Prime Furniture: Management Accounting Report and Financial Analysis

VerifiedAdded on 2023/01/12

|13

|3204

|100

Report

AI Summary

This report, prepared for Prime Furniture, delves into the core principles and applications of management accounting. It begins with an introduction to management accounting and its significance in decision-making. The report then explores various cost analysis techniques, including marginal and absorption costing, with detailed calculations and interpretations for both methods. Furthermore, it examines the advantages and disadvantages of different planning tools used for budgetary control, such as cash budgets and master budgets. Finally, the report addresses the effectiveness of management accounting systems in responding to financial problems, including late payments and poor accounting systems, using tools like Key Performance Indicators (KPI) and variance analysis to propose solutions. The report provides a comprehensive overview of management accounting practices and their impact on financial stability and performance, offering valuable insights into the application of these techniques within the context of Prime Furniture.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 2............................................................................................................................................1

P3) Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs......................................................................1

TASK 3............................................................................................................................................5

P4) Advantages and disadvantages of different types of planning tools used for budgetary

control.....................................................................................................................................5

TASK 4............................................................................................................................................8

P5) Effectiveness of management accounting systems to respond on financial problems....8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 2............................................................................................................................................1

P3) Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs......................................................................1

TASK 3............................................................................................................................................5

P4) Advantages and disadvantages of different types of planning tools used for budgetary

control.....................................................................................................................................5

TASK 4............................................................................................................................................8

P5) Effectiveness of management accounting systems to respond on financial problems....8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Management accounting is the analysis of budgets and expenses that administrators

inside the company need to be available. The main aim of this study to collect all the relevant

information in regard of business. This is the method of the identification, classification and

analysis of the records and details (Arroyo, 2012). This report based on the Prime furniture

which is situated in UK and provides their services to design effective furniture. It provides

facility to people to design their furniture according to their interest. In this report consist of

various techniques to calculate numerical problems and analysis the importance of management

accounting in regard of decision making procedure. Additionally, use different budgets as

planning tools to forecast future results that help in gain good return on capital. There are

identifying various problems that can sort out through accounting systems and tools use to

identify these problems.

TASK 2

P3) Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs

Different types of techniques

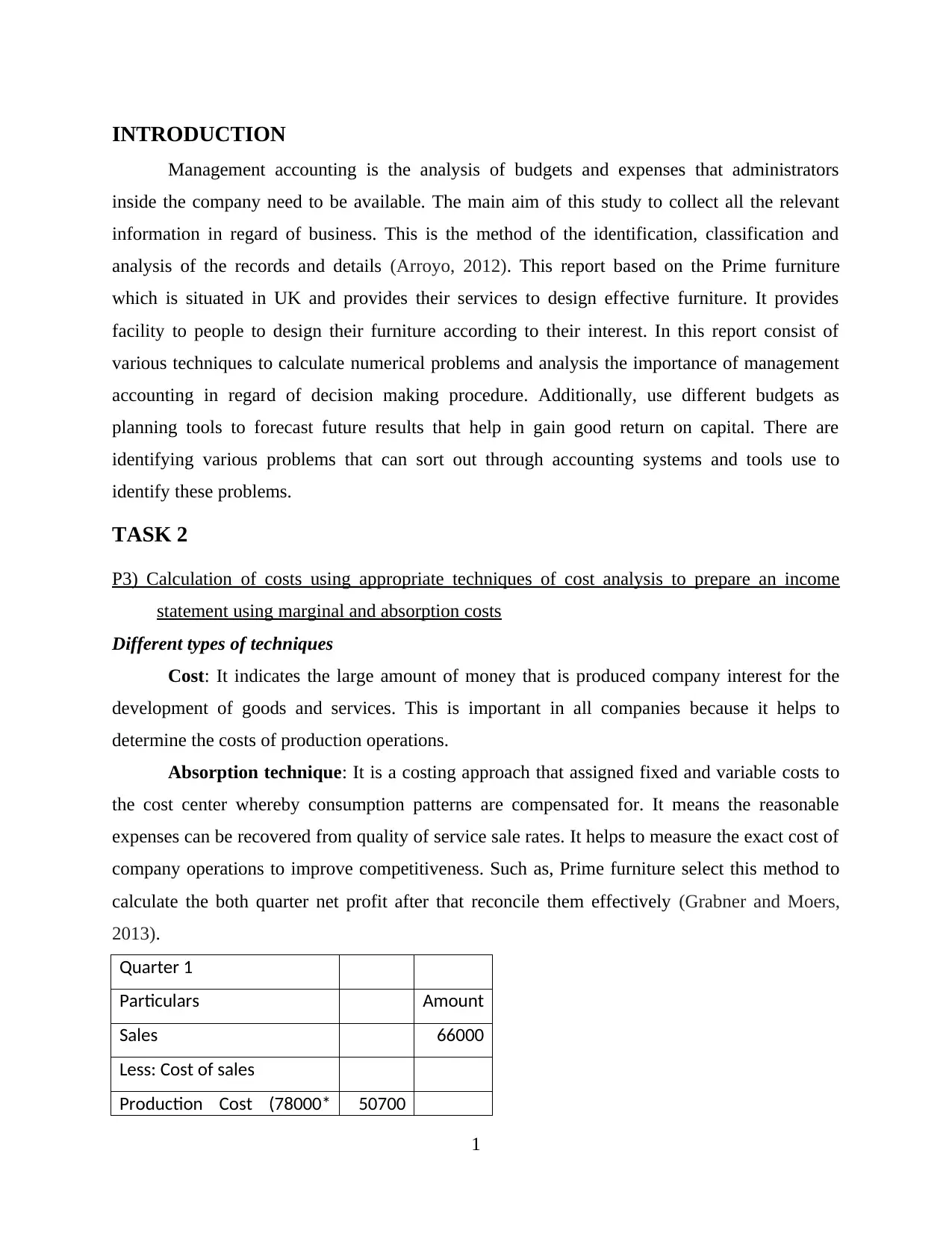

Cost: It indicates the large amount of money that is produced company interest for the

development of goods and services. This is important in all companies because it helps to

determine the costs of production operations.

Absorption technique: It is a costing approach that assigned fixed and variable costs to

the cost center whereby consumption patterns are compensated for. It means the reasonable

expenses can be recovered from quality of service sale rates. It helps to measure the exact cost of

company operations to improve competitiveness. Such as, Prime furniture select this method to

calculate the both quarter net profit after that reconcile them effectively (Grabner and Moers,

2013).

