Advantages and Disadvantages of Planning Tools in Management Accounting

VerifiedAdded on 2023/02/02

|12

|2984

|69

AI Summary

This report discusses the advantages and disadvantages of various planning tools in management accounting, such as budgets, fixed budgets, flexible budgets, incremental budgets, zero-based budgets, and variances analysis. It also explores the use of these planning tools for preparing and forecasting budgets, adapting management accounting systems to respond to financial problems, and how these systems can lead to long-term sustainable success. Additionally, it highlights the importance of planning tools in avoiding financial problems.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management

Accounting.

Accounting.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION.................................................................................................................................3

TASK 1.................................................................................................................................................3

A. Advantage and disadvantage of various types of planning tool....................................................3

B) Use of various planning tool for preparing and forecasting budgets.............................................7

C) Adaptation of management accounting system to respond financial problems.............................7

d) Management accounting system lead to long term sustainable success.........................................9

e) Planning tool to avoid financial problem.......................................................................................9

CONCLUSION...................................................................................................................................10

REFERENCES....................................................................................................................................11

INTRODUCTION.................................................................................................................................3

TASK 1.................................................................................................................................................3

A. Advantage and disadvantage of various types of planning tool....................................................3

B) Use of various planning tool for preparing and forecasting budgets.............................................7

C) Adaptation of management accounting system to respond financial problems.............................7

d) Management accounting system lead to long term sustainable success.........................................9

e) Planning tool to avoid financial problem.......................................................................................9

CONCLUSION...................................................................................................................................10

REFERENCES....................................................................................................................................11

INTRODUCTION

Management accounting is considered to the techniques of manager that help them

determine, organise, report and make effective decision (Anderson and Sedatole, 2013). This

collected information helps them in preparing management reports and accounts which

further provide them appropriate and timely financial and performance information about

worker and company. To understand the importance of management accounting Airdri is

taken into account.

In this report advantages and disadvantages of different planning tools are

implemented to control budgetary process and their effectiveness to solve financial problems

is described. Report also shows the importance of management accounting system to respond

the financial problems.

TASK 1

A. Advantage and disadvantage of various types of planning tool.

Budget:

It is defined as the financial plan which is a microeconomic idea that demonstrates the trade-

off made when one product is traded for another. In business term it is defined as an internal

tool used by management and is frequently not required for reporting by outside parties. A

financial plan is valuation of income and expenditures over a predefined future timeframe.

Budgets can be made for an individual, a household, group of personnel, a firm, for

government, country and international companies that all are willing to spend money and

making profit. In Airdri, manager makes use of different kind of budgets as a planning tool

that further helps in solving and overcoming various kinds of financial issues (Drury, 2015).

There are various advantages of budget that help in maintaining the budgetary control process

in Airdri. Budgetary control process is related to the actual comparison of income and

expenses by manager of company with the planned revenue and spending. Some of the

common advantages and disadvantages are explained below:

Advantages:

Budgets transform planned strategies into action of achievement. They state

the assets, incomes and events required perform the executed plan for the specific

period of Time.

It supports to have a great record of companies business activities.

Budgets improve communication with employees and help them to overcome any

problems.

Management accounting is considered to the techniques of manager that help them

determine, organise, report and make effective decision (Anderson and Sedatole, 2013). This

collected information helps them in preparing management reports and accounts which

further provide them appropriate and timely financial and performance information about

worker and company. To understand the importance of management accounting Airdri is

taken into account.

In this report advantages and disadvantages of different planning tools are

implemented to control budgetary process and their effectiveness to solve financial problems

is described. Report also shows the importance of management accounting system to respond

the financial problems.

TASK 1

A. Advantage and disadvantage of various types of planning tool.

Budget:

It is defined as the financial plan which is a microeconomic idea that demonstrates the trade-

off made when one product is traded for another. In business term it is defined as an internal

tool used by management and is frequently not required for reporting by outside parties. A

financial plan is valuation of income and expenditures over a predefined future timeframe.

Budgets can be made for an individual, a household, group of personnel, a firm, for

government, country and international companies that all are willing to spend money and

making profit. In Airdri, manager makes use of different kind of budgets as a planning tool

that further helps in solving and overcoming various kinds of financial issues (Drury, 2015).

