Management Accounting Report: Costing Methods and Planning

VerifiedAdded on 2021/02/19

|17

|3389

|31

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on the application of these principles within the context of NERO LTD, a manufacturing company. The report is structured into four key tasks. Task 1 defines management accounting, its essential requirements, and compares it with financial accounting, using examples like cost accounting, price optimization, job costing, and inventory management systems. Task 2 explores different costing methods, including marginal and absorption costing, and examines the preparation and interpretation of income statements. Task 3 delves into various planning tools used for budgetary control, evaluating their advantages and disadvantages. Finally, Task 4 addresses the adoption of management accounting systems to respond to financial problems, comparing different organizational approaches and strategies for achieving sustainable success. The report emphasizes the integration of management accounting and reporting, highlighting their role in achieving organizational goals through effective decision-making and efficient operations.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

P1: Management accounting along with its essential requirements............................................1

P2: Different methods for management accounting reporting....................................................3

M1 Benefits of management accounting system.........................................................................4

D1 Management accounting system and reporting integrated with each other...........................5

TASK 2............................................................................................................................................6

P3: Different costing methods.....................................................................................................6

M2. Management accounting techniques for preparation of financial reporting documents......9

D2. Interpretation of income statements......................................................................................9

TASK 3..........................................................................................................................................10

P4. Advantages and disadvantages of planning tools used for budgetary control:....................10

M3. Uses of various planning tools and their application for preparing and estimating budgets:

....................................................................................................................................................11

TASK 4..........................................................................................................................................12

P5. Adoption of management accounting system to respond the financial problems:..............12

M4. Responding to financial problems, management accounting to sustainable success:........14

D3 Planning tools for accounting period to respond financial problems appropriately:...........14

CONCLUSION..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

P1: Management accounting along with its essential requirements............................................1

P2: Different methods for management accounting reporting....................................................3

M1 Benefits of management accounting system.........................................................................4

D1 Management accounting system and reporting integrated with each other...........................5

TASK 2............................................................................................................................................6

P3: Different costing methods.....................................................................................................6

M2. Management accounting techniques for preparation of financial reporting documents......9

D2. Interpretation of income statements......................................................................................9

TASK 3..........................................................................................................................................10

P4. Advantages and disadvantages of planning tools used for budgetary control:....................10

M3. Uses of various planning tools and their application for preparing and estimating budgets:

....................................................................................................................................................11

TASK 4..........................................................................................................................................12

P5. Adoption of management accounting system to respond the financial problems:..............12

M4. Responding to financial problems, management accounting to sustainable success:........14

D3 Planning tools for accounting period to respond financial problems appropriately:...........14

CONCLUSION..............................................................................................................................14

INTRODUCTION

In any business organisation, there is a requirement to implement a management

accounting system which helps the company in managing its operations effectively and

efficiently. It is also know as cost accounting which assist the company in identifying,

measuring, analysing, interpreting and communicating information to mangers for achieving an

entity's goals. For better understanding of management accounting, company named NERO

LTD is chosen which is operated in manufacturing sector. This report divides in four tasks, first

task explains the term management accounting system and describe its essential types. Second

task describes uses of various appropriate cost accounting techniques for preparation of income

statement. Third task describes the various planning tools used in cost accounting system and its

advantages and disadvantages whereas fourth task provides the comparison between

organisations in adoption of this system and their responses to various financial problems.

P1: Management accounting along with its essential requirements

Management accounting relates with the internal management which considered non-

monetary as well as monetary information that helps to take an effective decision for the

organisation. It plays an crucial by making effective plans that increases the productivity of the

organisation. In these some of effective management accounting system that executed by Nero

Limited as follow:

Cost accounting system- The cost accounting system is implemented by Nero limited to

monitor the cost that is incurred while performing their daily activities. For this they record the

revenue, profits and cost that is record and manage by the organisation. In most of the

organisation finance department adopted this method because it refines the data and turn it into

meaningful information. Like the production cost measures the profitability of the organisation

In any business organisation, there is a requirement to implement a management

accounting system which helps the company in managing its operations effectively and

efficiently. It is also know as cost accounting which assist the company in identifying,

measuring, analysing, interpreting and communicating information to mangers for achieving an

entity's goals. For better understanding of management accounting, company named NERO

LTD is chosen which is operated in manufacturing sector. This report divides in four tasks, first

task explains the term management accounting system and describe its essential types. Second

task describes uses of various appropriate cost accounting techniques for preparation of income

statement. Third task describes the various planning tools used in cost accounting system and its

advantages and disadvantages whereas fourth task provides the comparison between

organisations in adoption of this system and their responses to various financial problems.

P1: Management accounting along with its essential requirements

Management accounting relates with the internal management which considered non-

monetary as well as monetary information that helps to take an effective decision for the

organisation. It plays an crucial by making effective plans that increases the productivity of the

organisation. In these some of effective management accounting system that executed by Nero

Limited as follow:

Cost accounting system- The cost accounting system is implemented by Nero limited to

monitor the cost that is incurred while performing their daily activities. For this they record the

revenue, profits and cost that is record and manage by the organisation. In most of the

organisation finance department adopted this method because it refines the data and turn it into

meaningful information. Like the production cost measures the profitability of the organisation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

through recording the data that is managed by them. In context of Nero limited this helps an

organisation to find the production and service cost of the organisation.

Price optimization system- This system helps an organisation to determine the cost or

price of products or services that is offer by them in the market to their customers. Price

optimization system is beneficial for Nero limited because it helps them to ensure the future

profitability for an organisation. Most of the organisation adopt this method for decide the price

of their products that is accepted by its stakeholders such as customer and employees. Along

with this it also helps them to achieve their objective effectively.

