Management Accounting Report: Costing, Reporting & Planning Tools

VerifiedAdded on 2023/01/18

|20

|4858

|30

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and practices, focusing on Stitchland Ltd as a case study. It elucidates the role of management accounting in organizational decision-making, performance analysis, and operational management. The report explicates various management accounting systems, including job costing, cost accounting, price optimization, and inventory management, detailing their benefits and applications. It also explores different methods of management accounting reporting, such as inventory management reports, budget reports, performance reports, and accounts receivable aging reports. Furthermore, the report delves into cost calculation methods, utilizing absorption and marginal costing techniques for income statement preparation. Finally, it discusses the merits and demerits of various planning tools within budgetary control and compares different approaches organizations adopt in management accounting systems to address financial challenges. This assignment solution is available on Desklib, a platform offering a wide range of study resources for students.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1 Explicate management accounting and their types...........................................................1

P2 Explicate methods for management accounting reporting................................................4

LO2..................................................................................................................................................6

P3 Calculation of cost for preparation of income statement by utilisation of absorption as well

as marginal costs.....................................................................................................................6

LO3................................................................................................................................................10

P4 Explicate merits and demerits of various kinds of planning tools within budgetary control.

..............................................................................................................................................10

LO4................................................................................................................................................14

P5 Comparison of ways in which organisations opt for management accounting systems with

respect to financial problems................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1 Explicate management accounting and their types...........................................................1

P2 Explicate methods for management accounting reporting................................................4

LO2..................................................................................................................................................6

P3 Calculation of cost for preparation of income statement by utilisation of absorption as well

as marginal costs.....................................................................................................................6

LO3................................................................................................................................................10

P4 Explicate merits and demerits of various kinds of planning tools within budgetary control.

..............................................................................................................................................10

LO4................................................................................................................................................14

P5 Comparison of ways in which organisations opt for management accounting systems with

respect to financial problems................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is defined as process of identification , measurement, analysis,

interpretation as well as communication of information to managers for pursuit of goals of

organisation (Aldehayyat and Maan, 2013). This aids management to formulate decisions as

well as inform them about business operation metrics. It is liable for handling of margin analysis

for assessment of profits and also involves calculation of contribution margin for identification

of unit volume at which business gross sales becomes identical to total expenditure. To

understand concept of management accounting Stitchland Ltd is taken into consideration those

deals within manufacturing of clothes but there finances are being handled out by Bright Star.

This report will contain details about management accounting along with diverse kinds of

systems. Apart from this, diverse methods of management accounting reporting have been

explicated and cost analysis with respect to absorption & marginal costs have been calculated.

Furthermore, various types of planning tools have been discussed and comparison has been made

for adapting to management accounting systems for responding to financial problems.

LO1.

P1 Explicate management accounting and their types.

The application of techniques, professional knowledge along with concepts within

preparation of accounting information in such a way that it assists management to formulate

policies and plans for managing operations of organisations as well as development of decisions

is known as management accounting (Anandarajan, Anandarajan and Srinivasan, 2012). This

will assist Stitchland Ltd to analyse performance of firm by speculation of strategies, making

comparisons, forecasting, budgeting and various others. Basically, it denotes presentation of

information associated with accounting for development of policies by adopting management as

well as aids within everyday operations. Stitchland Ltd can utilise these systems for furnishing

their operations with respect to manufacturing.

The systems that involves within internal systems and are being utilised by firms for

measuring as well as evaluating their performance is known as management accounting

system. Stitchland Ltd by making use of this can reach out their all the deparments and make

sure that operations are being carried out in an affirmative manner (Christ and Burritt, 2013).

Objective of this types of systems is to furnish suitable information to managers by which they

1

Management accounting is defined as process of identification , measurement, analysis,

interpretation as well as communication of information to managers for pursuit of goals of

organisation (Aldehayyat and Maan, 2013). This aids management to formulate decisions as

well as inform them about business operation metrics. It is liable for handling of margin analysis

for assessment of profits and also involves calculation of contribution margin for identification

of unit volume at which business gross sales becomes identical to total expenditure. To

understand concept of management accounting Stitchland Ltd is taken into consideration those

deals within manufacturing of clothes but there finances are being handled out by Bright Star.

This report will contain details about management accounting along with diverse kinds of

systems. Apart from this, diverse methods of management accounting reporting have been

explicated and cost analysis with respect to absorption & marginal costs have been calculated.

Furthermore, various types of planning tools have been discussed and comparison has been made

for adapting to management accounting systems for responding to financial problems.

LO1.

P1 Explicate management accounting and their types.

The application of techniques, professional knowledge along with concepts within

preparation of accounting information in such a way that it assists management to formulate

policies and plans for managing operations of organisations as well as development of decisions

is known as management accounting (Anandarajan, Anandarajan and Srinivasan, 2012). This

will assist Stitchland Ltd to analyse performance of firm by speculation of strategies, making

comparisons, forecasting, budgeting and various others. Basically, it denotes presentation of

information associated with accounting for development of policies by adopting management as

well as aids within everyday operations. Stitchland Ltd can utilise these systems for furnishing

their operations with respect to manufacturing.

The systems that involves within internal systems and are being utilised by firms for

measuring as well as evaluating their performance is known as management accounting

system. Stitchland Ltd by making use of this can reach out their all the deparments and make

sure that operations are being carried out in an affirmative manner (Christ and Burritt, 2013).

Objective of this types of systems is to furnish suitable information to managers by which they

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

can formulate their decisions within efficacious way. Therefore, Stitchland Ltd must utilise

accounting systems as this tool includes both financial as well as non-financial information

which assists in management of business.

