Management Accounting

VerifiedAdded on 2023/03/30

|13

|3576

|388

AI Summary

This assignment focuses on the concept of management accounting and its importance in decision-making. It analyzes the value chain of Woolworths Group Limited and discusses the procurement and operations processes of the organization. It also explores the competitive strategies adopted by Woolworths to gain a sustainable competitive advantage in the supermarket industry.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MANAGEMENT ACCOUNTING

Table of Contents

Introduction:..................................................................................................................2

Question 1:...................................................................................................................2

Requirement a:..........................................................................................................2

Requirement b:..........................................................................................................3

Part i:.....................................................................................................................3

Part ii:.....................................................................................................................3

Part iii:....................................................................................................................5

Part iv:...................................................................................................................5

Part v:....................................................................................................................7

Question 2:...................................................................................................................7

Requirement a:..........................................................................................................7

Requirement b:..........................................................................................................7

Requirement c:..........................................................................................................7

Requirement d:..........................................................................................................7

Requirement e:..........................................................................................................8

Question 3:...................................................................................................................8

Requirement a:..........................................................................................................8

Requirement b:..........................................................................................................8

Requirement c:..........................................................................................................9

Conclusion:...................................................................................................................9

References:................................................................................................................11

Table of Contents

Introduction:..................................................................................................................2

Question 1:...................................................................................................................2

Requirement a:..........................................................................................................2

Requirement b:..........................................................................................................3

Part i:.....................................................................................................................3

Part ii:.....................................................................................................................3

Part iii:....................................................................................................................5

Part iv:...................................................................................................................5

Part v:....................................................................................................................7

Question 2:...................................................................................................................7

Requirement a:..........................................................................................................7

Requirement b:..........................................................................................................7

Requirement c:..........................................................................................................7

Requirement d:..........................................................................................................7

Requirement e:..........................................................................................................8

Question 3:...................................................................................................................8

Requirement a:..........................................................................................................8

Requirement b:..........................................................................................................8

Requirement c:..........................................................................................................9

Conclusion:...................................................................................................................9

References:................................................................................................................11

2MANAGEMENT ACCOUNTING

Introduction:

In the current era, accounting is utilised in the form of a tool in evaluation of

business and its associated activities. There are different ways of presenting

accounting information so that the users of such information are assisted to gain an

understanding of the analysis. One accounting type is identified as management

accounting, which implies the presentation of evaluation of business activities to the

internal management for facilitating in decision-making (Alsharari, Dixon and

Youssef 2015). The current assignment is divided into three sections. The first

section would focus on analysing the value chain of an ASX listed organisation. For

this reason, Woolworths Group Limited is taken into consideration. The second

segment would emphasise on overhead allocation in the context of Prime Personal

Trainers, which provides personal training services to the people in Belgium. Finally,

the assignment would shed light on identifying and evaluating the cost pools for

Maleluka Council that owns animal shelter and provides different services.

Question 1:

Requirement a:

Value chain could be defined as a continuous procedure of accumulating,

analysing and communicating information to undertake decisions along with

assisting the organisation in identifying the value-creating process and activities

within the business. By using value chain, it becomes possible for the organisation to

identify the primary activities as well as the support activities through which value

would be created (Ax and Greve 2017). The primary activities are deemed to have

direct association with sales, production, marketing, service and delivery. They take

the shape of operations, outbound logistics, inbound logistics, sales, marketing and

after-sales services. However, the primary activities could not work alone. A helping

hand is required from the supporting activities for full maximisation of customer

value. Some instances of support activities mainly include procurement, human

resource management, technology development and organisational infrastructure

(Bobryshev et al. 2015).

There are certain ways through which value chain concept adds benefit to an

organisation, two of which are discussed below:

Low cost advantage:

By using value chain analysis, an organisation could identify the activities that

create value for the organisation and those unable to add value to the organisation.

By analysing the value-creating activities, it becomes possible for the organisation to

develop the cost drivers for all processes (Porter and Kramer 2019). Thus, it

provides the scope for cost improvement strategies to be enforced along with

maintaining customer value. After this, it becomes possible to detect those areas

having minimised cost of access to raw materials, innovative process technology or

distribution channels.

Differentiation:

By using value chain analysis, an organisation would be able to contrast its

activities with those of the rivals. By comparing own actions with those of the rivals,

the organisation would be able to concentrate on the perceived value of the

customers towards the products and services along with analysing differentiation

strategies such as marketing channels, pricing, product features, service support and

Introduction:

In the current era, accounting is utilised in the form of a tool in evaluation of

business and its associated activities. There are different ways of presenting

accounting information so that the users of such information are assisted to gain an

understanding of the analysis. One accounting type is identified as management

accounting, which implies the presentation of evaluation of business activities to the

internal management for facilitating in decision-making (Alsharari, Dixon and

Youssef 2015). The current assignment is divided into three sections. The first

section would focus on analysing the value chain of an ASX listed organisation. For

this reason, Woolworths Group Limited is taken into consideration. The second

segment would emphasise on overhead allocation in the context of Prime Personal

Trainers, which provides personal training services to the people in Belgium. Finally,

the assignment would shed light on identifying and evaluating the cost pools for

Maleluka Council that owns animal shelter and provides different services.

Question 1:

Requirement a:

Value chain could be defined as a continuous procedure of accumulating,

analysing and communicating information to undertake decisions along with

assisting the organisation in identifying the value-creating process and activities

within the business. By using value chain, it becomes possible for the organisation to

identify the primary activities as well as the support activities through which value

would be created (Ax and Greve 2017). The primary activities are deemed to have

direct association with sales, production, marketing, service and delivery. They take

the shape of operations, outbound logistics, inbound logistics, sales, marketing and

after-sales services. However, the primary activities could not work alone. A helping

hand is required from the supporting activities for full maximisation of customer

value. Some instances of support activities mainly include procurement, human

resource management, technology development and organisational infrastructure

(Bobryshev et al. 2015).

There are certain ways through which value chain concept adds benefit to an

organisation, two of which are discussed below:

Low cost advantage:

By using value chain analysis, an organisation could identify the activities that

create value for the organisation and those unable to add value to the organisation.