Quarter 1

Particulars Amount

Sales 66000

Less: Cost of sales

Production Cost (78000* 50700

1

Management accounting is the analysis of budgets and expenses that administrators

inside the company need to be available. The main aim of this study to collect all the relevant

information in regard of business. This is the method of the identification, classification and

analysis of the records and details (Arroyo, 2012). This report based on the Prime furniture

which is situated in UK and provides their services to design effective furniture. It provides

facility to people to design their furniture according to their interest. In this report consist of

various techniques to calculate numerical problems and analysis the importance of management

accounting in regard of decision making procedure. Additionally, use different budgets as

planning tools to forecast future results that help in gain good return on capital. There are

identifying various problems that can sort out through accounting systems and tools use to

identify these problems.

TASK 2

P3) Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs

Different types of techniques

Cost: It indicates the large amount of money that is produced company interest for the

development of goods and services. This is important in all companies because it helps to

determine the costs of production operations.

Absorption technique: It is a costing approach that assigned fixed and variable costs to

the cost center whereby consumption patterns are compensated for. It means the reasonable

expenses can be recovered from quality of service sale rates. It helps to measure the exact cost of

company operations to improve competitiveness. Such as, Prime furniture select this method to

calculate the both quarter net profit after that reconcile them effectively (Grabner and Moers,

2013).

Quarter 1

Particulars Amount

Sales 66000

Less: Cost of sales

Production Cost (78000* 50700

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

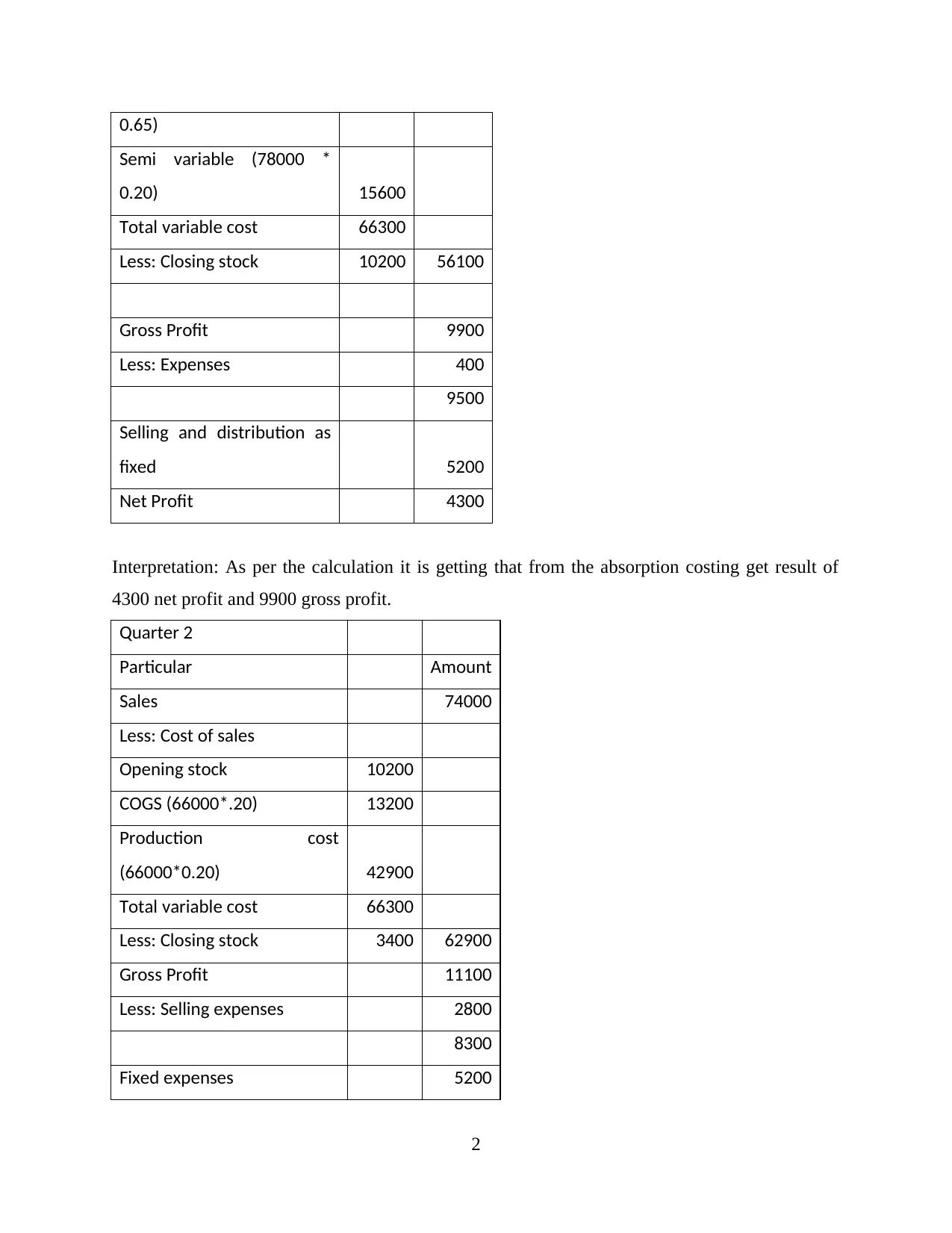

0.65)

Semi variable (78000 *

0.20) 15600

Total variable cost 66300

Less: Closing stock 10200 56100

Gross Profit 9900

Less: Expenses 400

9500

Selling and distribution as

fixed 5200

Net Profit 4300

Interpretation: As per the calculation it is getting that from the absorption costing get result of

4300 net profit and 9900 gross profit.

Quarter 2

Particular Amount

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*.20) 13200

Production cost

(66000*0.20) 42900

Total variable cost 66300

Less: Closing stock 3400 62900

Gross Profit 11100

Less: Selling expenses 2800

8300

Fixed expenses 5200

2

Semi variable (78000 *

0.20) 15600

Total variable cost 66300

Less: Closing stock 10200 56100

Gross Profit 9900

Less: Expenses 400

9500

Selling and distribution as

fixed 5200

Net Profit 4300

Interpretation: As per the calculation it is getting that from the absorption costing get result of

4300 net profit and 9900 gross profit.

