Management Accounting Case Study: HLW Club Financial Analysis Report

VerifiedAdded on 2020/05/28

|15

|2678

|87

Case Study

AI Summary

This case study focuses on the management accounting practices of the HLW club, analyzing its financial performance and the impact of different strategies. Part A delves into cost accounting, specifically overhead and direct costs related to product costing. Part B examines the club's revenue streams, including membership and court fees, and assesses the potential of a new membership plan to improve sales and cash flow. The analysis includes calculations of revenue under current and proposed plans, considering various assumptions about court usage. The study also addresses factors influencing the implementation of the new plan, such as potential member loss and the need for promotional campaigns. The conclusion highlights the benefits of activity-based costing and the importance of accurate business information for effective decision-making.

Running head: MANAGEMENT ACCOUNTIGN

Management Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Management Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTIGN

Executive summary:

Management accounting refers to the procedure used in the planning of the management

reports together with the accounts that helps in providing timely and appropriate

understanding of the monetary information to the executives. Such kind of management

accounting information helps the managers in undertaking the short and long term decisions.

On the alternative, the financial accounting assist in providing the information to the financial

users that helps in correct implementation of the business functions. Cost accounting on the

other hand helps in determining the cost that is engaged in the sale of products that is

manufactured by implementing numerous techniques and means. As evident in the first part

of the case study the ultimate purpose of this study is ascertain the cost of overhead that is

incurred in determining the product cost. The second part is engaged in the assessment of the

cash flow in order to determine the potentiality of the new plan that can be implemented by

the manager.

Executive summary:

Management accounting refers to the procedure used in the planning of the management

reports together with the accounts that helps in providing timely and appropriate

understanding of the monetary information to the executives. Such kind of management

accounting information helps the managers in undertaking the short and long term decisions.

On the alternative, the financial accounting assist in providing the information to the financial

users that helps in correct implementation of the business functions. Cost accounting on the

other hand helps in determining the cost that is engaged in the sale of products that is

manufactured by implementing numerous techniques and means. As evident in the first part

of the case study the ultimate purpose of this study is ascertain the cost of overhead that is

incurred in determining the product cost. The second part is engaged in the assessment of the

cash flow in order to determine the potentiality of the new plan that can be implemented by

the manager.

2MANAGEMENT ACCOUNTIGN

Table of Contents

Assessment task part A:.............................................................................................................4

Answer to requirement 1:...........................................................................................................4

Answer to requirement B:..........................................................................................................4

Answer to question C:................................................................................................................5

Assessment Task Part B:............................................................................................................6

Answer to requirement A:..........................................................................................................6

Answer to requirement 2:...........................................................................................................7

Revenue generated under the current plan:................................................................................8

Yearly Membership Revenue:....................................................................................................8

Total amount of Court Fees:......................................................................................................8

Total volume of Sales revenue derived:.....................................................................................9

Sales generated under the new plans of membership:...............................................................9

Revenue derived from the previous membership:.....................................................................9

Revenue generated from the usual membership:.......................................................................9