Job costing system- This accounting system plays an crucial role in the organisation as it

identify the cost of each unit on individual bases. Job order costing system provide more benefits

to those organisation which provides large number of products to their customers. In the context

of Nero limited finance manager measure or evaluate the cost that is earned by them from each

unit by making the estimation for different cost. Along with this it is also essential for the

organisation to measure their cost for each product or unit which helps them to add the margin

which is useful for organisation to complete their goals with approaching them through positive

forces.

Inventory management system:This system refer to the process that helps an

organisation to complete their goals with maintaining proper inventory. Moreover inventory

management system helps them to monitor regular and current stock that is required by them to

complete their daily activities. It determines that inventory plays an crucial role in the

organisation because mismanagement of inventory creates problems for organisation by

increasing their cost and waste of raw materials. Like Nero limited executed this system in order

to provide fast services to their customers. Along with this it also helps them to gain competitive

edge from their rivals.

Particular Financial accounting Management accounting

Definition Financial accounting refers to that

accounting system which prepare

the financial accounts or statement

for an organisation. The major of

this is to provide essential

Management accounting system

provides relevant information in all

departments of the organisation. It

helps them to develop effective

plans and policy for the

organisation to find the production and service cost of the organisation.

Price optimization system- This system helps an organisation to determine the cost or

price of products or services that is offer by them in the market to their customers. Price

optimization system is beneficial for Nero limited because it helps them to ensure the future

profitability for an organisation. Most of the organisation adopt this method for decide the price

of their products that is accepted by its stakeholders such as customer and employees. Along

with this it also helps them to achieve their objective effectively.

Job costing system- This accounting system plays an crucial role in the organisation as it

identify the cost of each unit on individual bases. Job order costing system provide more benefits

to those organisation which provides large number of products to their customers. In the context

of Nero limited finance manager measure or evaluate the cost that is earned by them from each

unit by making the estimation for different cost. Along with this it is also essential for the

organisation to measure their cost for each product or unit which helps them to add the margin

which is useful for organisation to complete their goals with approaching them through positive

forces.

Inventory management system:This system refer to the process that helps an

organisation to complete their goals with maintaining proper inventory. Moreover inventory

management system helps them to monitor regular and current stock that is required by them to

complete their daily activities. It determines that inventory plays an crucial role in the

organisation because mismanagement of inventory creates problems for organisation by

increasing their cost and waste of raw materials. Like Nero limited executed this system in order

to provide fast services to their customers. Along with this it also helps them to gain competitive

edge from their rivals.

Particular Financial accounting Management accounting

Definition Financial accounting refers to that

accounting system which prepare

the financial accounts or statement

for an organisation. The major of

this is to provide essential

Management accounting system

provides relevant information in all

departments of the organisation. It

helps them to develop effective

plans and policy for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

information to interested parties

such as investor, employees etc.

organisation.

Purpose Financial accounts are prepared to

maintain the records of monetary

transaction to evaluate the profits

of organisation.

The major purpose of this is to

gather all the essential information

that is require by the organisation.

Information Financial accounting provides only

monetary information that take

place in the organisation.

Management accounting provides

monetary as well as non- monetary

information to the organisation.

Objective They collect and deliver only

financial information to the

customers or outsiders.

Management accounting assist

management to plan and develop

effective decision making process.

P2: Different methods for management accounting reporting

Budget report- The budget report play an important role in the organisation that helps

them to recognize the difference between their actual cost and the estimated cost that take place

during their operations. Within circumstances of Nero limited it is mandatory to formulate the

budget in order to get the information about their economic condition. In result for this an

organisation recognises their cost level, expenditure level and others factors so it is easy for them

to take effective decisions. In this report the reason behind the fluctuation between their

estimated and actual budget are identify by an organisation. Along with this it also helps them to

control their transaction that creates an unnecessary burden on the organisation through

increasing their expenses.

Account receivable report- The main function of account receivable report is to identify

the number of debtors and creditors that are present in the organisation. In context of Nero

limited it helps them they find out number of debtors so it is easy for them to recover the amount

by formulating new strategies that help to increase their profits. Moreover it is also useful to

make policies by which they reduce the number of creditors as account receivable report helps

them to identify the number of bad-debtors that are present in the organisation. So they are able

to make strict policies for them.

such as investor, employees etc.

organisation.

Purpose Financial accounts are prepared to

maintain the records of monetary

transaction to evaluate the profits

of organisation.

The major purpose of this is to

gather all the essential information

that is require by the organisation.

Information Financial accounting provides only

monetary information that take

place in the organisation.

Management accounting provides

monetary as well as non- monetary

information to the organisation.

Objective They collect and deliver only

financial information to the

customers or outsiders.

Management accounting assist

management to plan and develop

effective decision making process.

P2: Different methods for management accounting reporting

Budget report- The budget report play an important role in the organisation that helps

them to recognize the difference between their actual cost and the estimated cost that take place

during their operations. Within circumstances of Nero limited it is mandatory to formulate the

budget in order to get the information about their economic condition. In result for this an

organisation recognises their cost level, expenditure level and others factors so it is easy for them

to take effective decisions. In this report the reason behind the fluctuation between their

estimated and actual budget are identify by an organisation. Along with this it also helps them to

control their transaction that creates an unnecessary burden on the organisation through

increasing their expenses.

Account receivable report- The main function of account receivable report is to identify

the number of debtors and creditors that are present in the organisation. In context of Nero

limited it helps them they find out number of debtors so it is easy for them to recover the amount

by formulating new strategies that help to increase their profits. Moreover it is also useful to

make policies by which they reduce the number of creditors as account receivable report helps

them to identify the number of bad-debtors that are present in the organisation. So they are able

to make strict policies for them.

