Management Accounting

VerifiedAdded on 2023/06/18

|8

|1077

|252

AI Summary

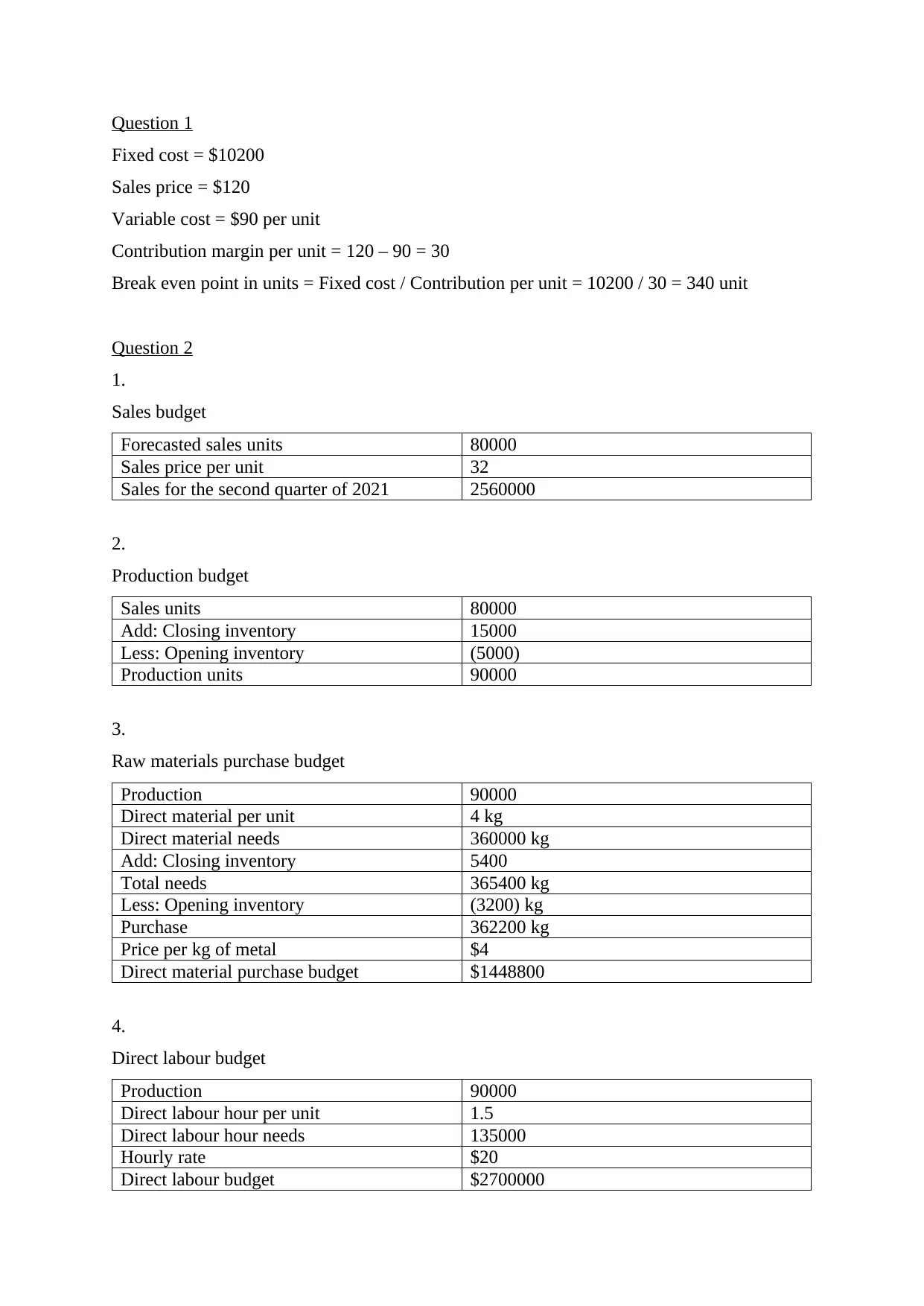

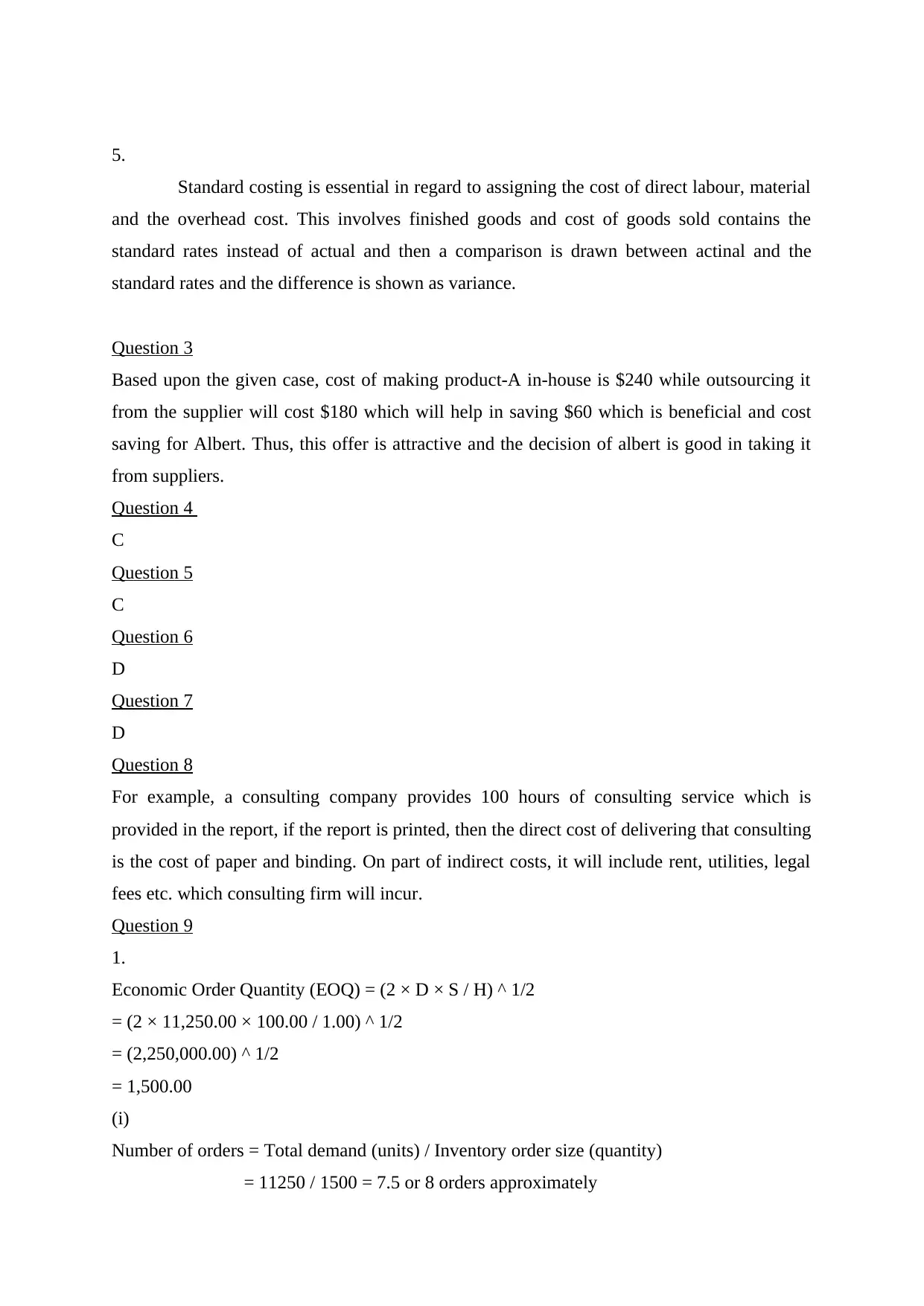

This article covers topics like fixed cost, sales budget, raw materials purchase budget, economic order quantity, job costing, variable costing and more related to Management Accounting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.