Financial Management Report: Budget Analysis and Variance for Houzit

VerifiedAdded on 2022/08/19

|17

|3164

|19

Report

AI Summary

This report provides a comprehensive financial analysis of Houzit's business operations, focusing on budget analysis and variance reporting. It examines different types of budgets, including sales, profit, and cash flow budgets, and assesses their effectiveness in planning and controlling business activities. The report identifies variances between budgeted and actual figures, highlighting areas where performance deviates from expectations. It also delves into statutory tax compliance, financial management software options (MYOB and Sage), and key accounting principles like the matching principle and the concept of account groups. Furthermore, the report discusses the implications of probity, critical dates for the business, and recommended budget items. It concludes with suggestions for modified internal control measures and financial management strategies, including improvements in cash management and debtor management policies. The overall goal is to provide insights into the financial health of Houzit and offer recommendations for enhancing financial performance.

Running head: MANAGE FINANCES

Manage Finances

Name of the Student:

Name of the University:

Author’s Note

Manage Finances

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGE FINANCES

Table of Contents

Assessment Task 1.....................................................................................................................3

Part A.....................................................................................................................................3

Introduction............................................................................................................................3

Different Types of Budgets....................................................................................................3

Analysis of Budgets...............................................................................................................6

Part B......................................................................................................................................8

Statutory Requirement for Tax Compliance..........................................................................8

Compliance Requirements.....................................................................................................9

Financial Management Software............................................................................................9

Principles of Accounting......................................................................................................10

Implication of Probity..........................................................................................................10

Critical Dates for the Business.............................................................................................10

Items recommended for the Budget.....................................................................................11

Modified Internal Control Measures....................................................................................11

Assessment Task 2...................................................................................................................12

Variance Report for the Business.........................................................................................12

Revenue Collected from Debtors.........................................................................................13

Issues Identified...................................................................................................................14

Variance Analysis................................................................................................................14

Recommendations................................................................................................................15

Table of Contents

Assessment Task 1.....................................................................................................................3

Part A.....................................................................................................................................3

Introduction............................................................................................................................3

Different Types of Budgets....................................................................................................3

Analysis of Budgets...............................................................................................................6

Part B......................................................................................................................................8

Statutory Requirement for Tax Compliance..........................................................................8

Compliance Requirements.....................................................................................................9

Financial Management Software............................................................................................9

Principles of Accounting......................................................................................................10

Implication of Probity..........................................................................................................10

Critical Dates for the Business.............................................................................................10

Items recommended for the Budget.....................................................................................11

Modified Internal Control Measures....................................................................................11

Assessment Task 2...................................................................................................................12

Variance Report for the Business.........................................................................................12

Revenue Collected from Debtors.........................................................................................13

Issues Identified...................................................................................................................14

Variance Analysis................................................................................................................14

Recommendations................................................................................................................15

2MANAGE FINANCES

Financial Management Strategy Issues................................................................................15

Reference..................................................................................................................................16

Assessment Task 1

Part A

Financial Management Strategy Issues................................................................................15

Reference..................................................................................................................................16

Assessment Task 1

Part A

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGE FINANCES

Introduction

The analysis which is conducted is for the business of Houzit for which detailed

review would be conducted so that any variances which take place can be identified along

with the reasons associated with the same. The discussion would be showing different kinds

of budgets which is prepared for effective planning for the business (Brigham & Ehrhardt,

2013). In addition to this financial management practices for the business would be analysed

if the same is efficient or not. The different budget which is prepared is to ensure

transparency and efficiency is maintained in the operations of the business.

Different Types of Budgets

Introduction

The analysis which is conducted is for the business of Houzit for which detailed

review would be conducted so that any variances which take place can be identified along

with the reasons associated with the same. The discussion would be showing different kinds

of budgets which is prepared for effective planning for the business (Brigham & Ehrhardt,

2013). In addition to this financial management practices for the business would be analysed

if the same is efficient or not. The different budget which is prepared is to ensure

transparency and efficiency is maintained in the operations of the business.