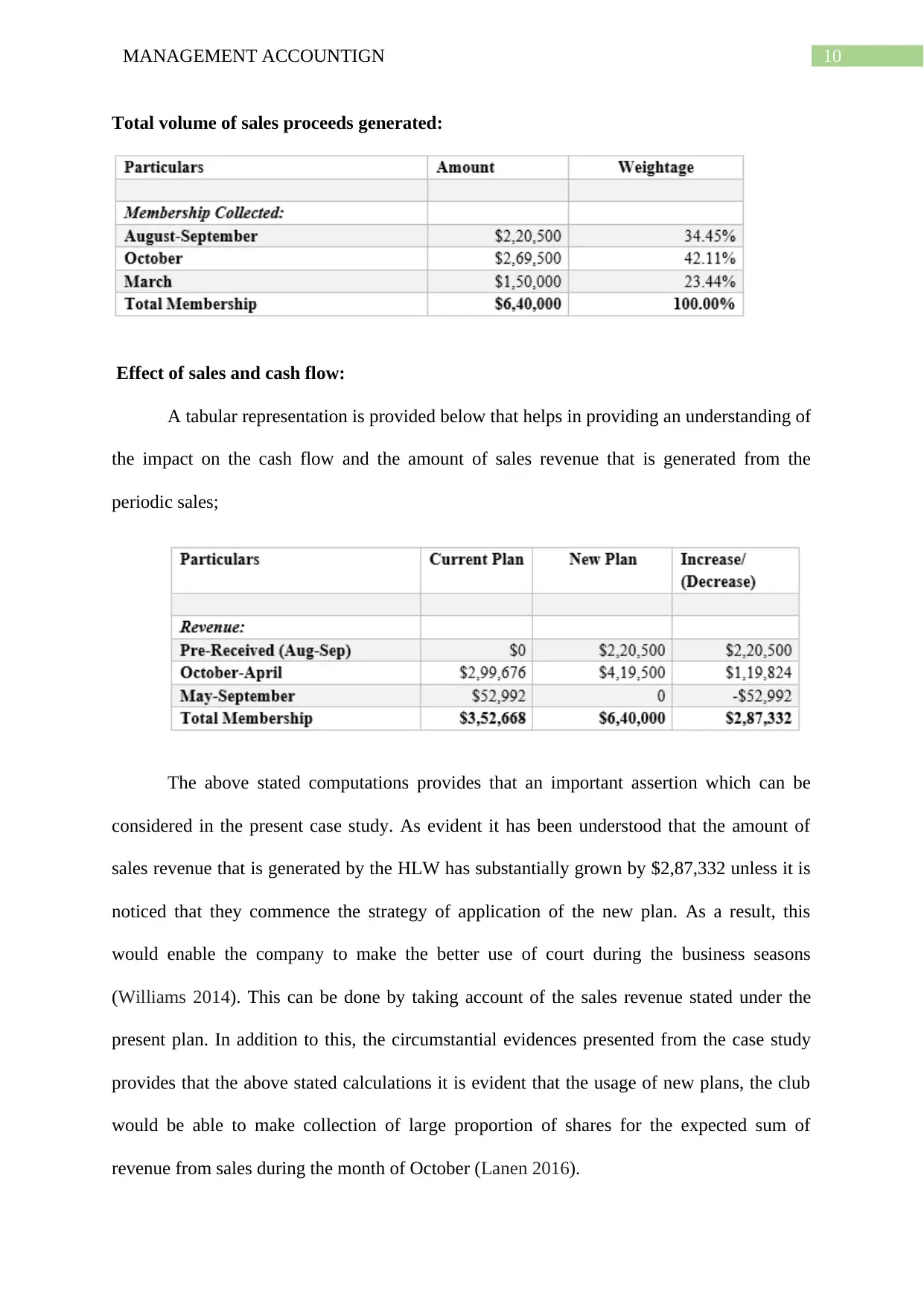

Total volume of sales proceeds generated:..............................................................................10

Effect of sales and cash flow:...................................................................................................10

Answer to requirement 3:.........................................................................................................11

Conclusion:..............................................................................................................................12

Reference List:.........................................................................................................................13

Table of Contents

Assessment task part A:.............................................................................................................4

Answer to requirement 1:...........................................................................................................4

Answer to requirement B:..........................................................................................................4

Answer to question C:................................................................................................................5

Assessment Task Part B:............................................................................................................6

Answer to requirement A:..........................................................................................................6

Answer to requirement 2:...........................................................................................................7

Revenue generated under the current plan:................................................................................8

Yearly Membership Revenue:....................................................................................................8

Total amount of Court Fees:......................................................................................................8

Total volume of Sales revenue derived:.....................................................................................9

Sales generated under the new plans of membership:...............................................................9

Revenue derived from the previous membership:.....................................................................9

Revenue generated from the usual membership:.......................................................................9

Total volume of sales proceeds generated:..............................................................................10

Effect of sales and cash flow:...................................................................................................10

Answer to requirement 3:.........................................................................................................11

Conclusion:..............................................................................................................................12

Reference List:.........................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTIGN

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTIGN

Assessment task part A:

