management accounting

VerifiedAdded on 2023/01/11

|16

|4034

|50

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

Management accounting principles........................................................................................................3

Role of management accounting and its system.....................................................................................5

Types of management accounting techniques........................................................................................6

Management accounting is integrated with company and benefits of function to business..................9

Conclusion that reflect application of management accounting...........................................................10

Task 2........................................................................................................................................................10

Different types of planning tools with their advantages and disadvantages.........................................10

Compare how organisations are adapting management accounting systems to respond to financial

problems...............................................................................................................................................12

CONCLUSION.............................................................................................................................................13

REFERENCES..............................................................................................................................................14

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

Management accounting principles........................................................................................................3

Role of management accounting and its system.....................................................................................5

Types of management accounting techniques........................................................................................6

Management accounting is integrated with company and benefits of function to business..................9

Conclusion that reflect application of management accounting...........................................................10

Task 2........................................................................................................................................................10

Different types of planning tools with their advantages and disadvantages.........................................10

Compare how organisations are adapting management accounting systems to respond to financial

problems...............................................................................................................................................12

CONCLUSION.............................................................................................................................................13

REFERENCES..............................................................................................................................................14

INTRODUCTION

Management accounting is known as managerial accounting, it defined as procedure of

providing financial info and resources to manager in decision making. It is only utilized by

internal group of company and this is only thing which makes it different from other accounting

such as financial. The current report is based on Napoleon hotel, is established in east London’s

Shoreditch has one suite. This study explains principles of management accounting and its role,

it also justified role of management accounting systems, techniques and methods used within it

by presenting calculations for an income statement.

Furthermore, this assignment will define critical application of management accounting.

Comparison between three planning tools utilize in MA including advantages and

disadvantages.Moreover, this report will compare ways in which concept applied and its

effectiveness in dealing with financial problems. At last conclusion and suggestions will be done

in context of company.

TASK 1

Management accounting principles

Designing & compiling-

Accounting info, reports and other evidence of past, current and the future outcomes can

be complied & created to meet needs of specific business (Burger and Middelberg, 2018).

According to this principle management accounting systems is developed in such as way

presenting relevant data.

Management by exception-

Principle of management by exception is used when presenting info to administration. It

means that standard costing methods and budgetary control programme is follower in MA

system. In that way, performance is compared with pre-identified one for finding deviations.

Control at source accounting-

Costs are controlled at points at which management are incurred control at source

accounting. Performance of workers, usage of service and details of resource problems are

Management accounting is known as managerial accounting, it defined as procedure of

providing financial info and resources to manager in decision making. It is only utilized by

internal group of company and this is only thing which makes it different from other accounting

such as financial. The current report is based on Napoleon hotel, is established in east London’s

Shoreditch has one suite. This study explains principles of management accounting and its role,

it also justified role of management accounting systems, techniques and methods used within it

by presenting calculations for an income statement.

Furthermore, this assignment will define critical application of management accounting.

Comparison between three planning tools utilize in MA including advantages and

disadvantages.Moreover, this report will compare ways in which concept applied and its

effectiveness in dealing with financial problems. At last conclusion and suggestions will be done

in context of company.

TASK 1

Management accounting principles

Designing & compiling-

Accounting info, reports and other evidence of past, current and the future outcomes can

be complied & created to meet needs of specific business (Burger and Middelberg, 2018).

According to this principle management accounting systems is developed in such as way

presenting relevant data.

Management by exception-

Principle of management by exception is used when presenting info to administration. It

means that standard costing methods and budgetary control programme is follower in MA

system. In that way, performance is compared with pre-identified one for finding deviations.

Control at source accounting-

Costs are controlled at points at which management are incurred control at source

accounting. Performance of workers, usage of service and details of resource problems are

prepared in form of qualitative & quantitative info, in this manner control can be applied over

staff and other things.

Accounting for inflation-

Income cannot be earned unless capital is handled intact in actual terms, which means

that money value is unstable. So it is essential according to this principle to assess value of

capital supported by entrepreneurs concern in term of real value of money via revaluation

accounting.

Use of return on investment-

It is also known as return on capital employed, return rate reflect efficiency of

organization concern.

Utility-

Management accounting programmes and related systems had to use only as longer as

they serve a effective purpose.

Integration-

Accordant to this principle, all needed info of management is connected so that it can be

utilize efficiently at maximum and at same period accounting service is offered at minimum cost.

Absorption of overhead costs-

Over head costs are adopted on anyone of pr-identified basis. They are combination of

indirect material, expenses and labor. Selected methods for absorption of overheads will bring

about desired outcomes in effective manner.

Use of resources-

According to this management accounting principle, people use all accessible resources

in systematic manner, reason is that some assets are available in plenty only in reason and some

other are accessible in scarcity throughout time period.

Controllable and uncontrollable costs-

On basis of controllability of costs, it can be classified into two kinds such as

uncontrollable and controllable. There is no meaning of taking phase to handle uncontrollable

costs. Management accounting systems are caters methods to control controllable costs

(Fengzhou, Shu and You, 2019).

Forward looking approach-

staff and other things.

Accounting for inflation-

Income cannot be earned unless capital is handled intact in actual terms, which means

that money value is unstable. So it is essential according to this principle to assess value of

capital supported by entrepreneurs concern in term of real value of money via revaluation

accounting.

Use of return on investment-

It is also known as return on capital employed, return rate reflect efficiency of

organization concern.

Utility-

Management accounting programmes and related systems had to use only as longer as

they serve a effective purpose.

Integration-

Accordant to this principle, all needed info of management is connected so that it can be

utilize efficiently at maximum and at same period accounting service is offered at minimum cost.

Absorption of overhead costs-

Over head costs are adopted on anyone of pr-identified basis. They are combination of

indirect material, expenses and labor. Selected methods for absorption of overheads will bring

about desired outcomes in effective manner.

Use of resources-

According to this management accounting principle, people use all accessible resources

in systematic manner, reason is that some assets are available in plenty only in reason and some

other are accessible in scarcity throughout time period.

Controllable and uncontrollable costs-

On basis of controllability of costs, it can be classified into two kinds such as

uncontrollable and controllable. There is no meaning of taking phase to handle uncontrollable

costs. Management accounting systems are caters methods to control controllable costs

(Fengzhou, Shu and You, 2019).

Forward looking approach-

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

It can guess future issues through standards costing procedures by means of fixing

standard. In this term, further problems may be controlled to occur.

Appropriate means-

Accordant to principle, most suitable means of accounting, presenting and recording

accounting info can be selected, which means that appropriate mechanization of accounts is

utilize in every business companies.