There are various advantages of budget that help in maintaining the budgetary control process

in Airdri. Budgetary control process is related to the actual comparison of income and

expenses by manager of company with the planned revenue and spending. Some of the

common advantages and disadvantages are explained below:

Advantages:

Budgets transform planned strategies into action of achievement. They state

the assets, incomes and events required perform the executed plan for the specific

period of Time.

It supports to have a great record of companies business activities.

Budgets improve communication with employees and help them to overcome any

problems.

It support in improving resources distribution because all requests for every

department are explained and acceptable.

Disadvantages:

The main problem happens when budgets are realistic and are applied automatically and

strictly that hinder the decision making of manager (Hilton and Platt, 2013).

An inflexible budget structure decreases creativity and innovation of other worker at

lower levels, so it is very difficult for companies to make money for new ideas thus

companies faces financial issues.

Fixed Budgets:

A developed fixed budget is about a basic instrument to evaluate the achievement of

private companies both long and short term period of time. Further, a fixed budget

supports in keeping the whole business monetarily careful when making little and

expenses. In companies like Airdri, this budget is prepared by manager to determine the

spending for a single business activity. The execution report is set up by contrasting

information from open tasks. Fixed budgets don't change when manufacture level

changes within an organisation. Some of the basic advantages and disadvantages are

described below:

Advantages:

Fixed budgeting helps manager to teach other employee, as they had a clear

difference between the things they need to do with their workforce.

A fixed budget permits a commercial firm to measure both short-term and long-

term finances resources that are required on single project.

The steady, fixed budgeting sanctions small business holders to have record each

changes and also changes the profitable model accordingly to take benefit of

helpful monetary variations of economy.

Disadvantages:

Flexible budgets also are not correct way to record expenditures. In detail, all they do

is gives a simple standard that will be hard to follow, should revenue or costs change.

department are explained and acceptable.

Disadvantages:

The main problem happens when budgets are realistic and are applied automatically and

strictly that hinder the decision making of manager (Hilton and Platt, 2013).

An inflexible budget structure decreases creativity and innovation of other worker at

lower levels, so it is very difficult for companies to make money for new ideas thus

companies faces financial issues.

Fixed Budgets:

A developed fixed budget is about a basic instrument to evaluate the achievement of

private companies both long and short term period of time. Further, a fixed budget

supports in keeping the whole business monetarily careful when making little and

expenses. In companies like Airdri, this budget is prepared by manager to determine the

spending for a single business activity. The execution report is set up by contrasting

information from open tasks. Fixed budgets don't change when manufacture level

changes within an organisation. Some of the basic advantages and disadvantages are

described below:

Advantages:

Fixed budgeting helps manager to teach other employee, as they had a clear

difference between the things they need to do with their workforce.

A fixed budget permits a commercial firm to measure both short-term and long-

term finances resources that are required on single project.

The steady, fixed budgeting sanctions small business holders to have record each

changes and also changes the profitable model accordingly to take benefit of

helpful monetary variations of economy.

Disadvantages:

Flexible budgets also are not correct way to record expenditures. In detail, all they do

is gives a simple standard that will be hard to follow, should revenue or costs change.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

These are less flexible budget and with the use of this budget manager may faces

problem and conflicts with other macroeconomic factor.

Flexible Budgets:

A flexible budget is a defined as a plan that regulates or bends for changes in the

capacity of business motion. It is more cultured and useful than a fixed budget, which rests at

one amount irrespective of the volume of activity (Innes and Mitchell, 2015). The important

advantages of flexible financial plan are as follows:

Advantages:

A flexible budget allows the manager of company to analyse the deviation of

real output from predictable production.

The management can match definite costs at the definite capacity with the budgeted

costs at the real book.

Disadvantages:

Flexible budgets need more preparation in order to record expenditures and modify

for any differences between ages.

It is a confuse things that comprise additional rules that can simply be bent or cracked

by somebody who is stressed to break within the limitations.

Incremental Budgets:

Incremental budget is a significant measure of management accounting based on the

evidence of making slight changes to the existing budget for arriving at the new budget. Only

incremental totals are added to arrive at the new planned figures. In Airdri, this Also help in

overcoming different financial problems that help in achieving predefined goals. Some of the

advantage and disadvantage are described below:

Advantages

Incremental planning guarantees that there is continuous flow of fund through

department of company without much full enquiry of funding necessity.

Incremental budgets method confirms no large deviations are seen in the budget year

as if requirements changes after that year in companies. With this type of budgeting, a

manager of Airdri is possible to have constant budgets year on year.

problem and conflicts with other macroeconomic factor.

