Strategic Business Management Plan

VerifiedAdded on 2020/02/19

|18

|3691

|369

AI Summary

This assignment delves into the core concepts of strategic business management. It requires students to demonstrate their understanding of planning, performance evaluation, risk modeling, and decision-making frameworks within a business context. The provided resources encompass various perspectives on strategic management, encompassing books, journal articles, and case studies. Students are expected to synthesize these insights and apply them to develop a comprehensive strategic business management plan.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGE FINANCES

Manage Finance

Name of the Student

Name of the University

Author Note

Manage Finance

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2MANAGE FINANCES

Table of Contents

Table of Contents.................................................................................................................2

Task 1:.................................................................................................................................3

Answer to Question 1. ....................................................................................................3

Answer to Question 2......................................................................................................3

Answer to Question 3......................................................................................................4

Answer to Question 4......................................................................................................5

Answer to Question 5.....................................................................................................6

Answer to Question 7 ....................................................................................................7

Answer to Question 8 ....................................................................................................8

Task 2.................................................................................................................................11

Answer to Question 1....................................................................................................11

Answer to Question 2....................................................................................................12

Answer to Question 3....................................................................................................12

Answer to Question 5....................................................................................................14

References..........................................................................................................................16

Table of Contents

Table of Contents.................................................................................................................2

Task 1:.................................................................................................................................3

Answer to Question 1. ....................................................................................................3

Answer to Question 2......................................................................................................3

Answer to Question 3......................................................................................................4

Answer to Question 4......................................................................................................5

Answer to Question 5.....................................................................................................6

Answer to Question 7 ....................................................................................................7

Answer to Question 8 ....................................................................................................8

Task 2.................................................................................................................................11

Answer to Question 1....................................................................................................11

Answer to Question 2....................................................................................................12

Answer to Question 3....................................................................................................12

Answer to Question 5....................................................................................................14

References..........................................................................................................................16

3MANAGE FINANCES

Task 1:

Answer to Question 1.

Identify the current statutory requirements forthe tax compliance and list and

calculate the tax liabilities for Houzit Pty Ltd under taxation legislation

The requirements according to the statutory regulation that is about 9% of the

wages and also the salaries of each and every quarter and tax for the payroll is 4.75% that

is in comparison to the wages and the salaries of that particular quarter. The

compensation that is being paid to the worker is 2% of the total salary that is being paid

as wages and also the salaries. The company’s annual taxes are 30% of the net profit that

is being generated by the company. (Latina, Paraskevas and Jang, 2015)

Answer to Question 2

Identify the current compliance requirements and liabilities for this organization

under the Corporations Act 2001.

For the corporation Act 2001, that in comparison with the value of the assets of

the organization, the total amount of disclosed assets and reports of the year. The basic

requirement according to the law the basic reports that are to be kept are as follows:

General recording in the ledger for the transaction that is being carried out and

Records of cash, debtors of the company and records of sales

Records of wages and salaries that is being paid

Task 1:

Answer to Question 1.

Identify the current statutory requirements forthe tax compliance and list and

calculate the tax liabilities for Houzit Pty Ltd under taxation legislation

The requirements according to the statutory regulation that is about 9% of the

wages and also the salaries of each and every quarter and tax for the payroll is 4.75% that

is in comparison to the wages and the salaries of that particular quarter. The

compensation that is being paid to the worker is 2% of the total salary that is being paid

as wages and also the salaries. The company’s annual taxes are 30% of the net profit that

is being generated by the company. (Latina, Paraskevas and Jang, 2015)

Answer to Question 2

Identify the current compliance requirements and liabilities for this organization

under the Corporations Act 2001.

For the corporation Act 2001, that in comparison with the value of the assets of

the organization, the total amount of disclosed assets and reports of the year. The basic

requirement according to the law the basic reports that are to be kept are as follows:

General recording in the ledger for the transaction that is being carried out and

Records of cash, debtors of the company and records of sales

Records of wages and salaries that is being paid

4MANAGE FINANCES

A property registration showing transaction and other balances that is in relation

with individual item. (Cokins, 2017)

Records of the investment that are being made and records of the inventory

Calculation of the tax paid or tax return.

Answer to Question 3

Review commercially available financial management software to select the most

suitable software for Houzit Pty Ltd. Ensure you diagnose software options by comparing

two commercially available software titles against the capabilities of the existing

technology for the organization and against the prioritized requirements, and outline the

reasons that lead you to this recommendation.

There are two options in regard to the software from MYOB that will be perfect for

Houzit Pty Ltd advanced standard

control and Collect all financials

Calculate and find GST (Armstrong and Taylor, 2014).

Management of lead and prospect

Management of relationship of supplier

Tracking of stocks at different areas

Cost and pricing of the customer management

Distribution and sales management

A property registration showing transaction and other balances that is in relation

with individual item. (Cokins, 2017)

Records of the investment that are being made and records of the inventory

Calculation of the tax paid or tax return.

Answer to Question 3

Review commercially available financial management software to select the most

suitable software for Houzit Pty Ltd. Ensure you diagnose software options by comparing

two commercially available software titles against the capabilities of the existing

technology for the organization and against the prioritized requirements, and outline the

reasons that lead you to this recommendation.

There are two options in regard to the software from MYOB that will be perfect for

Houzit Pty Ltd advanced standard

control and Collect all financials

Calculate and find GST (Armstrong and Taylor, 2014).

Management of lead and prospect

Management of relationship of supplier

Tracking of stocks at different areas

Cost and pricing of the customer management

Distribution and sales management

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5MANAGE FINANCES

Self service of the client portal

The software that is mentioned here, it is good for the type of business that has the

option to increase or decrease the cash flow amount and in regard to GST. The software

is very important in nature, it helps to manage the clients of the company and also helps

to keep track of the clients that are currently present in the pipeline and to understand the

function or the process how the organization. Every other organization is different and

they have different working style, this software helps to manage the client’s base and

other functions of the business. It helps in calculating the tax of the organization and

thereby helping in the functioning of the organization. (Cokins, 2017.).

Run your business your way, with a clever, customized solution

The software helps to systemize everything in a precise and systematic way

Helps to calculate the award in the Industry

It is designed especially for large business in Australia and New-Zealand

It helps to make plans to meet future demand (Trish kina, 2014).

Answer to Question 4

Explain how you can apply the following principles of accounting in

developing the budgets required for this task matching principle

In every quarter the revenue is to be matched with the expenses that are in relation

to the revenue. The revenue is to be matched with the items that are being sold within the

time period of the group of accounts. In creation of the budget the accounts groups that

are being used are Assets, equity, liability etc. In preparing the budget for the current

Self service of the client portal

The software that is mentioned here, it is good for the type of business that has the

option to increase or decrease the cash flow amount and in regard to GST. The software

is very important in nature, it helps to manage the clients of the company and also helps

to keep track of the clients that are currently present in the pipeline and to understand the

function or the process how the organization. Every other organization is different and

they have different working style, this software helps to manage the client’s base and

other functions of the business. It helps in calculating the tax of the organization and

thereby helping in the functioning of the organization. (Cokins, 2017.).

Run your business your way, with a clever, customized solution

The software helps to systemize everything in a precise and systematic way

Helps to calculate the award in the Industry

It is designed especially for large business in Australia and New-Zealand

It helps to make plans to meet future demand (Trish kina, 2014).

Answer to Question 4

Explain how you can apply the following principles of accounting in

developing the budgets required for this task matching principle

In every quarter the revenue is to be matched with the expenses that are in relation

to the revenue. The revenue is to be matched with the items that are being sold within the

time period of the group of accounts. In creation of the budget the accounts groups that

are being used are Assets, equity, liability etc. In preparing the budget for the current

6MANAGE FINANCES

financial year all the information in regard to the finance are being recorded in a

systematic manner such that a budget and be made from the following information. The

information is being recorded such that it helps the stake holders of the organization. The

budget also helps any person who is in relation of the organization and thereby is in

relation of the organization. (Barthelme et al, 2014)

Answer to Question 5.

Explain and discuss the implications of probity when preparing and revising

budgets.

While preparing the budget for the organization I have to keep in mind about all

the rules and clauses of the finance and should abide by them. Apart from that it is also to

be kept in mind that the ethics should be followed. Anything that is to be done or any

decision that is to be taken should be taken keeping in mind the ethics of the organization

and they should be strictly followed. Nothing should be done which is out of the ethical

context. A strong ethics will help the organization to strengthen its pillars. The activity

which is fraudulent in nature should be avoided in order to have a clean record and to see

that the ethical code of the organization should never be broken or compromised under

any circumstances whatsoever. (Dai et al, 2014).

Answer to Question 7

List the items you would recommend for inclusion in the budgets for Houzit

Pty Ltd. Store supplies or new car or Software upgrade.

Plan for information regarding budget of the organization

financial year all the information in regard to the finance are being recorded in a

systematic manner such that a budget and be made from the following information. The

information is being recorded such that it helps the stake holders of the organization. The

budget also helps any person who is in relation of the organization and thereby is in

relation of the organization. (Barthelme et al, 2014)

Answer to Question 5.