There is enhanced significance of combination of various accounting systems in a

firm. Stitchland Ltd can make use accounting systems as per their requirements. Like, they can

make use of cost accounting system for management of inventory in an efficacious way. In

addition to this by opting for price optimisation systems Stitchland Ltd will be able to render

framework for identification of prices (Cohen and Karatzimas, 2013). It denotes on the basis of

needs of organisation these systems can be used as each have their own importance as well as

usage.

Origin and principles of management accounting

According to the analysis, management accounting was given by England at the time of

industrial revolution. It includes execution of different activities by which financial problems can

be improvised. The major principles of management accounting involves influence and building

up of trust in context of orientation of organisation.

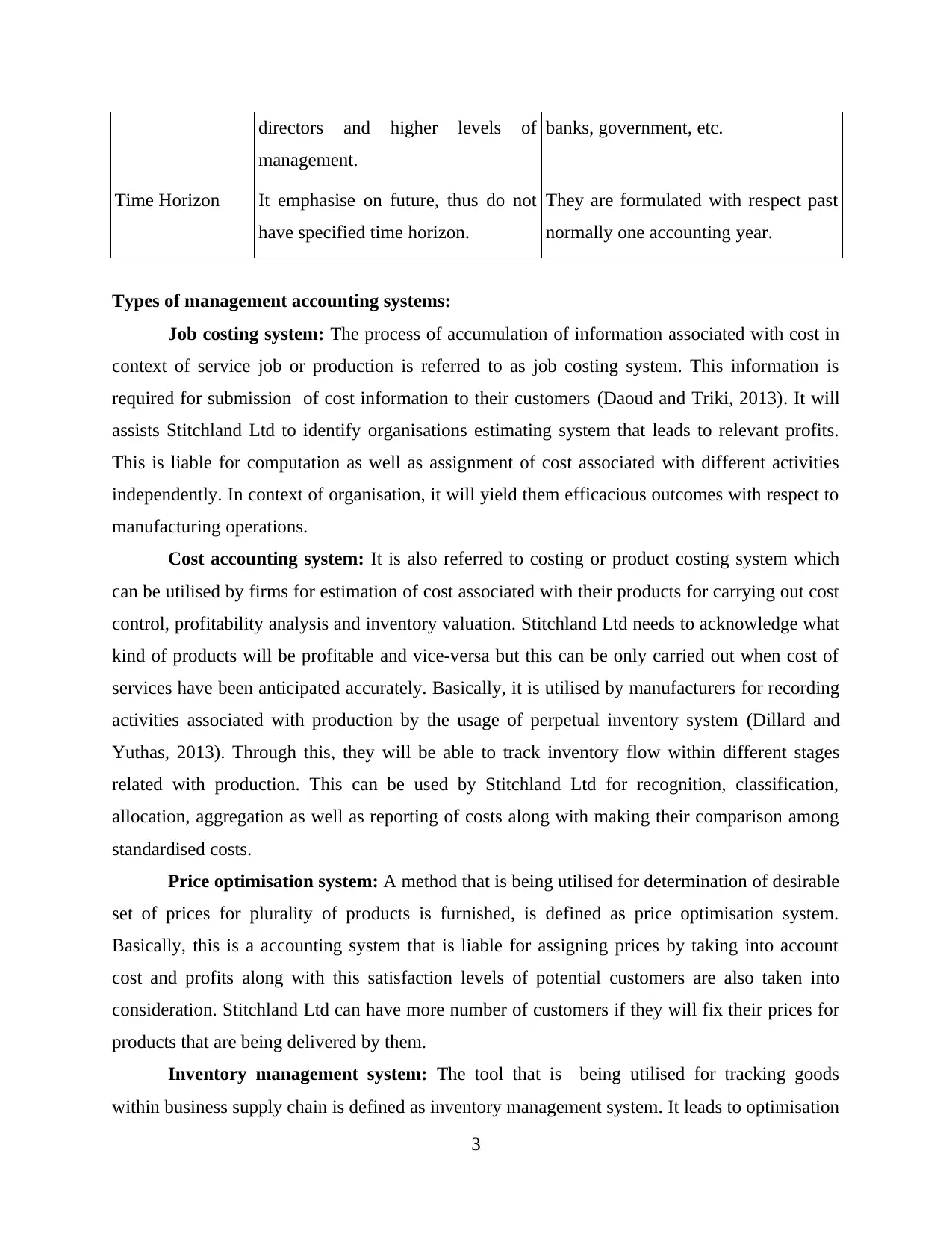

Divergence among Management & Financial Accounting:

Basis Management Accounting Financial Accounting

Aim They aims to assists management to

develop business decisions.

It aims at furnishing rendering

information to outer parties. They can

be customers, investors, creditors, etc.

as it will assist them within

formulation of decisions (Cooper,

2017) .

Governing

principles

There do not exists standard basis

for preparation of management

accounting statements, they are

formulated with respect to needs of

management team.

The statements are formulated on the

basis of GAAP (Generally Accepted

Accounting Principles). They

comprises of less or more features.

Reporting

beneficiaries

Reports that are build under this are

significant for CEO, promoters,

Financial accounting is developed for

external users, they can be suppliers,

2

accounting systems as this tool includes both financial as well as non-financial information

which assists in management of business.

There is enhanced significance of combination of various accounting systems in a

firm. Stitchland Ltd can make use accounting systems as per their requirements. Like, they can

make use of cost accounting system for management of inventory in an efficacious way. In

addition to this by opting for price optimisation systems Stitchland Ltd will be able to render

framework for identification of prices (Cohen and Karatzimas, 2013). It denotes on the basis of

needs of organisation these systems can be used as each have their own importance as well as

usage.