Flexible Budgets:

A flexible budget is a defined as a plan that regulates or bends for changes in the

capacity of business motion. It is more cultured and useful than a fixed budget, which rests at

one amount irrespective of the volume of activity (Innes and Mitchell, 2015). The important

advantages of flexible financial plan are as follows:

Advantages:

A flexible budget allows the manager of company to analyse the deviation of

real output from predictable production.

The management can match definite costs at the definite capacity with the budgeted

costs at the real book.

Disadvantages:

Flexible budgets need more preparation in order to record expenditures and modify

for any differences between ages.

It is a confuse things that comprise additional rules that can simply be bent or cracked

by somebody who is stressed to break within the limitations.

Incremental Budgets:

Incremental budget is a significant measure of management accounting based on the

evidence of making slight changes to the existing budget for arriving at the new budget. Only

incremental totals are added to arrive at the new planned figures. In Airdri, this Also help in

overcoming different financial problems that help in achieving predefined goals. Some of the

advantage and disadvantage are described below:

Advantages

Incremental planning guarantees that there is continuous flow of fund through

department of company without much full enquiry of funding necessity.

Incremental budgets method confirms no large deviations are seen in the budget year

as if requirements changes after that year in companies. With this type of budgeting, a

manager of Airdri is possible to have constant budgets year on year.

Disadvantages

This method may incline to make executives use more and can lead to excessive

spending of monetary resources which may not be acceptable.

Due to this management may face the situation of called as budgetary slack, whereby they

incline to build lower income development and advanced expense growth so as to have

positive adjustments (Ittner and Larcker, 2012).

Zero-based budgets:

Zero-based budget or budgeting is a technique of planning in advance about

all expenditures that must be right for each new period. The procedure of zero-based

budgeting starts from a "zero base," and each purpose within company like Airdri is

examined for its requirements and costs. Budgets be situated the most then assembled around

according to the needs of future period, anyway of whether each financial plan is advanced or

lower than the earlier one. In Airdri this budgets have various advantages and disadvantages

that are explained below:

Advantages

This helps in efficient allocation of resources (department-wise) as it does not look at

the historical numbers but looks at the actual numbers.

It leads to the identification of opportunities and more cost-effective ways of doing

things by removing all the unproductive or redundant activities.

Disadvantages

Zero-based budgeting is a very time-intensive exercise for a company or government-funded

entities to do every year as against incremental budgeting, which is a far easier method

(Advantages and disadvantages of zero based budgets, 2017).

Explaining every line item and every cost is a difficult task and requires training the

managers.

Variances analysis:

In business firm, while performing accounting a variance is the dissimilarity between

planned total and an actual total. Variance analysis goes to recognise and clarify the

details for the difference among a budgeted amount and definite amount. It is typically

This method may incline to make executives use more and can lead to excessive

spending of monetary resources which may not be acceptable.

Due to this management may face the situation of called as budgetary slack, whereby they

incline to build lower income development and advanced expense growth so as to have

positive adjustments (Ittner and Larcker, 2012).

Zero-based budgets:

Zero-based budget or budgeting is a technique of planning in advance about

all expenditures that must be right for each new period. The procedure of zero-based

budgeting starts from a "zero base," and each purpose within company like Airdri is

examined for its requirements and costs. Budgets be situated the most then assembled around

according to the needs of future period, anyway of whether each financial plan is advanced or

lower than the earlier one. In Airdri this budgets have various advantages and disadvantages

that are explained below:

Advantages

This helps in efficient allocation of resources (department-wise) as it does not look at

the historical numbers but looks at the actual numbers.

It leads to the identification of opportunities and more cost-effective ways of doing

things by removing all the unproductive or redundant activities.

Disadvantages

Zero-based budgeting is a very time-intensive exercise for a company or government-funded

entities to do every year as against incremental budgeting, which is a far easier method

(Advantages and disadvantages of zero based budgets, 2017).

Explaining every line item and every cost is a difficult task and requires training the

managers.

Variances analysis:

In business firm, while performing accounting a variance is the dissimilarity between

planned total and an actual total. Variance analysis goes to recognise and clarify the

details for the difference among a budgeted amount and definite amount. It is typically

related with a producer's product expenses. This method tries to classify the causes of the

differences between manufacturers. In Airdri it is considered to an effective planning tool

that helps manager to ease the process of budgetary control. Some of the basic

advantages and disadvantages are described below:

Advantages

This help in comparing more than two groups of data or information that are result

after an experiment.

