Management accounting and its different types

VerifiedAdded on 2021/01/02

|14

|4809

|67

AI Summary

This system is more relevant to manage operations of Ever joy Enterprises.2 P2 Methods for management accounting Reporting 2 TASK 24 P3 Cost calculations to prepare an income statement4 TASK 36 P4 Advantages and disadvantages of different types of planning tools for budgetary control6 TASK 49 P5 Comparison on how organizations are adapting management accounting system to resolve financial problems 9 CONCLUSION 11 REFERENCES 12 INTRODUCTION Management accounting is being defined as a process which aids in developing a number financial of reports

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its different types....................................................................1

Job costing system: Job costing system is useful tool for the appropriation of various costs in

respect to a specific job or project. This system is more relevant to manage operations of Ever

joy Enterprises. ...........................................................................................................................2

P2 Methods for management accounting Reporting...................................................................2

TASK 2............................................................................................................................................4

P3 Cost calculations to prepare an income statement.................................................................4

TASK 3............................................................................................................................................6

P4 Advantages and disadvantages of different types of planning tools for budgetary control...6

TASK 4............................................................................................................................................9

P5 Comparison on how organizations are adapting management accounting system to resolve

financial problems.......................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its different types....................................................................1

Job costing system: Job costing system is useful tool for the appropriation of various costs in

respect to a specific job or project. This system is more relevant to manage operations of Ever

joy Enterprises. ...........................................................................................................................2

P2 Methods for management accounting Reporting...................................................................2

TASK 2............................................................................................................................................4

P3 Cost calculations to prepare an income statement.................................................................4

TASK 3............................................................................................................................................6

P4 Advantages and disadvantages of different types of planning tools for budgetary control...6

TASK 4............................................................................................................................................9

P5 Comparison on how organizations are adapting management accounting system to resolve

financial problems.......................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting is being defined as a process which aids in developing a number

financial of reports and helps in managing the accounts of a business organisation. Considering

this procedure as an important part can help a company in managing its business operations,

finance, expenses and can also monitor performance as well (Kokubu and Tachikawa, 2013). In

this project, firm which has been taken to understand the concept of management accounting, i.e.

Delloite which is multinational audit advisory and service providing firm. “Ever Joy Enterprises”

that is a client of this firm to manage its management accounting department. Company is

dealing in United Kingdom in leisure and entertainment industry.

Assignment will focus on number of areas difference between management and financial

accounting, cost accounting systems, inventory management systems, job costing systems that will

help in understanding different concepts of management accounting. Away with this, it will also

focus on budgetary control. Lastly, adopting right management accounting systems, number of

financial problems are going to be resolved in specific time frame.

TASK 1

P1 Management accounting and its different types

Management accounting is being defined as the process of formulating accounts that

provides accurate and timely financial and statistical information needed for make both long and

short term determinations. On the other hand, financial accounting can be understood as an

activity which includes recording, summarizing and reporting a number of proceedings or

transactions that has been done in a business organisation for a certain time frame.

There are a number of differences between management accounting and financial

accounting. First difference which was pulled out is that financial account contains aggregation

related to account data which then develops statements related to finance (Burritt, Schaltegger

and Zvezdov, 2011). Away with this, management accounting is totally different from financial

one because it majorly communicate whole internal process which is used while developing

accounts for a business proceeding. Another difference which has been formulated is that

financial accounting shows profitability of a business firm and managerial accounting contains a

number of solutions for a problem which has been specifically found in a business company.

1

Management accounting is being defined as a process which aids in developing a number

financial of reports and helps in managing the accounts of a business organisation. Considering

this procedure as an important part can help a company in managing its business operations,

finance, expenses and can also monitor performance as well (Kokubu and Tachikawa, 2013). In

this project, firm which has been taken to understand the concept of management accounting, i.e.

Delloite which is multinational audit advisory and service providing firm. “Ever Joy Enterprises”

that is a client of this firm to manage its management accounting department. Company is

dealing in United Kingdom in leisure and entertainment industry.

Assignment will focus on number of areas difference between management and financial

accounting, cost accounting systems, inventory management systems, job costing systems that will

help in understanding different concepts of management accounting. Away with this, it will also

focus on budgetary control. Lastly, adopting right management accounting systems, number of

financial problems are going to be resolved in specific time frame.

TASK 1

P1 Management accounting and its different types

Management accounting is being defined as the process of formulating accounts that

provides accurate and timely financial and statistical information needed for make both long and

short term determinations. On the other hand, financial accounting can be understood as an

activity which includes recording, summarizing and reporting a number of proceedings or

transactions that has been done in a business organisation for a certain time frame.

There are a number of differences between management accounting and financial

accounting. First difference which was pulled out is that financial account contains aggregation

related to account data which then develops statements related to finance (Burritt, Schaltegger

and Zvezdov, 2011). Away with this, management accounting is totally different from financial

one because it majorly communicate whole internal process which is used while developing

accounts for a business proceeding. Another difference which has been formulated is that

financial accounting shows profitability of a business firm and managerial accounting contains a

number of solutions for a problem which has been specifically found in a business company.

1

Cost accounting system

It is being considered as a framework which is majorly used by companies through which

estimation of cost related to products can be improved with the help of profitability investigation

and cost control analysis. It is being found that, estimation related to accurate cost is critical in

nature (Van Dooren, Bouckaert and Halligan, 2015). Cost in management accounting refers to

the costs associated with production or manufacturing of goods and with the help of this per unit

cost can be calculated.

Direct Cost: A direct cost is a price that can be completely attributed to the production of

specific goods or services. A direct cost for Ever Joy can be a variable cost if it is inconsistent

and often fluctuates in amount. Examples of direct costs are freight, commissions etc.

Standard Cost: This costing method is used to compare the standard costs and revenues with

the actual results in Ever Joy, in order determine difference along with its causes as well as to

inform the management about the deviations and take corrective measures for improvement. For

instances, labour, material and overhead costs.

