,907.74

$

4,233.38

$

4,884.67

Repairs &

Maintenance

$

64,272.00

$

16,068.00

$

16,068.00

$

16,068.00

$

16,068.00

Rent

$

2,640,508.00

$

660,127.00

$

660,127.00

$

660,127.00

$

660,127.00

Assignment 1

Stott’s Pty Ltd is the retail chain conducting its business in Brisbane through 15 stores. It

is one of the largest homeware retailers hat is catered to the requirements of furnishing renovated

and new dwelling all over grater Brisbane. Various products it deals with are bathroom fittings,

mirror, bedroom fittings and the decorative items along with lighting fixtures that has been added

recently. The entity is registered with ASIC (Berk et al., 2013)

Part A

a. Budget development

Sales and profit budget

Particulars 2015/16 Quarter 1 Quarter 2 Quarter 3 Quarter 4

Revenue

Sales

$

16,971,236.64

$

3,394,247.76

$

4,073,096.88

$

4,412,521.44

$

5,091,370.56

(-) Cost of Goods

Sold

$

9,673,604.88

$

1,934,721.22

$

2,321,665.22

$

2,515,137.22

$

2,902,081.22

Gross Profit

$

7,297,631.76

$

1,459,526.54

$

1,751,431.66

$

1,897,384.22

$

2,189,289.34

Gross Profit % 43% 43% 43% 43% 43%

Less: Expenses

Accounting Fees

$

10,000.00

$

2,500.00

$

2,500.00

$

2,500.00

$

2,500.00

Interest Expenses

$

84,508.00

$

21,127.00

$

21,127.00

$

21,127.00

$

21,127.00

Bank Charges

$

1,600.00

$

400.00

$

400.00

$

400.00

$

400.00

Depreciation

$

170,000.00

$

42,500.00

$

42,500.00

$

42,500.00

$

42,500.00

Insurance

$

13,390.00

$

3,347.50

$

3,347.50

$

3,347.50

$

3,347.50

Store Supplies

$

3,749.20

$

749.84

$

899.81

$

974.79

$

1,124.76

Advertising

$

350,000.00

$

200,000.00

$

50,000.00

$

50,000.00

$

50,000.00

Cleaning

$

16,282.24

$

3,256.45

$

3,907.74

$

4,233.38

$

4,884.67

Repairs &

Maintenance

$

64,272.00

$

16,068.00

$

16,068.00

$

16,068.00

$

16,068.00

Rent

$

2,640,508.00

$

660,127.00

$

660,127.00

$

660,127.00

$

660,127.00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MANAGE FINANCEReference

Telephone

$

14,996.80

$

2,999.36

$

3,599.23

$

3,899.17

$

4,499.04

Electricity Expenses

$

26,780.00

$

5,356.00

$

6,427.20

$

6,962.80

$

8,034.00

Luxury Car Tax

$

12,000.00

$

12,000.00

$

-

$

-

$

-

Fringe Benefits Tax

$

28,000.00

$

7,000.00

$

7,000.00

$

7,000.00

$

7,000.00

Superannuation

$

187,020.00

$

37,404.00

$

44,884.80

$

48,625.20

$

56,106.00

Wages & Salaries

$

2,078,000.00

$

415,600.05

$

498,720.01

$

540,279.99

$

623,399.95

Payroll Tax

$

98,705.00

$

19,741.00

$

23,689.20

$

25,663.30

$

29,611.50

Workers

Compensation

$

41,560.00

$

8,312.00

$

9,974.40

$

10,805.60

$

12,468.00

Total Expenses

$

5,841,371.24

$

1,458,488.21

$

1,395,171.89

$

1,444,513.73

$

1,543,197.41

Net Profit (Before

Tax)

$

1,456,260.52

$

1,038.33

$

356,259.77

$

452,870.49

$

646,091.93

Income Tax

$

436,878.15

$

311.50

$

106,877.93

$

135,861.15

$

193,827.58

Net Profit

$

1,019,382.36

$

726.83

$

249,381.84

$

317,009.34

$

452,264.35

Cash flow analysis and GST

Debtor ageing analysis

Telephone

$

14,996.80

$

2,999.36

$

3,599.23

$

3,899.17

$

4,499.04

Electricity Expenses

$

26,780.00

$

5,356.00

$

6,427.20

$

6,962.80

$

8,034.00

Luxury Car Tax

$

12,000.00

$

12,000.00

$

-

$

-

$

-

Fringe Benefits Tax

$

28,000.00

$

7,000.00

$

7,000.00

$

7,000.00

$

7,000.00

Superannuation

$

187,020.00

$

37,404.00

$

44,884.80

$

48,625.20

$

56,106.00

Wages & Salaries

$

2,078,000.00

$

415,600.05

$

498,720.01

$

540,279.99

$

623,399.95

Payroll Tax

$

98,705.00

$

19,741.00

$

23,689.20

$

25,663.30

$

29,611.50

Workers

Compensation

$

41,560.00

$

8,312.00

$

9,974.40

$

10,805.60

$

12,468.00

Total Expenses

$

5,841,371.24

$

1,458,488.21

$

1,395,171.89

$

1,444,513.73

$

1,543,197.41

Net Profit (Before

Tax)