Origin and principles of management accounting

According to the analysis, management accounting was given by England at the time of

industrial revolution. It includes execution of different activities by which financial problems can

be improvised. The major principles of management accounting involves influence and building

up of trust in context of orientation of organisation.

Divergence among Management & Financial Accounting:

Basis Management Accounting Financial Accounting

Aim They aims to assists management to

develop business decisions.

It aims at furnishing rendering

information to outer parties. They can

be customers, investors, creditors, etc.

as it will assist them within

formulation of decisions (Cooper,

2017) .

Governing

principles

There do not exists standard basis

for preparation of management

accounting statements, they are

formulated with respect to needs of

management team.

The statements are formulated on the

basis of GAAP (Generally Accepted

Accounting Principles). They

comprises of less or more features.

Reporting

beneficiaries

Reports that are build under this are

significant for CEO, promoters,

Financial accounting is developed for

external users, they can be suppliers,

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

directors and higher levels of

management.

banks, government, etc.

Time Horizon It emphasise on future, thus do not

have specified time horizon.

They are formulated with respect past

normally one accounting year.

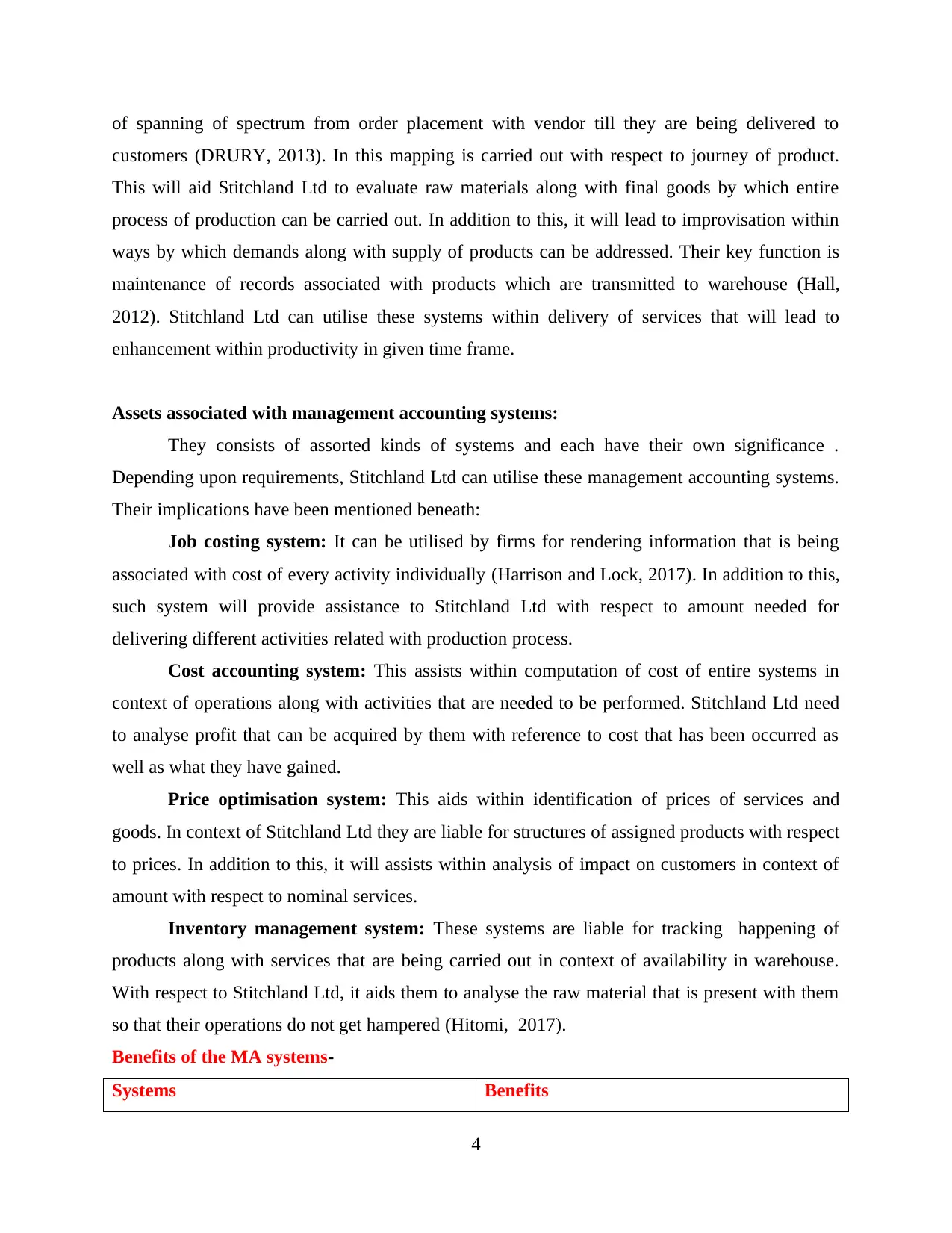

Types of management accounting systems:

Job costing system: The process of accumulation of information associated with cost in

context of service job or production is referred to as job costing system. This information is

required for submission of cost information to their customers (Daoud and Triki, 2013). It will

assists Stitchland Ltd to identify organisations estimating system that leads to relevant profits.

This is liable for computation as well as assignment of cost associated with different activities

independently. In context of organisation, it will yield them efficacious outcomes with respect to

manufacturing operations.