Inventory: Inventory is an accounting term that refers to goods on their various stages from raw

material to finished goods. Inventory at Ever Joy is generally its current asset that is expected for

sale within next year.

Inventory Management System: It is the combination of techniques and processes that

monitor and maintain the stocks of products, and determine the amount of finished goods, raw

material and work in progress. To manage this system at Ever Joy, the company can assemble a

team for it, which will have specific objectives. The team will frame a inventory process and

action plan to implement after integrating it all related systems. After developing a plan, it can be

implemented and reviewed if needed (Lay and Jusoh, 2012). Ever Joy Enterprises uses EOQ

approach for inventory management. According to this approach, it helps in maintaining optimal

level of inventory and at this level acquisition costs as well as carrying cost is minimum.

Job costing system: Job costing system is useful tool for the appropriation of various costs in

respect to a specific job or project. This system is more relevant to manage operations of Ever

joy Enterprises.

P2 Methods for management accounting Reporting

Different methods of management accounting reporting are as:

2

It is being considered as a framework which is majorly used by companies through which

estimation of cost related to products can be improved with the help of profitability investigation

and cost control analysis. It is being found that, estimation related to accurate cost is critical in

nature (Van Dooren, Bouckaert and Halligan, 2015). Cost in management accounting refers to

the costs associated with production or manufacturing of goods and with the help of this per unit

cost can be calculated.

Direct Cost: A direct cost is a price that can be completely attributed to the production of

specific goods or services. A direct cost for Ever Joy can be a variable cost if it is inconsistent

and often fluctuates in amount. Examples of direct costs are freight, commissions etc.

Standard Cost: This costing method is used to compare the standard costs and revenues with

the actual results in Ever Joy, in order determine difference along with its causes as well as to

inform the management about the deviations and take corrective measures for improvement. For

instances, labour, material and overhead costs.

Inventory: Inventory is an accounting term that refers to goods on their various stages from raw

material to finished goods. Inventory at Ever Joy is generally its current asset that is expected for

sale within next year.

Inventory Management System: It is the combination of techniques and processes that

monitor and maintain the stocks of products, and determine the amount of finished goods, raw

material and work in progress. To manage this system at Ever Joy, the company can assemble a

team for it, which will have specific objectives. The team will frame a inventory process and

action plan to implement after integrating it all related systems. After developing a plan, it can be

implemented and reviewed if needed (Lay and Jusoh, 2012). Ever Joy Enterprises uses EOQ

approach for inventory management. According to this approach, it helps in maintaining optimal

level of inventory and at this level acquisition costs as well as carrying cost is minimum.

Job costing system: Job costing system is useful tool for the appropriation of various costs in

respect to a specific job or project. This system is more relevant to manage operations of Ever

joy Enterprises.

P2 Methods for management accounting Reporting

Different methods of management accounting reporting are as:

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Budget reporting: Preparing budget reports for Ever Joy Enterprise is very crucial to

analyse performance because budgets are generated for every department separately and also as a

whole. Budgets are based on past performance with this also these are also useful in forecasting

future and Ever Joy Enterprise can tackle its risk with the help of these reports. Process of budget

includes firstly note down all the incomes and expenses after that a sufficient amount is set to

accomplish objectives of Ever Joy Enterprise. These budget reports assists to mangers in providing

relevant incentives to employees, bargaining with suppliers and in optimum utilization of resources

available with Ever Joy Enterprise.

Accounts receivable reporting: These reports are important for the company who extends

credit to customers on a large basis (Schaltegger, Burritt and Petersen, 2017). Collection process of

Ever Joy Enterprise should be appropriate because it remain convenient to determine customers

who regularly delays in payment and who makes timely payment. If in situation of large number of

defaulters, Ever Joy Enterprise should strengthen their credit extending policies. So accounts

receivable reports will prove a better ways to manage resources of Ever Joy Enterprise.

Job cost reporting: Profitability is calculated with the help of these reports of a project or

job . As when expenses and revenues of a particular project is matched with the expenses relevant to

this job then Ever Joy Enterprise will be able to estimate profit. These are essential in the way that

Ever Joy Enterprise can identify key performance areas which are cost efficient and areas which are

less profitable so that wasting of resources can be prevented. Instead resources can be applied in

more profitable areas to enhance performance. Listing of cost incurred on every project which is

currently ongoing and costs on already completed jobs are mentioned to find variances to improve.

Performance reporting: These reports are made by managers for assessment of

performance of individual employee as well as for Ever Joy Enterprise as a whole. Also department

wise performance reports for Ever Joy Enterprise are prepared to take important decisions.

Strategies are ascertained on the basis of performance. With the help of these one can easily develop

areas of underperformance.

Inventory management reporting: Ever Joy Enterprise can use these inventory reports in

assisting its manufacturing or production process. These operations will go in a smooth way because

all the details of inventory items are included in these such as raw materials, work in progress, and

finished goods. Inventory holding costs of Ever Joy Enterprise can be minimized, along with this

comparison between different assembly lines will be easy.

3

analyse performance because budgets are generated for every department separately and also as a

whole. Budgets are based on past performance with this also these are also useful in forecasting

future and Ever Joy Enterprise can tackle its risk with the help of these reports. Process of budget

includes firstly note down all the incomes and expenses after that a sufficient amount is set to

accomplish objectives of Ever Joy Enterprise. These budget reports assists to mangers in providing

relevant incentives to employees, bargaining with suppliers and in optimum utilization of resources

available with Ever Joy Enterprise.

Accounts receivable reporting: These reports are important for the company who extends

credit to customers on a large basis (Schaltegger, Burritt and Petersen, 2017). Collection process of

Ever Joy Enterprise should be appropriate because it remain convenient to determine customers

who regularly delays in payment and who makes timely payment. If in situation of large number of

defaulters, Ever Joy Enterprise should strengthen their credit extending policies. So accounts

receivable reports will prove a better ways to manage resources of Ever Joy Enterprise.

