Management Accounting: Cost Analysis, Planning Tools & Airdri Ltd.

VerifiedAdded on 2023/01/19

|18

|3927

|73

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems, principles, and techniques, emphasizing their application in solving financial problems, particularly in the context of Airdri Ltd., a UK-based hand dryer manufacturer. It covers various management accounting systems, including financial, cost, management, and tax accounting systems, and explores different methods of management accounting reporting, such as account retrievable ageing reports, job cost reports, and inventory reports. The report also delves into cost analysis techniques, comparing marginal and absorption costing methods, and examines planning tools for budgetary control. Furthermore, it discusses how organizations adopt management accounting systems to address financial challenges, offering insights into the integration of these systems and reports within organizational processes. The document is a student contribution available on Desklib, offering valuable information and examples for understanding management accounting practices.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

P1 Management accounting and different types of management accounting systems...............3

P2 Methods of management accounting reporting......................................................................4

M1 Benefits of management accounting systems and their application.....................................5

D1 Integration of management accounting systems and reports in organisational processes....6

LO 2.................................................................................................................................................6

P3 Techniques of cost analysis using marginal and absorption costs.........................................6

M2 Application of management accounting techniques...........................................................15

D2 Application and interpretation of financial reports.............................................................15

TASK 3..........................................................................................................................................15

P4 : Advantages and disadvantages of different types of planning tools .................................15

M3 : Analysis of different planning tool...................................................................................16

TASK 4..........................................................................................................................................17

P5 : Comparison of how organisations are adopting management accounting systems to

respond to financial problems...................................................................................................17

M4 : Analysis of management accounting and financial problems..........................................18

D3 : Evaluation of how planning tools can solve accounting issues........................................18

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

P1 Management accounting and different types of management accounting systems...............3

P2 Methods of management accounting reporting......................................................................4

M1 Benefits of management accounting systems and their application.....................................5

D1 Integration of management accounting systems and reports in organisational processes....6

LO 2.................................................................................................................................................6

P3 Techniques of cost analysis using marginal and absorption costs.........................................6

M2 Application of management accounting techniques...........................................................15

D2 Application and interpretation of financial reports.............................................................15

TASK 3..........................................................................................................................................15

P4 : Advantages and disadvantages of different types of planning tools .................................15

M3 : Analysis of different planning tool...................................................................................16

TASK 4..........................................................................................................................................17

P5 : Comparison of how organisations are adopting management accounting systems to

respond to financial problems...................................................................................................17

M4 : Analysis of management accounting and financial problems..........................................18

D3 : Evaluation of how planning tools can solve accounting issues........................................18

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION

Management accounting is related to gathering, analysing and reporting financial

information about the operations and finances of a business to help the managers in their

decision-making process. These reports are prepared to be used internally by the managers and

not external stakeholders. Management accounting can help in managing and controlling the

expenses so that profitability of organisation increases. In this report various management

accounting systems, principles and techniques will be discussed. Further how financial problems

can be solved using management accounting will be discussed in relation to Airdri Ltd. which is

located in Technology House, UK and deals in manufacture of hand dryer which are recognised

for their reliability and low energy consumption. Planning tools for budgetary control will also

be discussed in this report.

LO 1

P1 Management accounting and different types of management accounting systems

According to the Institute of Management Accounts (IMA) : “Management accounting

involves planning, decision-making and providing financial reports to assist management in the

formulation and effective implementation of an organisation's strategy”.

The key functions of management accounting are discussed below : Provide data : It helps in gathering information related to all the functions of a business

which can help managers in planning, organising, controlling and decision-making

(Yeshmin and Hossan2011). Analyses and interprets data : The data is analysed and interpreted so that reports and

statements can be made to help managers in important decision making. Serves as a means of communication : Management accounting is responsible for

communicating the information gathered and analysed to the various departments so that

their activities can be coordinated and integrated to reach common goals.

Facilitates accounts control : The accounts of the business can be managed to control

unnecessary expenses of the business (Agrawal, 2018).

Some management accounting systems are discussed below :

Financial accounting system : The purpose of this system is to maintain financial

accounts of a business by collecting financial records i.e. any transaction which debits or

Management accounting is related to gathering, analysing and reporting financial

information about the operations and finances of a business to help the managers in their

decision-making process. These reports are prepared to be used internally by the managers and

not external stakeholders. Management accounting can help in managing and controlling the

expenses so that profitability of organisation increases. In this report various management

accounting systems, principles and techniques will be discussed. Further how financial problems

can be solved using management accounting will be discussed in relation to Airdri Ltd. which is

located in Technology House, UK and deals in manufacture of hand dryer which are recognised

for their reliability and low energy consumption. Planning tools for budgetary control will also

be discussed in this report.