Explain and discuss the implications of probity when preparing and revising

budgets.

While preparing the budget for the organization I have to keep in mind about all

the rules and clauses of the finance and should abide by them. Apart from that it is also to

be kept in mind that the ethics should be followed. Anything that is to be done or any

decision that is to be taken should be taken keeping in mind the ethics of the organization

and they should be strictly followed. Nothing should be done which is out of the ethical

context. A strong ethics will help the organization to strengthen its pillars. The activity

which is fraudulent in nature should be avoided in order to have a clean record and to see

that the ethical code of the organization should never be broken or compromised under

any circumstances whatsoever. (Dai et al, 2014).

Answer to Question 7

List the items you would recommend for inclusion in the budgets for Houzit

Pty Ltd. Store supplies or new car or Software upgrade.

Plan for information regarding budget of the organization

7MANAGE FINANCES

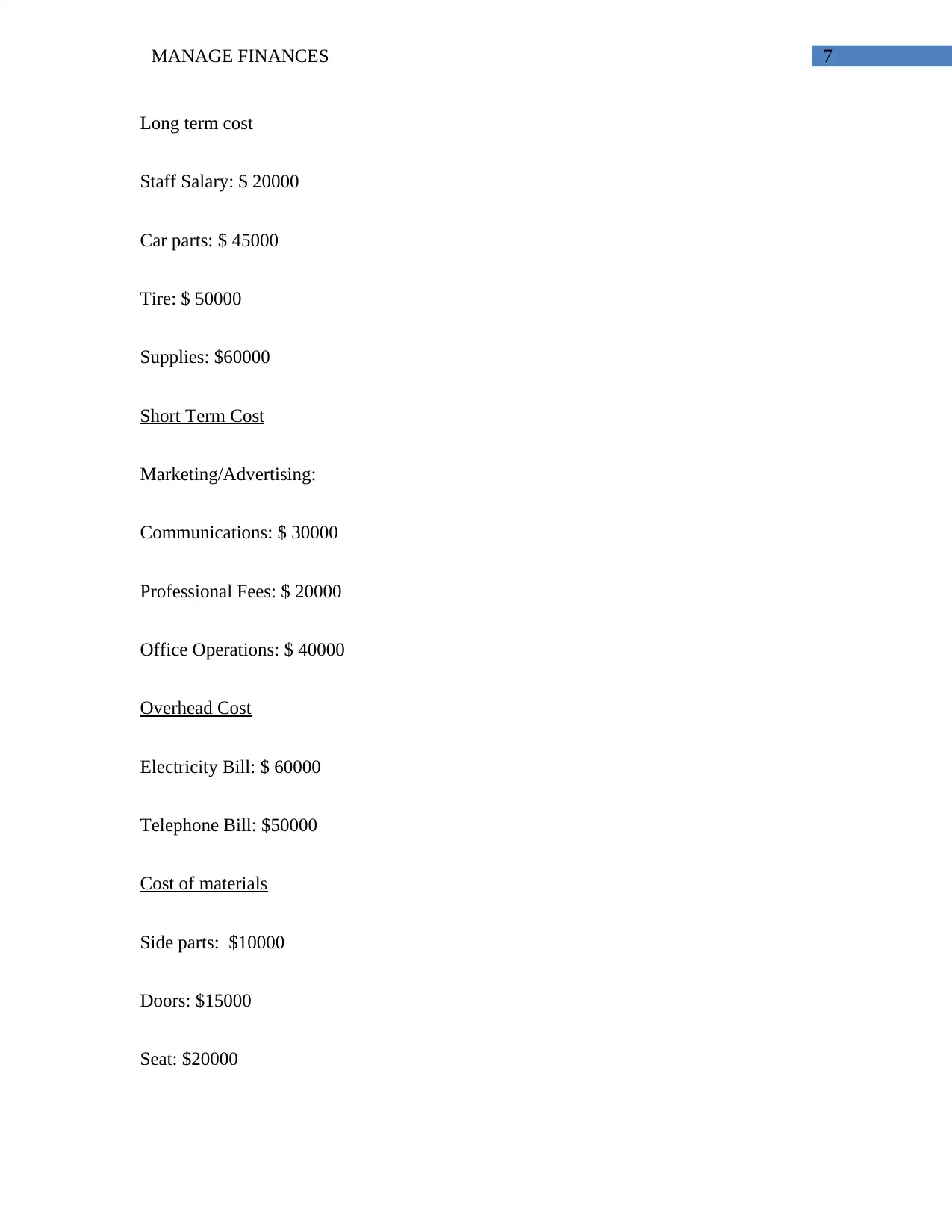

Long term cost

Staff Salary: $ 20000

Car parts: $ 45000

Tire: $ 50000

Supplies: $60000

Short Term Cost

Marketing/Advertising:

Communications: $ 30000

Professional Fees: $ 20000

Office Operations: $ 40000

Overhead Cost

Electricity Bill: $ 60000

Telephone Bill: $50000

Cost of materials

Side parts: $10000

Doors: $15000

Seat: $20000

Long term cost

Staff Salary: $ 20000

Car parts: $ 45000

Tire: $ 50000

Supplies: $60000

Short Term Cost

Marketing/Advertising:

Communications: $ 30000

Professional Fees: $ 20000

Office Operations: $ 40000

Overhead Cost

Electricity Bill: $ 60000

Telephone Bill: $50000

Cost of materials

Side parts: $10000

Doors: $15000

Seat: $20000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8MANAGE FINANCES

Finishing: $ 25000

Answer to Question 8

List the new or modified internal controls that could improve risk

management for Houzit Pty Ltd including the maintenance of audit trails.

Recording of the discounts

Maintaining cash register daily.

There should be proper form of authorization

Lines of communication should be open

There is a business separation need

Description of job

Minimize the possibility of fraudulent activities (Haines, 2015)

Information and technology which are current in nature

Make sure the systems are carefully selected and tested and staff fully trained.

Finishing: $ 25000

Answer to Question 8

List the new or modified internal controls that could improve risk

management for Houzit Pty Ltd including the maintenance of audit trails.

Recording of the discounts

Maintaining cash register daily.

There should be proper form of authorization

Lines of communication should be open

There is a business separation need

Description of job

Minimize the possibility of fraudulent activities (Haines, 2015)

Information and technology which are current in nature

Make sure the systems are carefully selected and tested and staff fully trained.

9MANAGE FINANCES

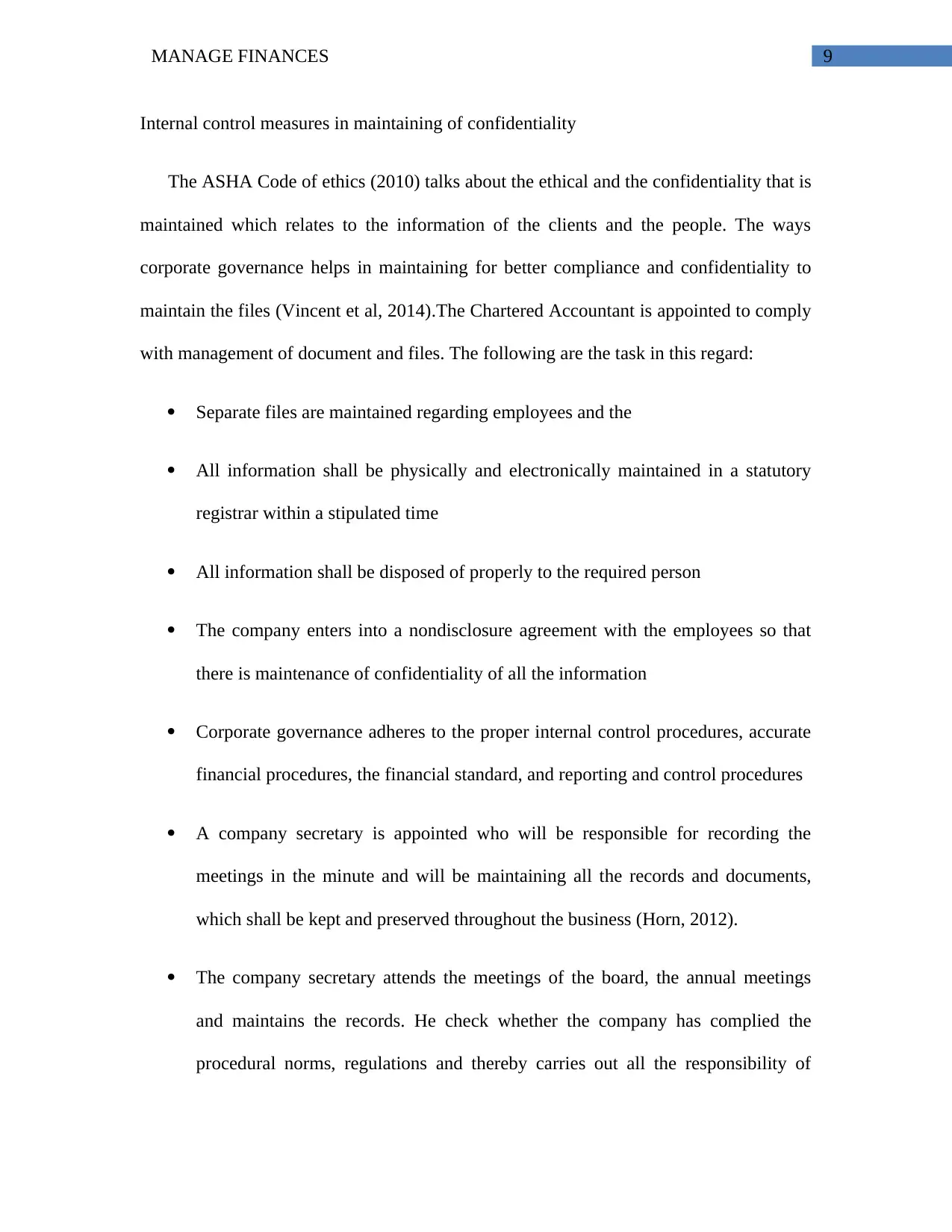

Internal control measures in maintaining of confidentiality

The ASHA Code of ethics (2010) talks about the ethical and the confidentiality that is