By analysing the value-creating activities, it becomes possible for the organisation to

develop the cost drivers for all processes (Porter and Kramer 2019). Thus, it

provides the scope for cost improvement strategies to be enforced along with

maintaining customer value. After this, it becomes possible to detect those areas

having minimised cost of access to raw materials, innovative process technology or

distribution channels.

Differentiation:

By using value chain analysis, an organisation would be able to contrast its

activities with those of the rivals. By comparing own actions with those of the rivals,

the organisation would be able to concentrate on the perceived value of the

customers towards the products and services along with analysing differentiation

strategies such as marketing channels, pricing, product features, service support and

3MANAGEMENT ACCOUNTING

others to maximise customer value (Holweg and Helo 2014). This would assist the

organisation in finding out innovative methods for conducting value-adding activities

leading to enhanced overall performance as well as competitive supremacy.

Thus, the value chain concept is a highly flexible strategy for looking at the

business operations, the competitors and the respective areas in the value chain

system of the sector. This assists in having an in-depth knowledge of the

organisational issues engaged with the promise to make customer value

commitments and promises, since it concentrates attention on the activities required

in order provide the value proposition (Boučková 2015).

Requirement b:

In this section, Woolworths Group Limited is selected as the organisation, which

operates retail stores in Australia and New Zealand. It is established in the year 1924 and its

current employee base stands at around 201,522.

Part i:

Woolworths believes in earning the trust of the customers along with

respecting service responsiveness both internal and external of its store operations

along with enabling them to undertake informed health, ethical and environmental

decisions. As a part of its mission statement, the focus has been kept on producing

and providing superior products to the Australian customers

(Woolworthsgroup.com.au 2019).

On the other hand, the objectives of Woolworths have been to enhance stock

returns and optimise network efficiency while assuring that its customers served by

above 800 stores found on virtually in every main street of Australia find in-stock the

value for money products, as per their expectations. For this, the organisation has

undertaken significant investment in its supply chain management systems that

affect all areas of the business (Woolworthsgroup.com.au 2019).

Part ii:

There are three generic strategies that an organisation could use for

accomplishing competitive edge along with ensuring sustained growth. These

include cost leadership, differentiation and focus. Cost leadership is dependent on

developing low-cost position in relation to the peers of an organisation. By using this

strategy, the organisation could manage the relationships across the entire value

chain by remaining devoted to lowering costs across the overall chain (Carlsson-

Wall, Kraus and Lind 2015). Differentiation needs an organisation to develop

products and services, which are unique and the customers value them. Focus

involves identification of a market segment based on which emphasis needs to be

placed on that segment (Chenhall and Moers 2015).

Woolworths is observed to adopt integrated competitive strategy by using a

mix of both cost leadership and differentiation strategies, in search for sustainable

competitive edge over the competitors in the supermarket sector. According to

Hopper and Bui (2016), it is possible for an organisation to outperform its

competitors only, if it could develop a difference that could be preserved effectively.

In case of Woolworths, there are certain important competencies identified that

makes the organisation as one of the leaders in the supermarket industry and they

are elucidated as follows:

World-class supply chain:

The innovation and competitive edge of Woolworths have been developed

with the help of its supply chain. The efficient distribution network of the organisation

others to maximise customer value (Holweg and Helo 2014). This would assist the

organisation in finding out innovative methods for conducting value-adding activities

leading to enhanced overall performance as well as competitive supremacy.

Thus, the value chain concept is a highly flexible strategy for looking at the

business operations, the competitors and the respective areas in the value chain

system of the sector. This assists in having an in-depth knowledge of the

organisational issues engaged with the promise to make customer value

commitments and promises, since it concentrates attention on the activities required

in order provide the value proposition (Boučková 2015).

Requirement b:

In this section, Woolworths Group Limited is selected as the organisation, which

operates retail stores in Australia and New Zealand. It is established in the year 1924 and its

current employee base stands at around 201,522.

Part i:

Woolworths believes in earning the trust of the customers along with

respecting service responsiveness both internal and external of its store operations

along with enabling them to undertake informed health, ethical and environmental

decisions. As a part of its mission statement, the focus has been kept on producing

and providing superior products to the Australian customers

(Woolworthsgroup.com.au 2019).

On the other hand, the objectives of Woolworths have been to enhance stock

returns and optimise network efficiency while assuring that its customers served by

above 800 stores found on virtually in every main street of Australia find in-stock the

value for money products, as per their expectations. For this, the organisation has

undertaken significant investment in its supply chain management systems that

affect all areas of the business (Woolworthsgroup.com.au 2019).

Part ii:

There are three generic strategies that an organisation could use for

accomplishing competitive edge along with ensuring sustained growth. These

include cost leadership, differentiation and focus. Cost leadership is dependent on

developing low-cost position in relation to the peers of an organisation. By using this

strategy, the organisation could manage the relationships across the entire value

chain by remaining devoted to lowering costs across the overall chain (Carlsson-

Wall, Kraus and Lind 2015). Differentiation needs an organisation to develop

products and services, which are unique and the customers value them. Focus

involves identification of a market segment based on which emphasis needs to be

placed on that segment (Chenhall and Moers 2015).

Woolworths is observed to adopt integrated competitive strategy by using a

mix of both cost leadership and differentiation strategies, in search for sustainable

competitive edge over the competitors in the supermarket sector. According to

Hopper and Bui (2016), it is possible for an organisation to outperform its

competitors only, if it could develop a difference that could be preserved effectively.

In case of Woolworths, there are certain important competencies identified that

makes the organisation as one of the leaders in the supermarket industry and they

are elucidated as follows:

World-class supply chain:

The innovation and competitive edge of Woolworths have been developed

with the help of its supply chain. The efficient distribution network of the organisation

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MANAGEMENT ACCOUNTING

is considered as a resource as well as capability in its outbound and inbound

logistics. It has focused on efficiency and cost reduction to manage unessential

expenditures. A mix of tangible and intangible assets like supplier relationships and

technological capabilities is significantly useful, since it contributes to considerable

cost minimisation across the entire logistics network of Woolworths

(Woolworthsgroup.com.au 2019). The extent of cost saving advantages provided by

the effective supply chain is not substitutable by other resources and it is difficult to

imitate, since the scope and level of technological capabilities engaged is highly

staggering and specialised.