Variance analysis supports capable budgeting action as manager needs to have lower

expenses from the budgeted expenses.

Disadvantages

Ii is very important to consider each factor; otherwise the budgeting application may

be lightly done which is bound to turn from the real figures.

It is an activity of manager within company that is based on financial outcomes which

are released much later.

B) Use of various planning tool for preparing and forecasting budgets.

In business world budgets play an important role, as it help companies to paned about

future expenses and makes a clear vision. With the formation of Budgets Companies like

Airdri are helpful in planning about future business activities by knowing the expected

outcome and expenses on a particular project (Roslender, 2016). There are various kinds of

budgets that are equally important in planning about future such as Fixed Budgets, Flexible

Budgets, Incremental Budgets, Zero-based budgets and Variances analysis. It is necessary for

manager of Airdri to make proper use of these planning tools in effective manner as they can

determine the total expenses and count the revenues to be earned from different project runs

in company. This helps them in achieving predefined goals. Mainly budget are made from the

last year expenses and determine to be effective if the planned result are matched.

C) Adaptation of management accounting system to respond financial problems.

Management accounting is the basic function that involves collecting of useful

information and distributing that data to decision maker of company. Responsible internal

accountant provide that relevant information to higher management so that they are able to

make faithful policies, standard to operate operation. In recent time it has been noticed that

management accounting has evolved from its existing application. So the role of management

accountant has transformed a lot such as the gathering of information to meet the uncertain of

business environment. They also play the role of business partner and information analysts

enabling manager of companies to have an effective decision making partner in business.

Business environment means all internal and external surrounding of company that can affect

the performance of business activity executed.

differences between manufacturers. In Airdri it is considered to an effective planning tool

that helps manager to ease the process of budgetary control. Some of the basic

advantages and disadvantages are described below:

Advantages

This help in comparing more than two groups of data or information that are result

after an experiment.

Variance analysis supports capable budgeting action as manager needs to have lower

expenses from the budgeted expenses.

Disadvantages

Ii is very important to consider each factor; otherwise the budgeting application may

be lightly done which is bound to turn from the real figures.

It is an activity of manager within company that is based on financial outcomes which

are released much later.

B) Use of various planning tool for preparing and forecasting budgets.

In business world budgets play an important role, as it help companies to paned about

future expenses and makes a clear vision. With the formation of Budgets Companies like

Airdri are helpful in planning about future business activities by knowing the expected

outcome and expenses on a particular project (Roslender, 2016). There are various kinds of

budgets that are equally important in planning about future such as Fixed Budgets, Flexible

Budgets, Incremental Budgets, Zero-based budgets and Variances analysis. It is necessary for

manager of Airdri to make proper use of these planning tools in effective manner as they can

determine the total expenses and count the revenues to be earned from different project runs

in company. This helps them in achieving predefined goals. Mainly budget are made from the

last year expenses and determine to be effective if the planned result are matched.

C) Adaptation of management accounting system to respond financial problems.

Management accounting is the basic function that involves collecting of useful

information and distributing that data to decision maker of company. Responsible internal

accountant provide that relevant information to higher management so that they are able to

make faithful policies, standard to operate operation. In recent time it has been noticed that

management accounting has evolved from its existing application. So the role of management

accountant has transformed a lot such as the gathering of information to meet the uncertain of

business environment. They also play the role of business partner and information analysts

enabling manager of companies to have an effective decision making partner in business.

Business environment means all internal and external surrounding of company that can affect

the performance of business activity executed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In every company there is a situation of financial problem that hinder the performance.

Financial problem refers to a situation when company do not have sufficient amount to run

their daily business project (Schaltegge and Csutora, 2012). They lack the amount to pay

salary to their staff, make payment of outstanding bills etc. sometime company also face

these issues just by spending excess amount on other activities. In Airdri manager uses

various techniques to determine different financial problem that are explained below:

KPI: A Key Performance Indicator (KPI) is a calculable importance that

determines in what way successfully a business entity is attaining key business objectives.

Large or small companies use key performance indicators at numerous levels to estimate their

achievement at realization of targets. In Airdri, Manager uses this technique to determine the

financial problem of more spending than earning.