Quarter 2

Particular Amount

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*.20) 13200

Production cost

(66000*0.20) 42900

Total variable cost 66300

Less: Closing stock 3400 62900

Gross Profit 11100

Less: Selling expenses 2800

8300

Fixed expenses 5200

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net profit 3100

Reconciliation

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Marginal Technique: This is the ascertainment, by defining the difference between fixed

cost and variable cost. In marginal costing, costing are mainly classified in to fixed and variable

cost. It focuses on different elements like office and administration expenditure, selling and

distribution and manufacturing expenses that defines cost of production. It helps to make profit

plan with the help of break even charts and profit graphs. It helps to make profit plan with the

help of break even charts and profit graphs (Hilton and Platt, 2013). In Prime furniture applied

this method to calculate the net profit with the helps to contribution.

Quarter 1

Particulars Amount

Sales 66000

Less: Cost of sales

Opening inventory 0

Production cost

(780000*0.65) 50700

Less: Closing stock

(12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

3

Reconciliation

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Marginal Technique: This is the ascertainment, by defining the difference between fixed

cost and variable cost. In marginal costing, costing are mainly classified in to fixed and variable

cost. It focuses on different elements like office and administration expenditure, selling and

distribution and manufacturing expenses that defines cost of production. It helps to make profit

plan with the help of break even charts and profit graphs. It helps to make profit plan with the

help of break even charts and profit graphs (Hilton and Platt, 2013). In Prime furniture applied

this method to calculate the net profit with the helps to contribution.

Quarter 1

Particulars Amount

Sales 66000

Less: Cost of sales

Opening inventory 0

Production cost

(780000*0.65) 50700

Less: Closing stock

(12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

3

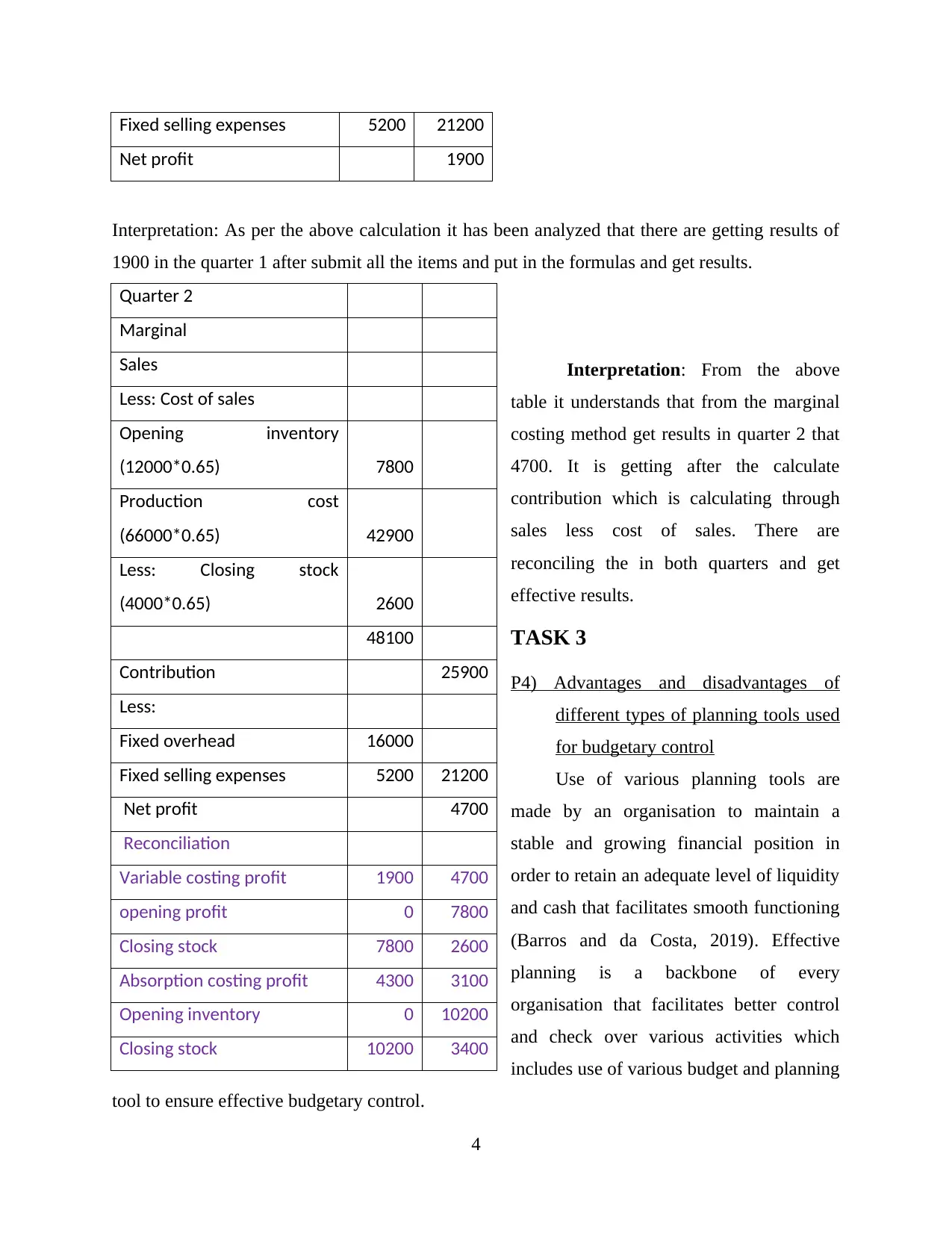

Fixed selling expenses 5200 21200

Net profit 1900

Interpretation: As per the above calculation it has been analyzed that there are getting results of

1900 in the quarter 1 after submit all the items and put in the formulas and get results.

Interpretation: From the above

table it understands that from the marginal

costing method get results in quarter 2 that

4700. It is getting after the calculate

contribution which is calculating through

sales less cost of sales. There are

reconciling the in both quarters and get

effective results.

TASK 3

P4) Advantages and disadvantages of

different types of planning tools used

for budgetary control

Use of various planning tools are

made by an organisation to maintain a

stable and growing financial position in

order to retain an adequate level of liquidity

and cash that facilitates smooth functioning

(Barros and da Costa, 2019). Effective

planning is a backbone of every

organisation that facilitates better control

and check over various activities which

includes use of various budget and planning

tool to ensure effective budgetary control.

4

Quarter 2

Marginal

Sales

Less: Cost of sales

Opening inventory

(12000*0.65) 7800

Production cost

(66000*0.65) 42900

Less: Closing stock

(4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed selling expenses 5200 21200

Net profit 4700

Reconciliation

Variable costing profit 1900 4700

opening profit 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Net profit 1900

Interpretation: As per the above calculation it has been analyzed that there are getting results of

1900 in the quarter 1 after submit all the items and put in the formulas and get results.

