Perception of Consumers towards Afterpay Payment Service in Australia

VerifiedAdded on 2022/12/23

|44

|8737

|79

AI Summary

This report evaluates the perception of consumers in Australia towards Afterpay as a payment service tool. It analyzes the impact on purchasing behavior and satisfaction. The study finds that a majority of millennials prefer Afterpay over other online payment methods, but cash on delivery is still widely used. The report also discusses the growth of electronic payment methods and the competition among payment service providers in Australia.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT

Management

Name of the Student

Name of the University

Author Note

Management

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MANAGEMENT

Abstract

In this report the purpose of the common people of Australia, on the Afterpay payment service

has been evaluated. In this era of technology, the earnings and spending of individuals are

getting reimangined each and every day with the help of technological advancement in payment

methods. Majority of the payment services in Australia provides the service users with both

prepaid and post paid option; the popularity of Afterpay, a post payment service has got raised to

a great extent currently. While some off the researchers are of the perspective that post payment

systems like Afterpay is beneficial for the mentioned organization, a good number of

psychologists are of the perspective that the mentioned system is imposing adverse effect on the

consumers purchasing behaviour. In order to evaluate the perspective of the consumers a

distributed quantitative analysis has been performed. Samples were provided with questionaries

in order to collect data from the result off the study, it has been found that Majority of the

millennial prefer the Afterpay payment service over any other online payment methods.

However, cash on delivery is still found to be one of the mostly used payment methods by

millennial.

Abstract

In this report the purpose of the common people of Australia, on the Afterpay payment service

has been evaluated. In this era of technology, the earnings and spending of individuals are

getting reimangined each and every day with the help of technological advancement in payment

methods. Majority of the payment services in Australia provides the service users with both

prepaid and post paid option; the popularity of Afterpay, a post payment service has got raised to

a great extent currently. While some off the researchers are of the perspective that post payment

systems like Afterpay is beneficial for the mentioned organization, a good number of

psychologists are of the perspective that the mentioned system is imposing adverse effect on the

consumers purchasing behaviour. In order to evaluate the perspective of the consumers a

distributed quantitative analysis has been performed. Samples were provided with questionaries

in order to collect data from the result off the study, it has been found that Majority of the

millennial prefer the Afterpay payment service over any other online payment methods.

However, cash on delivery is still found to be one of the mostly used payment methods by

millennial.

2MANAGEMENT

Table of Contents

Introduction......................................................................................................................................2

Research question............................................................................................................................5

Literature review..............................................................................................................................5

Methodology..................................................................................................................................17

Research Philosophy..................................................................................................................17

Research Design........................................................................................................................18

Research Approach....................................................................................................................19

Data collection method..............................................................................................................19

Sampling....................................................................................................................................20

Data analysis method.................................................................................................................21

Findings of the research.................................................................................................................21

Significance of the research paper.................................................................................................33

Limitations and delimitation..........................................................................................................33

Ethical consideration.....................................................................................................................34

References......................................................................................................................................35

Table of Contents

Introduction......................................................................................................................................2

Research question............................................................................................................................5

Literature review..............................................................................................................................5

Methodology..................................................................................................................................17

Research Philosophy..................................................................................................................17

Research Design........................................................................................................................18

Research Approach....................................................................................................................19

Data collection method..............................................................................................................19

Sampling....................................................................................................................................20

Data analysis method.................................................................................................................21

Findings of the research.................................................................................................................21

Significance of the research paper.................................................................................................33

Limitations and delimitation..........................................................................................................33

Ethical consideration.....................................................................................................................34

References......................................................................................................................................35

3MANAGEMENT

Research topic: people perception towards afterpay as a payment tool

Introduction

Tremendous growth in the usage of the internet as well as mobile phones has been

evidenced all over the world on the last decade. The earnings and spending of individuals are

getting reimangined each and every day with the help of technological advancement in payment

methods (Roozbahani, Hojjati and Azad 2015). In this era of technology, consumers are highly

concerned with the types as well as levels of payment methods that are being adopted by the

business operators. Therefore business owners have to keep up with the constant improvements

in order to avoid the risk of losing their consumers to the competitors. When it comes to the

millennium consumers, their chief and basic criteria of selecting payment methods include safety

and efficiency of the payment systems (Marinkovic and Kalinic 2017). A well functioning

system possesses the potential to stimulate the desire of the consumers to purchase services,

goods or assets from various business sectors. The costs of making payment differ on the basis of

the amount of transaction along with the payment tool used. In Australia, the internet penetration

rate is nearly 100 percent an approximately 70 percent of the population owns smartphones

(Cagliano, De Marco and Rafele 2017). Therefore, it can be understood that non cash payments

accounts for majority of the value of payments in the economy of Australia. As per the data

obtained from a survey conducted in the year 2027, non cash payments that are worth around

242 billion dollars were made in each of the business days that is almost 14 percent of the annual

GDP of the nation. More than 70 percent of the value of noncash transactions gets accounted for

by a limited number of high value payments that is made through the real time gross settlement

system of Australia (Liébana-Cabanillas, Herrera and Guillén 2016).

Research topic: people perception towards afterpay as a payment tool

Introduction

Tremendous growth in the usage of the internet as well as mobile phones has been

evidenced all over the world on the last decade. The earnings and spending of individuals are

getting reimangined each and every day with the help of technological advancement in payment

methods (Roozbahani, Hojjati and Azad 2015). In this era of technology, consumers are highly

concerned with the types as well as levels of payment methods that are being adopted by the

business operators. Therefore business owners have to keep up with the constant improvements

in order to avoid the risk of losing their consumers to the competitors. When it comes to the

millennium consumers, their chief and basic criteria of selecting payment methods include safety

and efficiency of the payment systems (Marinkovic and Kalinic 2017). A well functioning

system possesses the potential to stimulate the desire of the consumers to purchase services,

goods or assets from various business sectors. The costs of making payment differ on the basis of

the amount of transaction along with the payment tool used. In Australia, the internet penetration

rate is nearly 100 percent an approximately 70 percent of the population owns smartphones

(Cagliano, De Marco and Rafele 2017). Therefore, it can be understood that non cash payments

accounts for majority of the value of payments in the economy of Australia. As per the data

obtained from a survey conducted in the year 2027, non cash payments that are worth around

242 billion dollars were made in each of the business days that is almost 14 percent of the annual

GDP of the nation. More than 70 percent of the value of noncash transactions gets accounted for

by a limited number of high value payments that is made through the real time gross settlement

system of Australia (Liébana-Cabanillas, Herrera and Guillén 2016).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MANAGEMENT

Majority of the value of these payment methods are associated with the settlement of

foreign exchange along with the securities market transactions. One of the major payment

methods in Australia includes the Buy Now, Pay Later (BNPL) digital service that allows the

users to buy products both online as well as offline immediately and pay the purchase in

instalments within a limited period. Another payment service that has gained popularity in the

nation includes Paypal that makes almost 28 percent of the online payment of the nation (Chan et

al. 2017). Apart from the two mentioned payment methods, a good number of pre and post paid

services are available in Australia. Thus a huge competition exists between the existing payment

service providing organizations in the nation.

While majority of the mentioned payment services provides the service users with both

prepaid and post paid option, the popularity of Afterpay, a post payment service has got raised to

a great extent currently. The afterpay service has been launched in the year 2015, and within a

limited period of time the service as proved to be a revelation in Australia with approximately

2.32 million people using the service for transaction (Aswani et al. 2018). The chief attraction of

the mentioned service includes After Pay payment service provides the consumer with the

opportunity to buy whatever product or service they want and enables them to make the payment

in four instalments paid fortnightly. The target consumer of the after pay service includes the

millenniums. The service is available at more than 10,000 shops throughout Australia and New

Zealand. While the mentioned service has drastically increased the sales of the organizations,

according to researchers this service has the potential to contribute towards increased financial

stress amongst the shoppers. Over the past few years, the mode of payment has been of great

concern to a large number of consumers especially the youngsters of the current generation.