$

1,456,260.52

$

1,038.33

$

356,259.77

$

452,870.49

$

646,091.93

Income Tax

$

436,878.15

$

311.50

$

106,877.93

$

135,861.15

$

193,827.58

Net Profit

$

1,019,382.36

$

726.83

$

249,381.84

$

317,009.34

$

452,264.35

Cash flow analysis and GST

Debtor ageing analysis

5MANAGE FINANCEReference

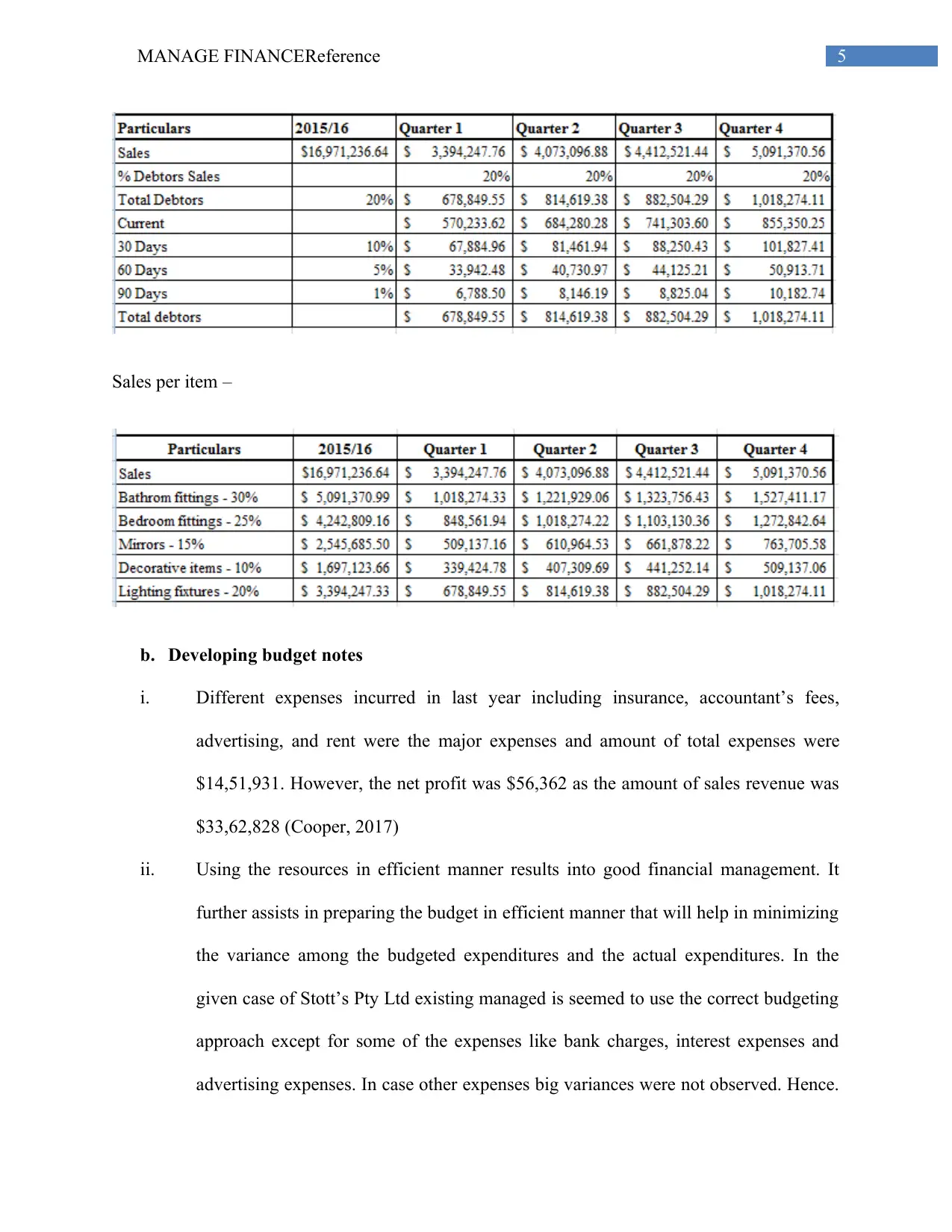

Sales per item –

b. Developing budget notes

i. Different expenses incurred in last year including insurance, accountant’s fees,

advertising, and rent were the major expenses and amount of total expenses were

$14,51,931. However, the net profit was $56,362 as the amount of sales revenue was

$33,62,828 (Cooper, 2017)

ii. Using the resources in efficient manner results into good financial management. It

further assists in preparing the budget in efficient manner that will help in minimizing

the variance among the budgeted expenditures and the actual expenditures. In the

given case of Stott’s Pty Ltd existing managed is seemed to use the correct budgeting

approach except for some of the expenses like bank charges, interest expenses and

advertising expenses. In case other expenses big variances were not observed. Hence.

Sales per item –

b. Developing budget notes

i. Different expenses incurred in last year including insurance, accountant’s fees,

advertising, and rent were the major expenses and amount of total expenses were

$14,51,931. However, the net profit was $56,362 as the amount of sales revenue was

$33,62,828 (Cooper, 2017)

ii. Using the resources in efficient manner results into good financial management. It

further assists in preparing the budget in efficient manner that will help in minimizing

the variance among the budgeted expenditures and the actual expenditures. In the

given case of Stott’s Pty Ltd existing managed is seemed to use the correct budgeting

approach except for some of the expenses like bank charges, interest expenses and

advertising expenses. In case other expenses big variances were not observed. Hence.

6MANAGE FINANCEReference

It can be stated that the budgeting and management approaches of the existing

management is efficient.

iii. Assumptions those were made while preparing the budgets are –

Inflation rate will increase at 4% per annum and all the expenses will be inflation

adjusted.