Different Types of Budgets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGE FINANCES

5MANAGE FINANCES

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGE FINANCES

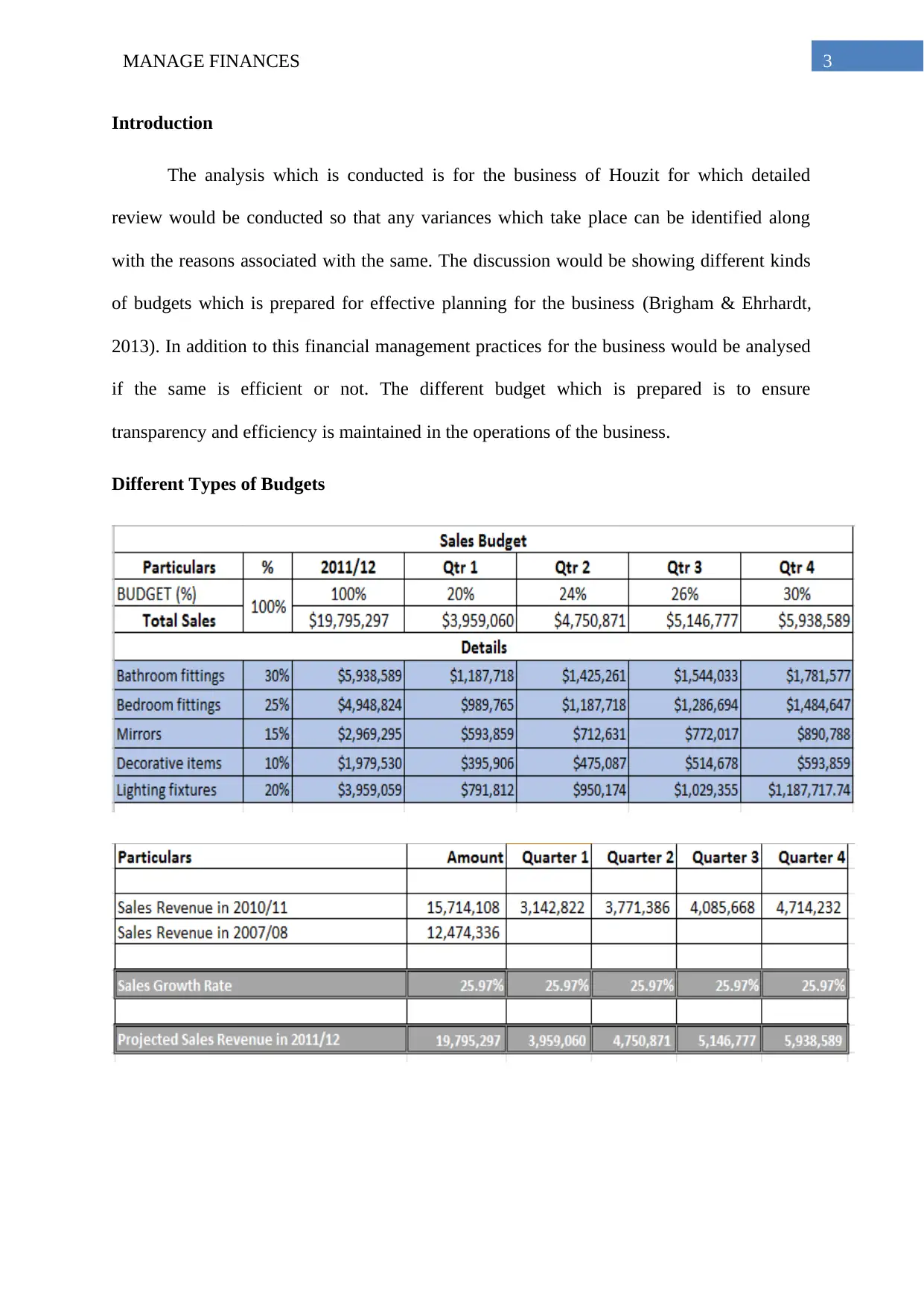

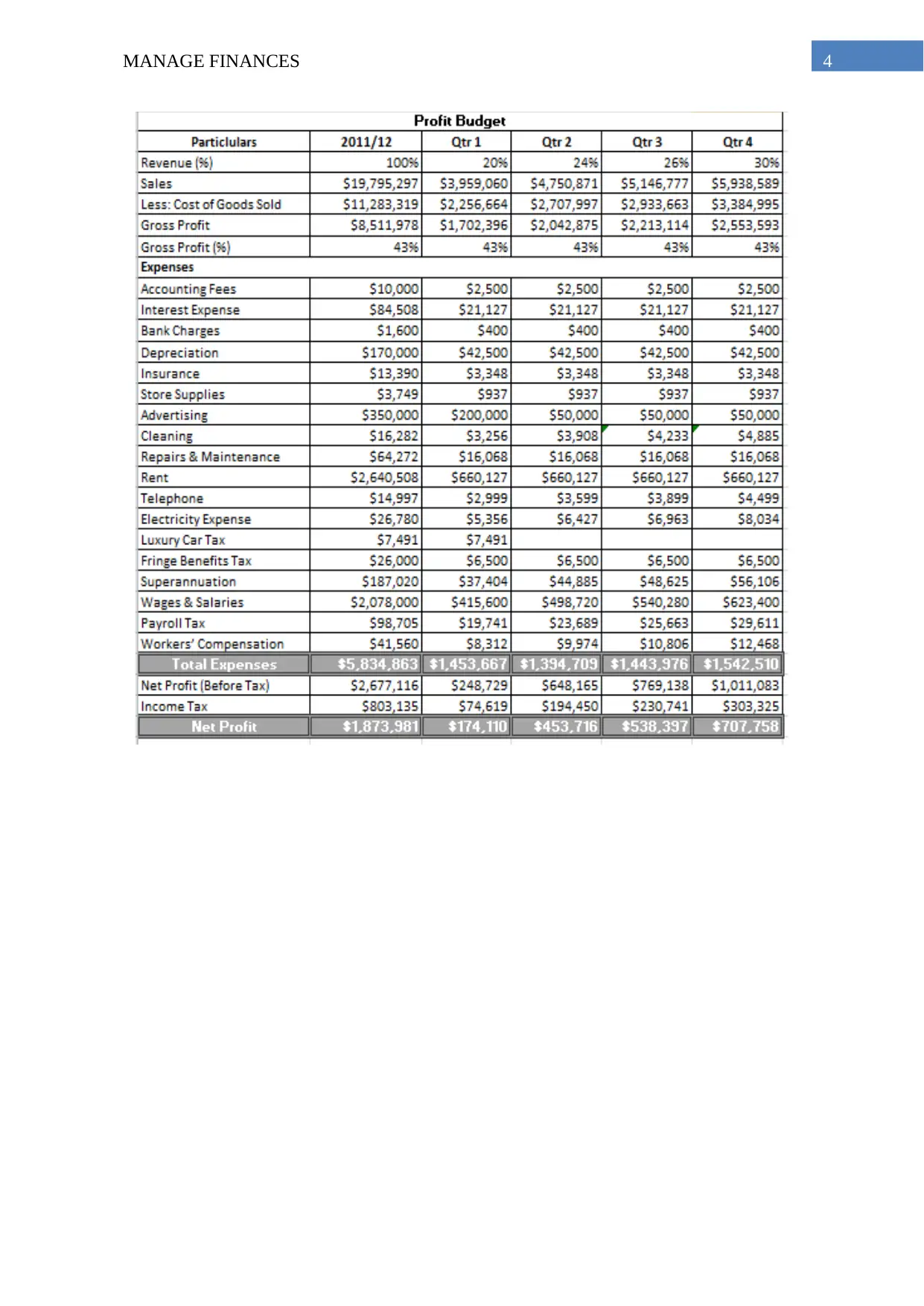

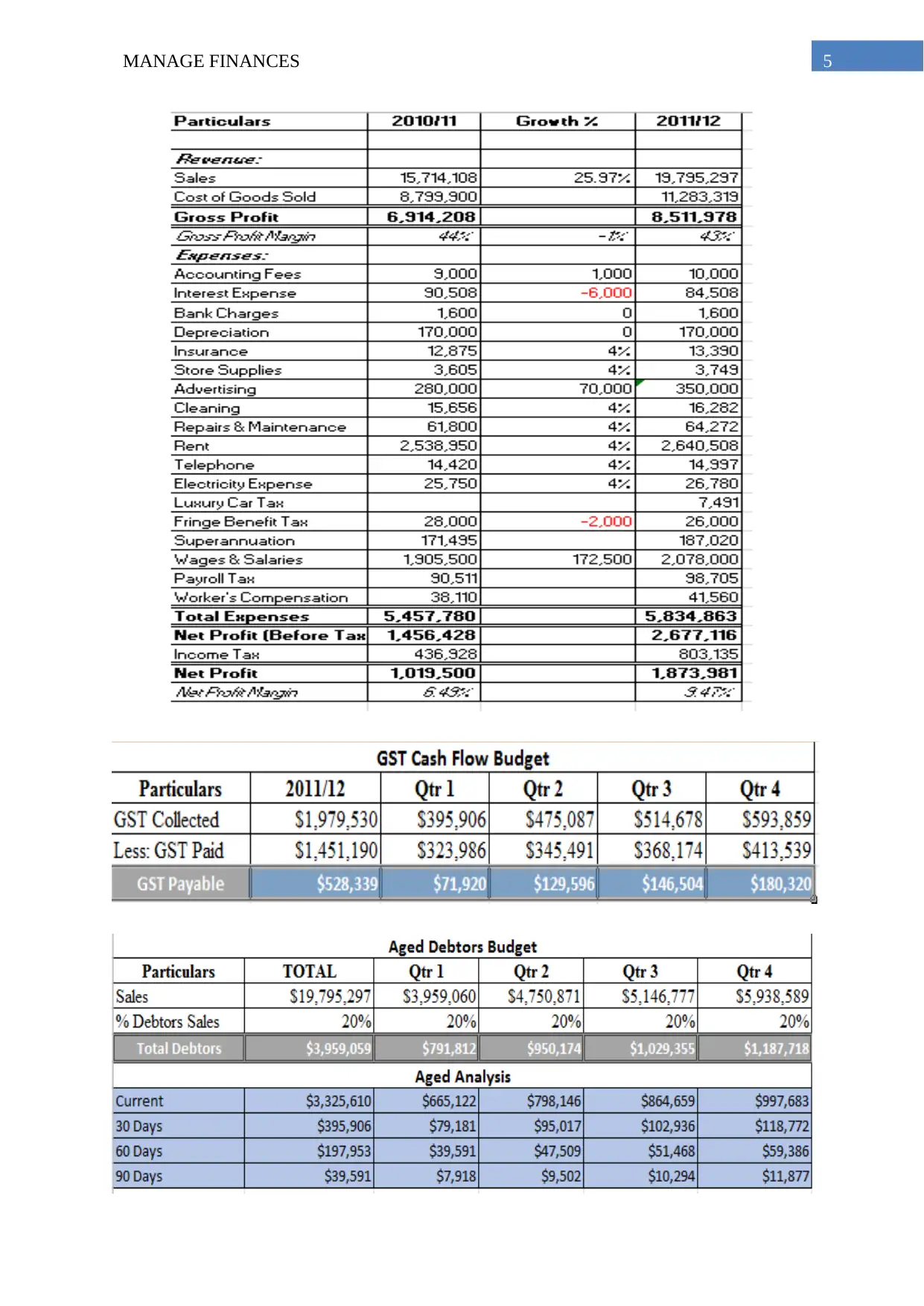

Analysis of Budgets

The above tables demonstrate different types of budgets which is prepared by Houzit

officials for better presentation of the targets of the business and also for proper planning of

the activities of the business (Barr & McClellan, 2018). The target which is shown in the

budgets is as per the long term goals and objectives of the business. Some of the budgets

which is shown in the above table are profit budgets, sales budgets, GST cash flow Budgets

and Aged Debtors Budgets. The different budgets covered different KRAs for the business

and therefore the same are considered to be important for the purpose of planning thee

activities of the business (Vernimmen et al., 2014). The sales budget is prepared to show the

sales revenue which is generated by the business while the profit budget is prepared to show

the profit which the business is able to generate. The gross profit for the entity is shown to

have declined significantly which can be mainly attributed to the low sales figure which is

achieved by the business. Another reason for the low gross profit margin is due to the rise in

the costs and the same is plainly shown in the profit budget for the business. As there is a

sharp decline in the gross profit margin of the company, the net profits of the entity would

also be impacted. However, the net profit has improved from previous year which shows that

the business has reduced some of the operational costs which has positively contributed to the

net revenue generated by the business. The net profit of the business is shown to be $

2,677,166 for the year 2011/12 which shows tremendous growth in terms of profitability of

the business. One of the long term objectives of the business is to achieve growth from the

operations and the same can be achieved if more and more profits are generated.