LO 1

P1 Management accounting and different types of management accounting systems

According to the Institute of Management Accounts (IMA) : “Management accounting

involves planning, decision-making and providing financial reports to assist management in the

formulation and effective implementation of an organisation's strategy”.

The key functions of management accounting are discussed below : Provide data : It helps in gathering information related to all the functions of a business

which can help managers in planning, organising, controlling and decision-making

(Yeshmin and Hossan2011). Analyses and interprets data : The data is analysed and interpreted so that reports and

statements can be made to help managers in important decision making. Serves as a means of communication : Management accounting is responsible for

communicating the information gathered and analysed to the various departments so that

their activities can be coordinated and integrated to reach common goals.

Facilitates accounts control : The accounts of the business can be managed to control

unnecessary expenses of the business (Agrawal, 2018).

Some management accounting systems are discussed below :

Financial accounting system : The purpose of this system is to maintain financial

accounts of a business by collecting financial records i.e. any transaction which debits or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

credits the account balance so that financial statements can be made. These financial

statements needs to be audited annually which helps in determining the position of a

business. The income statements are made so that profits and losses can be evaluated and

methods of controlling and managing losses can be formulated. The financial accounting

system helps in determining the financial position of business in market and the assets it

has along with its liabilities which helps investors in gaining a complete view about

company.

Cost accounting system : It is a framework used in businesses to estimate the accurate

cost of their products so that profits can be analysed, inventory can be managed and costs

can be controlled. This help the companies in controlling costs at various stages of

production so that the wastages can be managed and costs can be reduced (Baiman,

2014). This system helps in analysing the cost of company for the analysis of

profitability, inventory valuation and cost control. It is important to estimate the correct

cost associated with production of products and services so that total profits can be

analysed.

Management accounting system : This system helps the organisation in measuring and

evaluating the processes so that accurate and timely financial and statistical information

can be given to mangers to help them in decision making. The reports and statements

prepared based on the financial activities of an organisation can help in taking monetary

decisions and managing the expenses of business. This system determines the internal

systems that are used by company in order to measure and evaluate its processes for

managing the organisation. Also this system help in generating appropriate financial

statements so that stakeholders can analyse their interests associated with company.

Tax accounting system : This system focuses on managing taxes of the company by

following rules and regulations governed by the Internal Revenue Code to prepare their

tax returns. This system helps in calculating accurate amount of tax that is due to the

government so that its intervention can be prevented in the company activities. Also it is

important to follow the tax regulations while preparing tax returns so that deductions and

other rebates can be gained which help in increasing the profits of business and also the

correct amount of due tax can be calculated.

statements needs to be audited annually which helps in determining the position of a

business. The income statements are made so that profits and losses can be evaluated and

methods of controlling and managing losses can be formulated. The financial accounting

system helps in determining the financial position of business in market and the assets it

has along with its liabilities which helps investors in gaining a complete view about

company.

Cost accounting system : It is a framework used in businesses to estimate the accurate

cost of their products so that profits can be analysed, inventory can be managed and costs

can be controlled. This help the companies in controlling costs at various stages of

production so that the wastages can be managed and costs can be reduced (Baiman,

2014). This system helps in analysing the cost of company for the analysis of

profitability, inventory valuation and cost control. It is important to estimate the correct

cost associated with production of products and services so that total profits can be

analysed.

Management accounting system : This system helps the organisation in measuring and

evaluating the processes so that accurate and timely financial and statistical information

can be given to mangers to help them in decision making. The reports and statements

prepared based on the financial activities of an organisation can help in taking monetary

decisions and managing the expenses of business. This system determines the internal

systems that are used by company in order to measure and evaluate its processes for

managing the organisation. Also this system help in generating appropriate financial

statements so that stakeholders can analyse their interests associated with company.

Tax accounting system : This system focuses on managing taxes of the company by

following rules and regulations governed by the Internal Revenue Code to prepare their

tax returns. This system helps in calculating accurate amount of tax that is due to the

government so that its intervention can be prevented in the company activities. Also it is

important to follow the tax regulations while preparing tax returns so that deductions and

other rebates can be gained which help in increasing the profits of business and also the

correct amount of due tax can be calculated.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2 Methods of management accounting reporting

Management accounting reporting is a process of preparing internal reports that can be

used by managers in decision-making. Some of its types are discussed as follows : Account retrievable ageing report : This report contains the details about all the credit

transactions of a company which helps the managers in analysing the amount that is still

needed to be collected from the debtors. This report help in monitoring collection policies

to reduce old bad debts and manage the liquidity of the company (Bebbington, Unerman

and O'Dwyer, 2014). This report thus show unpaid invoice balances along with the

duration from which they have been outstanding. The estimation of bad debts can be

done by this method by listing the payments that have been due over a longer period of

time so that company losses can be identified. Job cost report : This report helps in identifying the cost, expenses and financial

efficiency of each job so that more profitable projects can given more attention. This can

help in evaluating the waste areas so that costs can be controlled and reduced. This report

help in identifying the total cost which is required to be incurred while performing each

job which helps in identifying the jobs which use a large number of company resources

and also the profitable jobs can be identified.