Sales will be increased as per the growth rate for the previous year

Gross profit will drop by 1% subjected to the estimation that the sales will grow owing to

lower sales price.

iv. Budget must be evaluated and compared with the actual expenses on regular basis to

find out the whether the variance is increasing or reducing. Apart from that while the

budget is prepared, industry scenario, market demand and the economic scenario shall

be taken into consideration.

Part B

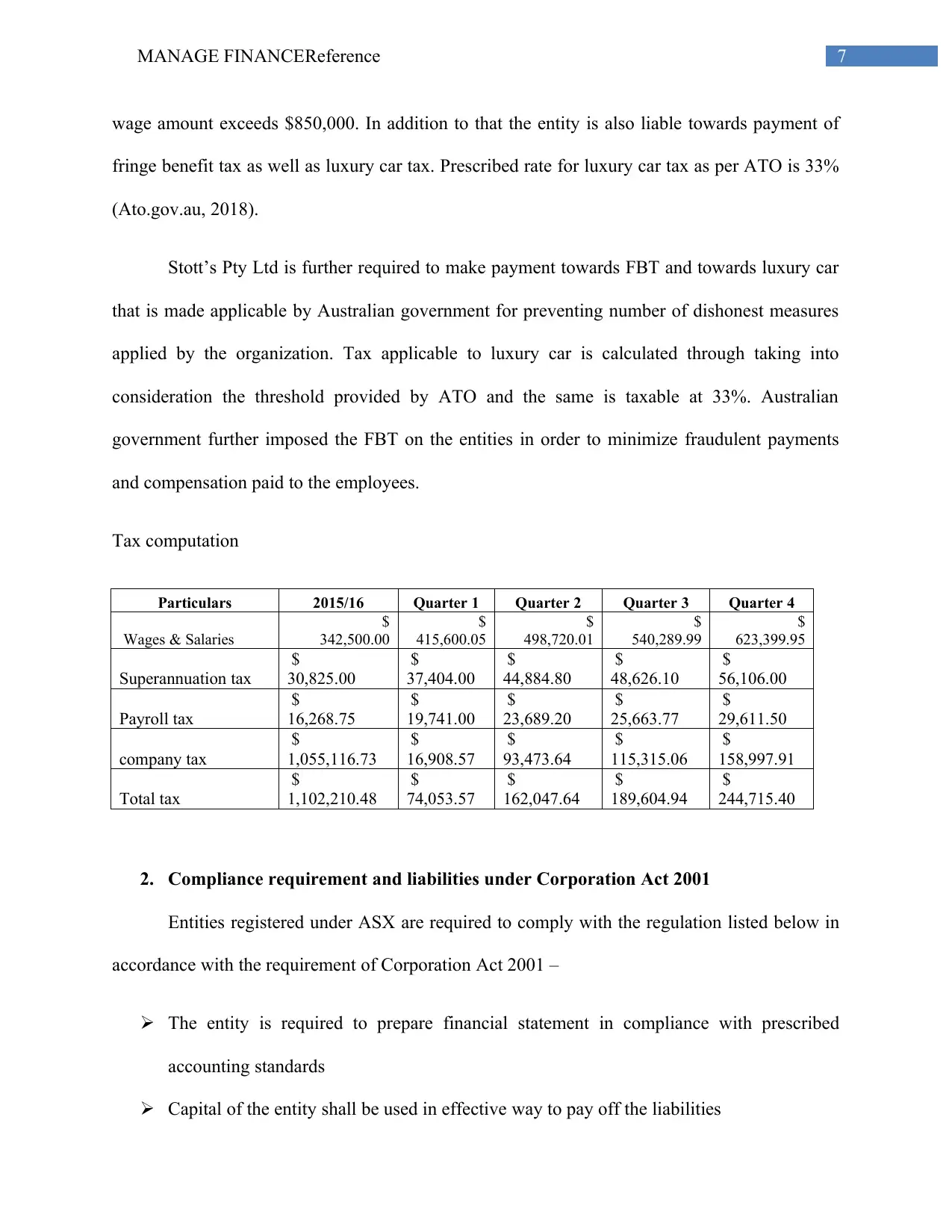

1. Statutory requirement to comply with the tax

Various rules and regulation are there those are applicable to the Australian business

entities. These rules and regulations are required to be complied with by the entities for

collection of adequate tax from the profit earning entities. Apart from that, Stott’s Pty Ltd is

accountable for payroll tax, fringe benefit tax, luxury car tax and superannuation tax for the year

2015-16. The company contributes about 9% on total wages paid to the workers towards

superannuation. As stated by Sazonov, Lukyanova and Popkova (2013) in accordance with ATO

(Australian Taxation Office) the entity i required to contribute towards superannuation for the

employees for preserving the earning flow on continuous basis after the retirement period.

Further, the entity is obliged to pay 4.75% towards payroll tax applicable on total wages if the

It can be stated that the budgeting and management approaches of the existing

management is efficient.

iii. Assumptions those were made while preparing the budgets are –

Inflation rate will increase at 4% per annum and all the expenses will be inflation

adjusted.

Sales will be increased as per the growth rate for the previous year

Gross profit will drop by 1% subjected to the estimation that the sales will grow owing to

lower sales price.

iv. Budget must be evaluated and compared with the actual expenses on regular basis to

find out the whether the variance is increasing or reducing. Apart from that while the

budget is prepared, industry scenario, market demand and the economic scenario shall

be taken into consideration.

