Management Accounting Report: ABC Limited Analysis

VerifiedAdded on 2023/02/01

|16

|4523

|35

Report

AI Summary

This report provides a detailed overview of management accounting, focusing on various systems, methods, and their applications within a manufacturing context, specifically referencing ABC Limited. The report explores essential requirements of different management accounting systems, including inventory management and cost accounting, and discusses different methods used for management accounting reporting, such as budget reports and performance reports. It includes an analysis of marginal and absorption costing, along with a discussion of the advantages and disadvantages of planning tools for budgetary control. Furthermore, the report addresses how management accounting systems can be adapted to solve financial problems, analyzing the role of planning tools in this process. The report concludes with insights into integrating management accounting and reporting systems for improved efficiency and cost reduction, providing a comprehensive understanding of the subject.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

Essential requirements of different types of management accounting system.........................................3

Different methods used for management accounting reporting...............................................................5

Benefits of management accounting system............................................................................................6

Integration of management accounting and reporting system..................................................................7

TASK 2..........................................................................................................................................................8

. Calculation of marginal and absorption costing.....................................................................................8

TASK 3........................................................................................................................................................10

Advantages and Disadvantages of various planning tools for budgetary control...................................10

TASK 4........................................................................................................................................................12

Adaption of management accounting system to solve financial problems.............................................12

Analyzing planning tools in solving financial problems........................................................................14

CONCLUSIONS...........................................................................................................................................14

REFERENCES..............................................................................................................................................15

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

Essential requirements of different types of management accounting system.........................................3

Different methods used for management accounting reporting...............................................................5

Benefits of management accounting system............................................................................................6

Integration of management accounting and reporting system..................................................................7

TASK 2..........................................................................................................................................................8

. Calculation of marginal and absorption costing.....................................................................................8

TASK 3........................................................................................................................................................10

Advantages and Disadvantages of various planning tools for budgetary control...................................10

TASK 4........................................................................................................................................................12

Adaption of management accounting system to solve financial problems.............................................12

Analyzing planning tools in solving financial problems........................................................................14

CONCLUSIONS...........................................................................................................................................14

REFERENCES..............................................................................................................................................15

INTRODUCTION

Management accounting is the application of skill and preparing information on various

accounts which help the management of the company in making policies for future planning and

carrying on the operations. It is used to provide information to the internal users and helps the company

in making decisions. With the help of available information, statistics and other financial as well as

non-financial data, the managers and employees can make sound investment decisions. The

objective of management accounting is to provide all the necessary financial information to the

management for making decisions. For further information on management accounting, the report will

state various requirements of management accounting systems which includes Cost accounting system,

Inventory management system, and Job costing system. The present report is based on ABC limited

which is a manufacturing company. The present report will discuss different types of

management accounting systems available and how organization can seek benefits. Further, the

report will discuss about the concept of management accounting reporting and it uses in decision

making. Income statement under marginal and absorption accounting of ABC limited using

appropriate technique for analyzing cost factor will be disclosed.

TASK 1

Essential requirements of different types of management accounting system

Management accounting helps internal users in providing all the relevant information. It

takes financial information of the company and develop reports which are used by managers.

Management accounting system of the company makes it easy for mangers by collecting

information based on trend charts, budgeting, break even charts etc which help the company in

forecasting future. It helps the company in improving its performance and increase its efficiency

and effectiveness (Martello, 2016). The management accounting system identifies, analyses and

record all the quantitative transactions which lead to overall development of the company.

Inventory Management System – This method of management accounting emphasizes

on cost controlling function which has been incurred on producing goods and services for

meeting the customer demands. It also assists in managing inventory and stock level of the

company. ABC limited can assess, monitor and track the quantity of goods, inventory and stock

through the supply chain or with the help of areas in which business operations takes place

(Gunarathne, 2018). This method helps company in making inventory valuation, improving the

accuracy of inventory by maintaining continuous workflow and its reorder so as to facilitate

smooth functioning of business operations. Valuation of inventory can be done with the help of

following two methods:

1. LIFO – It stands for Last In First Out. In this method, goods which are bought or

purchased at last are available for sale at first place.

Management accounting is the application of skill and preparing information on various

accounts which help the management of the company in making policies for future planning and

carrying on the operations. It is used to provide information to the internal users and helps the company

in making decisions. With the help of available information, statistics and other financial as well as

non-financial data, the managers and employees can make sound investment decisions. The

objective of management accounting is to provide all the necessary financial information to the

management for making decisions. For further information on management accounting, the report will

state various requirements of management accounting systems which includes Cost accounting system,

Inventory management system, and Job costing system. The present report is based on ABC limited

which is a manufacturing company. The present report will discuss different types of

management accounting systems available and how organization can seek benefits. Further, the

report will discuss about the concept of management accounting reporting and it uses in decision

making. Income statement under marginal and absorption accounting of ABC limited using

appropriate technique for analyzing cost factor will be disclosed.

TASK 1

Essential requirements of different types of management accounting system

Management accounting helps internal users in providing all the relevant information. It

takes financial information of the company and develop reports which are used by managers.

Management accounting system of the company makes it easy for mangers by collecting

information based on trend charts, budgeting, break even charts etc which help the company in

forecasting future. It helps the company in improving its performance and increase its efficiency

and effectiveness (Martello, 2016). The management accounting system identifies, analyses and

record all the quantitative transactions which lead to overall development of the company.