Inventory report : These reports give information about the inventory of a business so

that a balance between inventory investment and customer service can be established.

This report contains labour cost, per unit overhead cost and wastages related to inventory

so that improvement can be made in managing inventory. Also this report help in

maintaining sufficient inventory stock in company so that the company does not run out

of stock. Also over assimilation of inventory can be managed which help in reducing

inventory cost of business.

Purpose of financial statement : Profit and loss account : This helps in knowing the net profits and losses generated by

the business at the end of the financial year. Balance sheet : This helps in evaluating the assets and liabilities of the company at the

end of financial year. Cash flow statement : This helps in assessing the cash position of the business i.e. the

cash inflows and cash outflows.

Management accounting reporting is a process of preparing internal reports that can be

used by managers in decision-making. Some of its types are discussed as follows : Account retrievable ageing report : This report contains the details about all the credit

transactions of a company which helps the managers in analysing the amount that is still

needed to be collected from the debtors. This report help in monitoring collection policies

to reduce old bad debts and manage the liquidity of the company (Bebbington, Unerman

and O'Dwyer, 2014). This report thus show unpaid invoice balances along with the

duration from which they have been outstanding. The estimation of bad debts can be

done by this method by listing the payments that have been due over a longer period of

time so that company losses can be identified. Job cost report : This report helps in identifying the cost, expenses and financial

efficiency of each job so that more profitable projects can given more attention. This can

help in evaluating the waste areas so that costs can be controlled and reduced. This report

help in identifying the total cost which is required to be incurred while performing each

job which helps in identifying the jobs which use a large number of company resources

and also the profitable jobs can be identified.

Inventory report : These reports give information about the inventory of a business so

that a balance between inventory investment and customer service can be established.

This report contains labour cost, per unit overhead cost and wastages related to inventory

so that improvement can be made in managing inventory. Also this report help in

maintaining sufficient inventory stock in company so that the company does not run out

of stock. Also over assimilation of inventory can be managed which help in reducing

inventory cost of business.

Purpose of financial statement : Profit and loss account : This helps in knowing the net profits and losses generated by

the business at the end of the financial year. Balance sheet : This helps in evaluating the assets and liabilities of the company at the

end of financial year. Cash flow statement : This helps in assessing the cash position of the business i.e. the

cash inflows and cash outflows.

Cost of goods sold : It helps in providing information regarding the costs that is involved

in selling products (Christ and Burritt, 2013).

Types of management accounting system : Price optimising system : This system helps in determining the prices of the products of

the company by evaluating the fluctuations in demands by change in price levels of the

products. Airdri Ltd. can use this system to tailor prices for different products based on

the demand of customers. Also promotional pricing, initial pricing, discount pricing can

be determined by this system, Job costing system : This system helps in determining the manufacturing prices of each

individual product while keeping a track on the expenses incurred. The products provided

by Airdri Ltd. are significantly different which helps in determining their costs so as to be

able to satisfy the customer requirements (Cohen, 2012).

Inventory management system : Through this process technology can be used to monitor

and maintain the stock of products so that cost can be maintained at all the stages of

production by Airdri Ltd. in manufacture of hand dryers.

M1 Benefits of management accounting systems and their application

Management

Accounting

Systems

Benefits Application in Airdri Ltd.

Job costing

system

Help the managers in determining the

profits related to individual project

and check if they should be carried

out in future.

The company can determine the

costs of different types of hand

dryers it produces according to

customer requirements.

Price optimising

system

Helps in determining prices based on

customer demands that maximizes

organisational profits.

The company can use this system to

reduce operational costs and set

prices.

Cost accounting

system

Helps in making policies to control

and manage costs of materials, labour

and overhead costs.

The company can use this system to

ascertain cost of hair dryers.

Inventory Improves management of inventory The company can maintain sufficient

in selling products (Christ and Burritt, 2013).

Types of management accounting system : Price optimising system : This system helps in determining the prices of the products of

the company by evaluating the fluctuations in demands by change in price levels of the

products. Airdri Ltd. can use this system to tailor prices for different products based on

the demand of customers. Also promotional pricing, initial pricing, discount pricing can

be determined by this system, Job costing system : This system helps in determining the manufacturing prices of each

individual product while keeping a track on the expenses incurred. The products provided

by Airdri Ltd. are significantly different which helps in determining their costs so as to be

able to satisfy the customer requirements (Cohen, 2012).