Interpretation: From the above

table it understands that from the marginal

costing method get results in quarter 2 that

4700. It is getting after the calculate

contribution which is calculating through

sales less cost of sales. There are

reconciling the in both quarters and get

effective results.

TASK 3

P4) Advantages and disadvantages of

different types of planning tools used

for budgetary control

Use of various planning tools are

made by an organisation to maintain a

stable and growing financial position in

order to retain an adequate level of liquidity

and cash that facilitates smooth functioning

(Barros and da Costa, 2019). Effective

planning is a backbone of every

organisation that facilitates better control

and check over various activities which

includes use of various budget and planning

tool to ensure effective budgetary control.

4

Quarter 2

Marginal

Sales

Less: Cost of sales

Opening inventory

(12000*0.65) 7800

Production cost

(66000*0.65) 42900

Less: Closing stock

(4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed selling expenses 5200 21200

Net profit 4700

Reconciliation

Variable costing profit 1900 4700

opening profit 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

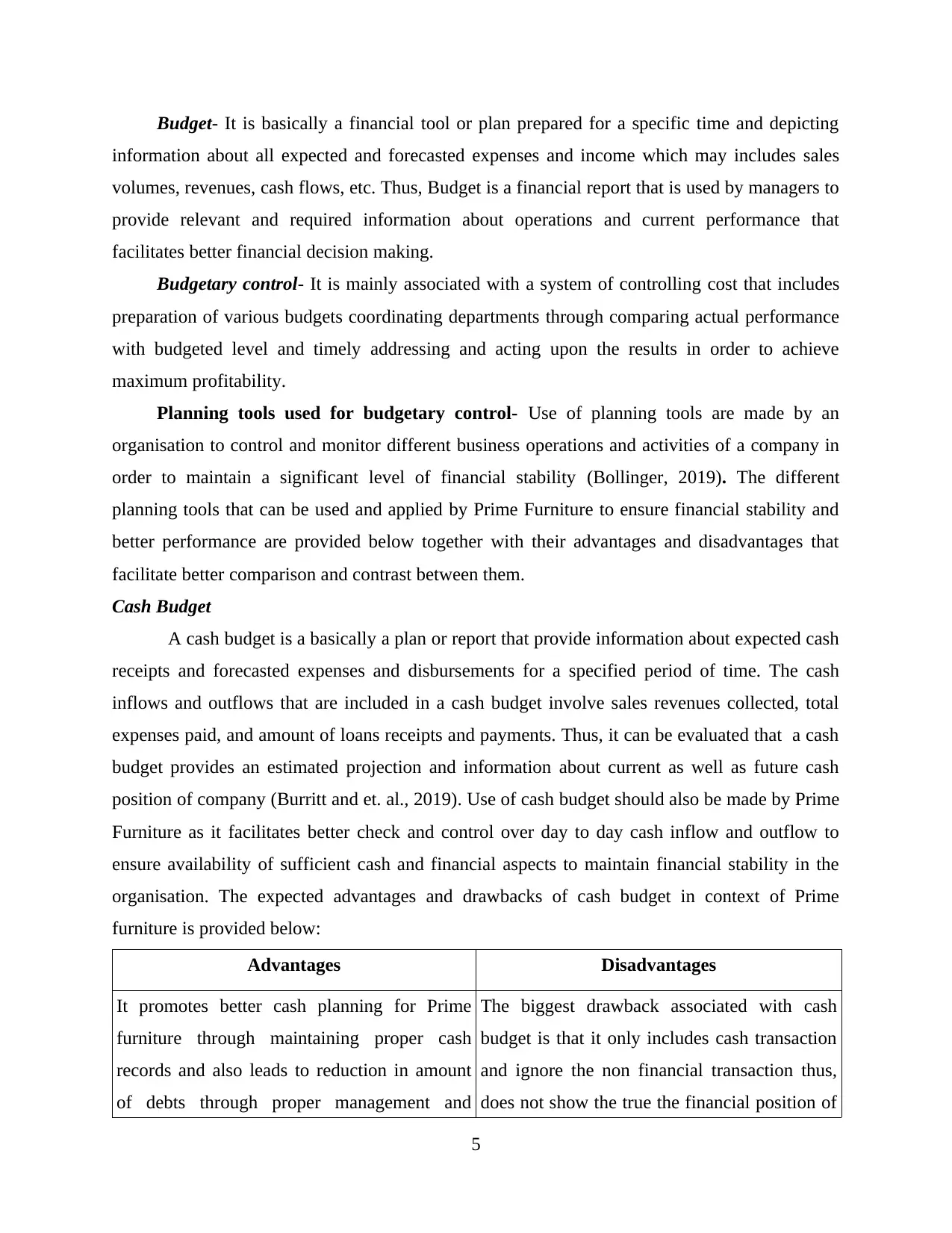

Budget- It is basically a financial tool or plan prepared for a specific time and depicting

information about all expected and forecasted expenses and income which may includes sales

volumes, revenues, cash flows, etc. Thus, Budget is a financial report that is used by managers to

provide relevant and required information about operations and current performance that

facilitates better financial decision making.

Budgetary control- It is mainly associated with a system of controlling cost that includes

preparation of various budgets coordinating departments through comparing actual performance

with budgeted level and timely addressing and acting upon the results in order to achieve

maximum profitability.

Planning tools used for budgetary control- Use of planning tools are made by an

organisation to control and monitor different business operations and activities of a company in

order to maintain a significant level of financial stability (Bollinger, 2019). The different

planning tools that can be used and applied by Prime Furniture to ensure financial stability and

better performance are provided below together with their advantages and disadvantages that

facilitate better comparison and contrast between them.