Inventory Management System – This method of management accounting emphasizes

on cost controlling function which has been incurred on producing goods and services for

meeting the customer demands. It also assists in managing inventory and stock level of the

company. ABC limited can assess, monitor and track the quantity of goods, inventory and stock

through the supply chain or with the help of areas in which business operations takes place

(Gunarathne, 2018). This method helps company in making inventory valuation, improving the

accuracy of inventory by maintaining continuous workflow and its reorder so as to facilitate

smooth functioning of business operations. Valuation of inventory can be done with the help of

following two methods:

1. LIFO – It stands for Last In First Out. In this method, goods which are bought or

purchased at last are available for sale at first place.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. FIFO – This stands for First In First Out, it emphasizes on selling first of that stock

which is purchase or bought in at first place.

Cost accounting system

Cost accounting system of the company helps the company in estimating its cost for their

particular products that are being offered to the customers for the purpose of profitability

analysis, valuation of inventory and controlling cost. It tracks the cost of raw materials as they go

through the stages of production . When company come to know about exact costing of products,

it can be critical for the production. It helps ABC limited in figuring out which products are

profitable and which are not. It takes raw materials, work in progress and finished goods for

preparation of financial statements. There are two main cost accounting system that includes:

Job order costing – It combines manufacturing cost separately for the job or task. It fits

to the firm who operated in unique and different products and can help the firm in finding out

which product is generating the highest profit.

Process costing – It collects manufacturing cost for each process separately. The firms

who involves in different departments and cost flow from one department to another can use

process costing.

Job costing

The information provided by job costing system helps in determining accuracy of estimating

system of company. This method is used when there are various products produced by the

company and have different cost. It included direct material and cost of direct labor that is used

in carrying out the particular activity along with overhead costs that includes depreciation, rent

etc. This system helps in improving efficiency of the company and to now better performing

product or service by comparing standard and actual performances of all the products. The job

costing method of management accounting is that business practice which aids ABC limited in

collecting and analysing all the important and relevant information related to the cost incurred

with the production function of some specific job or product group. It acknowledges company in

assessing the cost of operations and helps in taking corrective measures by minimising the cost

of that activity which is incurring more cost expense (Toussaint and et.al., 2015.). This method

considers each part of information which relates to direct materials, labour and overhead costs.

Under this system, information related to cost incurred for every job work completed is provided

to the customer for getting cost reimbursed as per the contract or agreement made. This system

helps in improving efficiency of the company and to now better performing product or service by

comparing standard and actual performances of all the products.

Different methods used for management accounting reporting

which is purchase or bought in at first place.

Cost accounting system

Cost accounting system of the company helps the company in estimating its cost for their

particular products that are being offered to the customers for the purpose of profitability

analysis, valuation of inventory and controlling cost. It tracks the cost of raw materials as they go

through the stages of production . When company come to know about exact costing of products,

it can be critical for the production. It helps ABC limited in figuring out which products are

profitable and which are not. It takes raw materials, work in progress and finished goods for

preparation of financial statements. There are two main cost accounting system that includes:

Job order costing – It combines manufacturing cost separately for the job or task. It fits

to the firm who operated in unique and different products and can help the firm in finding out

which product is generating the highest profit.

Process costing – It collects manufacturing cost for each process separately. The firms

who involves in different departments and cost flow from one department to another can use

process costing.

Job costing

The information provided by job costing system helps in determining accuracy of estimating

system of company. This method is used when there are various products produced by the

company and have different cost. It included direct material and cost of direct labor that is used

in carrying out the particular activity along with overhead costs that includes depreciation, rent

etc. This system helps in improving efficiency of the company and to now better performing

product or service by comparing standard and actual performances of all the products. The job

costing method of management accounting is that business practice which aids ABC limited in

collecting and analysing all the important and relevant information related to the cost incurred

with the production function of some specific job or product group. It acknowledges company in

assessing the cost of operations and helps in taking corrective measures by minimising the cost

of that activity which is incurring more cost expense (Toussaint and et.al., 2015.). This method

considers each part of information which relates to direct materials, labour and overhead costs.

Under this system, information related to cost incurred for every job work completed is provided

to the customer for getting cost reimbursed as per the contract or agreement made. This system

helps in improving efficiency of the company and to now better performing product or service by

comparing standard and actual performances of all the products.

Different methods used for management accounting reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting reports help business in getting all the relevant information

related to the business and to enable the manger of the company to know the true picture of the

company. To get an overall picture on business performance and finance, the management

reports need to be out on every quarterly or yearly basis. These reports helps in providing

transparency to the stakeholders of the company as well as provide accurate data for further

analysis. The various types of reports that are used by management are -

Budget reports – These reports are important in analyzing, evaluating and monitoring

performance of the company and can be generated for whole business or particular department.

A company's basic work is to create budget which helps the company in estimating cost of the

business. The preparation of the budget can be done on the basis of previous experience (Mahal,

2015). A budget of the company consists of income and expenditure sources of the company and

achieve its goals while staying in the budget. It helps the company in cost cutting and provide

employees with incentives. The budget report lays emphasis on making future projections and

estimation related to the amount of money to be spent on business operations. By making

budgetary plans and strategies ABC limited can conduct business operations smoothly with the

limited amount of budgeted amount and resources. With the help of budget report, a company

can make assessment of its performance as well as profitability level. Budget are prepared on the

basis of previous experience business has met with. With proper estimates and budget, company

can deal with future contingencies and cost expenses.

