Financial Analysis: Free Cash Flow, Ratios, and Budgeting for Finance

VerifiedAdded on 2023/06/15

|60

|11993

|405

Report

AI Summary

This report provides a comprehensive analysis of organisational finance, including free cash flow analysis for Penrith Council, graphical representations of cash flow trends, and financial ratio calculations. It also addresses internal control and governance within Harvey Norman. Furthermore, the report includes the preparation of various budgets for Hardwood Products, such as cost of production, cost of goods sold, sales forecasts, operating expenses, and a master budget, culminating in an income statement and budget report. The analysis aims to provide insights into the financial health and operational efficiency of the organisations, offering a detailed overview of their financial activities and strategic financial planning.

Manage

Organisational

Finance

Organisational

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

ASSESSMENT TASK 1.................................................................................................................4

TASK 1............................................................................................................................................4

1. Analyse the free cash flow of year 2009-2010........................................................................4

2. Make a Graphical representation of the operating cash flow trends.......................................4

3. Make graphs of the investing cash flow trends.......................................................................5

4. Draw a graph of total income trends from continuing operations..........................................6

5. Show the net operating profit trends.......................................................................................7

TASK 2............................................................................................................................................8

Calculate the financial ratio using the fiscal statement...............................................................8

Assessment Task 2.........................................................................................................................11

Part B.............................................................................................................................................11

Assessment Task 3.........................................................................................................................16

Prepare two budgets- cost of production and cost of goods sold..............................................16

ASSESSMENT TASK 4...............................................................................................................25

Make sales budget and determine the position of debtors on 30th September.........................25

ASSESSMENT TASK 5...............................................................................................................29

Prepare operating expense budget and master budget, on the basis of this prepare an income

statement along with budget report...........................................................................................29

CONCLUSION..............................................................................................................................53

REFERENCES..............................................................................................................................54

INTRODUCTION ..........................................................................................................................3

ASSESSMENT TASK 1.................................................................................................................4

TASK 1............................................................................................................................................4

1. Analyse the free cash flow of year 2009-2010........................................................................4

2. Make a Graphical representation of the operating cash flow trends.......................................4

3. Make graphs of the investing cash flow trends.......................................................................5

4. Draw a graph of total income trends from continuing operations..........................................6

5. Show the net operating profit trends.......................................................................................7

TASK 2............................................................................................................................................8

Calculate the financial ratio using the fiscal statement...............................................................8

Assessment Task 2.........................................................................................................................11

Part B.............................................................................................................................................11

Assessment Task 3.........................................................................................................................16

Prepare two budgets- cost of production and cost of goods sold..............................................16

ASSESSMENT TASK 4...............................................................................................................25

Make sales budget and determine the position of debtors on 30th September.........................25

ASSESSMENT TASK 5...............................................................................................................29

Prepare operating expense budget and master budget, on the basis of this prepare an income

statement along with budget report...........................................................................................29

CONCLUSION..............................................................................................................................53

REFERENCES..............................................................................................................................54

INTRODUCTION

Managing the organisational finances means that the company needs to develop new

skills and training in the financial management for the development of the undertakings. The key

skills which are to be needs to manage the fiscal resources of the corporation is the cash

management and the bookkeeping accounting. It should do to ensure the financial integrity to

obtain the economic control of the firm (Fitzgerald, 2021). To make sure that the firm is

performing as per its capability, it is essential to perform a fiscal analysis of the records,

transactions and the statements for giving a reality check to the organisation. It will be helpful in

knowing about the profitability and productivity of the firm. By the help of the budget analysis

and different ratios a comparative analysis of the company can be performed by another firm or

by the industry the firm is dealing in (Mirzaee, and et.al., 2018). It gives the improvement

criteria in which the business. Internal control refers to the policies and procedures that are

created within an organisation to comply with the moral code of conduct of the business itself. It

determines if a business is working in compliance with the applicable laws, regulations, policies

and procedures.

The report consists of five assessments. In the first assessment, the case and the financial

statements about the Penrith Council has been discussed, on the basis of which the free cash flow

is calculated and the analysis is done. Further, the operating, investing cash flow trends and the

income from the operating activities and the operating profits trends have been showed.