Branding and market position:

The store positioning has been made by Woolworths with the slogan of “The

Fresh Food People” developing a differentiated quality image and healthy range of

products at affordable prices. The consumers have sound experience with the

products, which is mainly due to strong procedures of quality assessment across the

supply chain (Kaplan and Atkinson 2015). Currently, 95% of fresh fruits and

vegetables and 100% of fresh meat are from the producers of Australia

(Woolworthsgroup.com.au 2019). Such brand reputation is valuable, since it assists

in providing meaningful differentiation to the rivals and as a result, there has been

increase in the level of customer satisfaction.

Innovation:

There are different innovative projects made by Woolworths like “new idea”,

“re-fresh” and “petrol retailing”. In addition, it has initiated “everyday money” credit

card by collaborating with MasterCard and HSBC Bank (Woolworthsgroup.com.au

2019). Furthermore, various convenience programs and consumer rewards are

initiated by the organisation, which include “everyday money shopping cards” and

“everyday rewards”. Such innovation in products and offerings could be clearly seen

as a competitive edge of Woolworths over its rivals.

Integration:

Vertical integration of some its supplies is conducted by Woolworths by

manufacturing its own inputs so that market power could be increased and

accordingly, it could respond to the trend of the private label. With the help of such

integration, it has availability of vast array of products under the brand of

“Woolworths Select” intending to provide consistent superior quality

(Woolworthsgroup.com.au 2019).

Marketing and sales:

The marketing strategy of Woolworths is its significant strength that has

assisted the organisation in differentiating its products along with ensuring its

position as one of the biggest retailers in Australia. The organisation incurs more on

marketing expenses via newspapers, television, distributed leaflets and magazines.

These sales and marketing activities of Woolworths have contributed to the fresh

food image along with successful brand awareness accomplished by the

organisation (Woolworthsgroup.com.au 2019).

is considered as a resource as well as capability in its outbound and inbound

logistics. It has focused on efficiency and cost reduction to manage unessential

expenditures. A mix of tangible and intangible assets like supplier relationships and

technological capabilities is significantly useful, since it contributes to considerable

cost minimisation across the entire logistics network of Woolworths

(Woolworthsgroup.com.au 2019). The extent of cost saving advantages provided by

the effective supply chain is not substitutable by other resources and it is difficult to

imitate, since the scope and level of technological capabilities engaged is highly

staggering and specialised.

Branding and market position:

The store positioning has been made by Woolworths with the slogan of “The

Fresh Food People” developing a differentiated quality image and healthy range of

products at affordable prices. The consumers have sound experience with the

products, which is mainly due to strong procedures of quality assessment across the

supply chain (Kaplan and Atkinson 2015). Currently, 95% of fresh fruits and

vegetables and 100% of fresh meat are from the producers of Australia

(Woolworthsgroup.com.au 2019). Such brand reputation is valuable, since it assists

in providing meaningful differentiation to the rivals and as a result, there has been

increase in the level of customer satisfaction.

Innovation:

There are different innovative projects made by Woolworths like “new idea”,

“re-fresh” and “petrol retailing”. In addition, it has initiated “everyday money” credit

card by collaborating with MasterCard and HSBC Bank (Woolworthsgroup.com.au

2019). Furthermore, various convenience programs and consumer rewards are

initiated by the organisation, which include “everyday money shopping cards” and

“everyday rewards”. Such innovation in products and offerings could be clearly seen

as a competitive edge of Woolworths over its rivals.

Integration:

Vertical integration of some its supplies is conducted by Woolworths by

manufacturing its own inputs so that market power could be increased and

accordingly, it could respond to the trend of the private label. With the help of such

integration, it has availability of vast array of products under the brand of

“Woolworths Select” intending to provide consistent superior quality

(Woolworthsgroup.com.au 2019).

Marketing and sales:

The marketing strategy of Woolworths is its significant strength that has

assisted the organisation in differentiating its products along with ensuring its

position as one of the biggest retailers in Australia. The organisation incurs more on

marketing expenses via newspapers, television, distributed leaflets and magazines.

These sales and marketing activities of Woolworths have contributed to the fresh

food image along with successful brand awareness accomplished by the

organisation (Woolworthsgroup.com.au 2019).