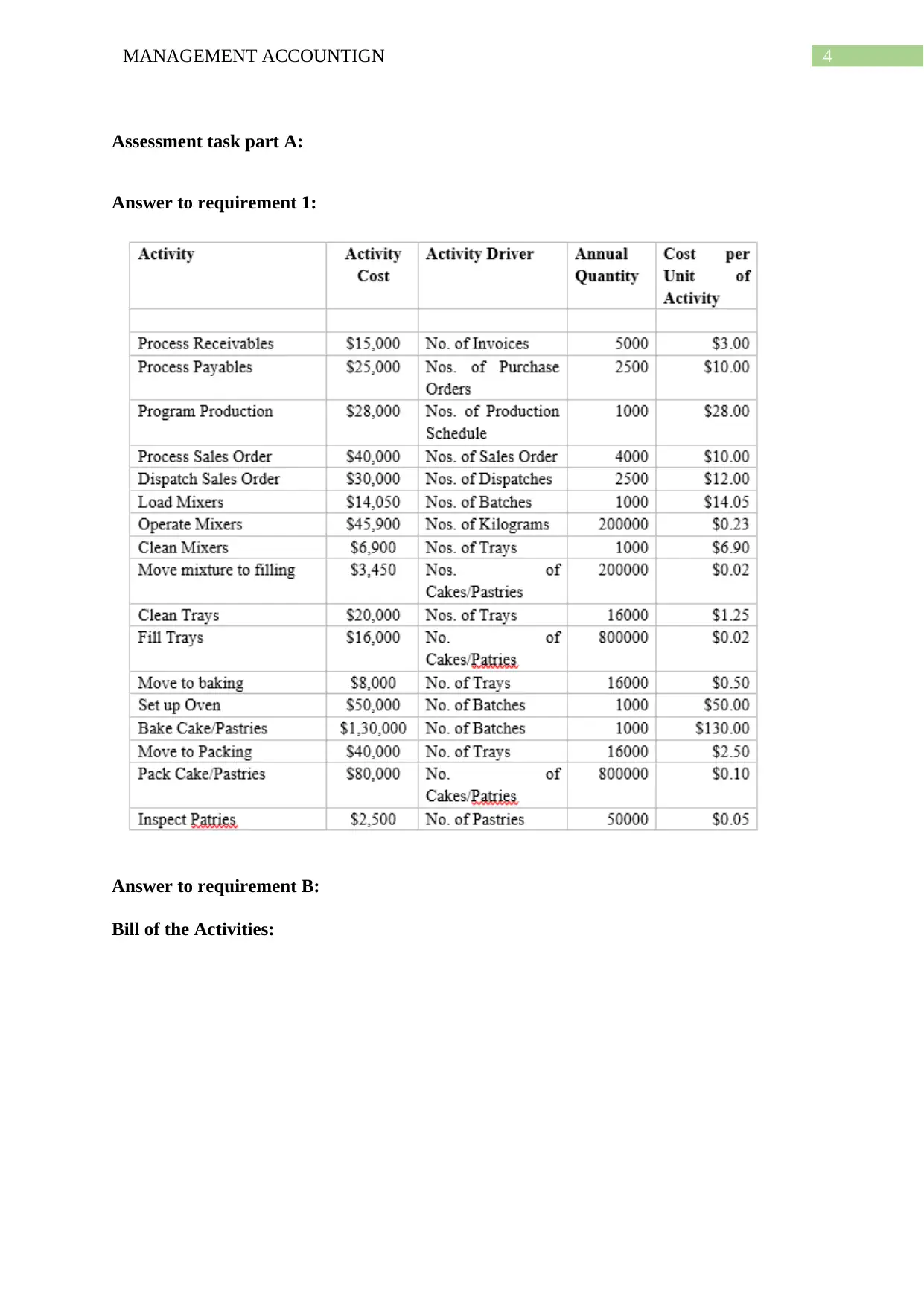

Answer to requirement 1:

Answer to requirement B:

Bill of the Activities:

Assessment task part A:

Answer to requirement 1:

Answer to requirement B:

Bill of the Activities:

5MANAGEMENT ACCOUNTIGN

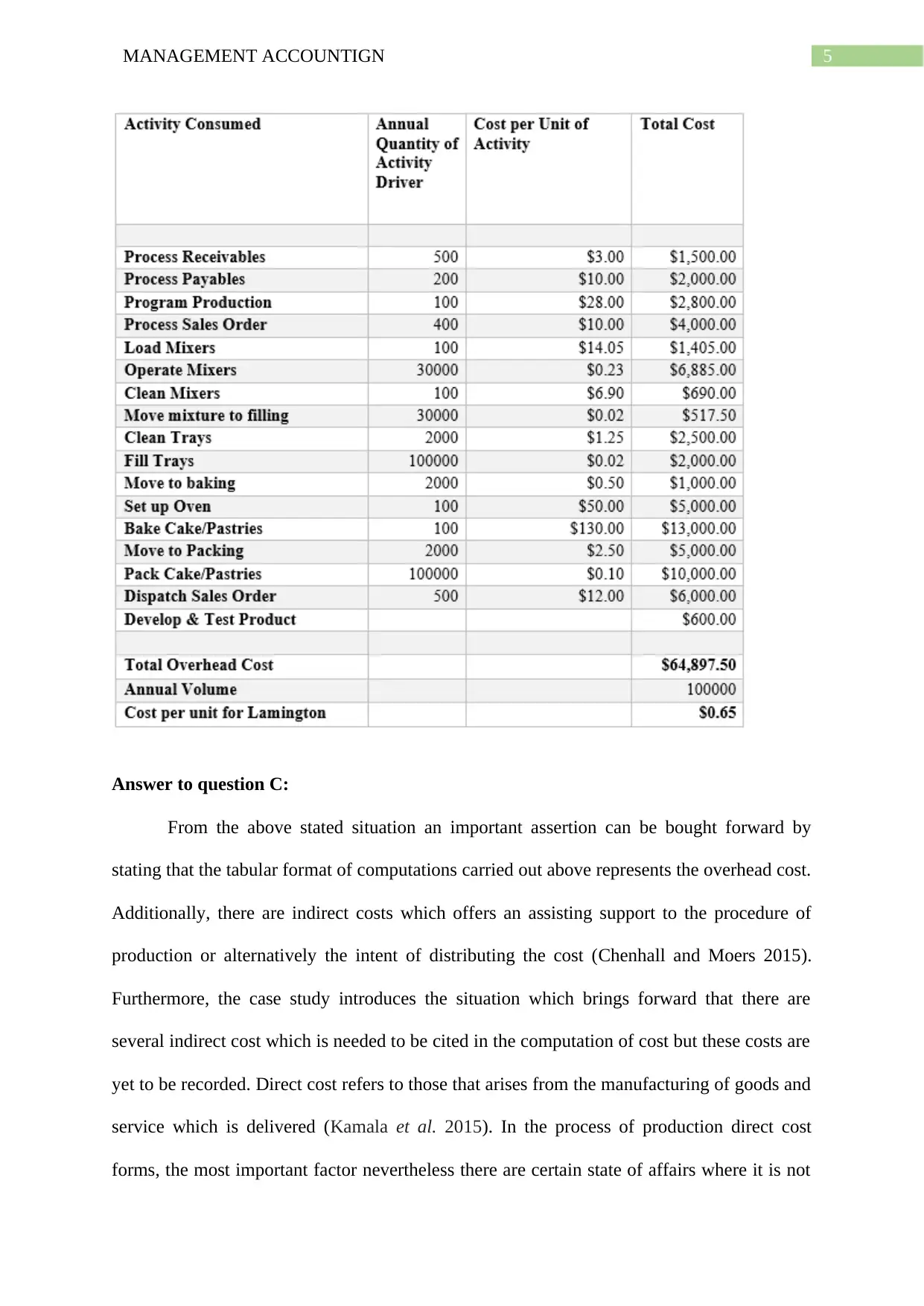

Answer to question C:

From the above stated situation an important assertion can be bought forward by

stating that the tabular format of computations carried out above represents the overhead cost.