Cost accounting system: It is also referred to costing or product costing system which

can be utilised by firms for estimation of cost associated with their products for carrying out cost

control, profitability analysis and inventory valuation. Stitchland Ltd needs to acknowledge what

kind of products will be profitable and vice-versa but this can be only carried out when cost of

services have been anticipated accurately. Basically, it is utilised by manufacturers for recording

activities associated with production by the usage of perpetual inventory system (Dillard and

Yuthas, 2013). Through this, they will be able to track inventory flow within different stages

related with production. This can be used by Stitchland Ltd for recognition, classification,

allocation, aggregation as well as reporting of costs along with making their comparison among

standardised costs.

Price optimisation system: A method that is being utilised for determination of desirable

set of prices for plurality of products is furnished, is defined as price optimisation system.

Basically, this is a accounting system that is liable for assigning prices by taking into account

cost and profits along with this satisfaction levels of potential customers are also taken into

consideration. Stitchland Ltd can have more number of customers if they will fix their prices for

products that are being delivered by them.

Inventory management system: The tool that is being utilised for tracking goods

within business supply chain is defined as inventory management system. It leads to optimisation

3

management.

banks, government, etc.

Time Horizon It emphasise on future, thus do not

have specified time horizon.

They are formulated with respect past

normally one accounting year.

Types of management accounting systems:

Job costing system: The process of accumulation of information associated with cost in

context of service job or production is referred to as job costing system. This information is

required for submission of cost information to their customers (Daoud and Triki, 2013). It will

assists Stitchland Ltd to identify organisations estimating system that leads to relevant profits.

This is liable for computation as well as assignment of cost associated with different activities

independently. In context of organisation, it will yield them efficacious outcomes with respect to

manufacturing operations.

Cost accounting system: It is also referred to costing or product costing system which

can be utilised by firms for estimation of cost associated with their products for carrying out cost

control, profitability analysis and inventory valuation. Stitchland Ltd needs to acknowledge what

kind of products will be profitable and vice-versa but this can be only carried out when cost of

services have been anticipated accurately. Basically, it is utilised by manufacturers for recording

activities associated with production by the usage of perpetual inventory system (Dillard and

Yuthas, 2013). Through this, they will be able to track inventory flow within different stages

related with production. This can be used by Stitchland Ltd for recognition, classification,

allocation, aggregation as well as reporting of costs along with making their comparison among

standardised costs.

Price optimisation system: A method that is being utilised for determination of desirable

set of prices for plurality of products is furnished, is defined as price optimisation system.

Basically, this is a accounting system that is liable for assigning prices by taking into account

cost and profits along with this satisfaction levels of potential customers are also taken into

consideration. Stitchland Ltd can have more number of customers if they will fix their prices for

products that are being delivered by them.

Inventory management system: The tool that is being utilised for tracking goods

within business supply chain is defined as inventory management system. It leads to optimisation

3

of spanning of spectrum from order placement with vendor till they are being delivered to

customers (DRURY, 2013). In this mapping is carried out with respect to journey of product.

This will aid Stitchland Ltd to evaluate raw materials along with final goods by which entire

process of production can be carried out. In addition to this, it will lead to improvisation within

ways by which demands along with supply of products can be addressed. Their key function is

maintenance of records associated with products which are transmitted to warehouse (Hall,

2012). Stitchland Ltd can utilise these systems within delivery of services that will lead to

enhancement within productivity in given time frame.

Assets associated with management accounting systems:

They consists of assorted kinds of systems and each have their own significance .

Depending upon requirements, Stitchland Ltd can utilise these management accounting systems.

Their implications have been mentioned beneath:

Job costing system: It can be utilised by firms for rendering information that is being

associated with cost of every activity individually (Harrison and Lock, 2017). In addition to this,

such system will provide assistance to Stitchland Ltd with respect to amount needed for

delivering different activities related with production process.

Cost accounting system: This assists within computation of cost of entire systems in

context of operations along with activities that are needed to be performed. Stitchland Ltd need

to analyse profit that can be acquired by them with reference to cost that has been occurred as

well as what they have gained.

Price optimisation system: This aids within identification of prices of services and

goods. In context of Stitchland Ltd they are liable for structures of assigned products with respect

to prices. In addition to this, it will assists within analysis of impact on customers in context of

amount with respect to nominal services.

Inventory management system: These systems are liable for tracking happening of

products along with services that are being carried out in context of availability in warehouse.

With respect to Stitchland Ltd, it aids them to analyse the raw material that is present with them

so that their operations do not get hampered (Hitomi, 2017).