5MANAGEMENT ACCOUNTING

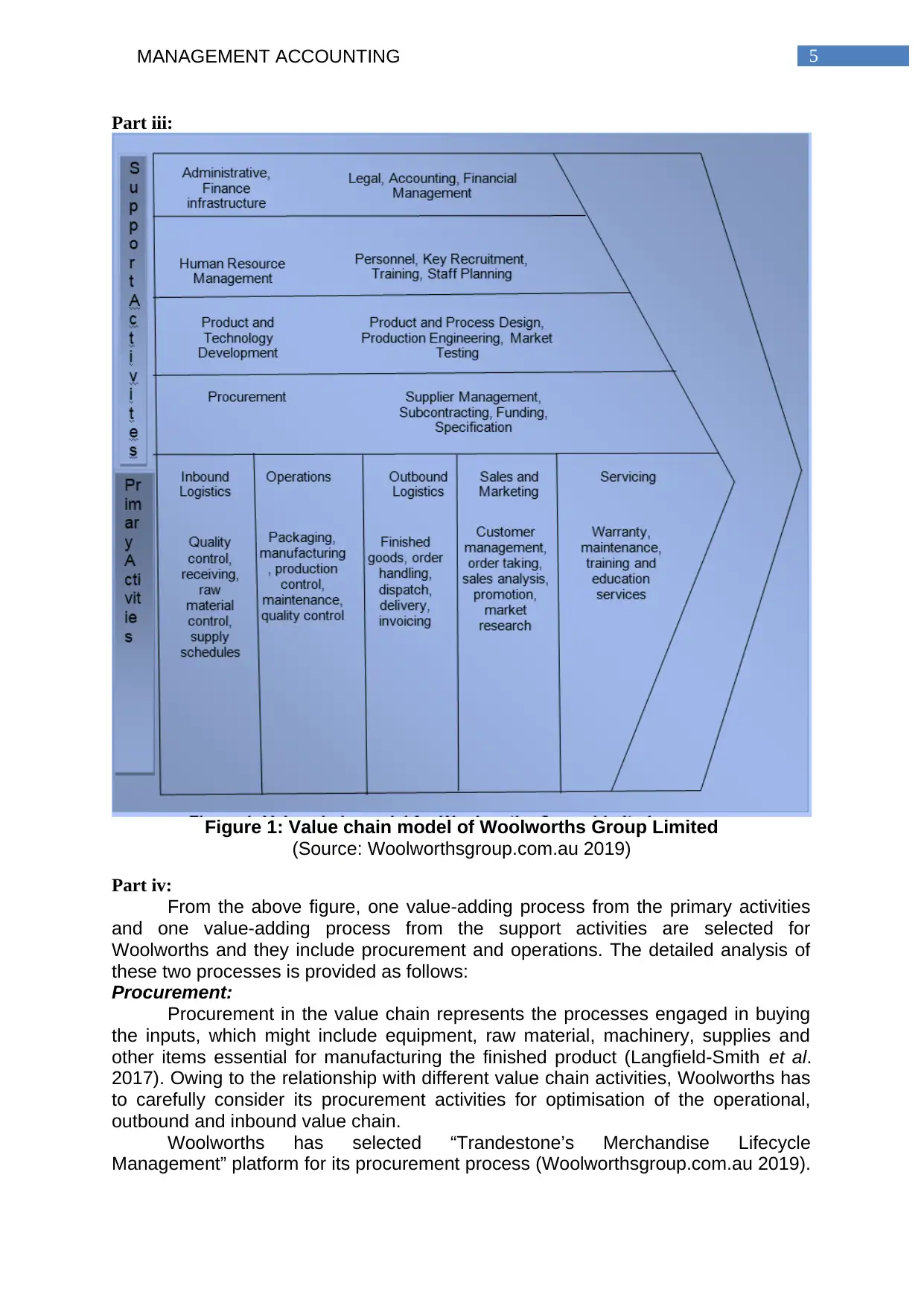

Part iii:

Figure 1: Value chain model of Woolworths Group Limited

(Source: Woolworthsgroup.com.au 2019)

Part iv:

From the above figure, one value-adding process from the primary activities

and one value-adding process from the support activities are selected for

Woolworths and they include procurement and operations. The detailed analysis of

these two processes is provided as follows:

Procurement:

Procurement in the value chain represents the processes engaged in buying

the inputs, which might include equipment, raw material, machinery, supplies and

other items essential for manufacturing the finished product (Langfield-Smith et al.

2017). Owing to the relationship with different value chain activities, Woolworths has

to carefully consider its procurement activities for optimisation of the operational,

outbound and inbound value chain.

Woolworths has selected “Trandestone’s Merchandise Lifecycle

Management” platform for its procurement process (Woolworthsgroup.com.au 2019).

Part iii:

Figure 1: Value chain model of Woolworths Group Limited

(Source: Woolworthsgroup.com.au 2019)

Part iv:

From the above figure, one value-adding process from the primary activities

and one value-adding process from the support activities are selected for

Woolworths and they include procurement and operations. The detailed analysis of

these two processes is provided as follows:

Procurement:

Procurement in the value chain represents the processes engaged in buying

the inputs, which might include equipment, raw material, machinery, supplies and

other items essential for manufacturing the finished product (Langfield-Smith et al.

2017). Owing to the relationship with different value chain activities, Woolworths has

to carefully consider its procurement activities for optimisation of the operational,

outbound and inbound value chain.

Woolworths has selected “Trandestone’s Merchandise Lifecycle

Management” platform for its procurement process (Woolworthsgroup.com.au 2019).

6MANAGEMENT ACCOUNTING

This provides a platform for the organisations to handle orders and suppliers,

business to business sales and financing. It links with above 6,000 suppliers.

Woolworths follows a strong process of certification when it comes to choosing the

suppliers. In terms of product quality assurance, the organisation is involved in

auditing its products before they are sold to the customers. On the other hand, it has

adopted the nationalisation of buying activities to the goal at fulfilling considerable

cost savings. With the help of this process, the consumers obtain superior quality

products at affordable prices, since the procurement system has allowed the

organisation in condensing costs by $2.5 billion (Woolworthsgroup.com.au 2019). In

addition to this, Woolworths has integrated its delivery network system by engaging

sound transport system and distribution centres into the same. In this manner, the

organisation has the better position of avoiding strikes of the staffs while having

better control to ensure its shipment activities (Lavia López and Hiebl 2014).

Furthermore, the operation via the centres of distribution and trucks in the supply

chain assists the organisation in maintaining optimum distribution efficiency as well

as the product quality.

Operations:

This section contains two primary activities, which assure the convenience of

the customers and value coupled with inventory management and quality

assessment. Woolworths is involved in maintaining standardised procedures for

identifying and eliminating the products from the delivery lots, which are obtained

from the suppliers. From the time the retail store receives the stocks to when the

products are displayed on the store shelves, the staffs working in the quality

assurance department are engaged in time-to-time checks for identifying and

removing the defective products (Woolworthsgroup.com.au 2019). Moreover, it is

observed to maintain “Minimum Presentation Level” for its stock keeping units

(SKUs). In this context, it is noteworthy to mention that space planning is necessary

to ensure the success of any retail store (Melnyk et al. 2014). Therefore, this

innovative process is used by Woolworths so that it could present the assortment in

different striking ways by often using plan-o-grams for depicting the minimum

presentation quantity.

Besides, the “Sophisticated Point of Sale” technology assists Woolworths in

maintaining track of the total SKUs sold for a particular item and at the time the stock

levels go below the M.P.L, the re-stocking order is dispatched to the corresponding

distribution centre. In this manner, the organisation is utilising its store space

optimally resulting in enhanced quality of products, as the quality check officers

immediately notice the defective products (Messner 2016). By using the POS

system, Woolworths is no longer needed to use the conventional cash register

system, since this system offers information regarding the customers and existing

inventory. By using enterprise data interface technology, Woolworths is involved in

maintaining error-free information regarding its business inventories. With the help of

this system, the user could have clear information about the purchase orders,

documents related to scheduling agreements, schedule line categories, types of

sales documents and others (Nielsen and Roslender 2015). By obtaining all pertinent

information, effectiveness could be witnessed in the inventory management system

of Woolworths. As a result, it never encountered a situation such as empty shelves

or unavailability of merchandise; thereby, making the customers reluctant in visiting

the stores in future.