Most of the young generation is fully focused on trending activities such as after pay method as

Majority of the value of these payment methods are associated with the settlement of

foreign exchange along with the securities market transactions. One of the major payment

methods in Australia includes the Buy Now, Pay Later (BNPL) digital service that allows the

users to buy products both online as well as offline immediately and pay the purchase in

instalments within a limited period. Another payment service that has gained popularity in the

nation includes Paypal that makes almost 28 percent of the online payment of the nation (Chan et

al. 2017). Apart from the two mentioned payment methods, a good number of pre and post paid

services are available in Australia. Thus a huge competition exists between the existing payment

service providing organizations in the nation.

While majority of the mentioned payment services provides the service users with both

prepaid and post paid option, the popularity of Afterpay, a post payment service has got raised to

a great extent currently. The afterpay service has been launched in the year 2015, and within a

limited period of time the service as proved to be a revelation in Australia with approximately

2.32 million people using the service for transaction (Aswani et al. 2018). The chief attraction of

the mentioned service includes After Pay payment service provides the consumer with the

opportunity to buy whatever product or service they want and enables them to make the payment

in four instalments paid fortnightly. The target consumer of the after pay service includes the

millenniums. The service is available at more than 10,000 shops throughout Australia and New

Zealand. While the mentioned service has drastically increased the sales of the organizations,

according to researchers this service has the potential to contribute towards increased financial

stress amongst the shoppers. Over the past few years, the mode of payment has been of great

concern to a large number of consumers especially the youngsters of the current generation.

Most of the young generation is fully focused on trending activities such as after pay method as

5MANAGEMENT

the purchasing tool across the world. While post payment services like Afterpay is imposing

positive impact on the sales of retail stores, it has the potential to impose negative impact on the

purchasing power of the consumers (Khalilzadeh, Ozturk and Bilgihan 2017). It has been found

that approximately 30 percent of the total users of Afterpay have missed the AfterPay payment

more than once. Considering the fact that majority of the purchases from Afterpay is made by

millenniums, in a survey, 65 percent of the participant stated that the fact they don’t have to pay

instantly for a particular product or the service enhanced their desire to buy the product which

they would not normally purchase. It has been seen that most purchased products that are being

purchased by the consumers using the after pay service includes luxury items. Majority of the

millenniums are found to be using this service for buying clothing.

According to psychologist, post payment services like AfterPay is deteriorating the

purchasing attitude of the teenagers as well as the millennium by enhancing their tendency to

purchase products on debts. While a good number of the Australian population is fine with the

concept of buying things in instalment since they believe that people who are opting for such a

option possess a steady income flow for meeting whatever payment they are obliged to,

according to several individuals, long term use of majority of the payment services can lead to a

scenario where people will lose track of the commitment or will get over burdened (Pei et al.

2015). Thus it has become really crucial for the organization to understand the perception of the

consumers about the Afterpay payment service. The chief purpose of this research study is to

indentify how the common people of Australia feels about Afterpay as a payment service tool.

The research paper will analyse if the consumers thinks that the Afterpay service has made their

life easier or have imposed negative impact on their purchasing behaviour.

the purchasing tool across the world. While post payment services like Afterpay is imposing

positive impact on the sales of retail stores, it has the potential to impose negative impact on the

purchasing power of the consumers (Khalilzadeh, Ozturk and Bilgihan 2017). It has been found

that approximately 30 percent of the total users of Afterpay have missed the AfterPay payment

more than once. Considering the fact that majority of the purchases from Afterpay is made by

millenniums, in a survey, 65 percent of the participant stated that the fact they don’t have to pay

instantly for a particular product or the service enhanced their desire to buy the product which

they would not normally purchase. It has been seen that most purchased products that are being

purchased by the consumers using the after pay service includes luxury items. Majority of the

millenniums are found to be using this service for buying clothing.

According to psychologist, post payment services like AfterPay is deteriorating the

purchasing attitude of the teenagers as well as the millennium by enhancing their tendency to

purchase products on debts. While a good number of the Australian population is fine with the

concept of buying things in instalment since they believe that people who are opting for such a

option possess a steady income flow for meeting whatever payment they are obliged to,

according to several individuals, long term use of majority of the payment services can lead to a

scenario where people will lose track of the commitment or will get over burdened (Pei et al.

2015). Thus it has become really crucial for the organization to understand the perception of the

consumers about the Afterpay payment service. The chief purpose of this research study is to

indentify how the common people of Australia feels about Afterpay as a payment service tool.

The research paper will analyse if the consumers thinks that the Afterpay service has made their

life easier or have imposed negative impact on their purchasing behaviour.

6MANAGEMENT

Research question

The chief aim of the research is to explore the perception of the individual towards afterpay as a

payment tool.

The chief objectives of this study are as follows:

a) To explore the customer behaviors over time

b) To explore the customer behavior theory and its application on the after pay methods

When it comes to the research questions of the paper, it is as follows:

a) What is consumer behaviour theory?

b) How does consumer behaviour theory affect market sales?

c) What is the effect of digital payments methods on consumer behaviours?

d) What are the effects of the After-play payments methods on consumer behaviours?

Literature review

After pay Payment tool

A payment system can be defined as a kind of system that is used for the settling the financial

transactions by transferring monetary value. The tool used for payment has been designed for

facilitating the acceptance of electronic payment for the purpose of online transactions. With the

emergence of technological development, online payment tools are gaining more and more

popularity (Kolinjivadi et al.2015). The chief reason behind this is the enhancement of internet

for both banking and shopping purposes by the consumers, especially the millennial. Amongst

Research question

The chief aim of the research is to explore the perception of the individual towards afterpay as a

payment tool.

The chief objectives of this study are as follows:

a) To explore the customer behaviors over time

b) To explore the customer behavior theory and its application on the after pay methods

When it comes to the research questions of the paper, it is as follows:

a) What is consumer behaviour theory?

b) How does consumer behaviour theory affect market sales?

c) What is the effect of digital payments methods on consumer behaviours?

d) What are the effects of the After-play payments methods on consumer behaviours?

Literature review

After pay Payment tool

A payment system can be defined as a kind of system that is used for the settling the financial

transactions by transferring monetary value. The tool used for payment has been designed for

facilitating the acceptance of electronic payment for the purpose of online transactions. With the

emergence of technological development, online payment tools are gaining more and more

popularity (Kolinjivadi et al.2015). The chief reason behind this is the enhancement of internet

for both banking and shopping purposes by the consumers, especially the millennial. Amongst

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT

the various online pay services available in Australia, the one that has attract the consumers to a

great level within a limited amount of time is the After pay payment service (Ab Hamid and

Cheng 2019). The mentioned payment service accepts both credits as well as debits and allows

the consumers to make any payment latter within a stipulated amount of time. The Afterpay

payment service was founded in Australia in the year 2015 and is currently used by more than 3

million users. According to Ab Hamid and Cheng (2019), the mentioned payment service is

currently one of the most used payment services available in Australia. In the year 2017, the

Afterpay group had merged with the After Touch group and this decision of the organization has

led to be the leader of the “buy now pay latter’ industry (Ab Hamid and Cheng 2019). Apart

from Australia, The Afterpay Touch group currently operates in United States, Australia and

New Zealand. The mentioned payment service is found to allow the retailers to offer the

consumers with the facility to buy any products on instalment which they are supposed to be paid

within 4 instalments. Additionally, the consumers are charged with no extra interest for the

instalment. However, in case a consumer fails to make the payment they are supposed to make

within the stipulated time, they needs to pay a penalty amount of 10 dollars as their first missed

payment penalty. Another obstacle of shopping or banking through the Afterpay payment service

includes the service can be used only by individuals who are above 18 years old (Imran et al.

2019).