maintained which relates to the information of the clients and the people. The ways

corporate governance helps in maintaining for better compliance and confidentiality to

maintain the files (Vincent et al, 2014).The Chartered Accountant is appointed to comply

with management of document and files. The following are the task in this regard:

Separate files are maintained regarding employees and the

All information shall be physically and electronically maintained in a statutory

registrar within a stipulated time

All information shall be disposed of properly to the required person

The company enters into a nondisclosure agreement with the employees so that

there is maintenance of confidentiality of all the information

Corporate governance adheres to the proper internal control procedures, accurate

financial procedures, the financial standard, and reporting and control procedures

A company secretary is appointed who will be responsible for recording the

meetings in the minute and will be maintaining all the records and documents,

which shall be kept and preserved throughout the business (Horn, 2012).

The company secretary attends the meetings of the board, the annual meetings

and maintains the records. He check whether the company has complied the

procedural norms, regulations and thereby carries out all the responsibility of

Internal control measures in maintaining of confidentiality

The ASHA Code of ethics (2010) talks about the ethical and the confidentiality that is

maintained which relates to the information of the clients and the people. The ways

corporate governance helps in maintaining for better compliance and confidentiality to

maintain the files (Vincent et al, 2014).The Chartered Accountant is appointed to comply

with management of document and files. The following are the task in this regard:

Separate files are maintained regarding employees and the

All information shall be physically and electronically maintained in a statutory

registrar within a stipulated time

All information shall be disposed of properly to the required person

The company enters into a nondisclosure agreement with the employees so that

there is maintenance of confidentiality of all the information

Corporate governance adheres to the proper internal control procedures, accurate

financial procedures, the financial standard, and reporting and control procedures

A company secretary is appointed who will be responsible for recording the

meetings in the minute and will be maintaining all the records and documents,

which shall be kept and preserved throughout the business (Horn, 2012).

The company secretary attends the meetings of the board, the annual meetings

and maintains the records. He check whether the company has complied the

procedural norms, regulations and thereby carries out all the responsibility of

10MANAGE FINANCES

carrying out the secretarial duties as instructed by the directors of the company

(Jason et al., 2016).

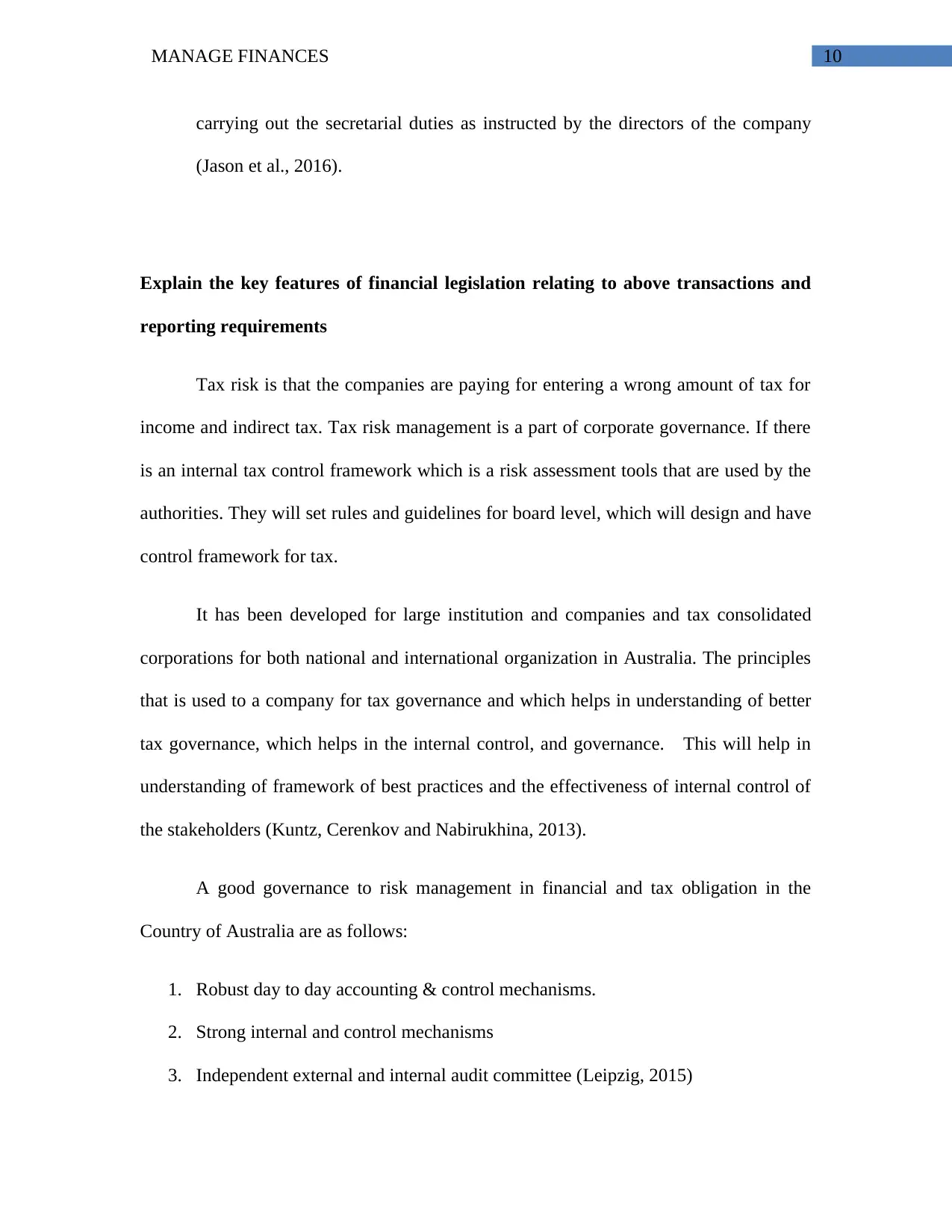

Explain the key features of financial legislation relating to above transactions and

reporting requirements

Tax risk is that the companies are paying for entering a wrong amount of tax for

income and indirect tax. Tax risk management is a part of corporate governance. If there

is an internal tax control framework which is a risk assessment tools that are used by the

authorities. They will set rules and guidelines for board level, which will design and have

control framework for tax.

It has been developed for large institution and companies and tax consolidated

corporations for both national and international organization in Australia. The principles

that is used to a company for tax governance and which helps in understanding of better

tax governance, which helps in the internal control, and governance. This will help in

understanding of framework of best practices and the effectiveness of internal control of

the stakeholders (Kuntz, Cerenkov and Nabirukhina, 2013).

A good governance to risk management in financial and tax obligation in the

Country of Australia are as follows:

1. Robust day to day accounting & control mechanisms.

2. Strong internal and control mechanisms

3. Independent external and internal audit committee (Leipzig, 2015)

carrying out the secretarial duties as instructed by the directors of the company

(Jason et al., 2016).

Explain the key features of financial legislation relating to above transactions and

reporting requirements

Tax risk is that the companies are paying for entering a wrong amount of tax for

income and indirect tax. Tax risk management is a part of corporate governance. If there

is an internal tax control framework which is a risk assessment tools that are used by the

authorities. They will set rules and guidelines for board level, which will design and have

control framework for tax.

It has been developed for large institution and companies and tax consolidated

corporations for both national and international organization in Australia. The principles

that is used to a company for tax governance and which helps in understanding of better

tax governance, which helps in the internal control, and governance. This will help in

understanding of framework of best practices and the effectiveness of internal control of

the stakeholders (Kuntz, Cerenkov and Nabirukhina, 2013).