This provides a platform for the organisations to handle orders and suppliers,

business to business sales and financing. It links with above 6,000 suppliers.

Woolworths follows a strong process of certification when it comes to choosing the

suppliers. In terms of product quality assurance, the organisation is involved in

auditing its products before they are sold to the customers. On the other hand, it has

adopted the nationalisation of buying activities to the goal at fulfilling considerable

cost savings. With the help of this process, the consumers obtain superior quality

products at affordable prices, since the procurement system has allowed the

organisation in condensing costs by $2.5 billion (Woolworthsgroup.com.au 2019). In

addition to this, Woolworths has integrated its delivery network system by engaging

sound transport system and distribution centres into the same. In this manner, the

organisation has the better position of avoiding strikes of the staffs while having

better control to ensure its shipment activities (Lavia López and Hiebl 2014).

Furthermore, the operation via the centres of distribution and trucks in the supply

chain assists the organisation in maintaining optimum distribution efficiency as well

as the product quality.

Operations:

This section contains two primary activities, which assure the convenience of

the customers and value coupled with inventory management and quality

assessment. Woolworths is involved in maintaining standardised procedures for

identifying and eliminating the products from the delivery lots, which are obtained

from the suppliers. From the time the retail store receives the stocks to when the

products are displayed on the store shelves, the staffs working in the quality

assurance department are engaged in time-to-time checks for identifying and

removing the defective products (Woolworthsgroup.com.au 2019). Moreover, it is

observed to maintain “Minimum Presentation Level” for its stock keeping units

(SKUs). In this context, it is noteworthy to mention that space planning is necessary

to ensure the success of any retail store (Melnyk et al. 2014). Therefore, this

innovative process is used by Woolworths so that it could present the assortment in

different striking ways by often using plan-o-grams for depicting the minimum

presentation quantity.

Besides, the “Sophisticated Point of Sale” technology assists Woolworths in

maintaining track of the total SKUs sold for a particular item and at the time the stock

levels go below the M.P.L, the re-stocking order is dispatched to the corresponding

distribution centre. In this manner, the organisation is utilising its store space

optimally resulting in enhanced quality of products, as the quality check officers

immediately notice the defective products (Messner 2016). By using the POS

system, Woolworths is no longer needed to use the conventional cash register

system, since this system offers information regarding the customers and existing

inventory. By using enterprise data interface technology, Woolworths is involved in

maintaining error-free information regarding its business inventories. With the help of

this system, the user could have clear information about the purchase orders,

documents related to scheduling agreements, schedule line categories, types of

sales documents and others (Nielsen and Roslender 2015). By obtaining all pertinent

information, effectiveness could be witnessed in the inventory management system

of Woolworths. As a result, it never encountered a situation such as empty shelves

or unavailability of merchandise; thereby, making the customers reluctant in visiting

the stores in future.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

Part v:

It needs to be mentioned that the theories learned about the value chain

concept have provided immense assistance in linking the same with the real case

scenario of Woolworths Group Limited. One value-adding process from the primary

activities and one value-adding process from the support activities are selected for

Woolworths and they include procurement and operations. In theory, it has been

learnt that Procurement in the value chain represents the processes engaged in

buying the inputs, which might include equipment, raw material, machinery, supplies

and other items essential for manufacturing the finished product. In terms of

operations, it has been learnt that it contains two primary activities, which assure the

convenience of the customers and value coupled with inventory management and

quality assessment. By using these theoretical concepts, it has become possible to

conduct the value chain analysis of Woolworths effectively.

Question 2:

Requirement a:

Particulars Details Values

Estimated variable overhead A $150,000

Estimated direct labour cost B $ 75,000

Fixed overhead C $120,000

Direct labour hours D 3,000

Variable overhead rate as

proportion of direct labour cost E=A/B 200%

Fixed overhead rate F=C/D $ 40

Requirement b:

Particulars Details Values

Variable overhead rate A 200%

Direct labour cost B $ 250

Fixed overhead rate C $ 40

Direct labour hours D 10

Overhead cost allocated to Job

20 E=(AxB)+(CxD) $ 900

Requirement c:

Particulars Details Values

Equipment and supplies cost A $ 1,000

Direct labour cost B $ 250

Overhead applied C $ 900

Total cost of Job 20 D=A+B+C $ 2,150

Requirement d:

Particulars Details Values

Total direct labour cost A $ 5,725

Part v:

It needs to be mentioned that the theories learned about the value chain

concept have provided immense assistance in linking the same with the real case

scenario of Woolworths Group Limited. One value-adding process from the primary

activities and one value-adding process from the support activities are selected for

Woolworths and they include procurement and operations. In theory, it has been

learnt that Procurement in the value chain represents the processes engaged in

buying the inputs, which might include equipment, raw material, machinery, supplies

and other items essential for manufacturing the finished product. In terms of

operations, it has been learnt that it contains two primary activities, which assure the

convenience of the customers and value coupled with inventory management and

quality assessment. By using these theoretical concepts, it has become possible to

conduct the value chain analysis of Woolworths effectively.

Question 2:

Requirement a:

Particulars Details Values

Estimated variable overhead A $150,000

Estimated direct labour cost B $ 75,000

Fixed overhead C $120,000

Direct labour hours D 3,000

Variable overhead rate as

proportion of direct labour cost E=A/B 200%

Fixed overhead rate F=C/D $ 40

Requirement b:

Particulars Details Values

Variable overhead rate A 200%

Direct labour cost B $ 250

Fixed overhead rate C $ 40

Direct labour hours D 10

Overhead cost allocated to Job

20 E=(AxB)+(CxD) $ 900

Requirement c:

Particulars Details Values

Equipment and supplies cost A $ 1,000

Direct labour cost B $ 250

Overhead applied C $ 900

Total cost of Job 20 D=A+B+C $ 2,150

Requirement d:

Particulars Details Values

Total direct labour cost A $ 5,725

8MANAGEMENT ACCOUNTING

Variable overhead rate B 200%

Total direct labour hours C 229

Fixed overhead rate D $ 40

Allocation of variable overhead E=AxB $ 11,450

Allocation of fixed overhead F=CxD $ 9,160

Total overhead allocation G=E+F $ 20,610

Requirement e:

It is necessary to use two cost pools for the accountant of Prime Personal

Trainers, instead of one, so that the product cost information is accurate. The

allocation bases used for each department would be realistic in representing the

linkage between the product and overhead costs, instead of using a single plant-

wide rate (Pavlatos and Kostakis 2015). On the contrary, the use of departmental

overhead rates requires the distribution of overhead expenses to the departments,

the allocation of expenses of the support departments to the production departments

and the collection of cost driver data by the production departments. Even though

useful information could be obtained from this approach than the single cost pool,

the expenses are more and there are chances of obtaining misleading information as

well (Tappura et al. 2015). Despite such drawbacks, the method is still deemed to be

superior when it comes to product costing and cost allocation.