Personal contacts-

This is the last principle of management accounting, according to which personal contact

with foreman, departmental manager and other could be replaced wholly by statements and

reports. It mean that personal interaction avoids miscomprehend between staff and top authority.

Role of management accounting and its system

Management accounting refer to efficient utilize of all those info which is connected to

management and that evolved effective decision making of companies (Mitter and Hiebl,

2017).Role of management accounting include gathering, reporting and recording financial data

from different units of companies, observe and examine their budget & suggest their allocation

and funding.

Budgeting-

It is the main roles of MA, for a small firm’s budget are direct to all expenditures. Small

companies decide a budget every era to fix their expenses on each procedure that is production

and operation cost and then further investment.

Stewardship accounting-

Another role of management accounting is to design frame work of cost as well as

financial accounts and prepares studies for routine operational & financial decision making.

Long and short term planning-

The third role of management accounting is forecasting the further economic and

business events for developing further plan like long term plans, formulating corporate strategy

and strategic MA (Gomez-Conde and Lopez-Valeiras, 2018).

Type of systems and their role-

Price optimizing systems-

This system is use of mathematical analysis by an organization to identify how

consumers will respond to varied prices for their products and services through varied channels.

standard. In this term, further problems may be controlled to occur.

Appropriate means-

Accordant to principle, most suitable means of accounting, presenting and recording

accounting info can be selected, which means that appropriate mechanization of accounts is

utilize in every business companies.

Personal contacts-

This is the last principle of management accounting, according to which personal contact

with foreman, departmental manager and other could be replaced wholly by statements and

reports. It mean that personal interaction avoids miscomprehend between staff and top authority.

Role of management accounting and its system

Management accounting refer to efficient utilize of all those info which is connected to

management and that evolved effective decision making of companies (Mitter and Hiebl,

2017).Role of management accounting include gathering, reporting and recording financial data

from different units of companies, observe and examine their budget & suggest their allocation

and funding.

Budgeting-

It is the main roles of MA, for a small firm’s budget are direct to all expenditures. Small

companies decide a budget every era to fix their expenses on each procedure that is production

and operation cost and then further investment.

Stewardship accounting-

Another role of management accounting is to design frame work of cost as well as

financial accounts and prepares studies for routine operational & financial decision making.

Long and short term planning-

The third role of management accounting is forecasting the further economic and

business events for developing further plan like long term plans, formulating corporate strategy

and strategic MA (Gomez-Conde and Lopez-Valeiras, 2018).

Type of systems and their role-

Price optimizing systems-

This system is use of mathematical analysis by an organization to identify how

consumers will respond to varied prices for their products and services through varied channels.

The role of this programme is to determine prices that firm determine will best meet their set

objectives such as maximizing operating profit.

Cost accounting systems-

It is a framework utilize by companies to estimate cost of their services or items

profitability analysis, cost control and inventory valuation. The role of this system is to keep

production activities on top.

Job costing programmes-

This system it suited for conditions where products are manufactured as per order &

specification given by consumers.It includes the procedure of collecting all essential information

related to cost with a particular manufacture job.It help manager of Hotel to calculate profit

earned on people jobs, supporting them to better ascertain whether particular role are desirable to

purse in the future.

Types of management accounting techniques

The different types of management accounting techniques are stated below.

Marginal costing

In this, variable cost is distributed to the unit cost. It helps in determining and analyzing

the cost information and profitability in accordance with the change in the level of activity

(Collis and Hussey, 2017). The fixed cost for the period is written off against the contribution.

This system helps in determining the break-even point after which company starts earning

profits. It assists in determining the optimum level of production.

Absorption costing

This method considers all the cost and expenses pertaining to the cost of production

irrespective of whether it is fixed or variable cost (Tabitha and Oluyinka, 2016). It is required for

external reporting and follows Generally Accepted Accounting Principles (GAAP) and

International Financial Reporting Standards (IFRS).

Cost profit volume analysis

This technique is used for analyzing how change in the volume and cost can affect the

income of the company (Schmid, 2019). It is based on certain assumptions like sales price and

variable cost per unit remains constant and everything produced is sold. For cost profit volume

analysis, cost related information is required to be bifurcated into fixed and variable cost.

objectives such as maximizing operating profit.

Cost accounting systems-

It is a framework utilize by companies to estimate cost of their services or items

profitability analysis, cost control and inventory valuation. The role of this system is to keep

production activities on top.

Job costing programmes-

This system it suited for conditions where products are manufactured as per order &

specification given by consumers.It includes the procedure of collecting all essential information

related to cost with a particular manufacture job.It help manager of Hotel to calculate profit

earned on people jobs, supporting them to better ascertain whether particular role are desirable to

purse in the future.

Types of management accounting techniques

The different types of management accounting techniques are stated below.

Marginal costing

In this, variable cost is distributed to the unit cost. It helps in determining and analyzing

the cost information and profitability in accordance with the change in the level of activity

(Collis and Hussey, 2017). The fixed cost for the period is written off against the contribution.

This system helps in determining the break-even point after which company starts earning

profits. It assists in determining the optimum level of production.

Absorption costing

This method considers all the cost and expenses pertaining to the cost of production

irrespective of whether it is fixed or variable cost (Tabitha and Oluyinka, 2016). It is required for

external reporting and follows Generally Accepted Accounting Principles (GAAP) and

International Financial Reporting Standards (IFRS).

Cost profit volume analysis

This technique is used for analyzing how change in the volume and cost can affect the

income of the company (Schmid, 2019). It is based on certain assumptions like sales price and

variable cost per unit remains constant and everything produced is sold. For cost profit volume

analysis, cost related information is required to be bifurcated into fixed and variable cost.