Job cost reporting: Profitability is calculated with the help of these reports of a project or

job . As when expenses and revenues of a particular project is matched with the expenses relevant to

this job then Ever Joy Enterprise will be able to estimate profit. These are essential in the way that

Ever Joy Enterprise can identify key performance areas which are cost efficient and areas which are

less profitable so that wasting of resources can be prevented. Instead resources can be applied in

more profitable areas to enhance performance. Listing of cost incurred on every project which is

currently ongoing and costs on already completed jobs are mentioned to find variances to improve.

Performance reporting: These reports are made by managers for assessment of

performance of individual employee as well as for Ever Joy Enterprise as a whole. Also department

wise performance reports for Ever Joy Enterprise are prepared to take important decisions.

Strategies are ascertained on the basis of performance. With the help of these one can easily develop

areas of underperformance.

Inventory management reporting: Ever Joy Enterprise can use these inventory reports in

assisting its manufacturing or production process. These operations will go in a smooth way because

all the details of inventory items are included in these such as raw materials, work in progress, and

finished goods. Inventory holding costs of Ever Joy Enterprise can be minimized, along with this

comparison between different assembly lines will be easy.

3

Cost reporting: Cost reporting is done to product manufactured by Ever Joy Enterprise.

Cost reports are prepared for the entire process of production that is from purchasing raw materials

to delivering goods to ultimate consumer.

TASK 2

P3 Cost calculations to prepare an income statement

Cost

Cost is being considered as an amount which is majorly being paid by a company to

generate profitability. On the other hand, it has been analysed that not every single cost is being

considered as an expense. Away with this, it is being found that there are different types of costs

like fixed and variable costs. Here, fixed cost is being considered as the cost which majorly stays

fix in nature which are electricity, depreciation, rent etc. Along with this, variable cost such as

labour, packaging, raw material varies in every single production cycle (Gullkvist, 2013). If the

productive unit is high then it is being found that variable cost will stay high and if the

production unit cost will be low then the variable cost will also stay low as well. In present

context, two types of costing, marginal and absorption are used in dealing with fixed

manufacturing overheads. Both these are mentioned below:

Marginal cost:- Marginal cost can be defined as additional cost received occurs due to

change in production units. This type of cost majorly comes under variable one that carries cost

related to both labour and the raw material as well. While developing the reference manual for

Ever Joy Enterprise, marginal cost got enhanced because various variable expenses enhanced

due to increased manufacturing units. This can be understood with an example: at the time of

promoting goods, marginal cost of company increases and then at the time when consumers

starts purchasing the products, the same cost gets decreases which can help Ever Joy Enterprise

in doing business.

Absorption cost:- Absorption costing refers to those management cost of accounting

which relates with manufacturing of product and delivering services. It relates with both fixed

and variables costing of a commodity. It includes direct labour, direct raw materials, accurate

manufacturing cost. Adding all fixed cost together in respect to direct expenses because at many

situations when goods are unsold this costing method will not work. This technique includes

overhead cost, sometimes this could be disadvantage. In context to Ever Joy Enterprises, this

4

Cost reports are prepared for the entire process of production that is from purchasing raw materials

to delivering goods to ultimate consumer.

TASK 2

P3 Cost calculations to prepare an income statement

Cost

Cost is being considered as an amount which is majorly being paid by a company to

generate profitability. On the other hand, it has been analysed that not every single cost is being

considered as an expense. Away with this, it is being found that there are different types of costs

like fixed and variable costs. Here, fixed cost is being considered as the cost which majorly stays

fix in nature which are electricity, depreciation, rent etc. Along with this, variable cost such as

labour, packaging, raw material varies in every single production cycle (Gullkvist, 2013). If the

productive unit is high then it is being found that variable cost will stay high and if the

production unit cost will be low then the variable cost will also stay low as well. In present

context, two types of costing, marginal and absorption are used in dealing with fixed

manufacturing overheads. Both these are mentioned below:

Marginal cost:- Marginal cost can be defined as additional cost received occurs due to

change in production units. This type of cost majorly comes under variable one that carries cost

related to both labour and the raw material as well. While developing the reference manual for

Ever Joy Enterprise, marginal cost got enhanced because various variable expenses enhanced

due to increased manufacturing units. This can be understood with an example: at the time of

promoting goods, marginal cost of company increases and then at the time when consumers

starts purchasing the products, the same cost gets decreases which can help Ever Joy Enterprise

in doing business.

Absorption cost:- Absorption costing refers to those management cost of accounting

which relates with manufacturing of product and delivering services. It relates with both fixed

and variables costing of a commodity. It includes direct labour, direct raw materials, accurate

manufacturing cost. Adding all fixed cost together in respect to direct expenses because at many

situations when goods are unsold this costing method will not work. This technique includes

overhead cost, sometimes this could be disadvantage. In context to Ever Joy Enterprises, this