Part B

1. Statutory requirement to comply with the tax

Various rules and regulation are there those are applicable to the Australian business

entities. These rules and regulations are required to be complied with by the entities for

collection of adequate tax from the profit earning entities. Apart from that, Stott’s Pty Ltd is

accountable for payroll tax, fringe benefit tax, luxury car tax and superannuation tax for the year

2015-16. The company contributes about 9% on total wages paid to the workers towards

superannuation. As stated by Sazonov, Lukyanova and Popkova (2013) in accordance with ATO

(Australian Taxation Office) the entity i required to contribute towards superannuation for the

employees for preserving the earning flow on continuous basis after the retirement period.

Further, the entity is obliged to pay 4.75% towards payroll tax applicable on total wages if the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGE FINANCEReference

wage amount exceeds $850,000. In addition to that the entity is also liable towards payment of

fringe benefit tax as well as luxury car tax. Prescribed rate for luxury car tax as per ATO is 33%

(Ato.gov.au, 2018).

Stott’s Pty Ltd is further required to make payment towards FBT and towards luxury car

that is made applicable by Australian government for preventing number of dishonest measures

applied by the organization. Tax applicable to luxury car is calculated through taking into

consideration the threshold provided by ATO and the same is taxable at 33%. Australian

government further imposed the FBT on the entities in order to minimize fraudulent payments

and compensation paid to the employees.

Tax computation

Particulars 2015/16 Quarter 1 Quarter 2 Quarter 3 Quarter 4

Wages & Salaries

$

342,500.00

$

415,600.05

$

498,720.01

$

540,289.99

$

623,399.95

Superannuation tax

$

30,825.00

$

37,404.00

$

44,884.80

$

48,626.10

$

56,106.00

Payroll tax

$

16,268.75

$

19,741.00

$

23,689.20

$

25,663.77

$

29,611.50

company tax

$

1,055,116.73

$

16,908.57

$

93,473.64

$

115,315.06

$

158,997.91

Total tax

$

1,102,210.48

$

74,053.57

$

162,047.64

$

189,604.94

$

244,715.40

2. Compliance requirement and liabilities under Corporation Act 2001

Entities registered under ASX are required to comply with the regulation listed below in

accordance with the requirement of Corporation Act 2001 –

The entity is required to prepare financial statement in compliance with prescribed

accounting standards

Capital of the entity shall be used in effective way to pay off the liabilities

wage amount exceeds $850,000. In addition to that the entity is also liable towards payment of

fringe benefit tax as well as luxury car tax. Prescribed rate for luxury car tax as per ATO is 33%

(Ato.gov.au, 2018).

Stott’s Pty Ltd is further required to make payment towards FBT and towards luxury car

that is made applicable by Australian government for preventing number of dishonest measures

applied by the organization. Tax applicable to luxury car is calculated through taking into

consideration the threshold provided by ATO and the same is taxable at 33%. Australian

government further imposed the FBT on the entities in order to minimize fraudulent payments

and compensation paid to the employees.

Tax computation

Particulars 2015/16 Quarter 1 Quarter 2 Quarter 3 Quarter 4

Wages & Salaries

$

342,500.00

$

415,600.05

$

498,720.01

$

540,289.99

$

623,399.95

Superannuation tax

$

30,825.00

$

37,404.00

$

44,884.80

$

48,626.10

$

56,106.00

Payroll tax

$

16,268.75

$

19,741.00

$

23,689.20

$

25,663.77

$

29,611.50

company tax

$

1,055,116.73

$

16,908.57

$

93,473.64

$

115,315.06

$

158,997.91

Total tax

$

1,102,210.48

$

74,053.57

$

162,047.64

$

189,604.94

$

244,715.40

2. Compliance requirement and liabilities under Corporation Act 2001

Entities registered under ASX are required to comply with the regulation listed below in

accordance with the requirement of Corporation Act 2001 –

The entity is required to prepare financial statement in compliance with prescribed

accounting standards

Capital of the entity shall be used in effective way to pay off the liabilities

8MANAGE FINANCEReference

The entity is required to issue actual records with regard to financial performances to the

debtors to enable them analysing the financial viability of the entity (Legislation.gov.au,

2018).

3. Financial management software

As mentioned by the entity that the existing software is not able to deliver the analysis of

revenues and the expenses and the process for estimating the profit is not easy, it shall opt for

better software that will be able to solve these issues. Hence, it may opt for XERO or MYOB

that will be efficient in doing the task which the existing software is lacking.

XERO – XERO is the cloud computing g software and is capable of reconciling, sending quotes

as well as invoices, creating claims for expenses and recording receipts. Further, the software is

simple and easy for using and it allows the users extending the features to enhance the usefulness

from every aspect. Further, this software can be installed by the entity irrespective of its software

history (King, 2015)

MYOB – this software is simple to use and it is widely used by the SMEs. It is powerful and is

focused on the procedures of business and the work flows. Further, the software is GST ready

and is able to comply with GST (Curtis, 2015)

Among the 2 software mentioned above, Stott’s Pty Ltd shall opt for MYOB software as

it is cheaper, simple to use and easy in installation as against XERO.

4. Accounting principles

a. Matching principle – it is one of the basic guidelines used in accounting. It directs the

entity in reporting expenses under the income statement in the same period in which the

associated revenues are earned. It is related to accrual basis of accounting as well as with

The entity is required to issue actual records with regard to financial performances to the

debtors to enable them analysing the financial viability of the entity (Legislation.gov.au,

2018).

3. Financial management software

As mentioned by the entity that the existing software is not able to deliver the analysis of

revenues and the expenses and the process for estimating the profit is not easy, it shall opt for

better software that will be able to solve these issues. Hence, it may opt for XERO or MYOB

that will be efficient in doing the task which the existing software is lacking.