Cash Budget

A cash budget is a basically a plan or report that provide information about expected cash

receipts and forecasted expenses and disbursements for a specified period of time. The cash

inflows and outflows that are included in a cash budget involve sales revenues collected, total

expenses paid, and amount of loans receipts and payments. Thus, it can be evaluated that a cash

budget provides an estimated projection and information about current as well as future cash

position of company (Burritt and et. al., 2019). Use of cash budget should also be made by Prime

Furniture as it facilitates better check and control over day to day cash inflow and outflow to

ensure availability of sufficient cash and financial aspects to maintain financial stability in the

organisation. The expected advantages and drawbacks of cash budget in context of Prime

furniture is provided below:

Advantages Disadvantages

It promotes better cash planning for Prime

furniture through maintaining proper cash

records and also leads to reduction in amount

of debts through proper management and

The biggest drawback associated with cash

budget is that it only includes cash transaction

and ignore the non financial transaction thus,

does not show the true the financial position of

5

information about all expected and forecasted expenses and income which may includes sales

volumes, revenues, cash flows, etc. Thus, Budget is a financial report that is used by managers to

provide relevant and required information about operations and current performance that

facilitates better financial decision making.

Budgetary control- It is mainly associated with a system of controlling cost that includes

preparation of various budgets coordinating departments through comparing actual performance

with budgeted level and timely addressing and acting upon the results in order to achieve

maximum profitability.

Planning tools used for budgetary control- Use of planning tools are made by an

organisation to control and monitor different business operations and activities of a company in

order to maintain a significant level of financial stability (Bollinger, 2019). The different

planning tools that can be used and applied by Prime Furniture to ensure financial stability and

better performance are provided below together with their advantages and disadvantages that

facilitate better comparison and contrast between them.

Cash Budget

A cash budget is a basically a plan or report that provide information about expected cash

receipts and forecasted expenses and disbursements for a specified period of time. The cash

inflows and outflows that are included in a cash budget involve sales revenues collected, total

expenses paid, and amount of loans receipts and payments. Thus, it can be evaluated that a cash

budget provides an estimated projection and information about current as well as future cash

position of company (Burritt and et. al., 2019). Use of cash budget should also be made by Prime

Furniture as it facilitates better check and control over day to day cash inflow and outflow to

ensure availability of sufficient cash and financial aspects to maintain financial stability in the

organisation. The expected advantages and drawbacks of cash budget in context of Prime

furniture is provided below:

Advantages Disadvantages

It promotes better cash planning for Prime

furniture through maintaining proper cash

records and also leads to reduction in amount

of debts through proper management and

The biggest drawback associated with cash

budget is that it only includes cash transaction

and ignore the non financial transaction thus,

does not show the true the financial position of

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

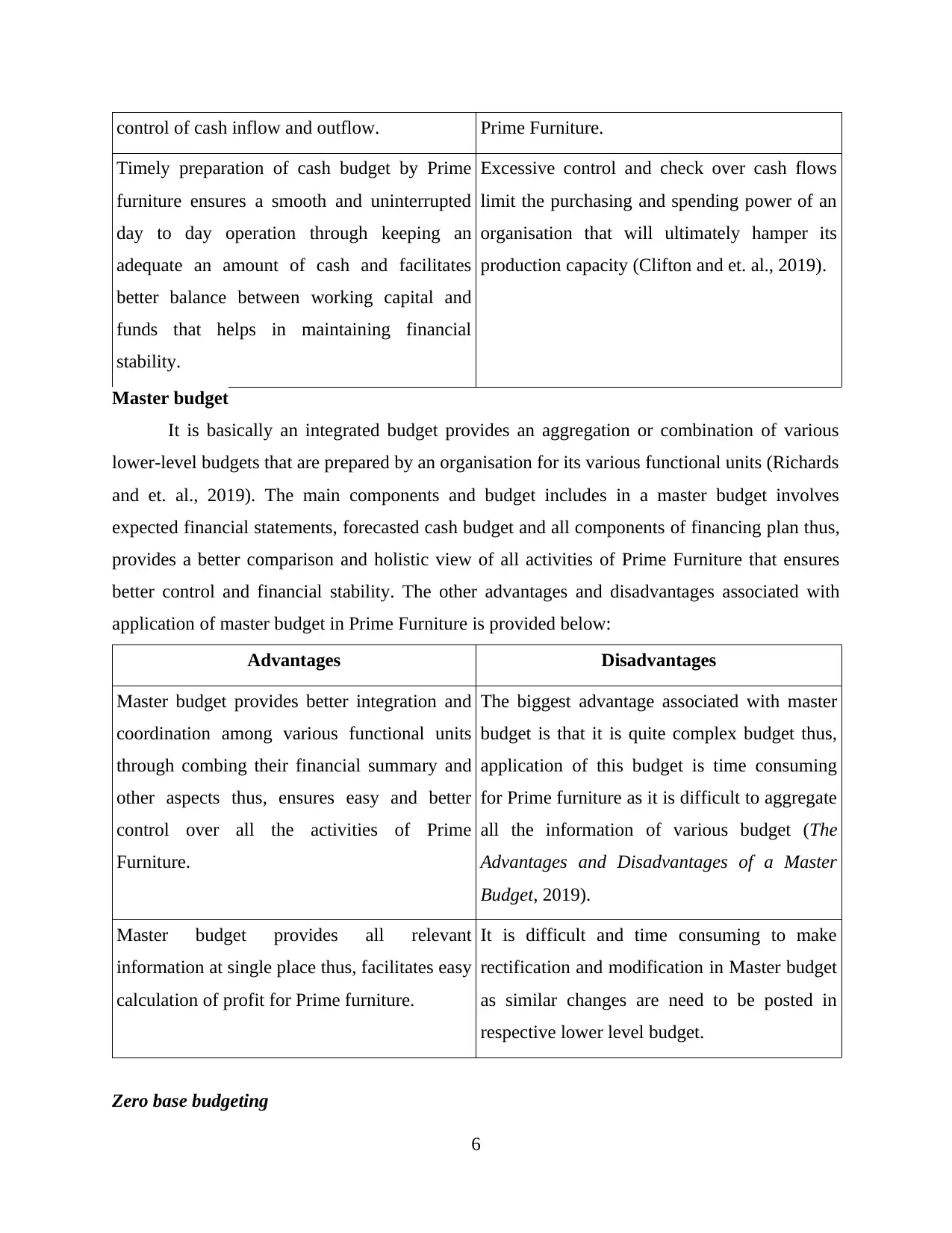

control of cash inflow and outflow. Prime Furniture.

Timely preparation of cash budget by Prime

furniture ensures a smooth and uninterrupted

day to day operation through keeping an

adequate an amount of cash and facilitates

better balance between working capital and

funds that helps in maintaining financial

stability.

Excessive control and check over cash flows

limit the purchasing and spending power of an

organisation that will ultimately hamper its

production capacity (Clifton and et. al., 2019).