4

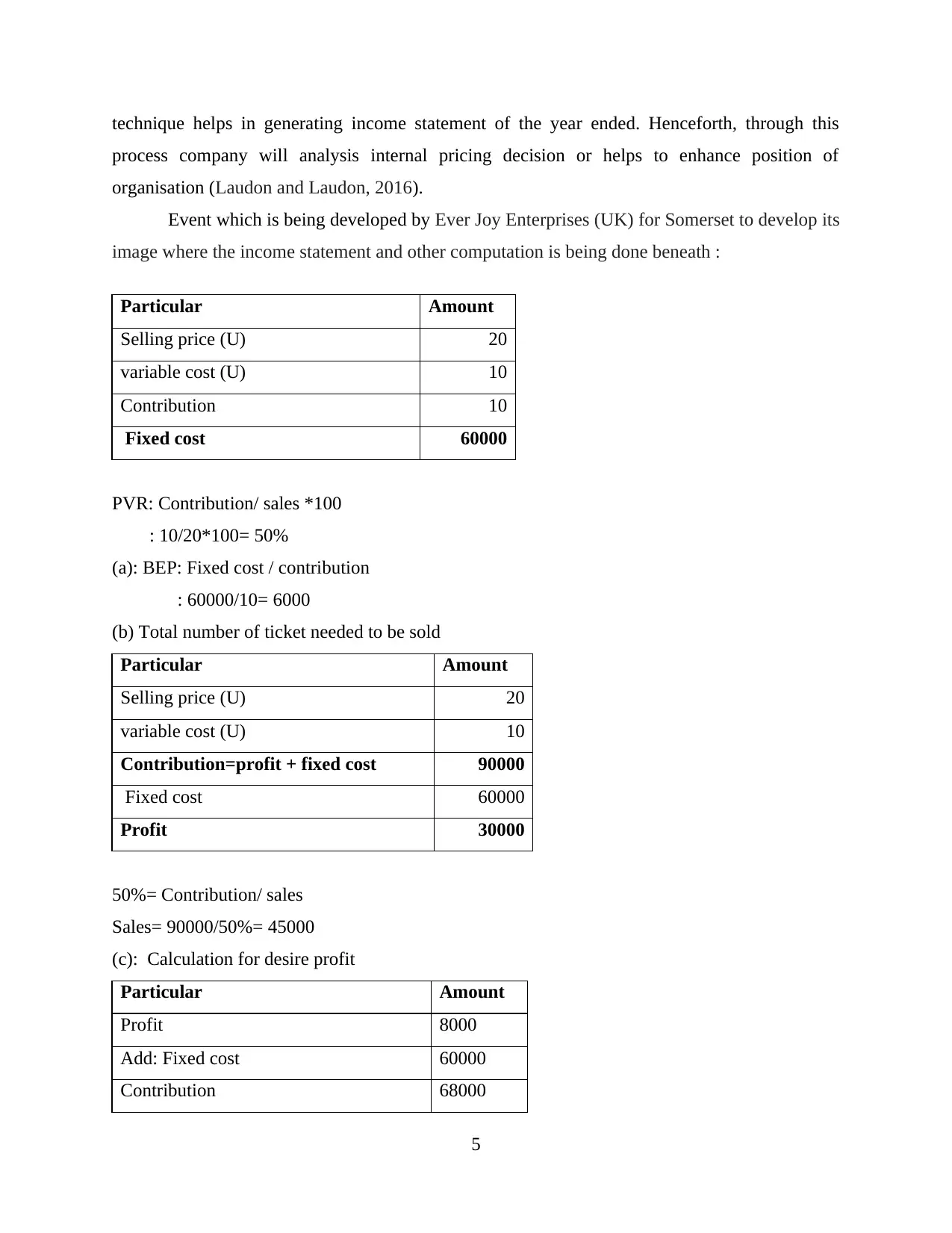

technique helps in generating income statement of the year ended. Henceforth, through this

process company will analysis internal pricing decision or helps to enhance position of

organisation (Laudon and Laudon, 2016).

Event which is being developed by Ever Joy Enterprises (UK) for Somerset to develop its

image where the income statement and other computation is being done beneath :

Particular Amount

Selling price (U) 20

variable cost (U) 10

Contribution 10

Fixed cost 60000

PVR: Contribution/ sales *100

: 10/20*100= 50%

(a): BEP: Fixed cost / contribution

: 60000/10= 6000

(b) Total number of ticket needed to be sold

Particular Amount

Selling price (U) 20

variable cost (U) 10

Contribution=profit + fixed cost 90000

Fixed cost 60000

Profit 30000

50%= Contribution/ sales

Sales= 90000/50%= 45000

(c): Calculation for desire profit

Particular Amount

Profit 8000

Add: Fixed cost 60000

Contribution 68000

5

process company will analysis internal pricing decision or helps to enhance position of

organisation (Laudon and Laudon, 2016).

Event which is being developed by Ever Joy Enterprises (UK) for Somerset to develop its

image where the income statement and other computation is being done beneath :

Particular Amount

Selling price (U) 20

variable cost (U) 10

Contribution 10

Fixed cost 60000

PVR: Contribution/ sales *100

: 10/20*100= 50%

(a): BEP: Fixed cost / contribution

: 60000/10= 6000

(b) Total number of ticket needed to be sold

Particular Amount

Selling price (U) 20

variable cost (U) 10

Contribution=profit + fixed cost 90000

Fixed cost 60000

Profit 30000

50%= Contribution/ sales

Sales= 90000/50%= 45000

(c): Calculation for desire profit

Particular Amount

Profit 8000

Add: Fixed cost 60000

Contribution 68000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variable cost 10

Desire Profit: Sales*variable cost

Profit: 8000*10= 80000.

Marginal costing tools: This is being considered as a technique that aids in analysing

total net profit of a company (Marginal and Absorption costing, 2012). In context of Ever Joy

Enterprises, its manager mainly uses this tool in order to pull out or compute additional unit

related to an output till the moment when marginal benefits stand outs over all marginal cost. It

also distinguish the fixed cost from variable cost and only variable cost is charge to quantity cost.

Break-Even Analysis: This sort of analysis is being done by a company when it comes to

analyse formulate the relation of both fixed along with variable cost of an organisation

considering the revenue (Zamora, 2011). BEP predicts on a single point, where sales gets high

with the help of revenue. Ever Joy Enterprises can use this tool when it comes to calculate that

how many units of goods needs to be sold so that cost can get cover.

Standard costing: This type of costing is majorly being considered as a measurable value

related to an asset that is already included in a balance sheet focusing on its original cost which

has been purchased by Ever Joy Enterprises. With the help of this, accountant of this company

can look into both profit and expenses at the same time.

TASK 3

P4 Advantages and disadvantages of different types of planning tools for budgetary control

Budget is formal statement carrying estimate of cash, revenues, expenses and resources

over a specified period, based future plans and objectives. It determines plan of action for

achieving qualified objectives at Ever joy and standard for measuring performance and source to

manage predictable contrary situations. In Ever Joy Enterprise, budget can be prepared by

considering following steps-

Obtaining Estimates: By obtaining its estimates of sales, expected costs, production

level, and availability of resources from all departments or divisions of an organisation, that is

required for future conditions and forecasting impactful activities and finally submitted to budget

committee at Ever Joy for approval.