XERO – XERO is the cloud computing g software and is capable of reconciling, sending quotes

as well as invoices, creating claims for expenses and recording receipts. Further, the software is

simple and easy for using and it allows the users extending the features to enhance the usefulness

from every aspect. Further, this software can be installed by the entity irrespective of its software

history (King, 2015)

MYOB – this software is simple to use and it is widely used by the SMEs. It is powerful and is

focused on the procedures of business and the work flows. Further, the software is GST ready

and is able to comply with GST (Curtis, 2015)

Among the 2 software mentioned above, Stott’s Pty Ltd shall opt for MYOB software as

it is cheaper, simple to use and easy in installation as against XERO.

4. Accounting principles

a. Matching principle – it is one of the basic guidelines used in accounting. It directs the

entity in reporting expenses under the income statement in the same period in which the

associated revenues are earned. It is related to accrual basis of accounting as well as with

9MANAGE FINANCEReference

the adjusting entries. Matching principle is crucial for preparation of budget as the

expenses is charged in accordance with determination of cost (De Simone, Ege &

Stomberg, 2014)

b. Account groups – it involves grouping of similar kind of accounts into the single group. It

assists in segregating the groups of accounts that is required for budget preparation.

Reason behind that is if items related to incomes are added with expenses, the entire

budget will go wrong (Sazonov, Lukyanova & Popkova 2013)

c. Time periods – time period refers to differentiating accounting transactions into quarter,

month or year. If the accounting transactions are not differentiated under proper periods,

data and amount of one period will be included under another period’s data (He & Shan,

2014)

5. Implication of probity

The significance of the term probity is relative and cannot be defined under the economic

and managerial framework. It protects the community and takes care of their interests and rights

for the entire group of people. It protects the right of the users and helps in knowing the entity’s

actual position.

6. Critical dates and initiatives

Most appropriate time for preparing the next year’s budget is after issuance of previous

year’s budget and its comparison with the actual expenses and incomes. Proposal must be

consider the following –

Budget must be prepared using the new software

the adjusting entries. Matching principle is crucial for preparation of budget as the

expenses is charged in accordance with determination of cost (De Simone, Ege &

Stomberg, 2014)

b. Account groups – it involves grouping of similar kind of accounts into the single group. It

assists in segregating the groups of accounts that is required for budget preparation.

Reason behind that is if items related to incomes are added with expenses, the entire

budget will go wrong (Sazonov, Lukyanova & Popkova 2013)

c. Time periods – time period refers to differentiating accounting transactions into quarter,

month or year. If the accounting transactions are not differentiated under proper periods,

data and amount of one period will be included under another period’s data (He & Shan,

2014)

5. Implication of probity

The significance of the term probity is relative and cannot be defined under the economic

and managerial framework. It protects the community and takes care of their interests and rights

for the entire group of people. It protects the right of the users and helps in knowing the entity’s

actual position.

6. Critical dates and initiatives

Most appropriate time for preparing the next year’s budget is after issuance of previous

year’s budget and its comparison with the actual expenses and incomes. Proposal must be

consider the following –

Budget must be prepared using the new software

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10MANAGE FINANCEReference

Various assumptions shall be made by the accountant taking into account the appropriate

bases. It will enable to narrow the gap among actual figure an budgeted figure (Henttu-

Aho & Järvinen, 2013)

7. Recommendation for inclusion of items

Various items those are to be introduced while preparing the budget for the next period

are as follows –

Improving privacy and safety to reduce the extent of manipulation that may take place

while budget is prepared.

Accounting system shall be implemented with the objective of processing the budget

accurately

Using of fair and realistic valuation with the objective of reducing the unfavourable

variances (Droms & Wright, 2015)

8. Modified list for internal control

Audit trail can be used to trace the associated items with the transaction reported by the

entity. Following recommendations are provided to maintain the internal control –

All the transactions shall be dated and numbered properly that will enable easy access

Inventories as well as stocks shall be verified physically that will reduce the level of

fraud.

Access to financial data shall be properly authorised (Hope & Fraser, 2013)

Regular reconciliation of financial records to minimize misstatements, frauds and errors.

Various assumptions shall be made by the accountant taking into account the appropriate

bases. It will enable to narrow the gap among actual figure an budgeted figure (Henttu-

Aho & Järvinen, 2013)

7. Recommendation for inclusion of items

Various items those are to be introduced while preparing the budget for the next period

are as follows –

Improving privacy and safety to reduce the extent of manipulation that may take place

while budget is prepared.

Accounting system shall be implemented with the objective of processing the budget

accurately

Using of fair and realistic valuation with the objective of reducing the unfavourable

variances (Droms & Wright, 2015)

8. Modified list for internal control

Audit trail can be used to trace the associated items with the transaction reported by the

entity. Following recommendations are provided to maintain the internal control –

All the transactions shall be dated and numbered properly that will enable easy access

Inventories as well as stocks shall be verified physically that will reduce the level of

fraud.

Access to financial data shall be properly authorised (Hope & Fraser, 2013)

Regular reconciliation of financial records to minimize misstatements, frauds and errors.