Cost managerial accounting reporting- In this report all the business activities that

impacts on cost of the organisation are included in cost accounting report. Nero limited

formulate this report because it helps them to identify the cost that is impacted in the

organisation. It helps them to identify the difference between the expenses and the income that is

generated by the organisation through selling different products and services in the market.

Moreover it also helps them to reduce their nu-necessary expenses so there is increase in the

profits of the organisation. Further it is essential for organisation to identify cost managerial

aspect because it impact on overall performance of the organisation.

Performance report- Nero limited formulate performance report for their organisation in

order to measure and evaluate the performance of each employee and organisation. The main

purpose of this report is to identify the current performance of the organisation that assist them to

identify different issue that are faced by the organisation to complete their task. Along with this

it is useful for achieving their mission through making effective strategy that is useful from

overcoming different issue. As it helps them to take right decisions to enhance the profitability of

their overall performance.

M1 Benefits of management accounting system

Management accounting system Benefits

Price optimisation system It is easy for the organisation to decide

the effective price for products that

helps them to attract more customers.

The another benefit of price

optimisation system is that an

organisation decide the price of their

product that increases sale of it.

Cost accounting system This system helps the organisation to

calculate their total cost so it is easy for

them to decide the margin that increases

their profits.

The other benefit of cost system it is

impacts on cost of the organisation are included in cost accounting report. Nero limited

formulate this report because it helps them to identify the cost that is impacted in the

organisation. It helps them to identify the difference between the expenses and the income that is

generated by the organisation through selling different products and services in the market.

Moreover it also helps them to reduce their nu-necessary expenses so there is increase in the

profits of the organisation. Further it is essential for organisation to identify cost managerial

aspect because it impact on overall performance of the organisation.

Performance report- Nero limited formulate performance report for their organisation in

order to measure and evaluate the performance of each employee and organisation. The main

purpose of this report is to identify the current performance of the organisation that assist them to

identify different issue that are faced by the organisation to complete their task. Along with this

it is useful for achieving their mission through making effective strategy that is useful from

overcoming different issue. As it helps them to take right decisions to enhance the profitability of

their overall performance.

M1 Benefits of management accounting system

Management accounting system Benefits

Price optimisation system It is easy for the organisation to decide

the effective price for products that

helps them to attract more customers.

The another benefit of price

optimisation system is that an

organisation decide the price of their

product that increases sale of it.

Cost accounting system This system helps the organisation to

calculate their total cost so it is easy for

them to decide the margin that increases

their profits.

The other benefit of cost system it is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

beneficial for organisation to identify

those goals that help to calculate their

cost.

Inventory management system In this an organisation identify different

needs that is required by customers so

they order essential amount of

inventories to fulfil their needs. This

help them to gain loyal customers for

the organisation.

It is useful because it helps them to

complete their goals by determining

different factors like they attain their

goals by managing their inventory with

formulating effective strategy.

Job costing system This system helps an organisation to

identify those goals which exist in

market and helps an organisation to

complete their goals with adding their

margin.

Another benefits is that it helps an

organisation to keep the track of their

teams and individuals that impact on

the cost control, efficiency which help

to track their regular performance.

D1 Management accounting system and reporting integrated with each other

Both concepts management accounting as well as management reporting both are

integrated with each other because they work for achieving common objective. They both helps

an organisation to achieve their goal within minimum time period. In order to easily understand

an example is mention. It helps them to monitor and control the activities that relates with the

those goals that help to calculate their

cost.

Inventory management system In this an organisation identify different

needs that is required by customers so

they order essential amount of

inventories to fulfil their needs. This

help them to gain loyal customers for

the organisation.

It is useful because it helps them to

complete their goals by determining

different factors like they attain their

goals by managing their inventory with

formulating effective strategy.

Job costing system This system helps an organisation to

identify those goals which exist in

market and helps an organisation to

complete their goals with adding their

margin.

Another benefits is that it helps an

organisation to keep the track of their

teams and individuals that impact on

the cost control, efficiency which help

to track their regular performance.

D1 Management accounting system and reporting integrated with each other

Both concepts management accounting as well as management reporting both are

integrated with each other because they work for achieving common objective. They both helps

an organisation to achieve their goal within minimum time period. In order to easily understand

an example is mention. It helps them to monitor and control the activities that relates with the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

inventory management. Like it helps them to identify that more stock is required by organisation

to identify the required budget. The other example is that to identify those goals that assist an

manager to evaluate their total cost that help to execute their cost effectively in industry. This

conditions are possible only for the organisation when they develop effective budget for the

organisation. As this prices are based on the estimation that are raised in the market or industry.

Therefore management accounting is essential for them because it helps them to complete their

goals with efficiency by keeping regular monitoring on their activities.

