Management Accounting Report: Cost Analysis, Planning, and Budgeting

VerifiedAdded on 2021/02/21

|17

|5403

|44

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on the case of Nero Ltd. It begins with an introduction to management accounting, differentiating it from financial accounting and highlighting its importance in organizational decision-making. The report explores various types of management accounting systems, including cost accounting, inventory management, job costing, and pricing optimization systems, detailing their advantages and disadvantages. It then delves into different methods used for management accounting reporting, such as budget reports, performance reports, and job cost reports, evaluating their benefits and drawbacks. The report further examines cost analysis techniques, including direct, indirect, fixed, and variable costs, and the application of marginal and absorption costing. Finally, it discusses the advantages and disadvantages of various planning techniques used for budgetary control, and compares different approaches to adapting management accounting systems to organizational needs. The report concludes with a summary of key findings and recommendations for effective management accounting practices.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

LO 1 ................................................................................................................................................1

P 1 Understanding of Management accounting and different types of accounting system ........1

P 2 Different methods utilized for management accounting reporting........................................4

LO 2 ................................................................................................................................................6

P 3 Calculate costs utilizing appropriate techniques of cost analysis to make income statement

......................................................................................................................................................6

LO 3 ................................................................................................................................................7

P 4 Advantages and disadvantages of various kinds of planning techniques utilize for

budgetary control.........................................................................................................................7

LO 4 ..............................................................................................................................................10

P 5 Compare ways in terms of adapting management accounting systems...............................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

LO 1 ................................................................................................................................................1

P 1 Understanding of Management accounting and different types of accounting system ........1

P 2 Different methods utilized for management accounting reporting........................................4

LO 2 ................................................................................................................................................6

P 3 Calculate costs utilizing appropriate techniques of cost analysis to make income statement

......................................................................................................................................................6

LO 3 ................................................................................................................................................7

P 4 Advantages and disadvantages of various kinds of planning techniques utilize for

budgetary control.........................................................................................................................7

LO 4 ..............................................................................................................................................10

P 5 Compare ways in terms of adapting management accounting systems...............................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting includes creating and giving financial and statistical data to

business managers timely, so that they can create daily and short term decisions of managers. It

is also called as managerial or cost accounting which is different from financial accounting

(Merchant and White, 2017). Study is based on the Nero Ltd. Report will explain management

accounting and give important requirements of various kinds of management accounting system.

It will state different methods utilized for management accounting reporting. It will calculate

costs like marginal and absorption costs utilizing appropriate techniques of cost analysis to create

income statement of firm. Furthermore, assignment will explain the advantages and

disadvantages of different kinds of planning tools utilized for budgetary control.

LO 1

P 1 Understanding of Management accounting and different types of accounting system

Management accounting can be referred as the process to prepare the management report

and accounting report in order to provide the accurate and correct financial information to the

company so that they can operate all its day to day operations in the company (Meaning and

Definition of Management Accounting. 2019).

This management accounting system defined as the systematic procedure of recoding,

analysing, evaluating the cost of an entity in the organization in the direction to prepare the

correct internal financial report and statical information which is being required by the managers

of the company to manage all its day to day functions in order to achieve their desired goals of

company (Weetman, 2019). This management accounting is being used only for the internal

team members of the that helps to formation of the different plans, policies and strategies and

control those plans and policies.

Basic difference between the management accounting and financial accounting is that

management accounting helps the managers of the company by providing the cost and finance

related information which is needed to assist the operations and taking decision for the

organization, whereas financial accounting helps the external parties and member of the

organization like all the stakeholders by preparing the financial report and provide them to take

corrective decision.

Importance of management accounting in organization

1

Management accounting includes creating and giving financial and statistical data to

business managers timely, so that they can create daily and short term decisions of managers. It

is also called as managerial or cost accounting which is different from financial accounting

(Merchant and White, 2017). Study is based on the Nero Ltd. Report will explain management

accounting and give important requirements of various kinds of management accounting system.

It will state different methods utilized for management accounting reporting. It will calculate

costs like marginal and absorption costs utilizing appropriate techniques of cost analysis to create

income statement of firm. Furthermore, assignment will explain the advantages and

disadvantages of different kinds of planning tools utilized for budgetary control.

LO 1

P 1 Understanding of Management accounting and different types of accounting system

Management accounting can be referred as the process to prepare the management report

and accounting report in order to provide the accurate and correct financial information to the

company so that they can operate all its day to day operations in the company (Meaning and

Definition of Management Accounting. 2019).

This management accounting system defined as the systematic procedure of recoding,

analysing, evaluating the cost of an entity in the organization in the direction to prepare the

correct internal financial report and statical information which is being required by the managers

of the company to manage all its day to day functions in order to achieve their desired goals of

company (Weetman, 2019). This management accounting is being used only for the internal

team members of the that helps to formation of the different plans, policies and strategies and

control those plans and policies.

Basic difference between the management accounting and financial accounting is that

management accounting helps the managers of the company by providing the cost and finance

related information which is needed to assist the operations and taking decision for the

organization, whereas financial accounting helps the external parties and member of the

organization like all the stakeholders by preparing the financial report and provide them to take

corrective decision.

Importance of management accounting in organization

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This management accounting help the NERO company to take its effective decision as it

provide the effective and accurate financial data to the managers.

This also play important role to create planing for the different operations in Nero

company as it gives the regular financial report to managers.

Principles of management accounting

Designing and compiling – One of the principle is to design the report by compiling all

the information, records, statements and statics, of past, present and future data (Lewis and Perez

Maldonado, 2019).

Control at source accounting – Required sources of the company is also controlled by

the accounting. As this give the qualitative and quantitative data of resource its utilization,

maintenance then have control over these resources.

Roles of management accounting

Management accounting play the role to planing all the strategies of the organization by

providing detailed financial reports.

Also play the role as controller, decision-making, by give the accurate and effective data

on the basis of the past and present performance of the company.

Different types of management accounting system

Cost accounting system – This accounting system refers as to recording, evaluating,

analysing and classifying the cost, in order to anticipate the cost of their products and services

(Sedevich-Fons, 2019). Purpose of this system is to identify the profitability, inventory valuation

and cost reduction.

Advantages Disadvantages

It can be followed, tinkered with and

applied as per modification wants of

the Nero Ltd.

This kind of accounting system can be

ideas of as sort of three-dimensional

problems such as accounts, calculations

and reports that can be handled and

viewed from various angles.

This method does remove uncertainty

and misappropriation of accounting

guidelines of cost accounting.

Workers have to receive additional

training and must sufficiently cooperate

with information input (Schaltegger

and Burritt, 2017).

2

provide the effective and accurate financial data to the managers.

This also play important role to create planing for the different operations in Nero

company as it gives the regular financial report to managers.

Principles of management accounting

Designing and compiling – One of the principle is to design the report by compiling all

the information, records, statements and statics, of past, present and future data (Lewis and Perez

Maldonado, 2019).