Master budget

It is basically an integrated budget provides an aggregation or combination of various

lower-level budgets that are prepared by an organisation for its various functional units (Richards

and et. al., 2019). The main components and budget includes in a master budget involves

expected financial statements, forecasted cash budget and all components of financing plan thus,

provides a better comparison and holistic view of all activities of Prime Furniture that ensures

better control and financial stability. The other advantages and disadvantages associated with

application of master budget in Prime Furniture is provided below:

Advantages Disadvantages

Master budget provides better integration and

coordination among various functional units

through combing their financial summary and

other aspects thus, ensures easy and better

control over all the activities of Prime

Furniture.

The biggest advantage associated with master

budget is that it is quite complex budget thus,

application of this budget is time consuming

for Prime furniture as it is difficult to aggregate

all the information of various budget (The

Advantages and Disadvantages of a Master

Budget, 2019).

Master budget provides all relevant

information at single place thus, facilitates easy

calculation of profit for Prime furniture.

It is difficult and time consuming to make

rectification and modification in Master budget

as similar changes are need to be posted in

respective lower level budget.

Zero base budgeting

6

Timely preparation of cash budget by Prime

furniture ensures a smooth and uninterrupted

day to day operation through keeping an

adequate an amount of cash and facilitates

better balance between working capital and

funds that helps in maintaining financial

stability.

Excessive control and check over cash flows

limit the purchasing and spending power of an

organisation that will ultimately hamper its

production capacity (Clifton and et. al., 2019).

Master budget

It is basically an integrated budget provides an aggregation or combination of various

lower-level budgets that are prepared by an organisation for its various functional units (Richards

and et. al., 2019). The main components and budget includes in a master budget involves

expected financial statements, forecasted cash budget and all components of financing plan thus,

provides a better comparison and holistic view of all activities of Prime Furniture that ensures

better control and financial stability. The other advantages and disadvantages associated with

application of master budget in Prime Furniture is provided below:

Advantages Disadvantages

Master budget provides better integration and

coordination among various functional units

through combing their financial summary and

other aspects thus, ensures easy and better

control over all the activities of Prime

Furniture.

The biggest advantage associated with master

budget is that it is quite complex budget thus,

application of this budget is time consuming

for Prime furniture as it is difficult to aggregate

all the information of various budget (The

Advantages and Disadvantages of a Master

Budget, 2019).

Master budget provides all relevant

information at single place thus, facilitates easy

calculation of profit for Prime furniture.

It is difficult and time consuming to make

rectification and modification in Master budget

as similar changes are need to be posted in

respective lower level budget.

Zero base budgeting

6

It is a method or process of budgeting in which a justification is required before making

any expenses each new period as this budget assumes to starts from a "zero base," and starch

level and operation and expense is analyzed on the basis of its needs and costs to make better

decision (Saona and Muro, 2018). Use of Zero base budgeting can be applied by Prime Furniture

as it facilitates better and strategic decision making on the basis of current requirements and

circumstances thus, ensures better financial stability and control. The other advantages and

disadvantages associated with use of zero base budgeting are provided below in context of Prime

furniture:

Advantages Disadvantages

It improves the overall efficiency of Prime

furniture through facilitating better decisions

making on the basis of current circumstances

irrespective of past facts and figure.

Highly trained and well educated mangers are

required to prepare Zero base budget thus, it is

an expensive tool.

Use of zero base budgeting by Prime Furniture

ensure better check and control over expenses

as proper verified justification is required for

making any expense and also ensure improved

allocation of income thus, facilitates better

financial stability.

This budget streets firm starch or zero level and

justification is required for all expenses, thus, it

is time consuming process to apply zero base

budgeting in Prime furniture.

TASK 4

P5) Effectiveness of management accounting systems to respond on financial problems

Financial problems are mainly associated with the situation when organisation face

difficulties in meeting and managing its day to day expenses due to lack of funds or shortage of

cash supply (Scott and et. al.,2018). The various financial problems that are faced by Prime

furniture and creating a financial instability are as follows:

Late payment by customers- Prime furniture is facing difficulties in getting turnover

payments from customers and clients to whom credit was offered that has created difficulty in

maintain adequate amount of finance and cash to met its day to day operation.

7

any expenses each new period as this budget assumes to starts from a "zero base," and starch

level and operation and expense is analyzed on the basis of its needs and costs to make better

decision (Saona and Muro, 2018). Use of Zero base budgeting can be applied by Prime Furniture

as it facilitates better and strategic decision making on the basis of current requirements and

circumstances thus, ensures better financial stability and control. The other advantages and

disadvantages associated with use of zero base budgeting are provided below in context of Prime

furniture:

Advantages Disadvantages

It improves the overall efficiency of Prime

furniture through facilitating better decisions

making on the basis of current circumstances

irrespective of past facts and figure.

Highly trained and well educated mangers are

required to prepare Zero base budget thus, it is

an expensive tool.

Use of zero base budgeting by Prime Furniture

ensure better check and control over expenses

as proper verified justification is required for

making any expense and also ensure improved

allocation of income thus, facilitates better

financial stability.

This budget streets firm starch or zero level and

justification is required for all expenses, thus, it

is time consuming process to apply zero base

budgeting in Prime furniture.

TASK 4

P5) Effectiveness of management accounting systems to respond on financial problems

Financial problems are mainly associated with the situation when organisation face

difficulties in meeting and managing its day to day expenses due to lack of funds or shortage of

cash supply (Scott and et. al.,2018). The various financial problems that are faced by Prime

furniture and creating a financial instability are as follows:

Late payment by customers- Prime furniture is facing difficulties in getting turnover

payments from customers and clients to whom credit was offered that has created difficulty in

maintain adequate amount of finance and cash to met its day to day operation.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