Additionally, there are indirect costs which offers an assisting support to the procedure of

production or alternatively the intent of distributing the cost (Chenhall and Moers 2015).

Furthermore, the case study introduces the situation which brings forward that there are

several indirect cost which is needed to be cited in the computation of cost but these costs are

yet to be recorded. Direct cost refers to those that arises from the manufacturing of goods and

service which is delivered (Kamala et al. 2015). In the process of production direct cost

forms, the most important factor nevertheless there are certain state of affairs where it is not

Answer to question C:

From the above stated situation an important assertion can be bought forward by

stating that the tabular format of computations carried out above represents the overhead cost.

Additionally, there are indirect costs which offers an assisting support to the procedure of

production or alternatively the intent of distributing the cost (Chenhall and Moers 2015).

Furthermore, the case study introduces the situation which brings forward that there are

several indirect cost which is needed to be cited in the computation of cost but these costs are

yet to be recorded. Direct cost refers to those that arises from the manufacturing of goods and

service which is delivered (Kamala et al. 2015). In the process of production direct cost

forms, the most important factor nevertheless there are certain state of affairs where it is not

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTIGN

possible to manufacture goods without incurring any form of related costs (Fullerton,

Kennedy and Widener 2014). It is noteworthy to denote that to determine the cost of

Lamington, an important consideration must be paid to take into the considerations the direct

cost that is associated with the products which is provided below;

a. Direct cost associated with the labour

b. Charges associated with the freight inward

c. Direct costs associated with the materials

Assessment Task Part B:

Answer to requirement A:

The case study evidently puts forward that the HLW has derived revenue from

namely two forms of different sources. These sources are revenue that is generated from the

annual membership and the revenue from the court in the form of fees (Lavia López and

Hiebl 2014). Consequently, it is noticed that greater than 40% percent of the total sum of

revenue is generated from the annual membership for the sum of two months. By considering

the left over part the revenue that is generated from the court fees is in terms of the annual

basis. Along with this the flow of money from the fees derived from court is not even for

every month. At the time when the business hits the peak form it is evidently found that the

flow of cash from the court fees is higher during that time and the revenue is greater than

45% of the total amount of revenue (Kotas 2014). On the other hand, during the months of

May to September an evidence has been noticed that the fees that is collected from the court

is less and only cover approximately 15% of the total sum of sales proceeds.

As evident from the HLW application of the new membership plan, it is necessary to

assemble about 80% of the total amount of sales revenue within the span of first month of

accounting year. (Hopper and Bui 2016) In addition to this, HLW will be capable of

possible to manufacture goods without incurring any form of related costs (Fullerton,

Kennedy and Widener 2014). It is noteworthy to denote that to determine the cost of

Lamington, an important consideration must be paid to take into the considerations the direct

cost that is associated with the products which is provided below;

a. Direct cost associated with the labour

b. Charges associated with the freight inward

c. Direct costs associated with the materials

Assessment Task Part B:

Answer to requirement A:

The case study evidently puts forward that the HLW has derived revenue from

namely two forms of different sources. These sources are revenue that is generated from the

annual membership and the revenue from the court in the form of fees (Lavia López and

Hiebl 2014). Consequently, it is noticed that greater than 40% percent of the total sum of

revenue is generated from the annual membership for the sum of two months. By considering

the left over part the revenue that is generated from the court fees is in terms of the annual

basis. Along with this the flow of money from the fees derived from court is not even for

every month. At the time when the business hits the peak form it is evidently found that the

flow of cash from the court fees is higher during that time and the revenue is greater than

45% of the total amount of revenue (Kotas 2014). On the other hand, during the months of

May to September an evidence has been noticed that the fees that is collected from the court

is less and only cover approximately 15% of the total sum of sales proceeds.

As evident from the HLW application of the new membership plan, it is necessary to

assemble about 80% of the total amount of sales revenue within the span of first month of

accounting year. (Hopper and Bui 2016) In addition to this, HLW will be capable of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTIGN

obtaining several benefits that is listed below the until the application of new plan is

implemented by HLW;

a. On the application of the new plan HLW would be in the position of gaining the

advantage of unhindered volume of cash flow from the functional sources from the

annual membership (Stede 2016). As evident from the current plan, the club would be

under obligation of remaining reliant on the individual program namely the hourly

charges that is derived by the court for deriving greater 50% of total amount of

revenue.

b. On implementing the new plan HLW would be able to gain benefit as this would

facilitate a platform which would enable the club in generating the steady amount of

cash flow for every month (Hald and Thrane 2016).

c. With the application of the new plan, HLW will be in the beneficial position because

the supervisor of the club will be in the position of gaining more than 80% of the total

amount of revenue in the early period of three months in compliance with the new

cash flow strategies rather than waiting for the completion of six months (Bromwich

and Scapens 2016). Therefore, such kind of benefit would help HLW in preparing the

appropriate use of the assembled funds by considering the several different forms of

decisions as and when necessary.