A good governance to risk management in financial and tax obligation in the

Country of Australia are as follows:

1. Robust day to day accounting & control mechanisms.

2. Strong internal and control mechanisms

3. Independent external and internal audit committee (Leipzig, 2015)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11MANAGE FINANCES

4. Separation of role from the external auditor with tax advisor

5. The code of conduct and tax structures

6. Accountabilities in relation to tax decisions

7. . Adequate resorting of the tax function

8. Transparency with tax officers

9. Board & senior management have a line of sight on tax risk management.

10. Responsive to changes in the environment, law etc.

11. Tax is considered as part of the decision making process for major transactions.

Task 2

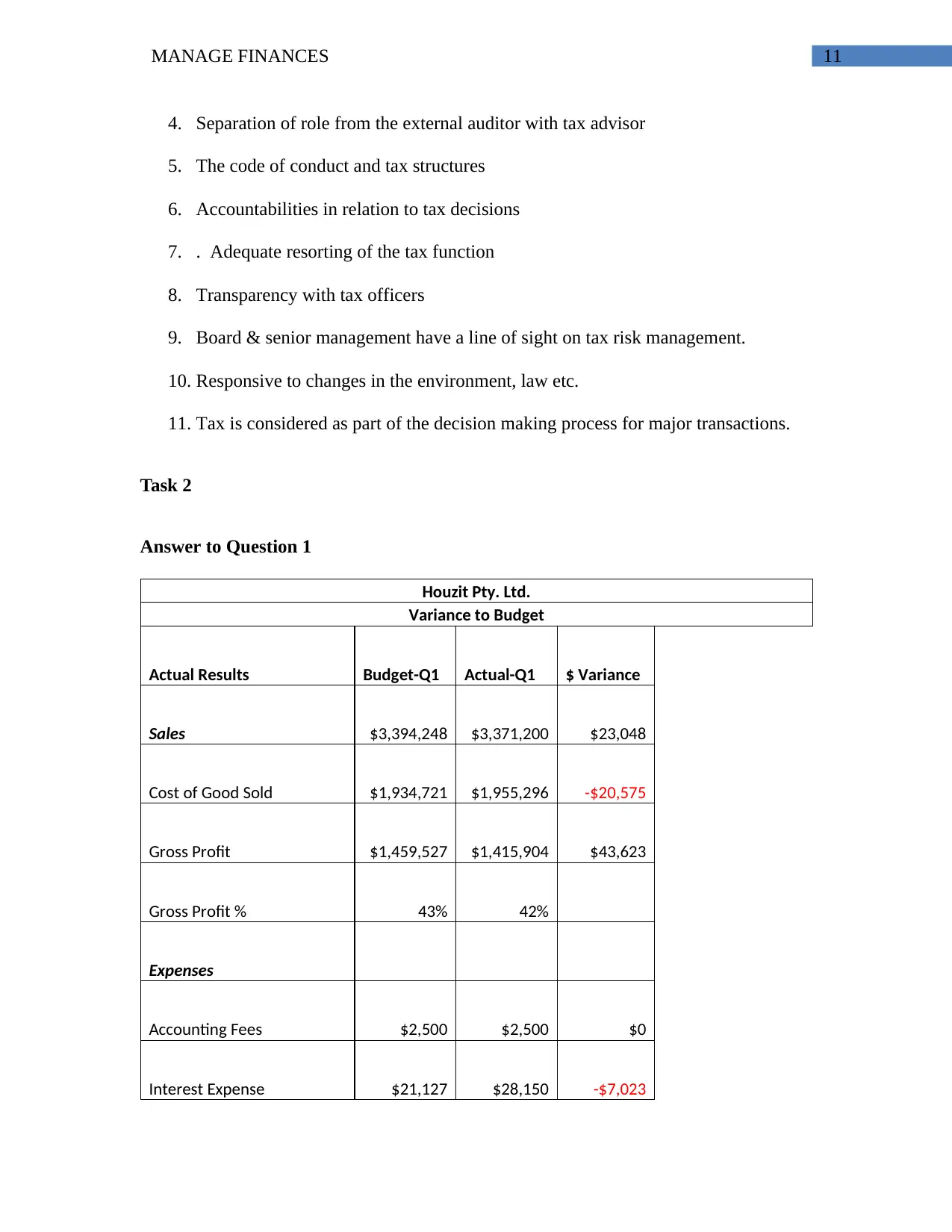

Answer to Question 1

Houzit Pty. Ltd.

Variance to Budget

Actual Results Budget-Q1 Actual-Q1 $ Variance

Sales $3,394,248 $3,371,200 $23,048

Cost of Good Sold $1,934,721 $1,955,296 -$20,575

Gross Profit $1,459,527 $1,415,904 $43,623

Gross Profit % 43% 42%

Expenses

Accounting Fees $2,500 $2,500 $0

Interest Expense $21,127 $28,150 -$7,023

4. Separation of role from the external auditor with tax advisor

5. The code of conduct and tax structures

6. Accountabilities in relation to tax decisions

7. . Adequate resorting of the tax function

8. Transparency with tax officers

9. Board & senior management have a line of sight on tax risk management.

10. Responsive to changes in the environment, law etc.

11. Tax is considered as part of the decision making process for major transactions.

Task 2

Answer to Question 1

Houzit Pty. Ltd.