Moreover, the financial ratios of the Penrith Council have been calculated, which can help in

doing the analysis for the company and will also assist in the decision – making. In the Part B of

assessment 2, the report will highlight how internal control and governance guides a business to

be effective in its operations. The company selected for this task is Harvey Norman, a retail

company dealing in furniture, computer and other consumer electrical products. The rest three

assessments of the report focuses on preparation of master budget for Hardwood Products. Its

third assessment deals with the preparation of cost of goods sold and cost of production budget.

The forth section prepares the anticipated sales forecast budget. The fifth assessment is about the

preparation of master budget along with operating expenses budget. It also focuses on a report on

master budget and income statement.

Managing the organisational finances means that the company needs to develop new

skills and training in the financial management for the development of the undertakings. The key

skills which are to be needs to manage the fiscal resources of the corporation is the cash

management and the bookkeeping accounting. It should do to ensure the financial integrity to

obtain the economic control of the firm (Fitzgerald, 2021). To make sure that the firm is

performing as per its capability, it is essential to perform a fiscal analysis of the records,

transactions and the statements for giving a reality check to the organisation. It will be helpful in

knowing about the profitability and productivity of the firm. By the help of the budget analysis

and different ratios a comparative analysis of the company can be performed by another firm or

by the industry the firm is dealing in (Mirzaee, and et.al., 2018). It gives the improvement

criteria in which the business. Internal control refers to the policies and procedures that are

created within an organisation to comply with the moral code of conduct of the business itself. It

determines if a business is working in compliance with the applicable laws, regulations, policies

and procedures.

The report consists of five assessments. In the first assessment, the case and the financial

statements about the Penrith Council has been discussed, on the basis of which the free cash flow

is calculated and the analysis is done. Further, the operating, investing cash flow trends and the

income from the operating activities and the operating profits trends have been showed.

Moreover, the financial ratios of the Penrith Council have been calculated, which can help in

doing the analysis for the company and will also assist in the decision – making. In the Part B of

assessment 2, the report will highlight how internal control and governance guides a business to

be effective in its operations. The company selected for this task is Harvey Norman, a retail

company dealing in furniture, computer and other consumer electrical products. The rest three

assessments of the report focuses on preparation of master budget for Hardwood Products. Its

third assessment deals with the preparation of cost of goods sold and cost of production budget.

The forth section prepares the anticipated sales forecast budget. The fifth assessment is about the

preparation of master budget along with operating expenses budget. It also focuses on a report on

master budget and income statement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ASSESSMENT TASK 1

TASK 1

1. Analyse the free cash flow of year 2009-2010.

Free Cash Flow is the amount which is generated by the organisation every year which is

free and not obligated for all the internal and external liabilities (Münster, 2020). It aims at

determining the amount that how much the company is sufficient to invest in the business and

distribute the dividends to its shareholders.

Free Cash Flow = Sales Revenue – Expenses

= 162081 – 167946 = (5865)

Analysis: From the above calculation it can analysed that the operating expenses are more than

the income. It resulted in the negative flow of the operating capital, which can be utilised as to

pay the dividends, debts and increase in the earnings. A negative free Cash flow implies that the

Penrith Council is unable to create cash which can be used in supporting and growing the

organisation. It tracks that how much money the company is left with after deducting its

operating expenses.

2. Make a Graphical representation of the operating cash flow trends.

TASK 1

1. Analyse the free cash flow of year 2009-2010.

Free Cash Flow is the amount which is generated by the organisation every year which is

free and not obligated for all the internal and external liabilities (Münster, 2020). It aims at

determining the amount that how much the company is sufficient to invest in the business and

distribute the dividends to its shareholders.

Free Cash Flow = Sales Revenue – Expenses

= 162081 – 167946 = (5865)

Analysis: From the above calculation it can analysed that the operating expenses are more than

the income. It resulted in the negative flow of the operating capital, which can be utilised as to

pay the dividends, debts and increase in the earnings. A negative free Cash flow implies that the

Penrith Council is unable to create cash which can be used in supporting and growing the

organisation. It tracks that how much money the company is left with after deducting its

operating expenses.