Account receivable aging report – It plays an important role in the business as it offers

credit to the customers. Based on these reports, the company analyses the customers and their

credit worthiness. It provides credit balances that company owes from the customers

segregated in categories of items that are 30, 60 and 90 days. These reports help the company

in tightening their credit policy accordingly. Such kind of report is helpful in case where

company conducts its business operations with the help of acquisition of raw material, labour

on credit basis. It is best suited for ABC limited it has to rely on large credit amount for

carrying on business activities. With the help of this report, the manager of ABC limited can

monitor and determine all the potential defaulters in context of non-payment of money. It

also helps in assessing the problem or issues which the company is facing in its money

collection process.

related to the business and to enable the manger of the company to know the true picture of the

company. To get an overall picture on business performance and finance, the management

reports need to be out on every quarterly or yearly basis. These reports helps in providing

transparency to the stakeholders of the company as well as provide accurate data for further

analysis. The various types of reports that are used by management are -

Budget reports – These reports are important in analyzing, evaluating and monitoring

performance of the company and can be generated for whole business or particular department.

A company's basic work is to create budget which helps the company in estimating cost of the

business. The preparation of the budget can be done on the basis of previous experience (Mahal,

2015). A budget of the company consists of income and expenditure sources of the company and

achieve its goals while staying in the budget. It helps the company in cost cutting and provide

employees with incentives. The budget report lays emphasis on making future projections and

estimation related to the amount of money to be spent on business operations. By making

budgetary plans and strategies ABC limited can conduct business operations smoothly with the

limited amount of budgeted amount and resources. With the help of budget report, a company

can make assessment of its performance as well as profitability level. Budget are prepared on the

basis of previous experience business has met with. With proper estimates and budget, company

can deal with future contingencies and cost expenses.

Account receivable aging report – It plays an important role in the business as it offers

credit to the customers. Based on these reports, the company analyses the customers and their

credit worthiness. It provides credit balances that company owes from the customers

segregated in categories of items that are 30, 60 and 90 days. These reports help the company

in tightening their credit policy accordingly. Such kind of report is helpful in case where

company conducts its business operations with the help of acquisition of raw material, labour

on credit basis. It is best suited for ABC limited it has to rely on large credit amount for

carrying on business activities. With the help of this report, the manager of ABC limited can

monitor and determine all the potential defaulters in context of non-payment of money. It

also helps in assessing the problem or issues which the company is facing in its money

collection process.

Cost Managerial Accounting Report – This accounting report helps ABC limited in

assessing and determining the amount of cost incurred for undertaking the manufacturing and

production function of any product or services. This assessment takes into consideration all the

cost related to raw material, overhead, labor and others factors. This helps managers in realizing

the cost and selling prices of their products and services which further helps in estimating the

profit or revenue amount for the company in the near future.

.

Performance report – These reports are prepared to review the performance of

employees as well a company at the end of the year. It helps mangers to make important

decisions regarding the organization. These reports helps in making organizational strategy

according t the performance of the employees of the company and also act as a base for decision

making. . It assists in evaluating the performance level of each employee of the company and

team as a whole involved in particular business activity or task. By using these performance

reports, the ABC limited can make important strategic decisions and plans for the betterment of

company, future growth and success of business organization. Performance related report

provides a deep insight about the working process, procedures used by the company in carrying

on business activities (Weygandt, and et.al, 2017). By framing and implementing strategies and

plans, company can achieve its business goals and continuous tracking of these strategies timely

can improve business standards as well.

Benefits of management accounting system

Evaluation of management accounting system are:

Inventory management system

Pro Con

It helps in cost cutting by saving a lot of

money and increases speed of the operation.

It increases performance delivery of outputs

and lead to efficient operations in the

company.

It increases burden of day to day updating.

The installation cost of the system is high.

It helps in controlling many risk but get open

to other risks.

assessing and determining the amount of cost incurred for undertaking the manufacturing and

production function of any product or services. This assessment takes into consideration all the

cost related to raw material, overhead, labor and others factors. This helps managers in realizing

the cost and selling prices of their products and services which further helps in estimating the

profit or revenue amount for the company in the near future.

.

Performance report – These reports are prepared to review the performance of

employees as well a company at the end of the year. It helps mangers to make important

decisions regarding the organization. These reports helps in making organizational strategy

according t the performance of the employees of the company and also act as a base for decision

making. . It assists in evaluating the performance level of each employee of the company and

team as a whole involved in particular business activity or task. By using these performance

reports, the ABC limited can make important strategic decisions and plans for the betterment of

company, future growth and success of business organization. Performance related report

provides a deep insight about the working process, procedures used by the company in carrying

on business activities (Weygandt, and et.al, 2017). By framing and implementing strategies and

plans, company can achieve its business goals and continuous tracking of these strategies timely

can improve business standards as well.

Benefits of management accounting system

Evaluation of management accounting system are:

Inventory management system

Pro Con

It helps in cost cutting by saving a lot of

money and increases speed of the operation.

It increases performance delivery of outputs

and lead to efficient operations in the

company.

It increases burden of day to day updating.

The installation cost of the system is high.

It helps in controlling many risk but get open

to other risks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It helps in asset tracking and saves time and

energy. It increased the efficiency of the

organization.

Cost accounting system

Pro Con

It allows the company to have separation in

cost.

It helps company in estimating the cost of the

product (Garrison and et.al., 2011).

It is easily adaptable in the organization and

provides ease of monitoring and control labor

costs.

This system record past performances which

does not help the company in taking future

decisions.

Installation of this system requires

maintenance of costing record which needs

heavy expenditure.

Job costing system

Pro Con

It helps the company in figuring out trend

analysis through compilation of historical costs

(Advantages and disadvantages of Job costing

system, 2019).

It helps in finding out cost of each job which

helps in finding out that which department is

performing better.

This system does not provide any

standardization.

When inflation hits, the comparison of jobs

became meaningless.

It is expensive method and there is no

standardization of job in job costing.

Integration of management accounting and reporting system

The integration of management accounting system and reporting system in the company

works together which helps the company in reducing its cost and create efficient operations. The

cost accounting system of the company helps in providing cost reports to the company which

energy. It increased the efficiency of the

organization.

