Manage Finances Within a Budget

VerifiedAdded on 2023/04/24

|14

|2853

|116

AI Summary

This article provides tips for managing finances within a budget for hospitality businesses. It covers legal requirements, variable costs, budget revisions, communication of budget changes, financial records, types of budgets, and more.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGE FINANCES WITHIN A BUDGET

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Assessment 3: 3

Reference List 12

2

Assessment 3: 3

Reference List 12

2

Assessment 3:

1. Hospitality businesses require to controlling costs and set budgets for every area of operation

in general. Legal requirements included allocating funds to a number of mandatory taxes and

liabilities (Henry, 2017). Legal aspects in which the companies require to allocate funds in

include:

- Insurance premiums

- Negotiation of service taxes

- Real estate taxes

- Energy management and consumption taxes

- Service taxes to labourers and builders for maintenance of pieces of furniture,

fixtures and equipment.

- Funds for renewing or obtaining new licenses

2. Variable costs are defined as the costs incurred by an organization which are not fixed with

time. The expenses in an organization operating in the hospitality industry which varies with the

staffing levels are included in the variable costs segment under the budget. Some examples of

variable costs for a commercial company in the hospitality industry may include:

- Direct labour costs

- Staff salaries

- Commissions and incentives

- Training costs

- Billable staff wages

- Medical insurance costs

3

1. Hospitality businesses require to controlling costs and set budgets for every area of operation

in general. Legal requirements included allocating funds to a number of mandatory taxes and

liabilities (Henry, 2017). Legal aspects in which the companies require to allocate funds in

include:

- Insurance premiums

- Negotiation of service taxes

- Real estate taxes

- Energy management and consumption taxes

- Service taxes to labourers and builders for maintenance of pieces of furniture,

fixtures and equipment.

- Funds for renewing or obtaining new licenses

2. Variable costs are defined as the costs incurred by an organization which are not fixed with

time. The expenses in an organization operating in the hospitality industry which varies with the

staffing levels are included in the variable costs segment under the budget. Some examples of

variable costs for a commercial company in the hospitality industry may include:

- Direct labour costs

- Staff salaries

- Commissions and incentives

- Training costs

- Billable staff wages

- Medical insurance costs

3

3. Some expenses that do not vary with the variable staff levels and charging of the labourers

are:

- Funds for intangible assets

- Depreciation costs

- Insurance

- Expense on interest payments

- Rents

- Costs of general utility facilities such as electricity, internet and phone bills

4. Budget revisions can be required if there are unexpected outcomes faced by the company

repeatedly. Some of the reasons for considering budget revision may include:

- Sudden changes in the external factors of the organisation affecting the financial

performance

- Mismatch in the expected outcomes indicating some miscalculation within the budget

- Required redistribution of funds depending on additional expenditures (Jacobs et al.

2018)

- Controlling expenses due to increased incomes and deciding about investments after

reaching financial targets

5. In a business in the hospitality industry, budget making is the primary step included in the

forecasting process. At some points, budget revisions are required as the expected performances

do not match the actual results. Therefore, in hospitality businesses, a budget revision might be

required in some specific situations such as:

a) The number of rooms booked per day surpasses the estimated numbers in the budget

which can change the whole framework of revenue collection (Ross and Harrington,

2016).

4

are:

- Funds for intangible assets

- Depreciation costs

- Insurance

- Expense on interest payments

- Rents

- Costs of general utility facilities such as electricity, internet and phone bills

4. Budget revisions can be required if there are unexpected outcomes faced by the company

repeatedly. Some of the reasons for considering budget revision may include:

- Sudden changes in the external factors of the organisation affecting the financial

performance

- Mismatch in the expected outcomes indicating some miscalculation within the budget

- Required redistribution of funds depending on additional expenditures (Jacobs et al.

2018)

- Controlling expenses due to increased incomes and deciding about investments after

reaching financial targets

5. In a business in the hospitality industry, budget making is the primary step included in the

forecasting process. At some points, budget revisions are required as the expected performances

do not match the actual results. Therefore, in hospitality businesses, a budget revision might be

required in some specific situations such as:

a) The number of rooms booked per day surpasses the estimated numbers in the budget

which can change the whole framework of revenue collection (Ross and Harrington,

2016).