2. Make a Graphical representation of the operating cash flow trends.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

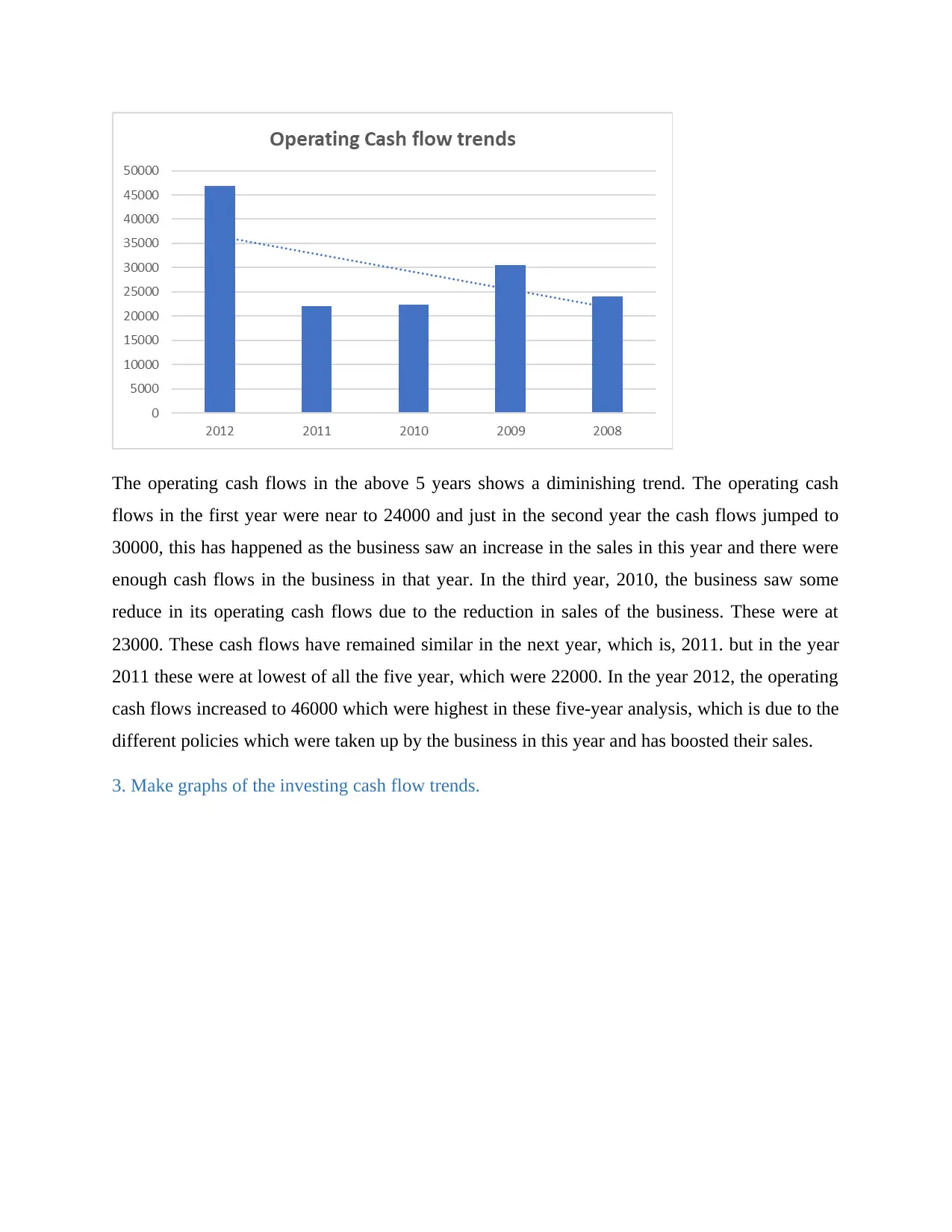

The operating cash flows in the above 5 years shows a diminishing trend. The operating cash

flows in the first year were near to 24000 and just in the second year the cash flows jumped to

30000, this has happened as the business saw an increase in the sales in this year and there were

enough cash flows in the business in that year. In the third year, 2010, the business saw some

reduce in its operating cash flows due to the reduction in sales of the business. These were at

23000. These cash flows have remained similar in the next year, which is, 2011. but in the year

2011 these were at lowest of all the five year, which were 22000. In the year 2012, the operating

cash flows increased to 46000 which were highest in these five-year analysis, which is due to the

different policies which were taken up by the business in this year and has boosted their sales.