Cost accounting system

Pro Con

It allows the company to have separation in

cost.

It helps company in estimating the cost of the

product (Garrison and et.al., 2011).

It is easily adaptable in the organization and

provides ease of monitoring and control labor

costs.

This system record past performances which

does not help the company in taking future

decisions.

Installation of this system requires

maintenance of costing record which needs

heavy expenditure.

Job costing system

Pro Con

It helps the company in figuring out trend

analysis through compilation of historical costs

(Advantages and disadvantages of Job costing

system, 2019).

It helps in finding out cost of each job which

helps in finding out that which department is

performing better.

This system does not provide any

standardization.

When inflation hits, the comparison of jobs

became meaningless.

It is expensive method and there is no

standardization of job in job costing.

Integration of management accounting and reporting system

The integration of management accounting system and reporting system in the company

works together which helps the company in reducing its cost and create efficient operations. The

cost accounting system of the company helps in providing cost reports to the company which

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

helps the company in deciding the price of its product by keeping in mind the competitors of the

company (Toussaint and et.al., 2015). The job costing system enable the company in giving

efficient job costing reports which give clear information to the company that which project is

profitable and which project is not. The other way in which both job costing system and report

are integrated is that they the job costing system includes direct material and cost of direct labor

that is used to make efficient job reports of the company. The inventory management helps in

making inventory reports on raw materials, in process goods and final goods which helps the

company in tracking inventory records of the company.

TASK 2

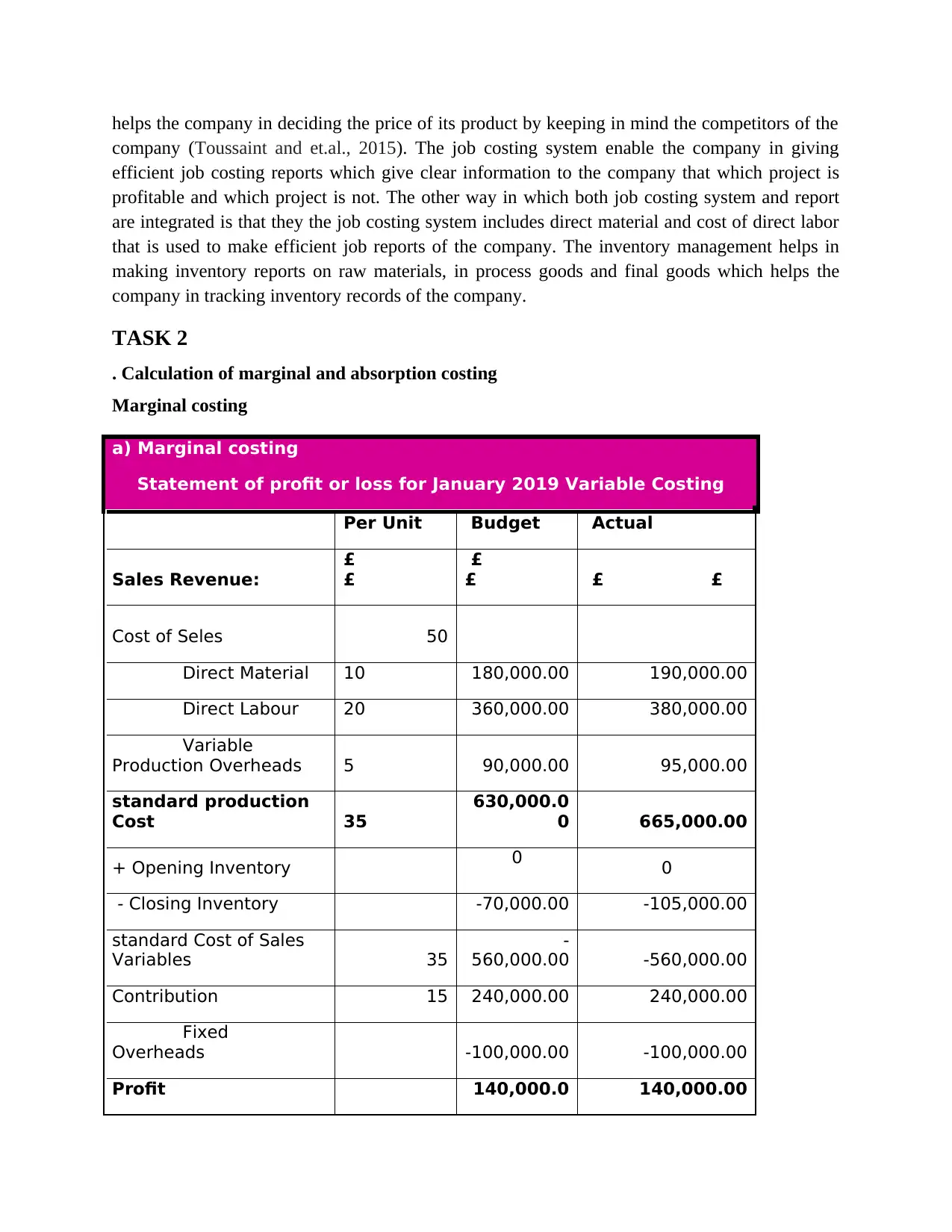

. Calculation of marginal and absorption costing

Marginal costing

a) Marginal costing

Statement of profit or loss for January 2019 Variable Costing

Per Unit Budget Actual

Sales Revenue:

£

£

£

£ £ £

Cost of Seles 50

Direct Material 10 180,000.00 190,000.00

Direct Labour 20 360,000.00 380,000.00

Variable

Production Overheads 5 90,000.00 95,000.00

standard production

Cost 35

630,000.0

0 665,000.00

+ Opening Inventory 0 0

- Closing Inventory -70,000.00 -105,000.00

standard Cost of Sales

Variables 35

-

560,000.00 -560,000.00

Contribution 15 240,000.00 240,000.00

Fixed

Overheads -100,000.00 -100,000.00

Profit 140,000.0 140,000.00

company (Toussaint and et.al., 2015). The job costing system enable the company in giving

efficient job costing reports which give clear information to the company that which project is

profitable and which project is not. The other way in which both job costing system and report

are integrated is that they the job costing system includes direct material and cost of direct labor

that is used to make efficient job reports of the company. The inventory management helps in

making inventory reports on raw materials, in process goods and final goods which helps the

company in tracking inventory records of the company.