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

b) If there is a sudden and unanticipated increase in attrition rate, then the budget will have

to be reviewed in order to employ and train new employees. In this case, hiring costs and

training costs will have to be included in the budget.

6. It is required to notify each and every department in an organisation about the proposed

changes. The ways to communicate budget changes within an organisation in the hospitality

industry can be of either verbal or non-verbal form (Fao.org, 2018). The non-verbal formats

included communication of the changes in the budget through written documents on paper. Some

means communications include:

- Involving entire teams and clarifying their needs according to the forecasted budget. Live

presentation is one of the most used means of communicating budget alterations.

- Financial changes may also be broadcasted to all parts of an organisation through the use

of organisation website or official social media

- Budget changes can also be notified to all workers through use of official letters or mails

non-verbally.

- Team meetings are also prevalent ways to communicate budget changes in hospitality

organisations.

7. Difference accounting related data is required for controlling and monitoring expenses of both

small and large scale businesses. According to Fitriany et al. (2015) accounting records need to

be maintained and updated regularly considering compliance with legislation and measures of

progress. While monitoring and altering budgets for an organisation it is essential to keep track

of a variable number of expense records. Some of the most important sources of expense records

are:

- Accounting records including financial statements and business ratios

- Bank statements such as tax filings and payment dues

- Insurance documents such as business liability policies or renter’s insurances

8. Successful budget creation is based on the previous trends in performances and incomes of

business organisations in the hospitality industry and therefore access to all sorts of income

5

to be reviewed in order to employ and train new employees. In this case, hiring costs and

training costs will have to be included in the budget.

6. It is required to notify each and every department in an organisation about the proposed

changes. The ways to communicate budget changes within an organisation in the hospitality

industry can be of either verbal or non-verbal form (Fao.org, 2018). The non-verbal formats

included communication of the changes in the budget through written documents on paper. Some

means communications include:

- Involving entire teams and clarifying their needs according to the forecasted budget. Live

presentation is one of the most used means of communicating budget alterations.

- Financial changes may also be broadcasted to all parts of an organisation through the use

of organisation website or official social media

- Budget changes can also be notified to all workers through use of official letters or mails

non-verbally.

- Team meetings are also prevalent ways to communicate budget changes in hospitality

organisations.

7. Difference accounting related data is required for controlling and monitoring expenses of both

small and large scale businesses. According to Fitriany et al. (2015) accounting records need to

be maintained and updated regularly considering compliance with legislation and measures of

progress. While monitoring and altering budgets for an organisation it is essential to keep track

of a variable number of expense records. Some of the most important sources of expense records

are:

- Accounting records including financial statements and business ratios

- Bank statements such as tax filings and payment dues

- Insurance documents such as business liability policies or renter’s insurances

8. Successful budget creation is based on the previous trends in performances and incomes of

business organisations in the hospitality industry and therefore access to all sorts of income

5

statements are necessary for predicting the future expenses and profits of the company. Types of

income records needed for monitoring the budget for any organization include:

- Income statements with all details of expenditure

- Cash flow statement showing amounts of revenue collected

- Sales invoices for timing of receipts

- Receipts of grants from the government

9. Surpassing costs for food and raw materials is one of the most common issues faced by

restaurants in general. Therefore may be multiple reasons behind such extra costing for foods.

Some of the reasons causing increased food costs in restaurants are:

- Increased costs of buying ingredients from a single vendor or supplier

- Failure to mix high and low-cost ingredients accordingly

- Employee theft of foods items especially in restaurants with unmonitored walk-in

refrigerators

- Ineffective portion control techniques used by the workers

- Poor staff training regarding bookkeeping about schedules when the ingredients are

bought and at which prices.