Control at source accounting – Required sources of the company is also controlled by

the accounting. As this give the qualitative and quantitative data of resource its utilization,

maintenance then have control over these resources.

Roles of management accounting

Management accounting play the role to planing all the strategies of the organization by

providing detailed financial reports.

Also play the role as controller, decision-making, by give the accurate and effective data

on the basis of the past and present performance of the company.

Different types of management accounting system

Cost accounting system – This accounting system refers as to recording, evaluating,

analysing and classifying the cost, in order to anticipate the cost of their products and services

(Sedevich-Fons, 2019). Purpose of this system is to identify the profitability, inventory valuation

and cost reduction.

Advantages Disadvantages

It can be followed, tinkered with and

applied as per modification wants of

the Nero Ltd.

This kind of accounting system can be

ideas of as sort of three-dimensional

problems such as accounts, calculations

and reports that can be handled and

viewed from various angles.

This method does remove uncertainty

and misappropriation of accounting

guidelines of cost accounting.

Workers have to receive additional

training and must sufficiently cooperate

with information input (Schaltegger

and Burritt, 2017).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

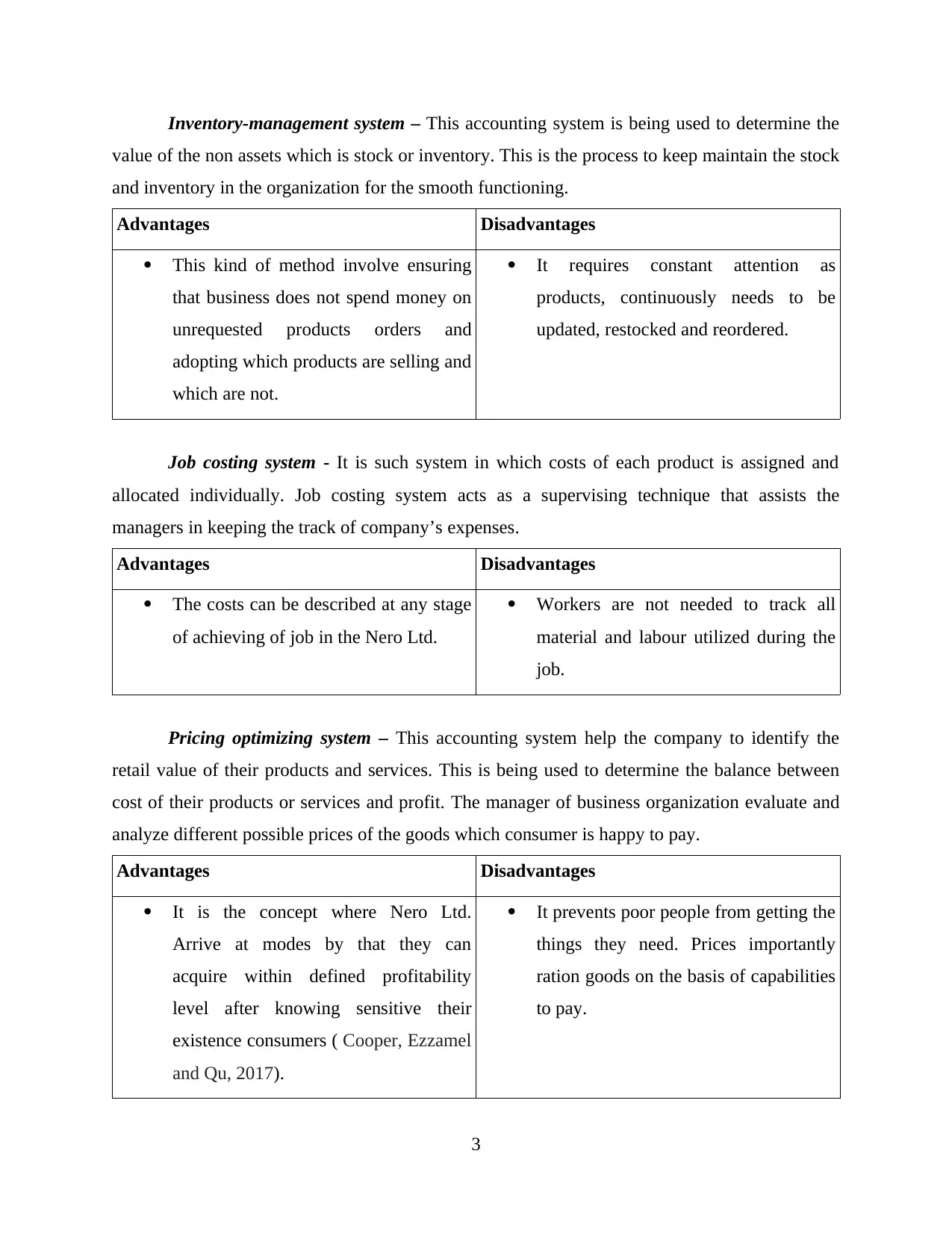

Inventory-management system – This accounting system is being used to determine the

value of the non assets which is stock or inventory. This is the process to keep maintain the stock

and inventory in the organization for the smooth functioning.

Advantages Disadvantages

This kind of method involve ensuring

that business does not spend money on

unrequested products orders and

adopting which products are selling and

which are not.

It requires constant attention as

products, continuously needs to be

updated, restocked and reordered.

Job costing system - It is such system in which costs of each product is assigned and

allocated individually. Job costing system acts as a supervising technique that assists the

managers in keeping the track of company’s expenses.

Advantages Disadvantages

The costs can be described at any stage

of achieving of job in the Nero Ltd.

Workers are not needed to track all

material and labour utilized during the

job.

Pricing optimizing system – This accounting system help the company to identify the

retail value of their products and services. This is being used to determine the balance between

cost of their products or services and profit. The manager of business organization evaluate and

analyze different possible prices of the goods which consumer is happy to pay.

Advantages Disadvantages

It is the concept where Nero Ltd.

Arrive at modes by that they can

acquire within defined profitability

level after knowing sensitive their

existence consumers ( Cooper, Ezzamel

and Qu, 2017).

It prevents poor people from getting the

things they need. Prices importantly

ration goods on the basis of capabilities

to pay.

3

value of the non assets which is stock or inventory. This is the process to keep maintain the stock

and inventory in the organization for the smooth functioning.

Advantages Disadvantages

This kind of method involve ensuring

that business does not spend money on

unrequested products orders and

adopting which products are selling and

which are not.

It requires constant attention as

products, continuously needs to be

updated, restocked and reordered.

Job costing system - It is such system in which costs of each product is assigned and

allocated individually. Job costing system acts as a supervising technique that assists the

managers in keeping the track of company’s expenses.

Advantages Disadvantages

The costs can be described at any stage

of achieving of job in the Nero Ltd.

Workers are not needed to track all

material and labour utilized during the

job.

Pricing optimizing system – This accounting system help the company to identify the

retail value of their products and services. This is being used to determine the balance between

cost of their products or services and profit. The manager of business organization evaluate and

analyze different possible prices of the goods which consumer is happy to pay.