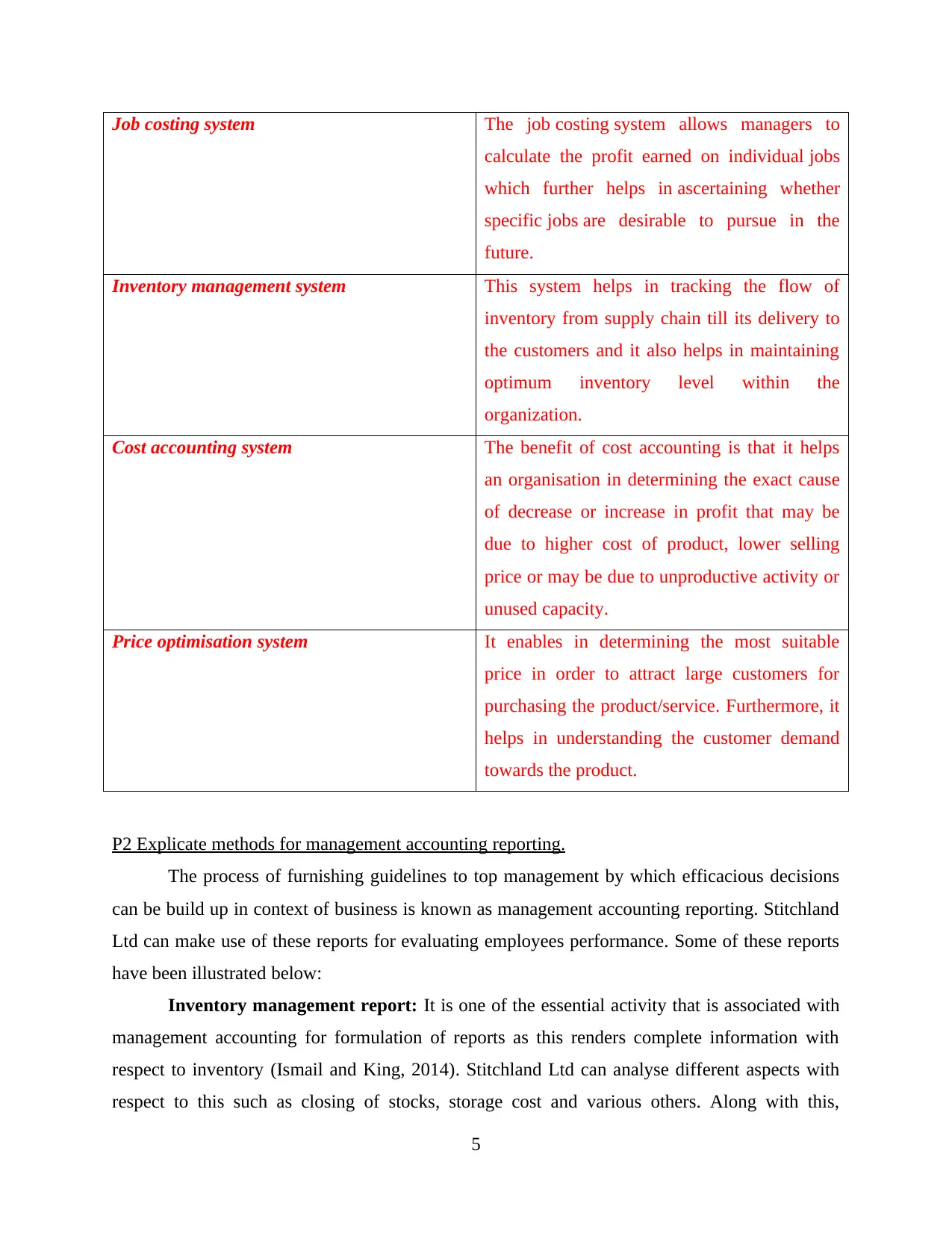

Benefits of the MA systems-

Systems Benefits

4

customers (DRURY, 2013). In this mapping is carried out with respect to journey of product.

This will aid Stitchland Ltd to evaluate raw materials along with final goods by which entire

process of production can be carried out. In addition to this, it will lead to improvisation within

ways by which demands along with supply of products can be addressed. Their key function is

maintenance of records associated with products which are transmitted to warehouse (Hall,

2012). Stitchland Ltd can utilise these systems within delivery of services that will lead to

enhancement within productivity in given time frame.

Assets associated with management accounting systems:

They consists of assorted kinds of systems and each have their own significance .

Depending upon requirements, Stitchland Ltd can utilise these management accounting systems.

Their implications have been mentioned beneath:

Job costing system: It can be utilised by firms for rendering information that is being

associated with cost of every activity individually (Harrison and Lock, 2017). In addition to this,

such system will provide assistance to Stitchland Ltd with respect to amount needed for

delivering different activities related with production process.

Cost accounting system: This assists within computation of cost of entire systems in

context of operations along with activities that are needed to be performed. Stitchland Ltd need

to analyse profit that can be acquired by them with reference to cost that has been occurred as

well as what they have gained.

Price optimisation system: This aids within identification of prices of services and

goods. In context of Stitchland Ltd they are liable for structures of assigned products with respect

to prices. In addition to this, it will assists within analysis of impact on customers in context of

amount with respect to nominal services.

Inventory management system: These systems are liable for tracking happening of

products along with services that are being carried out in context of availability in warehouse.

With respect to Stitchland Ltd, it aids them to analyse the raw material that is present with them

so that their operations do not get hampered (Hitomi, 2017).

Benefits of the MA systems-

Systems Benefits

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job costing system The job costing system allows managers to

calculate the profit earned on individual jobs

which further helps in ascertaining whether

specific jobs are desirable to pursue in the

future.

Inventory management system This system helps in tracking the flow of

inventory from supply chain till its delivery to

the customers and it also helps in maintaining

optimum inventory level within the

organization.

Cost accounting system The benefit of cost accounting is that it helps

an organisation in determining the exact cause

of decrease or increase in profit that may be

due to higher cost of product, lower selling

price or may be due to unproductive activity or

unused capacity.

Price optimisation system It enables in determining the most suitable

price in order to attract large customers for

purchasing the product/service. Furthermore, it

helps in understanding the customer demand

towards the product.

P2 Explicate methods for management accounting reporting.

The process of furnishing guidelines to top management by which efficacious decisions

can be build up in context of business is known as management accounting reporting. Stitchland

Ltd can make use of these reports for evaluating employees performance. Some of these reports

have been illustrated below:

Inventory management report: It is one of the essential activity that is associated with

management accounting for formulation of reports as this renders complete information with

respect to inventory (Ismail and King, 2014). Stitchland Ltd can analyse different aspects with

respect to this such as closing of stocks, storage cost and various others. Along with this,

5

calculate the profit earned on individual jobs

which further helps in ascertaining whether

specific jobs are desirable to pursue in the

future.