10. Variances in the budget forecasting and actual sales are inevitable in all businesses. There are

both positive and adverse unfavourable impacts of deviations on the performance of the

companies. However, all deviations do not result in negative impacts on the performances. For

example, if the actual sales figures exceed the forecasted figures, it actually has positive impacts

on the performance (Ter Bogt et al. 2015). Therefore such deviations can be ignored and budget

revisions are not required. Contradicting to this, in monitoring expenses, if the actual expenses

exceed the forecasted values, it has negative impacts on the financial performance of the

company. Such deviation requires attention as they hinder overall incomes of the company.

6

income records needed for monitoring the budget for any organization include:

- Income statements with all details of expenditure

- Cash flow statement showing amounts of revenue collected

- Sales invoices for timing of receipts

- Receipts of grants from the government

9. Surpassing costs for food and raw materials is one of the most common issues faced by

restaurants in general. Therefore may be multiple reasons behind such extra costing for foods.

Some of the reasons causing increased food costs in restaurants are:

- Increased costs of buying ingredients from a single vendor or supplier

- Failure to mix high and low-cost ingredients accordingly

- Employee theft of foods items especially in restaurants with unmonitored walk-in

refrigerators

- Ineffective portion control techniques used by the workers

- Poor staff training regarding bookkeeping about schedules when the ingredients are

bought and at which prices.

10. Variances in the budget forecasting and actual sales are inevitable in all businesses. There are

both positive and adverse unfavourable impacts of deviations on the performance of the

companies. However, all deviations do not result in negative impacts on the performances. For

example, if the actual sales figures exceed the forecasted figures, it actually has positive impacts

on the performance (Ter Bogt et al. 2015). Therefore such deviations can be ignored and budget

revisions are not required. Contradicting to this, in monitoring expenses, if the actual expenses

exceed the forecasted values, it has negative impacts on the financial performance of the

company. Such deviation requires attention as they hinder overall incomes of the company.

6

11. Budget meetings are essential for large scale hospitality businesses such as hotels as this

builds awareness about the overhead expenses in the organisation and how the next year's

expenditures can be managed according to the previous historical data. Therefore the information

topics that need to be covered in the said budget meeting may include:

- Previous years bank statements

- Present invoices

- Balance sheets

- Ledgers

- Previous non-profitable debts

- Penalties

- Fines to be paid and upcoming taxes

- Further pieces of information about breakouts and overhead new construction budgets (if

any)

- Projected revenues may also be discussed in such meetings

12. Budgets reflect on previous performance trends in the company's finances and predict the

performance in future. Sometimes, some years or phases can experience more sales and

increased incomes as compared to usual performance levels. If certain sections of the

organisations are performing better than expected, then it can be expected that placing more

targets can be sustained effectively (Beeler et al. 2015). For example, if a company exceeds

targeted sales in every quarter of a year, it may be feasible that in the next budget, the targets can

be increased in order to achieve higher levels of income and maintain the motivation levels of the

workers.

13. Uses of Financial records:

7

builds awareness about the overhead expenses in the organisation and how the next year's

expenditures can be managed according to the previous historical data. Therefore the information

topics that need to be covered in the said budget meeting may include:

- Previous years bank statements

- Present invoices

- Balance sheets

- Ledgers

- Previous non-profitable debts

- Penalties

- Fines to be paid and upcoming taxes

- Further pieces of information about breakouts and overhead new construction budgets (if

any)

- Projected revenues may also be discussed in such meetings

12. Budgets reflect on previous performance trends in the company's finances and predict the

performance in future. Sometimes, some years or phases can experience more sales and

increased incomes as compared to usual performance levels. If certain sections of the

organisations are performing better than expected, then it can be expected that placing more

targets can be sustained effectively (Beeler et al. 2015). For example, if a company exceeds

targeted sales in every quarter of a year, it may be feasible that in the next budget, the targets can

be increased in order to achieve higher levels of income and maintain the motivation levels of the

workers.