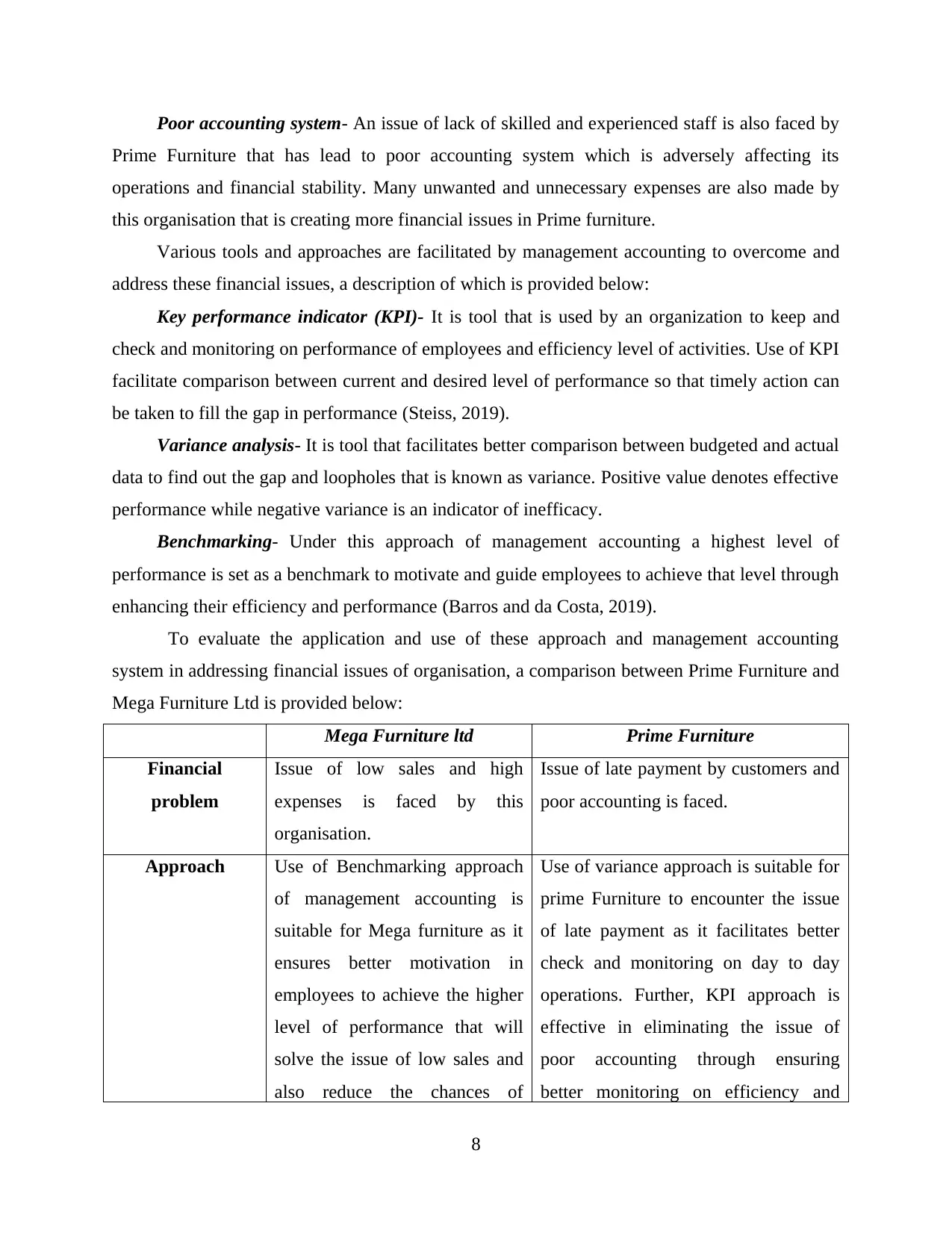

Poor accounting system- An issue of lack of skilled and experienced staff is also faced by

Prime Furniture that has lead to poor accounting system which is adversely affecting its

operations and financial stability. Many unwanted and unnecessary expenses are also made by

this organisation that is creating more financial issues in Prime furniture.

Various tools and approaches are facilitated by management accounting to overcome and

address these financial issues, a description of which is provided below:

Key performance indicator (KPI)- It is tool that is used by an organization to keep and

check and monitoring on performance of employees and efficiency level of activities. Use of KPI

facilitate comparison between current and desired level of performance so that timely action can

be taken to fill the gap in performance (Steiss, 2019).

Variance analysis- It is tool that facilitates better comparison between budgeted and actual

data to find out the gap and loopholes that is known as variance. Positive value denotes effective

performance while negative variance is an indicator of inefficacy.

Benchmarking- Under this approach of management accounting a highest level of

performance is set as a benchmark to motivate and guide employees to achieve that level through

enhancing their efficiency and performance (Barros and da Costa, 2019).

To evaluate the application and use of these approach and management accounting

system in addressing financial issues of organisation, a comparison between Prime Furniture and

Mega Furniture Ltd is provided below:

Mega Furniture ltd Prime Furniture

Financial

problem

Issue of low sales and high

expenses is faced by this

organisation.

Issue of late payment by customers and

poor accounting is faced.

Approach Use of Benchmarking approach

of management accounting is

suitable for Mega furniture as it

ensures better motivation in

employees to achieve the higher

level of performance that will

solve the issue of low sales and

also reduce the chances of

Use of variance approach is suitable for

prime Furniture to encounter the issue

of late payment as it facilitates better

check and monitoring on day to day

operations. Further, KPI approach is

effective in eliminating the issue of

poor accounting through ensuring

better monitoring on efficiency and

8

Prime Furniture that has lead to poor accounting system which is adversely affecting its

operations and financial stability. Many unwanted and unnecessary expenses are also made by

this organisation that is creating more financial issues in Prime furniture.

Various tools and approaches are facilitated by management accounting to overcome and

address these financial issues, a description of which is provided below:

Key performance indicator (KPI)- It is tool that is used by an organization to keep and

check and monitoring on performance of employees and efficiency level of activities. Use of KPI

facilitate comparison between current and desired level of performance so that timely action can

be taken to fill the gap in performance (Steiss, 2019).

Variance analysis- It is tool that facilitates better comparison between budgeted and actual

data to find out the gap and loopholes that is known as variance. Positive value denotes effective

performance while negative variance is an indicator of inefficacy.

Benchmarking- Under this approach of management accounting a highest level of

performance is set as a benchmark to motivate and guide employees to achieve that level through

enhancing their efficiency and performance (Barros and da Costa, 2019).

To evaluate the application and use of these approach and management accounting

system in addressing financial issues of organisation, a comparison between Prime Furniture and

Mega Furniture Ltd is provided below:

Mega Furniture ltd Prime Furniture

Financial

problem

Issue of low sales and high

expenses is faced by this

organisation.

Issue of late payment by customers and

poor accounting is faced.