Inventory management system : Through this process technology can be used to monitor

and maintain the stock of products so that cost can be maintained at all the stages of

production by Airdri Ltd. in manufacture of hand dryers.

M1 Benefits of management accounting systems and their application

Management

Accounting

Systems

Benefits Application in Airdri Ltd.

Job costing

system

Help the managers in determining the

profits related to individual project

and check if they should be carried

out in future.

The company can determine the

costs of different types of hand

dryers it produces according to

customer requirements.

Price optimising

system

Helps in determining prices based on

customer demands that maximizes

organisational profits.

The company can use this system to

reduce operational costs and set

prices.

Cost accounting

system

Helps in making policies to control

and manage costs of materials, labour

and overhead costs.

The company can use this system to

ascertain cost of hair dryers.

Inventory Improves management of inventory The company can maintain sufficient

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management

system

so that storage costs can be reduced

(Damodaran, 2012).

stock of hair dryers based on

customer needs.

D1 Integration of management accounting systems and reports in organisational processes

Type of reporting Integration with Airdri Ltd. processes

Budget report Aids in focusing efforts on profitable business activities so

that goals and objectives can be efficiently achieved.

Accounts receivable ageing

report

Helps in timely collection of accounts receivable and creating

appropriate collection policies.

Job cost report Helpful in determining prices of various products offered by

the company.

Inventory and manufacturing

report

Can be used in managing inventory levels and manufacturing

costs of the products.

LO 2

P3 Techniques of cost analysis using marginal and absorption costs

Cost means the total amount of money that was used in the manufacture of products or

services using various resources such as raw materials, labour, time risks, opportunity costs etc.

income statements can be prepared using marginal or absorption costings : Marginal costing : It is a costing technique wherein marginal or variable cost is charged

to units of cost i.e. it is the change in total cost when the quantity produced is increased

by one. Therefore is the cost of producing one more unit (Fowzia, 2011).

Absorption costing : In this method all the costs that are involved in production of one

unit i.e. the variable and fixed costs. In this method all the costs associated with the

production of products are accumulated and apportioned to individual products.

system

so that storage costs can be reduced

(Damodaran, 2012).

stock of hair dryers based on

customer needs.

D1 Integration of management accounting systems and reports in organisational processes

Type of reporting Integration with Airdri Ltd. processes

Budget report Aids in focusing efforts on profitable business activities so

that goals and objectives can be efficiently achieved.

Accounts receivable ageing

report

Helps in timely collection of accounts receivable and creating

appropriate collection policies.

Job cost report Helpful in determining prices of various products offered by

the company.

Inventory and manufacturing

report

Can be used in managing inventory levels and manufacturing

costs of the products.

LO 2

P3 Techniques of cost analysis using marginal and absorption costs

Cost means the total amount of money that was used in the manufacture of products or

services using various resources such as raw materials, labour, time risks, opportunity costs etc.

income statements can be prepared using marginal or absorption costings : Marginal costing : It is a costing technique wherein marginal or variable cost is charged

to units of cost i.e. it is the change in total cost when the quantity produced is increased

by one. Therefore is the cost of producing one more unit (Fowzia, 2011).

Absorption costing : In this method all the costs that are involved in production of one

unit i.e. the variable and fixed costs. In this method all the costs associated with the

production of products are accumulated and apportioned to individual products.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