13. Uses of Financial records:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

● Bank deposit documentation - used for documenting the information included in deposit

transaction by the depositor● Bank statements- Documents monthly record of activities in the account including

cheques issued, withdrawals, credits, interests and service charges● Banking summaries- This report is used in daily balancing procedure which enables

cross-referencing of deposits and creating three-way balances● Business activity statements- These statements are used for paying goods and services

taxes (GST) and other tax instalments (Miao et al. 2017).● Cheque books- Used for drawing depositing or granting money directly from the account

of the issuer.● Credit card transaction statements- Reports drawn amounts and available balance of the

user in the linked account● Invoices- Used in accounting to record sales and prices

● Journal entries- Special procedure in bookkeeping used in accounting containing all

financial transaction related details● Labour and wages reports- Used for recording employee names working under a

particular organisation and their gross wages against the number of hours worked.● Merchant statements- Records a merchant’s fees and transaction counts.

● Merchant summaries- Merchant summary reports are used for showing transactions in

each account, total amounts processed by each merchant gateway and average amounts

per credit card.● Transaction reports- Used for supervisory purposes by financial regulatory bodies

regarding individual transactions in accounts.

14. Types of budget:

8

transaction by the depositor● Bank statements- Documents monthly record of activities in the account including

cheques issued, withdrawals, credits, interests and service charges● Banking summaries- This report is used in daily balancing procedure which enables

cross-referencing of deposits and creating three-way balances● Business activity statements- These statements are used for paying goods and services

taxes (GST) and other tax instalments (Miao et al. 2017).● Cheque books- Used for drawing depositing or granting money directly from the account

of the issuer.● Credit card transaction statements- Reports drawn amounts and available balance of the

user in the linked account● Invoices- Used in accounting to record sales and prices

● Journal entries- Special procedure in bookkeeping used in accounting containing all

financial transaction related details● Labour and wages reports- Used for recording employee names working under a

particular organisation and their gross wages against the number of hours worked.● Merchant statements- Records a merchant’s fees and transaction counts.

● Merchant summaries- Merchant summary reports are used for showing transactions in

each account, total amounts processed by each merchant gateway and average amounts

per credit card.● Transaction reports- Used for supervisory purposes by financial regulatory bodies

regarding individual transactions in accounts.

14. Types of budget:

8

Cash budgets- Cash budgets are budget plans for expected cash inflows and outflows which are

formulated according to overall expenses and revenues collected.

Cash flow budgets- Cash flow budget is the estimated cash inflow and outflow for a business

within a particular time- period assessing availability of cash required for future operations

Departmental Budgets- Departmental budget is a budget predicting expenses and incomes of a

particular department within an organisation over a certain period of time (Weygandt et al.

2015).

Event budgets- Event budget is forecast for expenses and incomes involved in a particular event.

Project budgets- Project budget is allocated resources and funds for a certain project in specific

areas of application.

Purchasing budgets- Purchasing budget is a financial plan for documenting estimated costs for

the maintenance of inventory.

Sales budgets- Sales budget is the estimated sales for the consequent financial periods.

Wage budgets- Part of annual or quarterly expenditure involved in remunerating labourers in an

organization is called sales budget.

Statistical reports- A report consisting of multiple raw data sets about the performances of the

company in terms of sales and profitability.

The whole of organization budgets- This type of budget is the aggregate of all departmental

budgets and is aimed a representing the overall financial health and activity of an organisation.

9

formulated according to overall expenses and revenues collected.

Cash flow budgets- Cash flow budget is the estimated cash inflow and outflow for a business

within a particular time- period assessing availability of cash required for future operations

Departmental Budgets- Departmental budget is a budget predicting expenses and incomes of a

particular department within an organisation over a certain period of time (Weygandt et al.

2015).

Event budgets- Event budget is forecast for expenses and incomes involved in a particular event.

Project budgets- Project budget is allocated resources and funds for a certain project in specific

areas of application.

Purchasing budgets- Purchasing budget is a financial plan for documenting estimated costs for

the maintenance of inventory.

Sales budgets- Sales budget is the estimated sales for the consequent financial periods.

Wage budgets- Part of annual or quarterly expenditure involved in remunerating labourers in an

organization is called sales budget.