Coordinating Estimates: The different plans submitted by various units at Ever Joy are

evaluated by the budget committee to determine the potentiality of plan in overall profit of the

6

Desire Profit: Sales*variable cost

Profit: 8000*10= 80000.

Marginal costing tools: This is being considered as a technique that aids in analysing

total net profit of a company (Marginal and Absorption costing, 2012). In context of Ever Joy

Enterprises, its manager mainly uses this tool in order to pull out or compute additional unit

related to an output till the moment when marginal benefits stand outs over all marginal cost. It

also distinguish the fixed cost from variable cost and only variable cost is charge to quantity cost.

Break-Even Analysis: This sort of analysis is being done by a company when it comes to

analyse formulate the relation of both fixed along with variable cost of an organisation

considering the revenue (Zamora, 2011). BEP predicts on a single point, where sales gets high

with the help of revenue. Ever Joy Enterprises can use this tool when it comes to calculate that

how many units of goods needs to be sold so that cost can get cover.

Standard costing: This type of costing is majorly being considered as a measurable value

related to an asset that is already included in a balance sheet focusing on its original cost which

has been purchased by Ever Joy Enterprises. With the help of this, accountant of this company

can look into both profit and expenses at the same time.

TASK 3

P4 Advantages and disadvantages of different types of planning tools for budgetary control

Budget is formal statement carrying estimate of cash, revenues, expenses and resources

over a specified period, based future plans and objectives. It determines plan of action for

achieving qualified objectives at Ever joy and standard for measuring performance and source to

manage predictable contrary situations. In Ever Joy Enterprise, budget can be prepared by

considering following steps-

Obtaining Estimates: By obtaining its estimates of sales, expected costs, production

level, and availability of resources from all departments or divisions of an organisation, that is

required for future conditions and forecasting impactful activities and finally submitted to budget

committee at Ever Joy for approval.

Coordinating Estimates: The different plans submitted by various units at Ever Joy are

evaluated by the budget committee to determine the potentiality of plan in overall profit of the

6

company. This also estimate available resources and their fair allocation among various units in

an organisation.

Communicating Budget: This includes communication of prepared budget to the

concerned departments and managers of Ever Joy Enterprise. The budget must be approved in

light of departmental goals, organisational goals and availability of resources.

Implementing Budget Plan: The final budget is presented to concerned managers and

adopted as plan of operation for the coming budget period in Ever Joy Enterprise.

Review of Budget: In budgeting process, performance reports are prepared as a feedback

(Ismail and King, 2014). These performance reports at Ever Joy are prepared to inform

departmental managers and top level management about actual performance achieved in terms of

budgeted figures.

A company uses different types of budgets to plan and determine their revenues and expenses

such as:

Capital Budget: Is is a plan for raising long term funds for investing in acquisition and

maintenance of fixed assets, over a period. Ever Joy can use techniques such as internal rate of

return, net present value, and payback period for calculating capital budget.

Operating Budget: This budget is done for short term investments that forecast and

analysis of proposed income and expenses mainly by sales in Ever joy, over a specific time

period. Some advantages and disadvantages of operating budget are as:

Advantages:

Arriving benefits by tracking current expenses (Benefits of Operating Budget, 2018).

Assists in save money for future unforeseen events.

Disadvantages:

Excessive research for long-term planning.

Inaccurate data can lead to mismanagement of cash flow.

There are also some other alternative methods of budget such as:

Master Budget: A master budget is generally used in large companies having total record

of company's individual budgets designed to show a complete picture of financial activities and

situation of a company (Theriou and Aggelidis, 2014). This combines factors like sales, assets,

operating expenses, and income sources for Ever Joy to establish its goals.

7

an organisation.

Communicating Budget: This includes communication of prepared budget to the

concerned departments and managers of Ever Joy Enterprise. The budget must be approved in

light of departmental goals, organisational goals and availability of resources.

Implementing Budget Plan: The final budget is presented to concerned managers and

adopted as plan of operation for the coming budget period in Ever Joy Enterprise.

Review of Budget: In budgeting process, performance reports are prepared as a feedback

(Ismail and King, 2014). These performance reports at Ever Joy are prepared to inform

departmental managers and top level management about actual performance achieved in terms of

budgeted figures.

A company uses different types of budgets to plan and determine their revenues and expenses

such as:

Capital Budget: Is is a plan for raising long term funds for investing in acquisition and

maintenance of fixed assets, over a period. Ever Joy can use techniques such as internal rate of

return, net present value, and payback period for calculating capital budget.

Operating Budget: This budget is done for short term investments that forecast and

analysis of proposed income and expenses mainly by sales in Ever joy, over a specific time

period. Some advantages and disadvantages of operating budget are as:

Advantages:

Arriving benefits by tracking current expenses (Benefits of Operating Budget, 2018).

Assists in save money for future unforeseen events.

Disadvantages:

Excessive research for long-term planning.

Inaccurate data can lead to mismanagement of cash flow.

There are also some other alternative methods of budget such as:

Master Budget: A master budget is generally used in large companies having total record

of company's individual budgets designed to show a complete picture of financial activities and

situation of a company (Theriou and Aggelidis, 2014). This combines factors like sales, assets,

operating expenses, and income sources for Ever Joy to establish its goals.

7

Cash-flow Budget: This method help in projecting process and time duration of credit

and debits of cash in Ever Joy Enterprise in specified time period. It is useful to assist a company

determine flow of cash wisely within their company.

Financial Budget: This budget at Ever Joy presents its strategy for managing assets, cash

flow, income and expenses. It establishes framework of a company's financial health and

spending of revenues from core operations.

For Ever Joy Enterprises there are many pricing stargates such as :

Price skimming- In which Ever Joy Enterprise can set a high price in initial stage and

lower it after the market evolves.

Penetration pricing- Ever Joy Enterprise can set a low price to enter a competitive

market and raise it later.