TASK 2

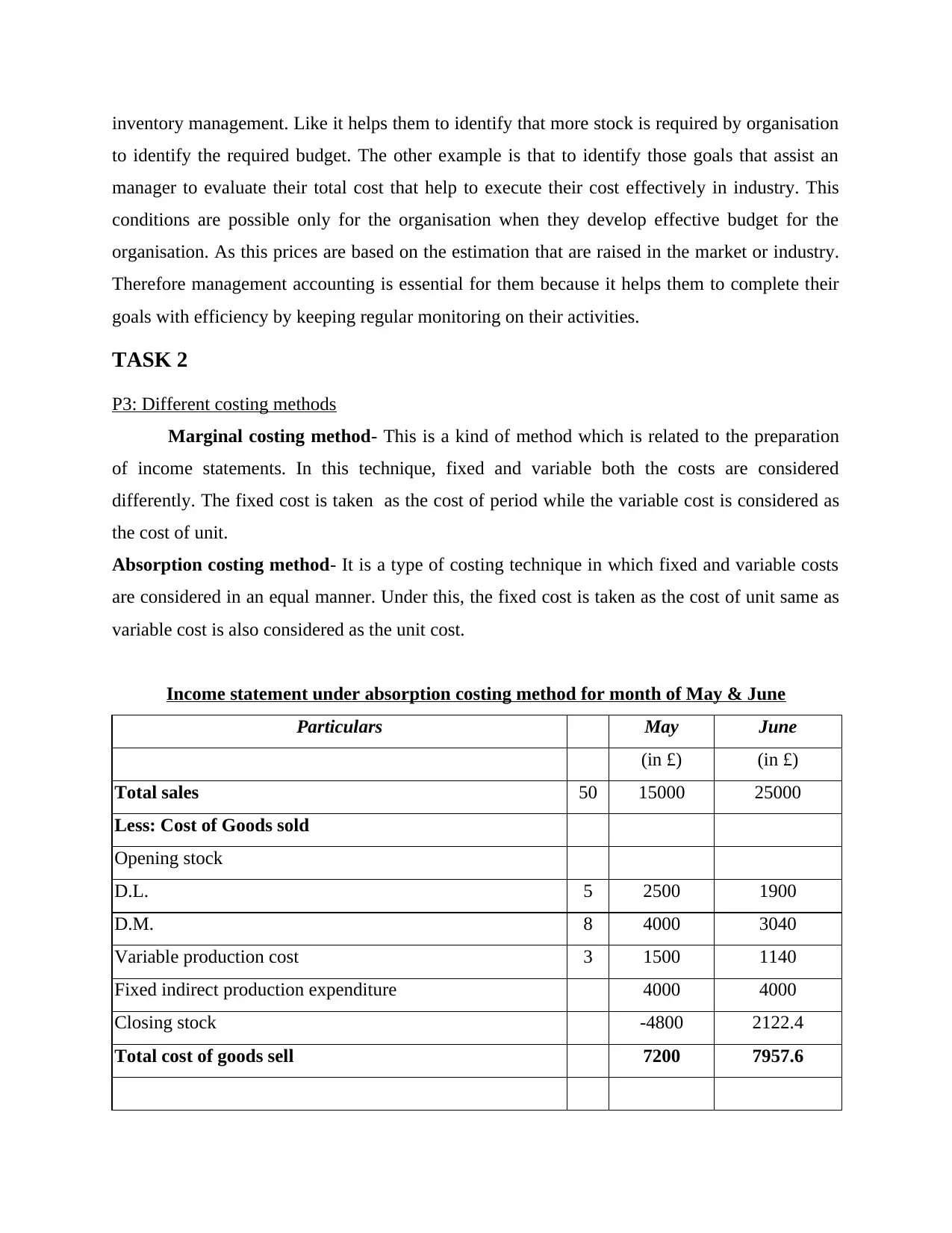

P3: Different costing methods

Marginal costing method- This is a kind of method which is related to the preparation

of income statements. In this technique, fixed and variable both the costs are considered

differently. The fixed cost is taken as the cost of period while the variable cost is considered as

the cost of unit.

Absorption costing method- It is a type of costing technique in which fixed and variable costs

are considered in an equal manner. Under this, the fixed cost is taken as the cost of unit same as

variable cost is also considered as the unit cost.

Income statement under absorption costing method for month of May & June

Particulars May June

(in £) (in £)

Total sales 50 15000 25000

Less: Cost of Goods sold

Opening stock

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable production cost 3 1500 1140

Fixed indirect production expenditure 4000 4000

Closing stock -4800 2122.4

Total cost of goods sell 7200 7957.6

to identify the required budget. The other example is that to identify those goals that assist an

manager to evaluate their total cost that help to execute their cost effectively in industry. This

conditions are possible only for the organisation when they develop effective budget for the

organisation. As this prices are based on the estimation that are raised in the market or industry.

Therefore management accounting is essential for them because it helps them to complete their

goals with efficiency by keeping regular monitoring on their activities.

TASK 2

P3: Different costing methods

Marginal costing method- This is a kind of method which is related to the preparation

of income statements. In this technique, fixed and variable both the costs are considered

differently. The fixed cost is taken as the cost of period while the variable cost is considered as

the cost of unit.

Absorption costing method- It is a type of costing technique in which fixed and variable costs

are considered in an equal manner. Under this, the fixed cost is taken as the cost of unit same as

variable cost is also considered as the unit cost.

Income statement under absorption costing method for month of May & June

Particulars May June

(in £) (in £)

Total sales 50 15000 25000

Less: Cost of Goods sold

Opening stock

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable production cost 3 1500 1140