The financial management strategies are not appropriate concerning some areas which

needs immediate improvements as the same is hampering the efficiency of the business. One

of the policies needs improvements is the cash management policies which directly are

related to the liquidity status for the business. The business also needs to work on debtor’s

Analysis of Budgets

The above tables demonstrate different types of budgets which is prepared by Houzit

officials for better presentation of the targets of the business and also for proper planning of

the activities of the business (Barr & McClellan, 2018). The target which is shown in the

budgets is as per the long term goals and objectives of the business. Some of the budgets

which is shown in the above table are profit budgets, sales budgets, GST cash flow Budgets

and Aged Debtors Budgets. The different budgets covered different KRAs for the business

and therefore the same are considered to be important for the purpose of planning thee

activities of the business (Vernimmen et al., 2014). The sales budget is prepared to show the

sales revenue which is generated by the business while the profit budget is prepared to show

the profit which the business is able to generate. The gross profit for the entity is shown to

have declined significantly which can be mainly attributed to the low sales figure which is

achieved by the business. Another reason for the low gross profit margin is due to the rise in

the costs and the same is plainly shown in the profit budget for the business. As there is a

sharp decline in the gross profit margin of the company, the net profits of the entity would

also be impacted. However, the net profit has improved from previous year which shows that

the business has reduced some of the operational costs which has positively contributed to the

net revenue generated by the business. The net profit of the business is shown to be $

2,677,166 for the year 2011/12 which shows tremendous growth in terms of profitability of

the business. One of the long term objectives of the business is to achieve growth from the

operations and the same can be achieved if more and more profits are generated.

The financial management strategies are not appropriate concerning some areas which

needs immediate improvements as the same is hampering the efficiency of the business. One

of the policies needs improvements is the cash management policies which directly are

related to the liquidity status for the business. The business also needs to work on debtor’s

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGE FINANCES

management policies as it is an important source of generation of revenue. The number of

days which is allowed to the debtors needs to be amended so that there is no lockup situation

of funds. It is to be noted that as the business expands its operations, the number of debtors

would also increase and therefore it is very important for the business to have an efficient

debtor management policy (Finkler, Smith & Calabrese, 2018). One other matter of concern

is that proper records are not maintained by the management which would affect scrutiny

process and further debtor balances are not reconciled on regular basis which can affect the

efficiency of the business. Therefore, such areas of the business need to be improved so that

proper financial management is initiated in the operations of the entity.

In order to prepare the budgets, some assumptions are considered which are essential

for accuracy and forecasting. The sales budget considers that all the units which is produced

by the business during the period is sold off completely which means that there would be no

closing stock. The percentage of credit sales which are estimated for the entity in preparation

of the budget is also clearly presented in the budgets shown above. The percentage of sales

quarter wise is also portrayed so that a level of clarity is maintained in the planning process

of the entity. The fluctuations in sales figures and the respective GST amounts are also shown

in the figure above.

In order to monitor and properly implement the budget which is to be carried out by

the senior officials needs to be efficient. This is important as the same would help to keep a

track of the goals and objective of the business. In order to properly monitor the operations of

the business and ensure that the strategies and plans are being followed, the supervisors of the

business need to be active.

management policies as it is an important source of generation of revenue. The number of

days which is allowed to the debtors needs to be amended so that there is no lockup situation

of funds. It is to be noted that as the business expands its operations, the number of debtors

would also increase and therefore it is very important for the business to have an efficient

debtor management policy (Finkler, Smith & Calabrese, 2018). One other matter of concern

is that proper records are not maintained by the management which would affect scrutiny

process and further debtor balances are not reconciled on regular basis which can affect the

efficiency of the business. Therefore, such areas of the business need to be improved so that

proper financial management is initiated in the operations of the entity.