Price bundling- By this Ever Joy can combine two products to increase value and prices.

Cost-plus pricing- In this method Ever Joy can simply calculate their costs and adding

marginal cost cost it.

Competitive pricing- By setting a price based on the pricing strategy of competitor, Ever

Joy can increase market share.

For Ever Joy Enterprise some Common Costing Systems are:

Actual costing: Cost on the basis of raw materials, overheads and labour (Hendriks, 2013). Thus

in Ever Joy Enterprise, only actual cost are taken into consideration not the budgeted cost.

Normal costing: Under this costing system budgeted amount is being used and it result in less

fluctuation in allocating of resource of Ever Joy Enterprises then actual costing method.

Standard costing: Standard cost avail its produced goods with the pre-decided material cost,

labour cost and overhead cost. This costing techniques in Ever Joy used to measure the

difference between actual cost and the cost which is incurred.

These costing activities are different from each other on the basis of:

Job costing: It consist of collection of cost related to material, overhead and labour. In Ever Joy

enterprise it is used for small unit level.

Process costing: In Ever Joy, this costing is used for mass production of similar products, where

the cost of individual units of finished goods can not be differentiated from each other.

Batch costing: Under this method, the cost is uncertain of batch of goods. This cost is not

adopted for similar type of product that can not be isolated while production.

8

and debits of cash in Ever Joy Enterprise in specified time period. It is useful to assist a company

determine flow of cash wisely within their company.

Financial Budget: This budget at Ever Joy presents its strategy for managing assets, cash

flow, income and expenses. It establishes framework of a company's financial health and

spending of revenues from core operations.

For Ever Joy Enterprises there are many pricing stargates such as :

Price skimming- In which Ever Joy Enterprise can set a high price in initial stage and

lower it after the market evolves.

Penetration pricing- Ever Joy Enterprise can set a low price to enter a competitive

market and raise it later.

Price bundling- By this Ever Joy can combine two products to increase value and prices.

Cost-plus pricing- In this method Ever Joy can simply calculate their costs and adding

marginal cost cost it.

Competitive pricing- By setting a price based on the pricing strategy of competitor, Ever

Joy can increase market share.

For Ever Joy Enterprise some Common Costing Systems are:

Actual costing: Cost on the basis of raw materials, overheads and labour (Hendriks, 2013). Thus

in Ever Joy Enterprise, only actual cost are taken into consideration not the budgeted cost.

Normal costing: Under this costing system budgeted amount is being used and it result in less

fluctuation in allocating of resource of Ever Joy Enterprises then actual costing method.

Standard costing: Standard cost avail its produced goods with the pre-decided material cost,

labour cost and overhead cost. This costing techniques in Ever Joy used to measure the

difference between actual cost and the cost which is incurred.

These costing activities are different from each other on the basis of:

Job costing: It consist of collection of cost related to material, overhead and labour. In Ever Joy

enterprise it is used for small unit level.

Process costing: In Ever Joy, this costing is used for mass production of similar products, where

the cost of individual units of finished goods can not be differentiated from each other.

Batch costing: Under this method, the cost is uncertain of batch of goods. This cost is not

adopted for similar type of product that can not be isolated while production.

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contract costing: In Ever Joy, this cost is used for tracking of cost related with specific contract

with customers.

TASK 4

P5 Comparison on how organizations are adapting management accounting system to resolve

financial problems

It is being analysed that financial problems can be considered as the situation when a

company goes through a financial crisis and this may majorly impacts upon a business operations.

Here, Ever Joy Enterprises have gone through a number of financial problems and still facing some

issues that have impacted on there both profit and productive margins. There are a number of

problems faced by the company from which one issue is being analysed properly and this is given

beneath :-

Failure in attainment of expected results or outcomes: In every single financial year, all

business organisations needs to develop a number of plans and procedures as well so that to meet

its future goals (Chang, 2016). Subject to Ever Joy Enterprise, where most of the managers and

leaders are not effective enough in nature which delays the overall process of developing a

program. In order to reduce the chances of facing the same situation again in future, organisation

have hired a consultant which suggested and delivered the information to use a number of

financial tools that may aid them in developing a much more secured position in near future.

These financial tools which will help are mentioned below:

Benchmarking: Benchmarking is a tool that may aid in improving business

performances along with practice as well. It has been found that, improvements and making

changes as per the requirements plays a crucial role in taking an organisation to an all new level.

Benchmarking majorly contains a number of stages like select subject, explain the process,

determine potential partners, determine information sources, collect information and choose

partners, identify the gape, set up activity differences, target future action, communicate, adjust

object, apply and review. In Ever Joy Enterprises, benchmarking is used to improve

performance, managing practices which are used for financial data recording as well as keeping.

When there is problem regarding operations or anything in Ever Joy Enterprises, benchmarking

helps in innovating their work by comparing from other competitors.

9

with customers.

TASK 4

P5 Comparison on how organizations are adapting management accounting system to resolve

financial problems

It is being analysed that financial problems can be considered as the situation when a

company goes through a financial crisis and this may majorly impacts upon a business operations.

Here, Ever Joy Enterprises have gone through a number of financial problems and still facing some

issues that have impacted on there both profit and productive margins. There are a number of

problems faced by the company from which one issue is being analysed properly and this is given

beneath :-

Failure in attainment of expected results or outcomes: In every single financial year, all

business organisations needs to develop a number of plans and procedures as well so that to meet

its future goals (Chang, 2016). Subject to Ever Joy Enterprise, where most of the managers and

leaders are not effective enough in nature which delays the overall process of developing a

program. In order to reduce the chances of facing the same situation again in future, organisation

have hired a consultant which suggested and delivered the information to use a number of

financial tools that may aid them in developing a much more secured position in near future.

These financial tools which will help are mentioned below:

Benchmarking: Benchmarking is a tool that may aid in improving business

performances along with practice as well. It has been found that, improvements and making

changes as per the requirements plays a crucial role in taking an organisation to an all new level.