Advantages Disadvantages

It is the concept where Nero Ltd.

Arrive at modes by that they can

acquire within defined profitability

level after knowing sensitive their

existence consumers ( Cooper, Ezzamel

and Qu, 2017).

It prevents poor people from getting the

things they need. Prices importantly

ration goods on the basis of capabilities

to pay.

3

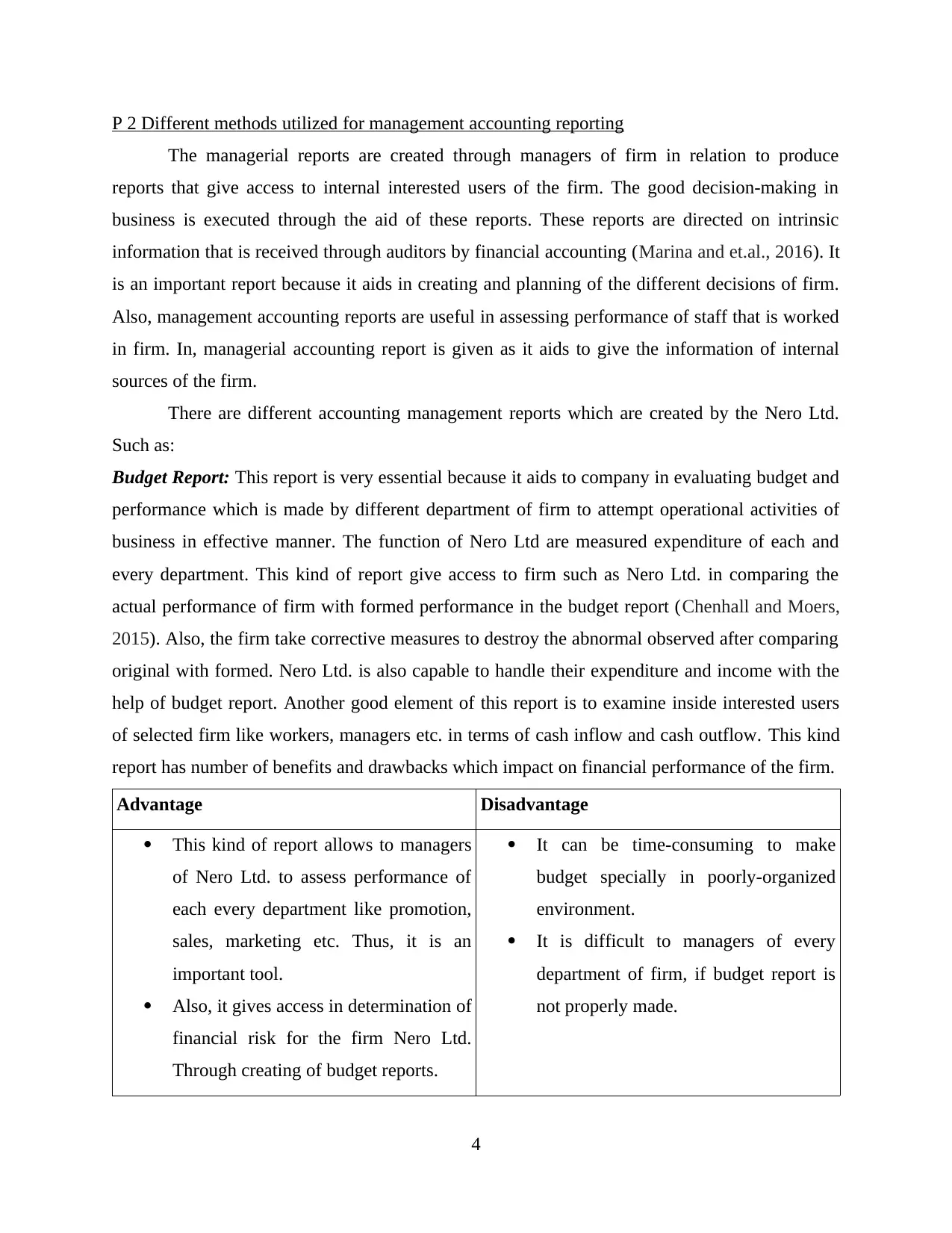

P 2 Different methods utilized for management accounting reporting

The managerial reports are created through managers of firm in relation to produce

reports that give access to internal interested users of the firm. The good decision-making in

business is executed through the aid of these reports. These reports are directed on intrinsic

information that is received through auditors by financial accounting (Marina and et.al., 2016). It

is an important report because it aids in creating and planning of the different decisions of firm.

Also, management accounting reports are useful in assessing performance of staff that is worked

in firm. In, managerial accounting report is given as it aids to give the information of internal

sources of the firm.

There are different accounting management reports which are created by the Nero Ltd.

Such as:

Budget Report: This report is very essential because it aids to company in evaluating budget and

performance which is made by different department of firm to attempt operational activities of

business in effective manner. The function of Nero Ltd are measured expenditure of each and

every department. This kind of report give access to firm such as Nero Ltd. in comparing the

actual performance of firm with formed performance in the budget report (Chenhall and Moers,

2015). Also, the firm take corrective measures to destroy the abnormal observed after comparing

original with formed. Nero Ltd. is also capable to handle their expenditure and income with the

help of budget report. Another good element of this report is to examine inside interested users

of selected firm like workers, managers etc. in terms of cash inflow and cash outflow. This kind

report has number of benefits and drawbacks which impact on financial performance of the firm.

Advantage Disadvantage

This kind of report allows to managers

of Nero Ltd. to assess performance of

each every department like promotion,

sales, marketing etc. Thus, it is an

important tool.

Also, it gives access in determination of

financial risk for the firm Nero Ltd.

Through creating of budget reports.

It can be time-consuming to make

budget specially in poorly-organized

environment.

It is difficult to managers of every

department of firm, if budget report is

not properly made.

4

The managerial reports are created through managers of firm in relation to produce

reports that give access to internal interested users of the firm. The good decision-making in

business is executed through the aid of these reports. These reports are directed on intrinsic

information that is received through auditors by financial accounting (Marina and et.al., 2016). It

is an important report because it aids in creating and planning of the different decisions of firm.

Also, management accounting reports are useful in assessing performance of staff that is worked

in firm. In, managerial accounting report is given as it aids to give the information of internal

sources of the firm.

There are different accounting management reports which are created by the Nero Ltd.

Such as:

Budget Report: This report is very essential because it aids to company in evaluating budget and

performance which is made by different department of firm to attempt operational activities of

business in effective manner. The function of Nero Ltd are measured expenditure of each and

every department. This kind of report give access to firm such as Nero Ltd. in comparing the

actual performance of firm with formed performance in the budget report (Chenhall and Moers,

2015). Also, the firm take corrective measures to destroy the abnormal observed after comparing

original with formed. Nero Ltd. is also capable to handle their expenditure and income with the

help of budget report. Another good element of this report is to examine inside interested users

of selected firm like workers, managers etc. in terms of cash inflow and cash outflow. This kind

report has number of benefits and drawbacks which impact on financial performance of the firm.