TASK 2

. Calculation of marginal and absorption costing

Marginal costing

a) Marginal costing

Statement of profit or loss for January 2019 Variable Costing

Per Unit Budget Actual

Sales Revenue:

£

£

£

£ £ £

Cost of Seles 50

Direct Material 10 180,000.00 190,000.00

Direct Labour 20 360,000.00 380,000.00

Variable

Production Overheads 5 90,000.00 95,000.00

standard production

Cost 35

630,000.0

0 665,000.00

+ Opening Inventory 0 0

- Closing Inventory -70,000.00 -105,000.00

standard Cost of Sales

Variables 35

-

560,000.00 -560,000.00

Contribution 15 240,000.00 240,000.00

Fixed

Overheads -100,000.00 -100,000.00

Profit 140,000.0 140,000.00

0

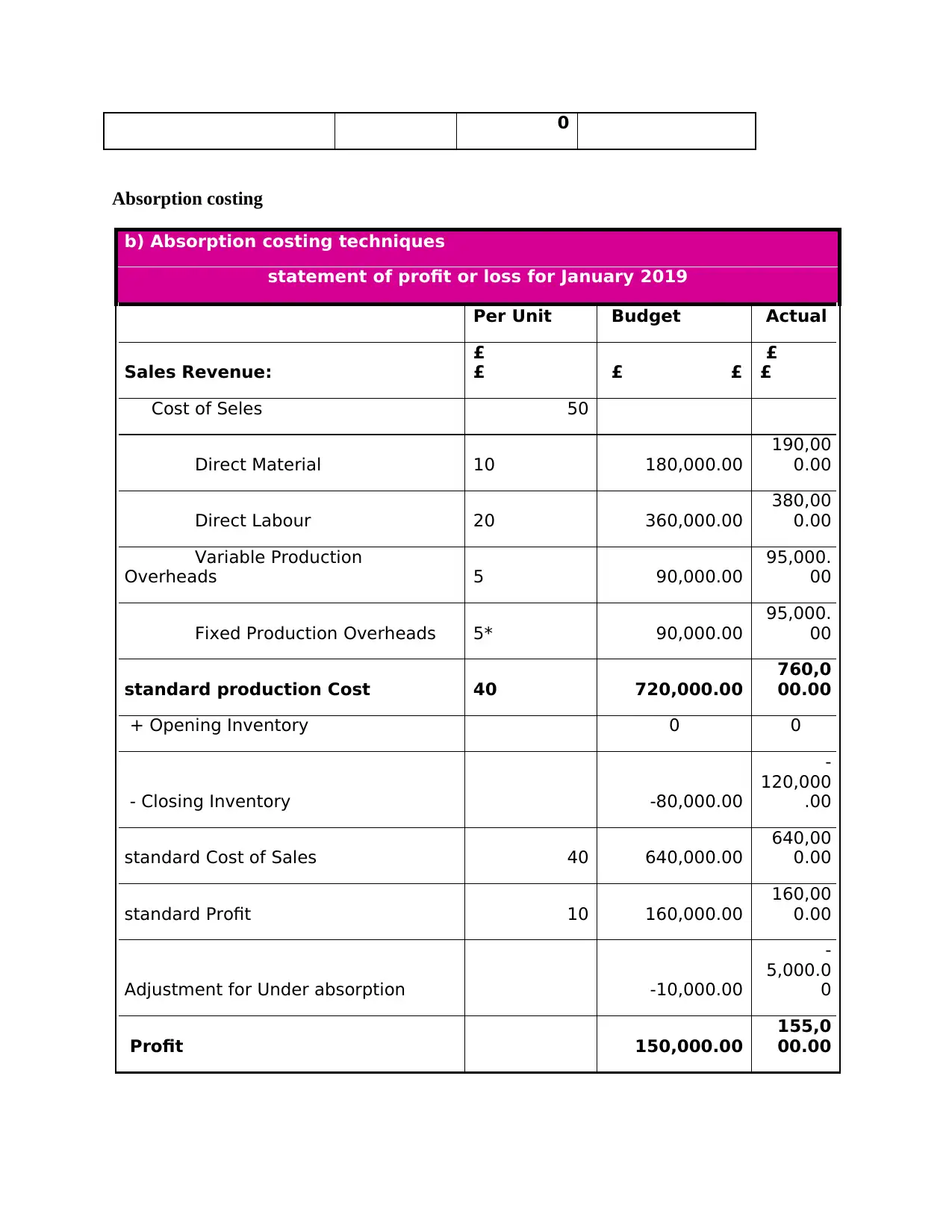

Absorption costing

b) Absorption costing techniques

statement of profit or loss for January 2019

Per Unit Budget Actual

Sales Revenue:

£

£ £ £

£

£

Cost of Seles 50

Direct Material 10 180,000.00

190,00

0.00

Direct Labour 20 360,000.00

380,00

0.00

Variable Production

Overheads 5 90,000.00

95,000.