Electronic payment

The term electronic payment is referred to the process of making payment for services or

goods through internet. An electronic payment includes any kind of non cash payment that does

not include a paper check. A good number of electronic payment methods are available in

Australia that includes credit cards, debit cards as well as Automated Clearing House Network.

the various online pay services available in Australia, the one that has attract the consumers to a

great level within a limited amount of time is the After pay payment service (Ab Hamid and

Cheng 2019). The mentioned payment service accepts both credits as well as debits and allows

the consumers to make any payment latter within a stipulated amount of time. The Afterpay

payment service was founded in Australia in the year 2015 and is currently used by more than 3

million users. According to Ab Hamid and Cheng (2019), the mentioned payment service is

currently one of the most used payment services available in Australia. In the year 2017, the

Afterpay group had merged with the After Touch group and this decision of the organization has

led to be the leader of the “buy now pay latter’ industry (Ab Hamid and Cheng 2019). Apart

from Australia, The Afterpay Touch group currently operates in United States, Australia and

New Zealand. The mentioned payment service is found to allow the retailers to offer the

consumers with the facility to buy any products on instalment which they are supposed to be paid

within 4 instalments. Additionally, the consumers are charged with no extra interest for the

instalment. However, in case a consumer fails to make the payment they are supposed to make

within the stipulated time, they needs to pay a penalty amount of 10 dollars as their first missed

payment penalty. Another obstacle of shopping or banking through the Afterpay payment service

includes the service can be used only by individuals who are above 18 years old (Imran et al.

2019).

Electronic payment

The term electronic payment is referred to the process of making payment for services or

goods through internet. An electronic payment includes any kind of non cash payment that does

not include a paper check. A good number of electronic payment methods are available in

Australia that includes credit cards, debit cards as well as Automated Clearing House Network.

8MANAGEMENT

Majority of the organizations provides the consumers with a good range of transaction options so

that they can pay for their purchase (Iberahim et al. 2016). Almost all the system of transaction,

the e-payment system is gaining high popularity and thank to its efficiency, convenience as well

as timeliness. Given its popularity, the mentioned payment system is largely embraced a well as

adopted continuously in the financial system inn both developing as well as developed countries.

In this era of information as well as communication technology, the operations have completely

changed the life of individuals (Gao and Waechter 2017). The digital technology is imposing

immense positive impact on the evolutionary development in finance. With the emergence of e-

payment, people are getting more and more inclined towards the current trend of cashless

transaction.

After the concept of cashless transaction is introduced, the payment methods used

globally is gradually changing from hard cash transaction to electronic forms which is not only

fast but is also more competitive in nature. The global annual non cash transactions are

facilitated by both mobile payment as well as e-payment (Chen et al. 2016). With emerging time,

the importance of e-payment in business is increasing over time since it is considered by both the

retailers as well as the shoppers to be both convenient as well as secure way of conducting

financial transaction.

Speed and efficiency

The speed of transactions in electronic payment services are meant for new technologies and for

satisfying the expectation as well as the requirements of the consumers (Drechsler et al. 2016).

The electronic payment is also quite efficient since it performs the best operation at each stage of

the process of payment.

Majority of the organizations provides the consumers with a good range of transaction options so

that they can pay for their purchase (Iberahim et al. 2016). Almost all the system of transaction,

the e-payment system is gaining high popularity and thank to its efficiency, convenience as well

as timeliness. Given its popularity, the mentioned payment system is largely embraced a well as

adopted continuously in the financial system inn both developing as well as developed countries.

In this era of information as well as communication technology, the operations have completely

changed the life of individuals (Gao and Waechter 2017). The digital technology is imposing

immense positive impact on the evolutionary development in finance. With the emergence of e-

payment, people are getting more and more inclined towards the current trend of cashless

transaction.

After the concept of cashless transaction is introduced, the payment methods used

globally is gradually changing from hard cash transaction to electronic forms which is not only

fast but is also more competitive in nature. The global annual non cash transactions are

facilitated by both mobile payment as well as e-payment (Chen et al. 2016). With emerging time,

the importance of e-payment in business is increasing over time since it is considered by both the

retailers as well as the shoppers to be both convenient as well as secure way of conducting

financial transaction.

Speed and efficiency

The speed of transactions in electronic payment services are meant for new technologies and for

satisfying the expectation as well as the requirements of the consumers (Drechsler et al. 2016).

The electronic payment is also quite efficient since it performs the best operation at each stage of

the process of payment.

9MANAGEMENT

Trust and Security

The e-payment system is known as the service that I used by individuals for transaction

of money with the help of using cash for purchasing product or services. the mention service is

popularly known as online payment system. The payment gate away as well as the payment

providers offers highly effective security along with tools that are antifraud for ensuring that the

transactions are highly reliable in nature. The challenges that are faced by the electronic payment

services mainly include concerns associated with privacy as well as information security.

Usually, the consumers as well as the commercial settings are known to have high trust on the

online payment system due to the efficient provision of the services as well as easy access to the

payment infrastructure (Safa and Von Solms 2016). Ehen it comes to the security in payment

system it generally includes information that is either personal or national and is confidential.

Since confidential information are needed while making e-payment, lack of security has the

potential to become a major obstacle between the consumers and the e-payment providing

organizations. In order to ensure data security, e-payment service providing organizations like

After pay involve methodology, practice as well as technology (Fletcher 2016). Therefore it can

be understood that electronic payment stools requires having all kinds of security features since

trust can be considered to be the mostly needed thing in order to ensure acceptance in clients.

Satisfaction of the consumers

The perception of the customers associated with digital payment is found to be highly

positive, thanks to numerous benefits associated with the same. According to Gafeeva, Hoelzl

and Roschk (2017), e-payment services that provides adequate information to the consumer and

are highly transparent in nature are found to have gained higher level of consumer satisfaction

Trust and Security

The e-payment system is known as the service that I used by individuals for transaction

of money with the help of using cash for purchasing product or services. the mention service is

popularly known as online payment system. The payment gate away as well as the payment

providers offers highly effective security along with tools that are antifraud for ensuring that the

transactions are highly reliable in nature. The challenges that are faced by the electronic payment

services mainly include concerns associated with privacy as well as information security.

Usually, the consumers as well as the commercial settings are known to have high trust on the

online payment system due to the efficient provision of the services as well as easy access to the

payment infrastructure (Safa and Von Solms 2016). Ehen it comes to the security in payment

system it generally includes information that is either personal or national and is confidential.

Since confidential information are needed while making e-payment, lack of security has the

potential to become a major obstacle between the consumers and the e-payment providing

organizations. In order to ensure data security, e-payment service providing organizations like

After pay involve methodology, practice as well as technology (Fletcher 2016). Therefore it can

be understood that electronic payment stools requires having all kinds of security features since

trust can be considered to be the mostly needed thing in order to ensure acceptance in clients.

Satisfaction of the consumers

The perception of the customers associated with digital payment is found to be highly

positive, thanks to numerous benefits associated with the same. According to Gafeeva, Hoelzl

and Roschk (2017), e-payment services that provides adequate information to the consumer and

are highly transparent in nature are found to have gained higher level of consumer satisfaction

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10MANAGEMENT

compared to the organizations that ensures confidentiality of their operation. The consumer

satisfaction gets affected by lower quality of information along with lower user interface quality.

In order to satisfy the requirements of the consumers, the information requires to be up to date

while offering the consumers with product or service. The information provided by the e-

payment organizations like After pay needs to be sufficient enough for helping the consumers to

make effective choices and to be user friendly. For this reason, it can be said that information

satisfaction will be affecting the behaviour of the customer purchase decision. The customers

with higher internet experience are supposed to be utilising the web channels for gathering the

item data. (Gao and Waechter 2017), According to Herbst-Murphy (2015), consumer

satisfaction can be considered as one of the most effective factor that determines the success rate

and enhancement in consumer base for a organization. recent studies have chiefly focused on

consumer satisfaction since this factor has imposed have impose impact on the behaviour of the

consumer while purchasing product a well as on their purchasing intentions.