3. Make graphs of the investing cash flow trends.

flows in the first year were near to 24000 and just in the second year the cash flows jumped to

30000, this has happened as the business saw an increase in the sales in this year and there were

enough cash flows in the business in that year. In the third year, 2010, the business saw some

reduce in its operating cash flows due to the reduction in sales of the business. These were at

23000. These cash flows have remained similar in the next year, which is, 2011. but in the year

2011 these were at lowest of all the five year, which were 22000. In the year 2012, the operating

cash flows increased to 46000 which were highest in these five-year analysis, which is due to the

different policies which were taken up by the business in this year and has boosted their sales.

3. Make graphs of the investing cash flow trends.

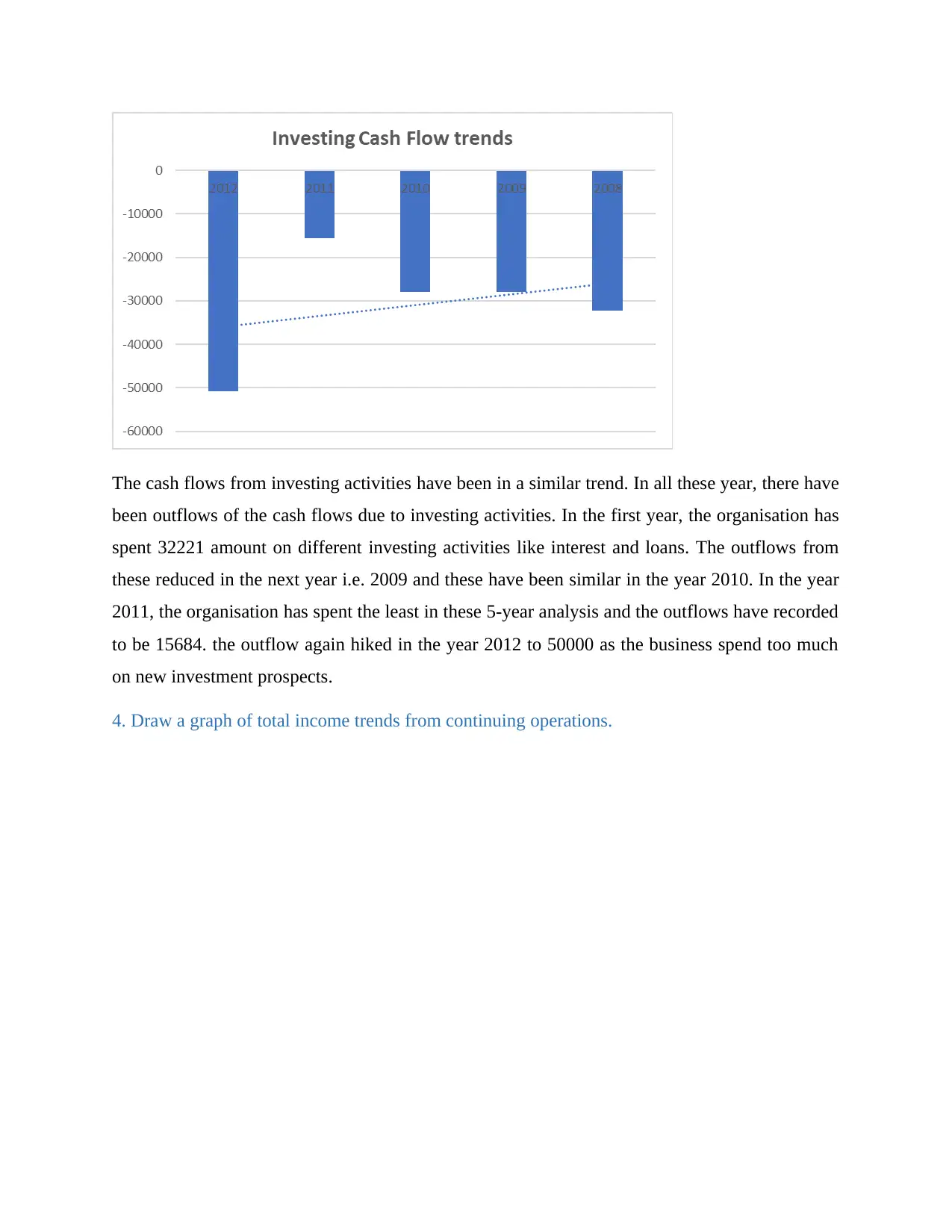

The cash flows from investing activities have been in a similar trend. In all these year, there have

been outflows of the cash flows due to investing activities. In the first year, the organisation has

spent 32221 amount on different investing activities like interest and loans. The outflows from

these reduced in the next year i.e. 2009 and these have been similar in the year 2010. In the year

2011, the organisation has spent the least in these 5-year analysis and the outflows have recorded

to be 15684. the outflow again hiked in the year 2012 to 50000 as the business spend too much

on new investment prospects.