Applying a range of management accounting techniques and produce appropriate financial

reporting documents

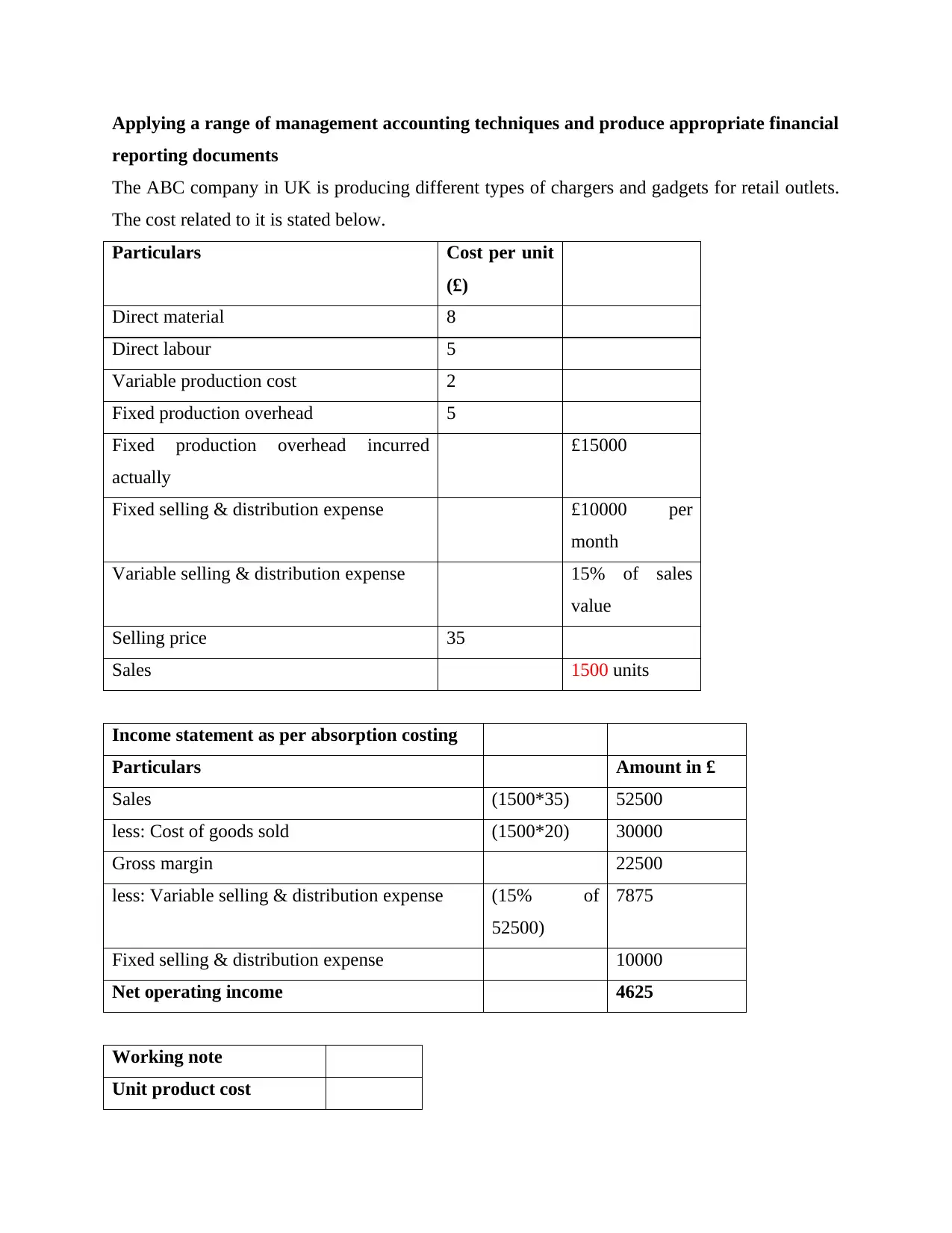

The ABC company in UK is producing different types of chargers and gadgets for retail outlets.

The cost related to it is stated below.

Particulars Cost per unit

(£)

Direct material 8

Direct labour 5

Variable production cost 2

Fixed production overhead 5

Fixed production overhead incurred

actually

£15000

Fixed selling & distribution expense £10000 per

month

Variable selling & distribution expense 15% of sales

value

Selling price 35

Sales 1500 units

Income statement as per absorption costing

Particulars Amount in £

Sales (1500*35) 52500

less: Cost of goods sold (1500*20) 30000

Gross margin 22500

less: Variable selling & distribution expense (15% of

52500)

7875

Fixed selling & distribution expense 10000

Net operating income 4625

Working note

Unit product cost

reporting documents

The ABC company in UK is producing different types of chargers and gadgets for retail outlets.

The cost related to it is stated below.

Particulars Cost per unit

(£)

Direct material 8

Direct labour 5

Variable production cost 2

Fixed production overhead 5

Fixed production overhead incurred

actually

£15000

Fixed selling & distribution expense £10000 per

month

Variable selling & distribution expense 15% of sales

value

Selling price 35

Sales 1500 units

Income statement as per absorption costing

Particulars Amount in £

Sales (1500*35) 52500

less: Cost of goods sold (1500*20) 30000

Gross margin 22500

less: Variable selling & distribution expense (15% of

52500)