The consumer satisfaction can also be een as an emotional and cognitive reaction that focuses on

the expectation of the consumers as well as their experience at a certain time It is known to

measure the perspective of the consumer on the service provided by an organization in terms of

quality of the product and serves provided by the same (Khan 2018). The consumers adopt a

technology when they find it quite easy for understanding along with finding it quite easy to

implement. The perceived usefulness is known to have a positive impact on the behavioural

intention for using the mobile banking.

Influencing the consumer behaviour

compared to the organizations that ensures confidentiality of their operation. The consumer

satisfaction gets affected by lower quality of information along with lower user interface quality.

In order to satisfy the requirements of the consumers, the information requires to be up to date

while offering the consumers with product or service. The information provided by the e-

payment organizations like After pay needs to be sufficient enough for helping the consumers to

make effective choices and to be user friendly. For this reason, it can be said that information

satisfaction will be affecting the behaviour of the customer purchase decision. The customers

with higher internet experience are supposed to be utilising the web channels for gathering the

item data. (Gao and Waechter 2017), According to Herbst-Murphy (2015), consumer

satisfaction can be considered as one of the most effective factor that determines the success rate

and enhancement in consumer base for a organization. recent studies have chiefly focused on

consumer satisfaction since this factor has imposed have impose impact on the behaviour of the

consumer while purchasing product a well as on their purchasing intentions.

The consumer satisfaction can also be een as an emotional and cognitive reaction that focuses on

the expectation of the consumers as well as their experience at a certain time It is known to

measure the perspective of the consumer on the service provided by an organization in terms of

quality of the product and serves provided by the same (Khan 2018). The consumers adopt a

technology when they find it quite easy for understanding along with finding it quite easy to

implement. The perceived usefulness is known to have a positive impact on the behavioural

intention for using the mobile banking.

Influencing the consumer behaviour

11MANAGEMENT

The electronic payment system is known to influence the consumer behaviour. The

shopping posses a paradigm shifts that takes place due to a technological influence. In this study,

the consumer behaviour of individuals along with the experiences or the ideas to satisfy the

requirements as well as the impacts of the processes on the consumers along with the society

(Aswani et al., 2018). This study aims to state the changes in the consumer behaviour as the

result of the electronic payment system. Individuals spend a good amount of time on shopping in

online sites and refer to by online products. There prevail a good number of changes when it

comes to modes of selection. According to researchers, convenience of shopping has been found

to be playing one of the most crucial roles for consumers while making decisions for online

shopping paying methods.

Cost

According to Omair (2014), online shopping procedures results in lower price payment for

products purchased by consumers compared to that of the traditional practices of payment.

Consumers are found to be charged higher for similar products when they shop offline.

Considering the fact that cost is a highly crucial parameter when it comes to the process of

consumer choice. The consumers possess the potential to research for a huge number of time for

going through the products along with evaluating the information of non process attributes. The

consumers associated with the e-market is supposed to have greater information about the

services as well as the products (Liébana-Cabanillas, Herrera and Guillén 2016), The annual non

cash transaction gets facilitate with the help of mobile payment as well as epayments. The

process of E-payment is considered to be one of the crucial mechanisms that is used by the

individuals along with the organizations as a secure as well as a convenient way of making the

payments over the internet. The system of electronic payment is found to have attracted a huge

The electronic payment system is known to influence the consumer behaviour. The

shopping posses a paradigm shifts that takes place due to a technological influence. In this study,

the consumer behaviour of individuals along with the experiences or the ideas to satisfy the

requirements as well as the impacts of the processes on the consumers along with the society

(Aswani et al., 2018). This study aims to state the changes in the consumer behaviour as the

result of the electronic payment system. Individuals spend a good amount of time on shopping in

online sites and refer to by online products. There prevail a good number of changes when it

comes to modes of selection. According to researchers, convenience of shopping has been found

to be playing one of the most crucial roles for consumers while making decisions for online

shopping paying methods.

Cost

According to Omair (2014), online shopping procedures results in lower price payment for

products purchased by consumers compared to that of the traditional practices of payment.

Consumers are found to be charged higher for similar products when they shop offline.

Considering the fact that cost is a highly crucial parameter when it comes to the process of

consumer choice. The consumers possess the potential to research for a huge number of time for

going through the products along with evaluating the information of non process attributes. The

consumers associated with the e-market is supposed to have greater information about the

services as well as the products (Liébana-Cabanillas, Herrera and Guillén 2016), The annual non

cash transaction gets facilitate with the help of mobile payment as well as epayments. The

process of E-payment is considered to be one of the crucial mechanisms that is used by the

individuals along with the organizations as a secure as well as a convenient way of making the

payments over the internet. The system of electronic payment is found to have attracted a huge

12MANAGEMENT

amount of attention from the researchers as well as the information system (Park and Ha 2014).

Due to this reason, while customers will be making choice of their products, they are supposed to

be include informed as well as will possess higher opportunity to be fully informed. Therefore, it

can be said that cost efficiency possess huge impact on the behaviour of the purchase of the

consumers.

Types of e payment service

There are also many e-payment facilities that are established throughout the world within the

payment system. The e-paid facilities include money, digital funds transfers and loan cards. The

electronic payments system has four categories: online card payments, electronic checks, small

payments and electronic cheques. Although the e-payment facilities in the sector present both

benefits and disadvantages. According to ( Marinkovic, V. and Kalinic, Z., 2017 ) there are also

many e-payment facilities that are established throughout the world within the payment system.

The e-paid facilities include money, digital funds transfers and loan cards. The electronic

payments system has four categories: online card payments, electronic checks, small payments

and electronic cheques. Although the e-payment facilities in the sector present both benefits and

disadvantages. Credit transfers, e-card cash, book charges and debit coins are considered to be

used in the commercial industry (Penz. and Sinkovics 2013). In addition to the technological

progress, the payment system has increased considerably. The e-commerce scheme and

technological developments now allow the convenience of electronic cashless transfers. In

activities which were expected to develop quickly, the electronic structure became more and

more complex since the 1960's (Saini and Sharma 2017). The electronic payments are known to

be one of the necessary part of the E commerce and is also one of the most critical aspects. An e

amount of attention from the researchers as well as the information system (Park and Ha 2014).

Due to this reason, while customers will be making choice of their products, they are supposed to

be include informed as well as will possess higher opportunity to be fully informed. Therefore, it

can be said that cost efficiency possess huge impact on the behaviour of the purchase of the

consumers.

Types of e payment service

There are also many e-payment facilities that are established throughout the world within the

payment system. The e-paid facilities include money, digital funds transfers and loan cards. The

electronic payments system has four categories: online card payments, electronic checks, small

payments and electronic cheques. Although the e-payment facilities in the sector present both

benefits and disadvantages. According to ( Marinkovic, V. and Kalinic, Z., 2017 ) there are also

many e-payment facilities that are established throughout the world within the payment system.

The e-paid facilities include money, digital funds transfers and loan cards. The electronic

payments system has four categories: online card payments, electronic checks, small payments

and electronic cheques. Although the e-payment facilities in the sector present both benefits and

disadvantages. Credit transfers, e-card cash, book charges and debit coins are considered to be

used in the commercial industry (Penz. and Sinkovics 2013). In addition to the technological

progress, the payment system has increased considerably. The e-commerce scheme and

technological developments now allow the convenience of electronic cashless transfers. In

activities which were expected to develop quickly, the electronic structure became more and

more complex since the 1960's (Saini and Sharma 2017). The electronic payments are known to

be one of the necessary part of the E commerce and is also one of the most critical aspects. An e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13MANAGEMENT

commerce payment system is known to facilitate the acceptance of electronic payment for the

online transaction.