Statistical reports- A report consisting of multiple raw data sets about the performances of the

company in terms of sales and profitability.

The whole of organization budgets- This type of budget is the aggregate of all departmental

budgets and is aimed a representing the overall financial health and activity of an organisation.

9

15. There may be many situations where lowering of targets might be required in a budget. For

example, in some cases, due to changes in the external factors such as interest rates in business

loans, some targets set in previously might not be achievable in limited times. In such cases

lowering of target may be required. Such requirement may also occur in case of lower demand

for services or products or emergence of new providers of similar services.

16. Some factors that need to be considered while preparing financial and statistical reports are:

- Inventory

- Sales activities

- Working capital

- Asset status

- Accounts receivable

- External environments

17. Budget Maestro is a popular software program used or budgeting in businesses. It provides

driver based modelling and effective forecasting without any hassle. It also has features such as

Expense budgeting, workforce planning, capital asset planning, revenue calculations and sales

forecasting.

18. Budgeting and control of expense is essential for all purposes in business since this helps in

ensuring that the available funds and expenditure within the company are adequate and

accordingly done (Fao.org, 2018). Budgetary control report may be generated yearly, monthly or

quarterly as per requirement of the firm.

19. Formulating budget helps in profit maximisation of a firm by improving the value of wealth

of the shareholders. It also helps in greater earnings through timely recognition of risks

associated with cash flows.

20. Cash flow refers to the total sum of cash being transmitted in and out of the business

particularly acting as effective liquidity.

21.Weekly: purchase invoices, cash receipts and account statements

Daily: Sales transactions and purchases

Monthly: Revenue losses, average gross margin and average cost per orders

22. Restaurant wastes can be classified as follows:

- Kitchen wastes

10

example, in some cases, due to changes in the external factors such as interest rates in business

loans, some targets set in previously might not be achievable in limited times. In such cases

lowering of target may be required. Such requirement may also occur in case of lower demand

for services or products or emergence of new providers of similar services.

16. Some factors that need to be considered while preparing financial and statistical reports are:

- Inventory

- Sales activities

- Working capital

- Asset status

- Accounts receivable

- External environments

17. Budget Maestro is a popular software program used or budgeting in businesses. It provides

driver based modelling and effective forecasting without any hassle. It also has features such as

Expense budgeting, workforce planning, capital asset planning, revenue calculations and sales

forecasting.

18. Budgeting and control of expense is essential for all purposes in business since this helps in

ensuring that the available funds and expenditure within the company are adequate and

accordingly done (Fao.org, 2018). Budgetary control report may be generated yearly, monthly or

quarterly as per requirement of the firm.

19. Formulating budget helps in profit maximisation of a firm by improving the value of wealth

of the shareholders. It also helps in greater earnings through timely recognition of risks

associated with cash flows.

20. Cash flow refers to the total sum of cash being transmitted in and out of the business

particularly acting as effective liquidity.