7875

Fixed selling & distribution expense 10000

Net operating income 4625

Working note

Unit product cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

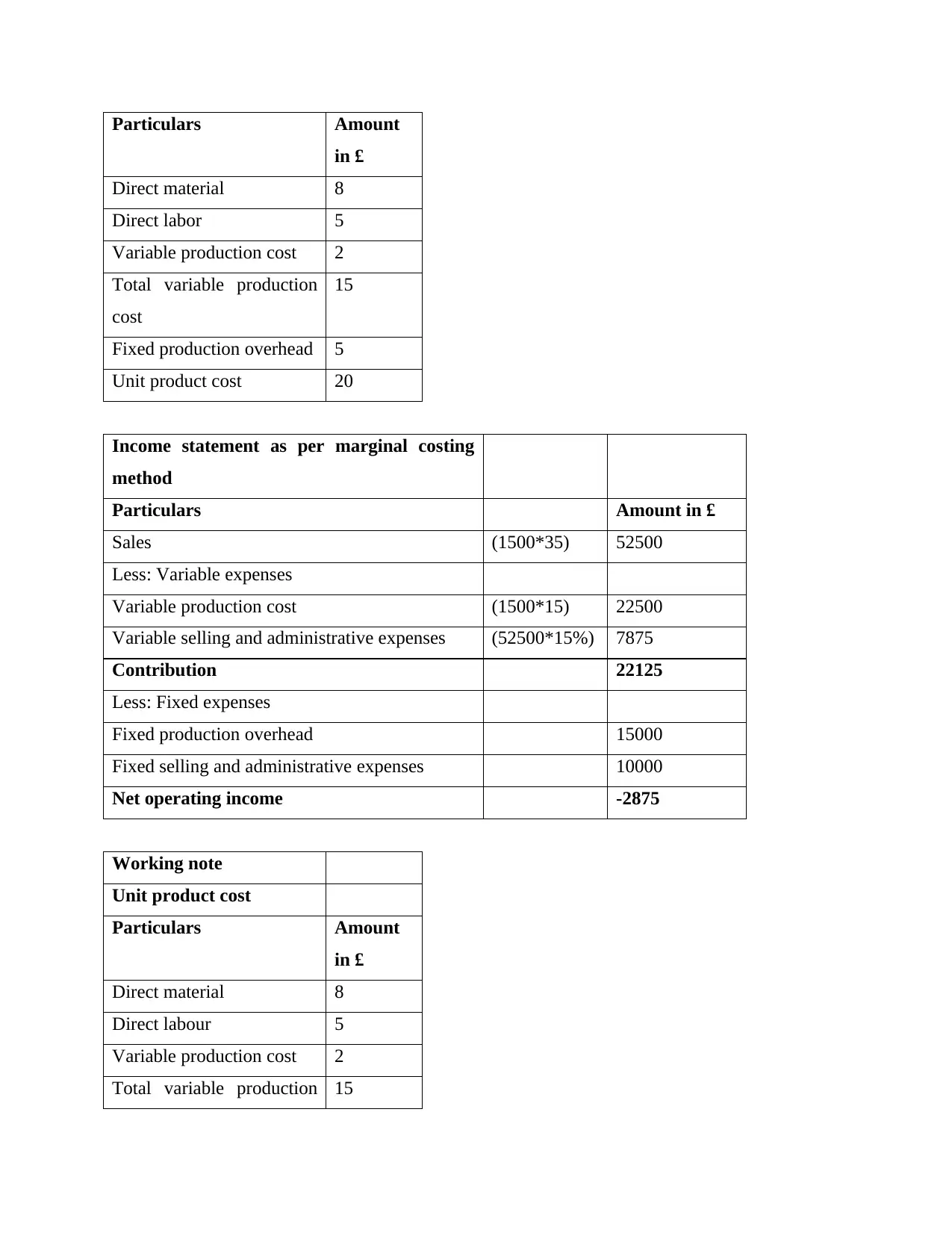

Particulars Amount

in £

Direct material 8

Direct labor 5

Variable production cost 2

Total variable production

cost

15

Fixed production overhead 5

Unit product cost 20

Income statement as per marginal costing

method

Particulars Amount in £

Sales (1500*35) 52500

Less: Variable expenses

Variable production cost (1500*15) 22500

Variable selling and administrative expenses (52500*15%) 7875

Contribution 22125

Less: Fixed expenses

Fixed production overhead 15000

Fixed selling and administrative expenses 10000

Net operating income -2875

Working note

Unit product cost

Particulars Amount

in £

Direct material 8

Direct labour 5

Variable production cost 2

Total variable production 15

in £

Direct material 8

Direct labor 5

Variable production cost 2

Total variable production

cost

15

Fixed production overhead 5

Unit product cost 20

Income statement as per marginal costing

method

Particulars Amount in £

Sales (1500*35) 52500

Less: Variable expenses

Variable production cost (1500*15) 22500

Variable selling and administrative expenses (52500*15%) 7875

Contribution 22125

Less: Fixed expenses

Fixed production overhead 15000

Fixed selling and administrative expenses 10000

Net operating income -2875

Working note

Unit product cost

Particulars Amount

in £

Direct material 8

Direct labour 5

Variable production cost 2

Total variable production 15

cost

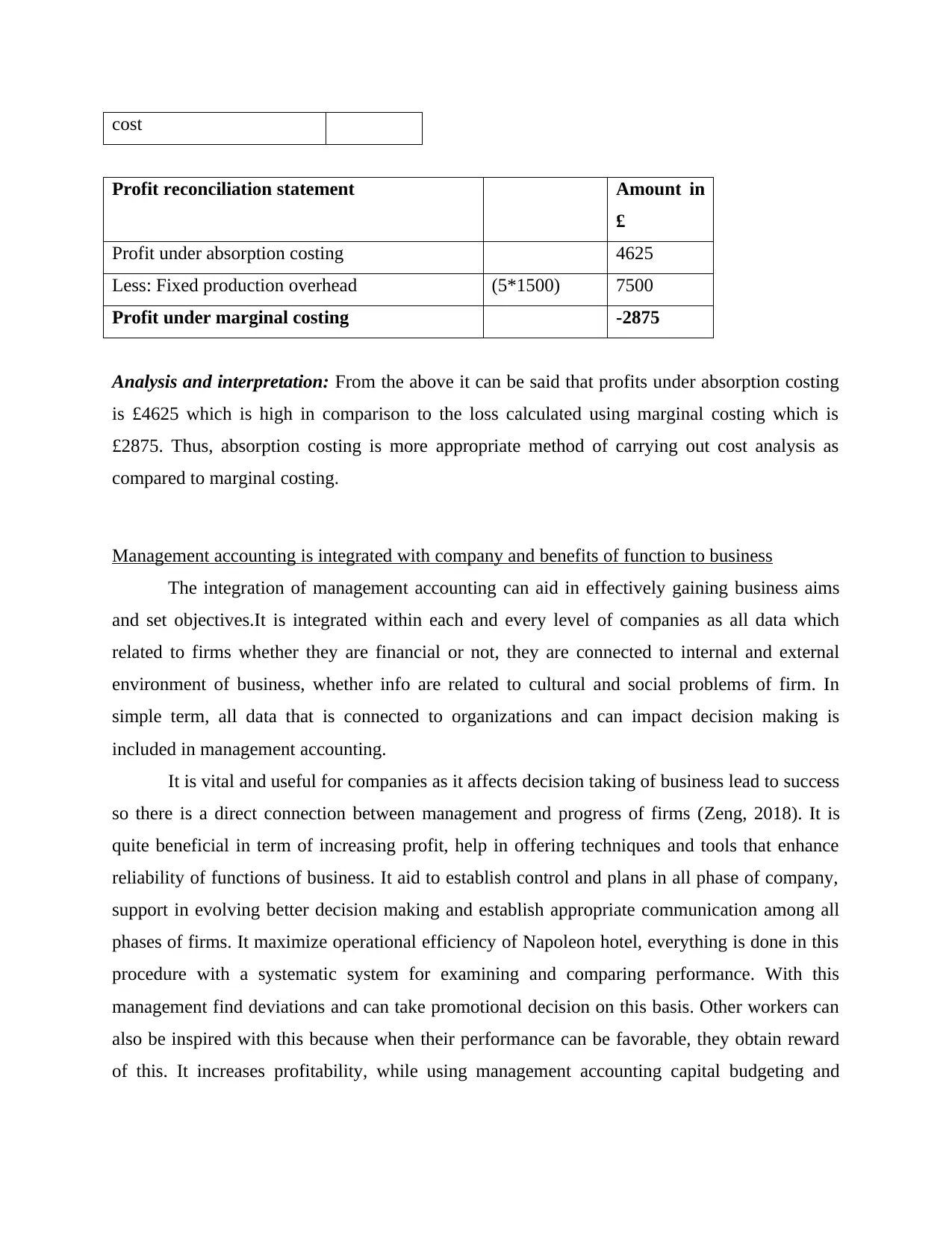

Profit reconciliation statement Amount in

£

Profit under absorption costing 4625

Less: Fixed production overhead (5*1500) 7500

Profit under marginal costing -2875

Analysis and interpretation: From the above it can be said that profits under absorption costing

is £4625 which is high in comparison to the loss calculated using marginal costing which is

£2875. Thus, absorption costing is more appropriate method of carrying out cost analysis as

compared to marginal costing.