In order to prepare the budgets, some assumptions are considered which are essential

for accuracy and forecasting. The sales budget considers that all the units which is produced

by the business during the period is sold off completely which means that there would be no

closing stock. The percentage of credit sales which are estimated for the entity in preparation

of the budget is also clearly presented in the budgets shown above. The percentage of sales

quarter wise is also portrayed so that a level of clarity is maintained in the planning process

of the entity. The fluctuations in sales figures and the respective GST amounts are also shown

in the figure above.

In order to monitor and properly implement the budget which is to be carried out by

the senior officials needs to be efficient. This is important as the same would help to keep a

track of the goals and objective of the business. In order to properly monitor the operations of

the business and ensure that the strategies and plans are being followed, the supervisors of the

business need to be active.

8MANAGE FINANCES

Part B

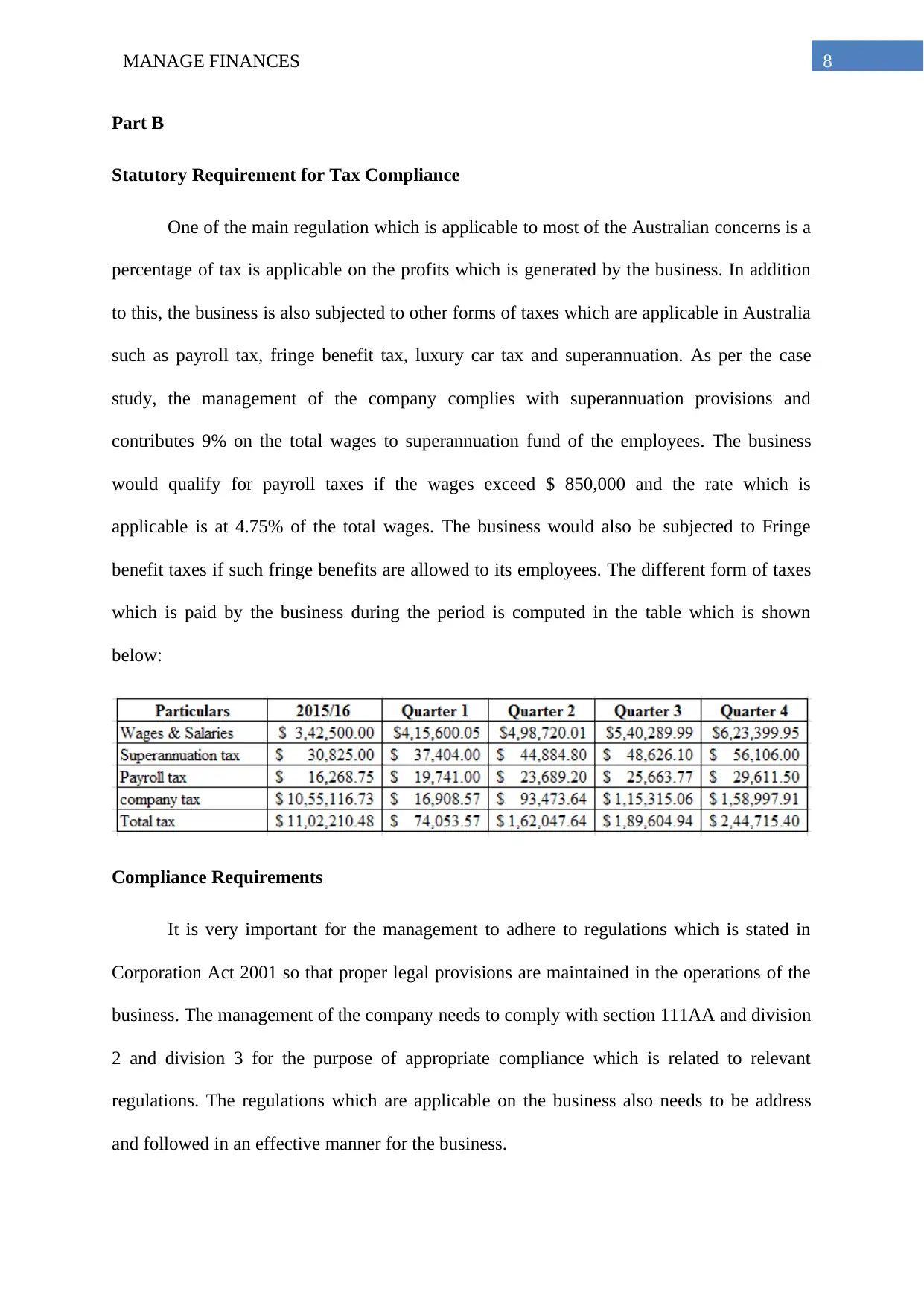

Statutory Requirement for Tax Compliance

One of the main regulation which is applicable to most of the Australian concerns is a