21.Weekly: purchase invoices, cash receipts and account statements

Daily: Sales transactions and purchases

Monthly: Revenue losses, average gross margin and average cost per orders

22. Restaurant wastes can be classified as follows:

- Kitchen wastes

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

- Electronic waste

- Paper and packaging wastages

- Prepared food wastes

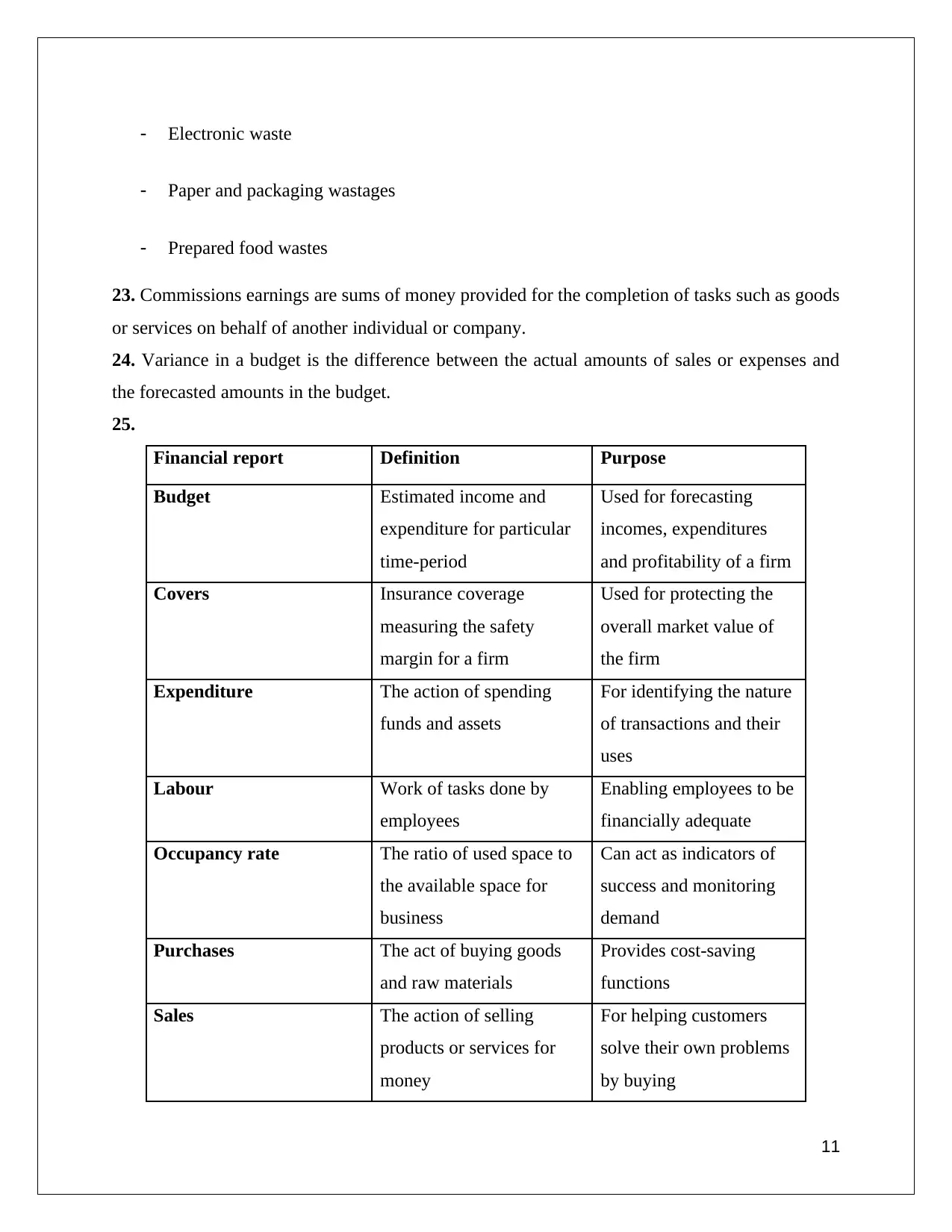

23. Commissions earnings are sums of money provided for the completion of tasks such as goods

or services on behalf of another individual or company.

24. Variance in a budget is the difference between the actual amounts of sales or expenses and

the forecasted amounts in the budget.

25.

Financial report Definition Purpose

Budget Estimated income and

expenditure for particular

time-period

Used for forecasting

incomes, expenditures

and profitability of a firm

Covers Insurance coverage

measuring the safety

margin for a firm

Used for protecting the

overall market value of

the firm

Expenditure The action of spending

funds and assets

For identifying the nature

of transactions and their

uses

Labour Work of tasks done by

employees

Enabling employees to be

financially adequate

Occupancy rate The ratio of used space to

the available space for

business

Can act as indicators of

success and monitoring

demand

Purchases The act of buying goods

and raw materials

Provides cost-saving

functions

Sales The action of selling

products or services for

money

For helping customers

solve their own problems

by buying

11

- Paper and packaging wastages

- Prepared food wastes

23. Commissions earnings are sums of money provided for the completion of tasks such as goods

or services on behalf of another individual or company.