Inventory management system This system helps in tracking the flow of

inventory from supply chain till its delivery to

the customers and it also helps in maintaining

optimum inventory level within the

organization.

Cost accounting system The benefit of cost accounting is that it helps

an organisation in determining the exact cause

of decrease or increase in profit that may be

due to higher cost of product, lower selling

price or may be due to unproductive activity or

unused capacity.

Price optimisation system It enables in determining the most suitable

price in order to attract large customers for

purchasing the product/service. Furthermore, it

helps in understanding the customer demand

towards the product.

P2 Explicate methods for management accounting reporting.

The process of furnishing guidelines to top management by which efficacious decisions

can be build up in context of business is known as management accounting reporting. Stitchland

Ltd can make use of these reports for evaluating employees performance. Some of these reports

have been illustrated below:

Inventory management report: It is one of the essential activity that is associated with

management accounting for formulation of reports as this renders complete information with

respect to inventory (Ismail and King, 2014). Stitchland Ltd can analyse different aspects with

respect to this such as closing of stocks, storage cost and various others. Along with this,

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

inventory management reports furnish information associated with methods that are crucial for

stocks closing. Its objective is to have a balance among inventory investment as well as customer

services.

Budget Report: Management of Stitchland Ltd is liable for production of these reports

with respect to future so that there operations can be carried out in enhanced manner for

identification business operations so that accordingly they can furnish their activities. This gives

details related with incentives or bonus that is given to employees in case they are able to carry

out their operations in a standard format. This report assists organisation for making sure that

resources of organisations can be used in a suitable way so that overall operations of firm can be

enhanced.

Performance report: This is formulated for conducting performance measurement with

respect to employees are being managed by management accountant. They comprises of in depth

statements associated with incentives which are furnished to employees in terms of performance

appraisals (Lavia López and Hiebl, 2014). It will lead Stitchland Ltd to encourage their

employees so that enhanced results can be attained with respect to activities they have to carry

out. Along with this, it will aid them to furnish effective training to them in this context.

Accounts receivable ageing report: This provides crucial information with respect to

invoices that are being rendered to customers about credits. This will assist Stitchland Ltd to

identify customers who are not paid in terms of both amount and credit memos. This tool will

yield firm affirmative results with respect to effectiveness of credits, gathering of functions and

overdue for payments.

LO2.