00

Fixed Production Overheads 5* 90,000.00

95,000.

00

standard production Cost 40 720,000.00

760,0

00.00

+ Opening Inventory 0 0

- Closing Inventory -80,000.00

-

120,000

.00

standard Cost of Sales 40 640,000.00

640,00

0.00

standard Profit 10 160,000.00

160,00

0.00

Adjustment for Under absorption -10,000.00

-

5,000.0

0

Profit 150,000.00

155,0

00.00

Absorption costing

b) Absorption costing techniques

statement of profit or loss for January 2019

Per Unit Budget Actual

Sales Revenue:

£

£ £ £

£

£

Cost of Seles 50

Direct Material 10 180,000.00

190,00

0.00

Direct Labour 20 360,000.00

380,00

0.00

Variable Production

Overheads 5 90,000.00

95,000.

00

Fixed Production Overheads 5* 90,000.00

95,000.

00

standard production Cost 40 720,000.00

760,0

00.00

+ Opening Inventory 0 0

- Closing Inventory -80,000.00

-

120,000

.00

standard Cost of Sales 40 640,000.00

640,00

0.00

standard Profit 10 160,000.00

160,00

0.00

Adjustment for Under absorption -10,000.00

-

5,000.0

0

Profit 150,000.00

155,0

00.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

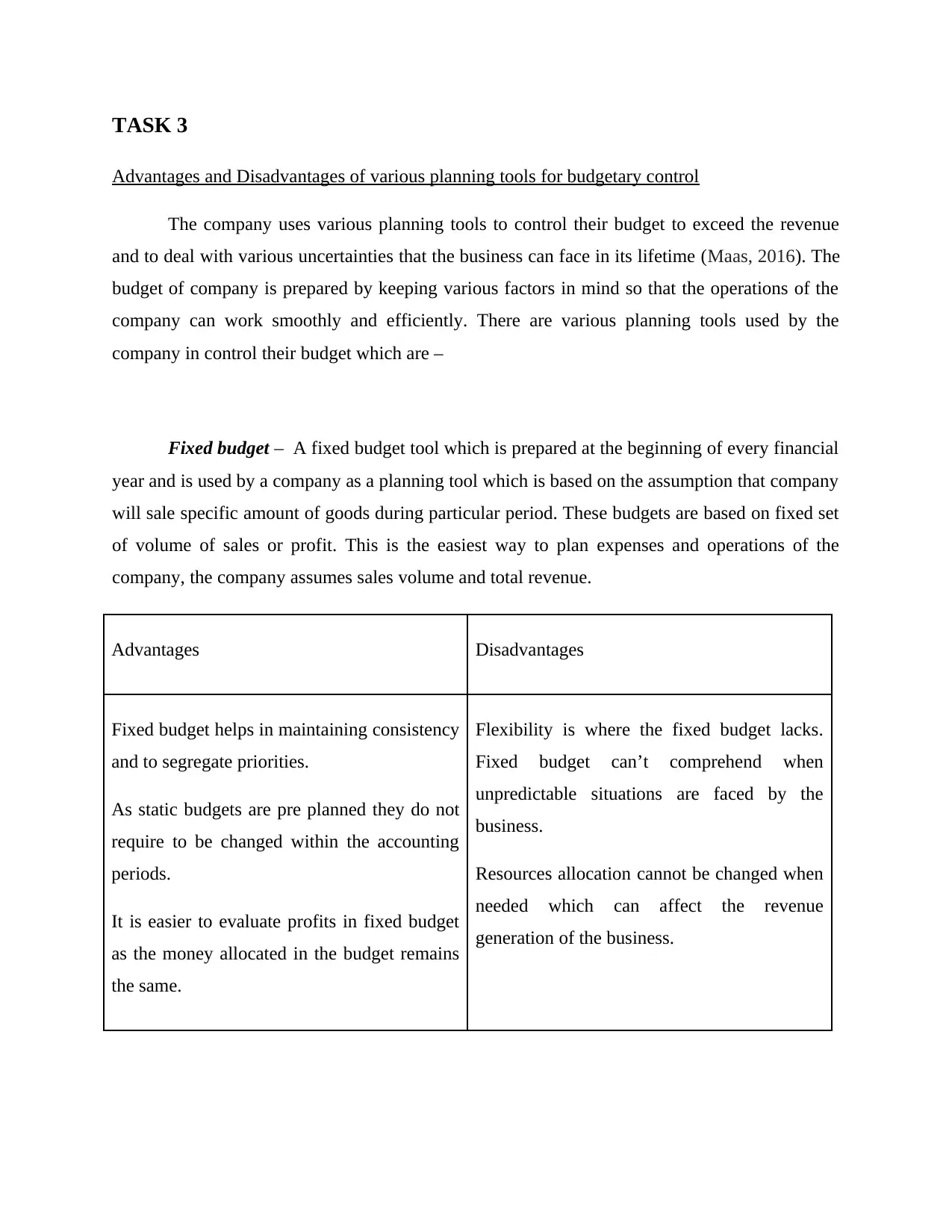

Advantages and Disadvantages of various planning tools for budgetary control

The company uses various planning tools to control their budget to exceed the revenue

and to deal with various uncertainties that the business can face in its lifetime (Maas, 2016). The

budget of company is prepared by keeping various factors in mind so that the operations of the

company can work smoothly and efficiently. There are various planning tools used by the

company in control their budget which are –

Fixed budget – A fixed budget tool which is prepared at the beginning of every financial

year and is used by a company as a planning tool which is based on the assumption that company

will sale specific amount of goods during particular period. These budgets are based on fixed set

of volume of sales or profit. This is the easiest way to plan expenses and operations of the

company, the company assumes sales volume and total revenue.