Benchmarking majorly contains a number of stages like select subject, explain the process,

determine potential partners, determine information sources, collect information and choose

partners, identify the gape, set up activity differences, target future action, communicate, adjust

object, apply and review. In Ever Joy Enterprises, benchmarking is used to improve

performance, managing practices which are used for financial data recording as well as keeping.

When there is problem regarding operations or anything in Ever Joy Enterprises, benchmarking

helps in innovating their work by comparing from other competitors.

9

Key performance indicator(KPI): This type of indicator contains an organisational

progress which takes a company to a whole new level. On the other hand, main motive of KPI is

to locate 'Key' related to a company and its business as well. A KPI mainly contains a strategy,

mission along with a vision of Ever Joy Enterprises as well at the same time. There are two types

which has been formulated and these are financial and non-financial KPI. Financial KPI are

accounting ratios which helps in determining financial position of Ever Joy Enterprises. While

non-financial KPI assists in resolution of problems regarding internal management system and

business operations. Both contributes to the success of Ever Joy Enterprises.

Financial Governance: With the help of this tool, Ever Joy Enterprises can easily gather,

monitor and manage the overall financial data. Away with this, it aids in formulating a number of

solutions considering policies, strategies which will help in maintaining the business information

keeping it much more reliable and authentic in nature. This tool can also aid Ever Joy Enterprises

looking at its weak and strong points at the same time.

Budgetary targets: This type of tools can be used by Ever Joy Enterprises at the time of

formulating financial and business related objectives. Away with this, budgetary techniques can

also be used for planing and controlling of Ever Joy Enterprises. With the help of this, company

may easily look into the overall performance and achievement of the objective.

Skills of management accountant:

Some of skills are presented beneath: Commercial Awareness – When it comes to resolve an issue related to finance, it is

required for accountant of Ever Joy Enterprises to stay aware about commercial policies

that may aid in reaching to a whole new level. Up to speed with technology - It is required for accountant of Ever Joy Enterprises to

have proper knowledge related to number of software like Oracle, MS Excel, and so on.

Knowledge of business fundamentals- Another skill that accountant of this company

needs to have is knowledge related to all the financial tools which will raise funds that

will maximise all the returns (Laudon and Laudon, 2015).

EVER JOY ENTERPRISE PARKWOOD ENTERPRISE

Business of this organisation deals in

adventure and leisure sector. They have their

own benchmarking through which they judge

This company provides their services locally to

complete their objectives. Organisation came

into existence in 1951. through, key

10

progress which takes a company to a whole new level. On the other hand, main motive of KPI is

to locate 'Key' related to a company and its business as well. A KPI mainly contains a strategy,

mission along with a vision of Ever Joy Enterprises as well at the same time. There are two types

which has been formulated and these are financial and non-financial KPI. Financial KPI are

accounting ratios which helps in determining financial position of Ever Joy Enterprises. While

non-financial KPI assists in resolution of problems regarding internal management system and

business operations. Both contributes to the success of Ever Joy Enterprises.

Financial Governance: With the help of this tool, Ever Joy Enterprises can easily gather,

monitor and manage the overall financial data. Away with this, it aids in formulating a number of

solutions considering policies, strategies which will help in maintaining the business information

keeping it much more reliable and authentic in nature. This tool can also aid Ever Joy Enterprises

looking at its weak and strong points at the same time.

Budgetary targets: This type of tools can be used by Ever Joy Enterprises at the time of

formulating financial and business related objectives. Away with this, budgetary techniques can

also be used for planing and controlling of Ever Joy Enterprises. With the help of this, company

may easily look into the overall performance and achievement of the objective.

Skills of management accountant:

Some of skills are presented beneath: Commercial Awareness – When it comes to resolve an issue related to finance, it is

required for accountant of Ever Joy Enterprises to stay aware about commercial policies

that may aid in reaching to a whole new level. Up to speed with technology - It is required for accountant of Ever Joy Enterprises to

have proper knowledge related to number of software like Oracle, MS Excel, and so on.

Knowledge of business fundamentals- Another skill that accountant of this company

needs to have is knowledge related to all the financial tools which will raise funds that

will maximise all the returns (Laudon and Laudon, 2015).

EVER JOY ENTERPRISE PARKWOOD ENTERPRISE

Business of this organisation deals in

adventure and leisure sector. They have their

own benchmarking through which they judge

This company provides their services locally to

complete their objectives. Organisation came

into existence in 1951. through, key

10

actual situation with standard performance.

Agency explore there dealing with consumers

internationally.

performance indicators park wood come to

know about their increasing growth can could

compare actual performance. This company

conduct various KPI are as follows:- employee

turnover, inventory management, marketing

strategies like advertising, health and safety

departments, capital recovery etc.

Enterprise relates with monetary fund goals

and objectives in order to achieve objectives

effectively. Aids to compare approximation

and revenue cost with potential estimated

records.

Parkwood enterprise also uses their own

benchmarking to generate high revenues. This

marking has it's own process as follows:-

determining data, assembling information,

judging content to evaluate actual performance

with standardized aggregation.

CONCLUSION

From presented data above, it can be concluded that accounting management play vital role

in organisation. Information can be predict in advance and mental process required for relating to

business activities in order to achieve organisational goals. It helps in developing mission, vision,

goal and objective. To overcome with conflicts and disorder it provides difference between actual

situation with standard performance. Different methods and strategies will enhance problems related

to production as well as financial. Hence, whether the organisation is short or long term accounting

should be managed to check financial statement of enterprise. By adapting various techniques

company can accomplish objectives effectively and efficiently.

11

Agency explore there dealing with consumers

internationally.

performance indicators park wood come to

know about their increasing growth can could

compare actual performance. This company

conduct various KPI are as follows:- employee

turnover, inventory management, marketing

strategies like advertising, health and safety

departments, capital recovery etc.

Enterprise relates with monetary fund goals

and objectives in order to achieve objectives

effectively. Aids to compare approximation

and revenue cost with potential estimated

records.