Benchmarking: In business world, benchmarking is a method in which a

firm compares its goods and approaches of business with other most effective companies in

same industry, that help them to improve its own performance. The main aim of

benchmarking is to recognize and calculate the present position of a business in relative to

best practice and to ascertain areas performance improvement. In Airdri manager uses this

method to detect the financial problem related to lack of money management.

Ratio analysis: This ratio analysis is a measurable examination of data controlled in a

company’s economic statements. It is used to estimate various features of a company’s

working and financial presentation such as its productivity, fluidity, profitability and

creditworthiness. With the help of this approach company determine the financial issue of

High debt level.

Comparison of two companies.

System Airdri A David & Co Ltd.

Cost accounting This system help in

controlling cost and

expenses involved in

production process. So

management of Airdri uses

this system by keeping

detail information of total

amount spends of

production and promotion

activities (Ward, 2012).

Thus help in overcoming

the issue of more spending

than earning.

With the help of this approach

company is able to resolve the

financial issue of late payment

of bills.

Price optimisation This system means fixing

the best price in industry

This is an effective system that

helps company in overcoming

Financial problem refers to a situation when company do not have sufficient amount to run

their daily business project (Schaltegge and Csutora, 2012). They lack the amount to pay

salary to their staff, make payment of outstanding bills etc. sometime company also face

these issues just by spending excess amount on other activities. In Airdri manager uses

various techniques to determine different financial problem that are explained below:

KPI: A Key Performance Indicator (KPI) is a calculable importance that

determines in what way successfully a business entity is attaining key business objectives.

Large or small companies use key performance indicators at numerous levels to estimate their

achievement at realization of targets. In Airdri, Manager uses this technique to determine the

financial problem of more spending than earning.

Benchmarking: In business world, benchmarking is a method in which a

firm compares its goods and approaches of business with other most effective companies in

same industry, that help them to improve its own performance. The main aim of

benchmarking is to recognize and calculate the present position of a business in relative to

best practice and to ascertain areas performance improvement. In Airdri manager uses this

method to detect the financial problem related to lack of money management.

Ratio analysis: This ratio analysis is a measurable examination of data controlled in a

company’s economic statements. It is used to estimate various features of a company’s

working and financial presentation such as its productivity, fluidity, profitability and

creditworthiness. With the help of this approach company determine the financial issue of

High debt level.

Comparison of two companies.

System Airdri A David & Co Ltd.

Cost accounting This system help in

controlling cost and

expenses involved in

production process. So

management of Airdri uses

this system by keeping

detail information of total

amount spends of

production and promotion

activities (Ward, 2012).

Thus help in overcoming

the issue of more spending

than earning.

With the help of this approach

company is able to resolve the

financial issue of late payment

of bills.