24. Variance in a budget is the difference between the actual amounts of sales or expenses and

the forecasted amounts in the budget.

25.

Financial report Definition Purpose

Budget Estimated income and

expenditure for particular

time-period

Used for forecasting

incomes, expenditures

and profitability of a firm

Covers Insurance coverage

measuring the safety

margin for a firm

Used for protecting the

overall market value of

the firm

Expenditure The action of spending

funds and assets

For identifying the nature

of transactions and their

uses

Labour Work of tasks done by

employees

Enabling employees to be

financially adequate

Occupancy rate The ratio of used space to

the available space for

business

Can act as indicators of

success and monitoring

demand

Purchases The act of buying goods

and raw materials

Provides cost-saving

functions

Sales The action of selling

products or services for

money

For helping customers

solve their own problems

by buying

11

Stock Capital raised by

companies through shares

Useful in issuing new

investment shares in

future

Transaction The complete event of

selling and obtaining

money in exchange

Save information about

total number of monetary

exchanges

Transaction exempted Type of transactions

involving securities

exchange that do not need

compliance with

legislation

To avoid registration with

Securities Exchange

Commission (SEC)

Unit sold Quantification of Sales

earned by a firm in a

particular reporting period

Used for total revenue

calculation

Wages Regular payment provided

for work

Paid in return for work

12

companies through shares

Useful in issuing new

investment shares in

future

Transaction The complete event of

selling and obtaining

money in exchange

Save information about

total number of monetary

exchanges

Transaction exempted Type of transactions

involving securities

exchange that do not need

compliance with

legislation

To avoid registration with

Securities Exchange

Commission (SEC)

Unit sold Quantification of Sales

earned by a firm in a

particular reporting period

Used for total revenue

calculation

Wages Regular payment provided

for work

Paid in return for work

12

Reference List

Beeler, M., Manea, V. and Bolick, J., Comtech EF Data Corp, 2015. System and method for

satellite link budget analysis (LBA) optimization. U.S. Patent 9,178,607. Available at:

https://patentimages.storage.googleapis.com/f8/71/89/d69f625112b851/US9178607.pdf

[Accessed 12/01/2019]

Fao.org (2018). Chapter 4 - Budgetary control Available at:

http://www.fao.org/docrep/W4343E/w4343e05.htm[Accessed 16/01/2019]

Fitriany, N., Masdjojo, G.N. and Suwarti, T., 2015. Exploring The Factors That Impact The

Accumulation Of Budget Absorption In The End Of The Fiscal Year 2013: A Case Study In

Pekalongan City Of Central Java Indonesia. South East Asia Journal of Contemporary Business,

Economics and Law, 7(3), pp.2289-1560. Available at:

http://seajbel.com/wp-content/uploads/2015/09/KLIBEL7_Econ-24.pdf [Accessed 16/01/2019]

Henry, M., 2017. A Congregational & Legal Study in the Practice of Hospitality at Faith

Community Center, Lacey, Washington. Available at:

https://scholar.csl.edu/cgi/viewcontent.cgi?article=1048&context=dmin [Accessed 02/01/2019]

Jacobs, T.L., Batra, S., Purnomo, H., Dege, K., Wegner, M.A. and Gulbranson, J., American

Airlines Inc, 2018. Reserve forecasting systems and methods for airline crew planning and

staffing. U.S. Patent Application 10/102,487. Available at:

https://patentimages.storage.googleapis.com/9c/36/75/00b2fccf44e284/US10102487.pdf

[Accessed 17/01/2019]

Miao, Y., Liu, Y., Chen, Y., Zhou, J. and Ji, P., 2017. Two uncertain chance-constrained

programming models to setting target levels of design attributes in quality function

deployment. Information Sciences, 415, pp.156-170. Available at:

http://my.shu.edu.cn/FCKeditor/userfiles/201710.pdf [Accessed 22/01/2019]