Management accounting is integrated with company and benefits of function to business

The integration of management accounting can aid in effectively gaining business aims

and set objectives.It is integrated within each and every level of companies as all data which

related to firms whether they are financial or not, they are connected to internal and external

environment of business, whether info are related to cultural and social problems of firm. In

simple term, all data that is connected to organizations and can impact decision making is

included in management accounting.

It is vital and useful for companies as it affects decision taking of business lead to success

so there is a direct connection between management and progress of firms (Zeng, 2018). It is

quite beneficial in term of increasing profit, help in offering techniques and tools that enhance

reliability of functions of business. It aid to establish control and plans in all phase of company,

support in evolving better decision making and establish appropriate communication among all

phases of firms. It maximize operational efficiency of Napoleon hotel, everything is done in this

procedure with a systematic system for examining and comparing performance. With this

management find deviations and can take promotional decision on this basis. Other workers can

also be inspired with this because when their performance can be favorable, they obtain reward

of this. It increases profitability, while using management accounting capital budgeting and

Profit reconciliation statement Amount in

£

Profit under absorption costing 4625

Less: Fixed production overhead (5*1500) 7500

Profit under marginal costing -2875

Analysis and interpretation: From the above it can be said that profits under absorption costing

is £4625 which is high in comparison to the loss calculated using marginal costing which is

£2875. Thus, absorption costing is more appropriate method of carrying out cost analysis as

compared to marginal costing.

Management accounting is integrated with company and benefits of function to business

The integration of management accounting can aid in effectively gaining business aims

and set objectives.It is integrated within each and every level of companies as all data which

related to firms whether they are financial or not, they are connected to internal and external

environment of business, whether info are related to cultural and social problems of firm. In

simple term, all data that is connected to organizations and can impact decision making is

included in management accounting.

It is vital and useful for companies as it affects decision taking of business lead to success

so there is a direct connection between management and progress of firms (Zeng, 2018). It is

quite beneficial in term of increasing profit, help in offering techniques and tools that enhance

reliability of functions of business. It aid to establish control and plans in all phase of company,

support in evolving better decision making and establish appropriate communication among all

phases of firms. It maximize operational efficiency of Napoleon hotel, everything is done in this

procedure with a systematic system for examining and comparing performance. With this

management find deviations and can take promotional decision on this basis. Other workers can

also be inspired with this because when their performance can be favorable, they obtain reward

of this. It increases profitability, while using management accounting capital budgeting and

budgetary control tool, firm can effectively success to reduce capital & operational expenditures.

After this, business can reduce their prices and them they will get super profits.

Conclusion that reflect application of management accounting

From above analysis it has been concluded that management accounting is quite

beneficial for Napoleon hotel in term increasing productivity, profit margin and revenue rather

than before. By applying management accounting within company or business practices workers

can examine in detail which items and accounts are earning the most money. Sales figure aid

them to pin down whether organization goods are attracting a specific demographic and whether

it is benefits to market specific items at particular time. This accounting info caters

administration tools they need to target marketing attempts and pinpoint manufacture numbers. It

has been examine that management accounting is used in long and short term decision making or

including financial health of hotel.It aid manager make operational and financial judgments

intended to support increase business operational efficiency while also aids in making long term

decision regarding investment as well. Uses of management accounting include permitting

administration to compare their accounts with real forecasts or budgets. It uses to manage

resources better, determine trends in business and highlight variations in spending or income

which may needed attention.

Task 2

Different types of planning tools with their advantages and disadvantages

Budgeting helps the businesses in planning for the future by allocating funds to various

business activities. It also helps in measuring any deviation of the actual from the budgeted ones.

The different types of planning tools are stated below.

Zero based budgeting

It is the technique which does not take into account the previous year’s data while

preparing the budget (Zemrani, 2019). Under this, proper research is carried out in relation to the

budget. This technique results into less errors and mistakes as it is prepared completely from the

scratch and nothing is taken from the previous year. It results into more accurate budgets with

very least variances.

Advantages

After this, business can reduce their prices and them they will get super profits.

Conclusion that reflect application of management accounting

From above analysis it has been concluded that management accounting is quite

beneficial for Napoleon hotel in term increasing productivity, profit margin and revenue rather

than before. By applying management accounting within company or business practices workers

can examine in detail which items and accounts are earning the most money. Sales figure aid

them to pin down whether organization goods are attracting a specific demographic and whether

it is benefits to market specific items at particular time. This accounting info caters

administration tools they need to target marketing attempts and pinpoint manufacture numbers. It

has been examine that management accounting is used in long and short term decision making or

including financial health of hotel.It aid manager make operational and financial judgments

intended to support increase business operational efficiency while also aids in making long term

decision regarding investment as well. Uses of management accounting include permitting

administration to compare their accounts with real forecasts or budgets. It uses to manage

resources better, determine trends in business and highlight variations in spending or income

which may needed attention.

Task 2

Different types of planning tools with their advantages and disadvantages

Budgeting helps the businesses in planning for the future by allocating funds to various

business activities. It also helps in measuring any deviation of the actual from the budgeted ones.

The different types of planning tools are stated below.

Zero based budgeting

It is the technique which does not take into account the previous year’s data while

preparing the budget (Zemrani, 2019). Under this, proper research is carried out in relation to the

budget. This technique results into less errors and mistakes as it is prepared completely from the

scratch and nothing is taken from the previous year. It results into more accurate budgets with

very least variances.

Advantages

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

New research is conducted each time budget is prepared.

Does not rely on the previous year budget.

Relevant for the businesses which are prone to frequent changes.

Disadvantages

It is a time-consuming process and requires lots of efforts.

It is very costly method to implement in the organization.