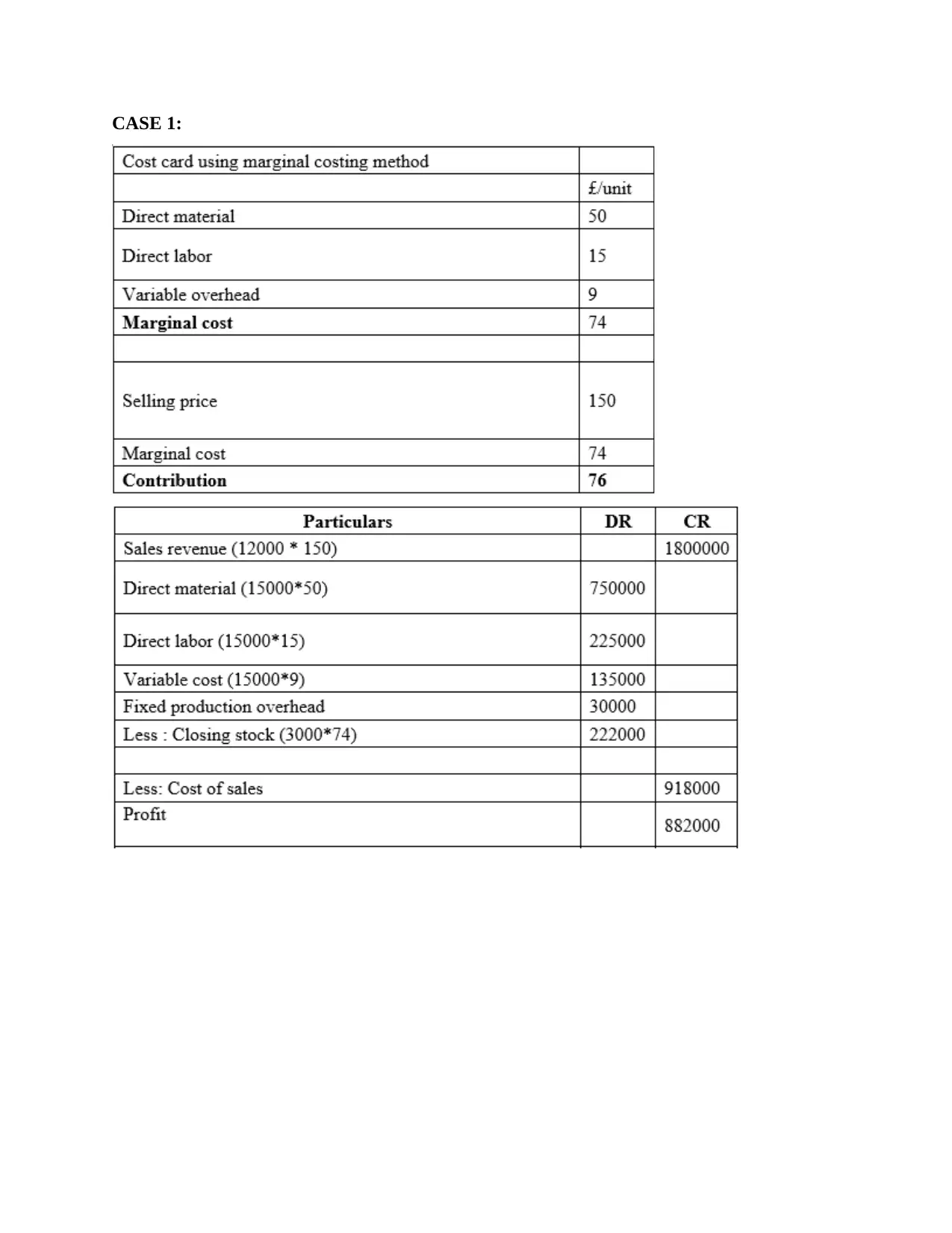

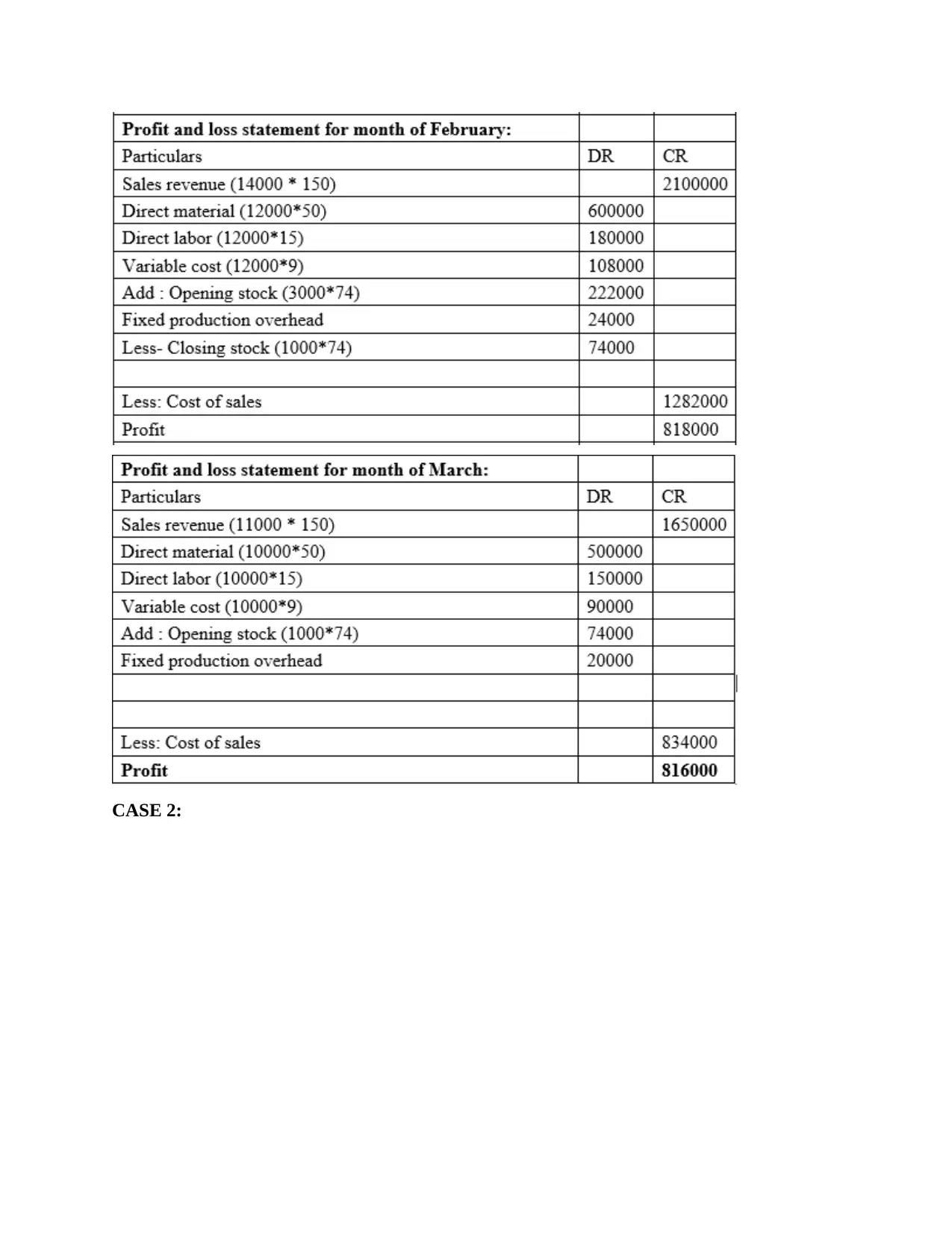

CASE 1:

CASE 2:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

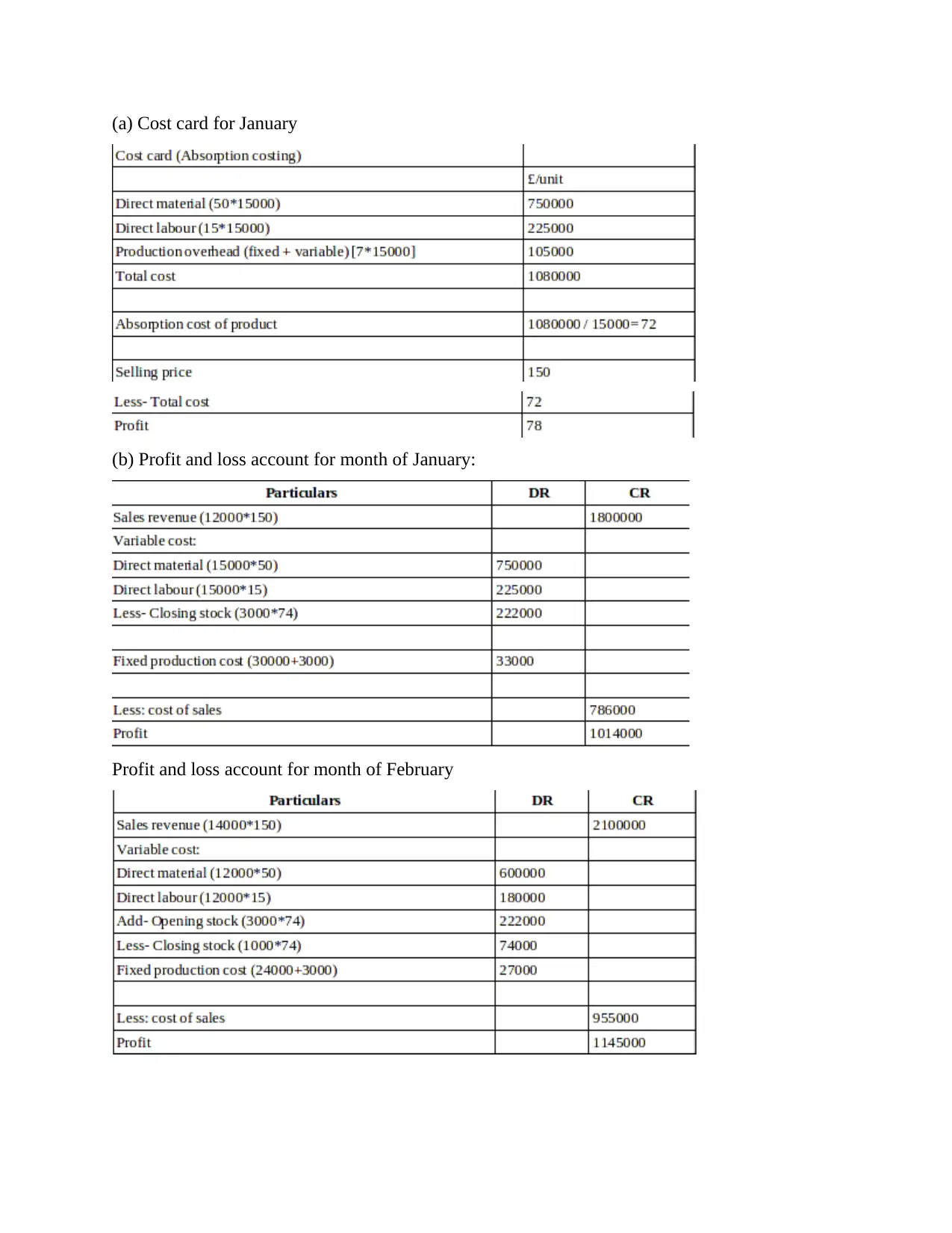

(a) Cost card for January

(b) Profit and loss account for month of January:

Profit and loss account for month of February