Parkwood enterprise also uses their own

benchmarking to generate high revenues. This

marking has it's own process as follows:-

determining data, assembling information,

judging content to evaluate actual performance

with standardized aggregation.

CONCLUSION

From presented data above, it can be concluded that accounting management play vital role

in organisation. Information can be predict in advance and mental process required for relating to

business activities in order to achieve organisational goals. It helps in developing mission, vision,

goal and objective. To overcome with conflicts and disorder it provides difference between actual

situation with standard performance. Different methods and strategies will enhance problems related

to production as well as financial. Hence, whether the organisation is short or long term accounting

should be managed to check financial statement of enterprise. By adapting various techniques

company can accomplish objectives effectively and efficiently.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Kokubu, K. and Tachikawa, H., 2013. Material Flow Cost Accounting: Significance and

Practical Approach . In∗ Handbook of sustainable engineering (pp. 351-369). Springer,

Dordrecht.

Burritt, R.L., Schaltegger, S. and Zvezdov, D., 2011. Carbon management accounting:

explaining practice in leading German companies. Australian Accounting Review. 21(1).

pp.80-98.

Van Dooren, W., Bouckaert, G. and Halligan, J., 2015. Performance management in the public

sector. Routledge.

Lay, T.A. and Jusoh, R., 2012. BUSINESS STRATEGY, STRATEGIC ROLE OF

ACCOUNTANT, STRATEGIC MANAGEMENT ACCOUNTING AND THEIR

LINKS TO FIRM PERFORMANCE: AN EXPLORATORY STUDY OF

MANUFACTURING COMPANIES IN MALAYSIA. Asia-Pacific Management

Accounting Journal. 7(1).

Schaltegger, S., Burritt, R. and Petersen, H., 2017. An introduction to corporate environmental

management: Striving for sustainability. Routledge.

Gullkvist, B.M., 2013. Drivers of change in management accounting practices in an ERP

environment.

Laudon, K.C. and Laudon, J.P., 2016. Management information system. Pearson Education

India.

Zamora, V.L., 2011. Using a social enterprise service-learning strategy in an introductory

management accounting course. Issues in Accounting Education. 27(1), pp.187-226.

Ismail, N.A. and King, M., 2014. Factors influencing the alignment of accounting information

systems in small and medium sized Malaysian manufacturing firms. Journal of

Information Systems and Small Business. 1(1-2), pp.1-20.

Theriou, G.N. and Aggelidis, V., 2014. Management Accounting Systems, Top Management

Team’s Risk Characteristics and their Effect on Strategic Change. International Journal

of Economics and Business Administration. 2(2), pp.3-38.

Hendriks, C.J., 2013. Integrated Financial Management Information Systems: Guidelines for

effective implementation by the public sector of South Africa. South African Journal of

Information Management. 15(1), pp.1-9.

Chang, J.F., 2016. Business process management systems: strategy and implementation.

Auerbach Publications.

Laudon, K.C. and Laudon, J.P., 2015. Management information systems (Vol. 8). Prentice Hall.

Online

Benefits of Operating Budget, 2018. [Online]. Available through :<

https://smallbusiness.chron.com/four-benefits-operating-budget-60927.html>.

Marginal and Absorption costing, 2012. [online]. Available through:

<http://kfknowledgebank.kaplan.co.uk/KFKB/Wiki%20Pages/Marginal%20and

%20absorption%20costing.aspx>

12

Books and Journals

Kokubu, K. and Tachikawa, H., 2013. Material Flow Cost Accounting: Significance and

Practical Approach . In∗ Handbook of sustainable engineering (pp. 351-369). Springer,

Dordrecht.

Burritt, R.L., Schaltegger, S. and Zvezdov, D., 2011. Carbon management accounting:

explaining practice in leading German companies. Australian Accounting Review. 21(1).

pp.80-98.

Van Dooren, W., Bouckaert, G. and Halligan, J., 2015. Performance management in the public

sector. Routledge.

Lay, T.A. and Jusoh, R., 2012. BUSINESS STRATEGY, STRATEGIC ROLE OF

ACCOUNTANT, STRATEGIC MANAGEMENT ACCOUNTING AND THEIR

LINKS TO FIRM PERFORMANCE: AN EXPLORATORY STUDY OF

MANUFACTURING COMPANIES IN MALAYSIA. Asia-Pacific Management

Accounting Journal. 7(1).

Schaltegger, S., Burritt, R. and Petersen, H., 2017. An introduction to corporate environmental

management: Striving for sustainability. Routledge.

Gullkvist, B.M., 2013. Drivers of change in management accounting practices in an ERP

environment.

Laudon, K.C. and Laudon, J.P., 2016. Management information system. Pearson Education

India.

Zamora, V.L., 2011. Using a social enterprise service-learning strategy in an introductory

management accounting course. Issues in Accounting Education. 27(1), pp.187-226.

Ismail, N.A. and King, M., 2014. Factors influencing the alignment of accounting information

systems in small and medium sized Malaysian manufacturing firms. Journal of

Information Systems and Small Business. 1(1-2), pp.1-20.

Theriou, G.N. and Aggelidis, V., 2014. Management Accounting Systems, Top Management

Team’s Risk Characteristics and their Effect on Strategic Change. International Journal

of Economics and Business Administration. 2(2), pp.3-38.

Hendriks, C.J., 2013. Integrated Financial Management Information Systems: Guidelines for

effective implementation by the public sector of South Africa. South African Journal of

Information Management. 15(1), pp.1-9.

Chang, J.F., 2016. Business process management systems: strategy and implementation.

Auerbach Publications.

Laudon, K.C. and Laudon, J.P., 2015. Management information systems (Vol. 8). Prentice Hall.

Online

Benefits of Operating Budget, 2018. [Online]. Available through :<

https://smallbusiness.chron.com/four-benefits-operating-budget-60927.html>.

Marginal and Absorption costing, 2012. [online]. Available through:

<http://kfknowledgebank.kaplan.co.uk/KFKB/Wiki%20Pages/Marginal%20and

%20absorption%20costing.aspx>

12

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.