Advantage Disadvantage

This kind of report allows to managers

of Nero Ltd. to assess performance of

each every department like promotion,

sales, marketing etc. Thus, it is an

important tool.

Also, it gives access in determination of

financial risk for the firm Nero Ltd.

Through creating of budget reports.

It can be time-consuming to make

budget specially in poorly-organized

environment.

It is difficult to managers of every

department of firm, if budget report is

not properly made.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

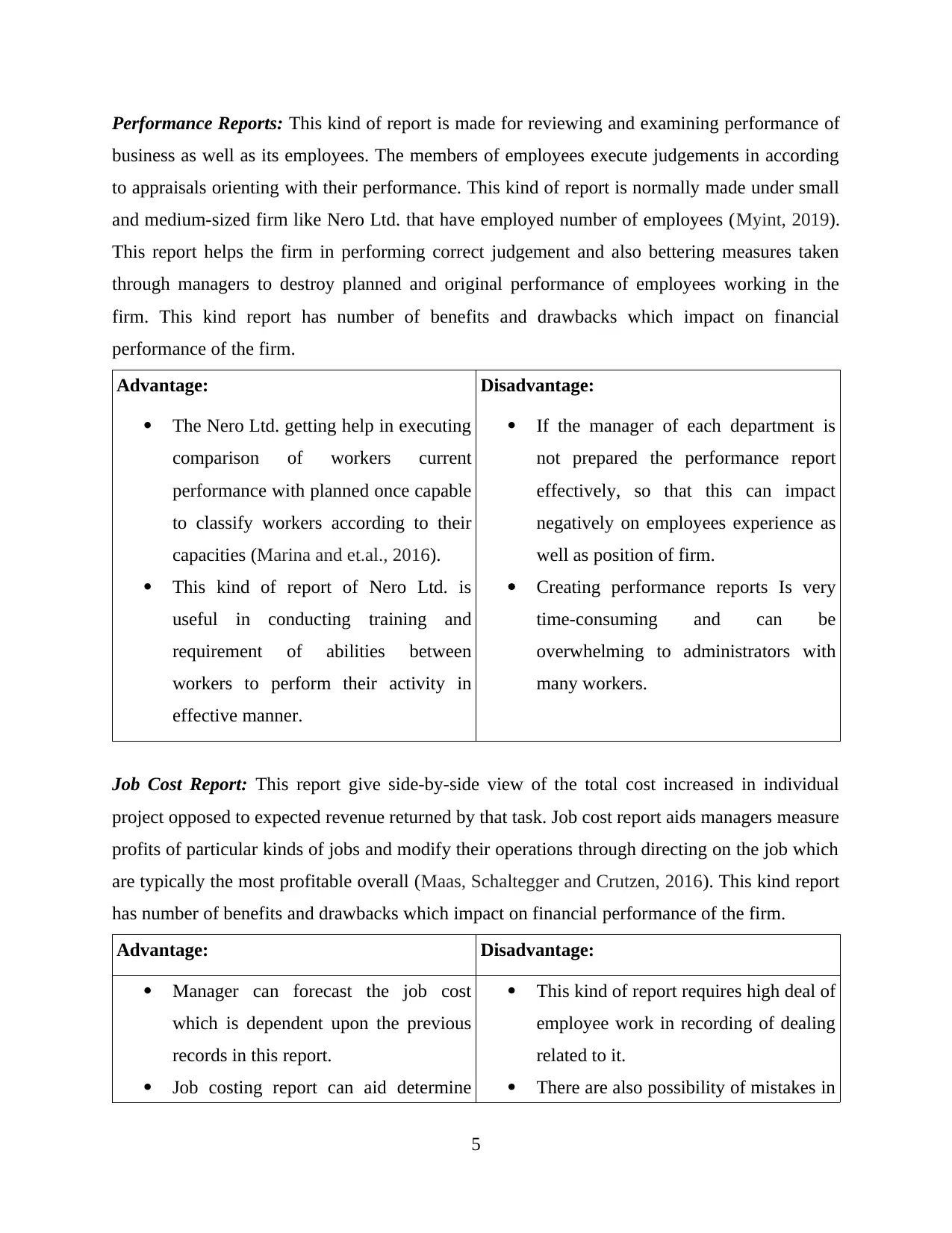

Performance Reports: This kind of report is made for reviewing and examining performance of

business as well as its employees. The members of employees execute judgements in according

to appraisals orienting with their performance. This kind of report is normally made under small

and medium-sized firm like Nero Ltd. that have employed number of employees (Myint, 2019).

This report helps the firm in performing correct judgement and also bettering measures taken

through managers to destroy planned and original performance of employees working in the

firm. This kind report has number of benefits and drawbacks which impact on financial

performance of the firm.

Advantage: Disadvantage:

The Nero Ltd. getting help in executing

comparison of workers current

performance with planned once capable

to classify workers according to their

capacities (Marina and et.al., 2016).

This kind of report of Nero Ltd. is

useful in conducting training and

requirement of abilities between

workers to perform their activity in

effective manner.

If the manager of each department is

not prepared the performance report

effectively, so that this can impact

negatively on employees experience as

well as position of firm.

Creating performance reports Is very

time-consuming and can be

overwhelming to administrators with

many workers.

Job Cost Report: This report give side-by-side view of the total cost increased in individual

project opposed to expected revenue returned by that task. Job cost report aids managers measure

profits of particular kinds of jobs and modify their operations through directing on the job which

are typically the most profitable overall (Maas, Schaltegger and Crutzen, 2016). This kind report

has number of benefits and drawbacks which impact on financial performance of the firm.

Advantage: Disadvantage:

Manager can forecast the job cost

which is dependent upon the previous

records in this report.

Job costing report can aid determine

This kind of report requires high deal of

employee work in recording of dealing

related to it.

There are also possibility of mistakes in

5

business as well as its employees. The members of employees execute judgements in according

to appraisals orienting with their performance. This kind of report is normally made under small

and medium-sized firm like Nero Ltd. that have employed number of employees (Myint, 2019).

This report helps the firm in performing correct judgement and also bettering measures taken

through managers to destroy planned and original performance of employees working in the

firm. This kind report has number of benefits and drawbacks which impact on financial

performance of the firm.

Advantage: Disadvantage:

The Nero Ltd. getting help in executing

comparison of workers current

performance with planned once capable

to classify workers according to their

capacities (Marina and et.al., 2016).

This kind of report of Nero Ltd. is

useful in conducting training and

requirement of abilities between

workers to perform their activity in

effective manner.

If the manager of each department is

not prepared the performance report

effectively, so that this can impact

negatively on employees experience as

well as position of firm.

Creating performance reports Is very

time-consuming and can be

overwhelming to administrators with

many workers.