Environment friendly

The disposal of paper cash is renowned to bring enormous advantages that go beyond

client comfort. The benefits of billing instruments for preventing economic risks include

reducing the expense of fare-taking, reducing repair costs, reducing the price of paper and

currency manufacturing, and also reducing vibration and water contamination. Currently, both

metropolitan traffic and water emissions are two of the major issues faced by towns. One of the

biggest advantage of the cash transaction is that they help in reducing pollution (Khalilzadeh,

Ozturk. and Bilgihan 2017). The need to produce document, print cash and delivery can also

readily be prevented with the aid of cashless operations. It is recognized that the electronic

payment technique reduces the global carbon footprint. Therefore, the cashless economy is well

regarded to be extremely common. It is recognized that digital cash is tracked very readily. The

electronic payment of this kind is considered to reduce the danger of disease transfer and thus

also reduces contamination from the records.

Issues related to payment tools

The utility suppliers and few companies presently provide billing instruments to a limited

extent due to multiple safety problems. Nevertheless, most of them are regarded to assist loan

card operations. Users must be provided with the option to adopt a variety of transaction

alternatives like ATM cards and E checks to exploit the complete capacity of internet e-

commerce (Waller, 2017). One of the problems that the billing gateways currently encounter is

that this system only applies to operations between clients and businesses, while disregarding

commerce payment system is known to facilitate the acceptance of electronic payment for the

online transaction.

Environment friendly

The disposal of paper cash is renowned to bring enormous advantages that go beyond

client comfort. The benefits of billing instruments for preventing economic risks include

reducing the expense of fare-taking, reducing repair costs, reducing the price of paper and

currency manufacturing, and also reducing vibration and water contamination. Currently, both

metropolitan traffic and water emissions are two of the major issues faced by towns. One of the

biggest advantage of the cash transaction is that they help in reducing pollution (Khalilzadeh,

Ozturk. and Bilgihan 2017). The need to produce document, print cash and delivery can also

readily be prevented with the aid of cashless operations. It is recognized that the electronic

payment technique reduces the global carbon footprint. Therefore, the cashless economy is well

regarded to be extremely common. It is recognized that digital cash is tracked very readily. The

electronic payment of this kind is considered to reduce the danger of disease transfer and thus

also reduces contamination from the records.

Issues related to payment tools

The utility suppliers and few companies presently provide billing instruments to a limited

extent due to multiple safety problems. Nevertheless, most of them are regarded to assist loan

card operations. Users must be provided with the option to adopt a variety of transaction

alternatives like ATM cards and E checks to exploit the complete capacity of internet e-

commerce (Waller, 2017). One of the problems that the billing gateways currently encounter is

that this system only applies to operations between clients and businesses, while disregarding

14MANAGEMENT

valuable public revenue (Cagliano, De Marco and Rafele 2017). Other problems include

problems, little data on payments and a absence of confidence. With on-line loans becoming very

common, safety risks can also occur in the manner of currently ongoing malware, robbery,

spyware, fraud and information safety violations. Confidentiality, privacy, honesty and non-

repudiation are regarded as the safety transaction portal. It can be stated, therefore, by stating

that safety is one of the clients ' greatest issues. Consumers will not be prepared to rely on fresh

technology to improve the safety of transaction instruments.

valuable public revenue (Cagliano, De Marco and Rafele 2017). Other problems include

problems, little data on payments and a absence of confidence. With on-line loans becoming very

common, safety risks can also occur in the manner of currently ongoing malware, robbery,

spyware, fraud and information safety violations. Confidentiality, privacy, honesty and non-

repudiation are regarded as the safety transaction portal. It can be stated, therefore, by stating

that safety is one of the clients ' greatest issues. Consumers will not be prepared to rely on fresh

technology to improve the safety of transaction instruments.

15MANAGEMENT

Consumer Behavior Theory

Consumer behaviors relate to how a person or a band chooses an item, buys it, uses it and

expects it to meet their requirements (Khan 2018). Park and Ha (2014) state that consumer

behaviors are a phenomenon which depends on the availability and requirement of products and

facilities in buying choices for products and facilities. The research of customer behavior in

relation to a commodity thus relates to the concept of customer conduct.

Consumer payment trends

Over the last century, payment techniques for shops have changed operations, a technological

growth and customer behaviour, from document controls to stamps and digital payments. In the

past, most of the world's consumers used cash and the credit card as their payment method.

However, one of the most non-cash transfers by customers has been a debit card during the

previous century (Linder 2017).

Factors affecting consumer payments choice

Even if most customer purchases are focused on private choice, supplies such as price, software,

billing tools and regulations are always regulated (Saini & Sharma 2017).

Cost

Payment costs are among the significant variables which both the customer and the merchant

take into consideration, although they are not always clear. The costs of compensation can have a

beneficial or adverse effect on the buying choices either directly or indirectly (Martínez-Camblor

and Corral 2011). If consumer costs are large, the majority of customers appear to search for

easier and easier techniques of payment. While little proof exists on the impact of the billing

Consumer Behavior Theory

Consumer behaviors relate to how a person or a band chooses an item, buys it, uses it and

expects it to meet their requirements (Khan 2018). Park and Ha (2014) state that consumer

behaviors are a phenomenon which depends on the availability and requirement of products and

facilities in buying choices for products and facilities. The research of customer behavior in

relation to a commodity thus relates to the concept of customer conduct.

Consumer payment trends

Over the last century, payment techniques for shops have changed operations, a technological

growth and customer behaviour, from document controls to stamps and digital payments. In the

past, most of the world's consumers used cash and the credit card as their payment method.

However, one of the most non-cash transfers by customers has been a debit card during the

previous century (Linder 2017).

Factors affecting consumer payments choice

Even if most customer purchases are focused on private choice, supplies such as price, software,

billing tools and regulations are always regulated (Saini & Sharma 2017).

Cost

Payment costs are among the significant variables which both the customer and the merchant

take into consideration, although they are not always clear. The costs of compensation can have a

beneficial or adverse effect on the buying choices either directly or indirectly (Martínez-Camblor

and Corral 2011). If consumer costs are large, the majority of customers appear to search for

easier and easier techniques of payment. While little proof exists on the impact of the billing

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16MANAGEMENT

technique on Australia's customer behavior, empirical proof exists throughout the globe.

Drechsler, Smith, Sturm and Wätzold (2016) found, for example, that the cost incentives had a

positive effect on the payment process both in Norway and the Netherlands on the demand for

products. Retailers use price discounts in the United States and give opportunities to encourage

clients to use payroll instruments that are considered to be less costly and permitted in the

corresponding shops to boost product revenues.

Security

Security of payments is now an significant part of the developing world of technology. The

results of this annual Survey, which introduces safety as the top over costs, comfort and other

elements, are provided by the Consumer Payment Choice (Waller 2017). Past studies indicate

that widely security breaches during the payment process have a direct impact on consumer

behaviour and payment choice since there subjective belief is affected.

Transparency

Purchasing choices are controlled by transparency of payments according to Gafeeva, Hoelzl,

and Roschk (2017) many customers. In addition of both concrete shape as well as valuation, the

writers state payment openness as the temporary outcome of compensation. Over the years, the

most transparent form of payments has been cash, as both stakeholders are able to see, touch and

feel both the exchange of money and the service and product. Herbst (2015) argues that

transparency is directly connected to purchase experienced during payment thus the use of cash

compares absolutely with the level of pain felt. Most clients therefore think that the after-

payment technique is more open than any other type in force, since they are able to use the goods

bought and to know about them before purchase is completed, contributing to high-quality goods

technique on Australia's customer behavior, empirical proof exists throughout the globe.

Drechsler, Smith, Sturm and Wätzold (2016) found, for example, that the cost incentives had a

positive effect on the payment process both in Norway and the Netherlands on the demand for

products. Retailers use price discounts in the United States and give opportunities to encourage

clients to use payroll instruments that are considered to be less costly and permitted in the

corresponding shops to boost product revenues.

Security

Security of payments is now an significant part of the developing world of technology. The

results of this annual Survey, which introduces safety as the top over costs, comfort and other

elements, are provided by the Consumer Payment Choice (Waller 2017). Past studies indicate

that widely security breaches during the payment process have a direct impact on consumer

behaviour and payment choice since there subjective belief is affected.