Activity Based Budgeting

In this, budget is prepared by taking into consideration the business activities rather than

departments. Budget is prepared in respect to the forecast the resources to be used and

productivity generated under specific activities (Ozyurek and Uluturk, 2016). It does not use the

budgets which are prepared from the previous year data for the current year budget. This

technique helps in identifying the cost and expenses pertaining to each business activity a

product is undertaken. It helps the organization in identifying any loophole in the system so that

effective actions can be taken to order to avoid wastage and reduce cost.

Advantages

This method is very easy to implement.

It also helps in identifying any variation in the production process which leads to cost

reduction.

It prepared without considering the previous year’s budget.

Disadvantages

It requires highly qualified personnel to undertake activity-based budgeting.

It is an expensive method.

Operational Budgets

This budget is prepared for with respect to the operating activities of the business (Cokins

and Dybvig, 2018). It includes forecasting the income and expenses of the organization which is

based on past years trends. This provides the company a map about the expenses that it can incur

during the particular time or for specific activity. It assists the organization in effective and

proper allocation of the resources among various departments and various other business

operations. The budgetary control provides deep analysis of the operational income and

expenditures.

Advantages

Does not rely on the previous year budget.

Relevant for the businesses which are prone to frequent changes.

Disadvantages

It is a time-consuming process and requires lots of efforts.

It is very costly method to implement in the organization.

Activity Based Budgeting

In this, budget is prepared by taking into consideration the business activities rather than

departments. Budget is prepared in respect to the forecast the resources to be used and

productivity generated under specific activities (Ozyurek and Uluturk, 2016). It does not use the

budgets which are prepared from the previous year data for the current year budget. This

technique helps in identifying the cost and expenses pertaining to each business activity a

product is undertaken. It helps the organization in identifying any loophole in the system so that

effective actions can be taken to order to avoid wastage and reduce cost.

Advantages

This method is very easy to implement.

It also helps in identifying any variation in the production process which leads to cost

reduction.

It prepared without considering the previous year’s budget.

Disadvantages

It requires highly qualified personnel to undertake activity-based budgeting.

It is an expensive method.

Operational Budgets

This budget is prepared for with respect to the operating activities of the business (Cokins

and Dybvig, 2018). It includes forecasting the income and expenses of the organization which is

based on past years trends. This provides the company a map about the expenses that it can incur

during the particular time or for specific activity. It assists the organization in effective and

proper allocation of the resources among various departments and various other business

operations. The budgetary control provides deep analysis of the operational income and

expenditures.

Advantages

These budgets are very easy to prepare and does not require lots of time and efforts.

It helps in proper allocation of resources.

This budget helps in exercising control over the various cost by providing a defined

spending plan.

Disadvantages

It uses past year budget which may lead to inaccurate decisions.

In this, it is impossible to make accurate forecast about the future.

Compare how organizations are adapting management accounting systems to respond to

financial problems

With the new evolving organizations where data is considered the most significant part

for evaluating the presentation of the business. The budgetary control techniques that can be

utilized for identifying the finance related issues are described below.

Benchmarking

It is the performance measuring tool in which the organization compare its performance

with another organization within the same industry (John and Eeckhout, 2018). It has certain

standards such as working pattern, expense per unit produced etc. the performance is compared

and then the deviation in the result is identified. It helps the organization in identifying the areas

of improvement and what makes the other business more prevalent which may include business

processes as well. The comparison is also includes processes, system, equipment used by the

competitor which helped it in attaining efficiency.

Key performance indicators

Under this method, various targets are set up which helps in recognising the progress of

the organization (Muhammad and et.al, 2018). It helps in checking the performance of the

organization dependent on certain parameters. There are different kinds of KPIs as per the

requirement of the business such as cost per unit, increase in sales etc. It helps in improving the

overall performance of the business.

Budgetary targets

In this method, the budgetary targets are set which helps in measuring and comparing the

actual result from the budgeted ones (Karpenko, Voronzhak and Sapron, 2017). This helps in

identifying the variation in the result and reasons are identified for the same. This method also

It helps in proper allocation of resources.

This budget helps in exercising control over the various cost by providing a defined

spending plan.

Disadvantages

It uses past year budget which may lead to inaccurate decisions.

In this, it is impossible to make accurate forecast about the future.

Compare how organizations are adapting management accounting systems to respond to

financial problems

With the new evolving organizations where data is considered the most significant part

for evaluating the presentation of the business. The budgetary control techniques that can be

utilized for identifying the finance related issues are described below.

Benchmarking

It is the performance measuring tool in which the organization compare its performance

with another organization within the same industry (John and Eeckhout, 2018). It has certain

standards such as working pattern, expense per unit produced etc. the performance is compared

and then the deviation in the result is identified. It helps the organization in identifying the areas

of improvement and what makes the other business more prevalent which may include business

processes as well. The comparison is also includes processes, system, equipment used by the

competitor which helped it in attaining efficiency.

Key performance indicators

Under this method, various targets are set up which helps in recognising the progress of

the organization (Muhammad and et.al, 2018). It helps in checking the performance of the

organization dependent on certain parameters. There are different kinds of KPIs as per the

requirement of the business such as cost per unit, increase in sales etc. It helps in improving the

overall performance of the business.

Budgetary targets

In this method, the budgetary targets are set which helps in measuring and comparing the

actual result from the budgeted ones (Karpenko, Voronzhak and Sapron, 2017). This helps in

identifying the variation in the result and reasons are identified for the same. This method also

helps the business in identifying its weaknesses which has restrain it from achieving the desired

result. This method will assist the organization in making relevant changes in their strategies.