Price optimisation This system means fixing

the best price in industry

This is an effective system that

helps company in overcoming

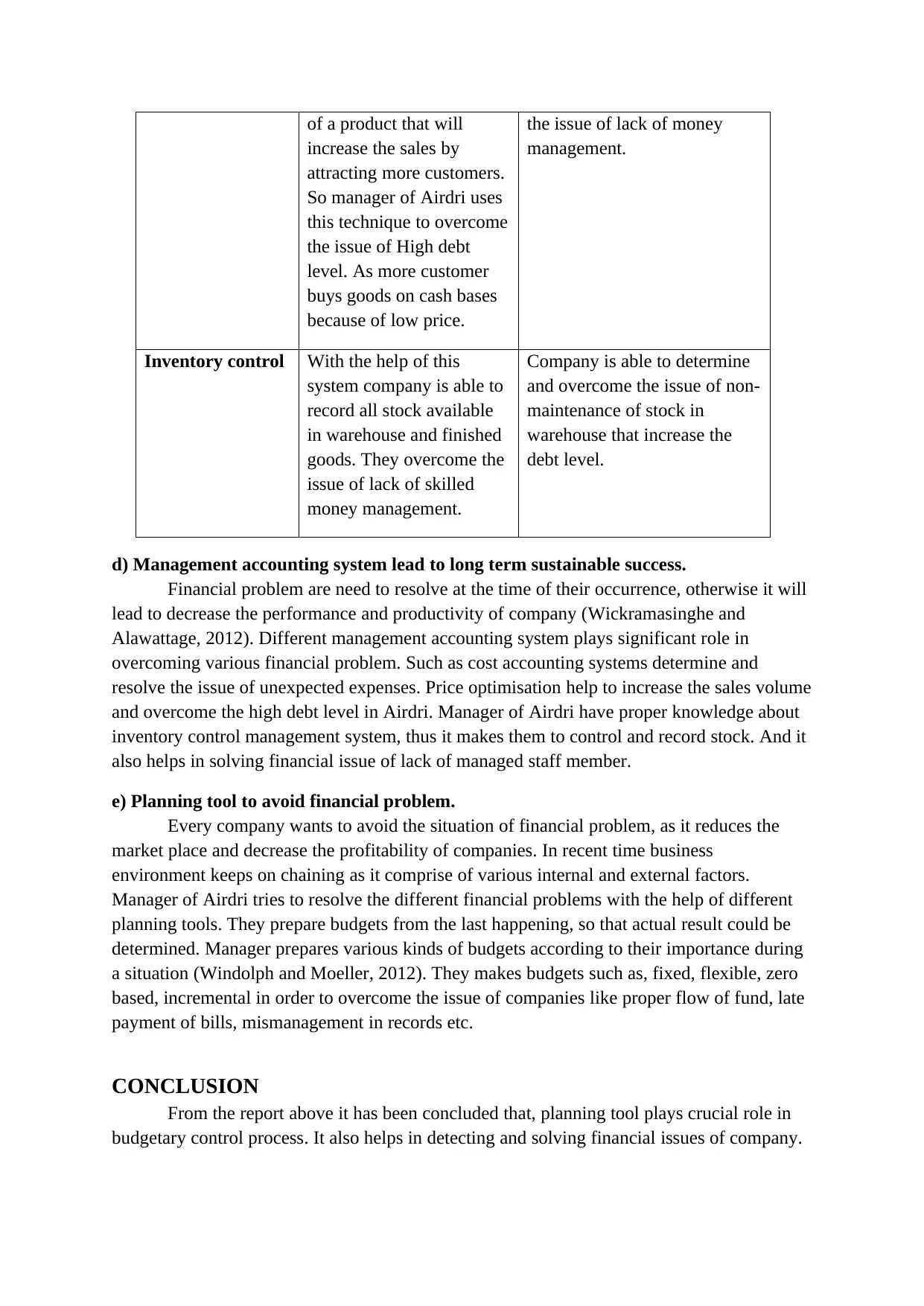

of a product that will

increase the sales by

attracting more customers.

So manager of Airdri uses

this technique to overcome

the issue of High debt

level. As more customer

buys goods on cash bases

because of low price.

the issue of lack of money

management.

Inventory control With the help of this

system company is able to

record all stock available

in warehouse and finished

goods. They overcome the

issue of lack of skilled

money management.

Company is able to determine

and overcome the issue of non-

maintenance of stock in

warehouse that increase the

debt level.

d) Management accounting system lead to long term sustainable success.

Financial problem are need to resolve at the time of their occurrence, otherwise it will

lead to decrease the performance and productivity of company (Wickramasinghe and

Alawattage, 2012). Different management accounting system plays significant role in

overcoming various financial problem. Such as cost accounting systems determine and

resolve the issue of unexpected expenses. Price optimisation help to increase the sales volume

and overcome the high debt level in Airdri. Manager of Airdri have proper knowledge about

inventory control management system, thus it makes them to control and record stock. And it

also helps in solving financial issue of lack of managed staff member.

e) Planning tool to avoid financial problem.

Every company wants to avoid the situation of financial problem, as it reduces the

market place and decrease the profitability of companies. In recent time business

environment keeps on chaining as it comprise of various internal and external factors.

Manager of Airdri tries to resolve the different financial problems with the help of different

planning tools. They prepare budgets from the last happening, so that actual result could be

determined. Manager prepares various kinds of budgets according to their importance during

a situation (Windolph and Moeller, 2012). They makes budgets such as, fixed, flexible, zero

based, incremental in order to overcome the issue of companies like proper flow of fund, late

payment of bills, mismanagement in records etc.

CONCLUSION

From the report above it has been concluded that, planning tool plays crucial role in

budgetary control process. It also helps in detecting and solving financial issues of company.

increase the sales by

attracting more customers.

So manager of Airdri uses

this technique to overcome

the issue of High debt

level. As more customer

buys goods on cash bases

because of low price.

the issue of lack of money

management.

Inventory control With the help of this

system company is able to

record all stock available

in warehouse and finished

goods. They overcome the

issue of lack of skilled

money management.