4. Draw a graph of total income trends from continuing operations.

been outflows of the cash flows due to investing activities. In the first year, the organisation has

spent 32221 amount on different investing activities like interest and loans. The outflows from

these reduced in the next year i.e. 2009 and these have been similar in the year 2010. In the year

2011, the organisation has spent the least in these 5-year analysis and the outflows have recorded

to be 15684. the outflow again hiked in the year 2012 to 50000 as the business spend too much

on new investment prospects.

4. Draw a graph of total income trends from continuing operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The above graphical presentation shows the trends of total income which have been earned from

continuing operations. The trend can be seen as an increasing slope in the 5 financial year. In the

year 2008 the total operating income received was 150000 which increased by a little in the next

year i.e. 2009. The income after that have shown a positive increasing trend and in the year 2012

the income was at its highest and near to 200000 in these 5 year analysis.

5. Show the net operating profit trends.

continuing operations. The trend can be seen as an increasing slope in the 5 financial year. In the

year 2008 the total operating income received was 150000 which increased by a little in the next

year i.e. 2009. The income after that have shown a positive increasing trend and in the year 2012

the income was at its highest and near to 200000 in these 5 year analysis.

5. Show the net operating profit trends.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The net operating profit trend of the business can be seen decreasing in the first 4 years and in

the last year the business recorded the highest profits in these 5 years. The organisation recorded

operating loss of -50000 and the highest profit recorded in these 5 years was near to 20000

TASK 2

Calculate the financial ratio using the fiscal statement.

1. Current Ratio: It is a form of the liquidity ratio which is measured to known about the

company's efficiency to pay – off its short term liabilities with respect to the current

assets (Neeser,and et.al., 2019). It estimated the amount which the organisation has to

raise the funds to pay off the liabilities. The ideal ratio is 2: 1. It means the existing assets

should be at least double of the existing liabilities.

= Current Assets / Current liabilities

= 73862 / 49576 = 1.49: 1

Interpretation: The current ratio of the organisation is 1.49: 1 which is a little less than what is

considered as the standard ratio. This means that the liquidity of the business is a stake. The

organisation's current assets are low to meet the standard ratio of current ratios. The existing

assets are not double the existing liabilities of the business this creates liquidity problems for the

organisation. Higher the current ratio, higher is the liquidity in the business and lower the ratio,

less is the cash and cash equivalents in the business for the period.

2. Debt – Equity Ratio: It is a leverage ratio that calculates the weight of total debt and

financial liabilities in relation to the total capital of shareholders. It gives the

proportionate between the debt and equity of the firm (Proczek, 2020). It also shows that

how much the equity amount of the shareholders is sufficient to pay it creditors. This

ratio shows how a company's capital structure is geared towards either debt or equity

financing.

= Debt / Equity

= 110693 / 2506435 = 0.04: 1

Interpretation: The debt to equity ratio of the organisation is 0.04: 1 which shows that the

business is operating on more equity than debt of the organisation. This interprets that the

organisation does not have any capacity to take risk and try new for the organisation. The

the last year the business recorded the highest profits in these 5 years. The organisation recorded

operating loss of -50000 and the highest profit recorded in these 5 years was near to 20000

TASK 2

Calculate the financial ratio using the fiscal statement.

1. Current Ratio: It is a form of the liquidity ratio which is measured to known about the

company's efficiency to pay – off its short term liabilities with respect to the current

assets (Neeser,and et.al., 2019). It estimated the amount which the organisation has to

raise the funds to pay off the liabilities. The ideal ratio is 2: 1. It means the existing assets

should be at least double of the existing liabilities.

= Current Assets / Current liabilities

= 73862 / 49576 = 1.49: 1

Interpretation: The current ratio of the organisation is 1.49: 1 which is a little less than what is

considered as the standard ratio. This means that the liquidity of the business is a stake. The

organisation's current assets are low to meet the standard ratio of current ratios. The existing

assets are not double the existing liabilities of the business this creates liquidity problems for the

organisation. Higher the current ratio, higher is the liquidity in the business and lower the ratio,

less is the cash and cash equivalents in the business for the period.