Fixed indirect production expenditure 4000 4000

Closing stock -4800 2122.4

Total cost of goods sell 7200 7957.6

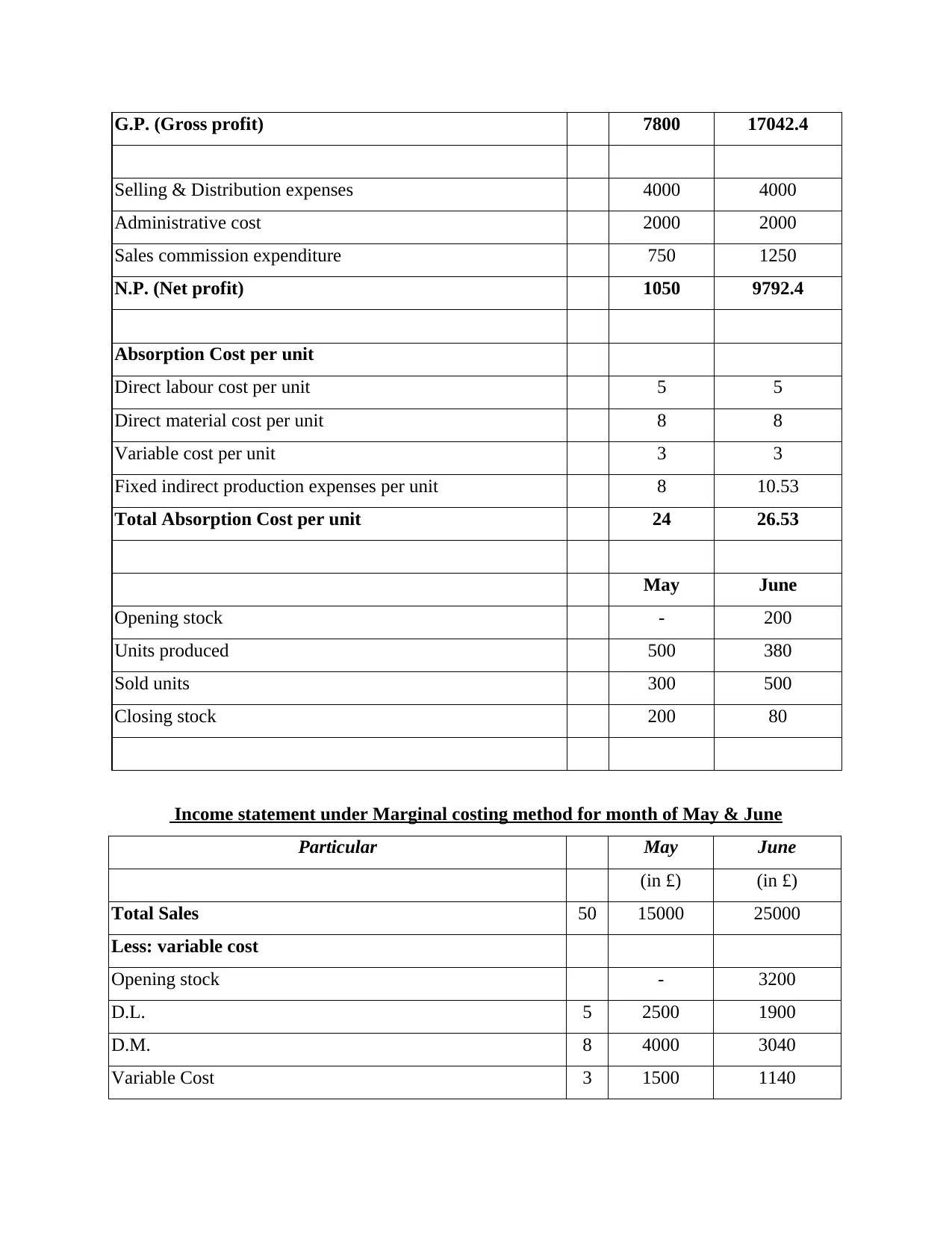

G.P. (Gross profit) 7800 17042.4

Selling & Distribution expenses 4000 4000

Administrative cost 2000 2000

Sales commission expenditure 750 1250

N.P. (Net profit) 1050 9792.4

Absorption Cost per unit

Direct labour cost per unit 5 5

Direct material cost per unit 8 8

Variable cost per unit 3 3

Fixed indirect production expenses per unit 8 10.53

Total Absorption Cost per unit 24 26.53

May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

Income statement under Marginal costing method for month of May & June

Particular May June

(in £) (in £)

Total Sales 50 15000 25000

Less: variable cost

Opening stock - 3200

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable Cost 3 1500 1140

Selling & Distribution expenses 4000 4000

Administrative cost 2000 2000

Sales commission expenditure 750 1250

N.P. (Net profit) 1050 9792.4

Absorption Cost per unit

Direct labour cost per unit 5 5

Direct material cost per unit 8 8

Variable cost per unit 3 3

Fixed indirect production expenses per unit 8 10.53

Total Absorption Cost per unit 24 26.53

May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

Income statement under Marginal costing method for month of May & June

Particular May June

(in £) (in £)