Variance to Budget

Actual Results Budget-Q1 Actual-Q1 $ Variance

Sales $3,394,248 $3,371,200 $23,048

Cost of Good Sold $1,934,721 $1,955,296 -$20,575

Gross Profit $1,459,527 $1,415,904 $43,623

Gross Profit % 43% 42%

Expenses

Accounting Fees $2,500 $2,500 $0

Interest Expense $21,127 $28,150 -$7,023

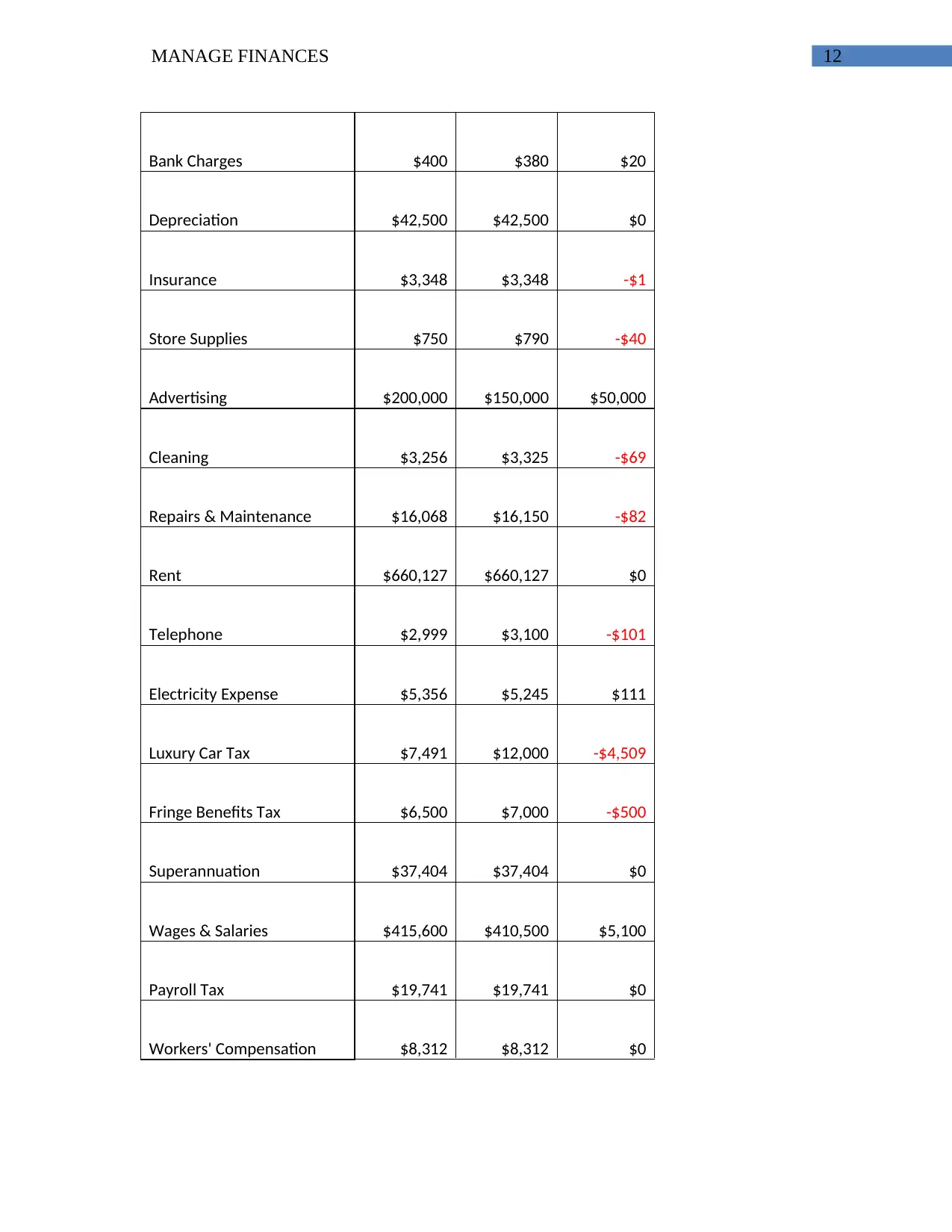

12MANAGE FINANCES

Bank Charges $400 $380 $20

Depreciation $42,500 $42,500 $0

Insurance $3,348 $3,348 -$1

Store Supplies $750 $790 -$40

Advertising $200,000 $150,000 $50,000

Cleaning $3,256 $3,325 -$69

Repairs & Maintenance $16,068 $16,150 -$82

Rent $660,127 $660,127 $0

Telephone $2,999 $3,100 -$101

Electricity Expense $5,356 $5,245 $111

Luxury Car Tax $7,491 $12,000 -$4,509

Fringe Benefits Tax $6,500 $7,000 -$500

Superannuation $37,404 $37,404 $0

Wages & Salaries $415,600 $410,500 $5,100

Payroll Tax $19,741 $19,741 $0

Workers' Compensation $8,312 $8,312 $0

Bank Charges $400 $380 $20

Depreciation $42,500 $42,500 $0

Insurance $3,348 $3,348 -$1

Store Supplies $750 $790 -$40

Advertising $200,000 $150,000 $50,000

Cleaning $3,256 $3,325 -$69

Repairs & Maintenance $16,068 $16,150 -$82

Rent $660,127 $660,127 $0

Telephone $2,999 $3,100 -$101

Electricity Expense $5,356 $5,245 $111

Luxury Car Tax $7,491 $12,000 -$4,509

Fringe Benefits Tax $6,500 $7,000 -$500

Superannuation $37,404 $37,404 $0

Wages & Salaries $415,600 $410,500 $5,100

Payroll Tax $19,741 $19,741 $0

Workers' Compensation $8,312 $8,312 $0

13MANAGE FINANCES

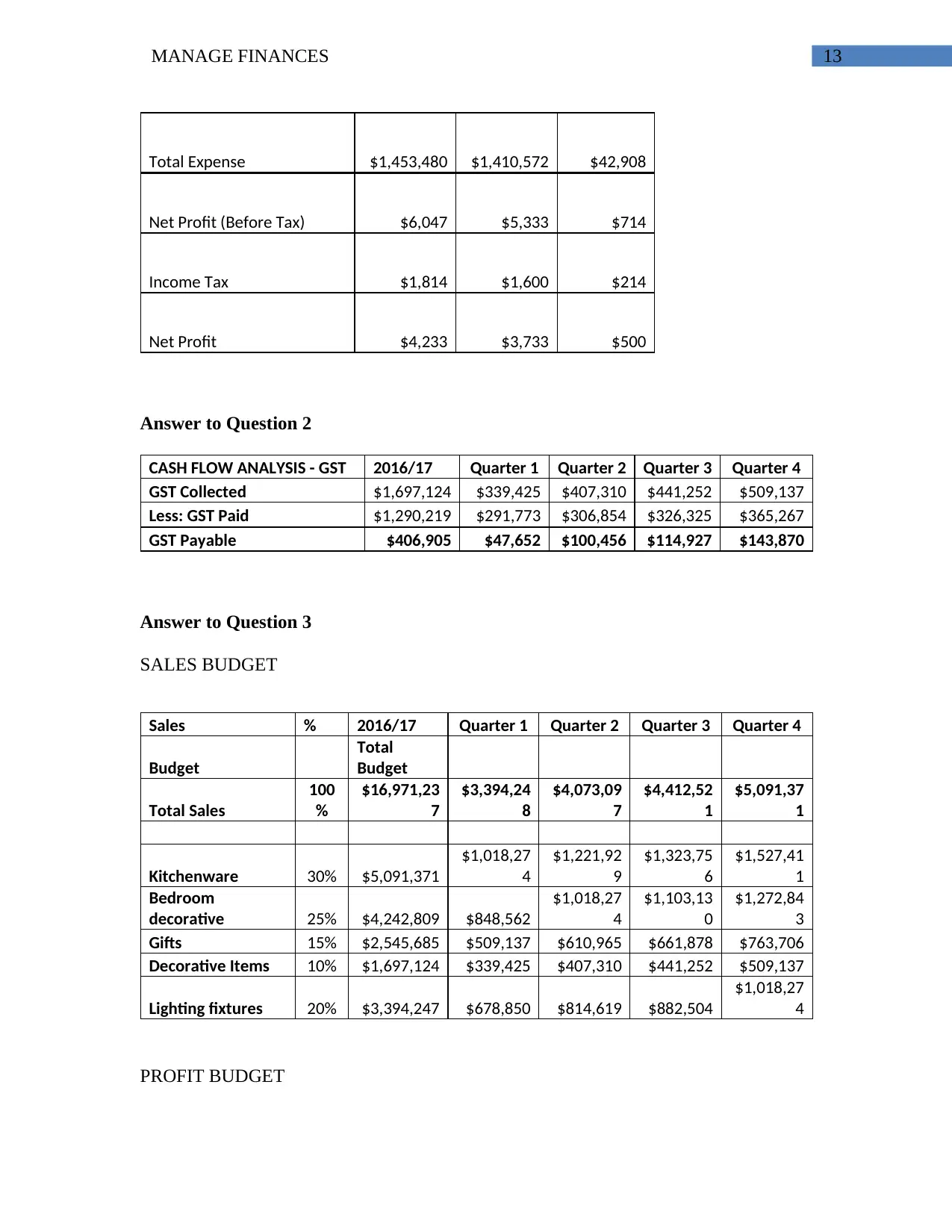

Total Expense $1,453,480 $1,410,572 $42,908

Net Profit (Before Tax) $6,047 $5,333 $714

Income Tax $1,814 $1,600 $214

Net Profit $4,233 $3,733 $500

Answer to Question 2

CASH FLOW ANALYSIS - GST 2016/17 Quarter 1 Quarter 2 Quarter 3 Quarter 4

GST Collected $1,697,124 $339,425 $407,310 $441,252 $509,137

Less: GST Paid $1,290,219 $291,773 $306,854 $326,325 $365,267

GST Payable $406,905 $47,652 $100,456 $114,927 $143,870

Answer to Question 3

SALES BUDGET

Sales % 2016/17 Quarter 1 Quarter 2 Quarter 3 Quarter 4

Budget

Total

Budget

Total Sales

100

%

$16,971,23

7

$3,394,24

8

$4,073,09

7

$4,412,52

1

$5,091,37

1

Kitchenware 30% $5,091,371

$1,018,27

4

$1,221,92

9

$1,323,75

6

$1,527,41

1

Bedroom

decorative 25% $4,242,809 $848,562

$1,018,27

4

$1,103,13

0

$1,272,84

3

Gifts 15% $2,545,685 $509,137 $610,965 $661,878 $763,706

Decorative Items 10% $1,697,124 $339,425 $407,310 $441,252 $509,137

Lighting fixtures 20% $3,394,247 $678,850 $814,619 $882,504

$1,018,27

4

PROFIT BUDGET

Total Expense $1,453,480 $1,410,572 $42,908

Net Profit (Before Tax) $6,047 $5,333 $714

Income Tax $1,814 $1,600 $214

Net Profit $4,233 $3,733 $500

Answer to Question 2

CASH FLOW ANALYSIS - GST 2016/17 Quarter 1 Quarter 2 Quarter 3 Quarter 4

GST Collected $1,697,124 $339,425 $407,310 $441,252 $509,137

Less: GST Paid $1,290,219 $291,773 $306,854 $326,325 $365,267

GST Payable $406,905 $47,652 $100,456 $114,927 $143,870

Answer to Question 3

SALES BUDGET

Sales % 2016/17 Quarter 1 Quarter 2 Quarter 3 Quarter 4

Budget

Total

Budget

Total Sales

100

%

$16,971,23

7

$3,394,24