Answer to requirement 2:

The case study evidently puts forward by stating that there are several such issues

which is emphasized and consequently there are specific number of assumptions that is

necessarily required to be undertaken in getting the understanding of the effect of new

membership plans to increase sales (Shields 2015). There are certain stated assumptions that

can be made;

obtaining several benefits that is listed below the until the application of new plan is

implemented by HLW;

a. On the application of the new plan HLW would be in the position of gaining the

advantage of unhindered volume of cash flow from the functional sources from the

annual membership (Stede 2016). As evident from the current plan, the club would be

under obligation of remaining reliant on the individual program namely the hourly

charges that is derived by the court for deriving greater 50% of total amount of

revenue.

b. On implementing the new plan HLW would be able to gain benefit as this would

facilitate a platform which would enable the club in generating the steady amount of

cash flow for every month (Hald and Thrane 2016).

c. With the application of the new plan, HLW will be in the beneficial position because

the supervisor of the club will be in the position of gaining more than 80% of the total

amount of revenue in the early period of three months in compliance with the new

cash flow strategies rather than waiting for the completion of six months (Bromwich

and Scapens 2016). Therefore, such kind of benefit would help HLW in preparing the

appropriate use of the assembled funds by considering the several different forms of

decisions as and when necessary.

Answer to requirement 2:

The case study evidently puts forward by stating that there are several such issues

which is emphasized and consequently there are specific number of assumptions that is

necessarily required to be undertaken in getting the understanding of the effect of new

membership plans to increase sales (Shields 2015). There are certain stated assumptions that

can be made;

8MANAGEMENT ACCOUNTIGN

a. It is necessary to make 100% use of court when the business is hitting the peak time

b. Around 60% of the total use of the capacity should be made during the non-peak time

c. It is estimated that around 40% of the use of court should be made when the business

hits the lean time (Marshall 2016).

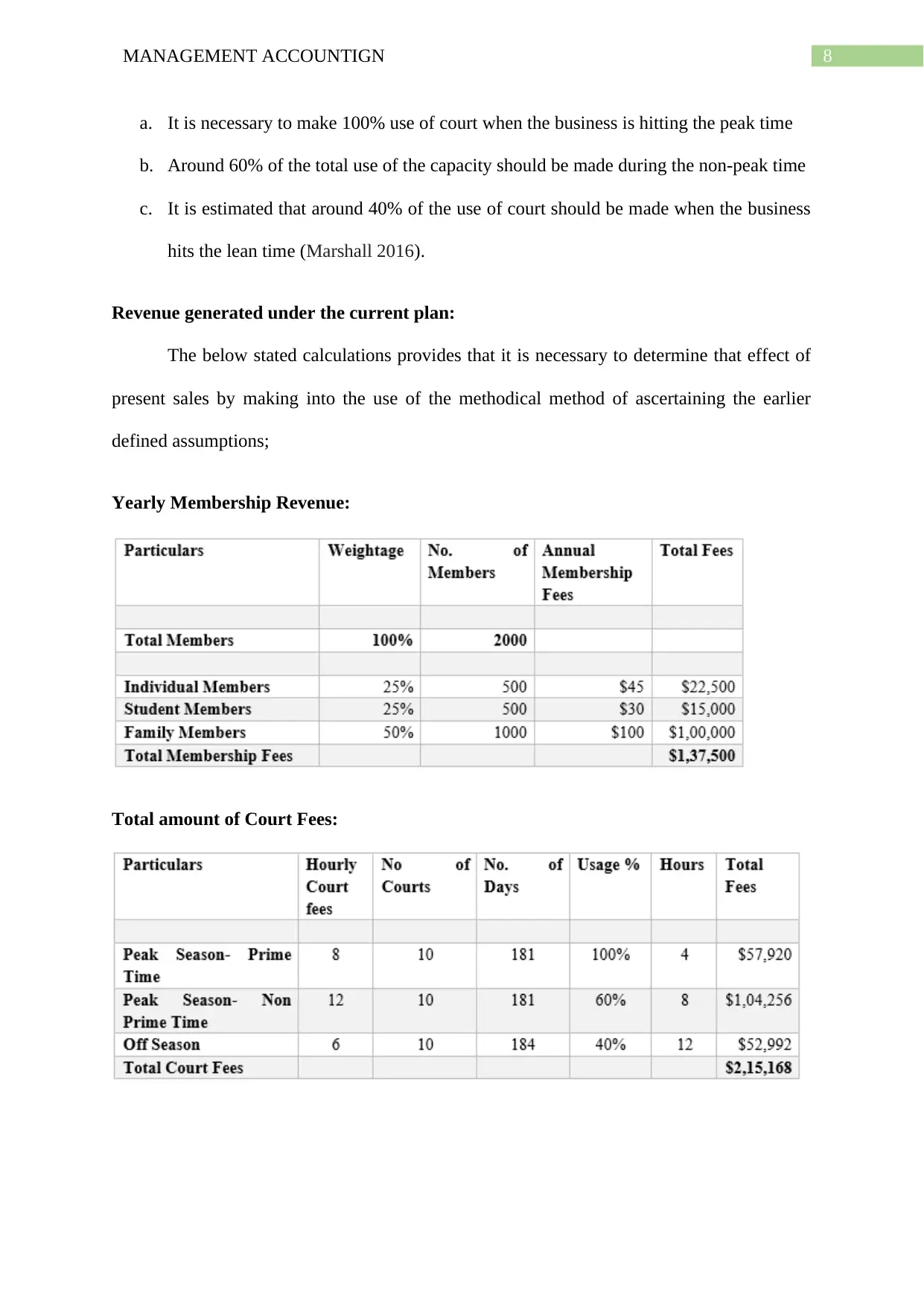

Revenue generated under the current plan:

The below stated calculations provides that it is necessary to determine that effect of

present sales by making into the use of the methodical method of ascertaining the earlier

defined assumptions;

Yearly Membership Revenue:

Total amount of Court Fees:

a. It is necessary to make 100% use of court when the business is hitting the peak time

b. Around 60% of the total use of the capacity should be made during the non-peak time

c. It is estimated that around 40% of the use of court should be made when the business

hits the lean time (Marshall 2016).