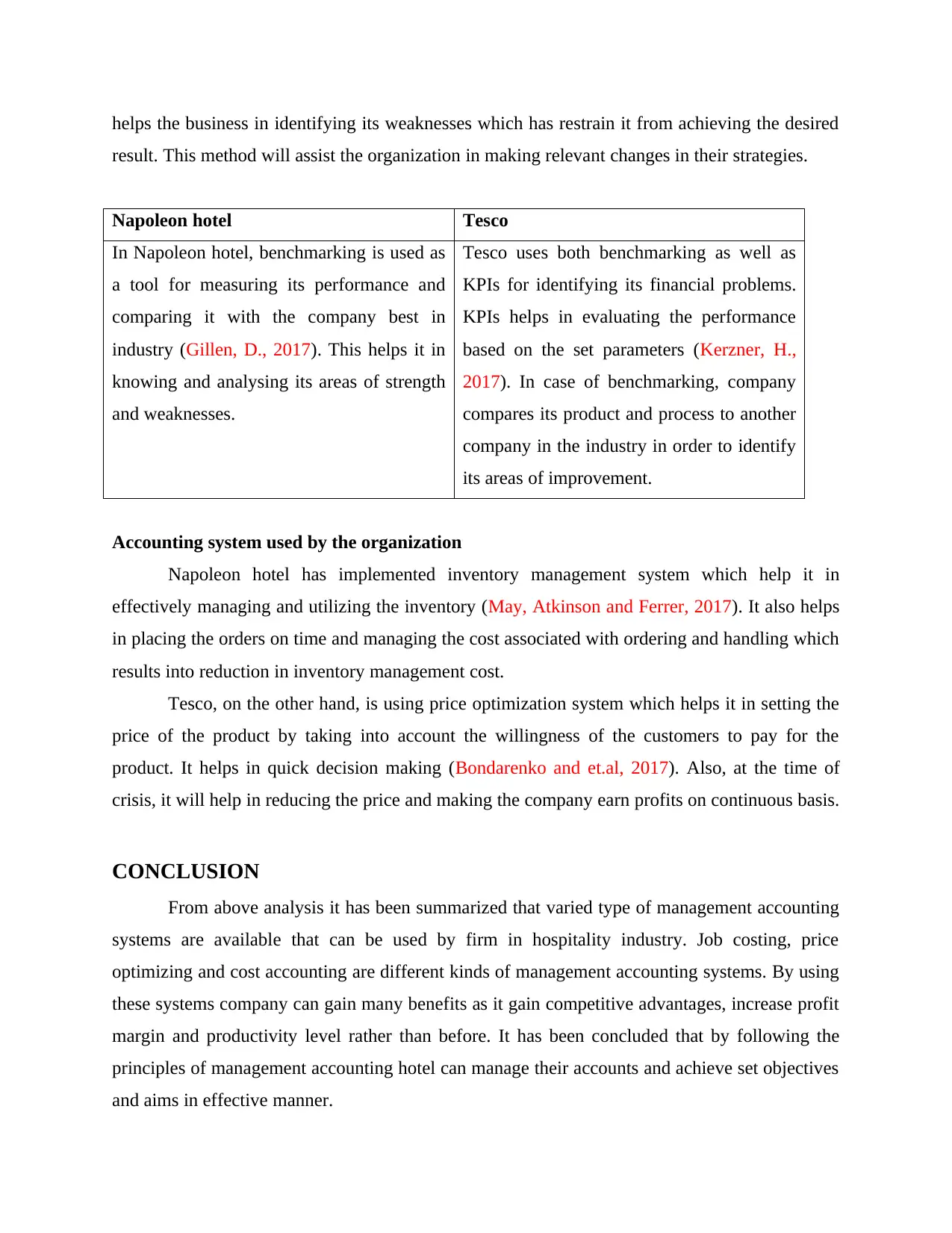

Napoleon hotel Tesco

In Napoleon hotel, benchmarking is used as

a tool for measuring its performance and

comparing it with the company best in

industry (Gillen, D., 2017). This helps it in

knowing and analysing its areas of strength

and weaknesses.

Tesco uses both benchmarking as well as

KPIs for identifying its financial problems.

KPIs helps in evaluating the performance

based on the set parameters (Kerzner, H.,

2017). In case of benchmarking, company

compares its product and process to another

company in the industry in order to identify

its areas of improvement.

Accounting system used by the organization

Napoleon hotel has implemented inventory management system which help it in

effectively managing and utilizing the inventory (May, Atkinson and Ferrer, 2017). It also helps

in placing the orders on time and managing the cost associated with ordering and handling which

results into reduction in inventory management cost.

Tesco, on the other hand, is using price optimization system which helps it in setting the

price of the product by taking into account the willingness of the customers to pay for the

product. It helps in quick decision making (Bondarenko and et.al, 2017). Also, at the time of

crisis, it will help in reducing the price and making the company earn profits on continuous basis.

CONCLUSION

From above analysis it has been summarized that varied type of management accounting

systems are available that can be used by firm in hospitality industry. Job costing, price

optimizing and cost accounting are different kinds of management accounting systems. By using

these systems company can gain many benefits as it gain competitive advantages, increase profit

margin and productivity level rather than before. It has been concluded that by following the

principles of management accounting hotel can manage their accounts and achieve set objectives

and aims in effective manner.

result. This method will assist the organization in making relevant changes in their strategies.

Napoleon hotel Tesco

In Napoleon hotel, benchmarking is used as

a tool for measuring its performance and

comparing it with the company best in

industry (Gillen, D., 2017). This helps it in

knowing and analysing its areas of strength

and weaknesses.

Tesco uses both benchmarking as well as

KPIs for identifying its financial problems.

KPIs helps in evaluating the performance

based on the set parameters (Kerzner, H.,

2017). In case of benchmarking, company

compares its product and process to another

company in the industry in order to identify

its areas of improvement.

Accounting system used by the organization

Napoleon hotel has implemented inventory management system which help it in

effectively managing and utilizing the inventory (May, Atkinson and Ferrer, 2017). It also helps

in placing the orders on time and managing the cost associated with ordering and handling which

results into reduction in inventory management cost.

Tesco, on the other hand, is using price optimization system which helps it in setting the

price of the product by taking into account the willingness of the customers to pay for the

product. It helps in quick decision making (Bondarenko and et.al, 2017). Also, at the time of

crisis, it will help in reducing the price and making the company earn profits on continuous basis.

CONCLUSION

From above analysis it has been summarized that varied type of management accounting

systems are available that can be used by firm in hospitality industry. Job costing, price

optimizing and cost accounting are different kinds of management accounting systems. By using

these systems company can gain many benefits as it gain competitive advantages, increase profit

margin and productivity level rather than before. It has been concluded that by following the

principles of management accounting hotel can manage their accounts and achieve set objectives

and aims in effective manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Book and Journals

Burger, A. B. and Middelberg, S. L., 2018. An evaluation of Global Management Accounting

Principles in the sustainability of a South African mechanised piggery. Journal of

Economic and Financial Sciences. 11(1). pp.1-9.

Cokins, G. and Dybvig, A., 2018. NEXT GENERATION BUDGETING: If you want more

accurate results from your budgeting process, it may be time to switch from traditional

budgeting to operational budgeting. Strategic Finance. 99(10). pp.38-46.

Collis, J. and Hussey, R., 2017. Cost and management accounting. Macmillan International

Higher Education.

Fengzhou, W., Shu, H. and You, H., 2019. Discussion on the Basic Assumptions of Management

Accounting.

Gomez-Conde, J. and Lopez-Valeiras, E., 2018. The dual role of management accounting and

control systems in exports: Drivers and payoffs. Spanish Journal of Finance and

Accounting/Revista Española de Financiación y Contabilidad. 47(3). pp.307-328.