8

$4,073,09

7

$4,412,52

1

$5,091,37

1

Kitchenware 30% $5,091,371

$1,018,27

4

$1,221,92

9

$1,323,75

6

$1,527,41

1

Bedroom

decorative 25% $4,242,809 $848,562

$1,018,27

4

$1,103,13

0

$1,272,84

3

Gifts 15% $2,545,685 $509,137 $610,965 $661,878 $763,706

Decorative Items 10% $1,697,124 $339,425 $407,310 $441,252 $509,137

Lighting fixtures 20% $3,394,247 $678,850 $814,619 $882,504

$1,018,27

4

PROFIT BUDGET

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14MANAGE FINANCES

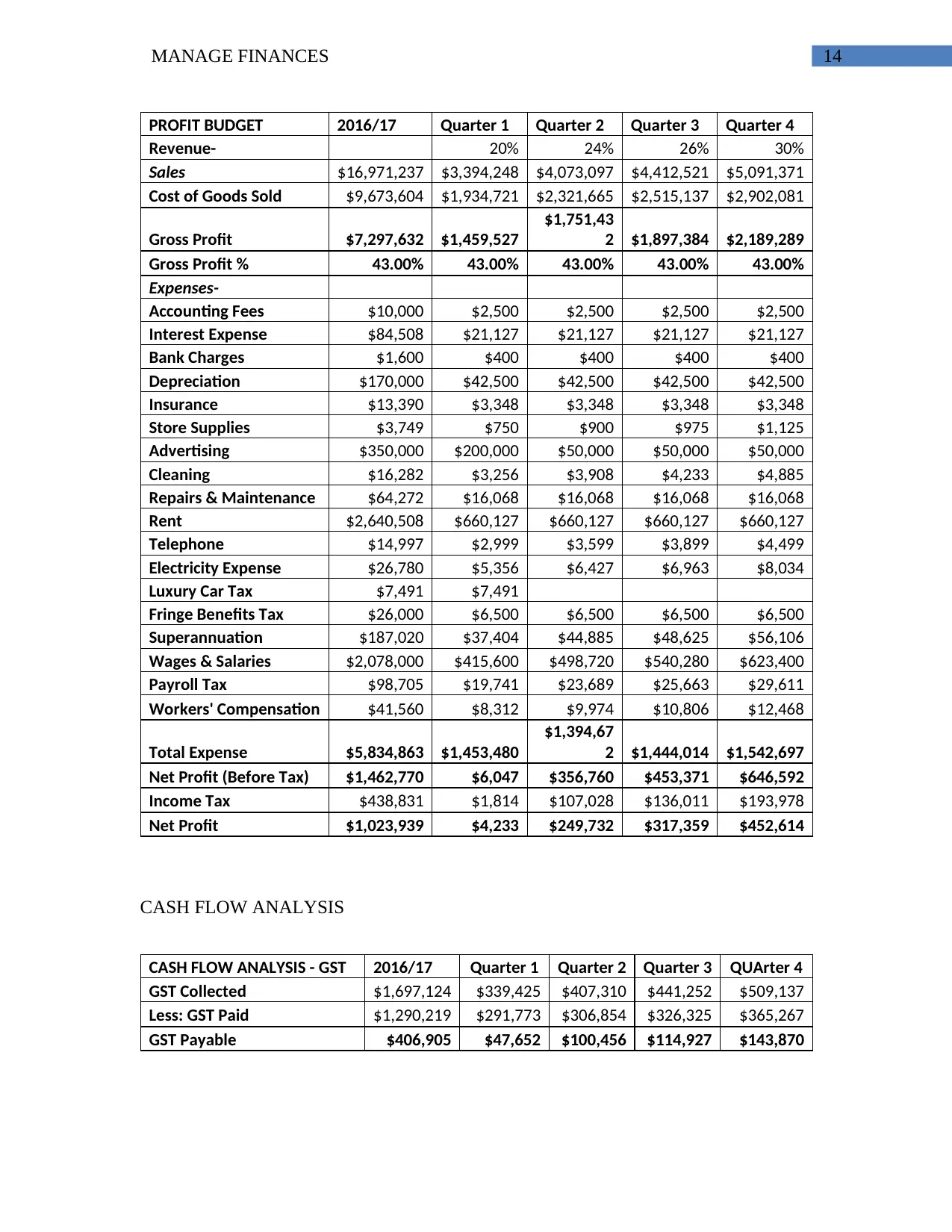

PROFIT BUDGET 2016/17 Quarter 1 Quarter 2 Quarter 3 Quarter 4

Revenue- 20% 24% 26% 30%

Sales $16,971,237 $3,394,248 $4,073,097 $4,412,521 $5,091,371

Cost of Goods Sold $9,673,604 $1,934,721 $2,321,665 $2,515,137 $2,902,081

Gross Profit $7,297,632 $1,459,527

$1,751,43

2 $1,897,384 $2,189,289

Gross Profit % 43.00% 43.00% 43.00% 43.00% 43.00%

Expenses-

Accounting Fees $10,000 $2,500 $2,500 $2,500 $2,500

Interest Expense $84,508 $21,127 $21,127 $21,127 $21,127

Bank Charges $1,600 $400 $400 $400 $400

Depreciation $170,000 $42,500 $42,500 $42,500 $42,500

Insurance $13,390 $3,348 $3,348 $3,348 $3,348

Store Supplies $3,749 $750 $900 $975 $1,125

Advertising $350,000 $200,000 $50,000 $50,000 $50,000

Cleaning $16,282 $3,256 $3,908 $4,233 $4,885

Repairs & Maintenance $64,272 $16,068 $16,068 $16,068 $16,068

Rent $2,640,508 $660,127 $660,127 $660,127 $660,127

Telephone $14,997 $2,999 $3,599 $3,899 $4,499

Electricity Expense $26,780 $5,356 $6,427 $6,963 $8,034

Luxury Car Tax $7,491 $7,491

Fringe Benefits Tax $26,000 $6,500 $6,500 $6,500 $6,500

Superannuation $187,020 $37,404 $44,885 $48,625 $56,106

Wages & Salaries $2,078,000 $415,600 $498,720 $540,280 $623,400

Payroll Tax $98,705 $19,741 $23,689 $25,663 $29,611

Workers' Compensation $41,560 $8,312 $9,974 $10,806 $12,468

Total Expense $5,834,863 $1,453,480

$1,394,67

2 $1,444,014 $1,542,697

Net Profit (Before Tax) $1,462,770 $6,047 $356,760 $453,371 $646,592

Income Tax $438,831 $1,814 $107,028 $136,011 $193,978

Net Profit $1,023,939 $4,233 $249,732 $317,359 $452,614

CASH FLOW ANALYSIS

CASH FLOW ANALYSIS - GST 2016/17 Quarter 1 Quarter 2 Quarter 3 QUArter 4

GST Collected $1,697,124 $339,425 $407,310 $441,252 $509,137

Less: GST Paid $1,290,219 $291,773 $306,854 $326,325 $365,267

GST Payable $406,905 $47,652 $100,456 $114,927 $143,870

PROFIT BUDGET 2016/17 Quarter 1 Quarter 2 Quarter 3 Quarter 4

Revenue- 20% 24% 26% 30%

Sales $16,971,237 $3,394,248 $4,073,097 $4,412,521 $5,091,371

Cost of Goods Sold $9,673,604 $1,934,721 $2,321,665 $2,515,137 $2,902,081

Gross Profit $7,297,632 $1,459,527

$1,751,43

2 $1,897,384 $2,189,289

Gross Profit % 43.00% 43.00% 43.00% 43.00% 43.00%

Expenses-

Accounting Fees $10,000 $2,500 $2,500 $2,500 $2,500

Interest Expense $84,508 $21,127 $21,127 $21,127 $21,127

Bank Charges $1,600 $400 $400 $400 $400

Depreciation $170,000 $42,500 $42,500 $42,500 $42,500

Insurance $13,390 $3,348 $3,348 $3,348 $3,348

Store Supplies $3,749 $750 $900 $975 $1,125

Advertising $350,000 $200,000 $50,000 $50,000 $50,000

Cleaning $16,282 $3,256 $3,908 $4,233 $4,885