2. Debt – Equity Ratio: It is a leverage ratio that calculates the weight of total debt and

financial liabilities in relation to the total capital of shareholders. It gives the

proportionate between the debt and equity of the firm (Proczek, 2020). It also shows that

how much the equity amount of the shareholders is sufficient to pay it creditors. This

ratio shows how a company's capital structure is geared towards either debt or equity

financing.

= Debt / Equity

= 110693 / 2506435 = 0.04: 1

Interpretation: The debt to equity ratio of the organisation is 0.04: 1 which shows that the

business is operating on more equity than debt of the organisation. This interprets that the

organisation does not have any capacity to take risk and try new for the organisation. The

business will have to pay more dividends onto these share capital which in turn uses more of its

profits. Higher the ratio, higher is the ability of the business to take risks in the business. Lower

the ratio, creates less retained earnings for the business and hence the business may not be able to

work on its growth prospects.

3. Return on Investment using Cash flow: It is basically the internal rate of return which

the company compares to understand that how the company is doing considering the

investment and the products (Buckley, and Doyle, 2017). It gives the investors a brief

understanding about how the cash is maintained in the organisation which can affect the

internal structure of the business. It is calculating be diving the operating cash flows by

the difference of total assets and current liabilities.

= Operating Cash flow / Capital Employed

Year 2012 = 46789 / (2617128 – 49576)

= 46789 / 2567552 = 0.018

Year 2011 = 22003 / (2361955 – 50385)

= 22003 / 2311570 = 0.01

Year 2010 = 22288 / (1432980 – 45762)

= 22288 / 1387218 = 0.016

Year 2009 = 30500 / (1152361 – 43352)

= 1152361 / 1109009 = 1.039

Year 2008 = 24119 / (1160728 – 39763)

= 24119 / 1120965 = 0.022

Interpretation: The above 5 year ratios shows how the business's return have been in these 5

year. The most return on investment have been seen in the year 2009 which was 1.039. The

business saw the least return on its investment in the year 2010, which was 0.016. The business

did not receive any good return and it also has not spend much on investment in this year. The

business recorded some increment on the return on their investment but it was just slight in the

year 2012 with 0.018.

profits. Higher the ratio, higher is the ability of the business to take risks in the business. Lower

the ratio, creates less retained earnings for the business and hence the business may not be able to

work on its growth prospects.

3. Return on Investment using Cash flow: It is basically the internal rate of return which

the company compares to understand that how the company is doing considering the

investment and the products (Buckley, and Doyle, 2017). It gives the investors a brief

understanding about how the cash is maintained in the organisation which can affect the

internal structure of the business. It is calculating be diving the operating cash flows by

the difference of total assets and current liabilities.

= Operating Cash flow / Capital Employed

Year 2012 = 46789 / (2617128 – 49576)

= 46789 / 2567552 = 0.018

Year 2011 = 22003 / (2361955 – 50385)

= 22003 / 2311570 = 0.01

Year 2010 = 22288 / (1432980 – 45762)

= 22288 / 1387218 = 0.016

Year 2009 = 30500 / (1152361 – 43352)

= 1152361 / 1109009 = 1.039

Year 2008 = 24119 / (1160728 – 39763)

= 24119 / 1120965 = 0.022

Interpretation: The above 5 year ratios shows how the business's return have been in these 5

year. The most return on investment have been seen in the year 2009 which was 1.039. The

business saw the least return on its investment in the year 2010, which was 0.016. The business

did not receive any good return and it also has not spend much on investment in this year. The

business recorded some increment on the return on their investment but it was just slight in the

year 2012 with 0.018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Gross profit Margin: An organization's net revenue is the most essential proportion of

an organization's productivity. It states that how much cash is left subsequent to

representing the expense of creating labour and products and paying employees. Money

managers and financial investors for the most part desire to see a steady or developing net

revenue; when this measure is contracting, either the business is putting resources into its

activities or it has an issue (Ghalehkhondabi, and et.al., 2017). It is calculated by splitting

the distinction between absolute income and the expense of labour and products sold by

complete income, and is by and large addressed as a rate.