The method could result in a difference, since the use of activities varies for

each overhead activity. Moreover, the overhead allocation would be made

depending on direct labour hours or direct labour cost (Shields 2015). Hence, if

additional equipment is used, there would be lower labour usage and minimised

overhead allocation resulting in lower cost.

Question 3:

Requirement a:

As commented by Salterio (2015), cost pool signifies the grouping of

individual costs into a class depending on cost centre or department. The same is

utilised for assigning costs to the cost units. Based on the provided information of

Malekula Council, the organisation provides three types of services that constitute of

the following:

Animal training services

Housing services to the stray dogs

Animal healthcare services

Hence, it is possible to classify costs into three cost pools based on the cost

objects. Such costs primarily constitute of animal shelter expenses, healthcare

service costs and training costs.

Requirement b:

When there is combined collection of indirect expenses, the same is identified

as overhead costs. All such cost components depend on specific activities, which are

deemed to be the cost drivers (Van Der Stede 2015). By analysing the cost structure

of the provided organisation, the cost drivers for the identified cost pools are number

of animal days, training classes attended and number of animal visits.

Variable overhead rate B 200%

Total direct labour hours C 229

Fixed overhead rate D $ 40

Allocation of variable overhead E=AxB $ 11,450

Allocation of fixed overhead F=CxD $ 9,160

Total overhead allocation G=E+F $ 20,610

Requirement e:

It is necessary to use two cost pools for the accountant of Prime Personal

Trainers, instead of one, so that the product cost information is accurate. The

allocation bases used for each department would be realistic in representing the

linkage between the product and overhead costs, instead of using a single plant-

wide rate (Pavlatos and Kostakis 2015). On the contrary, the use of departmental

overhead rates requires the distribution of overhead expenses to the departments,

the allocation of expenses of the support departments to the production departments

and the collection of cost driver data by the production departments. Even though

useful information could be obtained from this approach than the single cost pool,

the expenses are more and there are chances of obtaining misleading information as

well (Tappura et al. 2015). Despite such drawbacks, the method is still deemed to be

superior when it comes to product costing and cost allocation.

The method could result in a difference, since the use of activities varies for

each overhead activity. Moreover, the overhead allocation would be made

depending on direct labour hours or direct labour cost (Shields 2015). Hence, if

additional equipment is used, there would be lower labour usage and minimised

overhead allocation resulting in lower cost.

Question 3:

Requirement a:

As commented by Salterio (2015), cost pool signifies the grouping of

individual costs into a class depending on cost centre or department. The same is

utilised for assigning costs to the cost units. Based on the provided information of

Malekula Council, the organisation provides three types of services that constitute of

the following:

Animal training services

Housing services to the stray dogs

Animal healthcare services

Hence, it is possible to classify costs into three cost pools based on the cost

objects. Such costs primarily constitute of animal shelter expenses, healthcare

service costs and training costs.

Requirement b:

When there is combined collection of indirect expenses, the same is identified

as overhead costs. All such cost components depend on specific activities, which are

deemed to be the cost drivers (Van Der Stede 2015). By analysing the cost structure

of the provided organisation, the cost drivers for the identified cost pools are number

of animal days, training classes attended and number of animal visits.