11MANAGE FINANCEReference

Assessment 2

a. Issues involved in budget

i. Significant issues

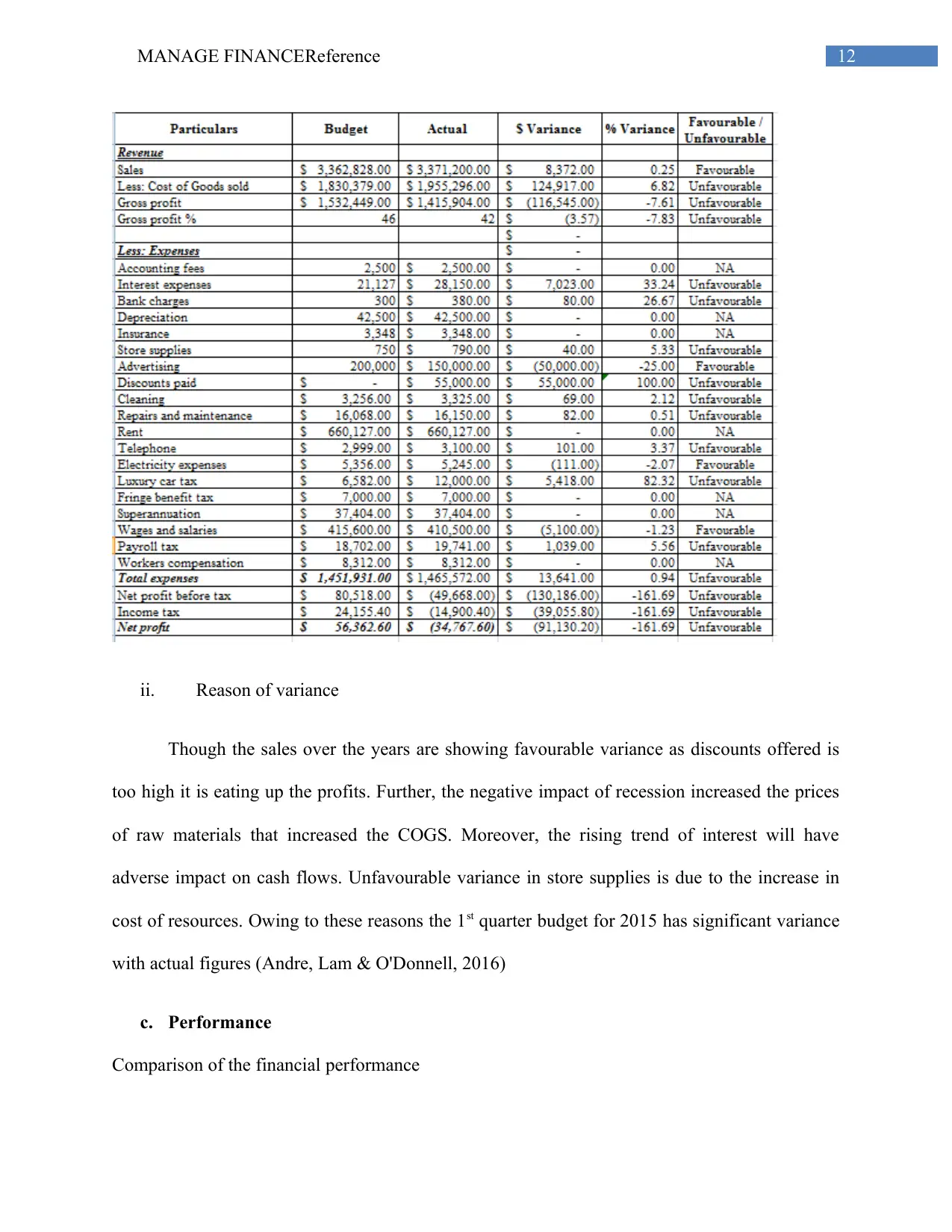

Most significant issue involved with Stott’s Pty Ltd is gross margin viability. As the

country is passing through recession impact on the retail sector is prominent as it will reduce the

spending power of the customers. Further, though the sales over the years is in rising trend as

discounts offered is too high it is eating up the profits. Further, the interest is at rising trend that

will have adverse impact on cash flows (Kelly, 2015)

b. Variance

i. Budget variance

Assessment 2

a. Issues involved in budget

i. Significant issues

Most significant issue involved with Stott’s Pty Ltd is gross margin viability. As the

country is passing through recession impact on the retail sector is prominent as it will reduce the

spending power of the customers. Further, though the sales over the years is in rising trend as

discounts offered is too high it is eating up the profits. Further, the interest is at rising trend that

will have adverse impact on cash flows (Kelly, 2015)

b. Variance

i. Budget variance

12MANAGE FINANCEReference

ii. Reason of variance

Though the sales over the years are showing favourable variance as discounts offered is

too high it is eating up the profits. Further, the negative impact of recession increased the prices

of raw materials that increased the COGS. Moreover, the rising trend of interest will have

adverse impact on cash flows. Unfavourable variance in store supplies is due to the increase in

cost of resources. Owing to these reasons the 1st quarter budget for 2015 has significant variance

with actual figures (Andre, Lam & O'Donnell, 2016)

c. Performance

Comparison of the financial performance

ii. Reason of variance

Though the sales over the years are showing favourable variance as discounts offered is

too high it is eating up the profits. Further, the negative impact of recession increased the prices

of raw materials that increased the COGS. Moreover, the rising trend of interest will have

adverse impact on cash flows. Unfavourable variance in store supplies is due to the increase in

cost of resources. Owing to these reasons the 1st quarter budget for 2015 has significant variance

with actual figures (Andre, Lam & O'Donnell, 2016)

c. Performance

Comparison of the financial performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13MANAGE FINANCEReference