Total Sales 50 15000 25000

Less: variable cost

Opening stock - 3200

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable Cost 3 1500 1140

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

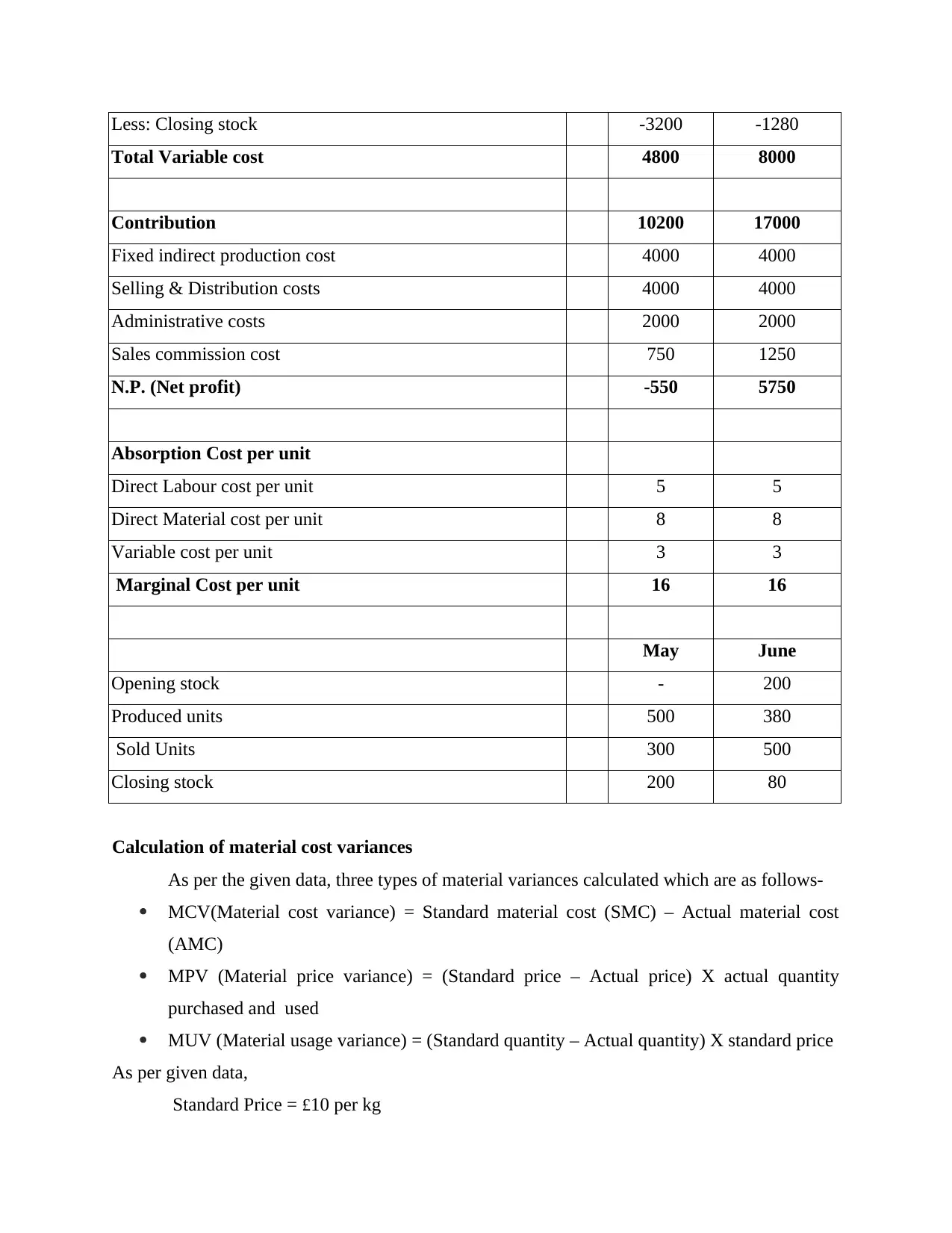

Less: Closing stock -3200 -1280

Total Variable cost 4800 8000

Contribution 10200 17000

Fixed indirect production cost 4000 4000

Selling & Distribution costs 4000 4000

Administrative costs 2000 2000

Sales commission cost 750 1250

N.P. (Net profit) -550 5750

Absorption Cost per unit

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Marginal Cost per unit 16 16