Repairs & Maintenance $64,272 $16,068 $16,068 $16,068 $16,068

Rent $2,640,508 $660,127 $660,127 $660,127 $660,127

Telephone $14,997 $2,999 $3,599 $3,899 $4,499

Electricity Expense $26,780 $5,356 $6,427 $6,963 $8,034

Luxury Car Tax $7,491 $7,491

Fringe Benefits Tax $26,000 $6,500 $6,500 $6,500 $6,500

Superannuation $187,020 $37,404 $44,885 $48,625 $56,106

Wages & Salaries $2,078,000 $415,600 $498,720 $540,280 $623,400

Payroll Tax $98,705 $19,741 $23,689 $25,663 $29,611

Workers' Compensation $41,560 $8,312 $9,974 $10,806 $12,468

Total Expense $5,834,863 $1,453,480

$1,394,67

2 $1,444,014 $1,542,697

Net Profit (Before Tax) $1,462,770 $6,047 $356,760 $453,371 $646,592

Income Tax $438,831 $1,814 $107,028 $136,011 $193,978

Net Profit $1,023,939 $4,233 $249,732 $317,359 $452,614

CASH FLOW ANALYSIS

CASH FLOW ANALYSIS - GST 2016/17 Quarter 1 Quarter 2 Quarter 3 QUArter 4

GST Collected $1,697,124 $339,425 $407,310 $441,252 $509,137

Less: GST Paid $1,290,219 $291,773 $306,854 $326,325 $365,267

GST Payable $406,905 $47,652 $100,456 $114,927 $143,870

15MANAGE FINANCES

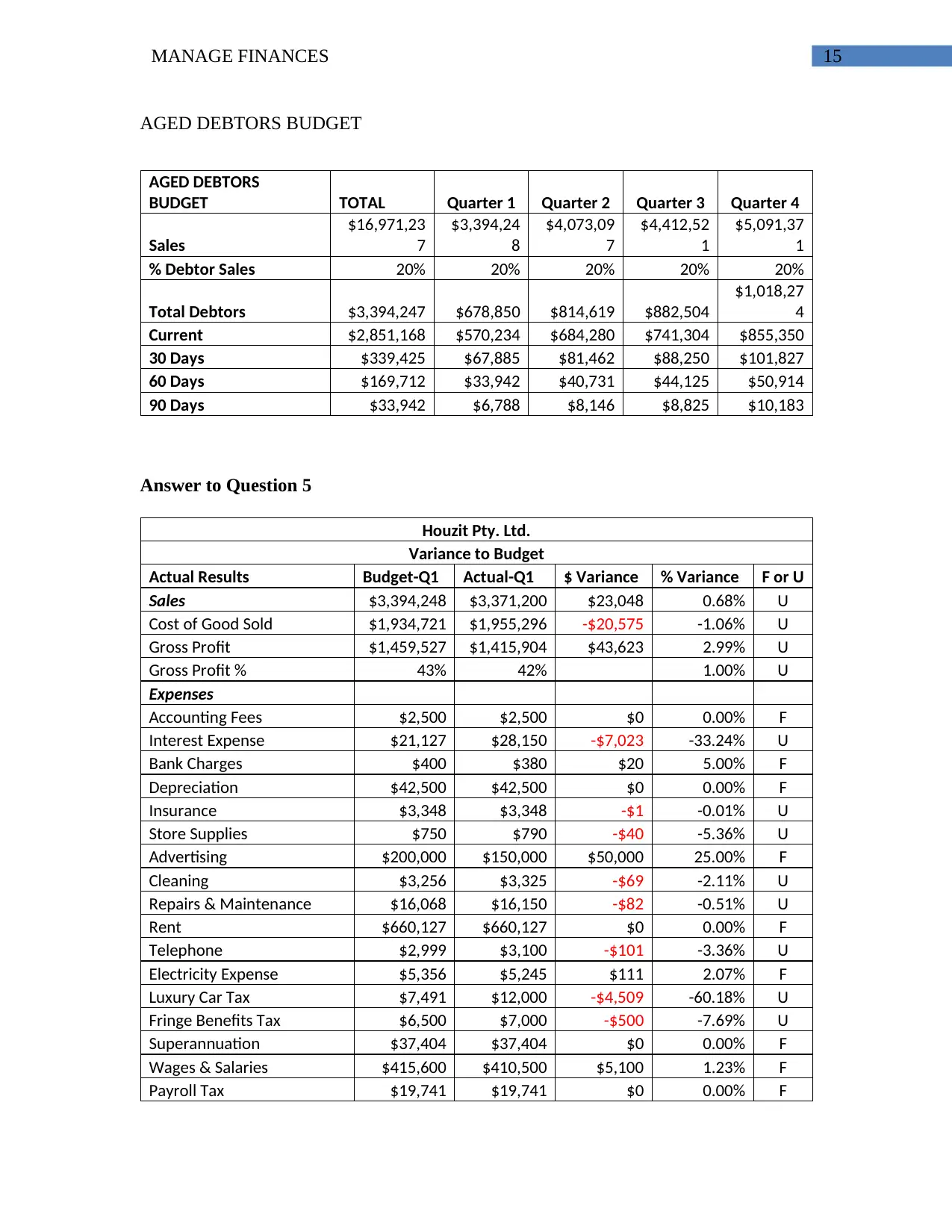

AGED DEBTORS BUDGET

AGED DEBTORS

BUDGET TOTAL Quarter 1 Quarter 2 Quarter 3 Quarter 4

Sales

$16,971,23

7

$3,394,24

8

$4,073,09

7

$4,412,52

1

$5,091,37

1

% Debtor Sales 20% 20% 20% 20% 20%

Total Debtors $3,394,247 $678,850 $814,619 $882,504

$1,018,27

4

Current $2,851,168 $570,234 $684,280 $741,304 $855,350

30 Days $339,425 $67,885 $81,462 $88,250 $101,827

60 Days $169,712 $33,942 $40,731 $44,125 $50,914

90 Days $33,942 $6,788 $8,146 $8,825 $10,183

Answer to Question 5

Houzit Pty. Ltd.

Variance to Budget

Actual Results Budget-Q1 Actual-Q1 $ Variance % Variance F or U

Sales $3,394,248 $3,371,200 $23,048 0.68% U

Cost of Good Sold $1,934,721 $1,955,296 -$20,575 -1.06% U

Gross Profit $1,459,527 $1,415,904 $43,623 2.99% U

Gross Profit % 43% 42% 1.00% U

Expenses

Accounting Fees $2,500 $2,500 $0 0.00% F

Interest Expense $21,127 $28,150 -$7,023 -33.24% U

Bank Charges $400 $380 $20 5.00% F

Depreciation $42,500 $42,500 $0 0.00% F

Insurance $3,348 $3,348 -$1 -0.01% U

Store Supplies $750 $790 -$40 -5.36% U

Advertising $200,000 $150,000 $50,000 25.00% F

Cleaning $3,256 $3,325 -$69 -2.11% U

Repairs & Maintenance $16,068 $16,150 -$82 -0.51% U

Rent $660,127 $660,127 $0 0.00% F

Telephone $2,999 $3,100 -$101 -3.36% U

Electricity Expense $5,356 $5,245 $111 2.07% F

Luxury Car Tax $7,491 $12,000 -$4,509 -60.18% U

Fringe Benefits Tax $6,500 $7,000 -$500 -7.69% U

Superannuation $37,404 $37,404 $0 0.00% F

Wages & Salaries $415,600 $410,500 $5,100 1.23% F

Payroll Tax $19,741 $19,741 $0 0.00% F

AGED DEBTORS BUDGET

AGED DEBTORS

BUDGET TOTAL Quarter 1 Quarter 2 Quarter 3 Quarter 4

Sales

$16,971,23

7

$3,394,24

8

$4,073,09

7

$4,412,52

1

$5,091,37

1

% Debtor Sales 20% 20% 20% 20% 20%

Total Debtors $3,394,247 $678,850 $814,619 $882,504

$1,018,27

4

Current $2,851,168 $570,234 $684,280 $741,304 $855,350

30 Days $339,425 $67,885 $81,462 $88,250 $101,827

60 Days $169,712 $33,942 $40,731 $44,125 $50,914

90 Days $33,942 $6,788 $8,146 $8,825 $10,183

Answer to Question 5

Houzit Pty. Ltd.