Revenue generated under the current plan:

The below stated calculations provides that it is necessary to determine that effect of

present sales by making into the use of the methodical method of ascertaining the earlier

defined assumptions;

Yearly Membership Revenue:

Total amount of Court Fees:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTIGN

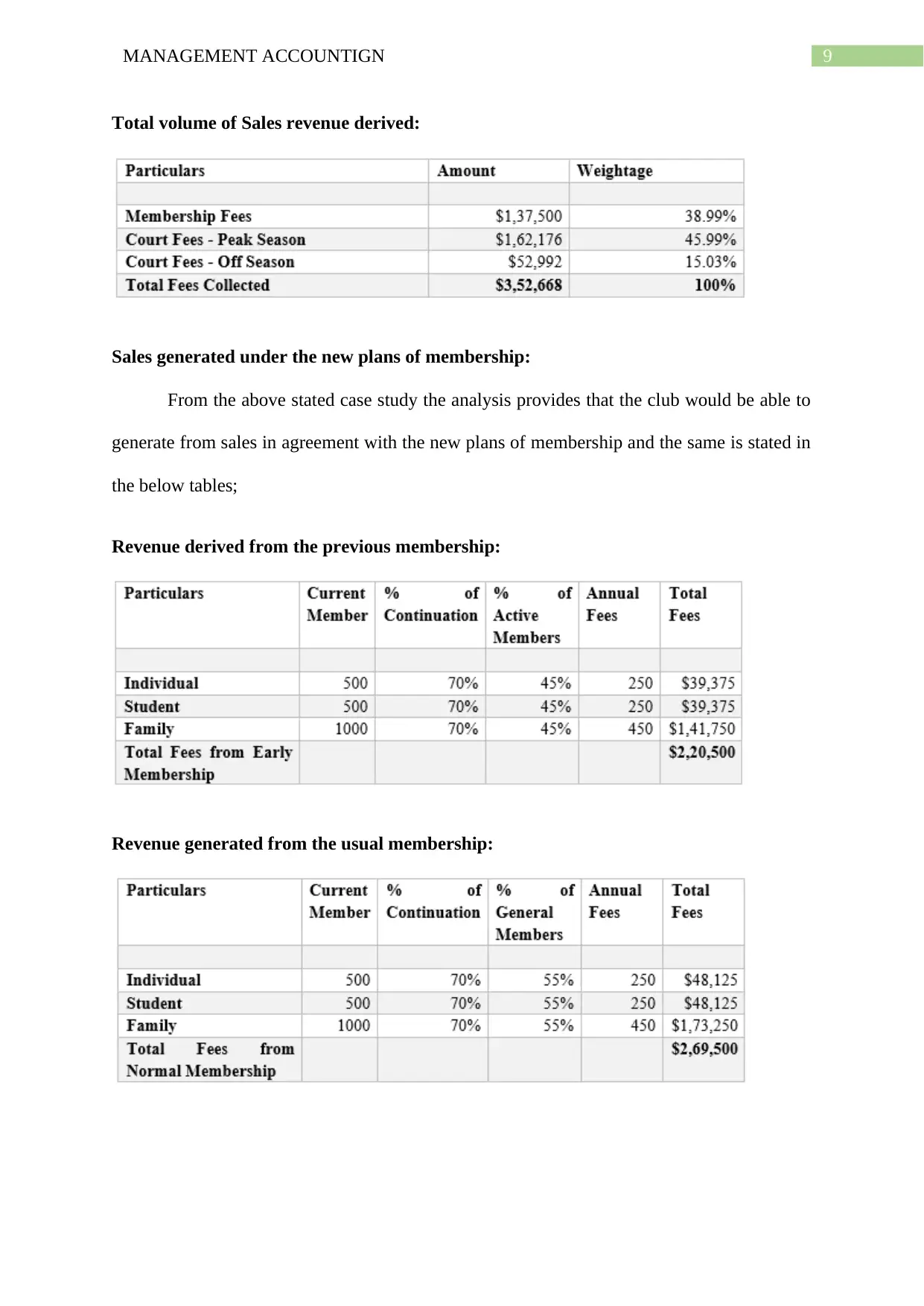

Total volume of Sales revenue derived:

Sales generated under the new plans of membership:

From the above stated case study the analysis provides that the club would be able to

generate from sales in agreement with the new plans of membership and the same is stated in

the below tables;

Revenue derived from the previous membership:

Revenue generated from the usual membership:

Total volume of Sales revenue derived:

Sales generated under the new plans of membership:

From the above stated case study the analysis provides that the club would be able to

generate from sales in agreement with the new plans of membership and the same is stated in

the below tables;