= (Gross profit / Net Sales) * 100

= (20871 / 208267) * 100 = 10.02%

Interpretation: The gross profit margin which have been seen in the business was 10.02 %. this

ratio shows the business is able to convert 10 % of its sales into its gross profits. This ratio has

been calculated on the basis of its operating profits as there were no direct expenses for the

business and hence there were no gross profits for this year.

5. Break even Revenues: It is a point at which the firm is in a situation of no loss no profit.

At this point, the organisations cover the total expenses which is incurred by the firm.

Break even quantity alludes to the quantity of units a venture should offer to take care of

all expenses, while break even sales refers to the business sum it should produce to take

care of its expenses. It is an interior administration bookkeeping setup that decides the

connection between cost, volume and benefit.

= Fixed Cost / Selling price – Variable Cost

According to the given operations of the Penrith Council, it can be analysed that there is

no fixed cost. It means that the organisation is not occurring any fixed cost. The breakeven

revenue for the year 2011-12 is 187396, because these are the expenses which have been

incurred to the company in respect to the consideration of the financial summary of the

organisation.

an organization's productivity. It states that how much cash is left subsequent to

representing the expense of creating labour and products and paying employees. Money

managers and financial investors for the most part desire to see a steady or developing net

revenue; when this measure is contracting, either the business is putting resources into its

activities or it has an issue (Ghalehkhondabi, and et.al., 2017). It is calculated by splitting

the distinction between absolute income and the expense of labour and products sold by

complete income, and is by and large addressed as a rate.

= (Gross profit / Net Sales) * 100

= (20871 / 208267) * 100 = 10.02%

Interpretation: The gross profit margin which have been seen in the business was 10.02 %. this

ratio shows the business is able to convert 10 % of its sales into its gross profits. This ratio has

been calculated on the basis of its operating profits as there were no direct expenses for the

business and hence there were no gross profits for this year.

5. Break even Revenues: It is a point at which the firm is in a situation of no loss no profit.

At this point, the organisations cover the total expenses which is incurred by the firm.

Break even quantity alludes to the quantity of units a venture should offer to take care of

all expenses, while break even sales refers to the business sum it should produce to take

care of its expenses. It is an interior administration bookkeeping setup that decides the

connection between cost, volume and benefit.

= Fixed Cost / Selling price – Variable Cost

According to the given operations of the Penrith Council, it can be analysed that there is

no fixed cost. It means that the organisation is not occurring any fixed cost. The breakeven

revenue for the year 2011-12 is 187396, because these are the expenses which have been

incurred to the company in respect to the consideration of the financial summary of the

organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment Task 2

Part B

Internal control refers to set of procedures, rules and workings that are enforced by a

company in its own working to ensure that different departments working in the business are

complying with the rules, regulations and policies that are formed by the business and promoting

success to achieve the predetermined objectives of the business. Internal auditing is one of the

crucial part of internal control (Hastings, 2021). It helps to check and audit the financial

information of the company and regulate any error or fraud which has occurred in the statements

of financial information. The structure of internal control has five following components:

Control Environment: This component derives the tone of the organisation and how it

influences the control consciousness of its people. The factors in this include the

Integrity, ethical values of the people working in the business. The philosophy and

operating style of the managers. The authority, responsibility relations between the

workforce, etc.,

Risk Assessment: It refers to the identification and interpreting of the different risks

which arise while achieving the objective. These can be assessed by monthly discussion

of risk issues, internal risk assessment and formal internal departmental risk etc.

Control Activities: These helps the management to ensure whether or not the directions

are being carried out while performing the range of activities like purchasing, sales, etc.

Information and communication: All the important information that is identified and

captured in the business needs to be well communicated that enables the mangers and the

employees of the business to work efficiently. Effective communication is needed to be

happened across whole organisation. Examples to these are reporting, visions and values.

Monitoring: The internal control systems are needed to be well monitored to assess the

quality of the performance over a period of time.

There are different types of Internal control and some of them are, Preventive and detection

controls, Hard and soft controls, Manual and automated controls, key and secondary controls.