Variance to Budget

Actual Results Budget-Q1 Actual-Q1 $ Variance % Variance F or U

Sales $3,394,248 $3,371,200 $23,048 0.68% U

Cost of Good Sold $1,934,721 $1,955,296 -$20,575 -1.06% U

Gross Profit $1,459,527 $1,415,904 $43,623 2.99% U

Gross Profit % 43% 42% 1.00% U

Expenses

Accounting Fees $2,500 $2,500 $0 0.00% F

Interest Expense $21,127 $28,150 -$7,023 -33.24% U

Bank Charges $400 $380 $20 5.00% F

Depreciation $42,500 $42,500 $0 0.00% F

Insurance $3,348 $3,348 -$1 -0.01% U

Store Supplies $750 $790 -$40 -5.36% U

Advertising $200,000 $150,000 $50,000 25.00% F

Cleaning $3,256 $3,325 -$69 -2.11% U

Repairs & Maintenance $16,068 $16,150 -$82 -0.51% U

Rent $660,127 $660,127 $0 0.00% F

Telephone $2,999 $3,100 -$101 -3.36% U

Electricity Expense $5,356 $5,245 $111 2.07% F

Luxury Car Tax $7,491 $12,000 -$4,509 -60.18% U

Fringe Benefits Tax $6,500 $7,000 -$500 -7.69% U

Superannuation $37,404 $37,404 $0 0.00% F

Wages & Salaries $415,600 $410,500 $5,100 1.23% F

Payroll Tax $19,741 $19,741 $0 0.00% F

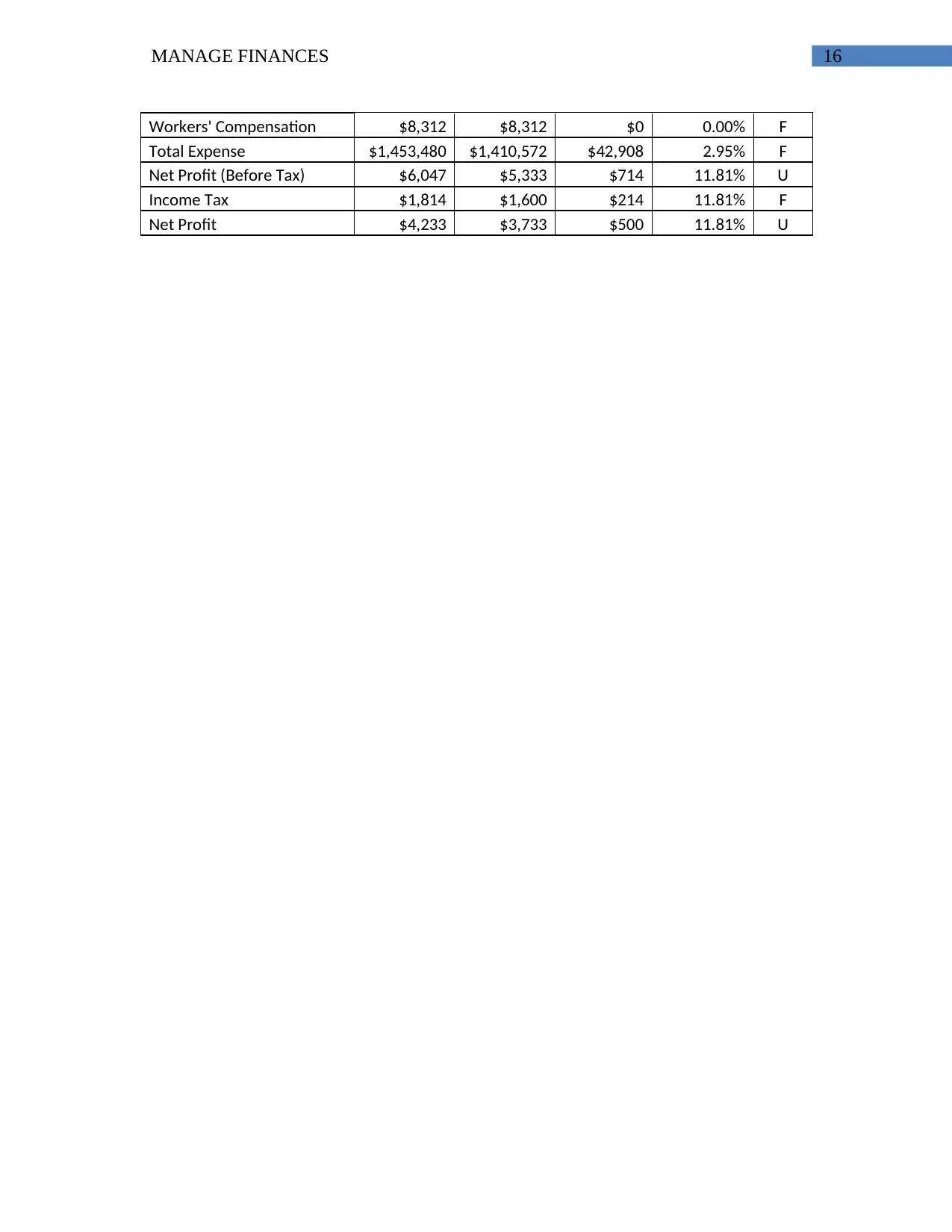

16MANAGE FINANCES

Workers' Compensation $8,312 $8,312 $0 0.00% F

Total Expense $1,453,480 $1,410,572 $42,908 2.95% F

Net Profit (Before Tax) $6,047 $5,333 $714 11.81% U

Income Tax $1,814 $1,600 $214 11.81% F

Net Profit $4,233 $3,733 $500 11.81% U

Workers' Compensation $8,312 $8,312 $0 0.00% F

Total Expense $1,453,480 $1,410,572 $42,908 2.95% F

Net Profit (Before Tax) $6,047 $5,333 $714 11.81% U

Income Tax $1,814 $1,600 $214 11.81% F

Net Profit $4,233 $3,733 $500 11.81% U

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

17MANAGE FINANCES

References

Armstrong, M., and Taylor, S. (2014). Armstrong's handbook of human resource

management practice Cogan Page Publishers.

Barthelme, R.M., Barkley, W.C., Oliver, P.M., Claymont, V. and Puckett, R., 2014

Academy of Nutrition and Dietetics: Revised 2014 standards of professional performance

for registered dietitian nutritionists in management of food and nutrition systems. Journal

of the Academy of Nutrition and Dietetics, 114(7), pp.1104-1112

Belay-Palmer, A. and Kinetic, I., 2015 22 Building sustainable communities through

alternative food systems Handbook on the Globalization of Agriculture, p.446

Butteries, S. C., Butteries, S. C., Gaudi, D., Gaudi, D., Dye, P., and Dye, P. (2016)

Continuous quality improvement in a Maltese hospital using logical framework

analysis. Journal of health organization and management, 30(7), 1026-1046.

Chiai, A., and Round, H. (2015) A Developmental Learning Framework for Business

Report Writing: Guidance for Management Educators”. Journal of Adolescent and Adult

Literacy, 45(7), 556-566.

Cokins, G., 2017 Strategic business management: From planning to performance. John

Wiley & Sons

Dai, J., Jiang, W., Liu, G., Hu, J., Zhao, L. and Liu, A., 2014, June Rating Aware Route

Planning in Road Networks In International Conference on Web-Age Information

Management (pp. 223-235). Springer, Cham

References

Armstrong, M., and Taylor, S. (2014). Armstrong's handbook of human resource

management practice Cogan Page Publishers.

Barthelme, R.M., Barkley, W.C., Oliver, P.M., Claymont, V. and Puckett, R., 2014

Academy of Nutrition and Dietetics: Revised 2014 standards of professional performance

for registered dietitian nutritionists in management of food and nutrition systems. Journal

of the Academy of Nutrition and Dietetics, 114(7), pp.1104-1112

Belay-Palmer, A. and Kinetic, I., 2015 22 Building sustainable communities through

alternative food systems Handbook on the Globalization of Agriculture, p.446

Butteries, S. C., Butteries, S. C., Gaudi, D., Gaudi, D., Dye, P., and Dye, P. (2016)

Continuous quality improvement in a Maltese hospital using logical framework

analysis. Journal of health organization and management, 30(7), 1026-1046.

Chiai, A., and Round, H. (2015) A Developmental Learning Framework for Business

Report Writing: Guidance for Management Educators”. Journal of Adolescent and Adult

Literacy, 45(7), 556-566.

Cokins, G., 2017 Strategic business management: From planning to performance. John

Wiley & Sons

Dai, J., Jiang, W., Liu, G., Hu, J., Zhao, L. and Liu, A., 2014, June Rating Aware Route

Planning in Road Networks In International Conference on Web-Age Information

Management (pp. 223-235). Springer, Cham

18MANAGE FINANCES

Dewey, M., 2016 planning public library buildings: Concepts and issues for the librarian.

Routledge

Gal, T., Stewart, T., and Hanne, T. (Eds.) (2013) Multicriteria decision making: advances

in MCDM models, algorithms, theory, and applications (Vol. 21) Springer Science &

Business Media

Haines, Y. Y. (2015). Risk modeling, assessment, and management John Wiley & Sons

Homemade, F., Hakims, F., Baba, V. V., and Baba, V. V. (2016) toward a theory of

collaboration for evidence-based management Management Decision, 54(10), 2587-2616

Isaiah, S., Guillaume, J. H., Fila ova, T., Rook, J., & Jake man, A. J. (2015). A

methodology for eliciting, representing, and analyzing stakeholder knowledge for

decision making on complex socio-ecological systems: From cognitive maps to agent-

based models. Journal of environmental management, 151, 500-516.

Kline, R. B. (2015). Principles and practice of structural equation modeling Guilford

publications

Latina, L., Paraskevas, A. and Jang, S.S., 2015. Planning research in hospitality and

tourism

Norton, S. B., and Schofield, K. A. (2017) Conceptual model diagrams as evidence

scaffolds for environmental assessment and management. Freshwater Science, 36(1),

231-239.

Scott, W. R., and Davis, G. F. (2015) Organizations and organizing: Rational, natural and

open systems perspectives. Routledge

Dewey, M., 2016 planning public library buildings: Concepts and issues for the librarian.

Routledge

Gal, T., Stewart, T., and Hanne, T. (Eds.) (2013) Multicriteria decision making: advances

in MCDM models, algorithms, theory, and applications (Vol. 21) Springer Science &

Business Media

Haines, Y. Y. (2015). Risk modeling, assessment, and management John Wiley & Sons

Homemade, F., Hakims, F., Baba, V. V., and Baba, V. V. (2016) toward a theory of

collaboration for evidence-based management Management Decision, 54(10), 2587-2616

Isaiah, S., Guillaume, J. H., Fila ova, T., Rook, J., & Jake man, A. J. (2015). A

methodology for eliciting, representing, and analyzing stakeholder knowledge for

decision making on complex socio-ecological systems: From cognitive maps to agent-

based models. Journal of environmental management, 151, 500-516.

Kline, R. B. (2015). Principles and practice of structural equation modeling Guilford

publications

Latina, L., Paraskevas, A. and Jang, S.S., 2015. Planning research in hospitality and

tourism

Norton, S. B., and Schofield, K. A. (2017) Conceptual model diagrams as evidence

scaffolds for environmental assessment and management. Freshwater Science, 36(1),

231-239.

Scott, W. R., and Davis, G. F. (2015) Organizations and organizing: Rational, natural and

open systems perspectives. Routledge

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.