9MANAGEMENT ACCOUNTING

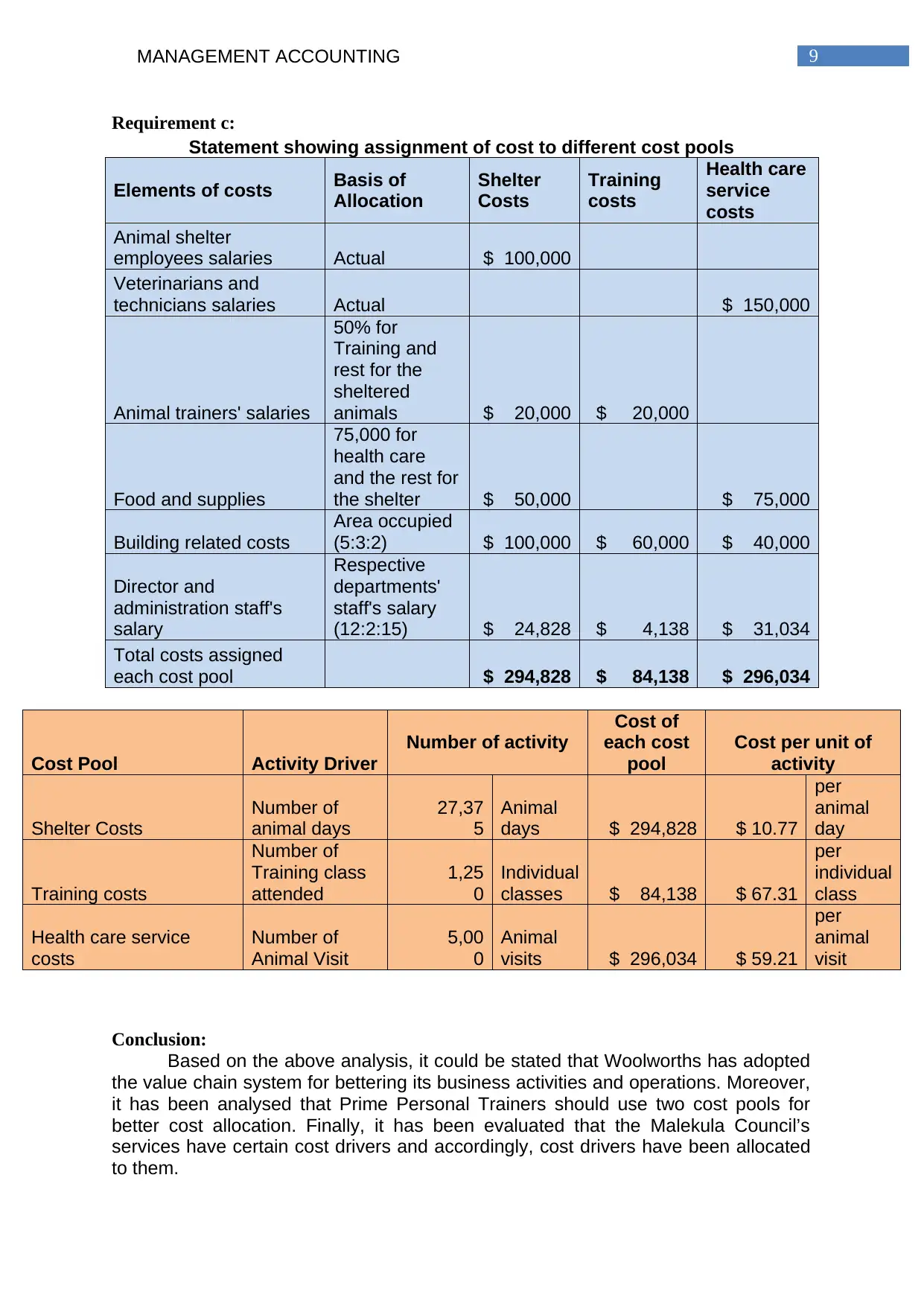

Requirement c:

Statement showing assignment of cost to different cost pools

Elements of costs Basis of

Allocation

Shelter

Costs

Training

costs

Health care

service

costs

Animal shelter

employees salaries Actual $ 100,000

Veterinarians and

technicians salaries Actual $ 150,000

Animal trainers' salaries

50% for

Training and

rest for the

sheltered

animals $ 20,000 $ 20,000

Food and supplies

75,000 for

health care

and the rest for

the shelter $ 50,000 $ 75,000

Building related costs

Area occupied

(5:3:2) $ 100,000 $ 60,000 $ 40,000

Director and

administration staff's

salary

Respective

departments'

staff's salary

(12:2:15) $ 24,828 $ 4,138 $ 31,034

Total costs assigned

each cost pool $ 294,828 $ 84,138 $ 296,034

Cost Pool Activity Driver

Number of activity

Cost of

each cost

pool

Cost per unit of

activity

Shelter Costs

Number of

animal days

27,37

5

Animal

days $ 294,828 $ 10.77

per

animal

day

Training costs

Number of

Training class

attended

1,25

0

Individual

classes $ 84,138 $ 67.31

per

individual

class

Health care service

costs

Number of

Animal Visit

5,00

0

Animal

visits $ 296,034 $ 59.21

per

animal

visit

Conclusion:

Based on the above analysis, it could be stated that Woolworths has adopted

the value chain system for bettering its business activities and operations. Moreover,

it has been analysed that Prime Personal Trainers should use two cost pools for

better cost allocation. Finally, it has been evaluated that the Malekula Council’s

services have certain cost drivers and accordingly, cost drivers have been allocated

to them.

Requirement c:

Statement showing assignment of cost to different cost pools

Elements of costs Basis of

Allocation

Shelter

Costs

Training

costs

Health care

service

costs

Animal shelter

employees salaries Actual $ 100,000

Veterinarians and

technicians salaries Actual $ 150,000

Animal trainers' salaries

50% for

Training and

rest for the

sheltered

animals $ 20,000 $ 20,000

Food and supplies

75,000 for

health care

and the rest for

the shelter $ 50,000 $ 75,000

Building related costs

Area occupied

(5:3:2) $ 100,000 $ 60,000 $ 40,000

Director and

administration staff's

salary

Respective

departments'

staff's salary

(12:2:15) $ 24,828 $ 4,138 $ 31,034

Total costs assigned

each cost pool $ 294,828 $ 84,138 $ 296,034

Cost Pool Activity Driver

Number of activity

Cost of

each cost

pool

Cost per unit of

activity

Shelter Costs

Number of

animal days

27,37

5

Animal

days $ 294,828 $ 10.77

per

animal

day

Training costs

Number of

Training class

attended

1,25

0

Individual

classes $ 84,138 $ 67.31

per

individual

class

Health care service

costs

Number of

Animal Visit

5,00

0

Animal

visits $ 296,034 $ 59.21

per

animal

visit

Conclusion:

Based on the above analysis, it could be stated that Woolworths has adopted

the value chain system for bettering its business activities and operations. Moreover,

it has been analysed that Prime Personal Trainers should use two cost pools for

better cost allocation. Finally, it has been evaluated that the Malekula Council’s

services have certain cost drivers and accordingly, cost drivers have been allocated

to them.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10MANAGEMENT ACCOUNTING

11MANAGEMENT ACCOUNTING

References:

Alsharari, N.M., Dixon, R. and Youssef, M.A.E.A., 2015. Management accounting

change: critical review and a new contextual framework. Journal of Accounting &

Organizational Change, 11(4), pp.476-502.

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations:

Organizational culture compatibility and perceived outcomes. Management

Accounting Research, 34, pp.59-74.

Bobryshev, A.N., Tatarinova, M.N., Grishanova, S.V. and Frolov, A.V.E., 2015.

Management accounting in Russia: problems of theoretical study and practical

application in the economic crisis. Journal of Advanced Research in Law and

Economics, 6(3 (13)), p.511.

Boučková, M., 2015. Management accounting and agency theory. Procedia

Economics and Finance, 25, pp.5-13.

Carlsson-Wall, M., Kraus, K. and Lind, J., 2015. Strategic management accounting in

close inter-organisational relationships. Accounting and Business Research, 45(1),

pp.27-54.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of

management accounting and its integration into management control. Accounting,

organizations and society, 47, pp.1-13.