(b) Profit and loss account for month of January:

Profit and loss account for month of February

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

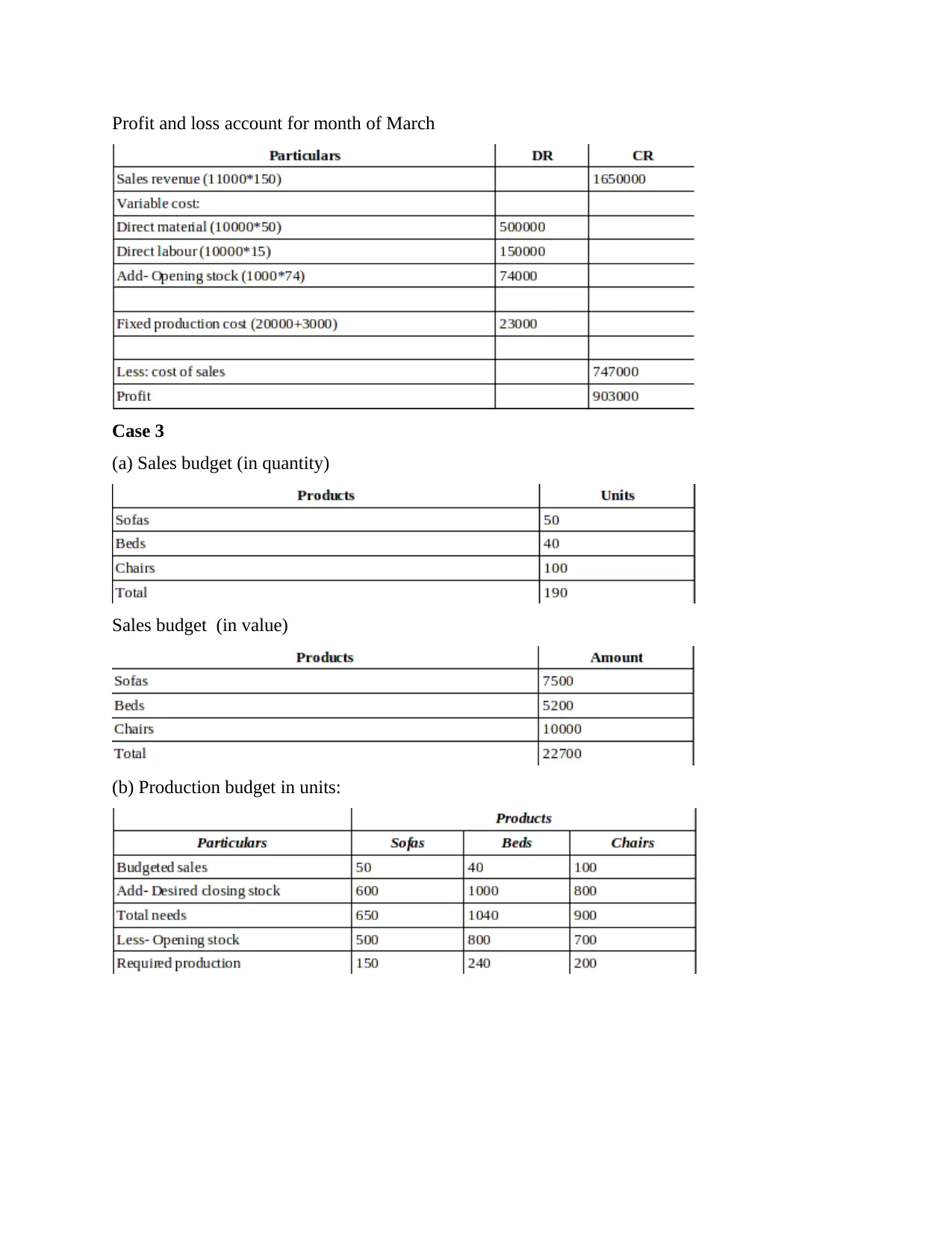

Profit and loss account for month of March

Case 3

(a) Sales budget (in quantity)