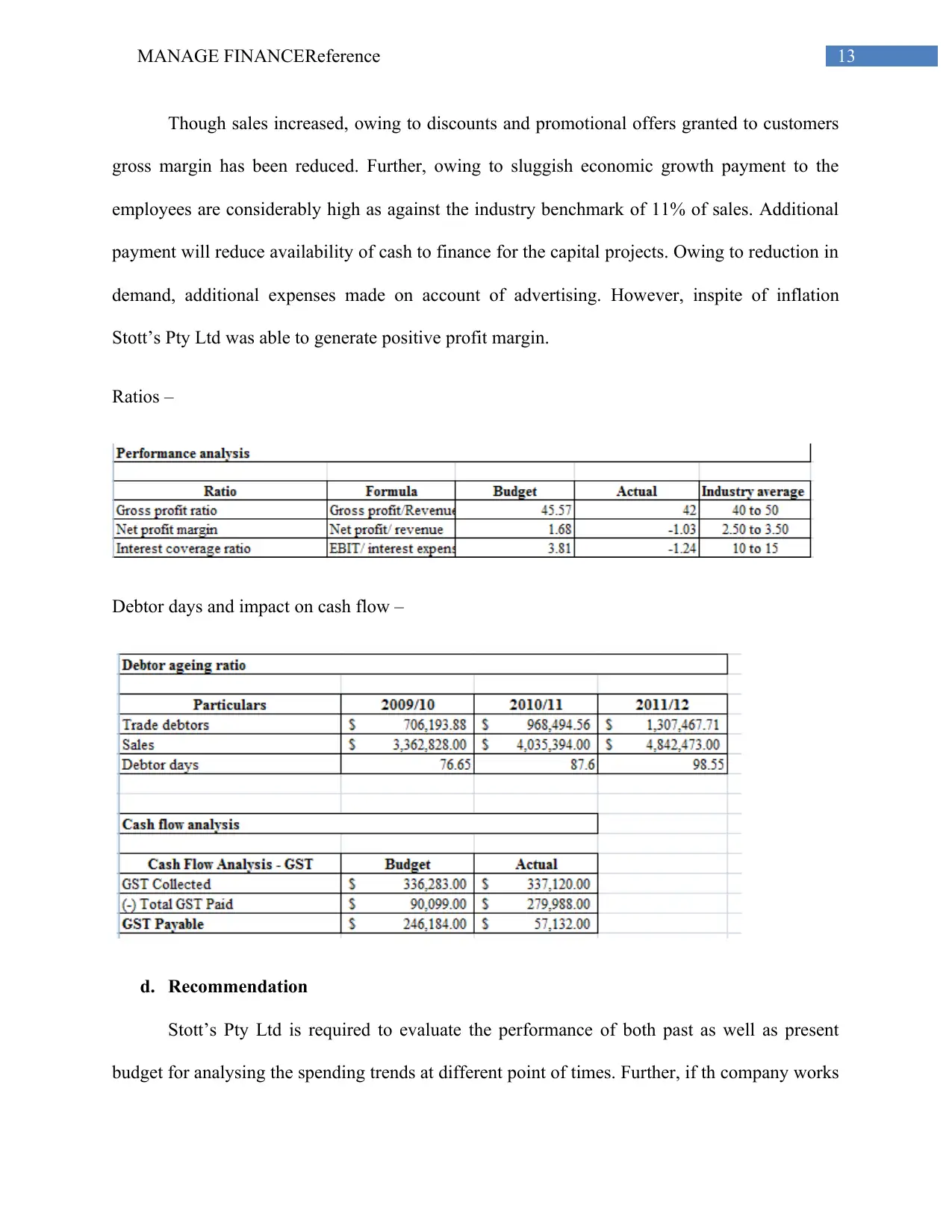

Though sales increased, owing to discounts and promotional offers granted to customers

gross margin has been reduced. Further, owing to sluggish economic growth payment to the

employees are considerably high as against the industry benchmark of 11% of sales. Additional

payment will reduce availability of cash to finance for the capital projects. Owing to reduction in

demand, additional expenses made on account of advertising. However, inspite of inflation

Stott’s Pty Ltd was able to generate positive profit margin.

Ratios –

Debtor days and impact on cash flow –

d. Recommendation

Stott’s Pty Ltd is required to evaluate the performance of both past as well as present

budget for analysing the spending trends at different point of times. Further, if th company works

Though sales increased, owing to discounts and promotional offers granted to customers

gross margin has been reduced. Further, owing to sluggish economic growth payment to the

employees are considerably high as against the industry benchmark of 11% of sales. Additional

payment will reduce availability of cash to finance for the capital projects. Owing to reduction in

demand, additional expenses made on account of advertising. However, inspite of inflation

Stott’s Pty Ltd was able to generate positive profit margin.

Ratios –

Debtor days and impact on cash flow –

d. Recommendation

Stott’s Pty Ltd is required to evaluate the performance of both past as well as present

budget for analysing the spending trends at different point of times. Further, if th company works

14MANAGE FINANCEReference

on short term assignments it will require revision in the budget for meeting the short term

objectives. If the entity plans for introducing new product budget revision is required until

justification received for real figures related to production and sales.

e. Financial management process

The company expanded in context of providing credit to large extent to its customers and

hence, must reduce the credit period. Hence, issuance of transparent as well as proper invoice

through usage of automated system of credit management is required for keeping track of

customer’s account. In addition to that, the entity shall obtain the insight regarding business cost

on everyday basis. Under such circumstance, the entity may think of reducing the wages and

salaries to make it in line with the industry benchmark that will save additional cost. Finally, the

entity shall implement MYOB software to track the required data and save the cost that in turn

will enhance the process for financial management.

on short term assignments it will require revision in the budget for meeting the short term

objectives. If the entity plans for introducing new product budget revision is required until

justification received for real figures related to production and sales.

e. Financial management process

The company expanded in context of providing credit to large extent to its customers and

hence, must reduce the credit period. Hence, issuance of transparent as well as proper invoice

through usage of automated system of credit management is required for keeping track of

customer’s account. In addition to that, the entity shall obtain the insight regarding business cost

on everyday basis. Under such circumstance, the entity may think of reducing the wages and

salaries to make it in line with the industry benchmark that will save additional cost. Finally, the

entity shall implement MYOB software to track the required data and save the cost that in turn

will enhance the process for financial management.