percentage of tax is applicable on the profits which is generated by the business. In addition

to this, the business is also subjected to other forms of taxes which are applicable in Australia

such as payroll tax, fringe benefit tax, luxury car tax and superannuation. As per the case

study, the management of the company complies with superannuation provisions and

contributes 9% on the total wages to superannuation fund of the employees. The business

would qualify for payroll taxes if the wages exceed $ 850,000 and the rate which is

applicable is at 4.75% of the total wages. The business would also be subjected to Fringe

benefit taxes if such fringe benefits are allowed to its employees. The different form of taxes

which is paid by the business during the period is computed in the table which is shown

below:

Compliance Requirements

It is very important for the management to adhere to regulations which is stated in

Corporation Act 2001 so that proper legal provisions are maintained in the operations of the

business. The management of the company needs to comply with section 111AA and division

2 and division 3 for the purpose of appropriate compliance which is related to relevant

regulations. The regulations which are applicable on the business also needs to be address

and followed in an effective manner for the business.

Part B

Statutory Requirement for Tax Compliance

One of the main regulation which is applicable to most of the Australian concerns is a

percentage of tax is applicable on the profits which is generated by the business. In addition

to this, the business is also subjected to other forms of taxes which are applicable in Australia

such as payroll tax, fringe benefit tax, luxury car tax and superannuation. As per the case

study, the management of the company complies with superannuation provisions and

contributes 9% on the total wages to superannuation fund of the employees. The business

would qualify for payroll taxes if the wages exceed $ 850,000 and the rate which is

applicable is at 4.75% of the total wages. The business would also be subjected to Fringe

benefit taxes if such fringe benefits are allowed to its employees. The different form of taxes

which is paid by the business during the period is computed in the table which is shown

below:

Compliance Requirements

It is very important for the management to adhere to regulations which is stated in

Corporation Act 2001 so that proper legal provisions are maintained in the operations of the

business. The management of the company needs to comply with section 111AA and division

2 and division 3 for the purpose of appropriate compliance which is related to relevant

regulations. The regulations which are applicable on the business also needs to be address

and followed in an effective manner for the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGE FINANCES

Financial Management Software

The senior officials of the business are planning to make changes to the financial

management practices of the business and thereby bring about operational change in the

operations of the business. The accuracy process of recording of revenue and expenses is

important and the same needs to be managed by the senior officials of the business. In order

to bring about more efficiency in the reporting process of financial information, financial

software can be implemented (Zietlow et al., 2018). One of the options which is available to

the senior management is MYOB software which can effectively help in recording financial

transactions in an effective manner. One other software which is available to the senior

officials of the business is Sage software which also is an efficient tool which can help the

business to maintain proper accounting records. Both the software which is mentioned above

can assist the senior officials to maintain efficiency and improvement the financial reporting

structure of the entity. If comparison is made between the suggested software above, MYOB

would be a better option as it is suitable to the business requirements of Houzit and it can

analyse information as well as generate reports.

Principles of Accounting

a. The matching principle is considered to be very important from the perspective of

accounting as the same requires the revenue generated should be equivalent to the

expenses incurred by the business (Kaplan & Atkinson, 2015). It is due to this

principle that the balance sheet of a company matches and this principle should be

considered while preparing the financial reports for the business.

b. Account Groups refers to different accounts which are important for the preparation

of financial records for the business. The concept of account groups is also important

when a management is preparing financial statement of a business.