Transparency

Purchasing choices are controlled by transparency of payments according to Gafeeva, Hoelzl,

and Roschk (2017) many customers. In addition of both concrete shape as well as valuation, the

writers state payment openness as the temporary outcome of compensation. Over the years, the

most transparent form of payments has been cash, as both stakeholders are able to see, touch and

feel both the exchange of money and the service and product. Herbst (2015) argues that

transparency is directly connected to purchase experienced during payment thus the use of cash

compares absolutely with the level of pain felt. Most clients therefore think that the after-

payment technique is more open than any other type in force, since they are able to use the goods

bought and to know about them before purchase is completed, contributing to high-quality goods

17MANAGEMENT

being obtained. There are countless advantages after delivery, such as an simple and effective

refund scheme, a stronger option for loan card, a quick billing method, both offline and internet

and no charge and interest-free billing processes (Herbst 2015). However, the tool also poses

some disadvantages to consumers such as impulse buying increasing spending thus might affect

the customer in future.

User-friendliness – The feelings of the consumer towards the instrument of compensation are

linked to variables such as security and velocity where delivery is fast and safe, and individuals

appear to have a favorable stance towards the tool (Humbani and Wiese 2017). Because of their

usability, most individuals use various transaction instruments. Due to the fact that

uncomplicated instruments are easily remembered in the past, they appear to generate a powerful

desire among individuals to use the instruments during the acquisitions phase, which is not a

complex instrument.

A conceptual model for payment perception

The mental transaction awareness system is built on a range of social and psychological

variables, including approach, intent and real behavior.

being obtained. There are countless advantages after delivery, such as an simple and effective

refund scheme, a stronger option for loan card, a quick billing method, both offline and internet

and no charge and interest-free billing processes (Herbst 2015). However, the tool also poses

some disadvantages to consumers such as impulse buying increasing spending thus might affect

the customer in future.

User-friendliness – The feelings of the consumer towards the instrument of compensation are

linked to variables such as security and velocity where delivery is fast and safe, and individuals

appear to have a favorable stance towards the tool (Humbani and Wiese 2017). Because of their

usability, most individuals use various transaction instruments. Due to the fact that

uncomplicated instruments are easily remembered in the past, they appear to generate a powerful

desire among individuals to use the instruments during the acquisitions phase, which is not a

complex instrument.

A conceptual model for payment perception

The mental transaction awareness system is built on a range of social and psychological

variables, including approach, intent and real behavior.

18MANAGEMENT

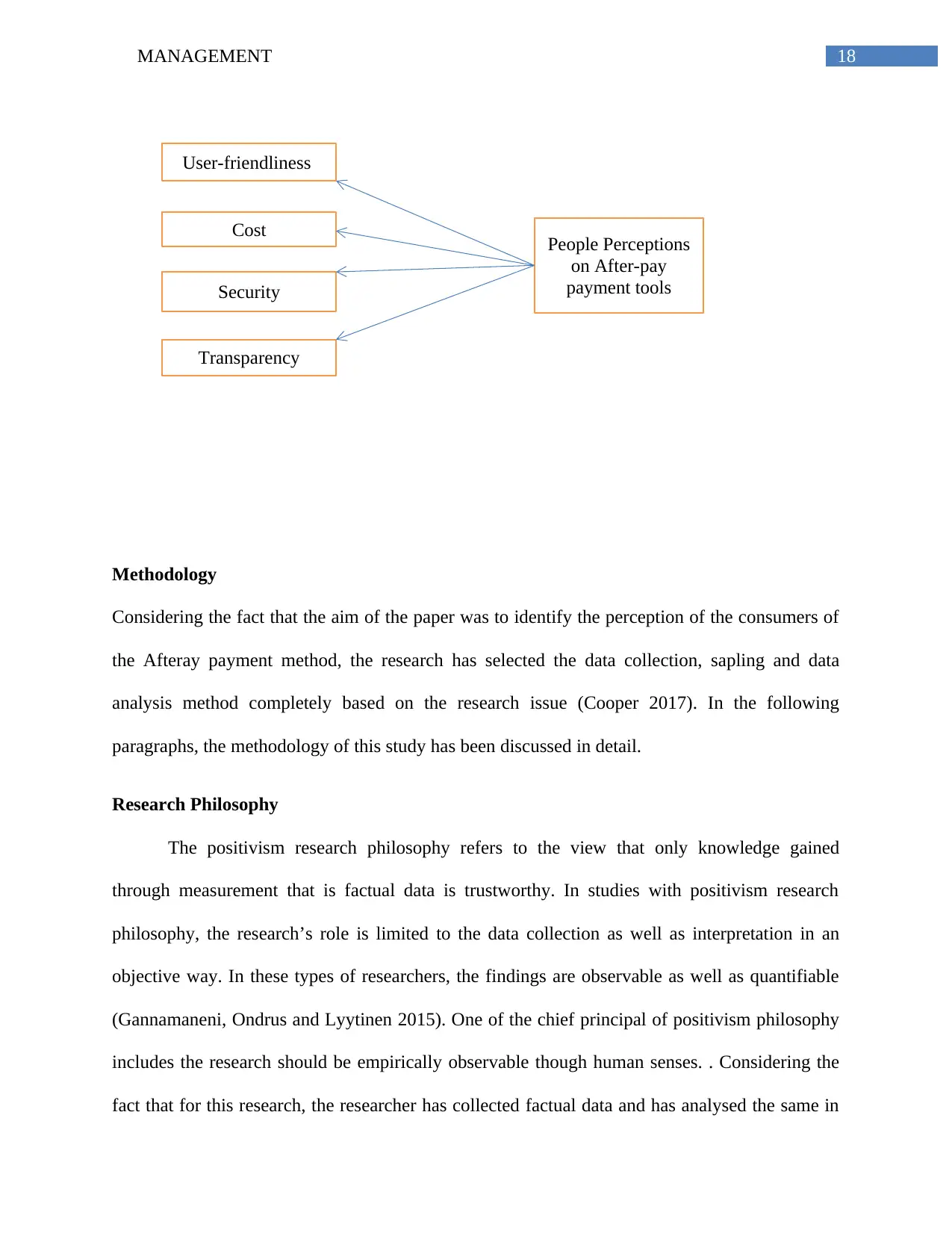

User-friendliness

Security

Transparency

Cost People Perceptions

on After-pay

payment tools

Methodology

Considering the fact that the aim of the paper was to identify the perception of the consumers of

the Afteray payment method, the research has selected the data collection, sapling and data

analysis method completely based on the research issue (Cooper 2017). In the following

paragraphs, the methodology of this study has been discussed in detail.

Research Philosophy

The positivism research philosophy refers to the view that only knowledge gained

through measurement that is factual data is trustworthy. In studies with positivism research

philosophy, the research’s role is limited to the data collection as well as interpretation in an

objective way. In these types of researchers, the findings are observable as well as quantifiable

(Gannamaneni, Ondrus and Lyytinen 2015). One of the chief principal of positivism philosophy

includes the research should be empirically observable though human senses. . Considering the

fact that for this research, the researcher has collected factual data and has analysed the same in

User-friendliness

Security

Transparency

Cost People Perceptions

on After-pay

payment tools

Methodology

Considering the fact that the aim of the paper was to identify the perception of the consumers of

the Afteray payment method, the research has selected the data collection, sapling and data

analysis method completely based on the research issue (Cooper 2017). In the following

paragraphs, the methodology of this study has been discussed in detail.

Research Philosophy

The positivism research philosophy refers to the view that only knowledge gained

through measurement that is factual data is trustworthy. In studies with positivism research

philosophy, the research’s role is limited to the data collection as well as interpretation in an

objective way. In these types of researchers, the findings are observable as well as quantifiable

(Gannamaneni, Ondrus and Lyytinen 2015). One of the chief principal of positivism philosophy

includes the research should be empirically observable though human senses. . Considering the

fact that for this research, the researcher has collected factual data and has analysed the same in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19MANAGEMENT

order to obtain the answer of the research questions, in this research paper, the positivism

research philosophy has been followed.