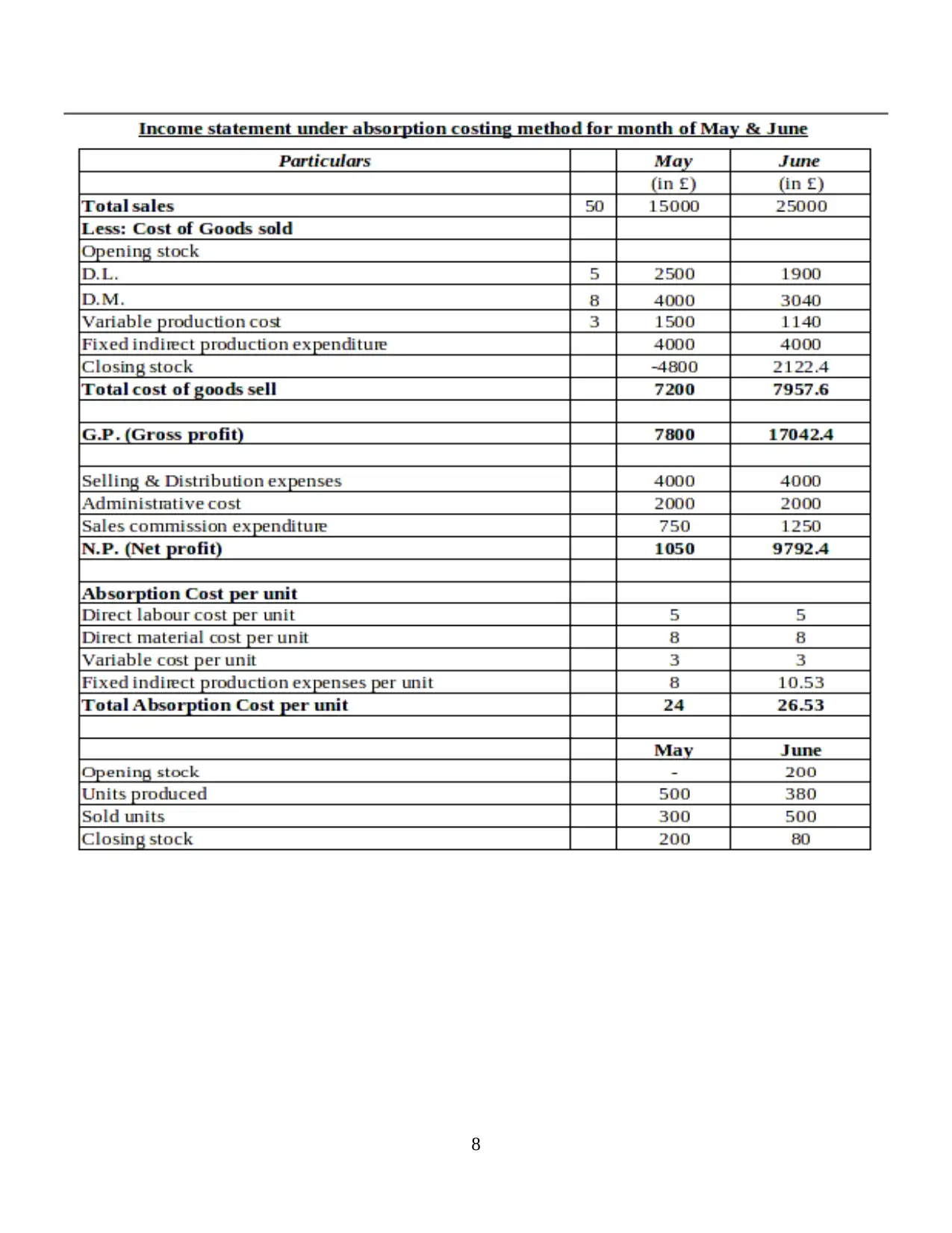

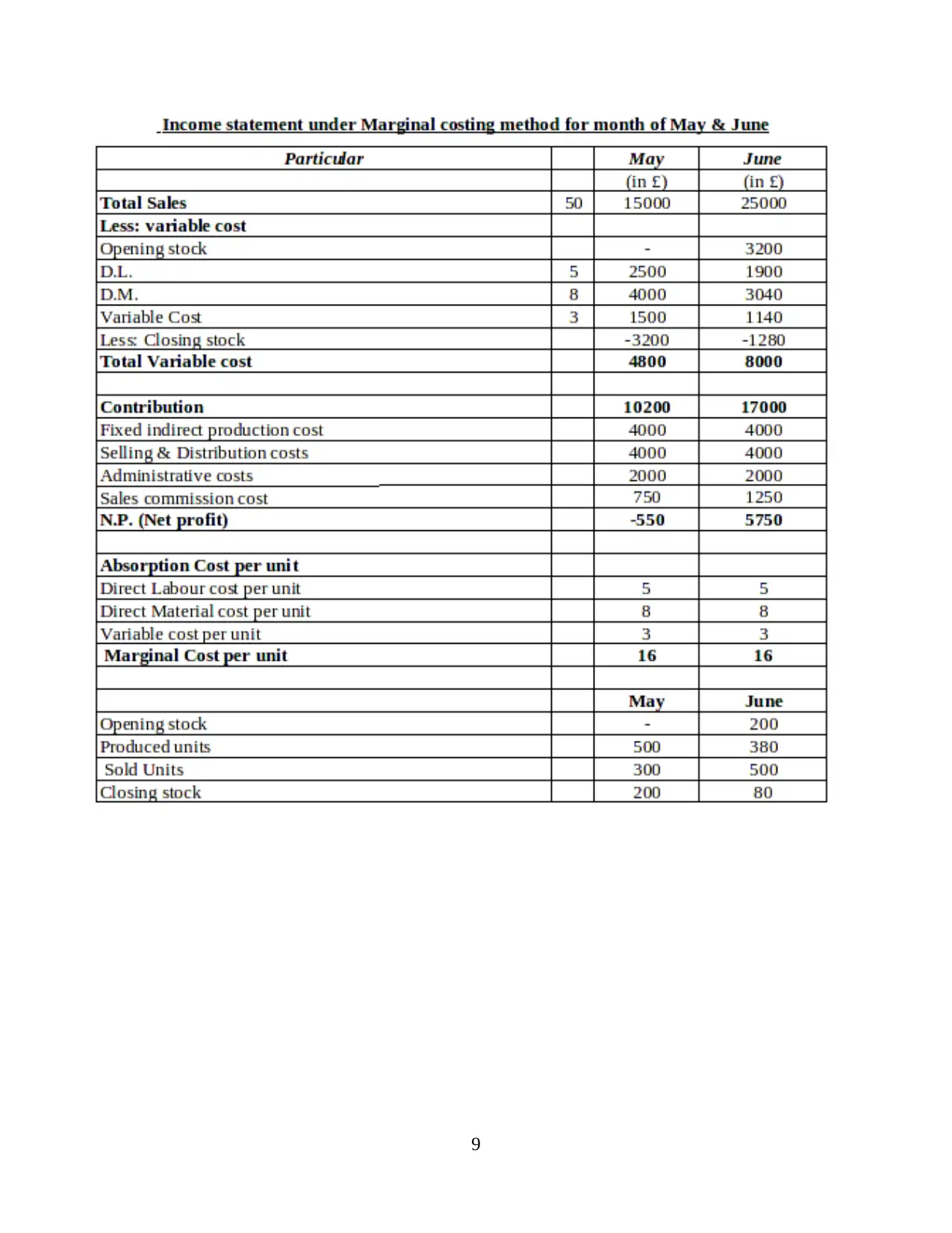

P3 Calculation of cost for preparation of income statement by utilisation of absorption as well as

marginal costs.

Absorption & marginal costing:

Absorption costing: This method comprises of expensing entire costs that are related

with manufacturing specified products as well as are needed for GAAP (Generally accepted

accounting principles) reporting externally (Soudani, 2012). This includes fixed and variable

costs of services as well as products that are being offered by firms like Stitchland Ltd.

6

stocks closing. Its objective is to have a balance among inventory investment as well as customer

services.

Budget Report: Management of Stitchland Ltd is liable for production of these reports

with respect to future so that there operations can be carried out in enhanced manner for

identification business operations so that accordingly they can furnish their activities. This gives

details related with incentives or bonus that is given to employees in case they are able to carry

out their operations in a standard format. This report assists organisation for making sure that

resources of organisations can be used in a suitable way so that overall operations of firm can be

enhanced.

Performance report: This is formulated for conducting performance measurement with

respect to employees are being managed by management accountant. They comprises of in depth

statements associated with incentives which are furnished to employees in terms of performance

appraisals (Lavia López and Hiebl, 2014). It will lead Stitchland Ltd to encourage their

employees so that enhanced results can be attained with respect to activities they have to carry

out. Along with this, it will aid them to furnish effective training to them in this context.