Financial Management Software

The senior officials of the business are planning to make changes to the financial

management practices of the business and thereby bring about operational change in the

operations of the business. The accuracy process of recording of revenue and expenses is

important and the same needs to be managed by the senior officials of the business. In order

to bring about more efficiency in the reporting process of financial information, financial

software can be implemented (Zietlow et al., 2018). One of the options which is available to

the senior management is MYOB software which can effectively help in recording financial

transactions in an effective manner. One other software which is available to the senior

officials of the business is Sage software which also is an efficient tool which can help the

business to maintain proper accounting records. Both the software which is mentioned above

can assist the senior officials to maintain efficiency and improvement the financial reporting

structure of the entity. If comparison is made between the suggested software above, MYOB

would be a better option as it is suitable to the business requirements of Houzit and it can

analyse information as well as generate reports.

Principles of Accounting

a. The matching principle is considered to be very important from the perspective of

accounting as the same requires the revenue generated should be equivalent to the

expenses incurred by the business (Kaplan & Atkinson, 2015). It is due to this

principle that the balance sheet of a company matches and this principle should be

considered while preparing the financial reports for the business.

b. Account Groups refers to different accounts which are important for the preparation

of financial records for the business. The concept of account groups is also important

when a management is preparing financial statement of a business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGE FINANCES

c. The concept timeline states that the budget or financial report which is prepared by

the business should be set within a time frame so that the performance can be

measured in an effective manner. The concept of timeline is also important when a

business wants to set short term as well as long term goals for the entity.

Implication of Probity

The principle of probity states that a professional should behave with honesty,

sincerity and integrity while executing the duties of the entity. The principle of probity is to

be followed so that the budgets which is prepared by the management is showing true and fair

view of the financial position of the business. The budgets which are prepared by the business

should show accurate capability of the business to perform the operations of the business.

Critical Dates for the Business

The critical dates which need to be considered for the business of Houzit include the

quarterly target dates on which the performance of the business is to be monitored. The same

would also monitor the timeline within which the project which is initiated by the business

can be completed. These dates are important for analysing the efficiency and implementation

process of the operational plan of the business.

Items recommended for the Budget

The management of the company needs to properly identify more costs in the budget

and the same should be based on day to day operations of the business. The management also

needs to identify the source of different costs which can be direct nature or indirect nature.

This also involves proper classification of the costs which would make the budget more

transparent.

c. The concept timeline states that the budget or financial report which is prepared by

the business should be set within a time frame so that the performance can be

measured in an effective manner. The concept of timeline is also important when a

business wants to set short term as well as long term goals for the entity.

Implication of Probity

The principle of probity states that a professional should behave with honesty,

sincerity and integrity while executing the duties of the entity. The principle of probity is to

be followed so that the budgets which is prepared by the management is showing true and fair

view of the financial position of the business. The budgets which are prepared by the business

should show accurate capability of the business to perform the operations of the business.

Critical Dates for the Business

The critical dates which need to be considered for the business of Houzit include the

quarterly target dates on which the performance of the business is to be monitored. The same

would also monitor the timeline within which the project which is initiated by the business

can be completed. These dates are important for analysing the efficiency and implementation

process of the operational plan of the business.

Items recommended for the Budget

The management of the company needs to properly identify more costs in the budget

and the same should be based on day to day operations of the business. The management also

needs to identify the source of different costs which can be direct nature or indirect nature.

This also involves proper classification of the costs which would make the budget more

transparent.

11MANAGE FINANCES

Modified Internal Control Measures

The internal control procedures of the entity need to be improved so that the entire

operations can be optimized. One of the steps which can be taken by the senior management

of the company is introduction of financial management procedures and implementation of

new accounting software so that the financial reporting process can be made more efficient.

This is expected to bring about significant improvement in the reporting framework of the

business. In addition to this, changes are also required to be made in financial management

practices such as cash management policies, debtor management policies so that efficiency

and transparency is maintained in the operational process of the business.

Modified Internal Control Measures

The internal control procedures of the entity need to be improved so that the entire

operations can be optimized. One of the steps which can be taken by the senior management

of the company is introduction of financial management procedures and implementation of

new accounting software so that the financial reporting process can be made more efficient.

This is expected to bring about significant improvement in the reporting framework of the

business. In addition to this, changes are also required to be made in financial management

practices such as cash management policies, debtor management policies so that efficiency

and transparency is maintained in the operational process of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.