15MANAGE FINANCEReference

Reference

Andre, S.M., Lam, M. & O'Donnell, M., (2016). Budgetary Slack: Exploring the Effect of

Different Types, Directions, and Repeated Attempts of Influence Tactics on Padding a

Budget. Academy of Accounting and Financial Studies Journal, 20(3), p.147.

Ato.gov.au., (2018). Working out the LCT on an import. [online] Available at:

https://www.ato.gov.au/Business/Luxury-car-tax/Working-out-the-LCT-amount/

Working-out-the-LCT-on-an-import/ [Accessed 08 August. 2018].

Berk, J., DeMarzo, P., Harford, J., Ford, G., Mollica, V. & Finch, N., (2013). Fundamentals of

corporate finance. Pearson Higher Education AU.

Cooper, S., (2017). Corporate social performance: A stakeholder approach. Routledge.

Curtis, V., (2015). MYOB Software for Dummies-Australia. John Wiley & Sons.

De Simone, L., Ege, M.S. & Stomberg, B., (2014). Internal control quality: The role of auditor-

provided tax services. The Accounting Review, 90(4), pp.1469-1496.

Droms, W.G. & Wright, J.O., (2015). Finance and accounting for nonfinancial managers: All

the basics you need to know. Basic Books.

HE, W. & SHAN, Y., (2014). International Evidence On the Matching Principle Between

Revenues And Expenses. American Accounting Association. In Annual Meeting and

Conference on teaching and Learning in Accounting. Atlanta, Georgia, August (pp. 2-6).

Reference

Andre, S.M., Lam, M. & O'Donnell, M., (2016). Budgetary Slack: Exploring the Effect of

Different Types, Directions, and Repeated Attempts of Influence Tactics on Padding a

Budget. Academy of Accounting and Financial Studies Journal, 20(3), p.147.

Ato.gov.au., (2018). Working out the LCT on an import. [online] Available at:

https://www.ato.gov.au/Business/Luxury-car-tax/Working-out-the-LCT-amount/

Working-out-the-LCT-on-an-import/ [Accessed 08 August. 2018].

Berk, J., DeMarzo, P., Harford, J., Ford, G., Mollica, V. & Finch, N., (2013). Fundamentals of

corporate finance. Pearson Higher Education AU.

Cooper, S., (2017). Corporate social performance: A stakeholder approach. Routledge.

Curtis, V., (2015). MYOB Software for Dummies-Australia. John Wiley & Sons.

De Simone, L., Ege, M.S. & Stomberg, B., (2014). Internal control quality: The role of auditor-

provided tax services. The Accounting Review, 90(4), pp.1469-1496.

Droms, W.G. & Wright, J.O., (2015). Finance and accounting for nonfinancial managers: All

the basics you need to know. Basic Books.

HE, W. & SHAN, Y., (2014). International Evidence On the Matching Principle Between

Revenues And Expenses. American Accounting Association. In Annual Meeting and

Conference on teaching and Learning in Accounting. Atlanta, Georgia, August (pp. 2-6).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16MANAGE FINANCEReference

Henttu-Aho, T. & Järvinen, J., (2013). A field study of the emerging practice of beyond

budgeting in industrial companies: an institutional perspective. European Accounting

Review, 22(4), pp.765-785.

Hope, J. & Fraser, R., (2013). Beyond budgeting: how managers can break free from the annual

performance trap. Harvard Business Press.

Kelly, (2015). Performance budgeting for state and local government. Me sharpe.

King, A., (2015). Xero soothes auditors on automation.

Legislation.gov.au. (2018). Corporations Act 2001 . [online] Available at:

https://www.legislation.gov.au/Details/C2018C00275 [Accessed 8 Aug. 2018].

Sazonov, S.P., Lukyanova, A.V. & Popkova, E.G., (2013). Towards the Financial Budgeting

Governance in Transitive Economies. World Applied Sciences Journal, 23(11), pp.1538-

1547.

Henttu-Aho, T. & Järvinen, J., (2013). A field study of the emerging practice of beyond

budgeting in industrial companies: an institutional perspective. European Accounting

Review, 22(4), pp.765-785.

Hope, J. & Fraser, R., (2013). Beyond budgeting: how managers can break free from the annual

performance trap. Harvard Business Press.

Kelly, (2015). Performance budgeting for state and local government. Me sharpe.

King, A., (2015). Xero soothes auditors on automation.

Legislation.gov.au. (2018). Corporations Act 2001 . [online] Available at:

https://www.legislation.gov.au/Details/C2018C00275 [Accessed 8 Aug. 2018].

Sazonov, S.P., Lukyanova, A.V. & Popkova, E.G., (2013). Towards the Financial Budgeting

Governance in Transitive Economies. World Applied Sciences Journal, 23(11), pp.1538-

1547.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.