Advantages Disadvantages

Fixed budget helps in maintaining consistency

and to segregate priorities.

As static budgets are pre planned they do not

require to be changed within the accounting

periods.

It is easier to evaluate profits in fixed budget

as the money allocated in the budget remains

the same.

Flexibility is where the fixed budget lacks.

Fixed budget can’t comprehend when

unpredictable situations are faced by the

business.

Resources allocation cannot be changed when

needed which can affect the revenue

generation of the business.

Advantages and Disadvantages of various planning tools for budgetary control

The company uses various planning tools to control their budget to exceed the revenue

and to deal with various uncertainties that the business can face in its lifetime (Maas, 2016). The

budget of company is prepared by keeping various factors in mind so that the operations of the

company can work smoothly and efficiently. There are various planning tools used by the

company in control their budget which are –

Fixed budget – A fixed budget tool which is prepared at the beginning of every financial

year and is used by a company as a planning tool which is based on the assumption that company

will sale specific amount of goods during particular period. These budgets are based on fixed set

of volume of sales or profit. This is the easiest way to plan expenses and operations of the

company, the company assumes sales volume and total revenue.

Advantages Disadvantages

Fixed budget helps in maintaining consistency

and to segregate priorities.

As static budgets are pre planned they do not

require to be changed within the accounting

periods.

It is easier to evaluate profits in fixed budget

as the money allocated in the budget remains

the same.

Flexibility is where the fixed budget lacks.

Fixed budget can’t comprehend when

unpredictable situations are faced by the

business.

Resources allocation cannot be changed when

needed which can affect the revenue

generation of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

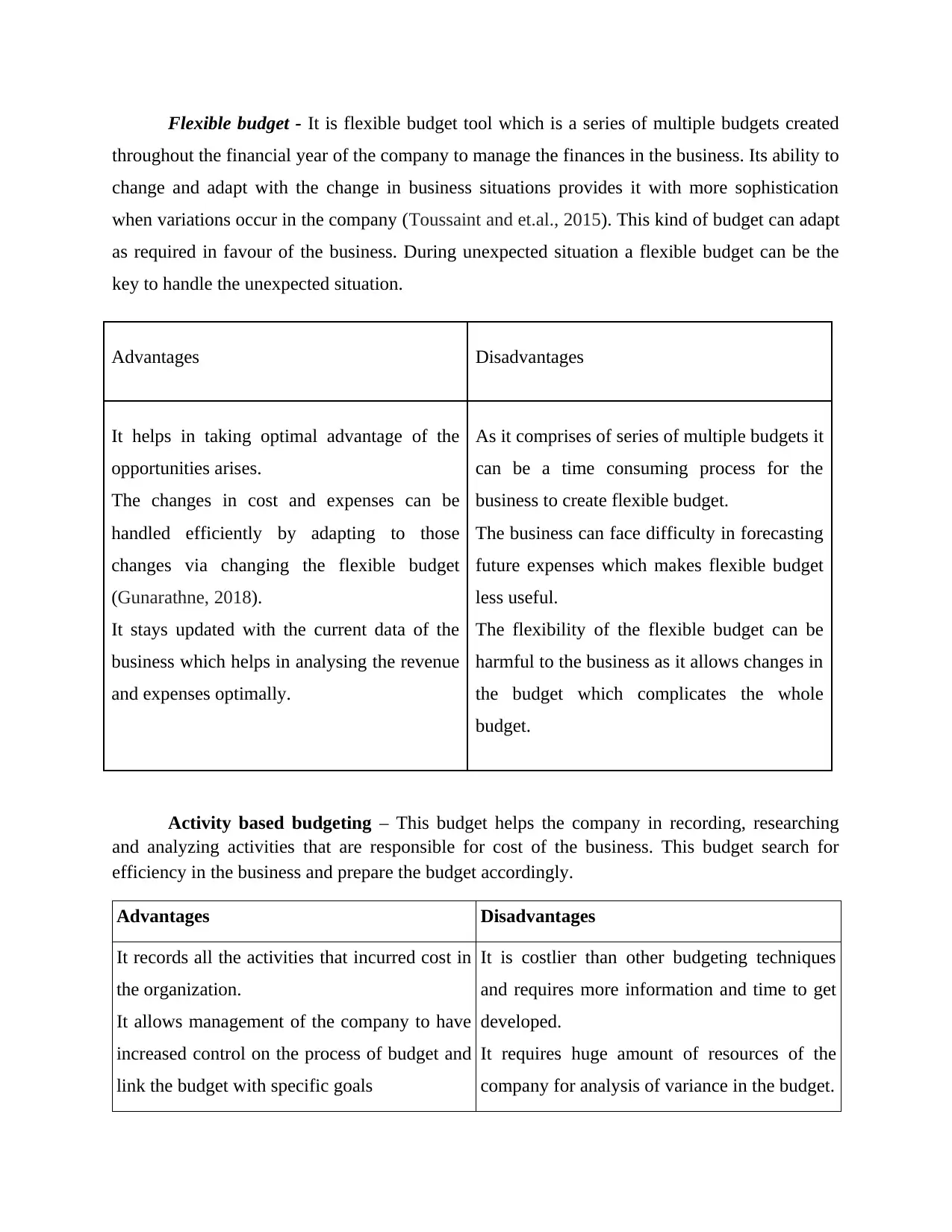

Flexible budget - It is flexible budget tool which is a series of multiple budgets created

throughout the financial year of the company to manage the finances in the business. Its ability to

change and adapt with the change in business situations provides it with more sophistication

when variations occur in the company (Toussaint and et.al., 2015). This kind of budget can adapt

as required in favour of the business. During unexpected situation a flexible budget can be the

key to handle the unexpected situation.