Ross, L. and Harrington, C., 2016. California Nursing Home Chains By Ownership Type Facility

and Resident Characteristics, Staffing, and Quality Outcomes in 2015. Available at:

http://theconsumervoice.org/uploads/files/general/CA-Chains-Report_20AUG2016.pdf

[Accessed 15/01/2019]

Ter Bogt, H.J., Van Helden, G.J. and Van Der Kolk, B., 2015. Challenging the NPM Ideas

About Performance Management: Selectivity and Differentiation in Outcome‐Oriented

13

Beeler, M., Manea, V. and Bolick, J., Comtech EF Data Corp, 2015. System and method for

satellite link budget analysis (LBA) optimization. U.S. Patent 9,178,607. Available at:

https://patentimages.storage.googleapis.com/f8/71/89/d69f625112b851/US9178607.pdf

[Accessed 12/01/2019]

Fao.org (2018). Chapter 4 - Budgetary control Available at:

http://www.fao.org/docrep/W4343E/w4343e05.htm[Accessed 16/01/2019]

Fitriany, N., Masdjojo, G.N. and Suwarti, T., 2015. Exploring The Factors That Impact The

Accumulation Of Budget Absorption In The End Of The Fiscal Year 2013: A Case Study In

Pekalongan City Of Central Java Indonesia. South East Asia Journal of Contemporary Business,

Economics and Law, 7(3), pp.2289-1560. Available at:

http://seajbel.com/wp-content/uploads/2015/09/KLIBEL7_Econ-24.pdf [Accessed 16/01/2019]

Henry, M., 2017. A Congregational & Legal Study in the Practice of Hospitality at Faith

Community Center, Lacey, Washington. Available at:

https://scholar.csl.edu/cgi/viewcontent.cgi?article=1048&context=dmin [Accessed 02/01/2019]

Jacobs, T.L., Batra, S., Purnomo, H., Dege, K., Wegner, M.A. and Gulbranson, J., American

Airlines Inc, 2018. Reserve forecasting systems and methods for airline crew planning and

staffing. U.S. Patent Application 10/102,487. Available at:

https://patentimages.storage.googleapis.com/9c/36/75/00b2fccf44e284/US10102487.pdf

[Accessed 17/01/2019]

Miao, Y., Liu, Y., Chen, Y., Zhou, J. and Ji, P., 2017. Two uncertain chance-constrained

programming models to setting target levels of design attributes in quality function

deployment. Information Sciences, 415, pp.156-170. Available at:

http://my.shu.edu.cn/FCKeditor/userfiles/201710.pdf [Accessed 22/01/2019]

Ross, L. and Harrington, C., 2016. California Nursing Home Chains By Ownership Type Facility

and Resident Characteristics, Staffing, and Quality Outcomes in 2015. Available at:

http://theconsumervoice.org/uploads/files/general/CA-Chains-Report_20AUG2016.pdf

[Accessed 15/01/2019]

Ter Bogt, H.J., Van Helden, G.J. and Van Der Kolk, B., 2015. Challenging the NPM Ideas

About Performance Management: Selectivity and Differentiation in Outcome‐Oriented

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance Budgeting. Financial Accountability & Management, 31(3), pp.287-315. Available

at: http://www.pbgchina.cn/u/cms/www/201609/29180804ixyh.pdf [Accessed 13/01/2019]

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting. John

Wiley & Sons. Available at:

https://www.uoguelph.ca/business/sites/uoguelph.ca.business/files/BUS%206180%20Financial

%20Managerial%20Accounting,%20Summer%202014,%20Jeffrey%20O

%E2%80%99Leary.pdf [Accessed 02/01/2019]

14

at: http://www.pbgchina.cn/u/cms/www/201609/29180804ixyh.pdf [Accessed 13/01/2019]

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting. John

Wiley & Sons. Available at:

https://www.uoguelph.ca/business/sites/uoguelph.ca.business/files/BUS%206180%20Financial

%20Managerial%20Accounting,%20Summer%202014,%20Jeffrey%20O

%E2%80%99Leary.pdf [Accessed 02/01/2019]

14

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.