Research Design

For this study, the research design chosen in exploratory research design. Exploratory researches

are defined as researches that are used for investigating a certain issue that is not clearly defined.

These types of researches are conducted in order to possess a better understanding of the existing

issue that does not possess the potential to provide conclusive result. In order to conduct an

exploratory research, a researcher initiates with a general idea and the research is used as a

medium for identifying various issues that has the potential to be the focus of the final research

(Anderson et al. 2017). When conducting exploratory research, the researcher ought to be willing

to change his/her direction as a result of revelation of new data and new insights. Considering the

fact the chief aim of the research is to explore the perception of the common people about the

Afterpay payment services, it can be clearly understood that the study aims to explore the

research topic with varying levels of depth. According to researcher, the exploratory researches

can be considered as initial researchers, that forms the basis of more conclusive research

(Pourfallah et al. 2017). Exploratory researchers like this one, tends to tackle ne issues on which

little or no previous research has been conducted. Considering the fact that very limited number

of researches has been conducted on the after pay payment services and its perception of the

same on the common people, the researcher has selected exploratory research design for this

study.

Research Approach

Inductive research approach, popularly known as inductive reasoning can be defined as the

research approach that initiate with the observation as well as theories are proposed towards the

order to obtain the answer of the research questions, in this research paper, the positivism

research philosophy has been followed.

Research Design

For this study, the research design chosen in exploratory research design. Exploratory researches

are defined as researches that are used for investigating a certain issue that is not clearly defined.

These types of researches are conducted in order to possess a better understanding of the existing

issue that does not possess the potential to provide conclusive result. In order to conduct an

exploratory research, a researcher initiates with a general idea and the research is used as a

medium for identifying various issues that has the potential to be the focus of the final research

(Anderson et al. 2017). When conducting exploratory research, the researcher ought to be willing

to change his/her direction as a result of revelation of new data and new insights. Considering the

fact the chief aim of the research is to explore the perception of the common people about the

Afterpay payment services, it can be clearly understood that the study aims to explore the

research topic with varying levels of depth. According to researcher, the exploratory researches

can be considered as initial researchers, that forms the basis of more conclusive research

(Pourfallah et al. 2017). Exploratory researchers like this one, tends to tackle ne issues on which

little or no previous research has been conducted. Considering the fact that very limited number

of researches has been conducted on the after pay payment services and its perception of the

same on the common people, the researcher has selected exploratory research design for this

study.

Research Approach

Inductive research approach, popularly known as inductive reasoning can be defined as the

research approach that initiate with the observation as well as theories are proposed towards the

20MANAGEMENT

end of the research process as a result of the observations. According to researchers, the

inductive research approach includes the search for patterns from observation as well as the

development of explanations for those patterns with the help of series of hypothesis

(Balachandran et al. 2015). Considering the fact that in this research paper the researcher has

explored a research issue that has been researched on by a highly limited number of researchers

previously, the research approach for this study is inductive research approach. No hypotheses

can be found at the initial stages of the research and the researcher is not sure about the type and

nature of the research findings until the study is completed.

Data collection method

Both primary as well as secondary data has been collected for this research. A primary data

source can be defined as the sources from high data are directly collected by the researcher for

the first time. A good number of sources are there from which researchers collect primary data

for their study (Arner, Barberis and Buckley 2015). Some of the popular primary data collection

sources for researcher include surveys, interviews, field observation, and experiments. In order to

conduct this research, the researcher has conducted a survey. The researcher have developed a

questionnaire on the basis of which a survey has been conducted. The questionnaire has been

provided with the participants and the questions developed have majorly focused on the

perception o the participants on the payment services used by them. The survey has been

conducted with the student of Holmes College of Australia The chief aim of the survey has been

providing specific information regarding the impact of Afterpay on the market a well as on the

store’s sale.

Along with the collection of primary data, for this research secondary data has also been

collected. The secondary data sources are referred to the sources which contains information that

end of the research process as a result of the observations. According to researchers, the

inductive research approach includes the search for patterns from observation as well as the

development of explanations for those patterns with the help of series of hypothesis

(Balachandran et al. 2015). Considering the fact that in this research paper the researcher has

explored a research issue that has been researched on by a highly limited number of researchers

previously, the research approach for this study is inductive research approach. No hypotheses

can be found at the initial stages of the research and the researcher is not sure about the type and

nature of the research findings until the study is completed.

Data collection method

Both primary as well as secondary data has been collected for this research. A primary data

source can be defined as the sources from high data are directly collected by the researcher for

the first time. A good number of sources are there from which researchers collect primary data

for their study (Arner, Barberis and Buckley 2015). Some of the popular primary data collection

sources for researcher include surveys, interviews, field observation, and experiments. In order to

conduct this research, the researcher has conducted a survey. The researcher have developed a

questionnaire on the basis of which a survey has been conducted. The questionnaire has been

provided with the participants and the questions developed have majorly focused on the

perception o the participants on the payment services used by them. The survey has been

conducted with the student of Holmes College of Australia The chief aim of the survey has been

providing specific information regarding the impact of Afterpay on the market a well as on the

store’s sale.

Along with the collection of primary data, for this research secondary data has also been

collected. The secondary data sources are referred to the sources which contains information that

21MANAGEMENT

was collected by individuals for other purposes rather than this specific research (Iorio 2015).

Some of the major sources of secondary data collection include organizational records,

governmental papers and academic journals. For this research, the secondary data has been

collected from previous academic journals that were relevant t the research topic. Along with this

information has also been collected from the official site of the After pay payment facility.

Sampling

For this research, probability sampling has been performed. Probability sampling

technique can be defined as sampling technique was the sample from a larger population is

selected using the method that is based on the theory of probability. Participants who are found