Advantages Disadvantages

It helps in taking optimal advantage of the

opportunities arises.

The changes in cost and expenses can be

handled efficiently by adapting to those

changes via changing the flexible budget

(Gunarathne, 2018).

It stays updated with the current data of the

business which helps in analysing the revenue

and expenses optimally.

As it comprises of series of multiple budgets it

can be a time consuming process for the

business to create flexible budget.

The business can face difficulty in forecasting

future expenses which makes flexible budget

less useful.

The flexibility of the flexible budget can be

harmful to the business as it allows changes in

the budget which complicates the whole

budget.

Activity based budgeting – This budget helps the company in recording, researching

and analyzing activities that are responsible for cost of the business. This budget search for

efficiency in the business and prepare the budget accordingly.

Advantages Disadvantages

It records all the activities that incurred cost in

the organization.

It allows management of the company to have

increased control on the process of budget and

link the budget with specific goals

It is costlier than other budgeting techniques

and requires more information and time to get

developed.

It requires huge amount of resources of the

company for analysis of variance in the budget.

throughout the financial year of the company to manage the finances in the business. Its ability to

change and adapt with the change in business situations provides it with more sophistication

when variations occur in the company (Toussaint and et.al., 2015). This kind of budget can adapt

as required in favour of the business. During unexpected situation a flexible budget can be the

key to handle the unexpected situation.

Advantages Disadvantages

It helps in taking optimal advantage of the

opportunities arises.

The changes in cost and expenses can be

handled efficiently by adapting to those

changes via changing the flexible budget

(Gunarathne, 2018).

It stays updated with the current data of the

business which helps in analysing the revenue

and expenses optimally.

As it comprises of series of multiple budgets it

can be a time consuming process for the

business to create flexible budget.

The business can face difficulty in forecasting

future expenses which makes flexible budget

less useful.

The flexibility of the flexible budget can be

harmful to the business as it allows changes in

the budget which complicates the whole

budget.

Activity based budgeting – This budget helps the company in recording, researching

and analyzing activities that are responsible for cost of the business. This budget search for

efficiency in the business and prepare the budget accordingly.

Advantages Disadvantages

It records all the activities that incurred cost in

the organization.

It allows management of the company to have

increased control on the process of budget and

link the budget with specific goals

It is costlier than other budgeting techniques

and requires more information and time to get

developed.

It requires huge amount of resources of the

company for analysis of variance in the budget.

TASK 4

Adaption of management accounting system to solve financial problems

Benchmarking - Benchmarking is the method which compares actual performance with

the standard performance which is set by the company as a benchmark that is need to be

achieved by the company. It helps the company in setting up of budget goals and financial

performance goals (Bromwich, 2016). Benchmarking helps in find out how departments of the

company perform individually and in the industry as whole. The company go through many

financial issues therefore benchmarking helps ABC limited in not only serves as a performance

metric but also provide a way in improving and take corrective measures to solve big issues. It

helps in setting margins of gross, operating and net profit.

Balanced scorecard - Balanced scorecard is used by the company to achieve its goals by

solving financial problems of the company. With the help of balanced scorecard, company can

solve the entire traditional accounting system problem. It shows overall information about the

company while considering objectives of the company (Bobryshev, and et.al., 2015). The

balanced scorecard links performances and compares it by taking 4 perspectives into action. It

links performance as how customer see the company which is Customer perspective, how

company can better at its operations which conclude internal perspective, how more can

company improve which deals with innovation and learning aspect and at last how shareholders

are being treated in the company analyse by financial perspective. Balance card minimizes the

load of passing information by limiting the number of measures used. It also helps manager to

see which area of the company needs improvement which can be achieved by limiting the

expense of other area.

Variance analysis - This is used by the company as statistical investigation between

actual and planned behaviour of the company. It solves various financial problems of the

company like it helps in controlling the cost of the company. It helps in differentiating the gap

between projected results and desired results (Klychova, and et.al., 2015). It highlights

deviations which are affecting financial performance of the company and finds out cause of

Adaption of management accounting system to solve financial problems

Benchmarking - Benchmarking is the method which compares actual performance with

the standard performance which is set by the company as a benchmark that is need to be

achieved by the company. It helps the company in setting up of budget goals and financial

performance goals (Bromwich, 2016). Benchmarking helps in find out how departments of the

company perform individually and in the industry as whole. The company go through many

financial issues therefore benchmarking helps ABC limited in not only serves as a performance

metric but also provide a way in improving and take corrective measures to solve big issues. It

helps in setting margins of gross, operating and net profit.

Balanced scorecard - Balanced scorecard is used by the company to achieve its goals by

solving financial problems of the company. With the help of balanced scorecard, company can

solve the entire traditional accounting system problem. It shows overall information about the

company while considering objectives of the company (Bobryshev, and et.al., 2015). The

balanced scorecard links performances and compares it by taking 4 perspectives into action. It

links performance as how customer see the company which is Customer perspective, how

company can better at its operations which conclude internal perspective, how more can

company improve which deals with innovation and learning aspect and at last how shareholders

are being treated in the company analyse by financial perspective. Balance card minimizes the

load of passing information by limiting the number of measures used. It also helps manager to

see which area of the company needs improvement which can be achieved by limiting the

expense of other area.

Variance analysis - This is used by the company as statistical investigation between

actual and planned behaviour of the company. It solves various financial problems of the

company like it helps in controlling the cost of the company. It helps in differentiating the gap

between projected results and desired results (Klychova, and et.al., 2015). It highlights

deviations which are affecting financial performance of the company and finds out cause of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.