May June

Opening stock - 200

Produced units 500 380

Sold Units 300 500

Closing stock 200 80

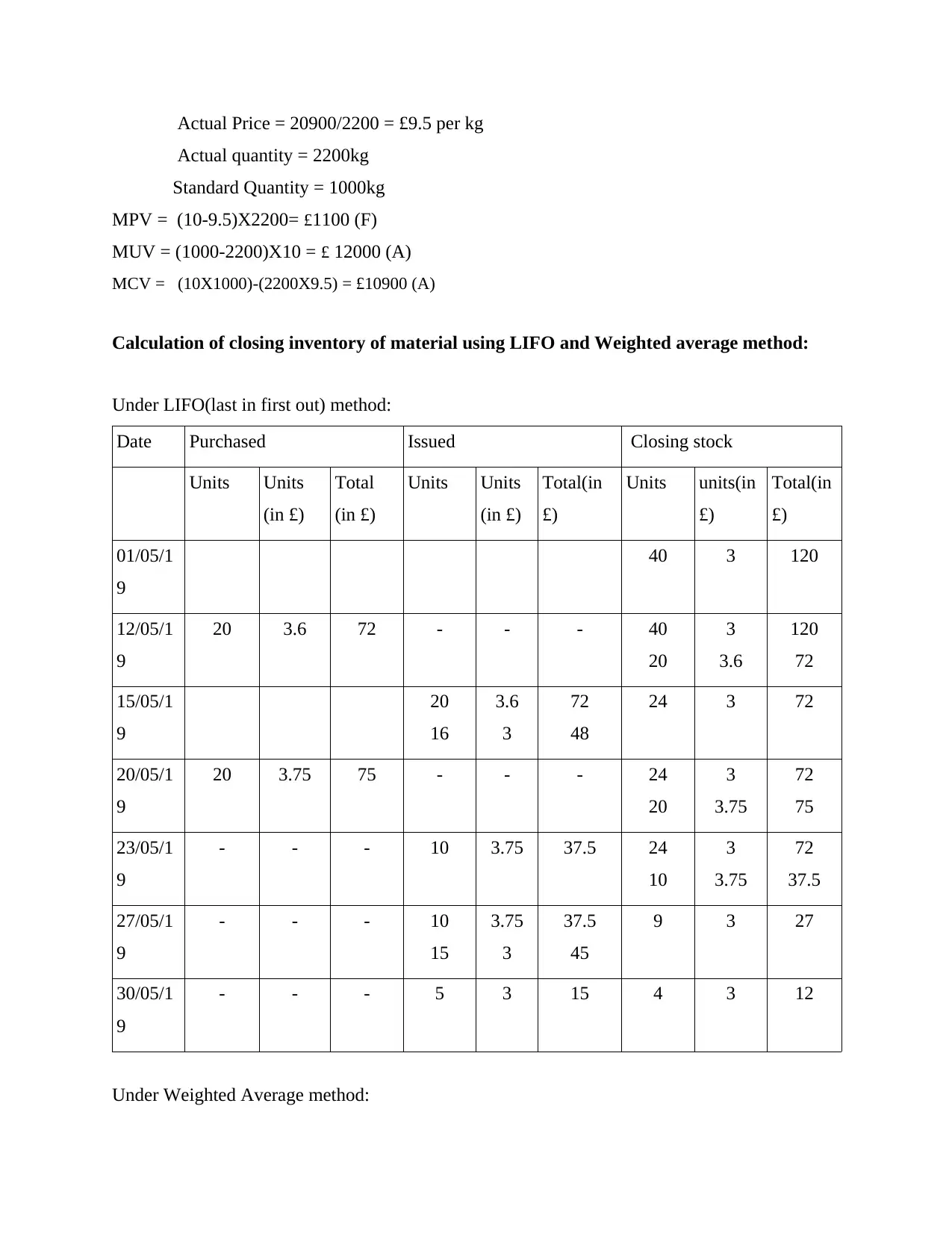

Calculation of material cost variances

As per the given data, three types of material variances calculated which are as follows-

MCV(Material cost variance) = Standard material cost (SMC) – Actual material cost

(AMC)

MPV (Material price variance) = (Standard price – Actual price) X actual quantity

purchased and used

MUV (Material usage variance) = (Standard quantity – Actual quantity) X standard price

As per given data,

Standard Price = £10 per kg

Total Variable cost 4800 8000

Contribution 10200 17000

Fixed indirect production cost 4000 4000

Selling & Distribution costs 4000 4000

Administrative costs 2000 2000

Sales commission cost 750 1250

N.P. (Net profit) -550 5750

Absorption Cost per unit

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Marginal Cost per unit 16 16

May June

Opening stock - 200

Produced units 500 380

Sold Units 300 500

Closing stock 200 80

Calculation of material cost variances

As per the given data, three types of material variances calculated which are as follows-

MCV(Material cost variance) = Standard material cost (SMC) – Actual material cost

(AMC)

MPV (Material price variance) = (Standard price – Actual price) X actual quantity

purchased and used

MUV (Material usage variance) = (Standard quantity – Actual quantity) X standard price

As per given data,

Standard Price = £10 per kg

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Actual Price = 20900/2200 = £9.5 per kg

Actual quantity = 2200kg

Standard Quantity = 1000kg

MPV = (10-9.5)X2200= £1100 (F)

MUV = (1000-2200)X10 = £ 12000 (A)

MCV = (10X1000)-(2200X9.5) = £10900 (A)

Calculation of closing inventory of material using LIFO and Weighted average method:

Under LIFO(last in first out) method:

Date Purchased Issued Closing stock

Units Units

(in £)

Total

(in £)

Units Units

(in £)

Total(in

£)

Units units(in

£)

Total(in

£)