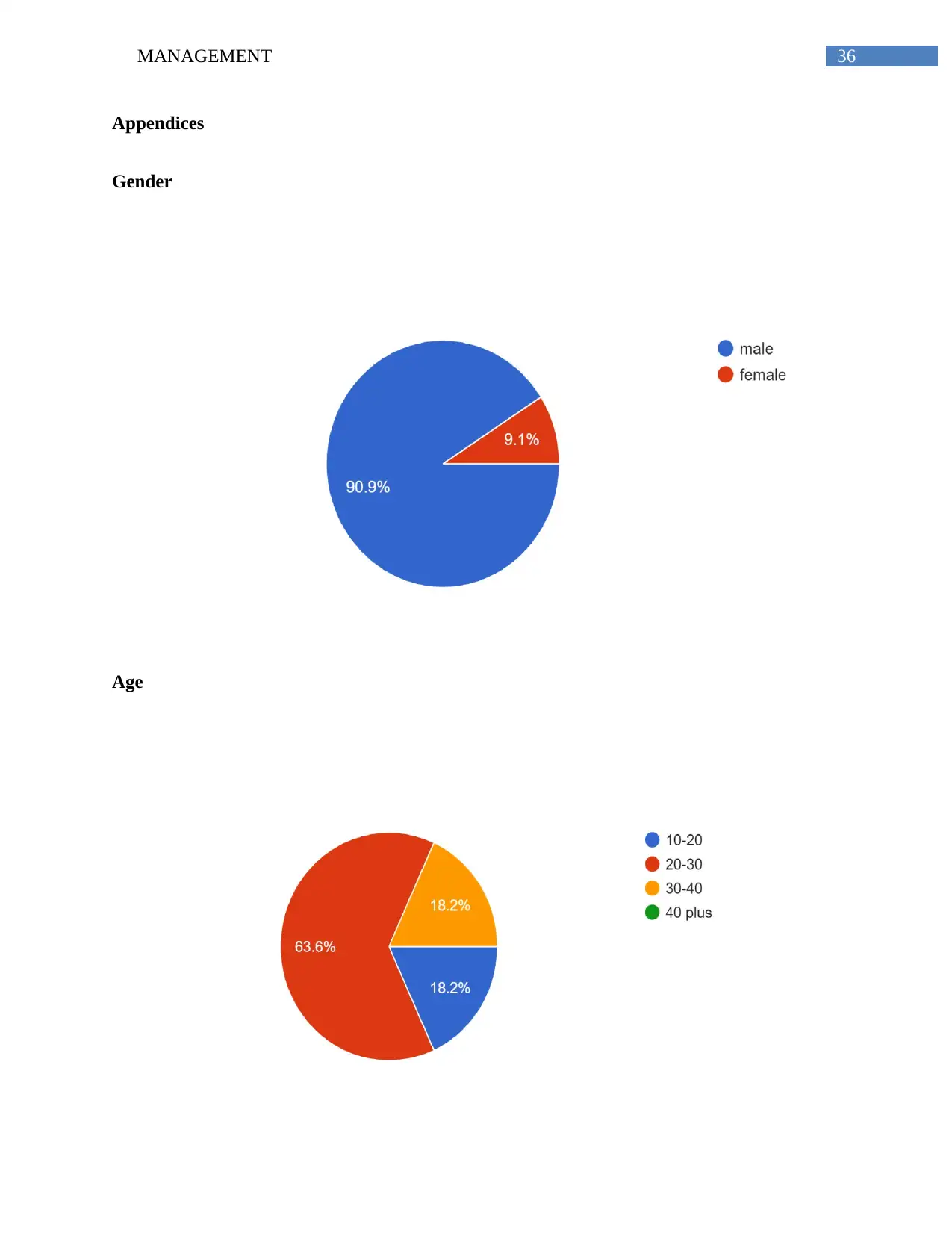

to be prone to shopping activates have been selected from Holmes College . A sample size of 11

students obtained from the entire population will be randomly approached, provided with all

information regarding the purpose of the paper as well as a consent form (Arner, Barberis and

Buckley 2015). Considering the fact that the research is free from gender bias, the samples were

selected irrespective of their Gender. However, all the samples selected were above 18 years old.

When it comes to sampling for secondary data, non probability sampling has been used

by the researcher. When it comes to the non probability sampling technique, it is refered to the

sample technique where the samples are gathered in a process in which equal chances for getting

selected is not provided to all the participants. 20 research articles that were relevant to the

research topic have been selected by the researcher. While selecting the articles, a good number

of exclusion criteria have been kept in mind. First of all, articles that are published within the

recent 5 years have been selected by the researcher in order to ensure relevancy with the

contemporary period. Along with this, articles that are written in the English language has been

was collected by individuals for other purposes rather than this specific research (Iorio 2015).

Some of the major sources of secondary data collection include organizational records,

governmental papers and academic journals. For this research, the secondary data has been

collected from previous academic journals that were relevant t the research topic. Along with this

information has also been collected from the official site of the After pay payment facility.

Sampling

For this research, probability sampling has been performed. Probability sampling

technique can be defined as sampling technique was the sample from a larger population is

selected using the method that is based on the theory of probability. Participants who are found

to be prone to shopping activates have been selected from Holmes College . A sample size of 11

students obtained from the entire population will be randomly approached, provided with all

information regarding the purpose of the paper as well as a consent form (Arner, Barberis and

Buckley 2015). Considering the fact that the research is free from gender bias, the samples were

selected irrespective of their Gender. However, all the samples selected were above 18 years old.

When it comes to sampling for secondary data, non probability sampling has been used

by the researcher. When it comes to the non probability sampling technique, it is refered to the

sample technique where the samples are gathered in a process in which equal chances for getting

selected is not provided to all the participants. 20 research articles that were relevant to the

research topic have been selected by the researcher. While selecting the articles, a good number

of exclusion criteria have been kept in mind. First of all, articles that are published within the

recent 5 years have been selected by the researcher in order to ensure relevancy with the

contemporary period. Along with this, articles that are written in the English language has been

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22MANAGEMENT

selected. Finally academic articles that belonged to scholar journals have been selected in order

to ensure the authenticity of the data obtained.

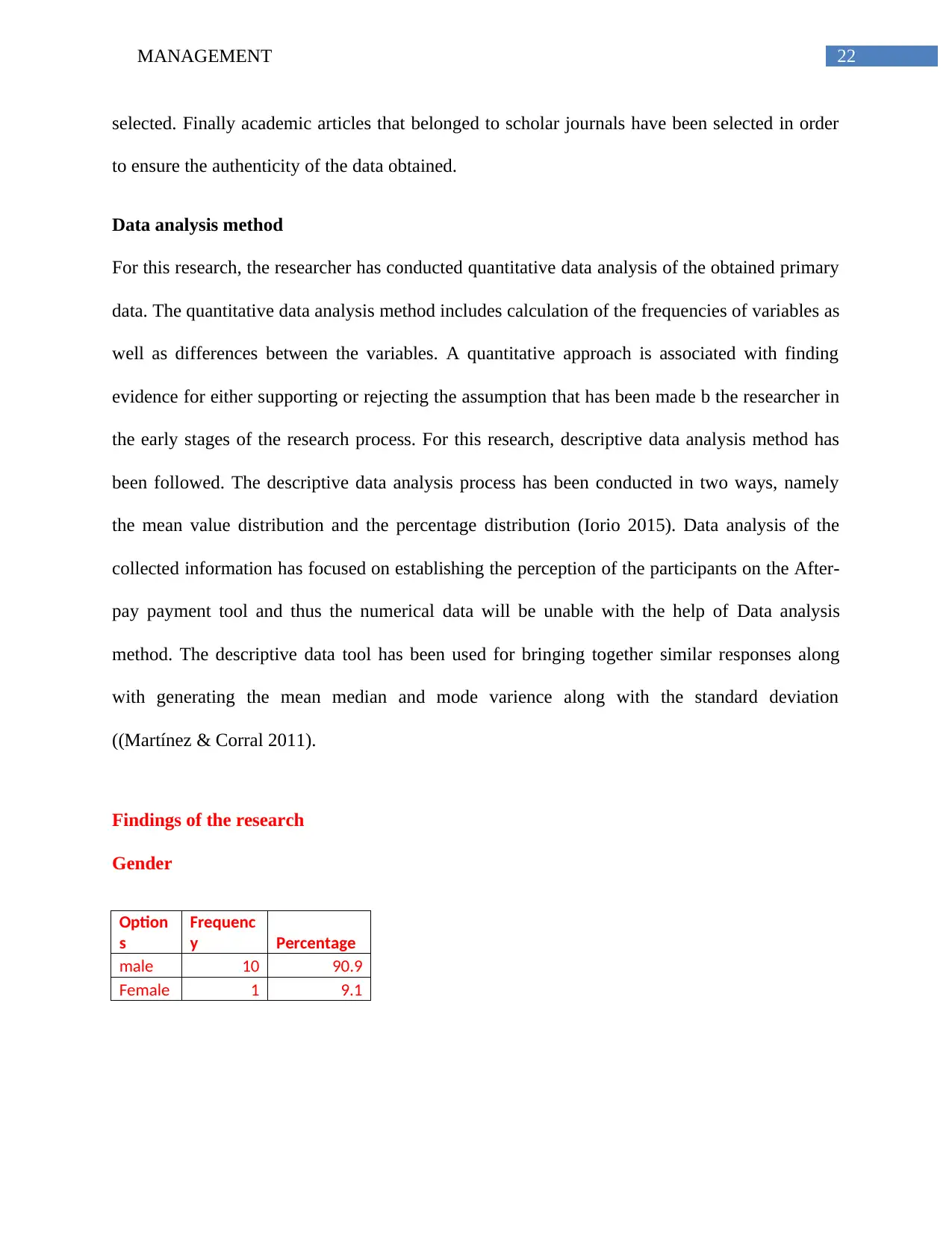

Data analysis method

For this research, the researcher has conducted quantitative data analysis of the obtained primary

data. The quantitative data analysis method includes calculation of the frequencies of variables as

well as differences between the variables. A quantitative approach is associated with finding