Job Cost Report: This report give side-by-side view of the total cost increased in individual

project opposed to expected revenue returned by that task. Job cost report aids managers measure

profits of particular kinds of jobs and modify their operations through directing on the job which

are typically the most profitable overall (Maas, Schaltegger and Crutzen, 2016). This kind report

has number of benefits and drawbacks which impact on financial performance of the firm.

Advantage: Disadvantage:

Manager can forecast the job cost

which is dependent upon the previous

records in this report.

Job costing report can aid determine

This kind of report requires high deal of

employee work in recording of dealing

related to it.

There are also possibility of mistakes in

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

problems during job and after

completing it. Problems such as

mistake in equipment count required to

end certain evaluation (Boiral, 2016).

job costing report.

LO 2

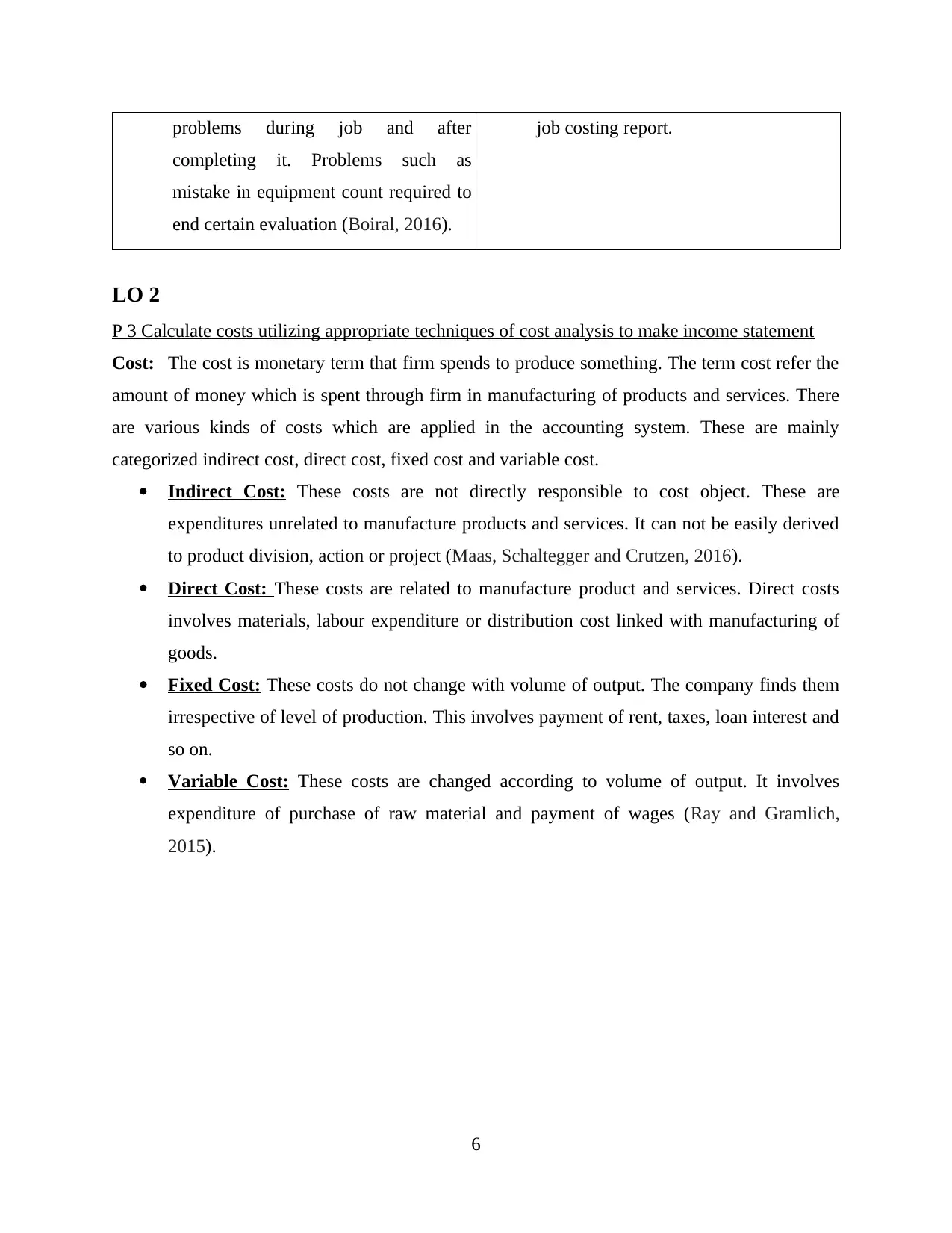

P 3 Calculate costs utilizing appropriate techniques of cost analysis to make income statement

Cost: The cost is monetary term that firm spends to produce something. The term cost refer the

amount of money which is spent through firm in manufacturing of products and services. There

are various kinds of costs which are applied in the accounting system. These are mainly

categorized indirect cost, direct cost, fixed cost and variable cost.

Indirect Cost: These costs are not directly responsible to cost object. These are

expenditures unrelated to manufacture products and services. It can not be easily derived

to product division, action or project (Maas, Schaltegger and Crutzen, 2016).

Direct Cost: These costs are related to manufacture product and services. Direct costs

involves materials, labour expenditure or distribution cost linked with manufacturing of

goods.

Fixed Cost: These costs do not change with volume of output. The company finds them

irrespective of level of production. This involves payment of rent, taxes, loan interest and

so on.

Variable Cost: These costs are changed according to volume of output. It involves

expenditure of purchase of raw material and payment of wages (Ray and Gramlich,

2015).

6

completing it. Problems such as

mistake in equipment count required to

end certain evaluation (Boiral, 2016).

job costing report.

LO 2

P 3 Calculate costs utilizing appropriate techniques of cost analysis to make income statement

Cost: The cost is monetary term that firm spends to produce something. The term cost refer the

amount of money which is spent through firm in manufacturing of products and services. There

are various kinds of costs which are applied in the accounting system. These are mainly

categorized indirect cost, direct cost, fixed cost and variable cost.

Indirect Cost: These costs are not directly responsible to cost object. These are

expenditures unrelated to manufacture products and services. It can not be easily derived

to product division, action or project (Maas, Schaltegger and Crutzen, 2016).

Direct Cost: These costs are related to manufacture product and services. Direct costs

involves materials, labour expenditure or distribution cost linked with manufacturing of

goods.

Fixed Cost: These costs do not change with volume of output. The company finds them

irrespective of level of production. This involves payment of rent, taxes, loan interest and

so on.

Variable Cost: These costs are changed according to volume of output. It involves

expenditure of purchase of raw material and payment of wages (Ray and Gramlich,

2015).