Approach Use of Benchmarking approach

of management accounting is

suitable for Mega furniture as it

ensures better motivation in

employees to achieve the higher

level of performance that will

solve the issue of low sales and

also reduce the chances of

Use of variance approach is suitable for

prime Furniture to encounter the issue

of late payment as it facilitates better

check and monitoring on day to day

operations. Further, KPI approach is

effective in eliminating the issue of

poor accounting through ensuring

better monitoring on efficiency and

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

wasteful expenses through

enhancing efficiency of

operations.

performance of employees (Bollinger,

2019).

Management

accounting

system

Use of prise optimisation system

is suitable for Mega Furniture

Ltd as it lead to better pricing of

products to cater and attract

larger customers to solve the

issue of low sales.

Use of cost accounting system is

suitable for Prime Furniture as it

facilitates better control over all income

and expenses through maintaining

proper record. It also yield a better tool

for employees to improve their

accounting skills and knowledge to

keep better check and control over

expenses.

Management accounting and their importance

Management accounting departments among all companies use various forms of records

for income reporting purposes. Business organization’s managers make strategic decisions about

financial and non-financial results. It is essential for organizations to better manage the

transactions by accumulating bookkeeping data and making remedial business decisions. It

considers as an inner framework that actually makes money by implementing various forms of

accounting management method (Fadzil and Rababah, 2012). It is utilized for the short term as

well as long term decisions in which consist of all financial health of a business. It supports a

manager in make operational decisions intended to supports increase the organization’s

performance that also supports in shorter as well as longer investment decision. The prime

furniture apply this accounting to take help in long tern investment activities in proper manner.

CONCLUSION

As per the above report is understanding that management accounting can provide all the

specific information through accounts and reports in order to take right decision. It is required to

understand the importance of MA because it helps to top executives to take shorter and longer

investment decision. There are taking different tools like zero, cash and many others to prepare

budget that guide for future activities and accordingly take further steps for get success. Along

with identify different problem that identify in the business after that apply effective tools like

9

enhancing efficiency of

operations.

performance of employees (Bollinger,

2019).

Management

accounting

system

Use of prise optimisation system

is suitable for Mega Furniture

Ltd as it lead to better pricing of

products to cater and attract

larger customers to solve the

issue of low sales.

Use of cost accounting system is

suitable for Prime Furniture as it

facilitates better control over all income

and expenses through maintaining

proper record. It also yield a better tool

for employees to improve their

accounting skills and knowledge to

keep better check and control over

expenses.

Management accounting and their importance

Management accounting departments among all companies use various forms of records

for income reporting purposes. Business organization’s managers make strategic decisions about

financial and non-financial results. It is essential for organizations to better manage the

transactions by accumulating bookkeeping data and making remedial business decisions. It

considers as an inner framework that actually makes money by implementing various forms of

accounting management method (Fadzil and Rababah, 2012). It is utilized for the short term as

well as long term decisions in which consist of all financial health of a business. It supports a

manager in make operational decisions intended to supports increase the organization’s

performance that also supports in shorter as well as longer investment decision. The prime

furniture apply this accounting to take help in long tern investment activities in proper manner.

CONCLUSION

As per the above report is understanding that management accounting can provide all the

specific information through accounts and reports in order to take right decision. It is required to

understand the importance of MA because it helps to top executives to take shorter and longer

investment decision. There are taking different tools like zero, cash and many others to prepare

budget that guide for future activities and accordingly take further steps for get success. Along

with identify different problem that identify in the business after that apply effective tools like

9

KPI and benchmarking to recognize in the business. To sort out these problems apply effective

systems then compare with other organisation to select right strategy.

REFERENCES

Books and journal

Arroyo, P., 2012. Management accounting change and sustainability: an institutional

approach. Journal of Accounting & Organizational Change. 8(3). pp.286-309.

Barros, R. S. and da Costa, A. M. D. S., 2019. Bridging management control systems and

innovation. Qualitative Research in Accounting & Management.

Bollinger, S. R., 2019. Creativity and forms of managerial control in innovation processes: tools,

viewpoints and practices. European Journal of Innovation Management.

Burritt, R. L., and et. al., 2019. Diffusion of environmental management accounting for cleaner

production: Evidence from some case studies. Journal of Cleaner Production. 224.

pp.479-491.

Clifton, M. B and et. al., 2019. Target costing: market driven product design. CRC Press

Fadzil, F. H. B. and Rababah, A., 2012. Management accounting change: ABC adoption and

implementation. Journal of Accounting and Auditing. 2012. p.1.

Grabner, I. and Moers, F., 2013. Management control as a system or a package? Conceptual and

empirical issues. Accounting, Organizations and Society. 38(6-7). pp.407-419.

Hilton, R. W. and Platt, D. E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Richards, G., and et. al., 2019. Business intelligence effectiveness and corporate performance

management: an empirical analysis. Journal of Computer Information Systems. 59(2).

pp.188-196.

Saona, P. and Muro, L., 2018. Firm-and Country-level attributes as determinants of earnings

management: an analysis for Latin American firms. Emerging Markets Finance and

Trade. 54(12). pp.2736-2764.

10

systems then compare with other organisation to select right strategy.

REFERENCES

Books and journal

Arroyo, P., 2012. Management accounting change and sustainability: an institutional

approach. Journal of Accounting & Organizational Change. 8(3). pp.286-309.

Barros, R. S. and da Costa, A. M. D. S., 2019. Bridging management control systems and

innovation. Qualitative Research in Accounting & Management.

Bollinger, S. R., 2019. Creativity and forms of managerial control in innovation processes: tools,

viewpoints and practices. European Journal of Innovation Management.

Burritt, R. L., and et. al., 2019. Diffusion of environmental management accounting for cleaner

production: Evidence from some case studies. Journal of Cleaner Production. 224.

pp.479-491.

Clifton, M. B and et. al., 2019. Target costing: market driven product design. CRC Press

Fadzil, F. H. B. and Rababah, A., 2012. Management accounting change: ABC adoption and

implementation. Journal of Accounting and Auditing. 2012. p.1.

Grabner, I. and Moers, F., 2013. Management control as a system or a package? Conceptual and

empirical issues. Accounting, Organizations and Society. 38(6-7). pp.407-419.

Hilton, R. W. and Platt, D. E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Richards, G., and et. al., 2019. Business intelligence effectiveness and corporate performance

management: an empirical analysis. Journal of Computer Information Systems. 59(2).

pp.188-196.

Saona, P. and Muro, L., 2018. Firm-and Country-level attributes as determinants of earnings

management: an analysis for Latin American firms. Emerging Markets Finance and

Trade. 54(12). pp.2736-2764.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.