01/05/1

9

40 3 120

12/05/1

9

20 3.6 72 - - - 40

20

3

3.6

120

72

15/05/1

9

20

16

3.6

3

72

48

24 3 72

20/05/1

9

20 3.75 75 - - - 24

20

3

3.75

72

75

23/05/1

9

- - - 10 3.75 37.5 24

10

3

3.75

72

37.5

27/05/1

9

- - - 10

15

3.75

3

37.5

45

9 3 27

30/05/1

9

- - - 5 3 15 4 3 12

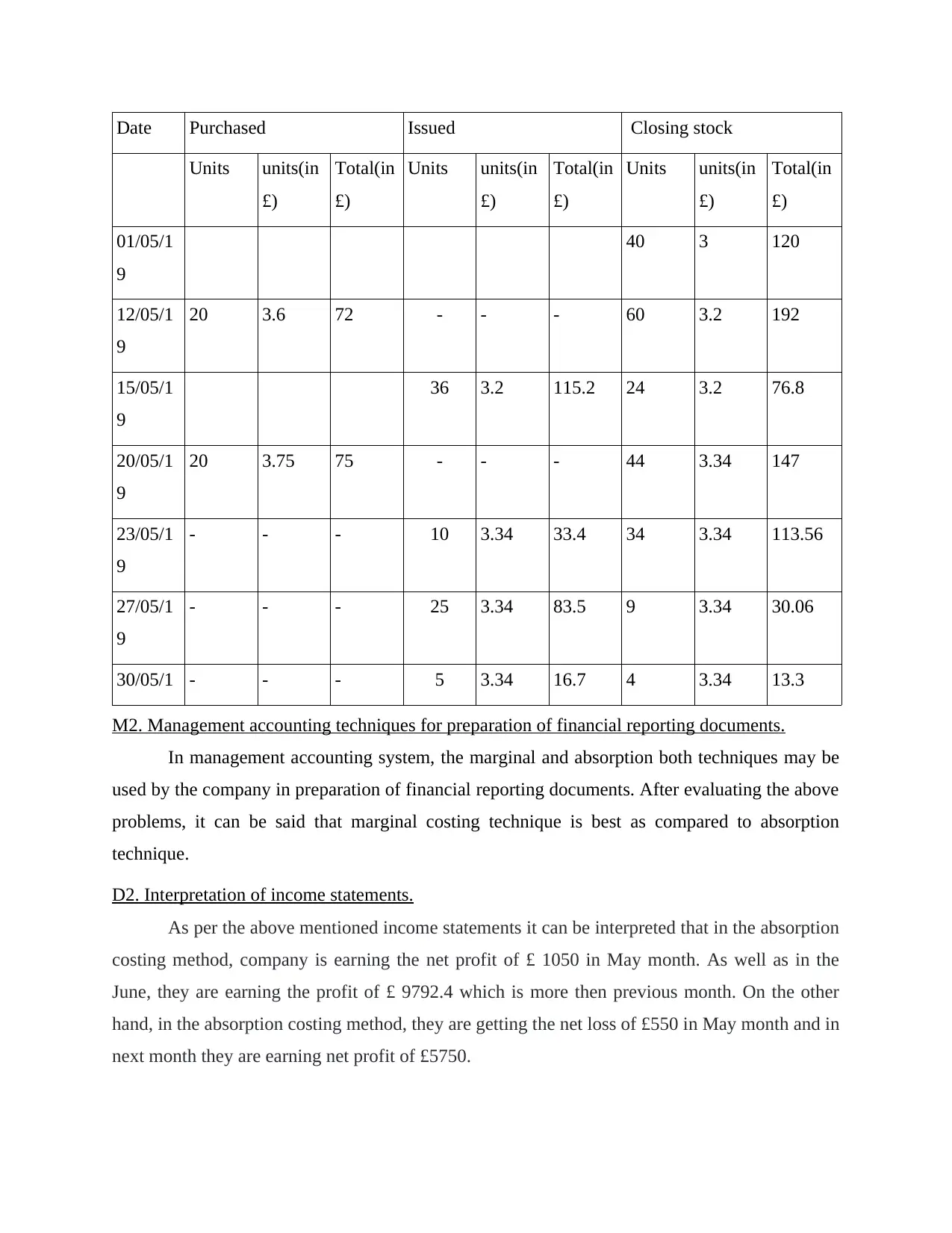

Under Weighted Average method:

Actual quantity = 2200kg

Standard Quantity = 1000kg

MPV = (10-9.5)X2200= £1100 (F)

MUV = (1000-2200)X10 = £ 12000 (A)

MCV = (10X1000)-(2200X9.5) = £10900 (A)

Calculation of closing inventory of material using LIFO and Weighted average method:

Under LIFO(last in first out) method:

Date Purchased Issued Closing stock

Units Units

(in £)

Total

(in £)

Units Units

(in £)

Total(in

£)

Units units(in

£)

Total(in

£)

01/05/1

9

40 3 120

12/05/1

9

20 3.6 72 - - - 40

20

3

3.6

120

72

15/05/1

9

20

16

3.6

3

72

48

24 3 72

20/05/1

9

20 3.75 75 - - - 24

20

3

3.75

72

75

23/05/1

9

- - - 10 3.75 37.5 24

10

3

3.75

72

37.5

27/05/1

9

- - - 10

15

3.75

3

37.5

45

9 3 27

30/05/1

9

- - - 5 3 15 4 3 12

Under Weighted Average method:

Date Purchased Issued Closing stock

Units units(in

£)

Total(in

£)

Units units(in

£)

Total(in

£)

Units units(in

£)

Total(in

£)

01/05/1

9

40 3 120

12/05/1

9

20 3.6 72 - - - 60 3.2 192

15/05/1

9

36 3.2 115.2 24 3.2 76.8

20/05/1

9

20 3.75 75 - - - 44 3.34 147

23/05/1

9

- - - 10 3.34 33.4 34 3.34 113.56

27/05/1

9

- - - 25 3.34 83.5 9 3.34 30.06

30/05/1 - - - 5 3.34 16.7 4 3.34 13.3

M2. Management accounting techniques for preparation of financial reporting documents.

In management accounting system, the marginal and absorption both techniques may be

used by the company in preparation of financial reporting documents. After evaluating the above

problems, it can be said that marginal costing technique is best as compared to absorption

technique.

D2. Interpretation of income statements.

As per the above mentioned income statements it can be interpreted that in the absorption

costing method, company is earning the net profit of £ 1050 in May month. As well as in the

June, they are earning the profit of £ 9792.4 which is more then previous month. On the other

hand, in the absorption costing method, they are getting the net loss of £550 in May month and in

next month they are earning net profit of £5750.

Units units(in

£)

Total(in

£)

Units units(in

£)

Total(in

£)

Units units(in

£)

Total(in

£)

01/05/1

9

40 3 120

12/05/1

9

20 3.6 72 - - - 60 3.2 192

15/05/1

9

36 3.2 115.2 24 3.2 76.8

20/05/1

9

20 3.75 75 - - - 44 3.34 147

23/05/1

9

- - - 10 3.34 33.4 34 3.34 113.56

27/05/1

9

- - - 25 3.34 83.5 9 3.34 30.06

30/05/1 - - - 5 3.34 16.7 4 3.34 13.3

M2. Management accounting techniques for preparation of financial reporting documents.

In management accounting system, the marginal and absorption both techniques may be

used by the company in preparation of financial reporting documents. After evaluating the above

problems, it can be said that marginal costing technique is best as compared to absorption

technique.

D2. Interpretation of income statements.

As per the above mentioned income statements it can be interpreted that in the absorption

costing method, company is earning the net profit of £ 1050 in May month. As well as in the

June, they are earning the profit of £ 9792.4 which is more then previous month. On the other

hand, in the absorption costing method, they are getting the net loss of £550 in May month and in

next month they are earning net profit of £5750.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.