Sales budget (in value)

(b) Production budget in units:

Case 3

(a) Sales budget (in quantity)

Sales budget (in value)

(b) Production budget in units:

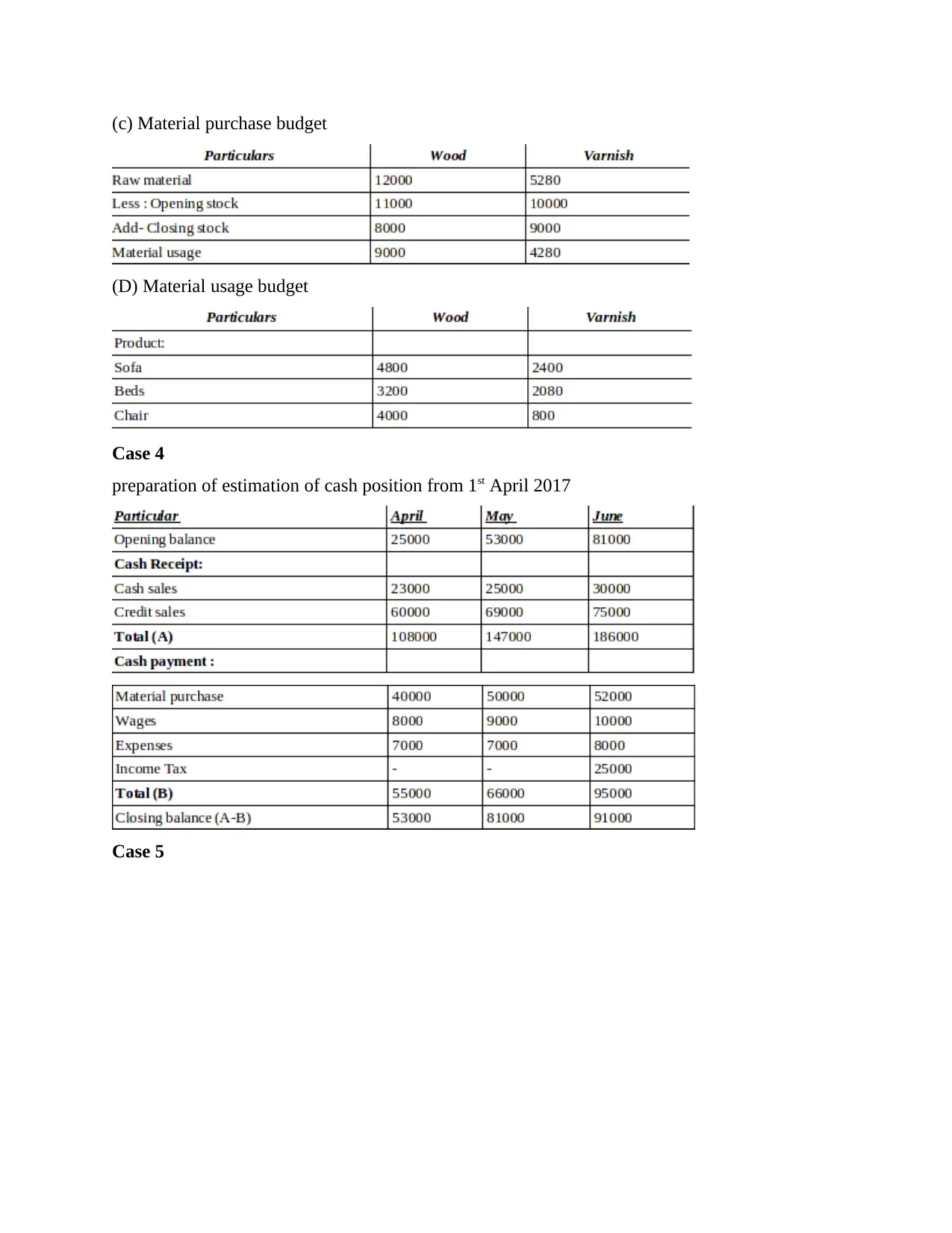

(c) Material purchase budget

(D) Material usage budget

Case 4

preparation of estimation of cash position from 1st April 2017

Case 5

(D) Material usage budget

Case 4

preparation of estimation of cash position from 1st April 2017

Case 5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.