6

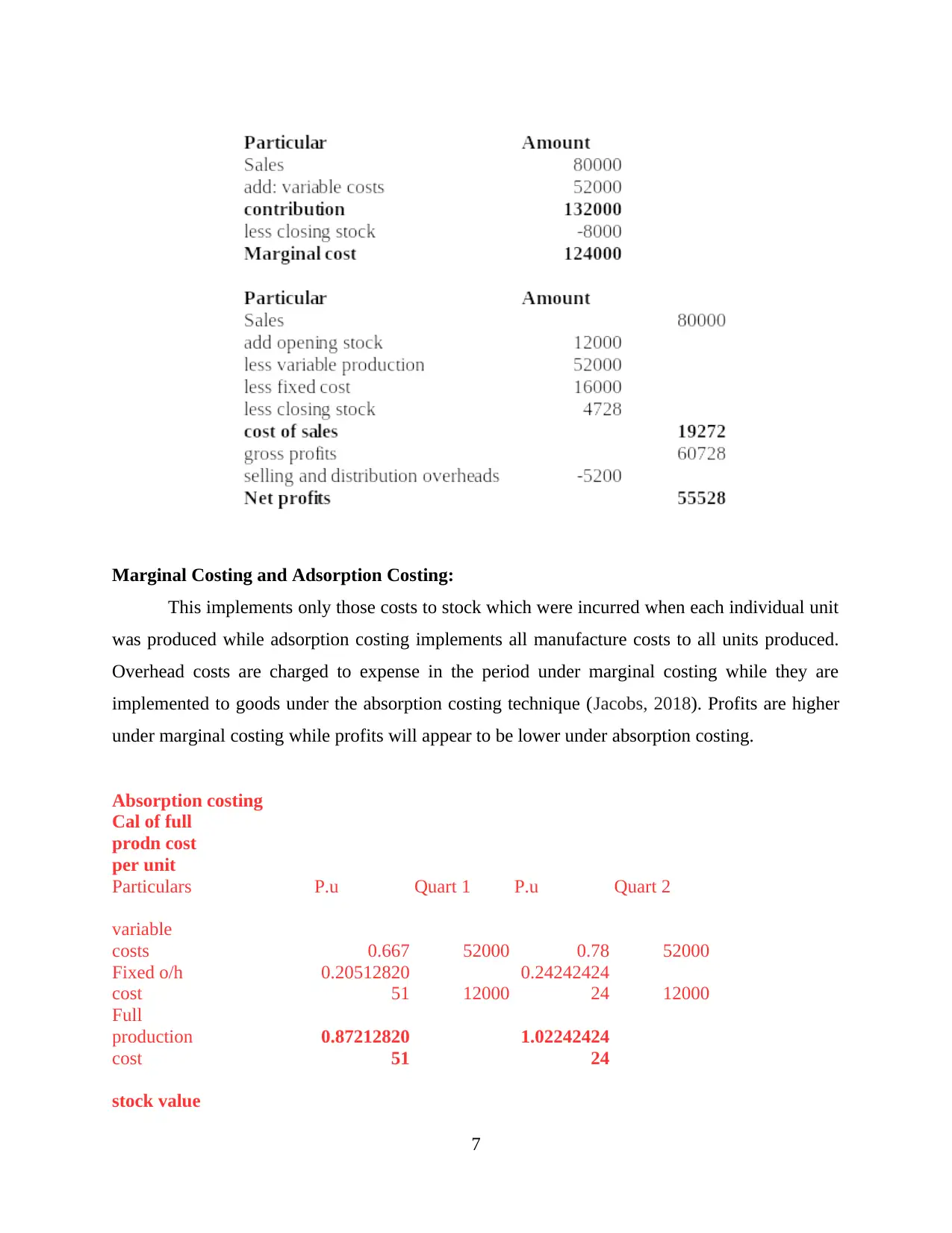

Marginal Costing and Adsorption Costing:

This implements only those costs to stock which were incurred when each individual unit

was produced while adsorption costing implements all manufacture costs to all units produced.

Overhead costs are charged to expense in the period under marginal costing while they are

implemented to goods under the absorption costing technique (Jacobs, 2018). Profits are higher

under marginal costing while profits will appear to be lower under absorption costing.

Absorption costing

Cal of full

prodn cost

per unit

Particulars P.u Quart 1 P.u Quart 2

variable

costs 0.667 52000 0.78 52000

Fixed o/h

cost

0.20512820

51 12000

0.24242424

24 12000

Full

production

cost

0.87212820

51

1.02242424

24

stock value

7

This implements only those costs to stock which were incurred when each individual unit

was produced while adsorption costing implements all manufacture costs to all units produced.

Overhead costs are charged to expense in the period under marginal costing while they are

implemented to goods under the absorption costing technique (Jacobs, 2018). Profits are higher

under marginal costing while profits will appear to be lower under absorption costing.