Holweg, M. and Helo, P., 2014. Defining value chain architectures: Linking strategic

value creation to operational supply chain design. International Journal of Production

Economics, 147, pp.230-238.

Hopper, T. and Bui, B., 2016. Has management accounting research been

critical?. Management Accounting Research, 31, pp.10-30.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI

Learning.

Langfield-Smith, K., Smith, D., Andon, P., Hilton, R. and Thorne, H.,

2017. Management accounting: Information for creating and managing value.

McGraw-Hill Education Australia.

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and

medium-sized enterprises: current knowledge and avenues for further

research. Journal of Management Accounting Research, 27(1), pp.81-119.

Melnyk, S.A., Bititci, U., Platts, K., Tobias, J. and Andersen, B., 2014. Is performance

measurement and management fit for the future?. Management Accounting

Research, 25(2), pp.173-186.

Messner, M., 2016. Does industry matter? How industry context shapes

management accounting practice. Management Accounting Research, 31, pp.103-

111.

Nielsen, C. and Roslender, R., 2015. Enhancing financial reporting: The contribution

of business models. The British Accounting Review, 47(3), pp.262-274.

Otley, D., 2016. The contingency theory of management accounting and control:

1980–2014. Management accounting research, 31, pp.45-62.

Pavlatos, O. and Kostakis, H., 2015. Management accounting practices before and

during economic crisis: Evidence from Greece. Advances in accounting, 31(1),

pp.150-164.

Porter, M.E. and Kramer, M.R., 2019. Creating shared value. In Managing

sustainable business (pp. 323-346). Springer, Dordrecht.

References:

Alsharari, N.M., Dixon, R. and Youssef, M.A.E.A., 2015. Management accounting

change: critical review and a new contextual framework. Journal of Accounting &

Organizational Change, 11(4), pp.476-502.

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations:

Organizational culture compatibility and perceived outcomes. Management

Accounting Research, 34, pp.59-74.

Bobryshev, A.N., Tatarinova, M.N., Grishanova, S.V. and Frolov, A.V.E., 2015.

Management accounting in Russia: problems of theoretical study and practical

application in the economic crisis. Journal of Advanced Research in Law and

Economics, 6(3 (13)), p.511.

Boučková, M., 2015. Management accounting and agency theory. Procedia

Economics and Finance, 25, pp.5-13.

Carlsson-Wall, M., Kraus, K. and Lind, J., 2015. Strategic management accounting in

close inter-organisational relationships. Accounting and Business Research, 45(1),

pp.27-54.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of

management accounting and its integration into management control. Accounting,

organizations and society, 47, pp.1-13.

Holweg, M. and Helo, P., 2014. Defining value chain architectures: Linking strategic

value creation to operational supply chain design. International Journal of Production

Economics, 147, pp.230-238.

Hopper, T. and Bui, B., 2016. Has management accounting research been

critical?. Management Accounting Research, 31, pp.10-30.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI

Learning.

Langfield-Smith, K., Smith, D., Andon, P., Hilton, R. and Thorne, H.,

2017. Management accounting: Information for creating and managing value.

McGraw-Hill Education Australia.

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and

medium-sized enterprises: current knowledge and avenues for further

research. Journal of Management Accounting Research, 27(1), pp.81-119.

Melnyk, S.A., Bititci, U., Platts, K., Tobias, J. and Andersen, B., 2014. Is performance

measurement and management fit for the future?. Management Accounting

Research, 25(2), pp.173-186.

Messner, M., 2016. Does industry matter? How industry context shapes

management accounting practice. Management Accounting Research, 31, pp.103-

111.

Nielsen, C. and Roslender, R., 2015. Enhancing financial reporting: The contribution

of business models. The British Accounting Review, 47(3), pp.262-274.

Otley, D., 2016. The contingency theory of management accounting and control:

1980–2014. Management accounting research, 31, pp.45-62.

Pavlatos, O. and Kostakis, H., 2015. Management accounting practices before and

during economic crisis: Evidence from Greece. Advances in accounting, 31(1),

pp.150-164.

Porter, M.E. and Kramer, M.R., 2019. Creating shared value. In Managing

sustainable business (pp. 323-346). Springer, Dordrecht.

12MANAGEMENT ACCOUNTING

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research, 31, pp.118-122.

Salterio, S.E., 2015. Barriers to knowledge creation in management accounting

research. Journal of Management Accounting Research, 27(1), pp.151-170.

Shields, M.D., 2015. Established management accounting knowledge. Journal of

Management Accounting Research, 27(1), pp.123-132.

Tappura, S., Sievänen, M., Heikkilä, J., Jussila, A. and Nenonen, N., 2015. A

management accounting perspective on safety. Safety science, 71, pp.151-159.

Van Der Stede, W.A., 2015. Management accounting: Where from, where now,

where to?. Journal of Management Accounting Research, 27(1), pp.171-176.

Woolworthsgroup.com.au., 2019. [online] Available at:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

[Accessed 2 Jun. 2019].

Woolworthsgroup.com.au., 2019. Strategy and objectives - Woolworths Group.

[online] Available at: https://www.woolworthsgroup.com.au/page/about-us/our-

approach/strategy-and-objectives/ [Accessed 2 Jun. 2019].

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research, 31, pp.118-122.

Salterio, S.E., 2015. Barriers to knowledge creation in management accounting

research. Journal of Management Accounting Research, 27(1), pp.151-170.

Shields, M.D., 2015. Established management accounting knowledge. Journal of

Management Accounting Research, 27(1), pp.123-132.

Tappura, S., Sievänen, M., Heikkilä, J., Jussila, A. and Nenonen, N., 2015. A

management accounting perspective on safety. Safety science, 71, pp.151-159.

Van Der Stede, W.A., 2015. Management accounting: Where from, where now,

where to?. Journal of Management Accounting Research, 27(1), pp.171-176.

Woolworthsgroup.com.au., 2019. [online] Available at:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

[Accessed 2 Jun. 2019].

Woolworthsgroup.com.au., 2019. Strategy and objectives - Woolworths Group.

[online] Available at: https://www.woolworthsgroup.com.au/page/about-us/our-

approach/strategy-and-objectives/ [Accessed 2 Jun. 2019].

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.