Revenue derived from the previous membership:

Revenue generated from the usual membership:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTIGN

Total volume of sales proceeds generated:

Effect of sales and cash flow:

A tabular representation is provided below that helps in providing an understanding of

the impact on the cash flow and the amount of sales revenue that is generated from the

periodic sales;

The above stated computations provides that an important assertion which can be

considered in the present case study. As evident it has been understood that the amount of

sales revenue that is generated by the HLW has substantially grown by $2,87,332 unless it is

noticed that they commence the strategy of application of the new plan. As a result, this

would enable the company to make the better use of court during the business seasons

(Williams 2014). This can be done by taking account of the sales revenue stated under the

present plan. In addition to this, the circumstantial evidences presented from the case study

provides that the above stated calculations it is evident that the usage of new plans, the club

would be able to make collection of large proportion of shares for the expected sum of

revenue from sales during the month of October (Lanen 2016).

Total volume of sales proceeds generated:

Effect of sales and cash flow:

A tabular representation is provided below that helps in providing an understanding of

the impact on the cash flow and the amount of sales revenue that is generated from the

periodic sales;

The above stated computations provides that an important assertion which can be

considered in the present case study. As evident it has been understood that the amount of

sales revenue that is generated by the HLW has substantially grown by $2,87,332 unless it is

noticed that they commence the strategy of application of the new plan. As a result, this

would enable the company to make the better use of court during the business seasons

(Williams 2014). This can be done by taking account of the sales revenue stated under the

present plan. In addition to this, the circumstantial evidences presented from the case study

provides that the above stated calculations it is evident that the usage of new plans, the club

would be able to make collection of large proportion of shares for the expected sum of

revenue from sales during the month of October (Lanen 2016).

11MANAGEMENT ACCOUNTIGN

Answer to requirement 3:

As evident from the above stated case study the revenue that is generated from the

case study represents that it is greater in regard to the plans that is made in the previous

instances. This primary reason behind this is that a large amount of factors is necessarily

required to be considered when decisions are made in the implementation of the new plan

(Lorenz 2015). Certain important factors are taken into the considerations on implementing

the below listed assumptions,

a. The analysis provides that the fees that is generated from the membership would

increase from the application of the new plan since an improved structure of fees is

better than the previous structure of fees. As a result of this, it is expected that there

may an instances of loss of members after the implementation of the new plan of

membership (Chenhall and Moers 2015). Additionally, it is has been found that there

are certain students that are not reliant in respect of the finance and may not be able to

afford greater charges of fees together with the renewal of the annual membership

plans relating to the new structure of fees. In addition to this, after assessing the result

of the consequence, it becomes vital to assess the feedback that is derived from the

members.

b. On implementing the new plans, the administration would be able to make the

collection of overall fees for the beginning period of three months (Velasquez,

Suomala and Järvenpää 2015). With the help of this procedure the management would

be able to reduce the cost of assembling the sales revenue generated from the court

fees together with the planning of the periodic accounting records for the amount of

revenue derived. Therefore, it becomes necessary to take account of the cost

reductions strategies at the time of assessment.

Answer to requirement 3:

As evident from the above stated case study the revenue that is generated from the

case study represents that it is greater in regard to the plans that is made in the previous

instances. This primary reason behind this is that a large amount of factors is necessarily

required to be considered when decisions are made in the implementation of the new plan

(Lorenz 2015). Certain important factors are taken into the considerations on implementing

the below listed assumptions,

a. The analysis provides that the fees that is generated from the membership would

increase from the application of the new plan since an improved structure of fees is

better than the previous structure of fees. As a result of this, it is expected that there

may an instances of loss of members after the implementation of the new plan of

membership (Chenhall and Moers 2015). Additionally, it is has been found that there

are certain students that are not reliant in respect of the finance and may not be able to

afford greater charges of fees together with the renewal of the annual membership

plans relating to the new structure of fees. In addition to this, after assessing the result

of the consequence, it becomes vital to assess the feedback that is derived from the

members.

b. On implementing the new plans, the administration would be able to make the

collection of overall fees for the beginning period of three months (Velasquez,

Suomala and Järvenpää 2015). With the help of this procedure the management would

be able to reduce the cost of assembling the sales revenue generated from the court

fees together with the planning of the periodic accounting records for the amount of

revenue derived. Therefore, it becomes necessary to take account of the cost

reductions strategies at the time of assessment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

12MANAGEMENT ACCOUNTIGN

c. Within the span of six months, the administration expects that the would lose some

members (Otley 2016). The management is under the obligation of implementing the

new plans or else they would fail to attain the expected volume of revenue.

d. An important assertion regarding the club can be bought forward by stating that the

club is under obligation of performing the special campaign as this will enable the

club in promoting the new plans (Cooper 2017). In addition to this, the cost that

would be incurred at the time of promotion campaigns must be taken into the account

at the time of computing the net income together with the cash flow derived from the

implementation of the new plans.