Accounts receivable ageing report: This provides crucial information with respect to

invoices that are being rendered to customers about credits. This will assist Stitchland Ltd to

identify customers who are not paid in terms of both amount and credit memos. This tool will

yield firm affirmative results with respect to effectiveness of credits, gathering of functions and

overdue for payments.

LO2.

P3 Calculation of cost for preparation of income statement by utilisation of absorption as well as

marginal costs.

Absorption & marginal costing:

Absorption costing: This method comprises of expensing entire costs that are related

with manufacturing specified products as well as are needed for GAAP (Generally accepted

accounting principles) reporting externally (Soudani, 2012). This includes fixed and variable

costs of services as well as products that are being offered by firms like Stitchland Ltd.

6

Marginal costing: The decrease or increase within entire cost of production for

formulating additional unit of product is refereed to marginal costing. It denotes that cost is

charged according to cost of units but fixed cost is not taken against contribution.

Difference between marginal and absorption costing:

•Marginal costing does not take fixed cost into consideration under product costing or inventory

valuation whereas absorption costing takes both fixed cost and variable cost into account.

•Marginal costing can be classified into both fixed and variable costs. Absorption costing can be

classified as production, distribution, and selling & administration.

7

formulating additional unit of product is refereed to marginal costing. It denotes that cost is

charged according to cost of units but fixed cost is not taken against contribution.

Difference between marginal and absorption costing:

•Marginal costing does not take fixed cost into consideration under product costing or inventory

valuation whereas absorption costing takes both fixed cost and variable cost into account.

•Marginal costing can be classified into both fixed and variable costs. Absorption costing can be

classified as production, distribution, and selling & administration.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

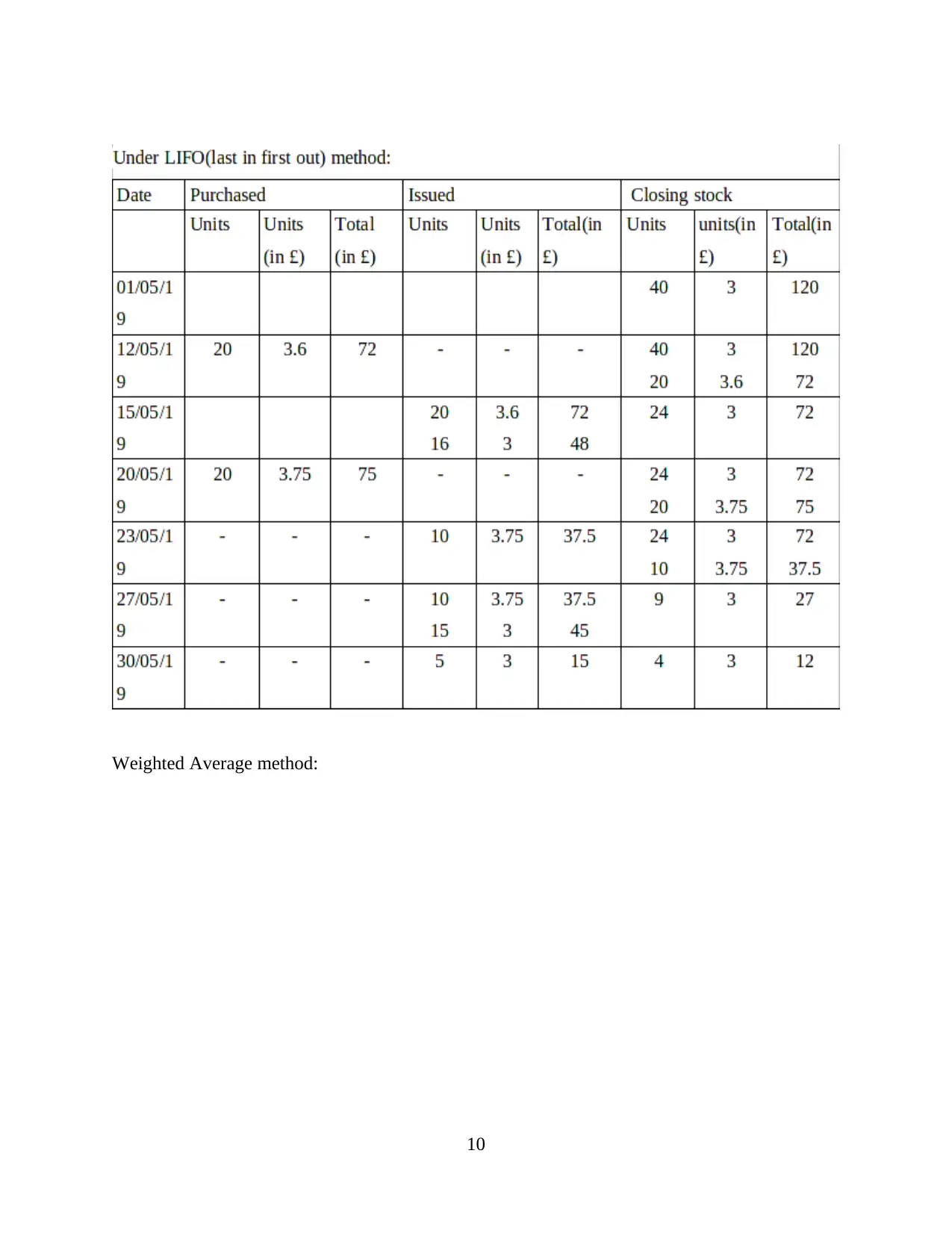

Weighted Average method:

10

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.