Absorption costing

Cal of full

prodn cost

per unit

Particulars P.u Quart 1 P.u Quart 2

variable

costs 0.667 52000 0.78 52000

Fixed o/h

cost

0.20512820

51 12000

0.24242424

24 12000

Full

production

cost

0.87212820

51

1.02242424

24

stock value

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

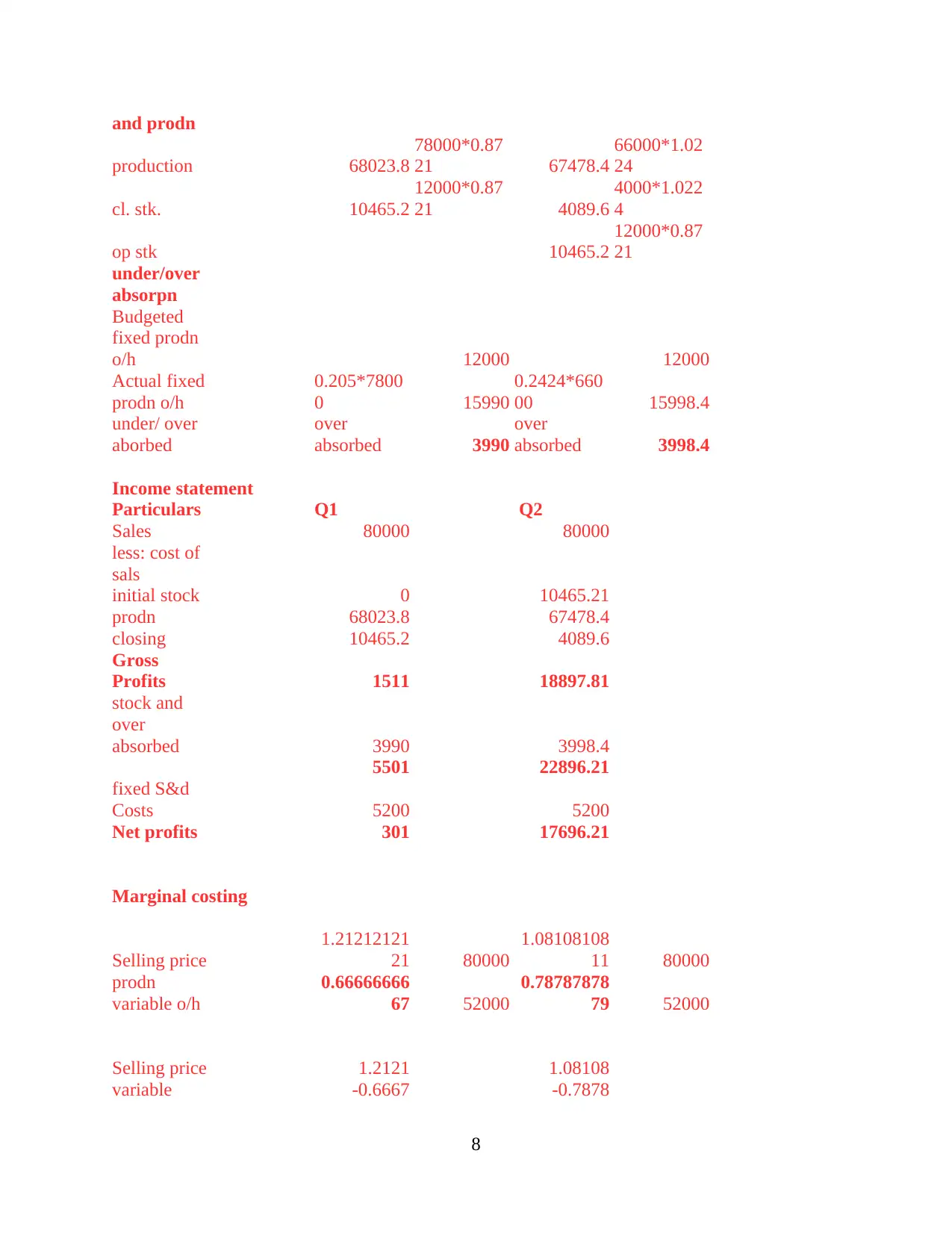

and prodn

production 68023.8

78000*0.87

21 67478.4

66000*1.02

24

cl. stk. 10465.2

12000*0.87

21 4089.6

4000*1.022

4

op stk 10465.2

12000*0.87

21

under/over

absorpn

Budgeted

fixed prodn

o/h 12000 12000

Actual fixed

prodn o/h

0.205*7800

0 15990

0.2424*660

00 15998.4

under/ over

aborbed

over

absorbed 3990

over

absorbed 3998.4

Income statement

Particulars Q1 Q2

Sales 80000 80000

less: cost of

sals

initial stock 0 10465.21

prodn 68023.8 67478.4

closing 10465.2 4089.6

Gross

Profits 1511 18897.81

stock and

over

absorbed 3990 3998.4

5501 22896.21

fixed S&d

Costs 5200 5200

Net profits 301 17696.21

Marginal costing

Selling price

1.21212121

21 80000

1.08108108

11 80000

prodn

variable o/h

0.66666666

67 52000

0.78787878

79 52000

Selling price 1.2121 1.08108

variable -0.6667 -0.7878

8

production 68023.8

78000*0.87

21 67478.4

66000*1.02

24

cl. stk. 10465.2

12000*0.87

21 4089.6

4000*1.022

4

op stk 10465.2

12000*0.87

21

under/over

absorpn

Budgeted

fixed prodn

o/h 12000 12000

Actual fixed

prodn o/h

0.205*7800

0 15990

0.2424*660

00 15998.4

under/ over

aborbed

over

absorbed 3990

over

absorbed 3998.4

Income statement

Particulars Q1 Q2

Sales 80000 80000

less: cost of

sals

initial stock 0 10465.21

prodn 68023.8 67478.4

closing 10465.2 4089.6

Gross

Profits 1511 18897.81

stock and

over

absorbed 3990 3998.4

5501 22896.21

fixed S&d

Costs 5200 5200

Net profits 301 17696.21

Marginal costing

Selling price

1.21212121

21 80000

1.08108108

11 80000

prodn

variable o/h

0.66666666

67 52000

0.78787878

79 52000

Selling price 1.2121 1.08108

variable -0.6667 -0.7878

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

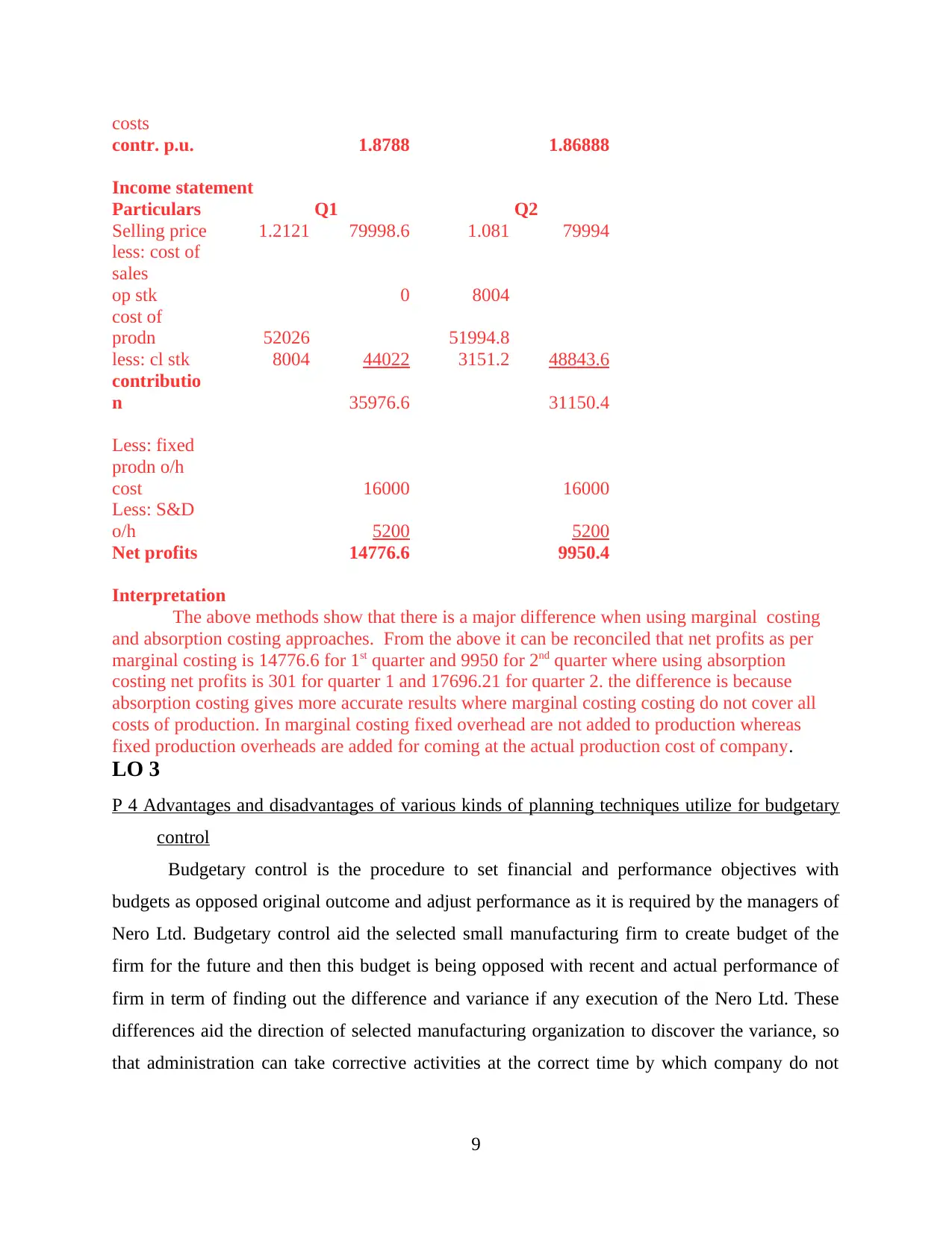

costs

contr. p.u. 1.8788 1.86888

Income statement

Particulars Q1 Q2

Selling price 1.2121 79998.6 1.081 79994

less: cost of

sales

op stk 0 8004

cost of

prodn 52026 51994.8

less: cl stk 8004 44022 3151.2 48843.6

contributio

n 35976.6 31150.4

Less: fixed

prodn o/h

cost 16000 16000

Less: S&D

o/h 5200 5200

Net profits 14776.6 9950.4

Interpretation

The above methods show that there is a major difference when using marginal costing

and absorption costing approaches. From the above it can be reconciled that net profits as per

marginal costing is 14776.6 for 1st quarter and 9950 for 2nd quarter where using absorption

costing net profits is 301 for quarter 1 and 17696.21 for quarter 2. the difference is because

absorption costing gives more accurate results where marginal costing costing do not cover all

costs of production. In marginal costing fixed overhead are not added to production whereas

fixed production overheads are added for coming at the actual production cost of company.

LO 3

P 4 Advantages and disadvantages of various kinds of planning techniques utilize for budgetary

control

Budgetary control is the procedure to set financial and performance objectives with

budgets as opposed original outcome and adjust performance as it is required by the managers of

Nero Ltd. Budgetary control aid the selected small manufacturing firm to create budget of the

firm for the future and then this budget is being opposed with recent and actual performance of

firm in term of finding out the difference and variance if any execution of the Nero Ltd. These

differences aid the direction of selected manufacturing organization to discover the variance, so

that administration can take corrective activities at the correct time by which company do not

9

contr. p.u. 1.8788 1.86888

Income statement

Particulars Q1 Q2

Selling price 1.2121 79998.6 1.081 79994

less: cost of

sales

op stk 0 8004

cost of

prodn 52026 51994.8

less: cl stk 8004 44022 3151.2 48843.6

contributio

n 35976.6 31150.4

Less: fixed

prodn o/h

cost 16000 16000

Less: S&D

o/h 5200 5200

Net profits 14776.6 9950.4

Interpretation

The above methods show that there is a major difference when using marginal costing

and absorption costing approaches. From the above it can be reconciled that net profits as per

marginal costing is 14776.6 for 1st quarter and 9950 for 2nd quarter where using absorption

costing net profits is 301 for quarter 1 and 17696.21 for quarter 2. the difference is because

absorption costing gives more accurate results where marginal costing costing do not cover all

costs of production. In marginal costing fixed overhead are not added to production whereas

fixed production overheads are added for coming at the actual production cost of company.

LO 3

P 4 Advantages and disadvantages of various kinds of planning techniques utilize for budgetary

control