Company is able to determine

and overcome the issue of non-

maintenance of stock in

warehouse that increase the

debt level.

d) Management accounting system lead to long term sustainable success.

Financial problem are need to resolve at the time of their occurrence, otherwise it will

lead to decrease the performance and productivity of company (Wickramasinghe and

Alawattage, 2012). Different management accounting system plays significant role in

overcoming various financial problem. Such as cost accounting systems determine and

resolve the issue of unexpected expenses. Price optimisation help to increase the sales volume

and overcome the high debt level in Airdri. Manager of Airdri have proper knowledge about

inventory control management system, thus it makes them to control and record stock. And it

also helps in solving financial issue of lack of managed staff member.

e) Planning tool to avoid financial problem.

Every company wants to avoid the situation of financial problem, as it reduces the

market place and decrease the profitability of companies. In recent time business

environment keeps on chaining as it comprise of various internal and external factors.

Manager of Airdri tries to resolve the different financial problems with the help of different

planning tools. They prepare budgets from the last happening, so that actual result could be

determined. Manager prepares various kinds of budgets according to their importance during

a situation (Windolph and Moeller, 2012). They makes budgets such as, fixed, flexible, zero

based, incremental in order to overcome the issue of companies like proper flow of fund, late

payment of bills, mismanagement in records etc.

CONCLUSION

From the report above it has been concluded that, planning tool plays crucial role in

budgetary control process. It also helps in detecting and solving financial issues of company.

Management accounting systems are helpful in overcoming various kind of financial

problem.

problem.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals:

Anderson, S. and Sedatole, K., 2013. Management accounting for the extended enterprise:

Performance management for strategic alliances and networked partners.

Drury, C., 2015. Management accounting for business. Cengage Learning EMEA.

Hilton, R. W. and Platt, D. E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Innes, J. and Mitchell, F., 2015. A survey of activity-based costing in the UK's largest

companies. Management accounting research. 6(2). pp.137-153.

Ittner, C. D. and Larcker, D. F., 2012. Quality strategy, strategic control systems, and

organizational performance. Accounting, Organizations and Society. 22(3-4). pp.293-

314.

Roslender, R., 2016. Relevance lost and found: critical perspectives on the promise of

management accounting. Critical Perspectives on Accounting. 7(5). pp.533-561.

Schaltegger, S. and Csutora, M., 2012. Carbon accounting for sustainability and management.

Status quo and challenges. Journal of Cleaner Production. 36. pp.1-16.

Ward, K., 2012. Strategic management accounting. Routledge.

Wickramasinghe, D. and Alawattage, C., 2012. Management accounting change: approaches

and perspectives. Routledge.

Windolph, M. and Moeller, K., 2012. Open-book accounting: Reason for failure of inter-firm

cooperation?. Management Accounting Research. 23(1). pp.47-60.

Online

Advantages and disadvantages of zero based budgets. 2017. [Online] Available Through:

<https://efinancemanagement.com/budgeting/zero-based>

Books and Journals:

Anderson, S. and Sedatole, K., 2013. Management accounting for the extended enterprise:

Performance management for strategic alliances and networked partners.

Drury, C., 2015. Management accounting for business. Cengage Learning EMEA.

Hilton, R. W. and Platt, D. E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Innes, J. and Mitchell, F., 2015. A survey of activity-based costing in the UK's largest

companies. Management accounting research. 6(2). pp.137-153.

Ittner, C. D. and Larcker, D. F., 2012. Quality strategy, strategic control systems, and

organizational performance. Accounting, Organizations and Society. 22(3-4). pp.293-

314.

Roslender, R., 2016. Relevance lost and found: critical perspectives on the promise of

management accounting. Critical Perspectives on Accounting. 7(5). pp.533-561.

Schaltegger, S. and Csutora, M., 2012. Carbon accounting for sustainability and management.

Status quo and challenges. Journal of Cleaner Production. 36. pp.1-16.

Ward, K., 2012. Strategic management accounting. Routledge.

Wickramasinghe, D. and Alawattage, C., 2012. Management accounting change: approaches

and perspectives. Routledge.

Windolph, M. and Moeller, K., 2012. Open-book accounting: Reason for failure of inter-firm

cooperation?. Management Accounting Research. 23(1). pp.47-60.

Online

Advantages and disadvantages of zero based budgets. 2017. [Online] Available Through:

<https://efinancemanagement.com/budgeting/zero-based>

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.