Corporate Governance refers to a system which is present in an organisation which forms

rules, procedures and practices to control an organisation to follow the laws and standards

Part B

Internal control refers to set of procedures, rules and workings that are enforced by a

company in its own working to ensure that different departments working in the business are

complying with the rules, regulations and policies that are formed by the business and promoting

success to achieve the predetermined objectives of the business. Internal auditing is one of the

crucial part of internal control (Hastings, 2021). It helps to check and audit the financial

information of the company and regulate any error or fraud which has occurred in the statements

of financial information. The structure of internal control has five following components:

Control Environment: This component derives the tone of the organisation and how it

influences the control consciousness of its people. The factors in this include the

Integrity, ethical values of the people working in the business. The philosophy and

operating style of the managers. The authority, responsibility relations between the

workforce, etc.,

Risk Assessment: It refers to the identification and interpreting of the different risks

which arise while achieving the objective. These can be assessed by monthly discussion

of risk issues, internal risk assessment and formal internal departmental risk etc.

Control Activities: These helps the management to ensure whether or not the directions

are being carried out while performing the range of activities like purchasing, sales, etc.

Information and communication: All the important information that is identified and

captured in the business needs to be well communicated that enables the mangers and the

employees of the business to work efficiently. Effective communication is needed to be

happened across whole organisation. Examples to these are reporting, visions and values.

Monitoring: The internal control systems are needed to be well monitored to assess the

quality of the performance over a period of time.

There are different types of Internal control and some of them are, Preventive and detection

controls, Hard and soft controls, Manual and automated controls, key and secondary controls.

Corporate Governance refers to a system which is present in an organisation which forms

rules, procedures and practices to control an organisation to follow the laws and standards

mandated by the state (Russell, 2021). The main goal of corporate governance is to safeguard

the interests of the different stakeholders like management, investors, government and the

community. Corporate governance considers principles of transparency, accountability and

security.

Following are these key principles of corporate governance discussed:

Shareholders Primacy: One of the most important principles of corporate governance is to

recognise the shareholders and their capital employed in the business. In this principle, the

corporate governance provides basic recognition to the people who buys the stock of the business

and after that it the principle follows the responsibility to the shareholders. The shareholders of

the business have a direct say as to how the business is supposed to run. The shareholders

themselves elect the board of directors who will look after the operations of the business and

report them about the same.

Transparency: The major focus is given to the interests of the shareholders in the corporate

governance. Transparency is a principle which focuses on review of company's actions by

anyone, internal or external to the business (Stolper, 2019). Corporate governance provides a

medium for this transparency about the business actions to the general public. It also motivates

individuals to invest into the business and become shareholders to the business.

Security: The corporate governance follows this principle as the customers and shareholders of

the business need to feel safe while dealing with the business. They need to know that all the

personal information related to them, is safe and not used by any third party. Everyone who is

working in the business need to follow the security procedures of the business like passwords

and authentication methods.

Following are the 8 principles which are required by the company to formulate their Corporate

governance report according to the Australian Securities Exchange:

1. Lay solid foundations for the management and oversight- The listed company is

required to formally make it clear the different roles and responsibilities of the board of

directors and its management and timely keep a check on their performance.

the interests of the different stakeholders like management, investors, government and the

community. Corporate governance considers principles of transparency, accountability and

security.

Following are these key principles of corporate governance discussed:

Shareholders Primacy: One of the most important principles of corporate governance is to

recognise the shareholders and their capital employed in the business. In this principle, the

corporate governance provides basic recognition to the people who buys the stock of the business

and after that it the principle follows the responsibility to the shareholders. The shareholders of

the business have a direct say as to how the business is supposed to run. The shareholders

themselves elect the board of directors who will look after the operations of the business and

report them about the same.

Transparency: The major focus is given to the interests of the shareholders in the corporate

governance. Transparency is a principle which focuses on review of company's actions by

anyone, internal or external to the business (Stolper, 2019). Corporate governance provides a

medium for this transparency about the business actions to the general public. It also motivates

individuals to invest into the business and become shareholders to the business.

Security: The corporate governance follows this principle as the customers and shareholders of

the business need to feel safe while dealing with the business. They need to know that all the

personal information related to them, is safe and not used by any third party. Everyone who is

working in the business need to follow the security procedures of the business like passwords

and authentication methods.

Following are the 8 principles which are required by the company to formulate their Corporate

governance report according to the Australian Securities Exchange:

1. Lay solid foundations for the management and oversight- The listed company is

required to formally make it clear the different roles and responsibilities of the board of

directors and its management and timely keep a check on their performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 60

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.