John, L. K. and Eeckhout, L., 2018. Performance evaluation and benchmarking. CRC Press.

Karpenko, L. M., Voronzhak, P. V. and Sapron, N. O., 2017. FEATURES OF THE

ORGANIZATION AND ESTABLISHMENT OF THE BUDGETING MANAGEMENT

AT THE ENTERPRISE IN GLOBALIZATION CHANGES CONDITIONS. Science and

practice: an innovative approach. p.110.

Mitter, C. and Hiebl, M.R., 2017. The role of management accounting in international

entrepreneurship. Journal of Accounting & Organizational Change.

Muhammad, U. and et.al, 2018, May. An approach for implementing key performance indicators

of a discrete manufacturing simulator based on the ISO 22400 standard. In 2018 IEEE

Industrial Cyber-Physical Systems (ICPS) (pp. 629-636). IEEE.

Ozyurek, H. and Uluturk, Y., 2016. Flexible budgeting under time-driven activity based cost as a

tool in management accounting: Application in educational institution. Journal of

Administrative and Business Studies. 2(2). pp.64-70.

Schmid, A. A., 2019. Benefit-cost analysis: A political economy approach. Routledge.

Tabitha, N. and Oluyinka, I. O., 2016. Cost Accounting Techniques Adopted By Manufacturing

And Service Industry Within The Last Decade. International Journal Of Advances In

Management And Economics. 5(1). pp.48-61.

Zemrani, A., 2019. Budgeting in the United States: From Theory to Practice Using Higher

Education. In Performance-Based Budgeting in the Public Sector (pp. 29-60). Palgrave

Macmillan, Cham.

Zeng, H., 2018. Reciprocal Interaction between Management Accounting and Other

Management Roles. Open Access Library Journal. 5(11). p.1.

Gillen, D., 2017. Benchmarking and performance measurement: the role in quality

management. AM Brewer, KJ Button, & DA Henshe, Handbook of Logistics and Supply-

Chain Management (Handbooks in Transport, Volume 2). pp.325-338.

Kerzner, H., 2017. Project management metrics, KPIs, and dashboards: a guide to measuring

and monitoring project performance. John Wiley & Sons.

Book and Journals

Burger, A. B. and Middelberg, S. L., 2018. An evaluation of Global Management Accounting

Principles in the sustainability of a South African mechanised piggery. Journal of

Economic and Financial Sciences. 11(1). pp.1-9.

Cokins, G. and Dybvig, A., 2018. NEXT GENERATION BUDGETING: If you want more

accurate results from your budgeting process, it may be time to switch from traditional

budgeting to operational budgeting. Strategic Finance. 99(10). pp.38-46.

Collis, J. and Hussey, R., 2017. Cost and management accounting. Macmillan International

Higher Education.

Fengzhou, W., Shu, H. and You, H., 2019. Discussion on the Basic Assumptions of Management

Accounting.

Gomez-Conde, J. and Lopez-Valeiras, E., 2018. The dual role of management accounting and

control systems in exports: Drivers and payoffs. Spanish Journal of Finance and

Accounting/Revista Española de Financiación y Contabilidad. 47(3). pp.307-328.

John, L. K. and Eeckhout, L., 2018. Performance evaluation and benchmarking. CRC Press.

Karpenko, L. M., Voronzhak, P. V. and Sapron, N. O., 2017. FEATURES OF THE

ORGANIZATION AND ESTABLISHMENT OF THE BUDGETING MANAGEMENT

AT THE ENTERPRISE IN GLOBALIZATION CHANGES CONDITIONS. Science and

practice: an innovative approach. p.110.

Mitter, C. and Hiebl, M.R., 2017. The role of management accounting in international

entrepreneurship. Journal of Accounting & Organizational Change.

Muhammad, U. and et.al, 2018, May. An approach for implementing key performance indicators

of a discrete manufacturing simulator based on the ISO 22400 standard. In 2018 IEEE

Industrial Cyber-Physical Systems (ICPS) (pp. 629-636). IEEE.

Ozyurek, H. and Uluturk, Y., 2016. Flexible budgeting under time-driven activity based cost as a

tool in management accounting: Application in educational institution. Journal of

Administrative and Business Studies. 2(2). pp.64-70.

Schmid, A. A., 2019. Benefit-cost analysis: A political economy approach. Routledge.

Tabitha, N. and Oluyinka, I. O., 2016. Cost Accounting Techniques Adopted By Manufacturing

And Service Industry Within The Last Decade. International Journal Of Advances In

Management And Economics. 5(1). pp.48-61.

Zemrani, A., 2019. Budgeting in the United States: From Theory to Practice Using Higher

Education. In Performance-Based Budgeting in the Public Sector (pp. 29-60). Palgrave

Macmillan, Cham.

Zeng, H., 2018. Reciprocal Interaction between Management Accounting and Other

Management Roles. Open Access Library Journal. 5(11). p.1.

Gillen, D., 2017. Benchmarking and performance measurement: the role in quality

management. AM Brewer, KJ Button, & DA Henshe, Handbook of Logistics and Supply-

Chain Management (Handbooks in Transport, Volume 2). pp.325-338.

Kerzner, H., 2017. Project management metrics, KPIs, and dashboards: a guide to measuring

and monitoring project performance. John Wiley & Sons.

May, B.I., Atkinson, M.P. and Ferrer, G., 2017. Applying inventory classification to a large

inventory management system. Journal of Operations and Supply Chain Management

(JOSCM). 10(1). pp.68-86.

Bondarenko, T.G and et.al, 2017. Optimization of the company strategic management system in

the context of economic instability.

Online

London smallest hotel. 2017. [Online]. Available through:

<https://www.thesun.co.uk/travel/3465134/londons-smallest-hotel-has-opened-in-

shoreditch-with-just-one-room/>

Principles of Management Accounting. 2020. [Online]. Available through:

<https://accountlearning.com/principles-management-accounting/>

inventory management system. Journal of Operations and Supply Chain Management

(JOSCM). 10(1). pp.68-86.

Bondarenko, T.G and et.al, 2017. Optimization of the company strategic management system in

the context of economic instability.

Online

London smallest hotel. 2017. [Online]. Available through:

<https://www.thesun.co.uk/travel/3465134/londons-smallest-hotel-has-opened-in-

shoreditch-with-just-one-room/>

Principles of Management Accounting. 2020. [Online]. Available through:

<https://accountlearning.com/principles-management-accounting/>

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.