Conclusion:

On arriving at the concluding note, the case study provides an explanatory situation

that the activity based costing is regarded as the most beneficial method of costing. There are

several forms of business information that is needed in the execution of the business activities

and the same should be considered at the time of determining the cost of product. A

circumstantial evidences suggest from the case study that adequate business information has

been complied in determining the cost of every activity. Furthermore, the activity based cost

is referred as the business cost that usually take account of both the ill effects and good

effects of the cost that is incurred by the business. An important consideration in this regard

is that the activity based costing is easy to understand and implement to ascertain the current

cost incurred by the business. On a considerable note, the study evidently provides that

activity based costing is regarded as the beneficial mode of costing because it helps the

management in making informed and correct decisions.

c. Within the span of six months, the administration expects that the would lose some

members (Otley 2016). The management is under the obligation of implementing the

new plans or else they would fail to attain the expected volume of revenue.

d. An important assertion regarding the club can be bought forward by stating that the

club is under obligation of performing the special campaign as this will enable the

club in promoting the new plans (Cooper 2017). In addition to this, the cost that

would be incurred at the time of promotion campaigns must be taken into the account

at the time of computing the net income together with the cash flow derived from the

implementation of the new plans.

Conclusion:

On arriving at the concluding note, the case study provides an explanatory situation

that the activity based costing is regarded as the most beneficial method of costing. There are

several forms of business information that is needed in the execution of the business activities

and the same should be considered at the time of determining the cost of product. A

circumstantial evidences suggest from the case study that adequate business information has

been complied in determining the cost of every activity. Furthermore, the activity based cost

is referred as the business cost that usually take account of both the ill effects and good

effects of the cost that is incurred by the business. An important consideration in this regard

is that the activity based costing is easy to understand and implement to ascertain the current

cost incurred by the business. On a considerable note, the study evidently provides that

activity based costing is regarded as the beneficial mode of costing because it helps the

management in making informed and correct decisions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13MANAGEMENT ACCOUNTIGN

Reference List:

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research, 31, pp.1-9.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society, 47, pp.1-13.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society, 47, pp.1-13.

Cooper, R., 2017. Supply chain development for the lean enterprise: interorganizational cost

management. Routledge.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7), pp.414-428.

Hald, K.S. and Thrane, S., 2016. Management Accounting and Supply Chain Strategy. In 1st

International Competitiveness Management Conference.

Hopper, T. and Bui, B., 2016. Has management accounting research been

critical?. Management Accounting Research, 31, pp.10-30.

Kamala, P., Struwig, J., Bornman, M., Boersman, R., Vermaak, M., McGill, M., Jordaan-

Marais, J., Matthew, J., Hurter, C. and Taylor, P., 2015. Principles of Cost Accounting. OUP

Catalogue.

Kotas, R., 2014. Management accounting for hotels and restaurants. Routledge.

Reference List:

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research, 31, pp.1-9.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society, 47, pp.1-13.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society, 47, pp.1-13.

Cooper, R., 2017. Supply chain development for the lean enterprise: interorganizational cost

management. Routledge.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7), pp.414-428.

Hald, K.S. and Thrane, S., 2016. Management Accounting and Supply Chain Strategy. In 1st

International Competitiveness Management Conference.

Hopper, T. and Bui, B., 2016. Has management accounting research been

critical?. Management Accounting Research, 31, pp.10-30.

Kamala, P., Struwig, J., Bornman, M., Boersman, R., Vermaak, M., McGill, M., Jordaan-

Marais, J., Matthew, J., Hurter, C. and Taylor, P., 2015. Principles of Cost Accounting. OUP

Catalogue.

Kotas, R., 2014. Management accounting for hotels and restaurants. Routledge.

14MANAGEMENT ACCOUNTIGN

Lanen, W., 2016. Fundamentals of cost accounting. McGraw-Hill Higher Education.

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and medium-sized

enterprises: current knowledge and avenues for further research. Journal of Management

Accounting Research, 27(1), pp.81-119.

Lorenz, A., 2015. Contemporary management accounting in the UK service sector (Doctoral

dissertation, University of Gloucestershire).

Marshall, D., 2016. Accounting: What the numbers mean. McGraw-Hill Higher Education.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

Shields, M.D., 2015. Established management accounting knowledge. Journal of

Management Accounting Research, 27(1), pp.123-132.

Van der Stede, W.A., 2016. Management accounting in context: Industry, regulation and

informatics. Management Accounting Research, 31, pp.100-102.

Velasquez, S., Suomala, P. and Järvenpää, M., 2015. Cost consciousness: conceptual

development from a management accounting perspective. Qualitative Research in

Accounting & Management, 12(1), pp.55-86.

Williams, J., 2014. Financial accounting. McGraw-Hill Higher Education.

Lanen, W., 2016. Fundamentals of cost accounting. McGraw-Hill Higher Education.

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and medium-sized

enterprises: current knowledge and avenues for further research. Journal of Management

Accounting Research, 27(1), pp.81-119.

Lorenz, A., 2015. Contemporary management accounting in the UK service sector (Doctoral

dissertation, University of Gloucestershire).

Marshall, D., 2016. Accounting: What the numbers mean. McGraw-Hill Higher Education.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, pp.45-62.

Shields, M.D., 2015. Established management accounting knowledge. Journal of

Management Accounting Research, 27(1), pp.123-132.

Van der Stede, W.A., 2016. Management accounting in context: Industry, regulation and

informatics. Management Accounting Research, 31, pp.100-102.

Velasquez, S., Suomala, P. and Järvenpää, M., 2015. Cost consciousness: conceptual

development from a management accounting perspective. Qualitative Research in

Accounting & Management, 12(1), pp.55-86.

Williams, J., 2014. Financial accounting. McGraw-Hill Higher Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.