Budgetary control is the procedure to set financial and performance objectives with

budgets as opposed original outcome and adjust performance as it is required by the managers of

Nero Ltd. Budgetary control aid the selected small manufacturing firm to create budget of the

firm for the future and then this budget is being opposed with recent and actual performance of

firm in term of finding out the difference and variance if any execution of the Nero Ltd. These

differences aid the direction of selected manufacturing organization to discover the variance, so

that administration can take corrective activities at the correct time by which company do not

9

have to suffer from any kind of large loss (Arias and et.al., 2016). This budgetary control is

being done for the various goals that are as follows:

This budgetary control system aids to keep the coordination among the different division

of the Nero Ltd.

Also, this aids to determine plans and approaches as according to the fix goal of the Nero

Ltd.

On of the leading goal is to constant differences of actual outcome and execution of the

Nero Ltd. As with the formed upcoming budget in relation to take the correct actions on

accurate time (Myint, 2019).

This budgetary-control assists to describe the goals of the Nero Ltd.

This budgetary control system include various techniques to figure out the differences in

the Nero Ltd. Management of selected small business implement the different techniques in their

organization to create the approach accordance of fill differences and can develop their financial

position in the industry. These techniques are:

Operating Budget: This kind of budget aids to present the revenue and related expenditure of

project of the Nero Ltd. for the upcoming year. This is normally for the next year and is being

displayed in current year statements. This operating cost is being started with the revenue and

then further involved other related expenditures. It will involve various expenditure of Nero Ltd.

such as variable cost which can vary according to sales of the products, cost of raw material,

production and so on (Chenhall and Moers, 2015). This can help to selected medium business to

figure out their all the operating cost, that is being further involved in final budget of the firm to

discover loss or profits. This kind of technique have many of pros and cons such as:

Advantages Disadvantages

This kind of budget tool aid the Nero

Ltd. to allocation of the money in the

short period for future utilization.

Also, this can create budget flexible

and give more financial freedom to

invest in future sources.

It becomes difficult to calculate

operational budget through

modification projection cost every time.

As the financial information is

modified every time month to month,

then cost of projection also can be

modified, this requires to modify the

10

being done for the various goals that are as follows:

This budgetary control system aids to keep the coordination among the different division

of the Nero Ltd.

Also, this aids to determine plans and approaches as according to the fix goal of the Nero

Ltd.

On of the leading goal is to constant differences of actual outcome and execution of the

Nero Ltd. As with the formed upcoming budget in relation to take the correct actions on

accurate time (Myint, 2019).

This budgetary-control assists to describe the goals of the Nero Ltd.

This budgetary control system include various techniques to figure out the differences in

the Nero Ltd. Management of selected small business implement the different techniques in their

organization to create the approach accordance of fill differences and can develop their financial

position in the industry. These techniques are:

Operating Budget: This kind of budget aids to present the revenue and related expenditure of

project of the Nero Ltd. for the upcoming year. This is normally for the next year and is being

displayed in current year statements. This operating cost is being started with the revenue and

then further involved other related expenditures. It will involve various expenditure of Nero Ltd.

such as variable cost which can vary according to sales of the products, cost of raw material,

production and so on (Chenhall and Moers, 2015). This can help to selected medium business to

figure out their all the operating cost, that is being further involved in final budget of the firm to

discover loss or profits. This kind of technique have many of pros and cons such as:

Advantages Disadvantages

This kind of budget tool aid the Nero

Ltd. to allocation of the money in the

short period for future utilization.

Also, this can create budget flexible

and give more financial freedom to

invest in future sources.

It becomes difficult to calculate

operational budget through

modification projection cost every time.

As the financial information is

modified every time month to month,

then cost of projection also can be

modified, this requires to modify the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.